Athletic Footwear Sole Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

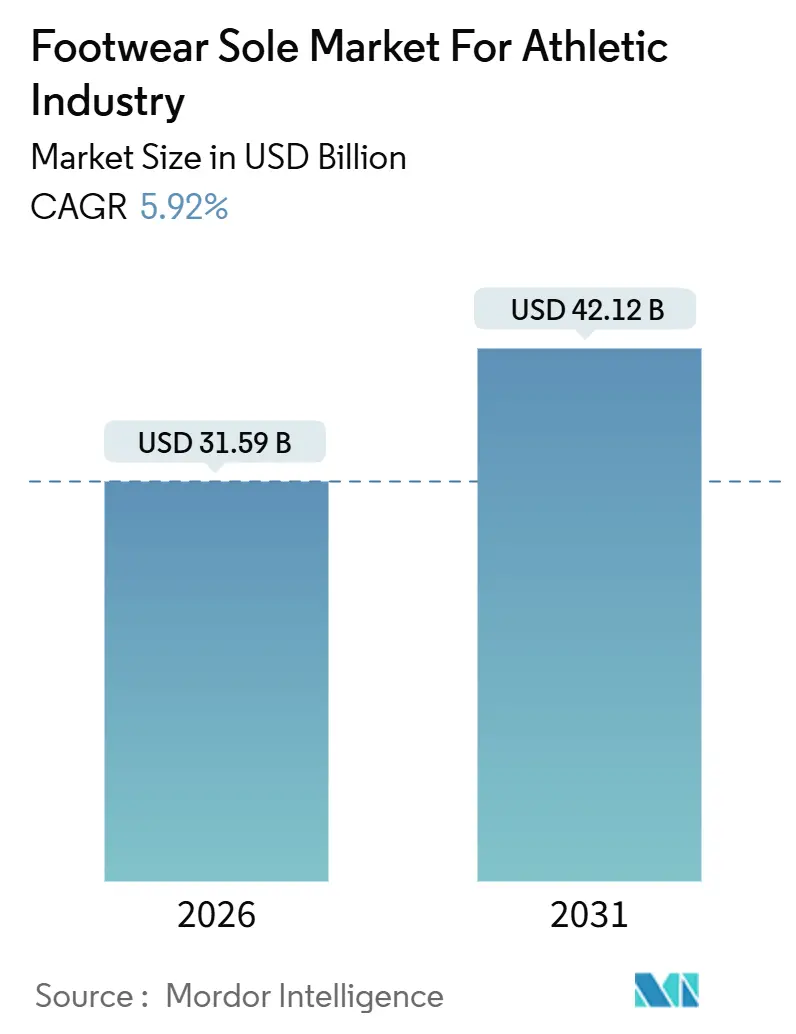

| Market Size (2026) | USD 31.59 Billion |

| Market Size (2031) | USD 42.12 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Athletic Footwear Sole Market Analysis by Mordor Intelligence

The Athletic Footwear Sole Market is expected to grow from USD 31.59 billion in 2026 to USD 42.12 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Continuous gains stem from performance-driven compound innovations, stricter sustainability mandates, and the ascent of direct-to-consumer channels that shorten design-to-shelf cycles. Brands now demand lighter midsoles with higher rebound, recyclable or compostable chemistries, and lot sizes that flex with weekly e-commerce drops. Regional micro-factories equipped with automated injection and supercritical-foaming lines are replacing high-volume, single-recipe plants, enabling a cut in inventory days. On the demand side, fast-growing athleisure consumption, youth sports participation, and global marquee tournaments intensify replacement frequency, while regulations such as the EU Ecodesign for Sustainable Products Regulation (2024/1781) push bio-based and recycled polymers into mainstream specifications.

Key Report Takeaways

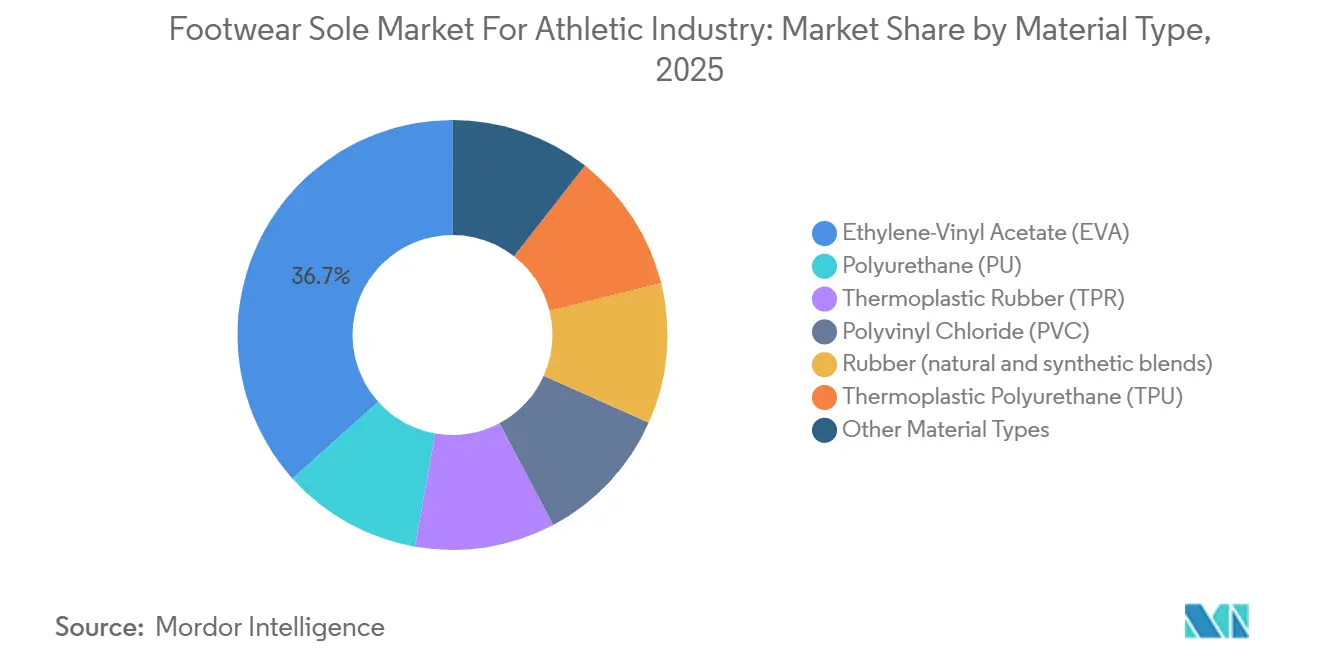

- By material type, ethylene-vinyl acetate led with 36.66% of the Footwear Sole Market for the Athletic Industry market share in 2025; polyurethane is forecast to register the fastest 7.57% CAGR through 2031.

- By manufacturing process, injection moulding accounted for 46.58% share of the Footwear Sole Market for the Athletic Industry market size in 2025 and is advancing at a 6.76% CAGR to 2031.

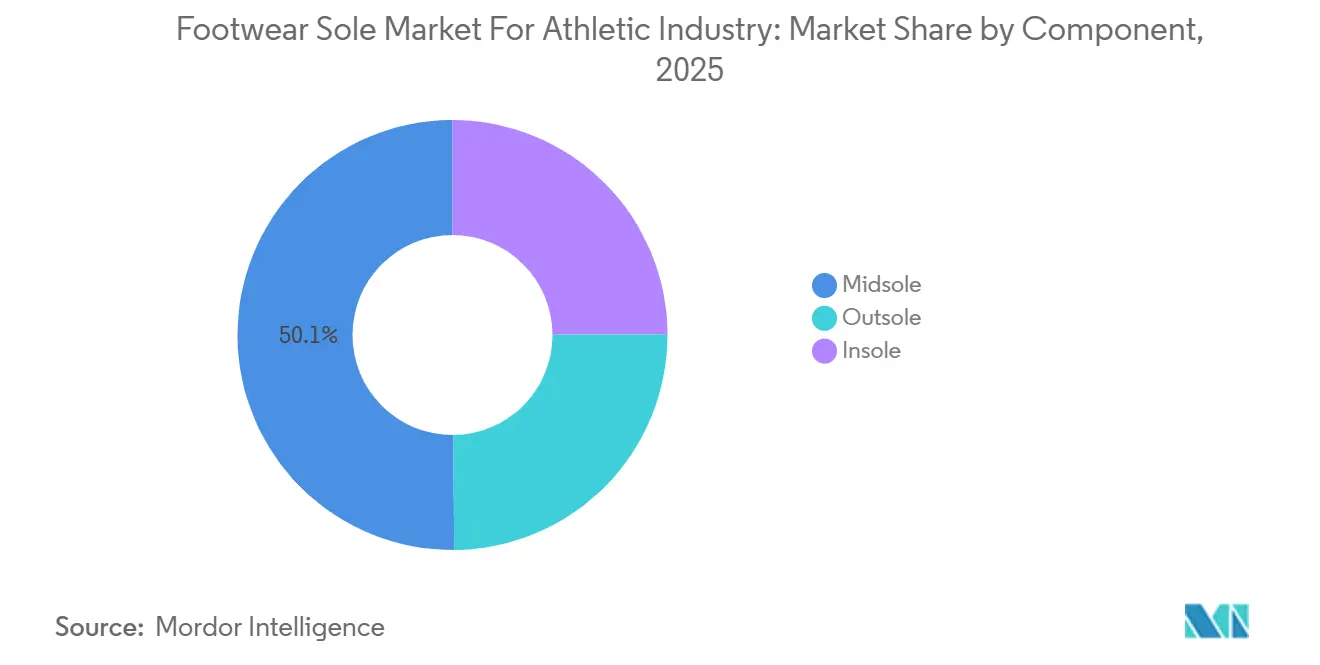

- By component, midsoles captured 50.13% revenue in 2025 and are projected to expand at a 6.78% CAGR to 2031.

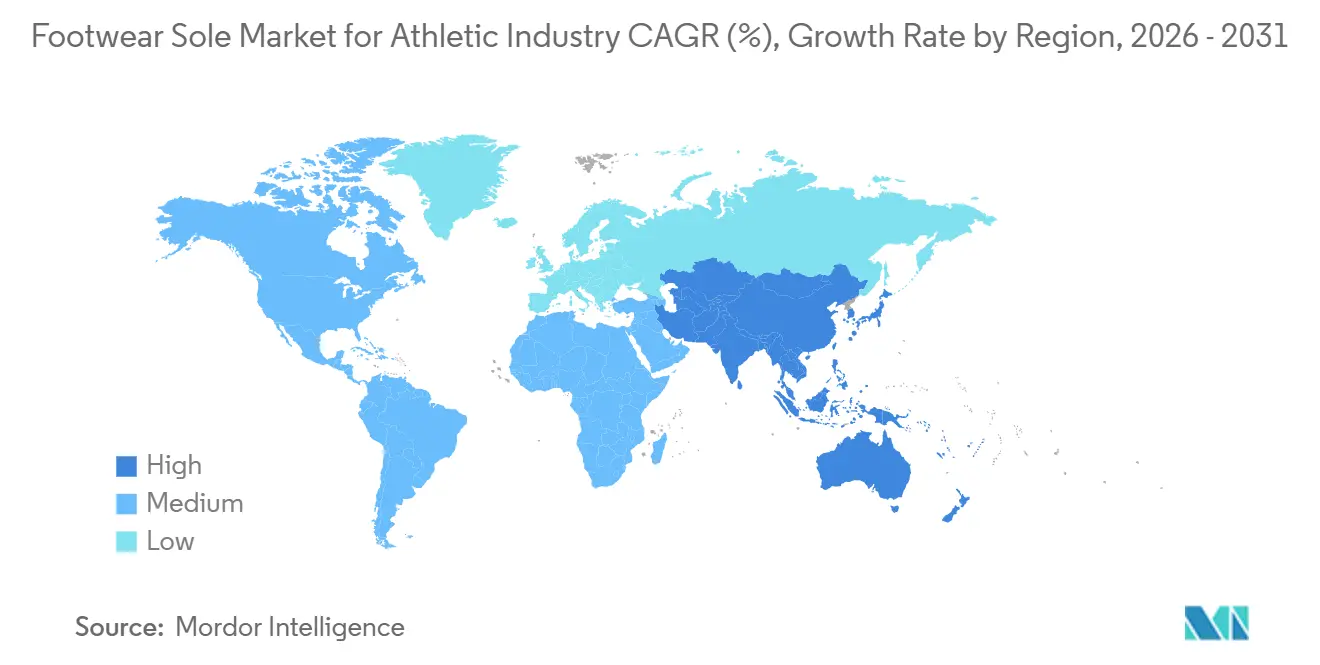

- Asia-Pacific held 49.01% of 2025 revenue and is projected to log the quickest 6.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Athletic Footwear Sole Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing sports participation and upcoming global tournaments | +1.2% | Global, with peak intensity in Europe and North America | Short term (≤ 2 years) |

| Athleisure-led shift to performance-styled casual shoes | +1.5% | North America and EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Online-first retail models accelerating product cycles | +1.0% | Global, led by North America and China | Short term (≤ 2 years) |

| Automated 3D printing and supercritical foaming enabling localized, custom sole production | +0.9% | APAC core (China, Vietnam), spill-over to North America | Long term (≥ 4 years) |

| Adoption of bio-based and recycled polymers to meet ESG scorecards | +1.1% | EU regulatory pressure, North America brand-led, APAC supply | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Sports Participation and Upcoming Global Tournaments

The 2024 Paris Olympics and the 2026 FIFA World Cup have spurred brand campaigns that tie credibility to measurable performance metrics. Retail sell-through data show that running and training shoes with midsoles delivering greater energy return turn twice as fast as lifestyle sneakers, prompting sole producers to prioritize high-rebound foams. Youth enrollment in organized sports rebounded to pre-pandemic levels across North America and Europe, cutting replacement intervals to near six months. These patterns lift OEM orders for midsoles and outsoles well ahead of formal season launches, stabilizing factory utilization during historically slow quarters. Simultaneously, sporting goods retailers allot extra shelf space to footwear certified for sport-specific standards such as ASTM F2913 slip resistance, embedding technical compliance into consumer choice.

Athleisure-Led Shift to Performance-Styled Casual Shoes

Athleisure captured roughly one-third of athletic footwear unit sales in 2025, redefining baseline expectations for cushioning and flexibility in everyday wear. Casual silhouettes now specify dual-density EVA or thin TPU lattices that deliver performance equal to core running models yet fit within 20 mm stack-height limits favored for street styling. The hybrid profile commands higher sole ASPs, a margin that offsets raw-material premiums associated with recycled or bio-content grades. Suppliers have responded with modular tooling that accepts both opaque EVA pellets and transparent TPU without extended downtime, allowing brands to alternate visual effects within the same production window.

Online-First Retail Models Accelerating Product Cycles

In 2024, Nike's digital channels contributed significantly to its revenue, while Adidas saw a smaller share, and On led with the highest percentage. This trend underscores the growing reliance on mobile apps for discovering and purchasing next-gen midsoles. As sell-in windows shorten, economic order quantities have plummeted, favoring plants adept at swiftly swapping molds or CAD files, often within hours. By harnessing predictive analytics, companies are aligning real-time sell-through data with upstream scheduling, effectively reducing excess sole inventory. Factories, now bolstered with collaborative robots and automated color cells, are not only meeting these heightened demands but also ensuring a precision of sub-1 mm dimensional tolerance.

Automated 3D Printing and Supercritical Foaming Enabling Localized, Custom Sole Production

Carbon's Digital Light Synthesis, along with its new supercritical-fluid foaming lines, enables real-time adjustments to lattice geometry or cell size. This innovation tailors cushioning profiles to individual consumer preferences. Adidas, leveraging this technology, prints 4DFWD midsoles in Germany and the U.S., ensuring delivery within 72 hours of order placement. This approach not only sidesteps container shipping but also reduces carbon emissions from finished goods. In North Vietnam, OrthoLite's plant, which began operations in November 2025, harnesses solar energy[1]OrthoLite, “North Vietnam Supercritical Foaming Facility Opens,” ORTHOLITE.COM . Its supercritical-foaming extruders reduce EVA consumption and enhance rebound. These localized production strategies not only cater to consumer demands but also shield brands from freight disruptions and tariff-related risks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit circulation diluting brand equity | -0.8% | Global, concentrated in China and Southeast Asia | Medium term (2-4 years) |

| Tightening global VOC/microplastic regulations on PU and EVA | -0.6% | EU and North America regulatory, APAC compliance | Long term (≥ 4 years) |

| Volatile MDI/TDI feedstock prices post-tariff revisions | -0.7% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit Circulation Diluting Brand Equity

Replica soles produced in Putian frequently mimic visible air pockets and tread geometry yet substitute lower-grade EVA, causing premature compression and rebound loss. Authentication measures—NFC tags and blockchain IDs embedded in insoles—raise unit cost and require consumer education to unlock full effectiveness. Brands continue to lobby customs authorities for expedited destruction protocols, but online marketplaces remain a fast-moving outlet for counterfeit listings.

Tightening Global VOC/Microplastic Regulations on PU and EVA

Effective 2026, the EPA's rule 40 CFR Part 63 Subpart OOOOOO banned the use of methylene chloride in the production of polyurethane foam[2]U.S. Environmental Protection Agency, “40 CFR Part 63 Subpart OOOOOO,” EPA.GOV. This move has compelled factories to retrofit their systems to water- or CO₂-blown methods, which initially deliver lower rebound. Meanwhile, the EU's microplastic action plan has prohibited the intentional addition of micro-particles. As a result, colorants are now shifting from traditional powders to masterbatch pellets. These compliance investments are putting a squeeze on smaller suppliers and driving an acceleration in industry consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyurethane Scaling Faster Than Entrenched EVA

Ethylene-vinyl acetate led with 36.66% of the Footwear Sole Market for the Athletic Industry market share in 2025, and polyurethane is forecast to register the fastest 7.57% CAGR through 2031. This growth is largely attributed to advancements like supercritical foaming, which boosts rebound while reducing mass. Notably, thermoplastic polyurethane grades boasting bio-based content have secured a coveted spot on EU vendor scorecards, driving their swift adoption in premium running lines. While rubber continues to play a dominant role, its growth is tempered by a modest CAGR, a reflection of challenges in high-energy-return compounds. On the other hand, specialty bio-composites like KUORI and Balena BioCir flex, currently holding a small market share, are drawing significant venture capital interest, especially for their promise of closed-loop solutions.

As demand for polyurethane surges, so do investments in its upstream processes. Zotefoams, for instance, has committed to a facility in Vietnam, focusing on scaling nitrogen-infused foam blocks. Similarly, OrthoLite has set aside a substantial amount to boost Cirql capacity. Suppliers tout the advantages of PU, noting its lower compression set, which ensures midsole integrity for over 500 km of running—an alignment with consumer durability demands. Yet, EVA continues to dominate in price-sensitive segments like training and children's footwear. This is bolstered by resin costs that are approximately lower than PU and a widespread familiarity across global contract factories.

By Manufacturing Process: Injection Moulding Retains the Automation Edge

Injection moulding captured 46.58% of the Footwear Sole Market for the Athletic Industry market size in 2025. This success is attributed to its rapid tool changes and cavity pressures, ensuring repeatability. The segment grows at 6.76% on the back of servo-electric presses that shorten cooling time and cut energy use. While compression moulding is vital for lug-rich rubber outsoles, its growth is tempered due to challenges like high tooling costs and long cycle times, which limit its responsiveness. Blow moulding, crucial for producing air bladders, commands a modest market share. However, it's witnessing consistent innovations, particularly with multilayer barriers that effectively delay gas permeation.

Emerging additive-manufacturing lines showcase the potential of on-demand micro-factories. For instance, carbon-printed lattices can be delivered to consumers quickly when produced locally. This not only sidesteps import duties but also reduces carbon emissions compared to ocean freight. Furthermore, regulatory leniency bolsters this process mix: CO₂-blown PU midsoles, compliant with EPA and EU solvent regulations, offer a new lease of life to reactive-foaming cells.

By Component: Midsole Platforms Anchor Brand Storytelling

Midsoles delivered 50.13% of 2025 revenues and are forecast to outpace overall growth at 6.78% CAGR. Energy-return claims, visible foam textures, and co-branded compounds drive willingness to pay, pushing midsole ASPs higher than generic foam. Advances such as OrthoLite Cirql compostable midsoles position brands for upcoming extended-producer-responsibility schemes. Outsoles lag as high-traction rubber already satisfies most performance thresholds. However, recyclate-rich blends unlock EU Green Public Procurement eligibility, ensuring baseline demand. Insoles, traditionally the least differentiated component, gained scale when Coats acquired OrthoLite, integrating thread and insole supply and enabling color-matched drop-in upgrades that lift perceived comfort scores in wear testing.

Geography Analysis

Asia-Pacific contributed 49.01% of the Footwear Sole Market for the Athletic Industry market size in 2025 and is projected to log the quickest 6.99% CAGR to 2031. This dominance was bolstered by Vietnam's export engine and Indonesia's significant output. While brands have shifted from coastal China to ASEAN corridors, drawn by wage arbitrage and trade agreements, Putian has maintained its edge. With its expertise in high-margin supercritical foaming, Putian secures premium orders, boasting material savings. India made significant strides in 2025-2026, highlighted by Hong Fu's inauguration of a facility in Tamil Nadu. This facility underscores the allure of state incentives for large-scale investors.

In North America, the growth is largely attributed to the rise of digital sell-throughs and quick-strike drops. In response to EPA solvent bans, sole manufacturers have localized PU blending close to distribution centers, sidestepping the complexities of cross-border VOC paperwork. Additionally, both big-box and specialty sports retailers have started showcasing carbon scores, pushing suppliers to document bio-content to maintain their shelf presence.

Europe grapples with significant compliance costs, primarily due to the Ecodesign Regulation and microplastic regulations. Factories serving EU brands are making a notable shift towards masterbatch colorants and recycled TPUs. These factories are willing to absorb a premium on raw materials, provided they secure longer-term purchasing contracts. Meanwhile, South America and the Middle East and Africa, though smaller players, hold strategic importance. Brazil caters to Mercosur's demand with a duty-free flow, and Saudi Arabia's 3PL hubs efficiently re-export branded footwear to East Africa within a swift 10-day window, facilitating agile replenishment cycles.

Competitive Landscape

The Footwear Sole Market for the Athletic Industry is moderately consolidated. Major players are increasingly turning to automation. On a different front, niche disruptors KUORI and NFW are venturing into bio-based elastomers, offering pilot volumes at a price premium, a cost deemed acceptable by brands prioritizing circularity. Patent filings reveal that industry giants Skechers, Nike, and Puma are proactively securing their foothold, exploring proprietary foaming and lattice designs to ensure process autonomy ahead of broader market introductions.

Athletic Footwear Sole Industry Leaders

Implus

Feng Tay Enterprises Co., Ltd.

Yue Yuen Industrial (Holdings) Limited

Vibram Corporation

MICHELIN

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Coats signed a definitive agreement to acquire OrthoLite Holdings LLC, positioning the combined business as a super-tier-2 supplier of structural footwear components.

- March 2025: Feng Tay cancelled a planned USD 23 million capital increase for its Nam Ha Footwear unit in Vietnam, citing changes in the operating environment.

Global Athletic Footwear Sole Market Report Scope

The athletic industry's footwear sole market centers on producing and supplying innovative materials—mainly ethylene-vinyl acetate, rubber, and polyurethane. These materials are crucial for the midsoles and outsoles of sports, performance, and athleisure shoes, with a keen emphasis on boosting cushioning, durability, weight reduction, and traction tailored for specific athletic pursuits.

The footwear sole market for the athletic industry is segmented by material type, manufacturing process, component, and geography. By material type, the market is segmented into polyurethane (PU), thermoplastic rubber (TPR), ethylene-vinyl acetate (EVA), polyvinyl chloride (PVC), rubber, thermoplastic polyurethane (TPU), and other material types (bio, composites, specialty). By manufacturing process, the market is segmented into injection moulding, compression moulding, blow moulding, and other processes (reactive foaming, 3D print, lamination). By component, the market is segmented into outsole, midsole, and insole. The report also covers the market size and forecasts in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Polyurethane (PU) |

| Thermoplastic Rubber (TPR) |

| Ethylene-Vinyl Acetate (EVA) |

| Polyvinyl Chloride (PVC) |

| Rubber (natural and synthetic blends) |

| Thermoplastic Polyurethane (TPU) |

| Other Material Types (bio, composites, specialty) |

| Injection Moulding |

| Compression Moulding |

| Blow Moulding |

| Other Manufacturing Processes (Reactive foaming, 3D print, Lamination) |

| Outsole |

| Midsole |

| Insole |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Polyurethane (PU) | |

| Thermoplastic Rubber (TPR) | ||

| Ethylene-Vinyl Acetate (EVA) | ||

| Polyvinyl Chloride (PVC) | ||

| Rubber (natural and synthetic blends) | ||

| Thermoplastic Polyurethane (TPU) | ||

| Other Material Types (bio, composites, specialty) | ||

| By Manufacturing Process | Injection Moulding | |

| Compression Moulding | ||

| Blow Moulding | ||

| Other Manufacturing Processes (Reactive foaming, 3D print, Lamination) | ||

| By Component | Outsole | |

| Midsole | ||

| Insole | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Footwear Sole Market for the Athletic Industry market in 2026?

The market reached USD 31.59 billion in 2026.

What CAGR is projected for foot-wear sole demand through 2031?

The market is expected to grow at a 5.92% CAGR through 2031, reaching USD 42.12 billion.

Which material type is growing fastest?

Polyurethane midsoles are expanding at a 7.57% CAGR, leading the speed among materials.

How are regulations shaping material choices?

EU Ecodesign rules and U.S. VOC bans drive adoption of bio-based and water-blown foams across new product lines.

Page last updated on: