France Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

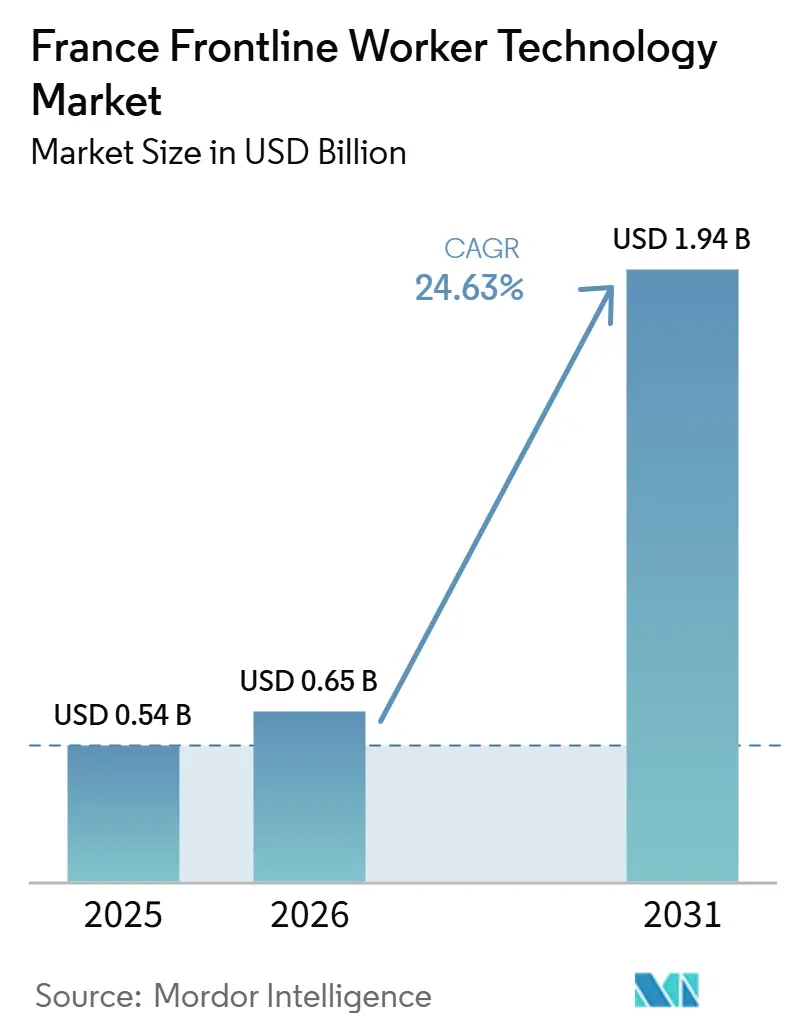

| Base Year Market Size (2025) | USD 0.54 Billion |

| Market Size (2026) | USD 0.65 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 24.63% CAGR |

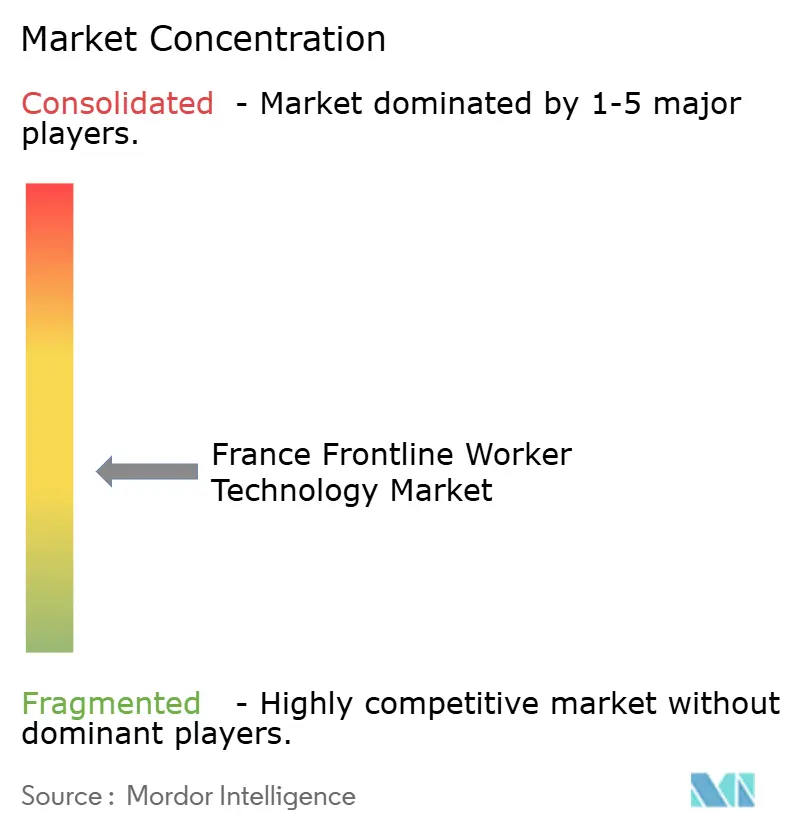

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Frontline Worker Technology Market Analysis by Mordor Intelligence

The France frontline worker technology market size is expected to increase from USD 0.54 billion in 2025 to USD 0.65 billion in 2026 and reach USD 1.94 billion by 2031, growing at a CAGR of 24.63% over 2026-2031. The France frontline worker technology market is moving from isolated pilot programs toward broader operational rollouts as employers try to improve output from existing frontline teams rather than rely on difficult hiring. Buyers are putting more emphasis on tools that support communication, task flow, scheduling, and workforce visibility because service delays and coordination gaps now have a direct cost in manufacturing, healthcare, logistics, and retail. The France frontline worker technology market is also benefiting from stronger interest in cloud deployments and mobile-first software, as organizations seek faster implementation with less friction across distributed sites. Competition is split between global enterprise software suites and specialist frontline platforms, which is pushing vendors to combine broader functionality with easier deployment and clearer payback. Compliance requirements around employee data, AI governance, and audit-ready workflows are raising the product standard, favoring vendors that pair a simple user experience with stronger control features.

Key Report Takeaways

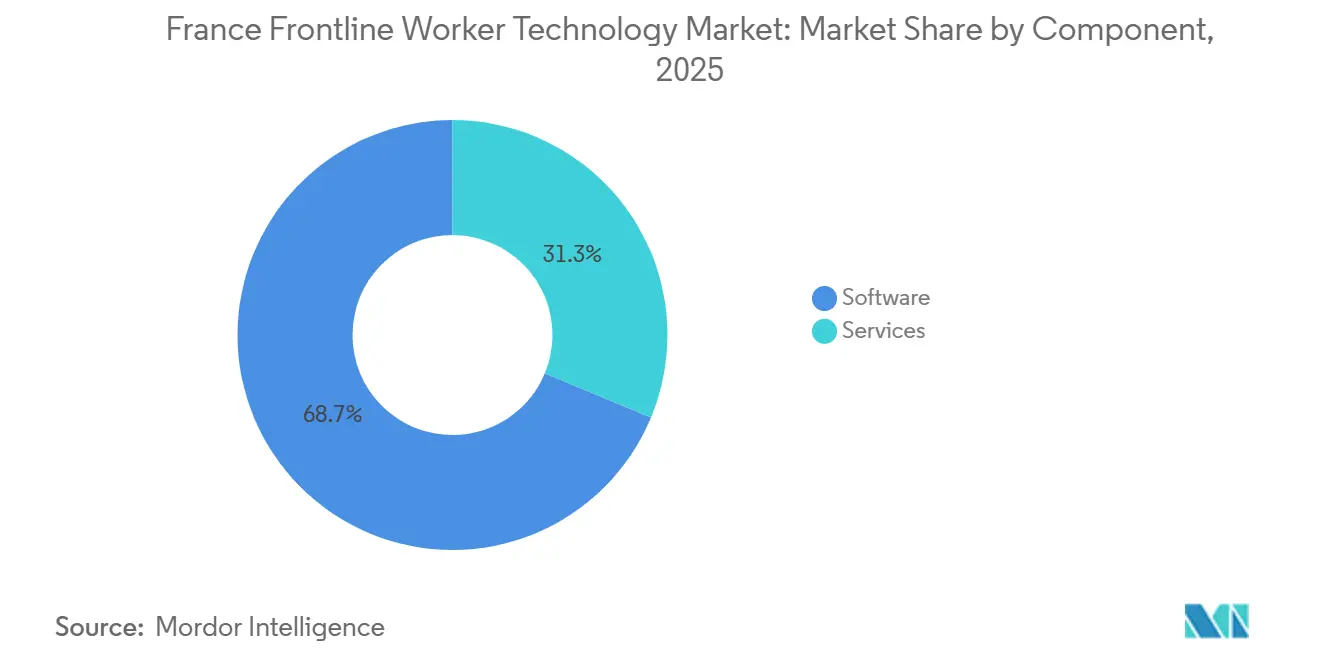

- By component, software held 68.74% of revenue in 2025, while services are projected to expand at a 26.91% CAGR from 2026 to 2031.

- By deployment, cloud-based accounted for 61.58% of the France frontline worker technology market size in 2025 and is projected to grow at a 27.84% CAGR through 2031.

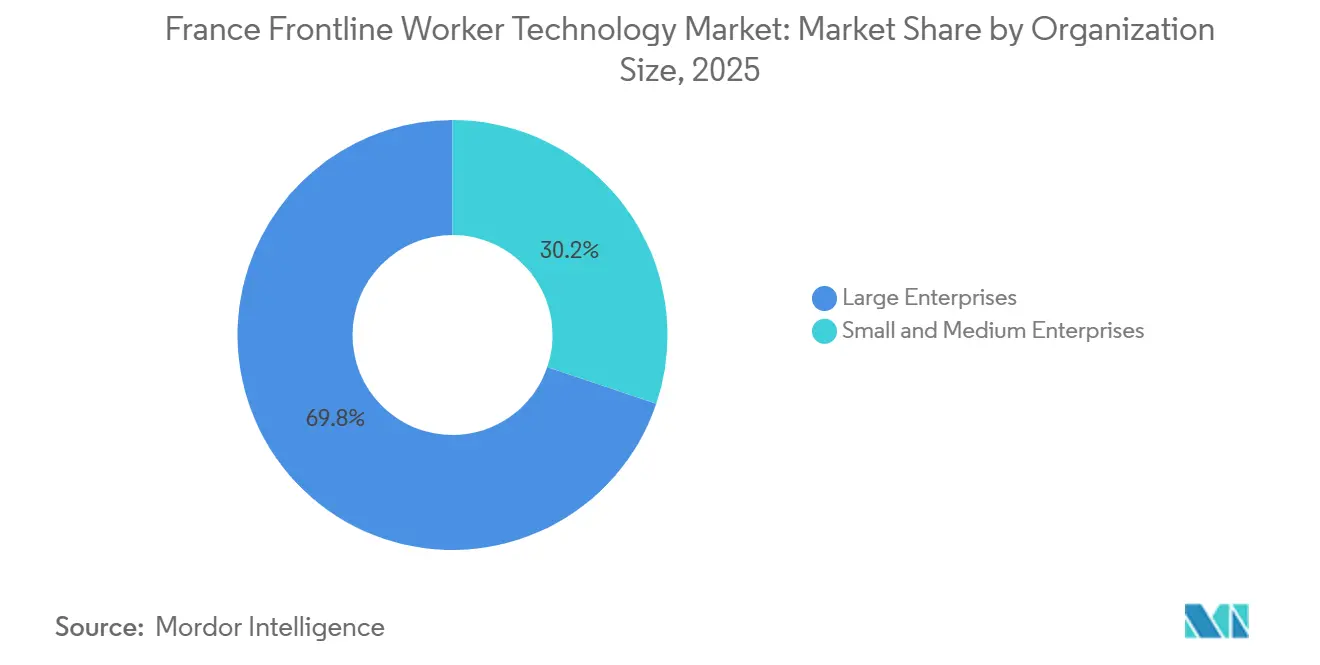

- By organization size, large enterprises held 69.82% of revenue in 2025, while small and medium enterprises are projected to record the fastest 27.46% CAGR through 2031.

- By application, employee communication and engagement held 24.63% of revenue in 2025, while workforce analytics and performance management is projected to expand at a 29.18% CAGR through 2031.

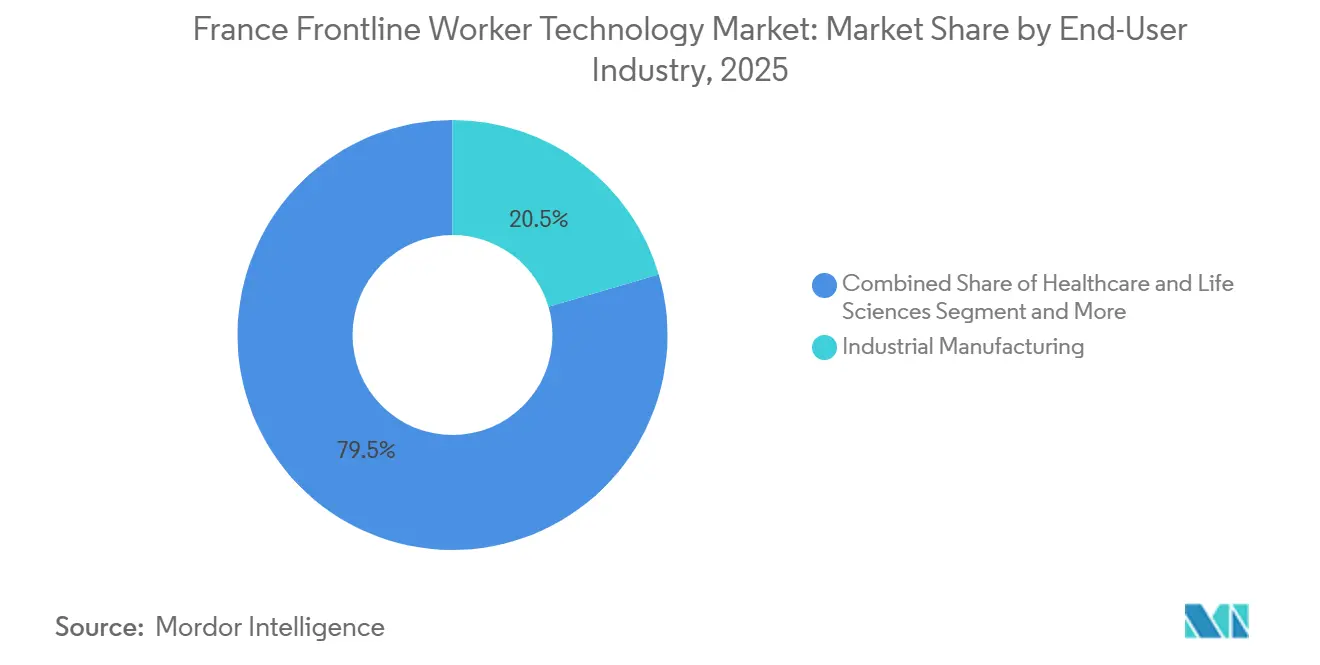

- By end-user industry, industrial manufacturing accounted for 20.46% of revenue in 2025, while healthcare and life sciences is projected to grow at a 28.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Real-Time Task Orchestration Across Distributed Frontline Teams | +6.5% | National, with high intensity in Ile-de-France, Grand Est, and Auvergne-Rhone-Alpes industrial clusters | Short term (≤ 2 years) |

| Compliance Pressure for Audit-Ready Digital Workflows | +5.3% | National, with regulatory influence concentrated in Paris-based enterprise headquarters and EU-headquartered multinationals | Medium term (2-4 years) |

| Workforce Shortages Increasing Dependence on Productivity Software | +4.6% | National, with elevated impact in Hauts-de-France manufacturing belt, Ile-de-France services sector, and healthcare regions | Short term (≤ 2 years) |

| Faster Adoption of AI-Assisted Remote Support and Guided Work Instructions | +4.2% | National, with early gains in automotive and aerospace manufacturing corridors in Grand Est and Occitanie | Medium term (2-4 years) |

| Expansion of Mobile-First Workforce Applications in Asset-Heavy Industries | +3.4% | National, with strongest pull in industrial manufacturing and logistics corridors | Medium term (2-4 years) |

| Rising Use of Wearables, Connected Devices, and Industrial Mobility | +2.8% | National, with spillover into construction and field services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Real-Time Task Orchestration Across Distributed Frontline Teams

French employers are moving from digital trial programs toward execution models that improve consistency on the frontline, and task orchestration sits near the center of that shift. In Rockwell Automation's 2026 survey, 41% of French manufacturers cited skills gaps as a leading barrier, while 36% cited communication challenges as a key drag on digital progress. Those two pressure points create a clear case for systems that route work instructions, surface exceptions, and coordinate teams across sites without depending on constant supervisor intervention. In practical terms, the France frontline worker technology market gains when companies treat structured workflow delivery as an operating requirement rather than a software feature. These tools also help preserve know-how because process steps can be encoded into repeatable mobile workflows and used by newer workers during shifts. Rockwell Automation also reported that cloud platforms delivered the highest reported ROI among French manufacturers in 2026, with recognition doubling year over year to 32%, which supports the case for cloud-native orchestration tools in the France frontline worker technology market.[1]Rockwell Automation, “French Manufacturers Shift Focus to ROI - State of Smart Manufacturing 2026,” Rockwell Automation, rockwellautomation.com

Compliance Pressure For Audit-Ready Digital Workflows

Compliance has become a direct buying factor for workforce software in France because employers now need clearer control over how employee data is captured, used, and reviewed. The CNIL reported cumulative fines of EUR 486,839,500 (USD 525.8 million) in 2025 and sanctioned 16 organizations for non-compliant employee surveillance practices, underscoring that workforce oversight practices are under active scrutiny.[2]Commission Nationale de l'Informatique et des Libertés, “Sanctions Et Mesures Correctrices, La CNIL Présente Le Bilan 2025,” CNIL, cnil.fr That enforcement pattern matters for the France frontline worker technology market because platforms used for scheduling, performance monitoring, or task assignment increasingly require robust audit trails and clear governance rules. The August 2026 implementation stage for core EU AI Act obligations has also raised the importance of human oversight, traceability, and worker transparency in AI-supported workforce tools. This is shifting vendor competition toward products that can show GDPR-ready data handling, reliable logs, and transparent decision support without slowing operations. In this setting, compliance readiness is becoming part of everyday product value rather than a separate legal concern.

Workforce Shortages Increasing Dependence On Productivity Software

Persistent hiring difficulties are pushing employers to seek productivity gains that do not depend on immediate labor expansion. The OECD stated that labor market tightness in France remained 22% above pre-COVID levels in 2025, which indicates that staffing pressure has eased less than many employers expected.[3]Organisation for Economic Co-operation and Development, “OECD Employment Outlook 2025, France,” OECD, oecd.org In the France frontline worker technology market, this has strengthened demand for software that can reduce planning friction, improve supervisor reach, and speed up onboarding for new hires. The goal is not simply labor replacement, because many operating teams still need people on site, but better output per shift and better coordination across locations. France Num reported that AI adoption among French TPEs and PMEs reached 26% in 2025, after doubling in one year, suggesting that smaller employers are becoming more willing to adopt practical digital tools amid persistent labor constraints.[4]Ministère de l'Économie / France Num, “Baromètre France Num 2025, Le Numérique Et L'Intelligence Artificielle Dans Les TPE Et PME,” France Num, francenum.gouv.fr As that willingness grows, the France frontline worker technology market should see broader adoption among employers that once viewed frontline software as optional.

Faster Adoption Of AI-Assisted Remote Support And Guided Work Instructions

AI-assisted support is gaining ground because the cost of waiting for help on the shop floor or in a warehouse is immediate and visible. Rockwell Automation reported that 50% of French manufacturers had already invested in AI and machine learning, and adoption of generative and causal AI also reached 50% in 2026. That matters for the France frontline worker technology market because guided instructions, remote support, and contextual knowledge prompts help teams act faster without needing long escalation loops. Honeywell's January 2026 launch of Performance+ for Guided Work also reflects a clear product response to this need, with software designed to reduce operator errors and accelerate onboarding in supply chain operations.[5]Honeywell International, “Honeywell Launches New Performance+ for Guided Work to Enable Faster, Smarter Supply Chain Operations,” Honeywell, honeywell.com AI-guided workflows also shorten the time it takes for newer staff to reach acceptable performance, which is important in sectors with turnover and uneven digital familiarity. As more vendors package these features into deployable tools, the France frontline worker technology market is likely to move further from communication-only use cases toward guided execution and performance support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy ERP, MES, and HR Systems | -2.5% | National, with highest friction among industrial SMEs in Hauts-de-France and Grand Est that run aging ERP environments | Medium term (2-4 years) |

| Data Privacy and Employee Monitoring Concerns | -2.2% | National, with compliance factors shaped by CNIL enforcement and EU AI Act obligations from August 2026 | Short term (≤ 2 years) |

| Low Change Readiness Among Supervisors and Frontline Users | -1.6% | National, with structural difficulty in sectors with older demographic frontline workforces such as manufacturing and construction | Medium term (2-4 years) |

| Uneven ROI Visibility for Smaller Deployments | -1.2% | National, with impact concentrated among TPEs and early-stage SME adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy ERP, MES, And HR Systems

Integration remains one of the most durable barriers because frontline platforms rarely operate in isolation within large organizations. Many French employers still run layered ERP, MES, HR, and device environments that were not built to exchange real-time workforce data in a simple way. That creates delays during implementation, increases reliance on specialist support, and limits the pace at which pilot programs can expand into company-wide rollouts. The issue is especially relevant in the France frontline worker technology market because buyers increasingly want communication, task, scheduling, and analytics tools to work within the same operating flow. When data fields, permissions, and process logic do not align across systems, the promised gains from frontline software take longer to appear. Vendors that offer stronger connectors, low-code configuration, and cleaner migration support should gain an advantage, but integration friction will continue to slow parts of the France frontline worker technology market through the medium term.

Data Privacy And Employee Monitoring Concerns

The privacy issue is more than a legal footnote because many frontline tools can capture location, activity, attendance, and performance data at high frequency. The CNIL's 2025 enforcement record showed EUR 486,839,500 (USD 525.8 million) in cumulative fines and included sanctions against 16 organizations for non-compliant employee surveillance practices. That record makes employers more cautious when evaluating features linked to tracking, monitoring, and AI-supported workforce decisions in the France frontline worker technology market. The effect is longer vendor reviews, tougher contract terms, and higher demand for clear role-based access, retention controls, and explainable workflows. Smaller vendors can feel this pressure more strongly because they must satisfy the same buyer expectations without the same compliance resources. As a result, privacy concerns are likely to remain a practical adoption brake, even as overall demand in the France frontline worker technology market continues to grow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Software Keeps the Lead

Software accounted for 68.74% of revenue in 2025, indicating that platform spending remains the main revenue base in this category. The France frontline worker technology market share for software remained the largest because buyers favored scalable applications that can be rolled out across sites without major hardware changes. French employers have shown greater interest in modular tools that combine communication, task assignment, scheduling, and reporting within a single operating layer. That pattern meets the needs of large, distributed workforces because managers want faster deployment and a lower administrative burden once the system is live. In the France frontline worker technology market, software demand is strongest where operating teams need repeatable processes rather than one-off digital projects.

Software leadership also reflects a broader buyer preference for platforms that can support multiple frontline use cases over time instead of isolated point tools. Once a communication or scheduling product is in place, employers often look to extend the same system into learning, compliance, or analytics workflows. That platform logic matters because replacement cycles can be slow, and buyers prefer vendors that can widen scope without major retraining. Rockwell Automation's 2026 findings on ROI also support this shift toward practical deployment models, especially where cloud environments improve speed and usability for frontline teams. As a result, software remains the main anchor of the France frontline worker technology market even while competition within the segment grows.

Services held the smaller share, but they are projected to grow at a 26.91% CAGR from 2026 to 2031. That pace shows that implementation, customization, training, and support are becoming more important as deployments grow in scope and become more operationally critical. The France frontline worker technology industry is not only selling licenses, it is also selling the ability to make those tools work inside complex operating environments. Service demand rises when buyers need change management, workflow design, connector support, or compliance setup that internal teams cannot manage alone. In the France frontline worker technology market, these needs are becoming more visible as employers move beyond pilot programs and seek repeatable outcomes across larger workforces.

By Deployment: Cloud-Based Models Keep Gaining Ground While On-Premises Stays Relevant In Select Cases

Cloud-based deployment accounted for 61.58% of revenue in 2025 and was the fastest-growing deployment type, with a 27.84% CAGR from 2026 to 2031. That combination indicates that the leading model is still expanding rapidly rather than entering maturity. Cloud tools fit the France frontline worker technology market because they simplify updates, support mobile access, and reduce the need for heavy local infrastructure across many operating sites. They also help vendors launch new features faster, which matters when buyers want to add analytics, guided workflows, or compliance controls without long upgrade cycles. In the France frontline worker technology market, the cloud case is strongest where deployment speed and ease of maintenance matter more than deep local hosting control.

Rockwell Automation reported that cloud platforms delivered the highest reported ROI among French manufacturers in 2026, and recognition of that benefit doubled year over year to 32%. That finding supports the commercial logic behind current deployment choices because frontline buyers increasingly need tangible operating gains rather than broad digital ambition. Cloud systems also help companies standardize user access and workflow delivery across factories, warehouses, stores, and care sites with less local IT intervention. The France frontline worker technology market is therefore seeing cloud adoption supported by both financial and operational arguments. As long as buyers continue to prioritize shorter rollouts and faster iteration, the cloud should keep its lead within the French frontline worker technology market.

Hybrid deployment holds a clear role for organizations that want cloud flexibility but cannot fully step away from existing internal systems. This model suits large manufacturers, healthcare networks, and regulated environments where some data or process layers must remain tied to internal infrastructure. Hybrid choices also reflect reality, because few large frontline employers can replace older systems all at once without disrupting operations. The France frontline worker technology market benefits from this middle path because it lets buyers move gradually while preserving continuity for sensitive workflows. Hybrid systems can therefore act as a bridge between old architecture and newer mobile-first workforce tools.

By Organization Size: Large Enterprises Lead Spending While SMEs Move Into Faster Adoption

Large enterprises accounted for 69.82% of revenue in 2025, reflecting their larger workforce and stronger software procurement capacity. These companies were often the first to fund broader frontline programs because they manage complex operations across many sites and have more resources for implementation. In the France frontline worker technology market, large employers in automotive, logistics, retail, and other distributed sectors have set the early pace for communication, compliance, and scheduling deployments. Their size also makes the payback case easier to validate because small efficiency gains can translate into meaningful operating impact across thousands of workers. As a result, large enterprises remain the spending anchor for the France frontline worker technology market.

Their leadership is also tied to system readiness, as larger companies typically have formal digital teams, multi-year vendor relationships, and defined rollout processes. Global suite providers can use those relationships to expand into frontline use cases with lower switching friction than smaller vendors often face. Even when specialist platforms win, large enterprises still tend to demand more configuration, stronger controls, and tighter integration. That makes the large-enterprise segment important for both revenue and product development in the France frontline worker technology market. In practice, many vendor roadmaps are shaped by the needs of these early, high-value accounts.

Small and medium enterprises are projected to grow at a 27.46% CAGR from 2026 to 2031, which makes them the fastest-growing organizational segment. This shift matters because it broadens the France frontline worker technology market beyond the early base of large enterprise buyers. SMEs are increasingly interested in modular cloud tools that do not require large IT teams or complex project structures to get started. France Num reported that AI usage among French TPEs and PMEs doubled in one year, to 26% in 2025, indicating faster digital adoption in smaller business settings.[6]Ministère de l'Économie / France Num, “Baromètre France Num 2025, Le Numérique Et L'Intelligence Artificielle Dans Les TPE Et PME,” France Num, francenum.gouv.fr That wider openness expands the addressable pool for frontline platforms focused on practical day-to-day operations.

By Application: Communication Leads Current Spending While Analytics Gains Strategic Weight

Employee communication and engagement accounted for 24.63% of revenue in 2025, making it the largest application segment. That position is logical because many organizations begin their frontline digital efforts by trying to close communication gaps between management teams and site-level workers. In Rockwell Automation's 2026 survey, 36% of French manufacturers said communication challenges were a leading obstacle to digital progress. In the French frontline worker technology market, communication tools often serve as the first entry point because they are visible, easy to explain, and immediately relevant across many sectors. They also create a base layer that vendors can later extend into tasking, learning, and analytics.

Communication products solve more than messaging because they also help distribute updates, standardize shift information, and reduce the lag between management intent and frontline action. That is especially important in operations where service quality depends on consistency across sites, shifts, and worker groups. The France frontline worker technology market continues to reward applications that improve routine coordination before moving into deeper operational control. Once employees are active on one platform, vendors gain a stronger chance to cross-sell adjacent functions. For many buyers, communication remains the easiest way to justify initial adoption in the France frontline worker technology market.

Workforce analytics and performance management is the fastest-growing application segment, with a projected 29.18% CAGR from 2026 to 2031. This reflects a more mature stage of buyer thinking, as employers want measurable proof that frontline software improves labor efficiency, process adherence, and operational consistency. The France frontline worker technology market for workforce analytics and performance management is projected to expand at a 29.18% CAGR through 2031, signaling stronger interest in quantifiable workforce outcomes. Safety and compliance management is also gaining importance as buyers seek greater auditability and clearer controls over workforce processes and data use. The CNIL's enforcement record has reinforced that governance cannot be separated from frontline software design in France. Together, these shifts suggest that the French frontline worker technology market is moving toward broader platforms that integrate communication, execution, analytics, and control within a single operating environment.

By End-User Industry: Manufacturing Provides The Largest Base While Healthcare And Life Sciences Expands Fastest

Industrial manufacturing accounted for 20.46% of end-user revenue in 2025, which made it the largest industry segment. Manufacturing fits the France frontline worker technology market because it combines large frontline workforces with time-sensitive operating tasks, strict process discipline, and measurable costs from breakdowns in coordination. Shift planning, safety compliance, quality traceability, and machine-side knowledge delivery all matter more when output depends on synchronized activity across people and equipment. The sector also contains many sites where older work routines must now coexist with newer digital workflows. That makes manufacturing a natural anchor for the France frontline worker technology market.

Rockwell Automation found that 85% of French manufacturers viewed digital transformation as a necessity in 2026, which supports the sector's role as the leading deployment base for frontline software. Manufacturing demand also tends to favor repeatable workflows, guided execution, and real-time visibility because these functions can affect both throughput and quality simultaneously. In the French frontline worker technology market, that combination gives vendors a clearer path to measurable value than in many less-structured service settings. The large installed base in factories, warehouses, and adjacent industrial operations should keep manufacturing at the center of vendor strategy. Even so, growth is now spreading more visibly into other sectors with similar coordination pressure.

Retail and e-commerce, transportation and logistics, and hospitality are important secondary verticals because they also manage large, distributed teams, high turnover, and significant variation across sites. Construction, government, and public administration are earlier in adoption, but they are becoming more relevant as vendors offer simpler mobile templates and stronger compliance support. These verticals broaden the breadth of the France frontline worker technology market by expanding demand beyond the traditional manufacturing core. Each segment values somewhat different features, but all share a need for clearer frontline coordination and faster operating response. That common need helps platform vendors widen their addressable use cases across sectors.

Geography Analysis

The France frontline worker technology market was most concentrated in Ile-de-France in 2026 because the region houses many of the country's largest enterprise headquarters and software budget owners. Procurement decisions for multi-site frontline programs are often made there first, even when the workers who use those systems are based elsewhere. This gives Ile-de-France an outsized role in setting deployment priorities, vendor selection, and rollout sequence across national operations. The France frontline worker technology market then spreads outward as approved platforms are rolled out to factories, warehouses, stores, and care settings in other regions. Regional growth is becoming more visible in Auvergne-Rhône-Alpes, Grand Est, and Hauts-de-France, where industrial operations are moving from pilot projects to more structured implementation. Rockwell Automation reported that 85% of French manufacturers viewed digital transformation as a necessity in 2026, which supports the broader shift from experimentation to rollout across industrial regions.

Healthcare follows a different regional pattern because purchasing is increasingly shaped by grouped networks rather than single facilities. Regional hospital groups are taking on a more centralized role in technology decisions, creating cluster-level demand in major metropolitan and peri-urban areas. Adoption is national in direction, but depth still varies between advanced university centers and smaller district facilities. Lyon, Marseille, Bordeaux, and Toulouse stand out as locations where larger care providers are more active in digital frontline deployment than smaller hospitals with tighter internal constraints.

The France frontline worker technology market share of demand still leans toward large-enterprise corridors, but the next layer of expansion is reaching regions with dense industrial and public-service activity. Large employers are still ahead because they have the scale, funding, and implementation structure needed for multi-site deployment. France Num's 2025 results, which showed AI usage among TPEs and PMEs rising to 26%, suggest that regional adoption outside the biggest corporate centers can strengthen as practical digital use becomes more accepted. Over the forecast period, geography in the France frontline worker technology market should reflect a widening rollout pattern, with headquarters-led buying gradually translating into broader regional operating use.

Competitive Landscape

The France frontline worker technology market is moderately fragmented, with a clear split between global enterprise software providers and specialist frontline platforms. Microsoft, SAP, Oracle, and Salesforce remain important in large accounts because they can extend from existing enterprise relationships into frontline use cases with lower switching friction. Specialist vendors such as YOOBIC, Staffbase, WorkJam, Connecteam, Axonify, and Legion compete by offering mobile-first design, stronger workflow focus, and more targeted frontline functionality. This structure keeps competition active because buyers often choose between broad-suit integration and faster, more focused frontline deployment. In the France frontline worker technology market, no single vendor approach fits every operating environment, which helps sustain room for both global and specialist players.

Hardware-linked vendors are also expanding their role beyond devices and into workflow and productivity software. Zebra Technologies introduced its Machine Vision Ecosystem at Automate 2026 in June 2026, which expanded its manufacturing workflow digitization portfolio with AI-powered fixed industrial scanning and vision solutions. Honeywell launched Performance+ for Guided Work in January 2026, showing a similar push toward software that supports frontline execution in supply chain and logistics settings. These moves matter because they show how vendors with established hardware or infrastructure positions are trying to capture more workflow value inside the France frontline worker technology market.

Partnerships and product expansion are also shaping competition among software specialists. Legion Technologies released more than 90 AI workforce management innovations in January 2026 and then announced a partnership with Wolt in February 2026 to deploy its workforce suite across 20 countries in EMEA. Staffbase and Cornerstone OnDemand announced a partnership in October 2025 to bring learning content and AI-powered recommendations into the Staffbase Employee App for frontline workers. The France frontline worker technology market still has open space in multilingual communication, sector-specific workflow design, and low-friction deployment models for mid-sized employers. Vendors that combine simple adoption with stronger compliance controls are likely to improve their position as the France frontline worker technology market becomes more operationally demanding.

France Frontline Worker Technology Industry Leaders

Microsoft Corporation

TeamViewer SE

SAP SE

LumApps

WorkJam, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies unveiled its Machine Vision Ecosystem at Automate 2026 (June 22, 2026), expanding its portfolio of manufacturing workflow digitization. The launch introduced AI-powered fixed industrial scanning and vision solutions targeted at production-line quality management, deepening Zebra's capability stack for industrial frontline environments.

- June 2026: Zebra Technologies launched Zebra Nucleus and Workcloud IO and Workcloud BI at its annual ZONE 2026 customer conference (June 2-4, 2026) in Nashville. The new AI-driven software solutions enable IT leaders to convert real-time frontline device data into operational insights, extending Zebra's strategy of building a connected frontline software platform above its hardware install base.

- February 2026: Legion Technologies announced a strategic partnership with Wolt (February 4, 2026) to deploy its full workforce management suite across 20 countries in EMEA, including AI-driven demand forecasting, automated scheduling, and labor optimization. The deployment is expected to be fully operational by the end of 2026 and represents a significant EMEA geographic expansion for Legion.

- January 2026: Honeywell International launched Performance+ for Guided Work, a new software offering for frontline workers in supply chain and logistics operations. The solution provides AI-assisted, step-by-step guided work instructions designed to reduce operator errors and accelerate the onboarding of new frontline workers at high-velocity distribution sites.

France Frontline Worker Technology Market Report Scope

The France Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, and More), and End-User Industry (Retail and E-Commerce, Industrial Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the size of the France frontline worker technology market in 2026?

The France frontline worker technology market stood at USD 0.65 billion in 2026 and is forecast to reach USD 1.94 billion by 2031 at a 24.63% CAGR.

What is driving adoption across French frontline operations?

Adoption is being supported by labor tightness, stronger demand for real-time task coordination, and higher interest in cloud and AI-assisted workflow tools.

Which deployment model is leading growth in France?

Cloud-based deployment led with 61.58% revenue share in 2025 and is projected to grow at a 27.84% CAGR through 2031.

Which buyer group is creating the largest revenue base?

Large enterprises accounted for 69.82% of revenue in 2025 because they can support wider multi-site rollouts and more complex implementations.

Which application area currently leads spending?

Employee communication and engagement led with 24.63% of revenue in 2025, reflecting the need to close communication gaps across distributed frontline teams.

Why is healthcare and life sciences drawing attention through 2031?

Healthcare and life sciences is projected to grow at a 28.73% CAGR as providers look for better communication, task support, and workflow efficiency in care settings.

Page last updated on: