FR-4 PCB Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 45.02 Billion |

| Market Size (2031) | USD 56.14 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

FR-4 PCB Market Analysis by Mordor Intelligence

The FR-4 Printed Circuit Board market size reached USD 45.02 billion in 2026 and is projected to advance to USD 56.14 billion by 2031, reflecting a 4.51% CAGR. Momentum comes from the structural miniaturization of consumer electronics, the thermal-cycling demands of electric-vehicle powertrains, and the shift to high-layer-count AI server boards. Asia-Pacific dominates current revenue, yet incentives in India and Vietnam are steadily redrawing regional supply routes. HDI and rigid-flex technologies carry higher average selling prices, while low-loss and high-Tg laminates gain ground in 5G radios and automotive inverters. Supply-chain vulnerabilities around high-Tg glass yarns, coupled with sustainability regulations that cap brominated flame retardants, keep pricing power with material innovators.

Key Report Takeaways

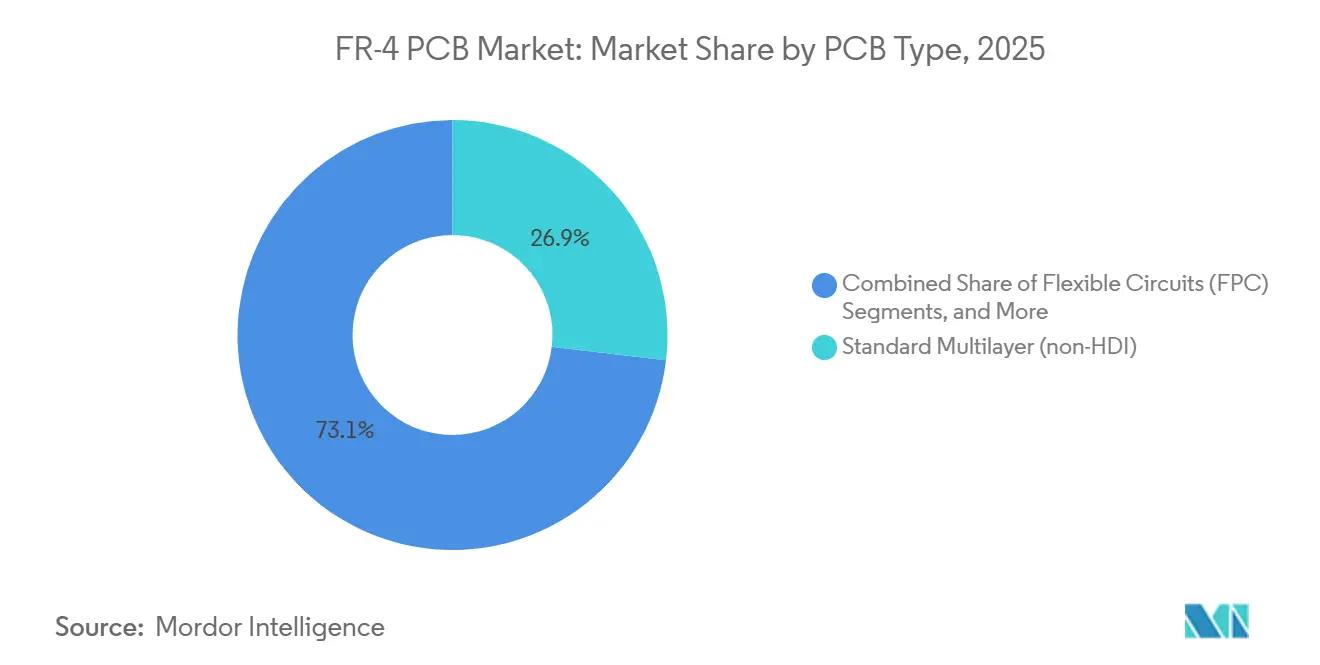

- By PCB type, standard multilayer non-HDI rigid boards held 26.87% FR-4 Printed Circuit Board market share in 2025, whereas flexible circuits are forecast to register a 5.99% CAGR through 2031.

- By material grade, standard FR-4 commanded 48.71% of the FR-4 printed circuit board market size in 2025, while mid-Tg and high-Tg laminates are expanding at a 5.22% CAGR through 2031.

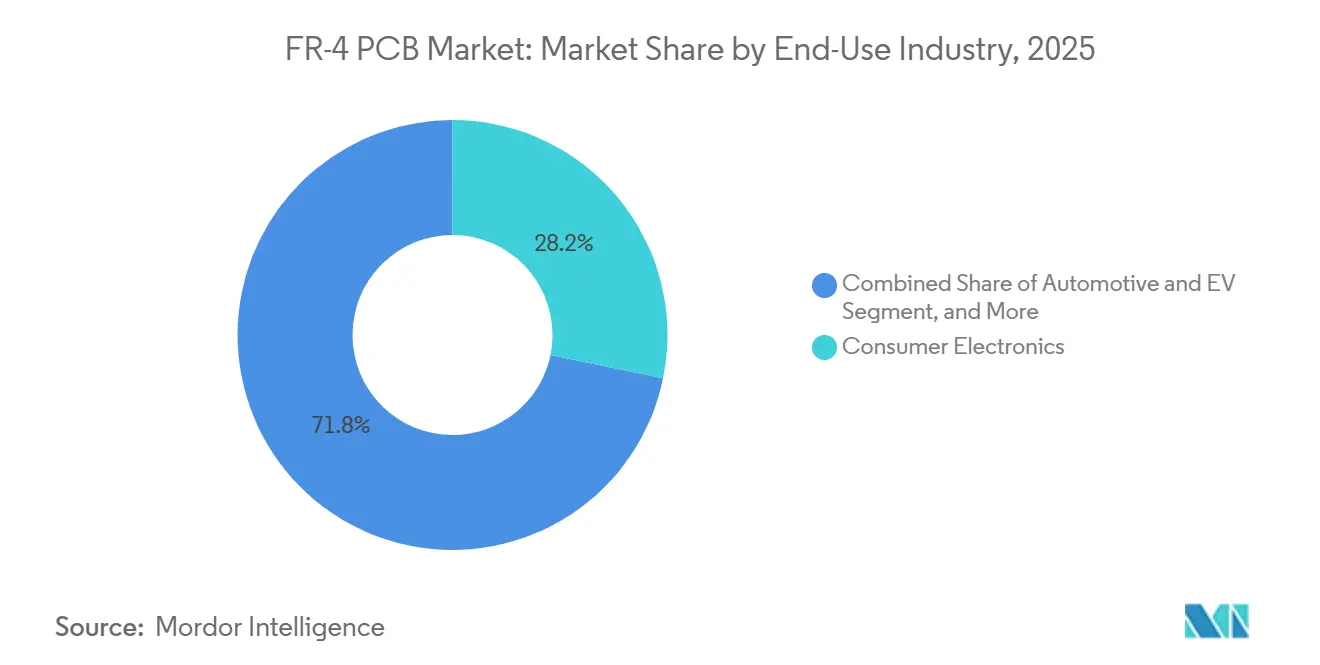

- By end-use industry, consumer electronics led with 28.22% revenue share in 2025, but automotive and EV applications are expected to record a 5.79% CAGR to 2031.

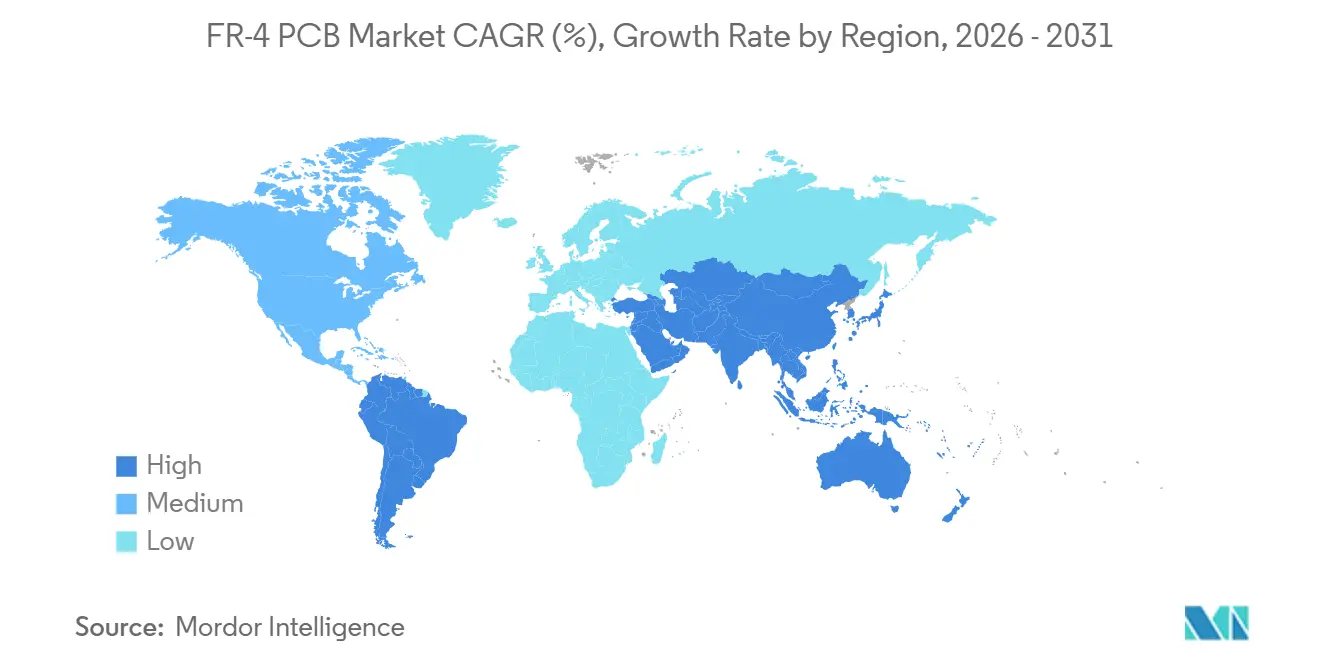

- By geography, Asia-Pacific accounted for 82.54% of the FR-4 printed circuit board market size in 2025 and is progressing at a 6.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global FR-4 PCB Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing miniaturization trend in consumer electronics | +0.80% | Global, with concentration in China, South Korea, Taiwan | Medium term (2-4 years) |

| Accelerating adoption of EV on-board chargers and powertrains | +1.10% | APAC core (China, Japan, South Korea), spillover to Europe and North America | Long term (≥ 4 years) |

| Rapid rollout of 5G base-stations requiring low-loss FR-4 variants | +0.70% | Global, led by China, India, Southeast Asia | Short term (≤ 2 years) |

| Shrinking server motherboard trace widths in hyperscale data centers | +0.90% | North America, Europe, APAC (Singapore, Hong Kong) | Medium term (2-4 years) |

| Government incentives for domestic PCB fabrication in India and Vietnam | +0.60% | India, Vietnam, with indirect effects in Southeast Asia | Long term (≥ 4 years) |

| Novel AI accelerator boards driving multilayer count per device | +0.90% | North America, Taiwan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Miniaturization Trend in Consumer Electronics

Demand for thinner smartphones and wearables has driven a 34% jump in component density since 2022. Flagship devices now carry any-layer HDI boards with microvias only 0.075 millimeters wide, held within a 1.2-millimeter stack height.[1]Apple Inc., “iPhone 16 Technical Specifications,” APPLE.COM Rigid-flex constructions enable glucose monitors to wrap around 3-millimeter radii while maintaining IPC Class 3 reliability. Layer counts in high-end handsets rose from 8 in 2020 to 12 in 2025, lifting average laminate consumption per phone by 22% even as shipment volumes plateaued. As the FR-4 printed circuit board market integrates these HDI designs, mid-Tg formulations with tighter coefficient-of-thermal-expansion control protect solder joints over five-year duty cycles. The result is steady upside for producers that can image sub-50-micron lines without yield loss.

Accelerating Adoption of EV On-Board Chargers and Powertrains

Electric-vehicle power electronics regularly expose boards to 800-volt transients and localized hot spots nearing 175°C. BYD specified high-Tg laminates with decomposition temperatures above 340°C to withstand 3,000 fast-charge cycles in its Blade Battery system.[2]BYD Company, “Investor Presentation 2025,” BYD.COM Infineon’s HybridPACK Drive G2 matches 1.2-kilovolt SiC MOSFETs to 10-layer FR-4 substrates clad with 105-micron copper foil, doubling conventional thickness to dissipate 15 kilowatts. Euro 7 diagnostics effective in July 2025 require voltage sensing within 10 millivolts, tightening trace-spacing rules to 0.05 millimeters. These conditions elevate high-Tg and heavy-copper constructions, securing a growth premium over the broader FR-4 Printed Circuit Board market.

Shrinking Server Motherboard Trace Widths in Hyperscale Data Centers

PCIe Gen5 at 32 gigatransfers per second and AI accelerator traffic force motherboard traces below 0.075 millimeters to curb crosstalk. Intel’s Eagle Stream platform mandates 16-layer sequential laminations that hold impedance skew under 5 picoseconds.[3]Intel Corporation, “Eagle Stream Platform Specifications,” INTEL.COM Meta’s next-generation training clusters will adopt 20-layer boards carrying 1,024 differential pairs each, consuming 40% more laminate per server than prior revisions. Open Compute Project standards add IPC 6012 Class 3A and lead-free finishes, lifting fabrication cost but cutting field failures by 60%. These requirements accelerate volume for fabricators that can deliver sub-75-micron line widths at scale.

Novel AI Accelerator Boards Driving Multilayer Count Per Device

Training clusters for large language models now deploy baseboards with 24-28 copper layers dispersing 1,200 watts across 800-square-millimeter GPU dies. NVIDIA’s GB200 NVL72 baseboard carries 6-ounce copper planes to handle 15,000-ampere peaks without exceeding an 85°C rise.[4]NVIDIA Corporation, “GTC 2025 Keynote,” NVIDIA.COM Google’s TPU v6 uses sequential build-up on high-Tg cores to route 2,048 differential pairs while holding insertion loss below 1.5 decibels at 56 gigahertz. As the FR-4 Printed Circuit Board market aligns with AI hardware roadmaps, ultra-high-layer-count demand boosts average selling price fourfold over a standard 8-layer product.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply insecurity of high-Tg glass yarns | -0.70% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Rising sustainability pressure versus halogen-rich epoxy chemistries | -0.50% | Europe, North America, spillover to APAC | Medium term (2-4 years) |

| Intensifying price competition from polyimide and metal-core PCBs | -0.40% | Automotive and industrial segments globally | Long term (≥ 4 years) |

| US-China tech decoupling complicating global sourcing | -0.60% | North America, Europe, indirect effects in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Insecurity of High-Tg Glass Yarns

Only three qualified producers supply alkali-resistant E-glass yarns able to maintain 0.02%-dimensional stability over 10,000 cycles. A fire at Jushi’s Tongxiang plant removed 12% of global capacity for nine weeks in early 2025, doubling modified-epoxy lead times to 16 weeks. OEMs air-freighted yarn from Owens Corning’s South Carolina site at quadruple normal cost. Automotive Tier-1 suppliers now hold 12-week buffer stock and pay a 6% premium for dual-sourced high-Tg laminates, tempering near-term volume elasticity in the FR-4 PCB market.

US-China Tech Decoupling Complicating Global Sourcing

Washington added 140 Chinese electronics entities to the Entity List in October 2024, compelling North American OEMs to dual-source laminates outside the People’s Republic even at a 22% bill-of-materials penalty. Taiwan Semiconductor Manufacturing Company pre-qualified seven alternative vendors for its Arizona plant, benefitting second-tier fabricators in Malaysia, Thailand, and Mexico. The geopolitical divide raises logistics complexity and working capital needs, subtracting 0.6 percentage points from the global CAGR forecast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: HDI And Rigid-Flex Capture Premium Niches

The FR-4 PCB market size for standard multilayer non-HDI product stood at USD 12.11 billion in 2025, translating to 26.87% of global revenue. Price-sensitive consumer devices and industrial controls continue to tolerate 0.15-millimeter lines and 0.3-millimeter through-hole vias. Yet flexible circuits are expanding at a 5.99% CAGR, a 148-basis-point uplift over the broader FR-4 printed circuit board market, as foldable phones and medical wearables demand 3-millimeter bend radii without delamination. HDI boards exceed 200 conductors per square inch, finding particular traction in AI accelerator modules and millimeter-wave radios. Rigid-flex designs, though lower in volume, remain indispensable for aerospace and defense contracts that specify IPC-6013 Class 3 endurance against 2,000 G shocks. One- and two-sided boards continue to exist in commodity lighting and power-supply niches as even low-cost appliances migrate to 4-layer layouts to satisfy stricter FCC radiated-emission rules. Heavy-copper FR-4 supports solar inverters and motor drives where trace current density reaches 10 amperes per square millimeter, commanding a threefold price premium over baseline laminates.

Demand elasticity differs sharply across types. HDI and rigid-flex orders carry cycle times of five to seven days in Taiwan and South Korea, reinforcing the competitive advantage of fabricators that invested early in laser-direct-imaging and automated optical inspection. Samsung Electro-Mechanics recorded a 34% year-over-year jump in rigid-flex shipments in 2025 as automotive head-up displays integrated flexible tails within tight instrument clusters. Meanwhile, Chinese quick-turn shops quote two-day prototype cycles for commodity eight-layer boards, driving 8-12% annual price erosion. As complexity rises, the FR-4 printed circuit board market share of high-layer-count product will continue to edge up at the expense of legacy double-sided formats.

By Material Grade: Mid-Tg and High-Tg Gain on Automotive Demand

Standard FR-4 held 48.71% of 2025 shipment volume, underpinning consumer electronics that rarely exceed 85°C ambient. However, mid-Tg and high-Tg laminates are growing at a 5.22% CAGR, outpacing the FR-4 printed circuit board market by 71 basis points as electric vehicles, on-board chargers, and industrial drives cycle between -40°C and 150°C. High-Tg formulations combine phenolic hardeners with dicyandiamide-cured epoxy to raise decomposition temperature to 340°C, enabling 260°C lead-free reflow without Z-axis expansion. European Union RoHS revisions effective January 2025 limit brominated flame retardants to 0.1% by weight, stimulating demand for halogen-free FR-4 despite its 15-20% price premium and 20% higher moisture absorption.

Automotive procurement rules now classify mid-Tg as the default grade for any board within 30 centimeters of a powertrain module, a standard Bosch formalized in March 2025. Aerospace and medical designers still hesitate to switch away from brominated variants because halogen-free laminates exhibit lower flexural strength. Material suppliers respond with hybrid chemistries: Isola’s Astra MT77 achieved UL 94 V-0 at 0.8-millimeter thickness by adding aluminium trihydrate fillers, though its higher dielectric constant slows signal propagation and excludes it from PCIe Gen5 and DDR5 interfaces. Over the forecast period, high-Tg shipments will capture incremental FR-4 PCB market size equal to USD 3 billion, primarily in automotive inverter and on-board charger assemblies.

By End-Use Industry: Automotive and EV Outpace Consumer Electronics

Consumer electronics delivered 28.00% of 2025 revenue, yet growth moderates as smartphone volumes level off. Automotive and electric-vehicle electronics, in contrast, are on a 5.79% CAGR trajectory, 128 basis points ahead of the overall FR-4 printed circuit board market. Silicon-carbide MOSFETs produce 30% more heat per square centimeter, demanding heavy-copper and high-Tg laminates. Tesla’s 4680 battery-management board integrates 12-layer rigid-flex panels that fold around cylindrical cells, shaving 25% pack volume. Computing and data-center demand remains solid as hyperscale operators shift to 24-layer motherboards supporting PCIe Gen5, while 5G base-station rollouts require low-loss FR-4 with tangent-delta below 0.008 at 24 gigahertz.

Industrial automation also extends its share. Wide-bandgap drives switch at 100 kilohertz versus 20 kilohertz for silicon, raising partial-discharge risk and necessitating mid-Tg cores with enhanced resin bleed control. Healthcare boards, though smaller in volume, command 40% gross margins due to FDA design-control requirements and IPC-6012 Class 3 qualification. Aerospace and defense programs remain niche but lucrative, requiring Kevlar-reinforced FR-4 to survive minus-55°C to 125°C and 2,000 G shocks. Across sectors, high-reliability niches preserve margin even as commodity consumer electronics face persistent price pressure.

Geography Analysis

Asia-Pacific anchored 82.54% of 2025 revenue and is on a 6.25% CAGR path through 2031. China supplied 58% of global capacity, yet India’s Production Linked Incentive outlays of INR 550 billion (USD 6.6 billion) and Vietnam’s USD 3.2 billion of 2025 investment signal a southward migration of cost-competitive volume. Taiwan preserves technology leadership with 22% of HDI capacity, serving Apple, NVIDIA, and AMD on 48-hour prototype cycles. Japan focuses on automotive and industrial jobs where zero-defect rates justify 30% price premiums.

North America and Europe combined for 17.46% of revenue in 2025 but benefit from reshoring. TTM Technologies doubled its Syracuse, New York, ITAR-compliant footprint in November 2025 to serve defense primes. AT&S added 24-layer HDI lines in Leoben, Austria, to chase 800-volt electric-vehicle contracts. Mexico’s Guadalajara corridor grew PCB output 18% in 2025 as automotive OEMs nearshored procurement from Asia. South America remains a net importer despite Brazil’s Lei de Informática incentives.

Geopolitical risk reshapes sourcing. The US-China tech split forces dual-sourcing outside the People’s Republic, lifting Malaysian, Thai, and Mexican share by 2026. European buyers favour in-region fabrication to comply with carbon-border-adjustment rules effective 2026. Meanwhile, lead times for prototypes in India dropped from 21 days in 2023 to 12 days by late 2025, narrowing the service gap with Taiwanese peers. Over the forecast horizon, the Asia-Pacific share of the FR-4 Printed Circuit Board market will ease modestly as regional diversification continues.

Competitive Landscape

The top five fabricators AT&S, TTM Technologies, Unimicron, Tripod Technology, and Kingboard controlled 38% of 2025 revenue, leaving a long tail of more than 200 regional specialists. Commodity multilayer boards face 8-12% annual price erosion due to aggressive Chinese and Taiwanese automation, whereas aerospace, defense, and automotive boards retain 25-35% margins because IPC Class 3 and IATF 16949 audits deter new entrants. Unimicron’s March 2025 purchase of a 30% stake in Elite Material secures high-Tg resin streams, exemplifying vertical integration moves.

Ultra-high-layer-count boards for AI clusters, priced at USD 800-1,200 per square meter, offer the richest white space. AT&S filed 14 patents covering laser-direct-structuring that removes photolithography steps, and Ibiden unveiled epoxy blends that cut CTE mismatch to 8 parts per million per degree Celsius. Quick-turn specialists like NCAB Group and Advanced Circuits capture 12% of the North American prototype niche by delivering 24-hour cycles and automated design-rule checking. Still, only 40% of Asia-Pacific plants hold IATF 16949, protecting incumbents that already serve EV powertrains.

Geographic hedging is the dominant strategy. Jabil shifted 20% of rigid-flex capacity from Wuxi to Penang in September 2025 to meet customer diversification mandates. Kingboard took a 60% stake in Vietnamese fabricator Elec and Eltek in October 2025, adding 150,000 square meters of capacity in Bac Ninh. These moves confirm that proximity and political alignment now outweigh marginal labour savings in sourcing decisions.

FR-4 PCB Industry Leaders

Unimicron Technology Corp.

Zhen Ding Technology Holding Ltd.

ATandS AG

Tripod Technology Corp.

TTM Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron committed TWD 18 billion (USD 565 million) to expand HDI capacity in Taoyuan, targeting AI accelerator and automotive powertrain boards with first output in Q3 2027.

- December 2025: AT&S completed a EUR 500 million (USD 565 million) clean-room expansion in Leoben, Austria, adding 18-layer and 24-layer HDI lines for European EV customers.

- November 2025: TTM Technologies opened a 180,000-square-foot addition in Syracuse, New York, doubling ITAR-compliant capacity for aerospace and defense boards.

- October 2025: Kingboard acquired a 60% stake in Vietnam-based Elec and Eltek for USD 85 million, adding 150,000 square meters of annual capacity in Bac Ninh.

Global FR-4 PCB Market Report Scope

The Global FR-4 Printed Circuit Board Market Report is Segmented by Type (Standard Multilayer, 1-2 Sided, HDI, Rigid-Flex, Other Types), Material Grade (Standard FR-4, Mid-Tg FR-4, High-Tg FR-4, Halogen-Free FR-4), End-Use Industry (Consumer Electronics, Computing and Data Centers, Telecommunications, Automotive and EV, Industrial and Power, Healthcare/Medical, Aerospace and Defense, Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) Rigid |

| 1-2 Sided |

| High-Density Interconnect (HDI) |

| Rigid-Flex |

| Other PCB Type |

| Standard FR-4 (Tg 130°C-140°C) |

| Mid-Tg FR-4 (Tg 150°C-160°C) |

| High-Tg FR-4 (Tg 170°C+) |

| Halogen-Free FR-4 |

| Consumer Electronics |

| Computing and Data Centres |

| Telecommunications |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-User Industries |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Taiwan | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Standard Multilayer (non-HDI) Rigid | |

| 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Rigid-Flex | ||

| Other PCB Type | ||

| By Material Grade | Standard FR-4 (Tg 130°C-140°C) | |

| Mid-Tg FR-4 (Tg 150°C-160°C) | ||

| High-Tg FR-4 (Tg 170°C+) | ||

| Halogen-Free FR-4 | ||

| By End-Use Industry | Consumer Electronics | |

| Computing and Data Centres | ||

| Telecommunications | ||

| Automotive and EV | ||

| Industrial and Power | ||

| Healthcare / Medical | ||

| Aerospace and Defense | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Taiwan | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

How large is the FR-4 Printed Circuit Board Market in 2026?

The FR-4 Printed Circuit Board Market size reached USD 45.02 billion in 2026.

What is the expected growth rate for FR-4 PCB demand through 2031?

The market is forecast to post a 4.51% CAGR, lifting value to USD 56.14 billion by 2031.

Which region leads global FR-4 Printed Circuit Board Market production?

Asia-Pacific delivered 82.54% of 2025 revenue and continues to expand fastest at a 6.25% CAGR.

Which end-use sector will grow quickest?

Automotive and electric-vehicle electronics are set to rise at a 5.79% CAGR through 2031.

Why are high-Tg laminates gaining share?

High-Tg laminates withstand 150-°C automotive cycles and 260-°C lead-free reflow, supporting EV powertrains and AI servers.

What supply-chain risk most affects Printed Circuit Board Market fabricators?

Limited suppliers of high-Tg glass yarns create bottlenecks, as shown when a February 2025 fire doubled lead times to 16 weeks.

Page last updated on: