France CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

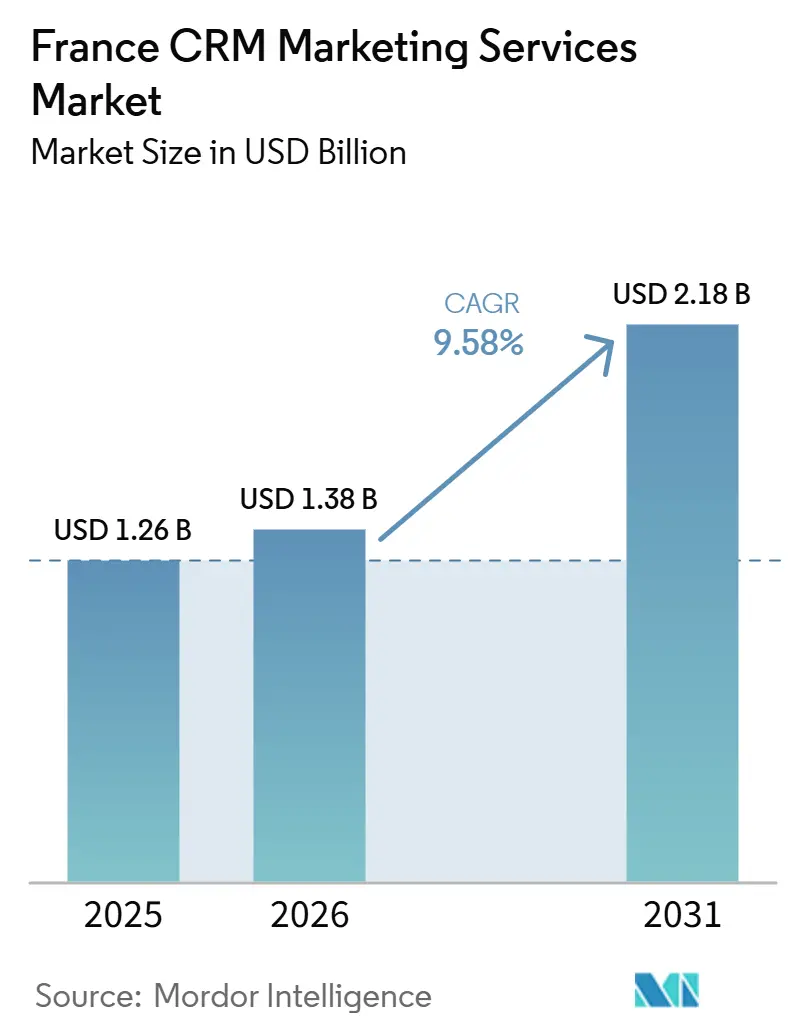

| Base Year Market Size (2025) | USD 1.26 Billion |

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 9.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France CRM Marketing Services Market Analysis by Mordor Intelligence

The France CRM marketing services market size is expected to increase from USD 1.26 billion in 2025 to USD 1.38 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 9.58% over 2026-2031. Demand is rising because more French enterprises now treat customer data as a core operating asset rather than a support function, and that shift is widening the need for CRM strategy, implementation, analytics, and governance services. AI-led campaign execution is also moving CRM work from one-time deployment into continuous tuning, data unification, and platform oversight, which gives the France CRM marketing services market a steadier revenue base. Consent management, data security, and European hosting priorities are extending service scopes into privacy design and ongoing compliance support, especially in regulated client environments. Mid-sized specialists with local delivery depth remain well placed because many buyers want certified expertise, faster rollout cycles, and GDPR-aware execution without the cost structure of the largest global integrators. Competitive pressure remains high, yet the combination of AI-enabled customer engagement, first-party data architecture, and managed service demand continues to support expansion across the France CRM marketing services market.

Key Report Takeaways

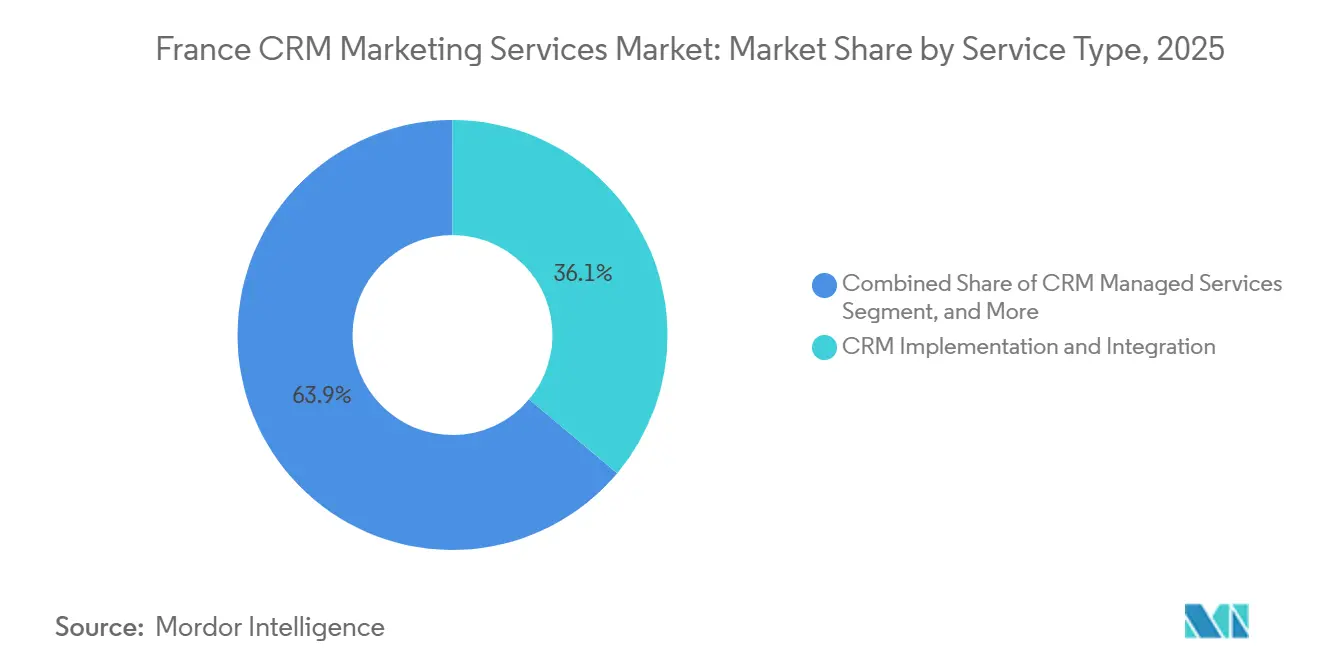

- By service type, CRM implementation and integration led with 36.11% of the France CRM marketing services market in 2025, while CRM Managed Services is projected to expand at a 12.46% CAGR through 2031.

- By enterprise size, large enterprises held 67.51% share in 2025, while small and medium enterprises are projected to grow at a 13.29% CAGR through 2031.

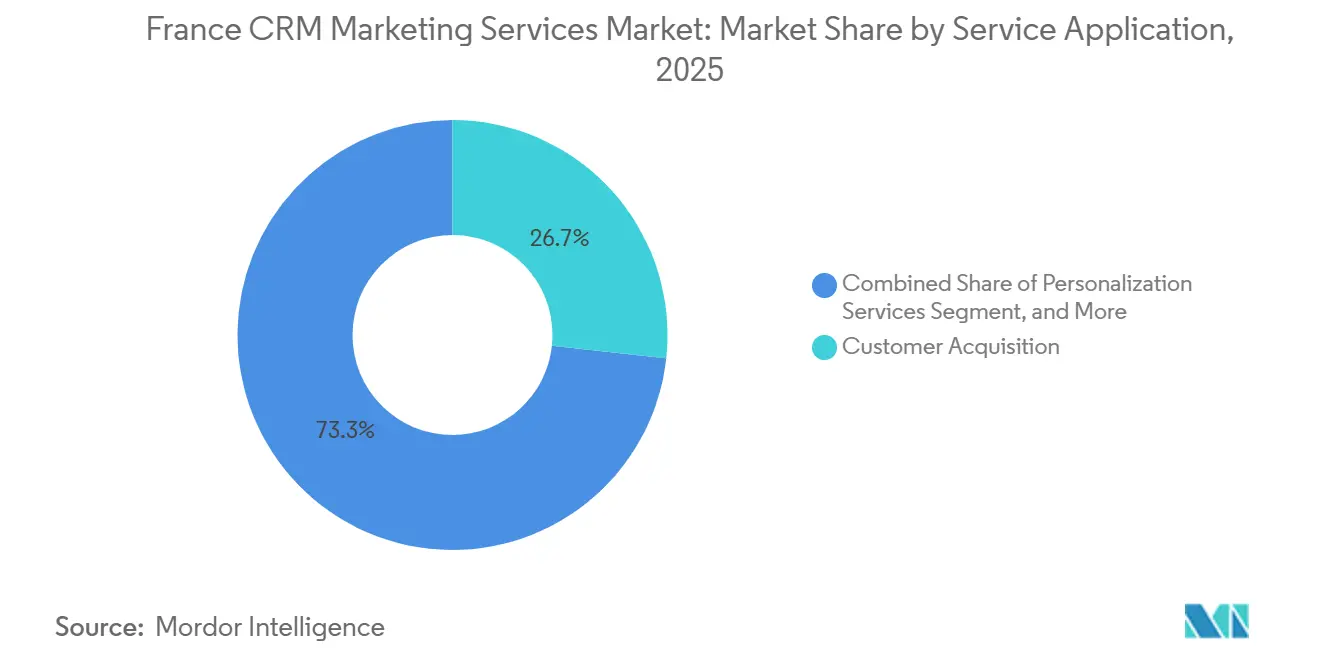

- By service application, customer acquisition accounted for 26.73% share in 2025, while customer analytics and insights are projected to advance at a 14.72% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance (BFSI) held 22.13% share in 2025, while retail and e-commerce are projected to expand at a 14.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising SME Adoption of Structured Customer Data Workflows | +2.0% | National, with concentrated early gains in Ile-de-France, Auvergne-Rhone-Alpes, and Occitanie | Short term (≤ 2 years) |

| Generative AI Assisted Campaign Orchestration | +1.8% | National, strongest in Ile-de-France with enterprise-grade infrastructure, expanding to Lyon, Toulouse, and Bordeaux tech corridors | Medium term (2-4 years) |

| Shift to First-Party Data and Consent-Based Marketing | +1.4% | National, driven by CNIL enforcement posture and GDPR compliance requirements across all French industry sectors | Short term (≤ 2 years) |

| Rising Demand for Unified Sales, Service, and Marketing Operations | +1.2% | National, with deepest penetration in BFSI and IT and Telecom verticals concentrated in Ile-de-France and Auvergne-Rhone-Alpes | Medium term (2-4 years) |

| Composable Customer Data Platform Adoption in Regulated Enterprises | +0.9% | Ile-de-France and Auvergne-Rhone-Alpes core markets, with early adoption in financial services and healthcare clusters in Lyon, Bordeaux, and Strasbourg | Medium term (2-4 years) |

| Verticalized CRM Services for Industry-Specific Workflows | +0.7% | National, with vertical depth emerging in BFSI in Paris and Lyon, and aerospace and manufacturing in Toulouse and Clermont-Ferrand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising SME Adoption of Structured Customer Data Workflows

Small and medium enterprises are moving from informal customer tracking toward structured CRM processes, and that shift is broadening the client base for the France CRM marketing services market. France Num’s 2025 Barometer found that 75% of French TPE and PME already use client and sales data to steer activity, which shows that data-led decision making has moved well beyond large enterprises. The same market direction is visible in near-term buying plans, with 43% of French organizations saying they plan to deploy or change their CRM platform in the near term. A 2025 peer-reviewed study found that CRM performance in SMEs improves when technology is matched with structured customer knowledge workflows, which supports demand for advisory, implementation, and adoption support rather than software alone.[1]Heider A. Yousif and Nuur Shazwani Binti Shamsuddin, “Strengthening CRM Performance Through Customer Knowledge, The Role Of Technological Capability In SMEs,” European Business Review, doi.org This pattern is one reason SMEs are becoming the fastest-growing enterprise tier in the France CRM marketing services market, especially as quick-start programs and modular cloud platforms lower entry barriers.

Generative AI Assisted Campaign Orchestration

Generative AI is changing campaign management from a manual process into a more continuous operating model, and that is creating fresh service demand across the France CRM marketing services market. Salesforce reported in 2025 that 75% of marketers had adopted AI, yet 84% still admitted they run generic campaigns, which points to a gap between tool adoption and execution quality. The same report found that marketers with unified customer data were 60% more likely to use AI agents to scale engagement, which makes data integration and CRM configuration work more important. SAP and Google Cloud expanded their partnership in April 2026 to deploy Joule Agents within SAP CX, allowing marketers to set business goals and let AI coordinate personalization, launch activity, and conversational engagement across channels. As AI moves inside the CRM layer, service work is shifting toward tuning, governance, integration, and ongoing oversight rather than one-time deployment.

Shift to First-Party Data and Consent-Based Marketing

The move to first-party data architecture has become a structural driver for the France CRM marketing services market because privacy rules now shape how campaigns are designed and executed. The European Data Protection Board launched 32 coordinated supervisory investigations in 2025 around the right to erasure, showing that data governance remains an active enforcement priority across Europe. GDPR fines exceeded EUR 3 billion (USD 3.24 billion) in 2025 and pushed the cumulative total past EUR 5 billion (USD 5.4 billion), which reinforces the cost of weak privacy controls.[2]European Data Protection Board, “Coordinated Enforcement Framework, Right To Erasure,” EDPB, edpb.europa.eu In France, 76% of organizations placed data security at the top of their CRM investment priorities, and 27% included digital sovereignty and European hosting in their top 3 decision criteria. This is pushing CRM service engagements beyond implementation into consent workflow redesign, retention policy alignment, segmentation controls, and long-term platform governance.

Rising Demand for Unified Sales, Service, and Marketing Operations

Many enterprises now want a single customer view across sales, service, and marketing, and that is supporting larger transformation programs in the France CRM marketing services market. Salesforce found that only 58% of marketers had complete access to service data, and 56% had complete access to sales data, which shows how fragmented customer context still limits execution. Microsoft described this shift in June 2026 through its agentic CRM model, where AI agents capture and update customer information from live interactions and reduce manual data entry. That model raises the value of integration architecture because customer records, workflows, and permissions must remain aligned across functions. As a result, CRM work is increasingly spanning vendor selection, migration, change management, data standardization, and ongoing optimization rather than a single system rollout.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Budget Pressure in Large Accounts and Slower Replacement Cycles | -1.2% | National, most pronounced in Ile-de-France where multi-year CRM contracts with large enterprises dominate | Medium term (2-4 years) |

| Fragmented Legacy Systems Increasing Integration Complexity | -1.0% | National, most acute in large enterprises in BFSI and industrial manufacturing clusters across Ile-de-France, Hauts-de-France, and Grand Est | Long term (≥ 4 years) |

| Data Privacy, Consent, and AI Governance Constraints | -0.8% | National, with GDPR, the EU AI Act, and CNIL enforcement creating particular scrutiny for AI-assisted marketing in financial services and public administration | Medium term (2-4 years) |

| Talent Shortage in CRM Architecture, MarTech, and Data Operations | -0.6% | National, concentrated in Paris and Lyon tech hubs, and more acute in secondary regional centers with smaller talent pools | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Pressure in Large Accounts and Slower Replacement Cycles

Large enterprises remain important buyers in the France CRM marketing services market, but they are reviewing CRM renewal budgets more carefully than before. Multi-year contracts now face stronger scrutiny because platform costs, AI spending priorities, and license escalation clauses can all compete for the same budget pool. This often slows seat expansion, delays module additions, and stretches replacement cycles for older CRM estates. The effect is strongest in large accounts where implementation and upgrade work tends to be highest in value. Smaller service providers are more exposed when these decisions are postponed because they often depend more heavily on discretionary project revenue than diversified global integrators.

Fragmented Legacy Systems Increasing Integration Complexity

Legacy integration estates continue to slow the France CRM marketing services market because many enterprises still operate older customer data flows, custom links, and undocumented system dependencies. CRM modernization projects often start with a platform change, but they can expand into a much broader remediation effort once hidden integration issues appear. This raises delivery risk, extends discovery work, and increases the pressure on both timelines and margins. Specialist firms can benefit when clients need deep architecture knowledge, but the same complexity can also create scope creep and resource strain. The result is a market where demand remains solid, yet execution risk stays elevated when clients carry years of technical debt across sales, service, and marketing systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Managed Services Define the Next Demand Cycle

CRM implementation and integration held 36.11% of France CRM marketing services market share in 2025, while CRM managed services are projected to grow at a 12.46% CAGR through 2031. Implementation and integration remained the largest service type because major buyers still need vendor selection, system design, migration planning, and workflow alignment when they consolidate older CRM environments. This pattern is especially visible in financial services and telecom programs where data controls, permissions, and reporting requirements make delivery more complex. Strategy and consulting continue to act as the entry point for first-time buyers and for firms that are reassessing platform fit before committing to larger rollouts. Migration and modernization are also gaining weight as enterprises that deployed Salesforce or Microsoft Dynamics years ago now need cleaner data structures, updated integrations, and AI-ready configurations.

Training and support remain the smallest service type by revenue, but they still matter in enterprise deployments, where change management and user adoption influence project outcomes. The service mix is also shifting because newer CRM environments require more continuous operational oversight than earlier generations of platform deployments. Microsoft’s June 2026 view of agentic CRM shows why this matters, since AI now captures and updates customer data in the flow of work rather than after the fact. SAP’s April 2026 expansion with Google Cloud points in the same direction because AI agents are being embedded directly into customer engagement processes. As a result, the France CRM marketing services market is moving toward a more recurring revenue profile in which managed services, governance, optimization, and AI supervision carry more weight over time.

By Enterprise Size: SME Momentum Challenges the Large-Account Revenue Model

Large enterprises accounted for 67.51% of the France CRM marketing services market size in 2025, while Small and Medium Enterprises are projected to expand at a 13.29% CAGR through 2031. Large organizations still dominate revenue because they manage broader user bases, more complex integration estates, and tighter regulatory obligations than smaller firms. These buyers also tend to run multi-phase programs that include architecture work, rollout support, change management, and longer post-launch service commitments. Even so, the faster growth path is shifting toward SMEs as cloud pricing, modular packages, and simpler deployment models improve accessibility. That change is widening the addressable base of the France CRM marketing services market beyond traditional large-account demand.

The momentum behind SMEs is supported by clear signals from the French business environment. France Num reported that 75% of TPE and PME already use client and sales data to guide business activity, which shows that the habit of structured customer management is already taking hold. Another 43% of organizations said they plan to deploy or change their CRM platform in the near term, which supports a healthy near-term service pipeline. The 2025 peer-reviewed study on SMEs also showed that strong CRM outcomes depend on customer knowledge workflows, not just software capability, which supports demand for process design and adoption services. This gives smaller specialist firms room to compete through fixed-scope rollout programs, faster implementation cycles, and operating models tailored to mid-market clients.

By Service Application: Analytics Overtakes Acquisition as the Strategic Imperative

Customer acquisition accounted for 26.73% of the France CRM marketing services market size in 2025, while Customer analytics and insights is projected to advance at a 14.72% CAGR through 2031. Acquisition remained the largest service application because retail, financial services, and telecom buyers continue to invest in lead generation, scoring, and outreach automation. The faster growth in analytics shows that buyers now want stronger intelligence from existing data rather than only higher campaign volumes. This shift is pulling the France CRM marketing services market toward use cases such as intent analysis, segmentation refinement, lifecycle orchestration, and next-best-action design. It also favors service providers that can align CRM data, AI models, and reporting logic rather than focus only on campaign execution.

HubSpot’s July 2026 acquisition of Warmly illustrates this direction because it addressed the problem that 96% of B2B website visitors remain anonymous and made real-time intent signals more usable inside CRM workflows.[3]HubSpot, “HubSpot Acquires Warmly To Advance AI-Driven CRM And Close The Anonymous Visitor Gap,” HubSpot Company News, hubspot.com Salesforce also found that brands with unified customer data were 42% more responsive to customer signals than organizations running fragmented stacks. Campaign management and marketing automation are moving in the same direction as AI orchestration becomes more central to CRM activity. SAP’s April 2026 partnership expansion with Google Cloud enabled multi-agent marketing activity inside SAP Engagement Cloud, from audience segmentation through personalized engagement. This means service providers now compete as much on data and analytics design as they do on campaign setup and channel execution.

By End-User Industry: BFSI Anchors Revenue While Retail Reshapes the Growth Narrative

BFSI held 22.13% of France CRM marketing services market share in 2025, while Retail and E-commerce is projected to grow at a 14.13% CAGR through 2031. BFSI remained the largest end-user industry because customer engagement in banking and insurance is tied to complex relationship workflows, audit trails, consent controls, and integration with core operating systems. That makes implementations more advisory-intensive and often longer in duration than work in less regulated sectors. CSI’s May 2026 launch of Customer Intelligence Suite showed how financial institutions are moving toward AI-powered insights in branch and digital channels rather than relying only on reactive service models.[4]CSI, “CSI Introduces Customer Intelligence Suite, Helping Financial Institutions Deepen Customer Relationships Through AI-Powered Insights,” CSI Newsroom, csiweb.com The scale and complexity of those requirements help keep BFSI central to the France CRM marketing services market even as faster growth appears elsewhere.

Retail and e-commerce is rising more quickly because post-cookie marketing now depends more heavily on first-party data, segmentation quality, and personalization at scale. The same logic supports growth in customer retention, loyalty design, and omnichannel engagement services, where data unification becomes the base requirement. Healthcare and life sciences also present a meaningful growth path as providers adopt composable customer data structures for compliant engagement models. IT and telecom buyers continue to invest in unified service and sales environments to reduce churn and improve account visibility across channels. Industrial manufacturing, once a slower adopter, is now using CRM services to support long B2B sales cycles, larger buying committees, and aftermarket revenue management.

Geography Analysis

Ile-de-France remains the largest geographic concentration within the France CRM marketing services market because the region holds the highest density of large enterprise headquarters and advanced service buyers. Financial services, media, luxury retail, and technology organizations in the Paris area continue to generate the most complex CRM programs, especially when projects involve platform consolidation, consent redesign, and AI-enabled customer engagement. France Num’s 2025 Barometer showed that financial and specialized services firms were among the most active digital spenders, which supports the region’s outsized role in CRM service demand. The CNIL’s stronger focus on AI-assisted marketing and behavioral profiling also keeps compliance-oriented CRM work firmly embedded in large-account projects in this region.

Auvergne-Rhone-Alpes is the strongest secondary region in the France CRM marketing services market, with Lyon acting as the main hub for technology, industrial, and life sciences demand. The region benefits from a mix of digital service buyers and B2B manufacturers, which creates demand for both marketing automation and account-based CRM programs. Its role is also expanding because AI adoption among regional enterprises has accelerated, with commercial and marketing uses becoming more common in the mid-market. The French government’s Osez l’IA program, launched in July 2025 with a EUR 200 million (USD 218 million) national envelope, identified Auvergne-Rhone-Alpes as an early implementation hub for broader AI diffusion among TPE and PME. That strengthens the local pipeline for CRM analytics, customer data unification, and managed support services.

Occitanie, Nouvelle-Aquitaine, and Hauts-de-France are emerging as the next growth corridors for the France CRM marketing services market. Toulouse creates specialized demand through aerospace and defense, where data sovereignty and structured relationship management matter more than standard campaign deployment. Bordeaux adds demand from tourism, viticulture, and agri-tech environments that need loyalty, account management, and targeted engagement programs. France Num also found that 78% of French TPE and PME leaders believe digital tools deliver real commercial benefits, which supports broader regional uptake beyond the largest metropolitan centers.

Competitive Landscape

The France CRM marketing services market remains moderately fragmented, with competition spread across global platform vendors, large system integrators, and a dense group of regional specialists. Salesforce, Microsoft, SAP, Oracle, Adobe, and HubSpot shape the technology layer, while Accenture, Capgemini, and Publicis Groupe compete for large transformation mandates. At the same time, local and regional firms such as Devoteam, Synolia, Klee Group, SQLI, ALMAVIA CX, Markentive, Isatech, and ChapsVision remain relevant because they offer certified platform expertise with more flexible delivery models. This structure keeps the France CRM marketing services market open enough for specialist firms to win work, especially when buyers want GDPR-aware execution, faster deployment cycles, or mid-market pricing discipline.

Capgemini strengthened its position in May 2026 by investing in the OpenAI Deployment Company, which reinforced its ability to embed frontier AI into enterprise CRM and customer workflow programs.[5]Capgemini, “Capgemini Strengthens Its Position In Enterprise AI With Investment In The OpenAI Deployment Company,” Capgemini Press Release, capgemini.com Publicis Groupe also committed EUR 300 million (USD 327 million) to CoreAI as part of its 2026 strategy, using Epsilon data and AI capabilities to deepen its role in personalization and technology-led client work. HubSpot’s July 2026 acquisition of Warmly showed a different strategic path, where CRM vendors are extending product capability to improve intent detection and real-time buyer engagement inside the platform itself. SAP’s expansion with Google Cloud in April 2026 further raised the bar by pushing multi-agent AI orchestration into customer engagement workflows. These moves show that competition in the France CRM marketing services market is shifting from basic implementation capacity toward AI integration depth, customer data fluency, and recurring managed service capability.

This shift also creates room for mid-tier firms that can bridge local execution with modern AI and data governance demands. White-space opportunities remain strongest in underpenetrated verticals such as industrial manufacturing, healthcare, and government, where process design and compliance knowledge can matter more than scale alone. The managed services gap is another opening because demand is growing faster than the supply of firms that can supervise AI-enabled CRM estates at enterprise standards. Devoteam’s May 2026 expansion with Google Cloud shows how regional players are trying to strengthen this position through AI-oriented capability building. Overall, the France CRM marketing services market rewards breadth at the top end, but it still leaves meaningful space for specialized firms with platform credentials, regional delivery strength, and strong governance skills.

France CRM Marketing Services Industry Leaders

Salesforce, Inc.

Microsoft Corporation

SAP SE

Oracle Corporation

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nokia, SAP, and Microsoft announced a multi-year strategic agreement to advance cloud and AI-driven business transformation, integrating SAP CX and Microsoft Azure capabilities to support enterprise-grade customer engagement and operational workflows across Nokia's global operations.

- June 2026: Salesforce, via Informatica, a Salesforce company, deepened its collaboration with Microsoft, unveiling new integrations designed to empower joint Azure customers to accelerate AI and analytics initiatives with trusted, high-quality data, reinforcing the convergence of CRM and enterprise data management platforms.

- May 2026: Capgemini announced an investment in the OpenAI Deployment Company, reinforcing its strategic partnership with OpenAI and expanding its enterprise AI deployment capacity globally. The move supports Capgemini's ability to embed frontier AI into core CRM and business operations workflows for clients.

- April 2026: SAP and Google Cloud expanded their partnership to deploy multi-agent AI at scale for CRM marketing use cases, integrating Joule Agents with Google's Gemini Enterprise. Joint customers can now execute AI-driven campaign orchestration, from audience segmentation to personalized engagement, within SAP Engagement Cloud, with availability in H2 2026.

France CRM Marketing Services Market Report Scope

France CRM marketing services market refers to the platforms and services that help businesses manage customer relationships and improve marketing operations. These services include customer data management, campaign automation, analytics, personalization, and omnichannel engagement. They help French businesses enhance customer loyalty and increase revenue while ensuring compliance with national and EU regulations, including the GDPR and France’s CNIL guidelines. France’s focus on data sovereignty, AI innovation hubs, and cloud compliance shapes the market, making CRM services both highly regulated and innovation-driven.

France CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current and forecast value of the France CRM marketing services space?

The France CRM marketing services market was valued at USD 1.26 billion in 2025, is expected to reach USD 1.38 billion in 2026, and is forecast to reach USD 2.18 billion by 2031 at a 9.58% CAGR.

Which service type leads revenue and which one grows the fastest in France?

CRM Implementation and Integration led with 36.11% share in 2025, while CRM Managed Services is projected to grow the fastest at a 12.46% CAGR through 2031.

Why are SMEs becoming more important in France CRM services demand?

SMEs are projected to grow at a 13.29% CAGR because cloud platforms are easier to adopt, quick-start delivery models are expanding, and more small businesses already use customer data to guide activity.

Which application area is seeing the strongest momentum through 2031?

Customer Analytics and Insights is the fastest-growing application at a 14.72% CAGR, reflecting a stronger focus on data unification, intent signals, and decision support inside CRM environments.

Which end-user group contributes the most revenue today?

BFSI led demand with a 22.13% share in 2025 because customer relationship workflows, compliance requirements, and integration needs are more complex than in many other sectors.

Which French regions matter most for CRM marketing services growth?

Ile-de-France remains the largest center of demand, while Auvergne-Rhone-Alpes stands out as the strongest secondary hub and Occitanie, Nouvelle-Aquitaine, and Hauts-de-France are emerging growth corridors.

Page last updated on: