France Social Commerce Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 32.53 Billion |

| Market Size (2030) | USD 110.25 Billion |

| Growth Rate (2025 - 2030) | 27.65% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Social Commerce Market Analysis by Mordor Intelligence

The France social commerce market size stands at USD 32.53 billion in 2025 and is projected to climb to USD 110.25 billion by 2030, reflecting a compelling 27.65% CAGR . Widespread 5G coverage, transparent advertising rules under the EU Digital Services Act, and a mobile-first culture are driving the development of France's social commerce market. Luxury brands are utilizing augmented-reality (AR) try-ons to enhance conversion rates. At the same time, French banks are streamlining payment processes with one-click APIs, significantly reducing checkout times. Consistent regulations from CNIL strengthen trust among privacy-conscious consumers. Furthermore, creator-driven commerce on platforms such as TikTok and Twitch channels directs traffic that brands convert at higher rates compared to traditional e-commerce. These factors collectively establish France as a leading example of seamless and data-compliant digital retail within the EU.

Key Report Takeaways

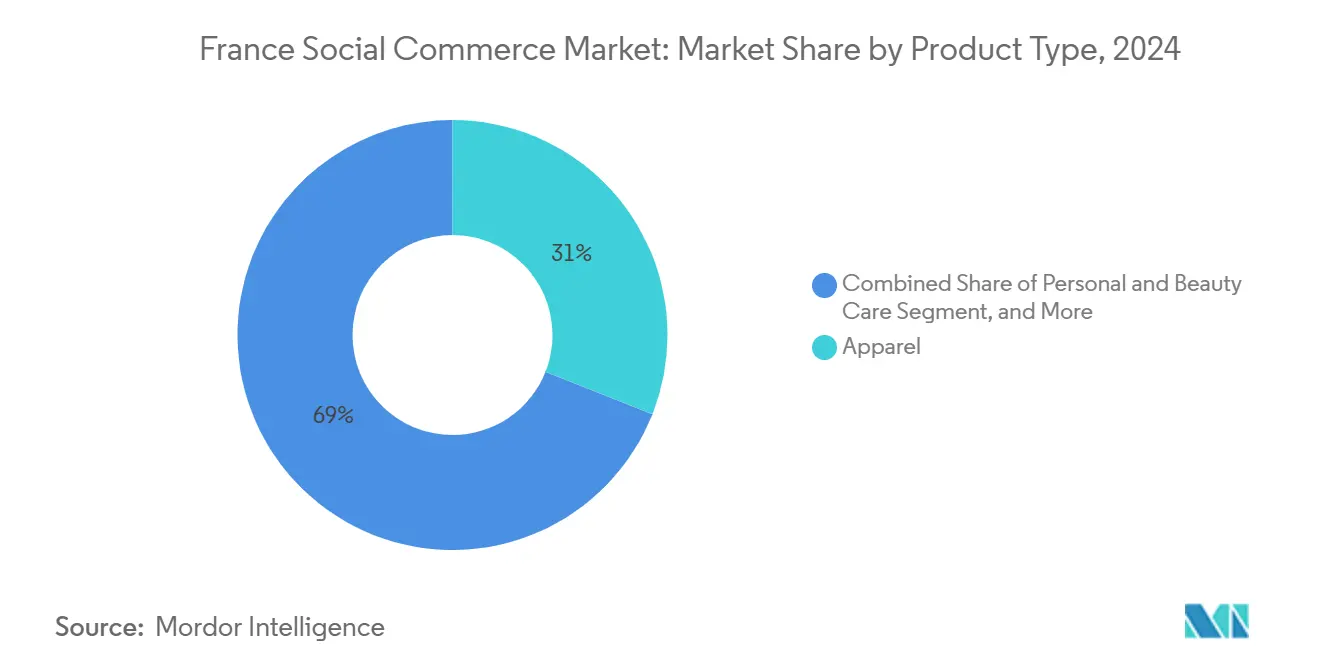

- By product type, Apparel commanded 31.27% of France social commerce market share in 2024, while Personal and Beauty Care is forecast to expand at a 29.01% CAGR to 2030.

- By device, Smartphones dominated with 90.77% share of the France social commerce market size in 2024, yet desktops still capture high-ticket fashion checkouts.

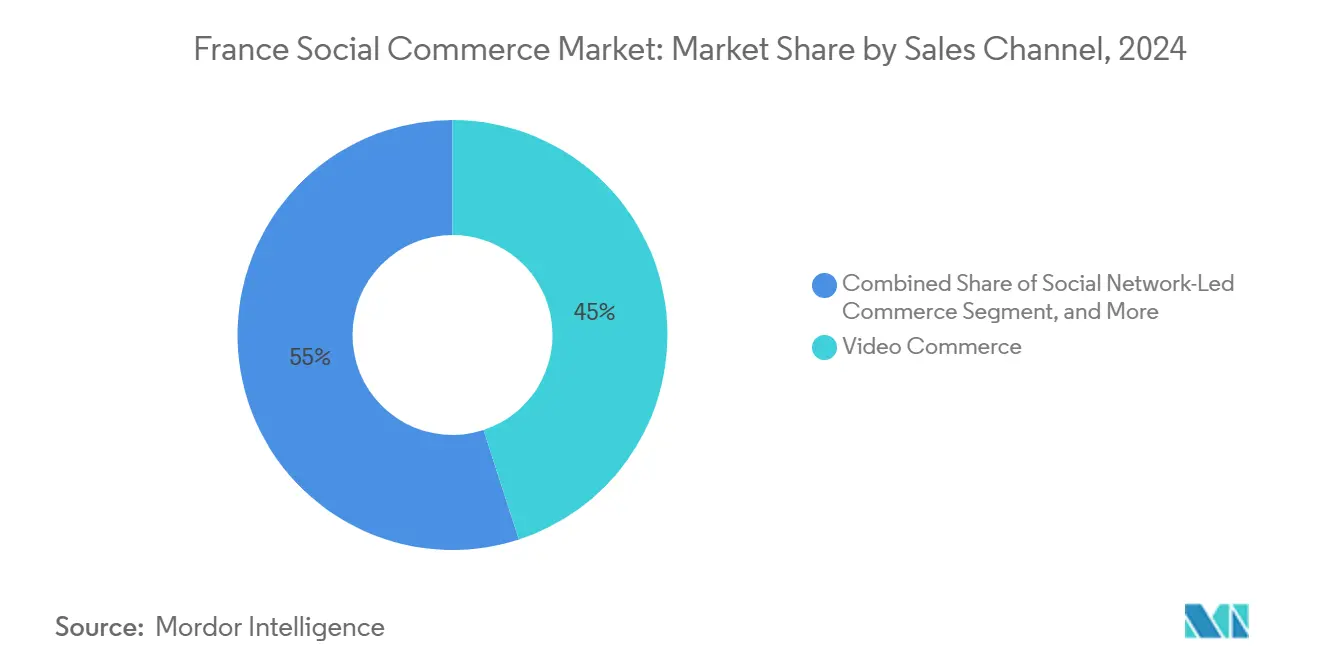

- By sales channel, Video Commerce led with a 44.82% revenue share in 2024, whereas Social Reselling is advancing at a 27.77% CAGR through 2030.

Competitive positioning in France includes both locally based firms and those operating across multiple regions. The market landscape in the global social commerce industry research shows how these players are arranged internationally.

France Social Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-first consumer journey and 5G rollout | +6.5% | National; early gains in Paris, Lyon, Marseille | Medium term (2-4 years) |

| One-click checkout APIs by French banks | +4.8% | National; led by Cartes Bancaires network | Short term (≤ 2 years) |

| EU Digital Services Act transparency rules | +3.2% | EU-wide; France an early adopter | Long term (≥ 4 years) |

| Creator-economy boom on TikTok and Twitch | +2.9% | National; urban concentration | Medium term (2-4 years) |

| Luxury AR “try-on” tools | +2.1% | Global luxury; France as innovation hub | Long term (≥ 4 years) |

| Prepaid e-money wallets for under-banked | +1.8% | National; suburban and rural areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mobile-First Consumer Journey and 5G Rollout

Orange's investment in its network has significantly expanded 5G population coverage by late 2024, improving video load times and enabling augmented reality (AR) try-ons that enhance mobile conversion rates compared to 4G. Consumers now move seamlessly from product discovery to purchase on mobile devices, with evening 5G usage driving increased activity in categories such as apparel and beauty. Enhanced engagement on 5G, as observed by retailers, demonstrates the impact of low latency and rich media in strengthening purchase intent. As operators extend coverage to rural areas, the social commerce market in France is expected to bring urban advantages to smaller regions, reducing disparities that previously affected regional businesses. Companies optimizing for 5G video commerce benefit from improved load times, sharper AR experiences, and higher transaction values, reinforcing the importance of mobile commerce.

Integration of One-Click Checkout APIs by French Banks

The Cartes Bancaires consortium integrated instant-payment rails with platforms such as Meta, TikTok, and Pinterest, significantly reducing social checkout times. This development led to a decline in cart abandonment rates for merchants, with categories like accessories experiencing notable growth in sales. Following the implementation, financial institutions observed an increase in completed transactions on social platforms. Additionally, these frictionless payment systems enhanced average basket values, demonstrating the role of speed and trust in encouraging higher consumer spending. By complying with stringent CNIL tokenization standards, privacy concerns have been effectively addressed, supporting the continued adoption of these systems across France's social commerce landscape.

EU Digital Services Act Forcing Transparent Ad-Based Social Commerce

In 2024, France's proactive enforcement of the Digital Services Act (DSA) required platforms to label paid content and disclose targeting criteria. [1]Kolsquare, “France: groundbreaking influencer law modified following EC and industry concerns”, kolsquare.comThis regulatory shift enhanced consumer trust and improved conversion rates. Luxury brands, such as L’Oréal, are utilizing this transparency to present their premium creatives without concerns of algorithmic bias. Their Instagram campaigns have experienced increased engagement under the DSA framework. Smaller sellers are also benefiting, as clear labeling creates a more equitable algorithmic environment, allowing quality content to gain visibility organically. This regulatory measure has evolved into a strategic advantage, redefining the relationship between platforms and merchants while emphasizing authenticity.

Influence-to-Earn Creator Economy Boom on TikTok and Twitch

In 2024, TikTok restructured its monetization system, replacing the Creator Fund with the Creator Rewards Program (formerly the Creativity Program Beta). This program offers performance-based payouts tied to video engagement and quality, with rates ranging from USD 4 to USD 8 per 1,000 views—significantly higher than the previous fund.[2]Fourthwall, “Is TikTok's Creator Rewards Program Worth the Payout?”, fourthwall.com Micro-influencers are performing well, as their engaged communities drive higher conversion rates, channeling spending toward niche artisans aligned with France's craftsmanship principles. Twitch's lifestyle streamers have demonstrated significant earning potential, with leading creators achieving substantial monthly income. This expanded earning framework increases the availability of creators, enhances specialized content, and distributes demand across a diverse merchant base within France's social commerce market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2024 privacy changes in iOS and CNIL cookie rules hitting conversion tracking | -2.1% | National, affecting all digital platforms | Short term (≤ 2 years) |

| Counterfeit goods clamp-down on marketplaces after EU Regulation 2023/988 | -1.5% | EU-wide, with France as strict enforcer | Medium term (2-4 years) |

| Logistics bottlenecks outside Île-de-France for same-day fulfilment | -1.3% | Regional, affecting non-metropolitan areas | Medium term (2-4 years) |

| Rising creator-commission expectations squeezing merchant margins | -0.9% | National, concentrated in high-engagement sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

2024 Privacy Changes in iOS and CNIL Cookie Rules Hitting Conversion Tracking

Apple's iOS 17.4 restricted cross-app identifiers, and stricter cookie consents from CNIL impacted retargeting accuracy.[3]Peelinsights, “iOS 17 Disrupts Link Tracking”, peelinsights.com In response, brands shifted toward server-side tagging. However, the high implementation costs created challenges for smaller sellers lacking advanced data science capabilities. Despite these disruptions, a privacy-focused approach is gaining acceptance as consumers increasingly favor brands that transparently communicate their data usage policies. Over the medium term, businesses proficient in first-party analytics are expected to recover lost attribution while strengthening their reputational standing.

Counterfeit Goods Clamp-Down on Marketplaces After EU Regulation 2023/988

Compliance with authentication requirements has led to an increase in platform costs, while significantly reducing counterfeit listings. Veepee and Showroomprivé have jointly invested in advanced technologies such as AI-driven image recognition and blockchain-based provenance systems. Although the time required for listing approvals has increased, resulting in a temporarily reduced assortment, the emphasis on verified authenticity has strengthened consumer trust, which is critical for the luxury resale segment. In the French social commerce market, brands that provide clear and reliable proof of product origin are better positioned to address regulatory demands while enhancing their value proposition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Leads While Beauty Accelerates

Apparel retained a 31.27% slice of France social commerce market share in 2024, underscoring fashion’s entrenched social roots. Influencer lookbooks, live hauls and limited-drop countdowns keep conversion elevated, and the segment’s visual nature syncs perfectly with short-form video rhythms. Personal and Beauty Care, spurred by AR shade-matching that heightens confidence, is projected to compound at 29.01% through 2030, the sharpest trajectory among all categories. Luxury skincare demonstrates significant pricing power, while mass cosmetics utilize creator-led tutorials to broaden their consumer base. Accessories benefit from impulse purchasing behavior and also gain traction through niche creators who emphasize the craftsmanship of these products.

The Food and Beverages sector leverages region-specific narratives, with French gourmet brands emphasizing terroir-driven stories to justify premium pricing. The Health Supplements segment faces challenges due to French pharmaceutical marketing regulations, which limit direct promotional activities on social platforms. As a result, brands in this segment focus on delivering educational content rather than adopting aggressive sales strategies. The Home Products category is experiencing growth, as visual content inspired by platforms like Pinterest seamlessly integrates into shoppable tags within social media feeds. Across all sectors, the French social commerce market places a strong emphasis on high-quality visual content and transparent sourcing practices, which contribute to enhancing consumer trust and perceived product value.

By Device: Smartphone Dominance Masks Cross-Device Complexity

Smartphones captured 90.77% of the France social commerce market size in 2024. Instant gratification, biometric security, and embedded wallets are influencing on-the-go purchasing behaviors, particularly among younger consumers who predominantly rely on mobile devices for social commerce transactions. However, desktops continue to play a significant role in high-value purchases, as larger screens enable detailed comparisons and provide a sense of security for risk-averse buyers. Mobile devices dominate evening shopping activities, while office laptops are frequently used during midday browsing, which often transitions to mobile-based purchases later. Businesses that effectively synchronize session data across multiple devices achieve improved revenue per user, highlighting the importance of cohesive identity management strategies.

Regulatory considerations also impact consumer behavior. Desktop browsers, offering advanced privacy settings, appeal to older, privacy-conscious demographics. On the other hand, mobile applications, with their secure environments for payment information, foster trust for smaller transactions. Consequently, businesses must adopt a comprehensive device strategy that supports the entire shopping journey, from discovery to purchase, across platforms where consumers feel most secure. This multi-faceted approach emphasizes the necessity of adaptable content and seamless authentication mechanisms within the French social commerce environment.

By Sales Channel: Video Commerce Leadership Faces Social Reselling Disruption

In 2024, Video Commerce constituted 44.82% of total revenue, driven by France's increasing preference for demonstrative storytelling through live streams and shoppable reels. Conversion rates experienced notable growth during time-sensitive broadcasts, where hosts addressed real-time inquiries, replicating the experience of in-store consultations. Simultaneously, Social Reselling demonstrated a strong 27.77% CAGR, supported by Gen Z's emphasis on sustainability and demand for authenticated pre-owned luxury goods. To enhance trust and mitigate counterfeit risks, platforms have implemented escrow services and AI-powered image verification systems.

Social Network-Led Commerce leverages extensive user bases, enabling marketers to optimize their spending through closed-loop analytics. In France, Group Buying aligns with the country's sociable culture, aggregating demand to achieve cost savings on essential goods and electronics. Additionally, Product Review and Discovery Platforms function as preparatory stages, where users engage with comparative content before transitioning to streamlined checkout processes. As a result, effective multichannel coordination is essential; brands that deliver consistent messaging across platforms not only gather valuable first-party data but also enhance their positioning within France's social commerce market.

Geography Analysis

Île-de-France, supported by extensive 5G coverage and efficient same-day fulfillment networks, holds a significant portion of the market value. In Paris, higher disposable incomes drive larger luxury purchases, while a concentration of creator communities fosters a cycle of content creation and consumption. Lyon and Marseille also exhibit higher adoption rates compared to rural areas, driven by their younger populations and proactive technological initiatives.

In regions outside major metropolitan areas, delivery times are longer, reducing the appeal of impulse purchases. To address this, merchants collaborate with local corner stores and locker networks, enhancing click-to-collect services in smaller communities. Additionally, the growing use of fintech wallets among suburban teenagers is increasing spending in areas with limited access to traditional banking services. French overseas departments present emerging opportunities due to improving broadband access and a cultural preference for French luxury, although high logistics costs remain a challenge for same-day delivery.

Cross-border dynamics are also significant. French platforms with DSA-compliant processes experience smoother expansion into Spain, Belgium, and Italy, where transparency regulations are aligned. However, differing privacy laws in Britain create obstacles, emphasizing the critical role of regulatory frameworks. Geography influences both the economics of fulfillment and regulatory compatibility within France's social commerce landscape.

Mordor Intelligence tracks the social commerce market with additional country-level coverage spanning India, Brazil, Canada, and China, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

France's social commerce ecosystem is undergoing significant transformation, driven by three key competitive segments: global social networks, domestic retail companies, and fintech-driven challengers. Global platforms such as Meta's Instagram and Facebook, along with ByteDance's TikTok, are shaping influencer-driven commerce and livestream shopping formats, offering extensive reach.[4]Remotestaff, “The Rise of Social Commerce: How TikTok and Instagram Are Reshaping Online Shopping”, remotestaff.com Domestic companies like Carrefour and FNAC Darty utilize their established physical presence and proprietary media studios to deliver integrated omnichannel experiences. Luxury brands, including LVMH and L’Oréal, are advancing augmented reality (AR) virtual try-ons, enhancing customer engagement and conversion rates.[5]Everything-pr, “L’Oréal’s Virtual Makeup Try-On: Transforming Beauty Marketing in the Digital Age”, everything-pr.com

Fintech firms such as Lydia and Pixpay are improving payment accessibility, focusing on younger demographics and underserved groups. Authentication services supported by blockchain technology are strengthening the luxury resale segment, while SaaS tools facilitate seamless catalog integration across platforms like Instagram, TikTok, and emerging French platforms such as BeReal Commerce. Compliance with CNIL data protection guidelines is becoming a strategic advantage, enabling companies to introduce new features efficiently while managing regulatory risks and maintaining consumer trust.

The sector is moving towards live-commerce studios, micro-influencer platforms, and blockchain-based authenticity solutions. Acquisitions, such as Veepee's purchase of Rebag France, highlight the growing importance of authenticated second-hand luxury markets. As these trends progress, France's social commerce sector increasingly prioritizes platforms that integrate regulatory compliance, innovation, and streamlined payment processes within a mobile-first framework, ensuring scalability and competitive positioning.

France Social Commerce Industry Leaders

Meta Platforms, Inc.

ByteDance Ltd.

Pinterest, Inc.

Snap Inc.

Cdiscount SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Walmart introduced a weekly livestreaming series aimed at collectors, reflecting the increasing global integration of entertainment and e-commerce. This approach, which incorporates live product demonstrations, giveaways, and community interaction, is modeled after established practices in China and the U.S. It highlights an opportunity for French retailers to explore similar strategies. The initiative demonstrates how livestreaming can facilitate real-time sales, strengthen brand engagement, and cater to younger, mobile-oriented consumers in France.

- September 2025: La Poste, through its parcel delivery division Colissimo, formalized a Memorandum of Understanding (MOU) with global e-commerce platform Temu. This agreement focuses on enhancing logistics collaboration and providing support to local sellers in France. The initiative aims to improve services for French consumers and sellers, facilitate international sales for local businesses, and optimize logistics operations. By integrating Colissimo’s logistics capabilities with Temu’s digital platform, the collaboration offers local sellers—particularly SMEs—reliable domestic and international delivery, adaptable fulfillment options, and environmentally conscious shipping solutions. This partnership expands seller accessibility, simplifies cross-border trade, and aligns with mobile-driven shopping trends, improving the efficiency of social commerce for French consumers and businesses.

- March 2025: TikTok has introduced TikTok Shop in France, offering an integrated in-app shopping feature tailored to Gen Z users. This initiative provides opportunities for both local and international sellers while adhering to EU VAT regulations, which designate TikTok as a deemed supplier for non-EU sellers. This approach streamlines compliance processes and facilitates cross-border trade, contributing to the development of France's mobile-focused retail environment and supporting creator-driven product exploration.

- November 2024: Wero, a company under the European Payments Initiative (EPI), has introduced a payment solution in France. Designed as a pan-European instant payment platform, Wero facilitates efficient and secure peer-to-peer and e-commerce transactions through mobile applications, enhancing the overall user experience. By collaborating with major French banks and transitioning from Paylib, Wero has streamlined digital payment processes. This initiative supports mobile-centric shopping and creator-driven commerce, enabling faster and more accessible social buying across various platforms.

France Social Commerce Market Report Scope

The France Social Commerce Market Report is Segmented by Product Type (Apparel, Personal and Beauty Care, Accessories, Home Products, Health Supplements, Food and Beverages, Other Product Types), Device (Laptops and Desktops, Smartphone), Sales Channel (Video Commerce, Social Network-Led Commerce, Social Reselling, and Other Sales Channel Types), and Geography (France). The Market Forecasts are Provided in Terms of Value (USD).

| Apparel |

| Personal and Beauty Care |

| Accessories |

| Home Products |

| Health Supplements |

| Food and Beverages |

| Other Product Types |

| Laptops and Desktops |

| Smartphone |

| Video Commerce |

| Social Network-Led Commerce |

| Social Reselling |

| Group Buying / Team Purchase |

| Product Review and Discovery Platforms |

| By Product Type | Apparel |

| Personal and Beauty Care | |

| Accessories | |

| Home Products | |

| Health Supplements | |

| Food and Beverages | |

| Other Product Types | |

| By Device | Laptops and Desktops |

| Smartphone | |

| By Sales Channel | Video Commerce |

| Social Network-Led Commerce | |

| Social Reselling | |

| Group Buying / Team Purchase | |

| Product Review and Discovery Platforms |

Key Questions Answered in the Report

What revenue does the France social commerce market generate in 2025?

The France social commerce market size is valued at USD 32.53 billion in 2025.

How fast is French social commerce forecast to grow through 2030?

Market value is expected to reach USD 110.25 billion by 2030, charting a 27.65% CAGR.

Which product category grows the quickest?

Personal and Beauty Care leads with a projected 29.01% CAGR to 2030 thanks to accurate AR try-ons.

Why do smartphones dominate transactions?

Smartphones account for 90.77% of 2024 volume because 5G speeds and in-app wallets eliminate friction, though desktops still close high-value baskets.

What regulation most influences advertiser strategy?

The EU Digital Services Act mandates transparent ad disclosures, which has improved conversion by 31% since rollout in 2024.

Who are notable innovators in French social commerce?

L’Oréal, LVMH and Carrefour stand out for AR, blockchain authentication, and live-streaming store formats respectively.

Page last updated on: