France Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

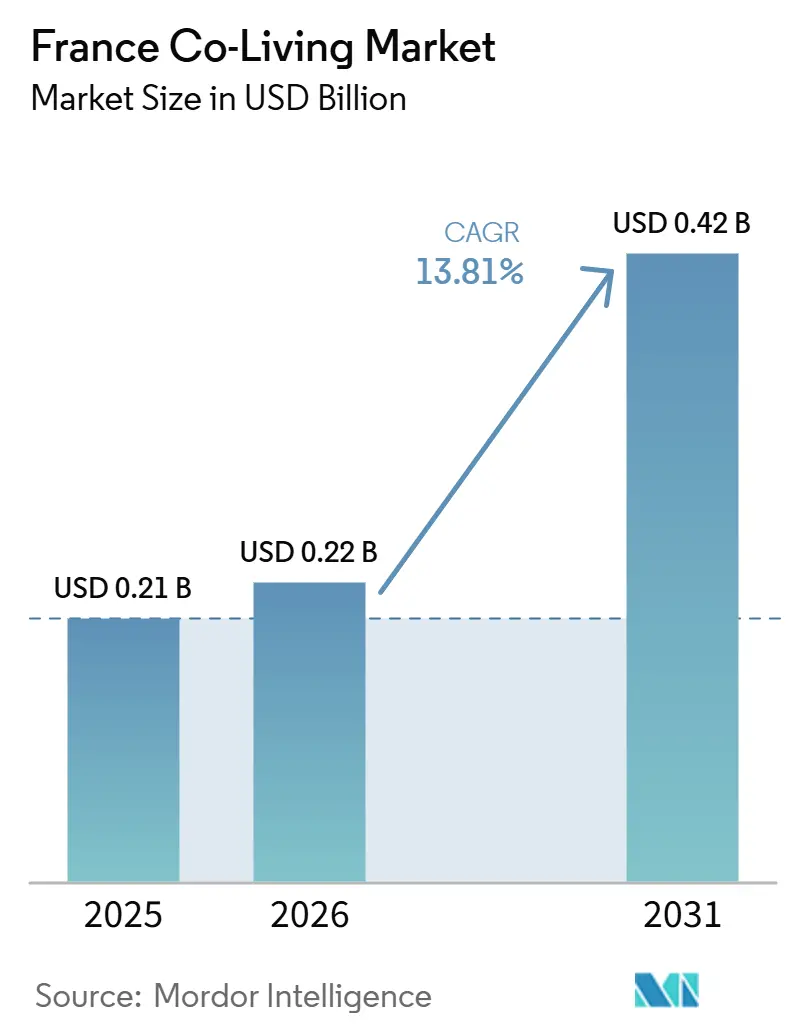

| Base Year Market Size (2025) | USD 0.21 Billion |

| Market Size (2026) | USD 0.22 Billion |

| Market Size (2031) | USD 0.42 Billion |

| Growth Rate (2026 - 2031) | 13.81% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Co-Living Market Analysis by Mordor Intelligence

The France Co-Living Market size is expected to increase from USD 0.21 billion in 2025 to USD 0.22 billion in 2026 and reach USD 0.42 billion by 2031, growing at a CAGR of 13.81% over 2026-2031.

The France co-living market is being supported by a housing environment where young people still face limited access to suitable rental stock, and a 2025 youth housing report described the situation as a social emergency because housing shortages are affecting education and labor mobility. The same demand base is also linked to shorter early-career work cycles, because first employment contracts in France commonly last close to 2 years, which makes standard long leases less suitable for many new workers. Legal changes to the bail mobilité framework in 2025 expanded tenant eligibility, making flexible furnished housing more accessible to a broader range of mobile residents, including remote workers, career changers, and family caregivers. Operators are also pushing growth through managed buildings, adaptive reuse, and amenity-led formats, with new openings and projects in Paris, Lille, Bordeaux, Montpellier, and other cities showing that the offer is broadening beyond its earlier base. Paris also adopted a restrictive political stance in late 2025, and that pressure is redirecting part of the operator pipeline toward secondary cities, which is helping the France co-living market expand on a wider geographic base.

Key Report Takeaways

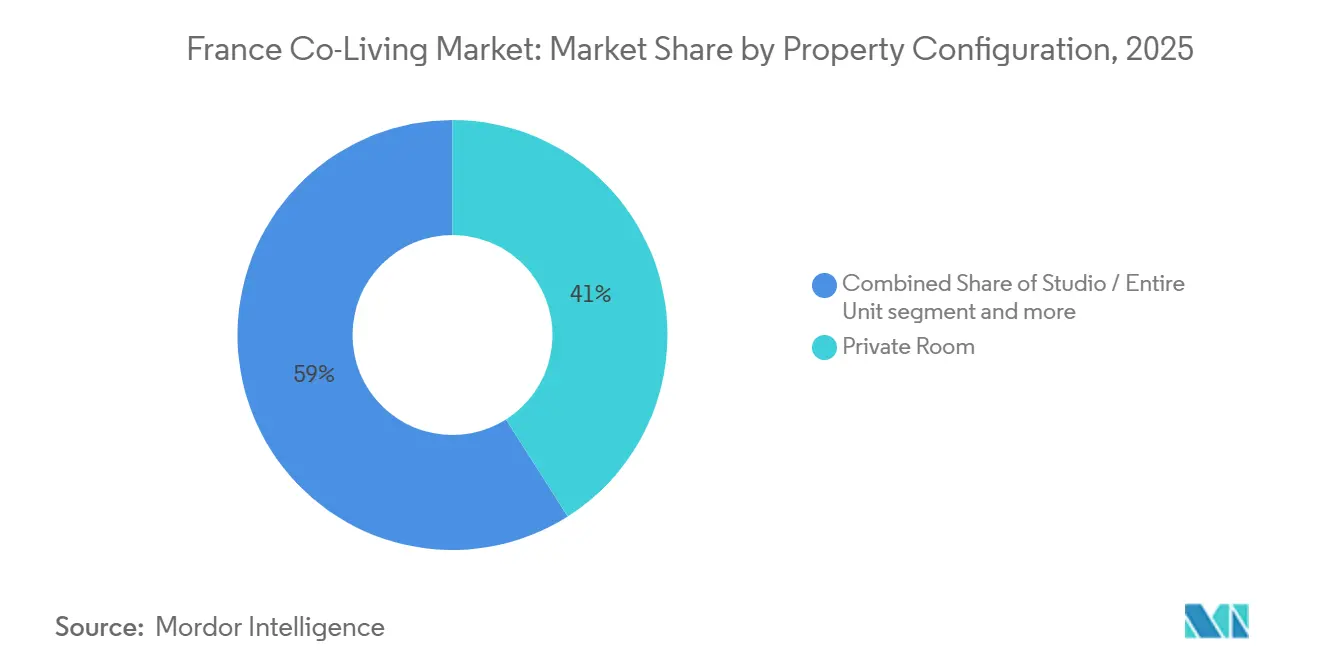

- By property configuration, private rooms led with a 41% revenue share in 2025, while studios / entire units are forecast to expand at a 15.20% CAGR through 2031.

- By business model, asset-light master lease / lease arbitrage held 44% of the France co-living market share in 2025, while asset-light management agreement recorded the highest projected CAGR of 14.90% through 2031.

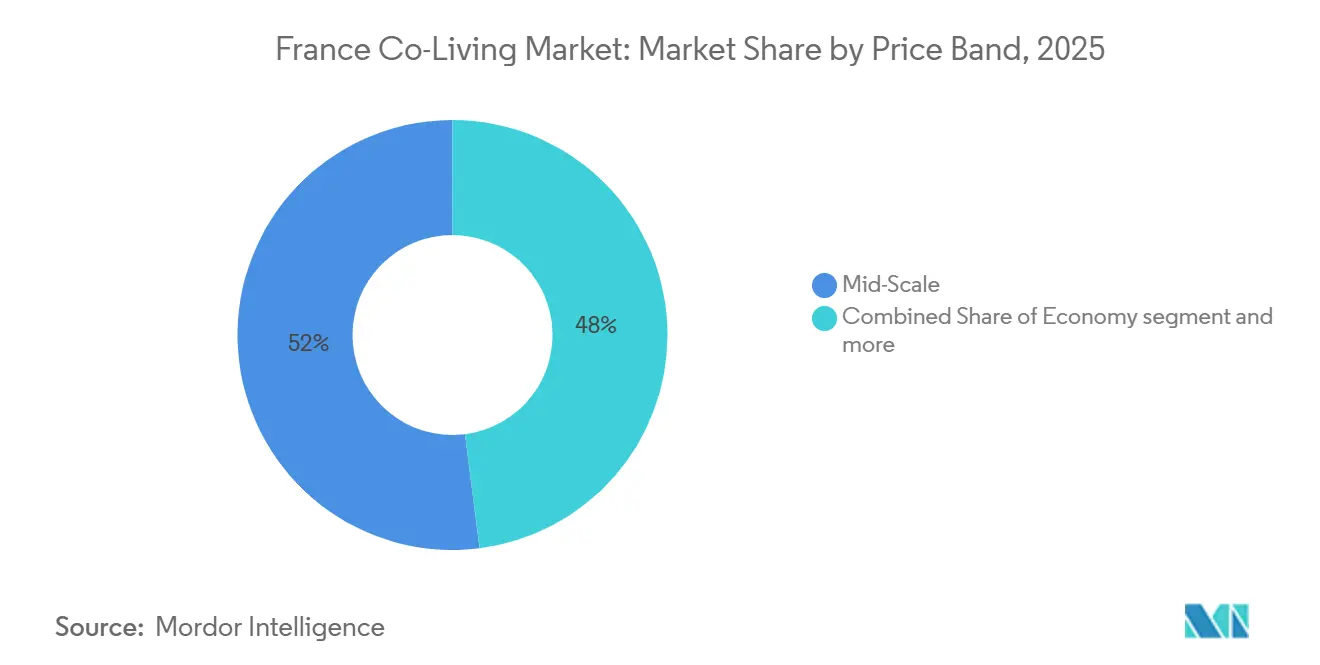

- By price band, mid-scale accounted for 52% of revenue in 2025, while premium / luxury is advancing at a 15.50% CAGR through 2031.

- By end user, students accounted for 53% of the France co-living market share in 2025, while working professionals are projected to grow at a 14.88% CAGR through 2031.

- By city, Paris held a 42% share of the France co-living market size in 2025, whereas Marseille is anticipated to witness the fastest growth, at a CAGR of 16.00% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Housing Shortages in Major Cities Drive Co-Living Demand | +2.8% | National, most acute in Paris, Lyon, Marseille, Bordeaux | Short term (≤ 2 years) |

| High Rental Costs Increase Demand for Affordable Shared Housing | +2.5% | Paris, Lyon, Bordeaux | Medium term (2-4 years) |

| Growing Young Professional and Student Population Expands Occupancy | +2.0% | National, with early gains in Paris, Lyon, Lille | Medium term (2-4 years) |

| Preference for Flexible Ready-to-Move-in Housing Boosts Market Adoption | +1.8% | National, with stronger penetration in Paris and major university cities | Medium term (2-4 years) |

| Rising Acceptance of Community-Led Living Supports Market Growth | +1.5% | National, with concentrated momentum in Paris and Bordeaux | Long term (≥ 4 years) |

| Expansion of Build-to-Rent Housing Supports Co-Living Adoption | +1.2% | Paris region, Aix-Marseille metropolis, Lyon | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Housing Shortages in Major Cities Drive Co-Living Demand

France’s housing shortage remains structural, and the pressure is most visible among younger residents who need affordable and flexible accommodation near study and work centers[1]Sénat, “Mission D'information Sur Le Logement Des Jeunes,” Sénat, senat.fr. A 2025 Senate-linked youth housing review found that 17% of students had already dropped out of school because they could not secure affordable housing, underscoring how housing stress is spilling into educational outcomes. The France co-living market benefits from this mismatch because furnished, managed residences can absorb residents who cannot wait for conventional student or social housing allocations to catch up. Shorter work cycles add to that demand, because first-job contracts in France often last close to 2 years and leave many early-career tenants poorly matched to long, rigid lease structures. This makes co-living more than a lifestyle product, because it also serves as overflow housing for students, young workers, and other mobile residents whose housing needs change faster than conventional supply can respond. The pressure intensified after low-energy-rated homes faced stronger leasing restrictions from 2025, which removed part of the older rental stock from the market and increased competition for compliant units.

High Rental Costs Increase Demand for Affordable Shared Housing

High urban rental costs remain a direct support for the France co-living market because many residents are looking for housing that lowers total monthly setup and living costs rather than only headline rent. Paris authorities cited a situation in which 1 in 2 tenants spent one-third of their income on housing, and that level of cost stress helps explain why shared formats remain relevant even when priced at a premium over bare rent alone. The end of the Pinel tax incentive in January 2025 also reduced support for new rental supply, making the existing market tighter and increasing the value of ready-to-occupy housing products. In practice, co-living reduces several cash burdens at once because residents do not need to furnish units, open multiple utility accounts, or fund the same level of move-in setup that a normal lease often requires. That matters for recent graduates and mobile workers who may have income but limited savings, and for students who are already competing in a strained housing environment. The result is that the France co-living market competes not only on monthly price, but also on lower friction at the moment of move-in, which is often the bigger barrier for short-stay renters.

Growing Young Professional and Student Population Expands Occupancy

The France co-living market is closely tied to the country’s large student and young adult population, as this group has the strongest need for mobility, affordability, and furnished housing. The Senate noted that people aged 18 to 29 accounted for 17.6% of the population in 2024, and that 37.4% of those aged 15 to 24 were enrolled in higher education, which keeps demand concentrated in university cities and employment hubs. The Cour des Comptes also reported that 2.7 million young people aged 18 to 30 received housing allowances in 2023, with total support reaching EUR 4.4 billion (USD 4.8 billion), yet undersupply persisted across the housing system. Operators have been scaling around that demand base, and The Boost Society signaled this by targeting a much larger national bed count as it expanded the KLEY and Hife brands. Occupancy is no longer shaped solely by students, as Oqoro’s 2025 portfolio data showed that young professionals almost matched students in the use of shared housing, suggesting a broader resident mix. That shift matters because it supports higher resilience for the France co-living market across academic cycles and strengthens demand in cities with diversified employment bases.

Preference for Flexible Ready-to-Move-in Housing Boosts Market Adoption

The France co-living market is also benefiting from a stronger preference for housing that is furnished, digitally managed, and immediately usable from the day of move-in. Reforms to the bail mobilité framework in 2025 widened eligibility to remote workers, family caregivers, and career changers, and later changes extended possible occupancy duration for some employment-related stays. That legal expansion improved alignment between flexible lease structures and operator business models, as co-living depends on shorter-cycle occupancy without the friction of standard long residential leases. Managed co-living and student residences command all-inclusive rents that are 10% to 15% higher than comparable local market offerings, reflecting demand for convenience, services, and flexibility rather than floor area alone. Operators that added resident apps, digital check-in, and service layers also achieved strong occupancy, with The Babel Community reporting a 94% occupancy rate across its portfolio in 2024. This supports a wider move in the France co-living market toward product quality and operational ease, not only toward the lowest possible entry price.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Rental and Tenant Protection Rules Limit Market Flexibility | -1.5% | Paris, Lyon, Montreuil, with national implications | Short term (≤ 2 years) |

| Planning and Zoning Restrictions Delay New Co-Living Developments | -1.2% | Paris, Lyon, Bordeaux, high-density municipal zones | Medium term (2-4 years) |

| High Property Acquisition and Renovation Costs Constrain New Supply | -0.8% | Paris, Île-de-France, Lyon | Medium term (2-4 years) |

| Limited Availability of Suitable Urban Assets Restricts Market Expansion | -0.6% | National, most acute in central Paris and Lyon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Rental and Tenant Protection Rules Limit Market Flexibility

The main regulatory challenge for the France co-living market is that the product still sits inside legal and political categories that were not built specifically for it. The French government confirmed in January 2026 that it would not create a dedicated legal framework for co-living, removing one path toward clarity and leaving operators to work under existing rental rules. Paris then heightened the political risk by adopting a zero-carbon resolution in November 2025, even though it was non-binding, signaling a harder stance toward new projects. A Senate bill filed in the same month proposed public registries, prior authorization, and stricter rent-control measures for co-living residences, indicating that the debate is widening beyond one city. This pressure does not affect every operator equally, because management agreement models carry less direct lease exposure than models built on long-term leased liabilities. Even so, the lack of a dedicated framework keeps compliance risk elevated and can slow expansion decisions across the France co-living market.

Planning and Zoning Restrictions Delay New Co-Living Developments

Planning rules are another brake on the France co-living market because municipal zoning systems still struggle to classify projects that blend private rooms, shared amenities, and service elements. The proposed Senate legislation would allow local authorities to track and regulate co-living more directly and could even support geographic caps in dense areas if local opposition remains strong. France passed a 2025 law to make office-to-residential conversions easier, which helps operators access more buildings for adaptive reuse, but the conversion path still involves entitlement and design complexities that can delay delivery. Adaptive reuse is already central to some operator strategies, and The Babel Community said that close to 80% of its projects involved this type of urban recycling. Those projects can unlock valuable central locations, but they also bring higher planning uncertainty, more technical work, and a slower path to revenue. This means the France co-living market can keep growing, but it will often do so through staged pipelines rather than rapid, high-volume project launches in the tightest urban cores.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Private Rooms Lead, Studio / Entire Units Gain Ground Among Long-Stayers

Private rooms held 41% of the France co-living market share in 2025, which kept them in the leading position because they offer a practical balance between individual privacy and efficient use of floor space. This format still aligns with the core promise of co-living because it provides residents with a personal sleeping and working area while maintaining shared kitchens, lounges, and community features. It also allows operators to maintain bed density without fully adopting dorm-style layouts that are less attractive to working professionals. Shared rooms remain relevant for lower-priced offers, but they face growing substitution pressure from other flexible housing formats that can match price while offering more independence. That pressure is likely to keep shared rooms important in economy-oriented offers, but less central in premium assets where privacy is a stronger part of the value proposition.

The faster change is happening in studio / entire units, where the France co-living market size for this format is projected to rise at a 15.2% CAGR through 2031. This shift reflects the wider tenant mix now entering the France co-living market, especially remote workers and professionals who want autonomy inside a managed building. The 2025 changes to bail mobilité widened the legal path for these residents and made shorter, furnished stays easier to structure. Premium brands such as Hife and Bikube are also pushing this configuration by pairing more self-contained private units with large amenity zones and service layers that preserve the community element. The ECLA Lille-Lomme project, with 787 beds and a summer 2026 opening, shows how purpose-built assets are bringing higher environmental standards and broader amenity packages into this part of the France co-living market.

By Business Model: Asset-Light Master Lease / Lease Arbitrage Dominance and the Management Agreement Inflection

Asset-light master lease / lease arbitrage held 44% of the France co-living market by business model in 2025, which kept it as the leading structure for operator growth. This model has remained attractive because it allows operators to control resident experience and revenue without owning the building. It also suited a period when operators wanted to keep scaling even as investment conditions became less favorable for direct development. In operational terms, the model supports faster entry into cities where the core challenge is not resident demand, but the speed of securing suitable assets and launching them. That explains why it still carries weight in the France co-living market even as the funding environment becomes more selective.

The clearest directional move is now toward management agreements, which are forecast to grow at a 14.90% CAGR through 2031. The management contracts are an important strategic shift because they align owner and operator interests more closely and reduce operator balance-sheet exposure relative to lease-heavy structures. Goldman Sachs Asset Management’s acquisition of Urban Campus, announced in March 2026, reinforced that view, as the platform's plan emphasized expansion through management-agreement-led growth across France and nearby markets. That transaction matters because it shows that institutional capital still sees long-term value in the France co-living market when the operating model is lighter and more scalable. The own-develop-operate model remains relevant for large groups such as Vinci Immobilier and UXCO that can support longer project cycles and heavier capital commitments. Still, it is not the format driving the next phase of expansion.

By Price Band: Mid-Scale Majority Masking a Premium / Luxury Breakout

Mid-scale co-living held 52% share in 2025, which shows that the France co-living market is still rooted in practicality and affordability rather than a narrow luxury niche. This tier appeals to students and early-career professionals who need managed housing but remain price-conscious. It is also the most direct expression of co-living’s original role as a bridge between expensive conventional rentals and undersupplied student accommodation. Economy formats continue to serve cost-sensitive users, especially outside the most expensive districts, but margin pressure is becoming harder to ignore when acquisition, compliance, and renovation costs keep rising. That means mid-scale remains the volume base of the France co-living market even as the product evolves upward.

The premium / luxury segment is the standout because it is projected to grow at a 15.50% CAGR through 2031, the fastest rate across the segment set. Managed residences in this tier often charge all-inclusive rents 10% to 15% above comparable local options, which are justified by utilities, wellness, coworking space, and curated services rather than by unit size alone. This shift is also changing how the France co-living market positions itself, because premium offers are easier to defend as a differentiated housing product than as a workaround to rent-controlled mainstream rentals. The upcoming ECLA Bordeaux residence, scheduled for August 2026, reflects that move with RE2020 compliance, BREEAM credentials, furnished units, and an integrated amenity package. In effect, the higher end is no longer a side segment, because it is becoming one of the clearest ways operators protect margins and broaden the resident base of the France co-living market.

By End User: Students Anchor Volume, Working Professionals Drive Value

Students accounted for 53% of the France co-living market size in 2025, which confirms that student demand still anchors total occupancy. The underlying reason is simple, because France continues to have a large gap between student numbers and dedicated housing capacity. Around 3 million students competed for nearly 450,000 beds, of which only 150,000 were in the private sector, highlighting the continued importance of private accommodation providers. The student housing market drew strong investment in 2025, suggesting institutional capital still sees this demand gap as durable, even as broader co-living investment appetite remains uneven. In the France co-living market, student demand therefore remains the main volume base and the most dependable occupancy anchor.

Working professionals are the faster-growing user group, with a 14.88% CAGR projected through 2031. Their growth is tied to labor mobility, shorter early-career contracts, and a stronger preference for furnished housing that requires shorter setup periods. The 2025 expansion of bail mobilité also widened eligibility to more mobile adults, which strengthened the legal fit for this resident cohort. Operators such as Hife and Ecla are responding by offering larger private formats and amenities focused on work, wellness, and convenience rather than a purely student lifestyle[2]Banque des Territoires, “ECLA Lille Lomme, Une Nouvelle Résidence Étudiante Innovante,” Banque des Territoires, banquedesterritoires.fr. This means professionals are becoming a value driver for the France co-living market even while students continue to supply most of the base demand.

Geography Analysis

Paris accounted for 42% of revenue in 2025, making it the largest geography in the France co-living market. That position came from the city’s strong demand base, its concentration of students and young professionals, and its earlier lead in operator presence. Paris and the surrounding region also offered the widest pool of buildings that could be repositioned into managed residential use. The Babel Community’s 2025 expansion included a 245-unit residence in Saint-Quentin-en-Yvelines, demonstrating that operators were already moving into the wider Paris region to stay close to the capital while reducing direct exposure to city-center restrictions[3]Après-demain SA, “Après-Demain SA And The Babel Community, An Alliance To Promote Co-Living In France,” Après-demain SA, apres-demain.com. Paris, therefore, remains the anchor geography of the France co-living market, but its expansion path is now more suburban and more selective than before.

Lyon, Bordeaux, and Lille now form the next layer of strategic importance. These cities combine student demand with rising appeal to mobile workers, giving operators a more balanced resident mix throughout the year. Lille is gaining extra visibility through large-format, purpose-built stock, and the ECLA Lille-Lomme project will add 787 beds with a summer 2026 opening. Bordeaux is also becoming more visible in the France co-living market because major operators have expanded there and premium projects are coming online. Lyon remains important for the same reasons, although it also shares some of the regulatory caution seen in Paris.

Marseille has attracted both local and international operators, suggesting the city is being viewed as a scalable managed-housing location rather than merely a peripheral experiment. Montpellier is following with a new hybrid project that mixes housing, coworking, and amenity space, which fits the product direction now spreading across the France co-living market. This regional shift does not mean Paris is losing relevance. It means future supply growth is being redirected toward cities where entitlements are more workable, competition is less crowded, and managed housing can still scale with fewer political barriers.

Competitive Landscape

The France co-living market is fragmented, with a mix of institutional platforms, regional operators, and independent providers competing across major cities. Companies such as The Boost Society, UXCO, Urban Campus, The Babel Community, Colonies, and Vinci Immobilier are among the more visible participants, but no single operator holds a dominant market position. Competition is shaped by location strategy, operating quality, resident services, and the ability to build partnerships rather than by portfolio size alone. This allows both established platforms and smaller regional operators to compete effectively across different customer segments.

Competition is increasingly shifting toward asset-light operating models and partnership-based expansion. Management agreements are gaining traction because they reduce capital requirements while allowing operators to scale through operational expertise. Recent investments, including Goldman Sachs Asset Management's backing of Urban Campus and Eurazeo's acquisition of a majority stake in Babylon, demonstrate continued investor interest in scalable operating platforms and adaptive reuse projects. These developments strengthen competition while preserving the fragmented nature of the France co-living market.

Product differentiation has also become an important competitive factor. The Boost Society continues to expand student and young professional residences, UXCO focuses on premium large-scale developments, The Babel Community emphasizes adaptive reuse projects, and Vinci Immobilier's Bikube brand combines hospitality and co-living concepts for mobile residents. At the same time, numerous local operators continue to compete through city-specific expertise, flexible leasing models, and tailored resident experiences. As a result, the France co-living market is expected to remain fragmented, with competition driven by operating capability, product differentiation, and local market execution rather than overall market dominance.

France Co-Living Industry Leaders

Colonies

The Babel Community

Sharies

Ecla

Studapart

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eurazeo's EZORE fund took a majority position in Babylon, an integrated Paris-region aparthotel operator, with a stated objective of tripling the portfolio by 2030 through management contracts and the acquisition of vacant offices and obsolete hotels. The investment reflects institutional capital entering adjacent managed-residential formats.

- April 2026: Groupe M&A broke ground on a 160-apartment co-living and coworking hybrid residence in Montpellier's Cité Créative district, featuring a rooftop restaurant and fitness center, with completion targeted for 2028. The project signals growing operator interest in mid-sized southern markets beyond Marseille.

- January 2026: The government published its response in the Journal Officiel, confirming it will not create a specific legal framework for co-living, citing the sufficiency of existing rental provisions. This removes a near-term regulatory overhang but leaves zoning ambiguity unresolved.

- November 2025: The Paris city council formally adopted a "zero co-living" deliberation on November 7, 2025, signalling to developers and operators the city's refusal of new co-living projects, citing concerns about rent-control circumvention. The resolution is symbolic and non-binding, but it establishes a political baseline for future enforcement.

France Co-Living Market Report Scope

The France Co-Living Market Report is Segmented by Property Configuration (Studio / Entire Unit, Private Room, and Shared Room), Business Model (Asset-Light Master Lease / Lease Arbitrage and More), Price Band (Economy, Mid-Scale, and Premium / Luxury), End User (Students, and Working Professionals), and City (Paris, Lyon, Bordeaux, Lille, and Rest of France). The Market Forecasts are Provided in Terms of Value (USD).

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement |

| Asset-Heavy Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| Paris |

| Lyon |

| Bordeaux |

| Lille |

| Rest of France |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light Master Lease / Lease Arbitrage |

| Asset-Light Management Agreement | |

| Asset-Heavy Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium/Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Paris |

| Lyon | |

| Bordeaux | |

| Lille | |

| Rest of France |

Key Questions Answered in the Report

How large is France co-living by 2031?

France co-living is forecast to reach USD 0.42 billion by 2031 from USD 0.22 billion in 2026, with a 13.81% CAGR over 2026-2031.

What is driving demand in France?

Demand is being supported by student housing shortages, high rental pressure, shorter work cycles for young professionals, and stronger preference for furnished flexible leases.

Which resident group is most important today?

Students held 53% of revenue in 2025, so they remain the largest user group, while working professionals are growing faster at a projected 14.88% CAGR.

Which property format is leading?

Private rooms led with 41% share in 2025 because they balance privacy with shared amenities and efficient building economics.

Page last updated on: