France Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

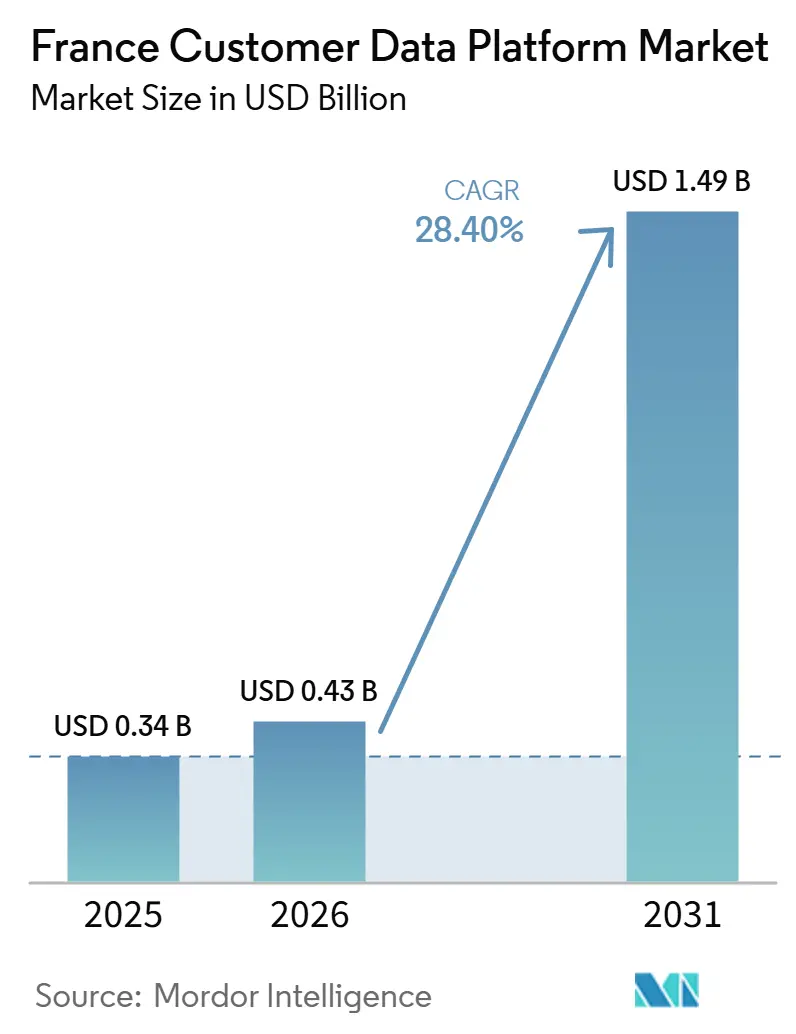

| Base Year Market Size (2025) | USD 0.34 Billion |

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 28.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Customer Data Platform Market Analysis by Mordor Intelligence

The France customer data platform market size is expected to increase from USD 0.34 billion in 2025 to USD 0.43 billion in 2026 and reach USD 1.49 billion by 2031, growing at a CAGR of 28.40% over 2026-2031. This pace keeps the France customer data platform market among the faster-growing enterprise software categories in Western Europe, as consent enforcement and the removal of third-party cookies keep first-party data investment high. The France customer data platform market is also being shaped by France's mix of luxury groups, national retailers, banks, insurers, and healthcare organizations, because all of them need tighter control over identity, consent, and activation. Data sovereignty is moving from a technical preference to a procurement condition, which is pushing vendors to support hybrid and sovereign cloud designs for regulated workloads. Growth is also moving beyond basic data unification, because buyers are adding analytics, AI-enabled segmentation, and managed services once core customer records are in place. Competition remains strongest at the enterprise end, but the France customer data platform market still faces compliance risk, integration friction, and legal review cycles that can slow deployments even when demand remains strong.

Key Report Takeaways

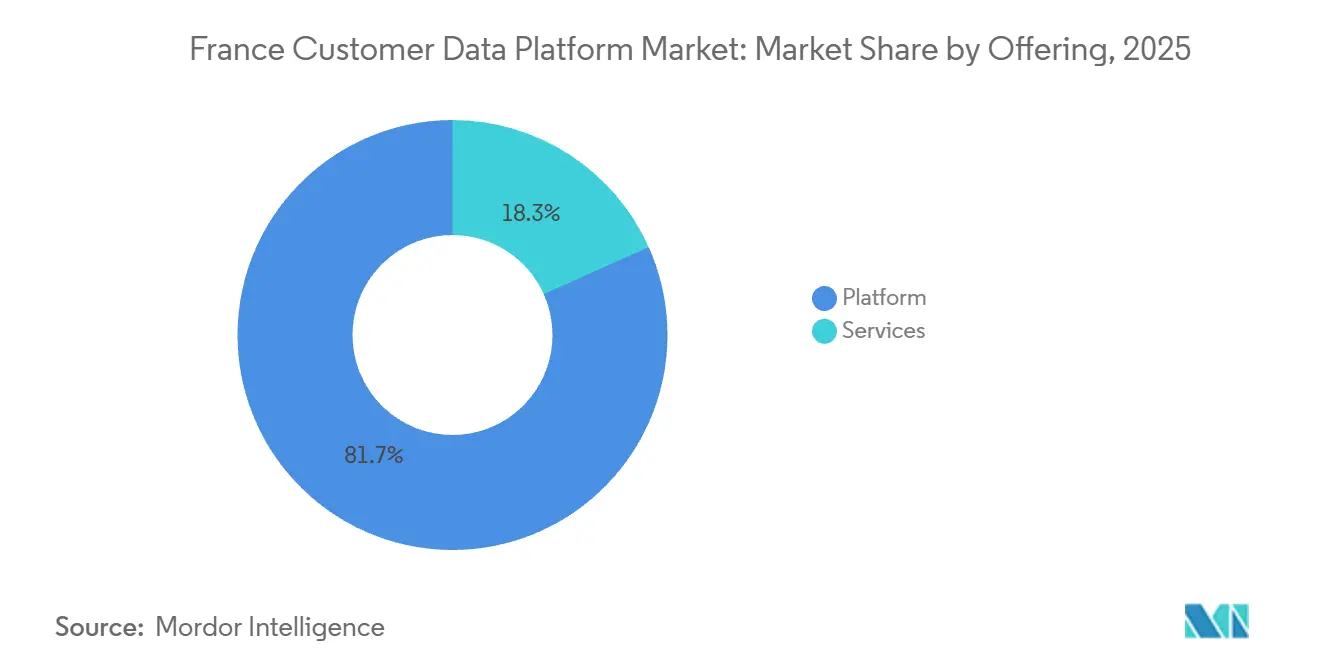

- By offering, platform held 81.70% of the France customer data platform market in 2025, while services is projected to grow at 30.84% CAGR through 2031.

- By deployment mode, cloud accounted for 67.26% share in 2025, while hybrid is projected to expand at 31.42% CAGR through 2031.

- By organization size, large enterprises held 69.68% of the France customer data platform market share in 2025, while SMEs are projected to record the fastest CAGR of 30.18% through 2031.

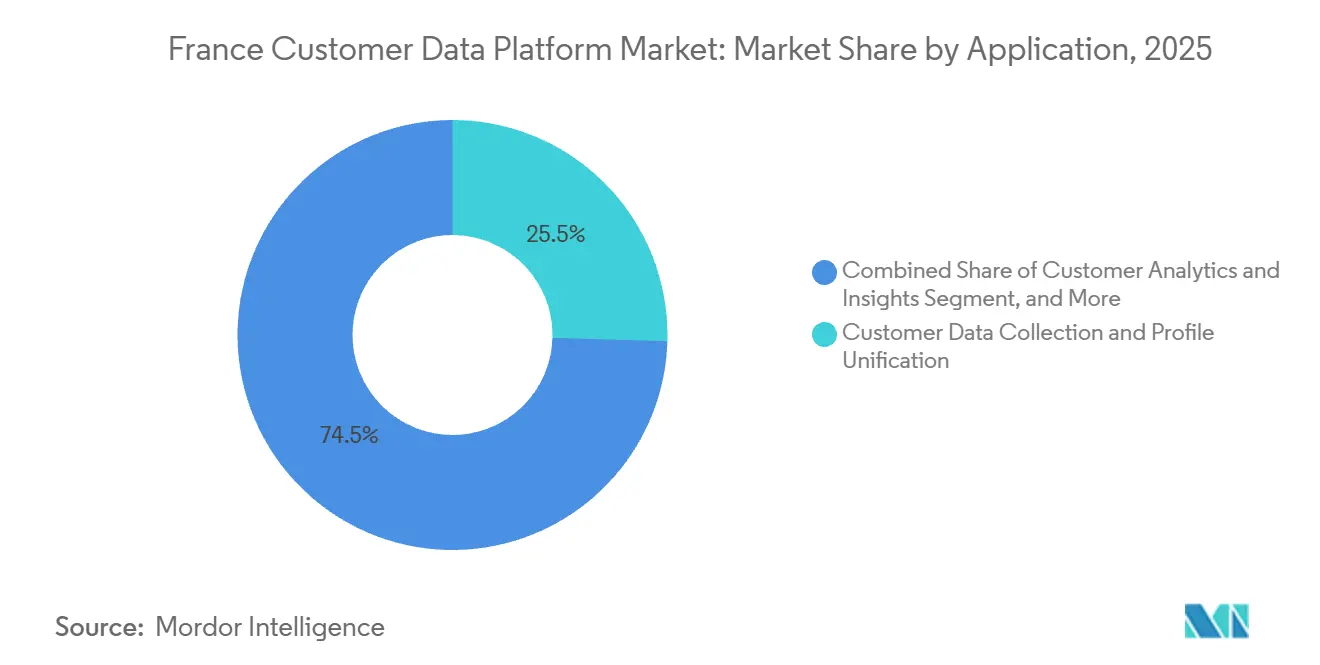

- By application, customer data collection and profile unification accounted for 25.46% share in 2025, while customer analytics and insights is projected to expand at 32.86% CAGR through 2031.

- By end-user industry, BFSI held 24.60% share in 2025, while healthcare and life sciences is projected to grow at 33.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising First-Party Data Activation Under Consent-Driven Marketing | +5.2% | National, with concentrated early gains in Ile-de-France, Lyon, and Bordeaux enterprise corridors | Short term (≤ 2 years) |

| Growing Demand for Real-Time Customer Profile Unification | +4.7% | Global, concentrated in France's retail, BFSI, and luxury sectors | Short term (≤ 2 years) |

| Shift Toward Cloud-Native CDP Deployment | +4.1% | National, with spill-over to EU sovereign cloud hubs | Medium term (2-4 years) |

| Need for Cross-Channel Personalization in Retail and Luxury Commerce | +3.6% | National, concentrated in Paris and major retail and luxury corridors | Short term (≤ 2 years) |

| Increasing Adoption of Identity Resolution for Omnichannel Journeys | +3.0% | Global, with material early adoption in France's media, telecom, and retail sectors | Medium term (2-4 years) |

| Rising Use of CDPs for AI-Enabled Segmentation | +2.8% | Global, with France-specific acceleration from EU AI Act compliance tooling | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Activation Under Consent-Driven Marketing

France is turning consent enforcement into a direct buying trigger for customer data platforms, because organizations need systems that can document permission, store clean first-party data, and control downstream activation. CNIL's strict approach to valid consent means a CDP is not just a marketing tool in France, it is also part of the compliance stack that supports lawful data collection and reuse. In December 2025, the CNIL imposed a EUR 3.5 million (USD 3.815 million) fine on a loyalty program operator for transmitting personal data from more than 10.5 million members to a social network for ad targeting without valid consent, and the case was coordinated with 16 other European supervisory authorities. That decision raised the cost of weak consent governance, so French enterprises are moving faster on architectures that can connect consent capture, profile creation, and activation controls in one operating model. In practice, the France customer data platform market is benefiting because compliance-led buying tends to involve broader stakeholder groups, including marketing, legal, privacy, and IT teams, which often expands contract scope. This is why first-party activation in France is producing durable demand, since the platform has to serve governance needs before it serves personalization needs.

Growing Demand for Real-Time Customer Profile Unification

Large organizations in France still manage customer information across CRM systems, data warehouses, consent tools, service platforms, and channel-specific stores, which leaves them with inconsistent versions of identity and fragmented decisioning. That fragmentation is pushing buyers toward real-time unification, because batch updates are often too slow for live personalization, service workflows, and compliance reporting. AXA France treated a CDP as part of the core Nadia Data and AI transformation program, which shows that profile unification is being positioned as enterprise infrastructure rather than as a narrow campaign tool. Twilio reported a 57% year-over-year increase in predictive trait usage across its platform in 2025, which supports the pattern that buyers who start with unification often move quickly into analytics and AI-based activation.[1]Twilio, “2025 Customer Data Platform Report,” Twilio, twilio.com This progression matters for the France customer data platform market because the commercial value of a unified profile rises when it becomes the input for sales, service, and marketing decisions at the same time. It also explains why vendors with stronger connectors, faster event handling, and deeper implementation support are gaining attention as French deployments move from basic integration to real-time orchestration.

Shift Toward Cloud-Native CDP Deployment

Cloud-native deployment remains central to new CDP buying, but France is not moving toward a simple public cloud model for every workload, because sensitive data still needs tighter jurisdictional control. The strongest signal comes from hybrid growth, which is outpacing the core cloud segment as buyers combine cloud-native tools with local hosting rules for regulated and high-risk data. SAP launched its sovereign cloud in France in March 2026 through a partnership with Bleu, which gave organizations a path to run critical workloads under a France-specific sovereignty structure tied to SecNumCloud expectations. SAP then expanded that position with an investment of up to EUR 300 million (USD 333 million) in France, while Salesforce announced a USD 2 billion investment through 2030 that included encryption key control through Thales and Eviden and local LLM integration through Mistral AI. These moves show that major vendors now see sovereign extension paths as necessary for winning regulated French accounts, not as optional product packaging. As a result, the France customer data platform market is shifting toward hybrid sovereign designs that can preserve local control without giving up cloud-based speed and scalability.

Need For Cross-Channel Personalization In Retail And Luxury Commerce

France's large luxury and retail base creates a distinct demand pattern for CDPs, because these companies need consistent customer recognition across stores, e-commerce, loyalty programs, service interactions, and premium brand environments. The requirement is not only to personalize messages, but also to do so without weakening control over proprietary consumer data and brand-level governance. Google Cloud described how LVMH built a centralized AI and data platform across maisons such as Louis Vuitton, Sephora, and Dom Pérignon while keeping brand-level data firewalls intact. That model matters because it reflects the kind of architecture many French enterprises want, where group-level intelligence is possible but local business units still retain separation and control. In this environment, a CDP must support acquisition, service, retention, and measurement within a single, governed layer, underscoring the value of consent-aware identity resolution and profile management. The France customer data platform market is therefore being supported by personalization demand that is tied closely to governance expectations rather than to campaign speed alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Data Privacy Compliance Burden Under GDPR and CNIL Expectations | -3.8% | National, with regulatory influence most pronounced in BFSI, healthcare, and media sectors | Short term (≤ 2 years) |

| Integration Complexity with Legacy CRM, DWH, and Consent Tools | -3.2% | National, concentrated in mid-market and public sector organizations | Medium term (2-4 years) |

| High Total Cost of Ownership for Mid-Market Buyers | -2.4% | National, affecting large enterprises | Medium term (2-4 years) |

| Limited Internal CDP Skills Across French Mid-Sized Enterprises | -1.8% | National, with skill gaps most acute outside the Ile-de-France technology ecosystem | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Data Privacy Compliance Burden Under GDPR And CNIL Expectations

The compliance burden in France is slowing some deployments, because buyers have to test architecture choices against CNIL expectations, GDPR obligations, cross-border processing risks, and internal legal review cycles. CMS Law recorded 83 sanctions in France in 2025 with a combined value of EUR 486.8 million (USD 530.6 million), which kept enforcement pressure visible across the market.[2]CMS Law, “Data Protection Laws and GDPR Enforcement in France,” CMS Law, cms.law For large enterprises, this creates longer procurement cycles, more frequent data protection impact assessments, and tighter contractual review of how processors handle identity, segmentation, and activation. The burden is not removing demand, but it is raising the amount of work needed to turn demand into signed and deployed contracts. That is why privacy compliance acts as a restraint in the France customer data platform market even while it also supports long-term investment in governed first-party data systems.

Integration Complexity with Legacy CRM, DWH, And Consent Tools

Integration remains one of the hardest execution issues in France, because many large organizations still operate older ERP, CRM, and warehouse estates that were not built for modern API-first data movement. A CDP may look straightforward in a product demo, but real deployment often requires data model alignment, connector work, governance mapping, and process redesign across several business systems. Composable architectures help by leaving data in the customer's warehouse rather than replicating it into a separate vendor environment, which can reduce movement overhead and simplify control boundaries. Imagino's Snowflake Native App launch in October 2025 showed how local vendors are responding to this issue with zero-copy models that fit governed warehouse environments more closely. Even so, this route mainly helps organizations that already have modern cloud data foundations, while buyers on older stacks still face heavier migration and integration work. The France customer data platform market, therefore, continues to move at different speeds, with modern data estates onboarding faster and legacy environments carrying higher switching costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Dominance with Faster Services Expansion

The platform segment held 81.70% of the France customer data platform market share in 2025, which reflected the high upfront cost and enterprise-led nature of early CDP rollouts. Most large buyers started with the core system that could collect data, unify identity, and manage activation logic before expanding into deeper support layers. That pattern shows that the France customer data platform market was still led by foundational software purchases in 2025, especially where large organizations were standardizing customer records across several brands, channels, and business units. It also suggests that many contracts were written around long implementation horizons, because platform decisions often set the rules for later analytics, service, and compliance workflows. In practical terms, the platform segment benefited from being the first budget line approved when French enterprises decided to reorganize customer data operations.

Services is projected to grow at 30.84% CAGR through 2031, which makes it the faster-expanding part of this offering split. This faster rise reflects the amount of work needed after purchase, including implementation planning, data mapping, governance setup, training, and long-term optimization. GDPR Article 28 duties are also increasing service needs, because vendors and clients have to formalize processor obligations, maintain audit trails, and support structured responses to data requests across changing use cases. In the France customer data platform market, that means professional services and managed support are becoming harder to separate from the product itself, especially in regulated accounts. The France customer data platform market is therefore moving toward a model where delivery strength and local execution capacity matter almost as much as core platform features. Over time, this should narrow the revenue gap between software and services more quickly than in markets where legal and integration requirements are less demanding.

By Deployment Mode: Cloud Leadership with Hybrid Acceleration

Cloud deployment commanded 67.26% of the France customer data platform market in 2025, showing that many buyers had already accepted cloud infrastructure as the default base for customer data operations. That share reflected years of enterprise movement toward scalable hosted environments, broader API ecosystems, and faster release cycles than older on-premises models could offer. Even so, the France customer data platform market is not moving toward a fully uniform cloud structure, because regulated workloads still require more control over residency, access, and certification alignment. Hybrid deployment is projected to grow at 31.42% CAGR through 2031, which is the fastest rate among deployment modes and points to an architectural transition rather than to mature standardization. In effect, the market is using cloud for flexibility while reserving local or sovereign pathways for more sensitive processing layers.

SAP's March 2026 sovereign cloud launch with Bleu, its April 2026 deployment path on S3NS, and its June 2026 investment of up to EUR 300 million (USD 333 million) in France made hybrid sovereign deployment more commercially credible for large organizations. Salesforce took a parallel path in June 2026 with a USD 2 billion investment through 2030 that included local encryption control and local LLM integration, both of which spoke directly to French sovereignty concerns.[3]Salesforce, “Salesforce Deepens Commitment to France With USD 2 Billion Investment to Accelerate AI Transformation,” Salesforce, salesforce.com These moves matter because public administration, healthcare, defense, and critical infrastructure buyers often need proof that local control has been engineered into the deployment model. Vendors that insist on full data transfer outside French jurisdiction will therefore face more resistance as procurement becomes more compliance-led. As on-premises systems age and vendors retire older architectures, migration demand should continue to support both cloud expansion and hybrid acceleration across the France customer data platform market.

By Organization Size: Large Enterprises Hold Value While SMEs Accelerate

Large enterprises represented 69.68% of the France customer data platform market in 2025, which kept most revenue concentrated in the highest-spend customer group. These accounts usually buy multi-year platform licenses, integration services, governance support, and post-deployment optimization together, so their contract values remain well above smaller customer budgets. Large companies in BFSI, retail, and luxury have also set the tone for adoption by making CDP architecture part of broader data and AI programs rather than a stand-alone marketing purchase. When organizations such as BNP Paribas, Carrefour, LVMH, and L'Oréal advance customer data programs, adjacent buyers often treat the category as more mature and less experimental. As a result, the France customer data platform market still depends on large enterprises for revenue scale, reference value, and early proof of use cases that other buyers later follow.

SMEs are projected to grow at 30.18% CAGR through 2031, which makes them the faster-moving size cohort even though they start from a smaller base. Their expansion is being supported by lower upfront pricing, composable models, lighter implementation paths, and French-language delivery that reduces adoption friction. Imagino's June 2024 Series A raise of EUR 25 million (USD 27.25 million) and reported 70% revenue growth in 2024 showed that there is active commercial space for vendors targeting this mid-market opportunity. The company's zero-copy, Snowflake-native positioning also points to the kind of SME buyer now entering the category, which is one that wants faster deployment without giving up data control. Even in this part of the market, buyers still expect strong security credentials and GDPR-native processing terms, which limits room for underdeveloped vendors. The France customer data platform industry is therefore widening through SME participation, while most absolute revenue remains anchored in larger enterprises.

By Application: Foundational Unification Today and Analytics Growth Ahead

Customer data collection and profile unification led with 25.46% of 2025 value, which shows that many buyers were still focused on building the base layer before trying to scale advanced activation. The first task for many French organizations is still to create one governed record that can be used across channels, brands, and internal teams without creating conflicting identity views. Audience segmentation and personalization, along with campaign and journey orchestration, already account for a meaningful share of demand, which indicates that activation use cases are present but remain downstream of the unification step. This sequence gives the France customer data platform market a clear maturity curve, because adoption often starts with data assembly and only later shifts into automated decisioning and deeper intelligence. Twilio's 2025 report noted a 57% year-over-year rise in predictive trait usage, which supports the view that analytics demand tends to accelerate once the base profile layer is stable.

Customer analytics and insights is projected to grow at 32.86% CAGR through 2031, making it the fastest-growing application in the France customer data platform market. This shift suggests that buyers are moving from asking who the customer is toward asking what action should be taken next, across service, retention, and acquisition use cases. Consent and preference management is also becoming a more visible application area, because French enterprises need a stronger record of how permissions were captured, stored, and applied to each form of activation. In healthcare, the May 2026 CNIL action against IQVIA Operations France showed that governance rules for sensitive data platforms can directly affect how engagement, profiling, and data access models are built. Industrial manufacturing and government administration are also beginning to treat first-party data as a managed strategic asset rather than as a byproduct of separate operational systems. The France customer data platform industry is therefore moving from basic profile creation toward analytics, governed activation, and more specialized use cases shaped by sector rules.

By End-User Industry: BFSI Leads While Healthcare Expands Fastest

BFSI contributed 24.60% of the France customer data platform market in 2025, which made it the largest end-user industry by value. This lead reflects the sector's early need for unified customer data architectures that can support marketing, service, compliance, and customer interaction documentation in parallel. Financial institutions usually bring higher contract values and longer account duration, but they also require more review around governance, certification, and change management. BNP Paribas Personal Finance has publicly highlighted AI use in customer engagement, which fits the wider pattern of regulated financial players moving from controlled data consolidation into more advanced personalization and intelligence workflows. For that reason, BFSI remains a key revenue anchor for the France customer data platform market even as other verticals increase their adoption pace.

Healthcare and life sciences is projected to grow at 33.42% CAGR through 2031, which makes it the fastest-growing vertical in the France customer data platform market. The segment is starting from a smaller base, but adoption is rising as healthcare and life sciences organizations seek structured ways to manage sensitive engagement data under tighter oversight. The CNIL's May 2026 EUR 5 million (USD 5.55 million) fine against IQVIA Operations France raised the visibility of lawful design requirements for health data warehouse activity and reinforced the need for stronger control models. Retail and e-commerce, IT and telecom, media and entertainment, industrial manufacturing, and government and public administration account for the rest of the demand, with several of these sectors building around first-party data and cross-channel engagement needs. Media and retail remain especially relevant where audience monetization and omnichannel recognition matter, while the public sector and manufacturing are emerging from a much smaller starting point. The France customer data platform market will keep drawing vertical momentum from sectors where customer intelligence needs and compliance obligations are rising together.

Geography Analysis

France is treated as a single geographic unit in this market, and the France customer data platform market stood at USD 0.43 billion in 2026 after reaching USD 0.34 billion in 2025. Commercial activity is concentrated in Ile-de-France because the region hosts many CAC 40 headquarters and the French operations of major global software providers. That concentration gives Paris a central role in procurement, partner ecosystems, implementation planning, and early reference deployments. At the same time, the national environment is what really defines buying behavior, because all participants operate under one of Europe's more demanding data governance frameworks.

This means geography in the France customer data platform market is less about province-by-province demand shares and more about the legal and infrastructure context attached to each deployment. French buyers are placing more weight on consent governance, local hosting options, auditability, and contractual clarity when they evaluate vendors. SAP's sovereign cloud actions in 2026 and Salesforce's France investment both showed that local infrastructure alignment has become a strategic requirement rather than a secondary differentiator. As a result, the France customer data platform market is rewarding vendors that can align cloud speed with French-jurisdiction control over sensitive workloads.

Beyond compliance, France's luxury, retail, media, and financial sectors are giving the market a distinctive use case structure. Google Cloud's description of LVMH's centralized AI and data platform showed how French enterprises want group-level intelligence while still preserving brand-level separation and control. BNP Paribas Personal Finance also showed that AI-led customer engagement is moving deeper into regulated financial services environments where data control is already strict. These sector examples help explain why the France customer data platform market is growing at 28.40%, because demand is being pulled by both compliance work and advanced activation plans. The market remains national in reporting scope, but the growth logic is concentrated in industry mix, sovereignty requirements, and the types of enterprises that dominate French customer data spending.

Competitive Landscape

The France customer data platform market is moderately concentrated at the enterprise tier, where Adobe Real-Time CDP and Salesforce Data Cloud are competing for many large and complex accounts. That concentration becomes much weaker below the top tier, where Twilio Segment, Tealium, Oracle Unity, Treasure Data, BlueConic, and French-native specialists compete across narrower use cases and mid-market budgets. The result is a two-level structure, with practical duopoly conditions at the top and active fragmentation across the broader field. Salesforce strengthened its position in June 2026 with a USD 2 billion commitment to France through 2030, including local encryption control through Thales and Eviden and local LLM integration with Mistral AI. That move mattered because it addressed one of the most important buying issues in the France customer data platform market, which is the need to match product capability with sovereignty and compliance expectations.

SAP advanced along a similar line through its sovereign cloud launch with Bleu, its deployment path on S3NS, and its broader France investment plan, all of which improved its case for regulated-sector deployments. Imagino has taken a more targeted position with its Snowflake Native App and zero-copy deployment model, which speaks directly to buyers that want governed warehouse control and faster implementation. Databricks added more pressure in 2026 by launching CustomerLake, showing that data platform vendors are moving directly into CDP territory with embedded identity resolution and AI capabilities.[4]Databricks, “Introducing CustomerLake: The Agentic CDP Embedded in Databricks,” Databricks Blog, databricks.com These moves show that competition is increasingly centered on architecture, sovereignty, and embedded intelligence rather than on profile storage alone.

The next shift is the move from batch-oriented platforms toward systems that support real-time context and agent-driven orchestration. Twilio's 2025 report pointed to this direction through a sharp rise in predictive trait usage, which suggests that unified profiles are now being expected to support live decisioning and not only historical segmentation. Tealium's Context API launch in June 2026, its AI at the Edge and AI Decisioning release in May 2026, and its AI Partner Ecosystem announcement in April 2026 all reflected that push toward faster AI-ready customer context. BlueConic's April 2026 Growth Plays and AI Canvas release, followed by its June 2026 acquisition of Blueshift, showed a similar effort to combine first-party data control with faster automated actioning. For French buyers, however, new AI features still need to fit within strict governance boundaries, so vendors that can combine local trust, integration depth, and real-time activation should remain in the strongest position across the France customer data platform market.

France Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Twilio Inc.

Tealium, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Salesforce announced a USD 2 billion investment in France through 2030 at the Choose France summit, including the opening of a new AI Innovation Hub in Paris. The investment includes data sovereignty infrastructure enabling encryption via Thales and Eviden and local LLM integration with Mistral AI, directly addressing CNIL and ANSSI requirements.

- June 2026: SAP announced a long-term investment of up to EUR 300 million (USD 333 million) in France to expand sovereign cloud and Business AI capabilities at the Choose France summit. SAP is targeting a new SecNumCloud-qualified sovereign cloud region with 3 data center sites in Paris, opening in Q1 2027.

- June 2026: BlueConic acquired Blueshift, an AI-powered cross-channel marketing platform, combining BlueConic's first-party CDP capabilities with Blueshift's AI decisioning engine and closed-loop learning system. The acquisition positions BlueConic as a full-stack agentic CDP vendor competing directly with Salesforce's Agentforce Marketing Cloud and Adobe's CX Enterprise.

- April 2026: BlueConic launched Growth Plays and AI Canvas, providing marketing teams with an agentic system that acts on customer data across all channels simultaneously, closing the loop from customer signal to revenue without manual assembly.

France Customer Data Platform Market Report Scope

The France Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The France Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the France customer data platform market size and growth outlook?

The France customer data platform market was valued at USD 0.34 billion in 2025, stands at USD 0.43 billion in 2026, and is projected to reach USD 1.49 billion by 2031 at a 28.40% CAGR.

What is driving customer data platform adoption in France?

The main drivers are stronger first-party data activation needs, tighter consent enforcement, real-time profile unification demand, and growing interest in sovereign and hybrid deployment models.

Which deployment model is expanding fastest in France?

Hybrid deployment is projected to grow the fastest at 31.42% CAGR through 2031, as buyers balance cloud agility with French-jurisdiction data control.

Which company size group is creating the most revenue and which is growing fastest?

Large enterprises accounted for 69.68% of 2025 value, while SMEs are projected to post the fastest growth at 30.18% CAGR through 2031.

Why is healthcare becoming an important growth area for CDPs in France?

Healthcare and life sciences is projected to grow at 33.42% CAGR, supported by rising demand for compliant patient and engagement data architectures under stricter regulatory scrutiny.

How are vendors competing in the French CDP space?

Competition is increasingly based on sovereignty features, local implementation strength, zero-copy or warehouse-native architecture, and real-time AI-ready activation rather than profile storage alone.

Page last updated on: