France Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

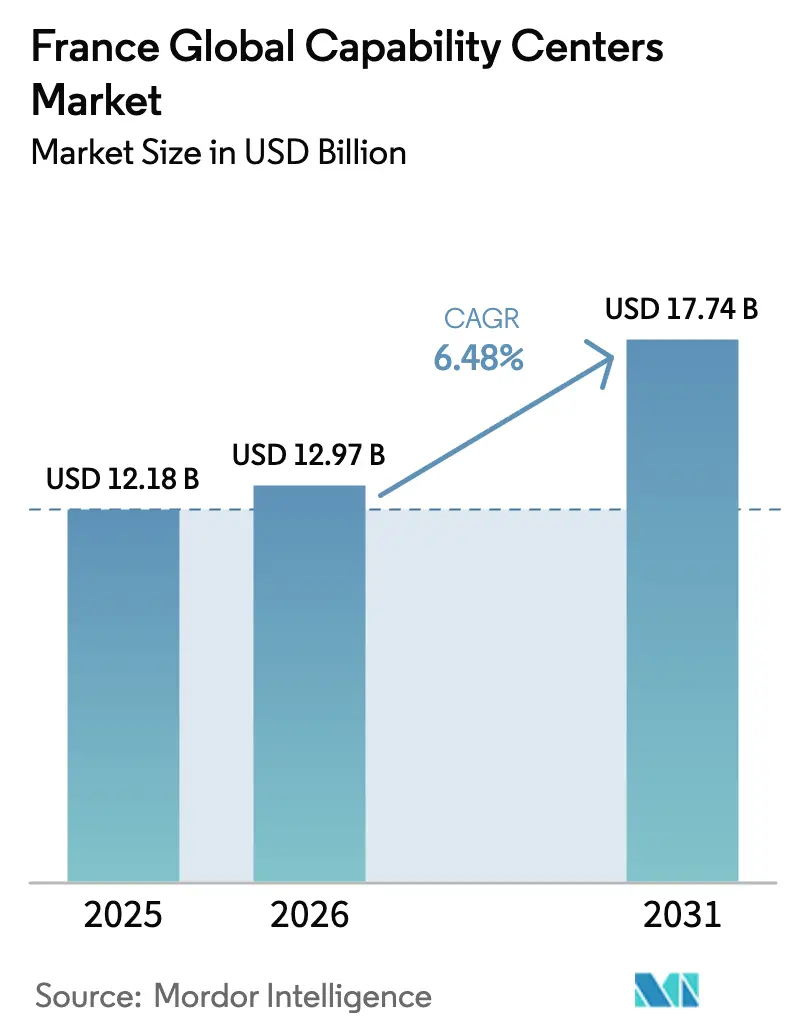

| Base Year Market Size (2025) | USD 12.18 Billion |

| Market Size (2026) | USD 12.97 Billion |

| Market Size (2031) | USD 17.74 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Global Capability Centers Market Analysis by Mordor Intelligence

The France global capability centers market size is expected to grow from USD 12.18 billion in 2025 to USD 12.97 billion in 2026 and is forecast to reach USD 17.74 billion by 2031 at 6.48% CAGR over 2026-2031. Strength comes from the France 2030 innovation program, Brexit-triggered relocations, and a widening STEM talent pipeline. Multinational corporations view France as a jurisdiction that safeguards intellectual property while remaining fully aligned with European data regulations, prompting accelerated R&D-centric investment. Large brownfield sites released by financial institutions exiting the United Kingdom shorten the time-to-market for new centers, while nationwide 5G and edge-compute corridors underpin Industry 4.0 use cases. Cost premiums tied to social charges persist, yet companies justify the differential by focusing on higher-value, regulation-intensive capabilities.

Key Report Takeaways

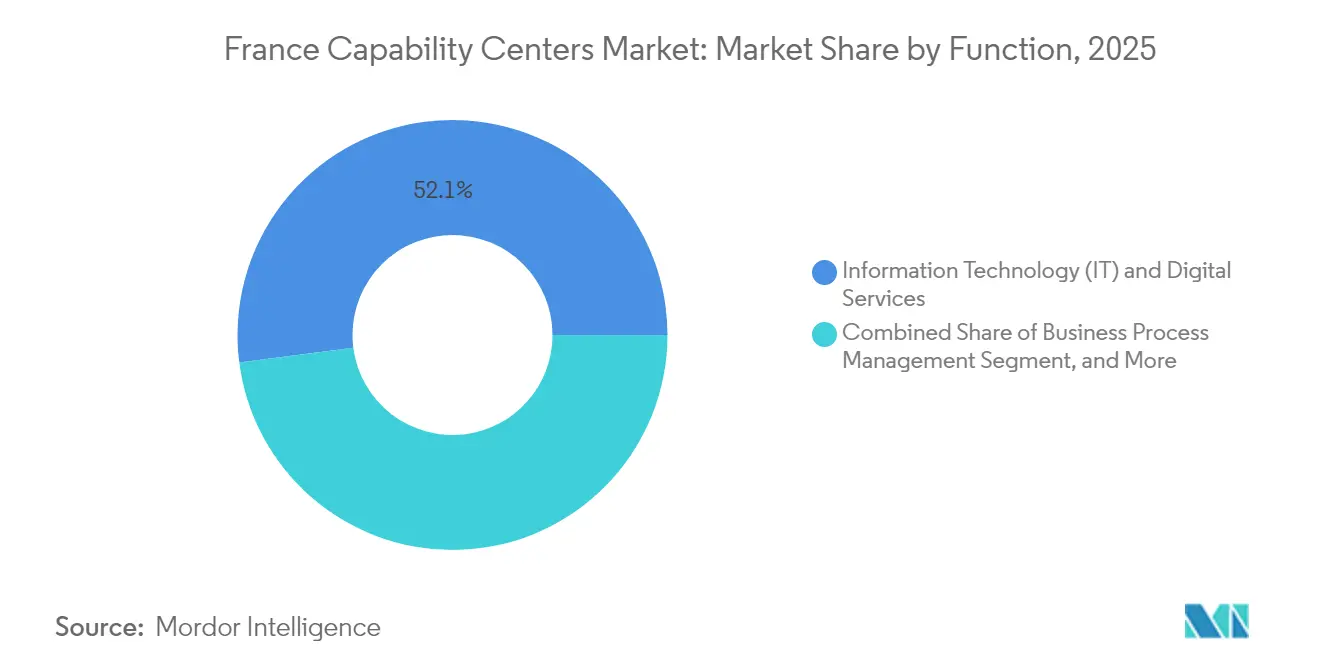

- By function, Information Technology and Digital Services held 52.05% of the France global capability centers market share in 2025, while Knowledge Process Outsourcing is advancing at a 6.82% CAGR through 2031.

- By engagement model, captive operations accounted for 58.35% of the France global capability centers market size in 2025; Hybrid Build-Operate-Transfer structures are expected to expand at a 7.22% CAGR through 2031.

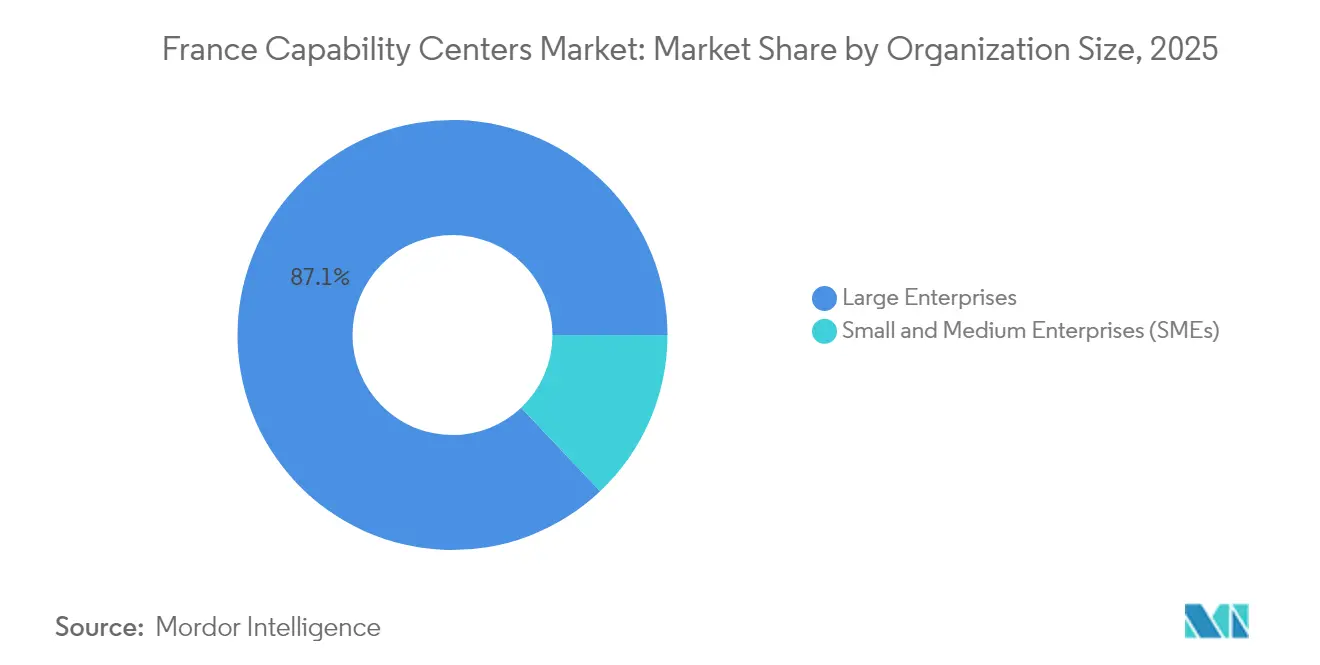

- By organization size, large enterprises represented 87.05% of demand in 2025, whereas small and medium enterprises are forecast to grow at an 8.03% CAGR.

- By industry vertical, Banking, Financial Services, and Insurance led with 38.60% revenue share in 2025, while Healthcare and Life Sciences are set to rise at a 7.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing nearshore preference by EU-headquartered MNCs for IP-safeguarded R&D | +1.8% | European Union, with a concentration in France and Germany | Medium term (2-4 years) |

| France 2030 Plan's USD 34 billion innovation stimulus unlocking Global Capability Center capital | +1.5% | National, with early gains in the Paris, Lyon, and Toulouse regions | Long term (≥ 4 years) |

| Deep STEM graduate pool boosted by French Tech Visa reforms | +1.2% | National, strongest in Île-de-France, and major metropolitan areas | Medium term (2-4 years) |

| Paris region's 5G and edge-compute corridors enabling Industry 4.0 Global Capability Center use-cases | +0.9% | Paris region, expanding to Lyon and Marseille corridors | Short term (≤ 2 years) |

| Availability of brownfield sites vacated by Brexit-driven relocations | +0.7% | Paris financial district and La Défense business district | Short term (≤ 2 years) |

| Tax credit for collaborative research (CIR) lowers the total cost of ownership | +0.6% | National, with higher utilization in R&D-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Nearshore Preference by EU-Headquartered MNCs for IP-Safeguarded R&D

European corporations now prioritize jurisdictional sovereignty and data protection when choosing R&D sites. Roughly 3,500 financial services positions relocated to Paris following Brexit, underscoring a broader preference for locations fully aligned with EU regulations.[1]Fortune Europe staff, “French government steps in to rescue Atos, once renowned as the nation's top tech firm,” Fortune Europe, fortune.com The French legal framework provides robust intellectual property safeguards and GDPR compliance, offering engineering and analytics teams the confidence to process sensitive datasets. Proximity to the European Patent Office accelerates time-to-market for new products, while close access to customers in major EU capitals improves iterative design cycles. As a result, France attracts disproportionately large investment volumes compared to traditional Central and Eastern European alternatives.

France 2030 Plan Innovation Stimulus Unlocking Global Capability Center Capital

France 2030 dedicates USD 54 billion to ten strategic objectives, and more than USD 33 billion is already deployed across 3,500 projects. The program funds collaborative research facilities, subsidizes pilot production lines, and grants tax credits on qualifying research and development (R&D), directly lowering establishment costs for capability centers. High-profile commitments, such as Microsoft’s EUR 4 billion (USD 4.4 billion) cloud investment, validate the ecosystem’s pull effect. The plan further aligns with EU green and digital objectives, creating long-duration demand for analytics, simulation, and decarbonization skills inside French sites.

Deep STEM Graduate Pool Boosted by French Tech Visa Reforms

France graduates about 750,000 STEM students annually from institutes like École Polytechnique. Recent French Tech Visa changes remove bureaucratic barriers for foreign specialists, thereby accelerating the onboarding process for AI and cybersecurity talent. The larger talent supply lets capability centers scale advanced functions instead of routine services. Competitive salary levels remain above those in Eastern Europe, but employers report lower attrition and higher productivity, underpinning a shift toward knowledge-intensive workloads that better absorb France’s 45% social charge premium.

Paris Region 5G and Edge-Compute Corridors Enabling Industry 4.0 Global Capability Center Use-Cases

Nationwide 5G rollouts by operators such as Orange complement extensive edge data-center grids around Paris. Aerospace primes like Airbus already operate private 5G networks to test digital twin models and predictive maintenance. These infrastructure layers are essential for real-time analytics and low-latency industrial automation, giving France’s capital an edge over offshore hubs without mature edge ecosystems. Automotive, energy, and logistics firms, therefore, anchor next-generation engineering centers in the region, feeding demand for software-defined manufacturing talent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent labor code increases separation costs | -1.1% | National, with a higher impact in traditional industrial regions | Long term (≥ 4 years) |

| Higher social security contributions versus CEE countries | -0.8% | National, affecting all employment categories | Medium term (2-4 years) |

| Scarcity of large contiguous Grade-A office space in Tier-2 French cities | -0.5% | Lyon, Marseille, Toulouse, and other tier-2 metropolitan areas | Short term (≤ 2 years) |

| Rising anti-outsourcing sentiment among local unions | -0.3% | National, concentrated in traditional manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Labor Code Increasing Separation Costs

French employment law mandates extensive consultation, retraining, and severance that can total 6-12 months of salary, far exceeding the 1-3 month norms in Poland or the Czech Republic. Workforce reductions, therefore, necessitate long lead times and detailed social plans, thereby increasing compliance overhead for capability centers in volatile tech niches. On the upside, strong protections lower attrition, creating stable knowledge retention and supporting long-term R&D roadmaps.

Higher Social Security Contributions Versus CEE Countries

Employers face aggregated social charges near 45% of gross wages, covering health, unemployment, and retirement schemes.[2]Business Reporter team, “Atos open for French state to take minority stake in strategic business unit BDS,” business-reporter.co.uk The differential erodes competitiveness for labor-intensive processes. However, France’s 30% credit under the Crédit d’Impôt Recherche partially offsets the burden for qualifying R&D tasks, nudging portfolios toward high-value activities that capitalize on world-class research assets, rather than focusing solely on pure cost savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Digital Services Anchor the Portfolio

Information Technology and Digital Services held a 52.05% market share of the French global capability centers market in 2025, benefiting from relentless cloud migration, cybersecurity mandates, and EU digital sovereignty goals. The segment’s dominance persists as firms deploy DevSecOps pipelines and zero-trust architectures that must remain within EU borders. The France global capability centers market size for Knowledge Process Outsourcing is projected to expand at a 6.82% CAGR, powered by demand for AML screening, IP-portfolio valuation, and multilingual regulatory-filing support. Engineering and R&D hubs, particularly in aerospace propulsion and battery chemistry, are growing steadily as conglomerates tap into France’s research clusters. Business Process Management exhibits flat trajectories because repetitive workflows are increasingly automated or shifted to lower-cost regions, although data-protection-sensitive back-office tasks remain in-country.

In the medium term, digital product teams will integrate generative AI toolchains that rely on in-country model training sandboxes to meet stringent data localization stipulations. R&D units pursue hydrogen-fuel research linked to Europe’s decarbonization requirements and count on proximity to Grenoble and Toulouse laboratories. The evolving functional mix underscores that France no longer competes on wage advantage; instead, centers absorb higher social-charge outlays in exchange for world-class engineering depth, easy access to EU regulators, and robust IP defenses. Consequently, workloads migrate up the value chain, confirming that complex digital-service delivery and governed analytics will remain the nucleus of future capability center charters.

By Engagement Model: Hybrid Structures Gain Momentum

Captive entities contributed 58.35% to the France global capability centers market size in 2025, as multinationals prefer full control of sensitive codebases and compliance processes. Yet Build-Operate-Transfer frameworks are forecast to advance at a 7.22% CAGR as firms seek quicker market entry without committing heavy upfront capital. French integrators oversee initial hiring, payroll, and property leases, then relinquish day-to-day control once knowledge baselines are established. The approach helps mid-cap European firms overcome hurdles related to unfamiliarity with labor laws and complex reporting obligations.

Joint ventures also blossom, pairing foreign product owners with French telecom or engineering majors to navigate local standards. Contractual clauses are increasingly incorporating ESG metrics, reflecting France’s corporate responsibility statutes. While outsourcing contracts for commodity IT continue to shrink, a blended model that marries partner agility with ultimate parent oversight now prevails. Over the forecast period, multinationals are expected to break large captive portfolios into modular transfer tranches, fostering incremental risk management and agile workforce scaling. The result will be an engagement-landscape mosaic rather than a binary captive-versus-outsourced mix, sustaining healthy consulting and integration pipelines for domestic service providers.

By Organization Size: SMEs Accelerate Participation

Large enterprises dominated 2025 with an 87.05% share, a natural outcome of their substantial capital and robust internal compliance teams. However, France’s digitized one-stop registration portals, along with fast-track French Tech Visas, entice growth-stage startups and mid-sized manufacturers to establish engineering or analytics teams within the country. The France global capability centers industry is therefore experiencing democratization, with SME activity climbing at an 8.03% CAGR. Cloud-native toolchains, remote collaboration suites, and subscription-based cyber-defense platforms relieve smaller firms from high fixed costs traditionally associated with cross-border operations.

Public programs, such as Première usine, subsidize first-time industrial sites, having funneled grants to 31 projects so far. In turn, SMEs gain access to manufacturing or testing bays adjacent to elite research labs, thereby compressing prototype cycles. These dynamics inject fresh competitive tension as smaller innovators vie for the same AI, robotics, and semiconductor talent that once monopolized blue-chip companies. Over time, a more diversified demand base should reinforce local supplier ecosystems ranging from legal advisory to facility management.

By Industry Vertical: Financial Services Lead, Life Sciences Surge

Banking, Financial Services, and Insurance accounted for 38.60% of revenue in 2025, underpinned by Paris’s stature as Europe’s second-largest financial center. Regulatory reporting, anti-money laundering analytics, and quantitative risk engines require teams with expertise in both capital markets mathematics and EU directives, thereby cementing France’s appeal. Conversely, life-sciences capability centers will expand at the fastest rate, with a 7.08% CAGR, driven by synergies with Sanofi, the Institut Pasteur, and a maturing biotech start-up scene.

Automotive and aerospace complexes around Toulouse and Nantes leverage their in-depth knowledge of composites and access to funding streams for battery research and development. Telecom operators utilize 5G testbeds to refine private-network orchestration, while retail groups establish circular-economy analytics desks in alignment with France’s stringent environmental regulations. As sectoral breadth widens, cross-industry talent mobility intensifies, compelling employers to craft sharper value propositions in areas such as quantum-safe encryption, sustainable finance data modeling, and climate-aligned supply chain transparency.

Geography Analysis

Paris and its inner suburbs anchor more than half of France's current global capability centers, with market activity driven by La Défense’s dense concentration of financial tenants, direct TGV links to Brussels and Frankfurt, and short-hop access to EU institutions in Strasbourg. Brexit relocations freed large trading-floor footprints that now host data-science pods and regulatory-reporting cells. The Grand Paris Express, which will add 68 metro stations by 2030, broadens talent catchment zones and unlocks office hotspots in Saint-Denis and Villejuif. [3]Apur research unit, “Office stock dynamics in the Greater Paris - Grand Paris,” apur.org

Second-tier cities, such as Lyon, Marseille, and Toulouse, present compelling cost arbitrage of up to 20% on real estate and salary packages compared to the capital. Lyon benefits from pharmaceutical clusters, Marseille from subsea-cable gateways, and Toulouse from aerospace giants. Nonetheless, a shortage of contiguous Grade-A space above 10,000 square meters constrains mega-hub ambitions. Firms therefore deploy hub-and-spoke models: flagship R&D or compliance teams remain Paris-centric, while digital operations or multilingual support sit in regional satellites.

France’s EU membership simplifies cross-border service passports, allowing centers to support pan-European clients without supplementary licensing hurdles. Double-taxation treaties further streamline intercompany pricing. National R&D tax credits, in effect through 2029, help offset Paris rental premiums and social charges for innovation-intensive workloads. Looking ahead, regions along the Bordeaux-Toulouse-Montpellier axis may capture increased quantum-computing investment as universities scale physics faculties and utility-grade power capacity expands.

Competitive Landscape

The competitive field is moderately concentrated. Domestic integrators, such as Capgemini and Sopra Steria, secure contracts that hinge on an intimate familiarity with French procurement norms and labor statutes. Capgemini generated EUR 4.537 billion (USD 4.99 billion) of France-specific revenue in 2023. Sopra Steria followed at EUR 2.808 billion (USD 3.09 billion), while global pure-play consultancies, such as Accenture, position French delivery nodes as regulatory-compliant extensions of pan-EU managed-service footprints.

Indian tier-1 vendors, including TCS and Infosys, pursue tuck-in acquisitions of niche cybersecurity boutiques to gain local regulatory credentials. Meanwhile, the French state signaled willingness to acquire Atos’s Advanced Computing arm for up to EUR 625 million (USD 688 million), underscoring sovereign-tech priorities.[4]Atos press office, “Atos receives non-binding offer from the French State to acquire its Advanced Computing activities,” atos.net Such interventions stabilize critical HPC and quantum talent pools that feed broader capability-center needs. Sustainability-driven IT outsourcing is also on the rise; the Atos-Open-Sopra Steria consortium recently secured a public-sector framework to supply digital transformation services grounded in precise CO₂ metrics.

Strategic moves trend toward hybrid engagement: Capgemini’s Future4Care partnership combines healthcare incumbents with AI startups, creating data-sharing sandboxes in accordance with French data protection laws. Accenture has opened a Generative AI studio in Paris, promising model fine-tuning that is wholly on EU soil. Vendors also cultivate ties with top engineering schools to lock early access to graduates, recognizing that talent scarcity, not client demand, poses the greatest growth constraint through 2030.

France Global Capability Centers Industry Leaders

Accenture plc

Capgemini SE

Tata Consultancy Services Limited

Cognizant Technology Solutions Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Atos successfully completed its financial restructuring plan, emerging with EUR 2.9 billion (USD 3.19 billion) less debt and a sharper focus on digital transformation and cybersecurity services, positioning the firm for renewed competitiveness in France’s GCC landscape while safeguarding key sovereign technology contracts.

- September 2025: Tata Consultancy Services formed a strategic partnership with CEA to co-develop physical-AI and robotics solutions for industrial use, blending TCS’s AI strengths with CEA’s research depth to advance France’s manufacturing and energy sectors.

- August 2025: DXC Technology secured a three-year, EUR 150 million (USD 165 million) contract extension with French government agencies to modernize IT infrastructure, covering cloud migration, cybersecurity, and digital-workplace upgrades across several ministries.

- July 2025: Atos finalized the EUR 625 million (USD 688 million) sale of its Advanced Computing activities to the French State, transferring high-performance computing, quantum, and AI divisions and roughly 2,500 employees, thereby ensuring national control over strategic defense technologies and allowing Atos to concentrate on commercial pursuits.

France Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) (Joint Venture / Strategic Partnership and Virtual Captive Model) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) (Joint Venture / Strategic Partnership and Virtual Captive Model) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the size of the France global capability centers market in 2026?

The France global capability centers market size is USD 12.97 billion in 2026.

What is the forecast CAGR through 2031?

The market is expected to grow at a 6.48% CAGR between 2026 and 2031.

Which function contributes the most revenue?

Information Technology and Digital Services lead with a 52.05% share in 2025.

Which engagement model is growing fastest?

Hybrid Build-Operate-Transfer structures are expanding at a 7.22% CAGR through 2031.

Why do companies choose France over Eastern Europe?

Firms prioritize robust IP protection, GDPR alignment, and easy access to EU regulators, which outweigh the higher labor costs.

Which industry vertical will see the fastest growth?

Healthcare and Life Sciences capability centers are projected to rise at a 7.08% CAGR to 2031.

Page last updated on: