Foundry Consumables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.24 Billion |

| Market Size (2031) | USD 10.76 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

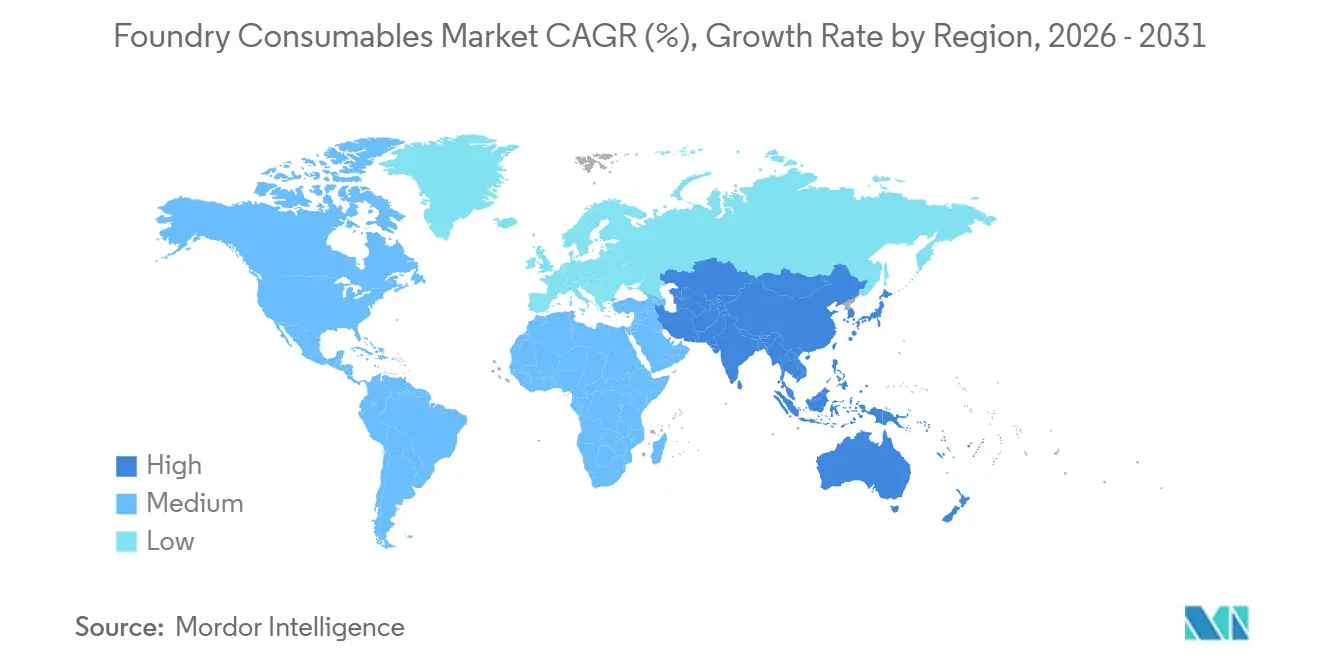

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foundry Consumables Market Analysis by Mordor Intelligence

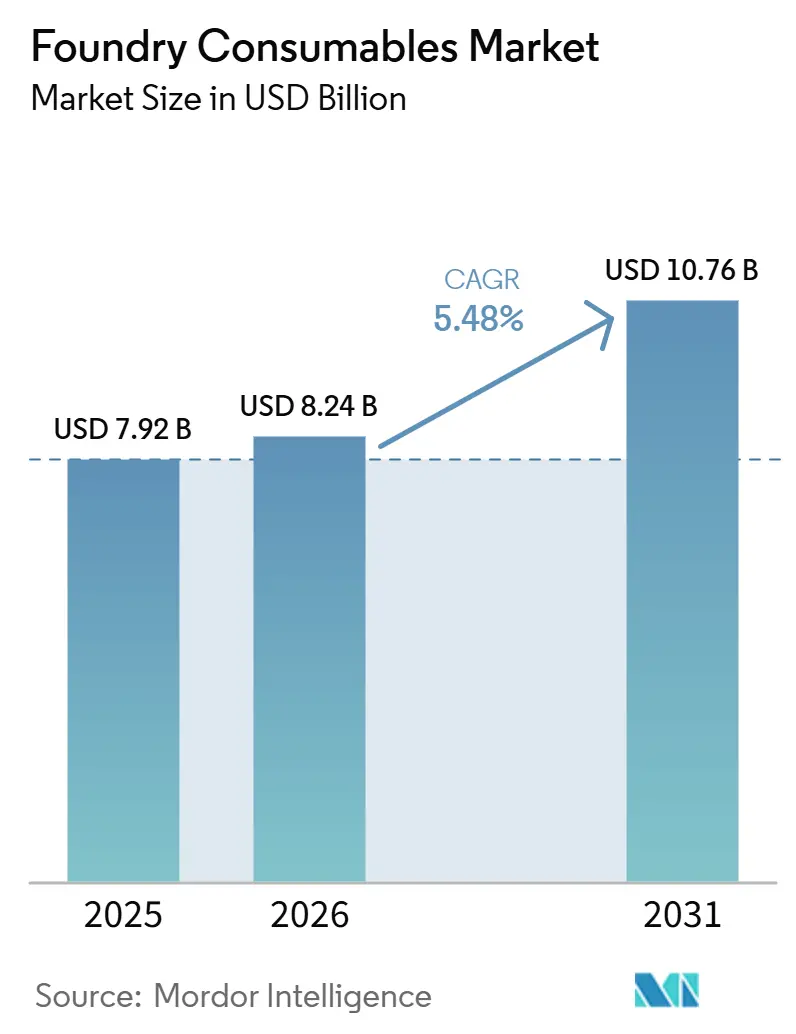

The foundry consumables market size is expected to increase from USD 7.92 billion in 2025 to USD 8.24 billion in 2026 and reach USD 10.76 billion by 2031, growing at a CAGR of 5.48% over 2026-2031. Growing orders for ductile-iron pipe in global infrastructure programs and the rapid adoption of high-pressure die-cast aluminum parts in electric vehicles are changing purchasing patterns toward cleaner binders, specialty sands, and zircon-alternative coatings. Bentonite-based engineering sand remains the volume anchor, but resin-coated sand and advanced foundry coatings are scaling quickly as foundries chase tighter dimensional tolerances and lower emissions. Asia-Pacific’s weight in the foundry consumables market reached almost half of global revenue in 2025, and the region is adding the most value thanks to India’s low-cost bentonite exports and China’s push for greener casting resins. Competitive pressure from Chinese fused-alumina and phenolic-resin suppliers is compressing margins for long-established Western vendors, prompting a pivot toward ultra-high-purity ceramics, bio-based binders, and digital sand-management platforms. Even so, sustained infrastructure spending, lightweighting in mobility, and automation in core-making keep the demand outlook positive across all major geographies.

Key Report Takeaways

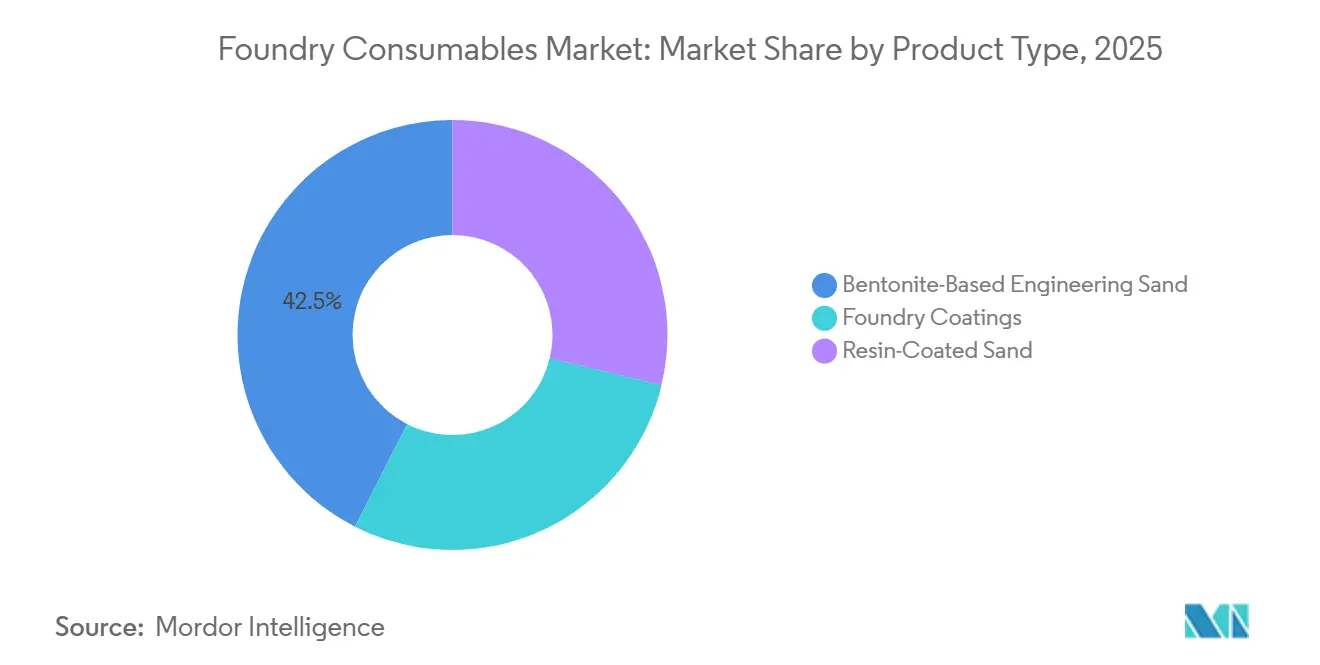

- By product type, bentonite-based engineering sand held 42.51% of the foundry consumables market share in 2025, while foundry coatings posted the fastest 6.81% CAGR during the forecast period (2026-2031).

- By end-user application, automotive foundries accounted for 35.67% of revenue in 2025; pipes and fittings recorded the highest 6.62% CAGR during the forecast period (2026-2031).

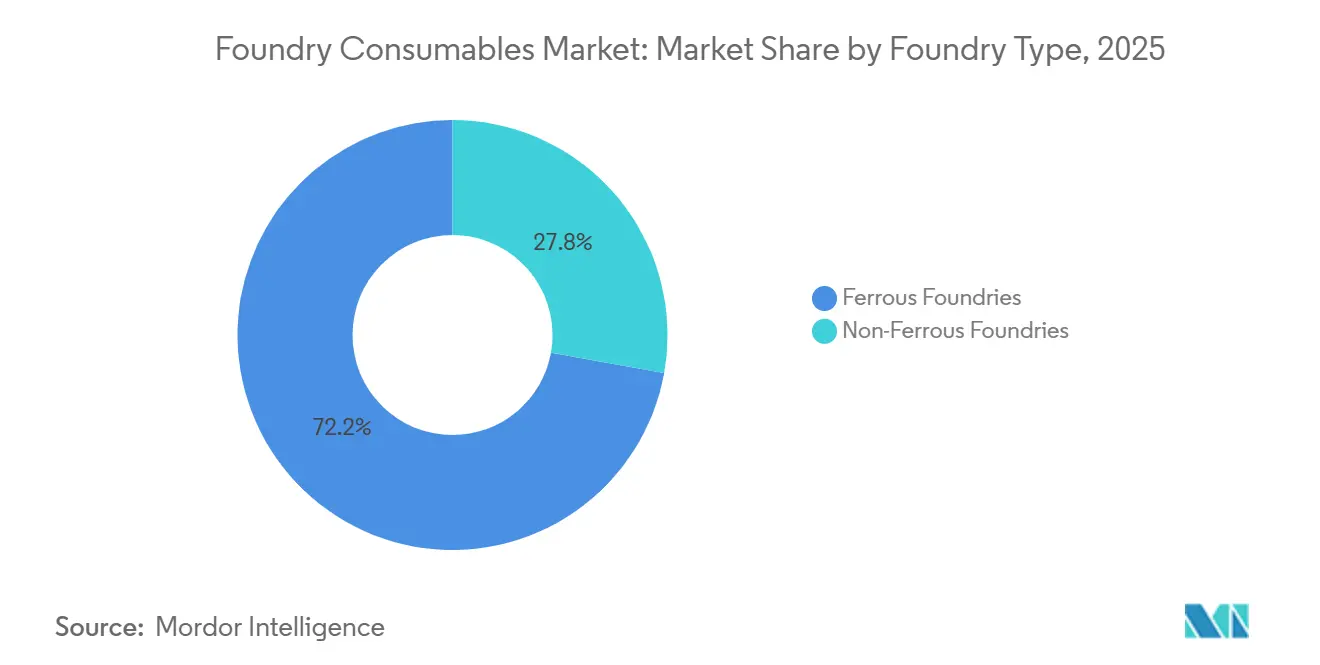

- By foundry type, ferrous operations commanded 72.18% of the foundry consumables market size in 2025, and non-ferrous foundries are expected to expand at a 6.37% CAGR between 2026 and 2031.

- By geography, Asia-Pacific accounted for 48.24% of 2025 revenue and is set to grow at a 5.93% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Foundry Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing foundry output propelled by global infrastructure spending | +1.20% | Global, with a concentration in Asia-Pacific and the Middle-East | Medium term (2-4 years) |

| Cost-competitive India-sourced bentonite, coatings and additives in SEA markets | +0.80% | Asia-Pacific (India, Southeast Asia) | Short term (≤ 2 years) |

| Shift to high-pressure die and investment casting boosts resin-coated sand demand | +1.00% | Global, led by North America, Europe, and China | Medium term (2-4 years) |

| Lightweight EV and hybrid programs lift non-ferrous consumables penetration | +1.30% | Global, strongest in China, Europe, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Foundry Output Propelled by Global Infrastructure Spending

Ferrous foundries benefit directly from water and wastewater pipe projects that consume high volumes of ductile-iron castings, locking in steady bentonite and coal-dust purchases. Governments in the Middle-East and North Africa are accelerating desalination and irrigation upgrades that rely on corrosion-resistant ductile-iron systems, opening export channels for Indian and Chinese pipe producers that source local bentonite to avoid freight premiums. India’s foundry sector, hosting thousands of plants, continues to ramp ferrous output for pumps, valves, and fittings to meet national infrastructure targets, which lifts demand for low-cost green-sand formulations. Longer furnace campaign times and higher melt rates under large backlogs drive incremental sales of crucible linings and tundish coatings that prolong refractory life and reduce contamination risk. The structural nature of infrastructure budgets gives this driver a multi-year tailwind even if cyclical industries slow.

Cost-Competitive India-Sourced Bentonite, Coatings and Additives in SEA Markets

Customs data show India exported USD 90.79 million of bentonite in 2023 to Indonesia, Malaysia, Vietnam, and Thailand, undercutting Australian or United States grades by 15-20% on delivered cost[1]World Bank, “India Bentonite Exports by Country 2023” . Gujarat-based suppliers are expanding automated blending lines that cut mud content below 0.3%, a threshold essential for resin-sand applications in second-tier automotive castings. Southeast Asian tier-2 suppliers to Japanese OEMs often place price ahead of brand, so Indian phenolic coatings and additives capture share by matching basic performance at materially lower cost. The trade flow backstops India’s own scale-up of mining and milling capacity, reinforcing a virtuous cycle of higher volumes and sharper pricing. For foundries in Indonesia and Vietnam, whose energy tariffs are lower than in Japan or South Korea, cheaper consumables amplify total cost competitiveness, deepening India’s foothold in the region.

Shift to High-Pressure Die and Investment Casting Boosts Resin-Coated Sand Demand

Automotive lightweighting and miniaturized powertrain parts have accelerated the use of high-pressure die casting and lost-wax investment casting that rely on resin-coated sands and ceramic shell systems. A North American investment foundry cut its shell-building sequence from 2-1-4 dips to 1-1-4 after switching to CARBO Ceramics’ alumina-based OPTICAST media, reducing labor, energy, and cycle times while maintaining accuracy. Shell-molding machines equipped with cold-box core systems cure phenolic or furan resins at room temperature, eliminating energy-intensive ovens and improving shop safety, a configuration now standard at Japanese suppliers of turbocharger housings and electric-motor end bells. China has placed ultrafine ceramic powders and advanced resins on its 2025 Catalog for Encouraging Foreign Investment, signaling policy support for domestic production of high-margin consumables that shorten supply lines. Collectively, these shifts accelerate volume growth for high-value coated sands well above traditional green-sand demand.

Lightweight EV and Hybrid Programs Lift Non-Ferrous Consumables Penetration

Battery-electric platforms aim to offset battery mass with large aluminum and magnesium castings, pushing non-ferrous foundries to source consumables able to withstand molten aluminum’s 660-750°C working window without gas pickup. Tesla-style gigacasting consolidates multiple stampings into single aluminum structures, demanding coatings with superior anti-sticking and thermal-shock resistance to protect tools and molds. Vesuvius’ 2025 purchase of Molten Metal Systems added degassing, filtration, and dosing technologies critical for aluminum melt quality, underlining the vendor's appetite to broaden non-ferrous portfolios. Magnesium die-casting for seat frames and battery enclosures requires sulfur-free coatings and inert-atmosphere handling, creating premium opportunities for boron-nitride release agents. As more automakers roll out gigacasting lines in Europe and China, the volume of resin-coated sand and specialty coatings consumed by non-ferrous foundries will continue to climb faster than ferrous grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility for bentonite, phenolic resins, and specialty minerals | -0.60% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Import competition in premium coatings and specialty sands | -0.40% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility for Bentonite, Phenolic Resins, and Specialty Minerals

Free on Board (FOB) Tianjin bentonite prices edged higher in late 2025 as port congestion and delayed rail dispatches from Inner Mongolia tightened spot supply despite steady mine output. Phenolic resin costs diverged sharply across regions when crude-phenol feedstock prices and power tariffs spiked in the United States but stayed muted in Indonesia, widening landed-cost gaps. Foundries that operate on slim 3%-5% net margins face a dilemma: absorb input increases or downgrade to lower-grade sands that elevate scrap rates. Zircon sand shortages after Australian mine closures in 2024-2025 forced many investment casters to trial OPTICAST alumina media, illustrating how sudden price moves can catalyze rapid material substitution. While vertically integrated players such as Imerys hedge raw-material swings, smaller distributors simply pass costs through, discouraging new-product trials and delaying capacity expansions.

Import Competition in Premium Coatings and Specialty Sands

Chinese suppliers offer 20%-30% price discounts on fused alumina, zircon flour, and phenolic coatings, denting North American and European sales of Western incumbents. Imerys booked a EUR 467 million (USD 510 million) goodwill impairment in 2025, attributing the charge to “substantially more difficult market conditions and competitive pressure from Chinese producers” despite EU anti-dumping duties that took effect on January 16, 2026[2]Imerys, “FY 2025 Press Release” . The speed with which ISO 9001-qualified Chinese zircon flour penetrated European investment casting shows how quickly price-led imports can erode share in commodity-grade materials. Japanese bentonite producers in Shimane and Okayama prefectures protect domestic share through low-impurity, high-viscosity grades, but freight costs restrict them from competing across Southeast Asia, where Indian cargoes dominate. Mid-tier Western suppliers that lack the scale for research and development on low-volatile organic compound (VOC) binders or automated dosing systems see margins compress and risk strategic withdrawal from undifferentiated product lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coatings Lead Innovation, Bentonite Anchors Volume

Bentonite-based engineering sand contributed a 42.51% foundry consumables market share in 2025 and underpins high-volume ferrous molding because it delivers wet strength and collapsibility at the lowest cost. The segment’s entrenched position keeps the foundry consumables market firmly linked to global mining output in Gujarat, Inner Mongolia, and Xinjiang, yet coatings are the fastest-rising line, growing at a 6.81% CAGR from 2026 to 2031. In absolute terms, coatings add the most value where electric-vehicle, aerospace, and medical castings demand zircon-alternative refractories and low-volatile organic compounds chemistries. CARBO Ceramics Inc.'s OPTICAST alumina media cut shell-building cycles at a United States investment foundry, validating premium pricing for predictability and throughput gains. Resin-coated sand sits between the two extremes, favored for complex automotive cores that need better dimensional precision than green sand but at lower cost than ceramic shell systems. Chinese producers are marketing low-residue phenolic resins that drop addition rates from 5% to 3% while keeping tensile strength double the ZBG39005-89 benchmark, a move that trims gas evolution and hard-cost per ton.

Coatings attract disproportionate research and development because regulatory limits on VOCs tighten annually in Europe and North America. India’s bentonite exporters funded micronization upgrades during 2025 to lift product consistency and open premium grades for export, bolstering long-run bentonite volume. Japan’s shell-molding sector favors phenolic cold-box systems cured with amine gas at ambient temperature, a setup that eliminates ovens and lowers total energy bills. As China promotes ultrafine SiC and Al₂O₃ powders for investment casting, indigenous suppliers will seize higher-margin niches, altering price points worldwide. Overall, while bentonite sustains tonnage leadership, coatings and resin-coated sand will capture most incremental revenue as precision casting expands in mobility and infrastructure components.

By End-User Application: Pipes Outpace Automotive in Growth Velocity

Automotive foundries delivered 35.67% of 2025 revenue, anchored in cylinder blocks, suspension members, and e-drive housings, but pipes and fittings are the fastest-growing consumer at 6.62% CAGR from 2026 to 2031 on the back of global water and wastewater upgrades. Large-diameter ductile-iron mains specified for desalination and municipal networks in the Middle-East drive bulk tonnage that translates directly into bentonite and coal-dust orders. Automotive volumes are more cyclical and face a composition shift away from ferrous engine castings toward larger aluminum structural pieces for electric vehicle (EV) crash management. That move increases non-ferrous consumables intensity and cycles out some green-sand demand while adding resin-coated sand and high-temperature coatings.

Industrial machinery, power generation, and railways provide a stable mid-tier in line with capital-equipment replacements. Rail demand rises in India and China under high-speed and freight-corridor projects that require fatigue-resistant wheelsets and brake shoes cast to tight tolerances, sustaining orders for specialty coatings. Sanitary castings remain niche yet deliver high margins thanks to premium enamel surfaces and batch production that justifies lost-wax or shell molds. Overall, the diverging growth curves between infrastructure pipe and mature automotive segments diversify revenue streams and guard the foundry consumables market from single-sector dependency.

By Foundry Type: Non-Ferrous Gains Share Despite Ferrous Dominance

Ferrous foundries commanded a dominant 72.18% slice of the foundry consumables market size in 2025, but non-ferrous plants expand at 6.37% CAGR from 2026 to 2031, propelled by aluminum and magnesium giga casting. Ferrous shops prioritize low-cost bentonite blends and graphite coatings suited to green-sand loops handling ductile-iron pipes, brake rotors, and pump housings. Non-ferrous sites need resin-coated sands, boron-nitride release agents, and silicon-carbide coatings to manage molten aluminum reactivity and mitigate die erosion on ultra-large presses. Vesuvius’ GBP 92.7 million (USD 118 million) purchase of Molten Metal Systems signals the strategic premium vendors place on aluminum filtration and degassing technology. Tesla-style giga casting lines in Europe and China triple consumables value per vehicle relative to traditional die cast parts because each shot involves larger surface areas and longer solidification windows.

Magnesium die-casting remains smaller than aluminum but drives outsized innovation in sulfur-free coatings and inert-gas handling, areas where Japanese and German suppliers hold technical leads. Cross-segment technologies such as 3D-printed ceramic cores, boosted by SINTOKOGIO’s 2026 acquisition of Bosch Advanced Ceramics, blur the boundary between ferrous and non-ferrous segments, creating new addressable pockets in turbine blades and aerospace housings. As regulatory pressures reward lighter, more efficient components, non-ferrous foundries will continue to chip away at ferrous share, raising the average value-per-ton of consumables sold.

Geography Analysis

Asia-Pacific generated 48.24% of the worldwide foundry consumables market revenue in 2025 and leads growth at a 5.93% CAGR from 2026 to 2031. India’s bentonite exports alone totaled USD 90.79 million in 2023, feeding Indonesian, Malaysian, Vietnamese, and Thai foundries that prize cost-advantaged supply. China’s 2025 Catalogue for Encouraging Foreign Investment promotes greener casting resins and ultrafine ceramic powders, a stance that secures domestic demand while creating joint-venture opportunities for foreign chemical firms. Japanese suppliers focus on low-volatile organic compound (VOC), high-purity coatings, leveraging decades of automotive core-making know-how. During Q4 2025, bentonite free on board (FOB) Tianjin rose due to logistics delays, underscoring Asia’s influence on global price discovery.

North America, Europe, and South America share the remainder of global revenue. The United States benefits from reshored aerospace and defense investment, casting lines now adopting zircon-alternative alumina media to de-risk supply. EU anti-dumping duties on fused alumina offered partial relief, yet Imerys’ EUR 467 million (USD 510 million) impairment shows how far price pressure from Chinese imports extends even with tariff shields. Mexico’s proximity to U.S. auto plants sustains steady green-sand volumes but limits local mark-ups because Indian bentonite and Chinese coatings enter tariff-free under United States-Mexico-Canada Agreement (USMCA) rules. Brazil, Argentina, and Colombia link growth to cyclical mining and agriculture equipment, creating a more volatile demand profile than North America.

The Middle-East and Africa, though smaller in absolute value, clock above-average gains powered by desalination buildouts and oil-and-gas infrastructure. Saudi Arabia and South Africa imported USD 8.38 million of Indian bentonite in 2023 combined, highlighting how cost-driven procurement supports Indian miners. Local content rules in Gulf Cooperation Council states incentivize joint ventures that establish regional blending plants, reducing exposure to long transit times from Asia. South African foundries, battling electricity shortages, invest in in-house resin dosing to control quality and lessen reliance on imports, a trend likely to replicate in other power-constrained African markets. Collectively, regional diversification shields the foundry consumables market from localized downturns and supports a balanced global expansion.

Competitive Landscape

The Foundry Consumables Market is moderately fragmented. Chinese phenolic-resin producers win business by reducing binder addition without sacrificing strength, a feature prized by foundries chasing lower gas evolution and better surface finish. Western mid-tier vendors lacking large research and development budgets are most exposed; many now white-label Asian materials while channeling resources into digital sand analytics that cut scrap and justify service fees.

Foundry Consumables Industry Leaders

ASK Chemicals

Imerys S.A.

Hüttenes-Albertus

SINTOKOGIO, LTD.

Vesuvius

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sintokogio Group strengthened its position in the global foundry consumables market through the acquisition of Bosch Advanced Ceramics. This move enhances their capabilities in delivering advanced solutions to the foundry consumables market.

- August 2025: Vesuvius acquired Molten Metal Systems from Morgan Advanced Materials for GBP 92.7 million (USD 118 million), adding degassing, filtration, and dosing technologies that strengthen its non-ferrous consumables portfolio.

Global Foundry Consumables Market Report Scope

Foundry consumables are materials and products used in metal casting processes to support molding, melting, and finishing operations. They include items like refractories, filters, binders, coatings, sleeves, and exothermic or insulating materials. These consumables ensure quality casting, reduce defects, improve efficiency, and extend equipment life.

The Foundry Consumables Market is segmented by product type, end-user application, foundry type, and geography. By product type, the market is segmented into bentonite-based engineering sand, resin-coated sand, and foundry coatings. By end-user application, the market is segmented into automotive foundries, industrial machinery, pipes and fittings, automotive equipment, power generation, railways, sanitary castings, and other end-user applications. By foundry type, the market is segmented into ferrous foundries and non-ferrous foundries. The report also covers the market size and forecasts for the Foundry Consumables Market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Bentonite-Based Engineering Sand |

| Resin-Coated Sand |

| Foundry Coatings |

| Automotive Foundries |

| Industrial Machinery |

| Pipes and Fittings |

| Automotive Equipment |

| Power Generation |

| Railways |

| Sanitary Castings |

| Other End-user Applications |

| Ferrous Foundries |

| Non-Ferrous Foundries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Bentonite-Based Engineering Sand | |

| Resin-Coated Sand | ||

| Foundry Coatings | ||

| By End-User Application | Automotive Foundries | |

| Industrial Machinery | ||

| Pipes and Fittings | ||

| Automotive Equipment | ||

| Power Generation | ||

| Railways | ||

| Sanitary Castings | ||

| Other End-user Applications | ||

| By Foundry Type | Ferrous Foundries | |

| Non-Ferrous Foundries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the foundry consumables market?

The foundry consumables market stands at USD 8.24 billion in 2026 and is forecast to reach USD 10.76 billion by 2031 at a 5.48% CAGR from 2026 to 2031.

Which product category is expanding the quickest?

Foundry coatings lead growth at a 6.81% CAGR between 2026 and 2031as investment casting and die-cast processes adopt low-VOC, zircon-free formulations.

Why are non-ferrous foundries gaining momentum?

Aluminum and magnesium giga casting for electric vehicles elevate non-ferrous output and drive consumables needs for high-temperature, anti-reactive coatings.

What competitive challenges face traditional suppliers?

Margin pressure from lower-cost Chinese fused-alumina and phenolic-resin imports is forcing Western incumbents to pivot toward premium ceramics and digital services.

Page last updated on: