Football Streaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.67 Billion |

| Market Size (2031) | USD 21.65 Billion |

| Growth Rate (2026 - 2031) | 13.16% CAGR |

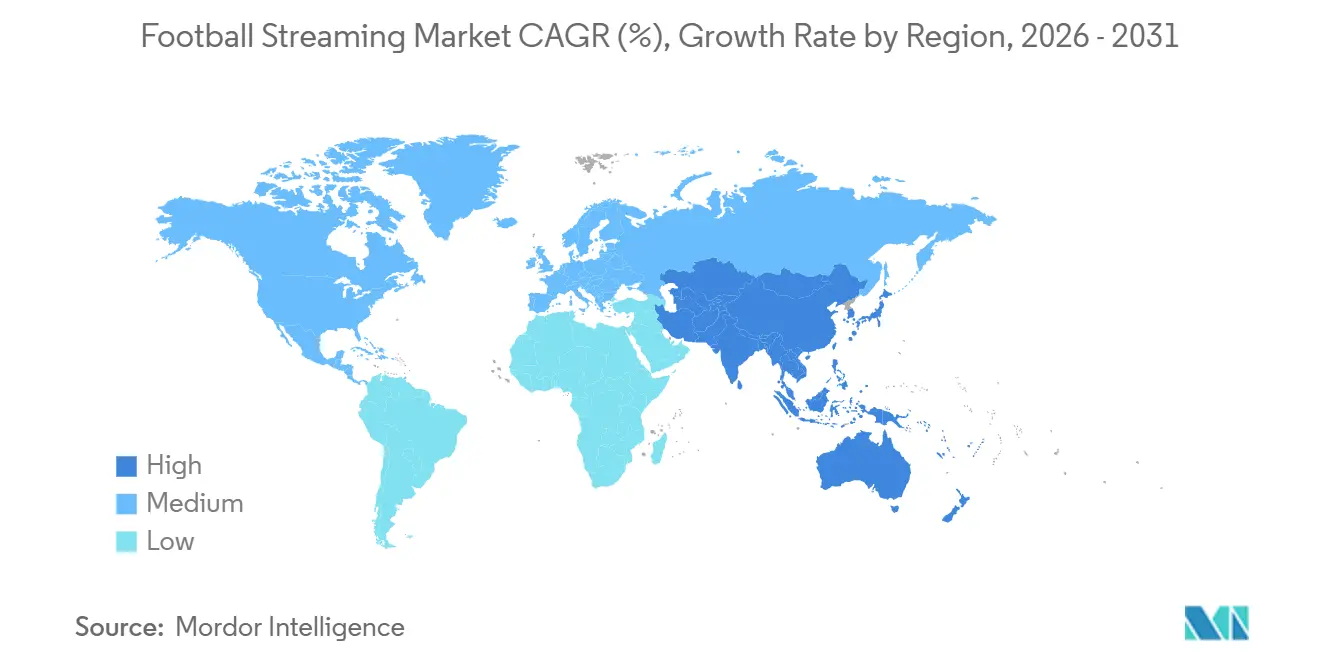

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Football Streaming Market Analysis by Mordor Intelligence

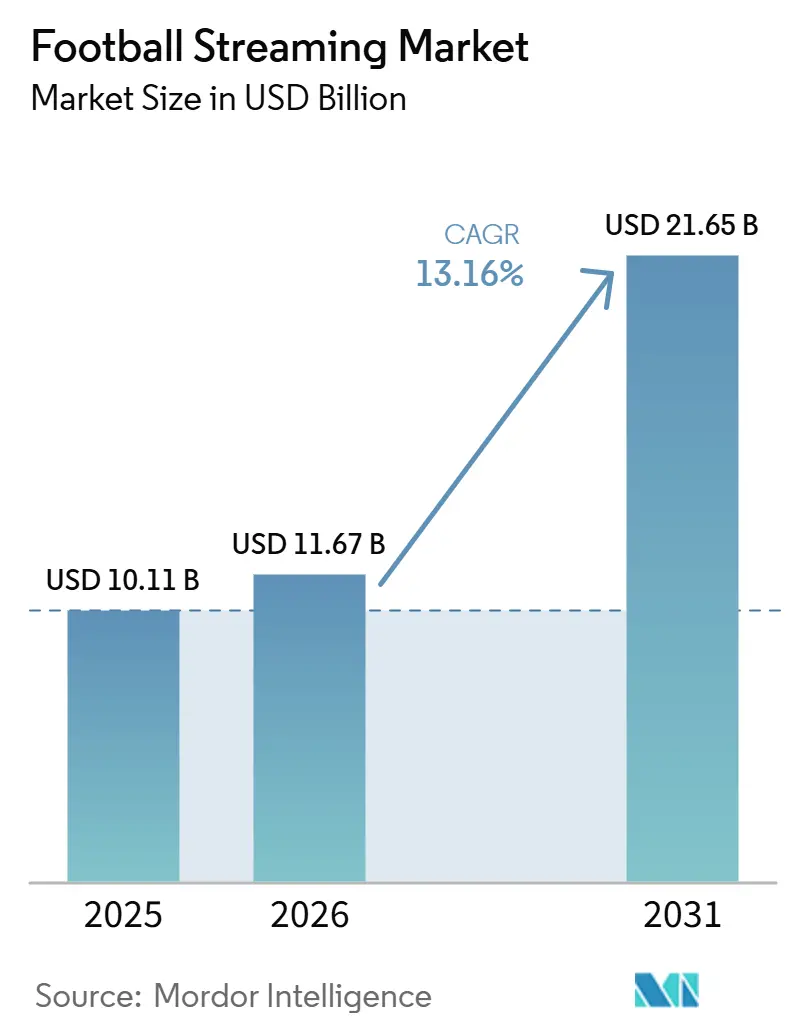

The football streaming market size is expected to increase from USD 10.11 billion in 2025 to USD 11.67 billion in 2026 and reach USD 21.65 billion by 2031, growing at a CAGR of 13.16% over 2026-2031. The football streaming market is expanding because premium football rights now sit at the center of platform strategy, with major services using football to support subscriptions, advertising, commerce, and broader digital ecosystems rather than treating match access as a single product line. The football streaming market is also benefiting from a stronger balance between live viewing and follow-on engagement, since platforms now keep users active through archives, highlights, documentaries, and related fan experiences between match windows. Competitive behavior in the football streaming market is becoming more uneven, because sports-focused platforms still depend heavily on subscriber revenue while larger aggregators can spread rights costs across wider businesses and absorb pressure for longer. The football streaming market is seeing new opportunity in regions where mobile viewing, direct-to-consumer delivery, and localized league distribution can unlock audiences that were either under-monetized or poorly served by earlier pay TV models. The 2026 FIFA World Cup is reinforcing this shift, because it is validating large-scale streaming as a credible distribution model for football while also pushing platforms to improve rights depth, reliability, and fan retention ahead of the next rights cycle.

Key Report Takeaways

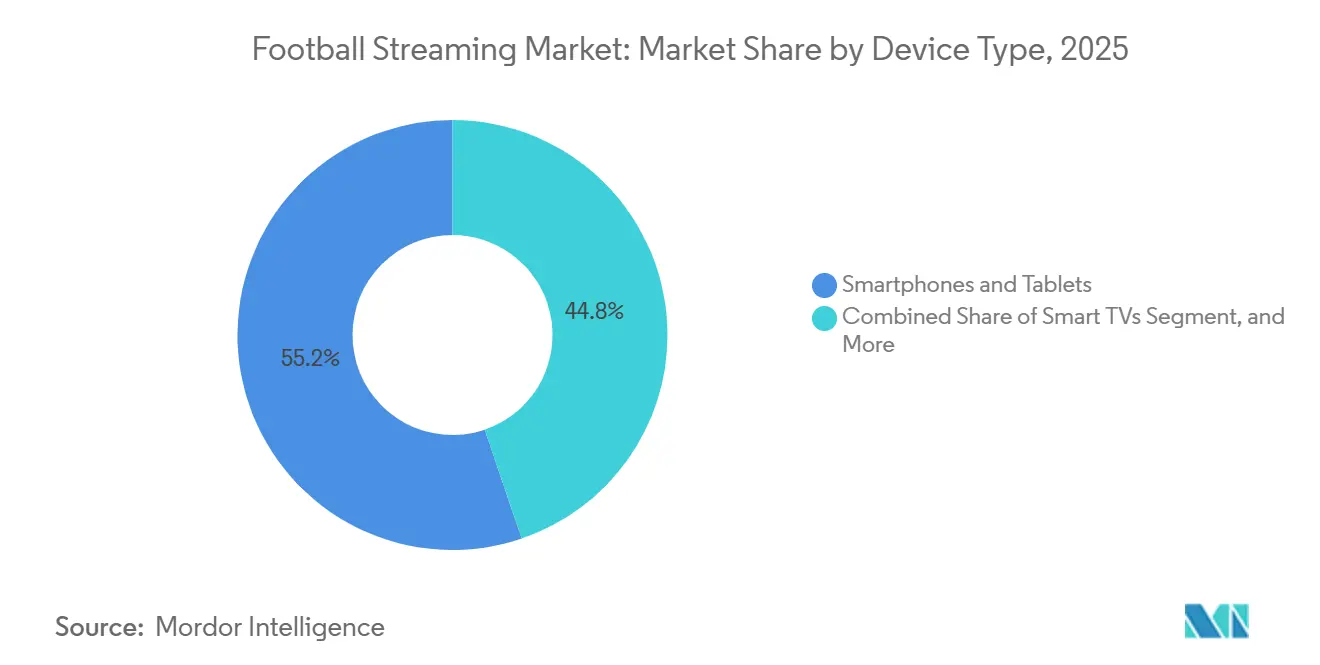

- By device type, smartphones and tablets held 55.22% of the football streaming market share in 2025, while smart TVs are projected to record the highest CAGR of 13.42% through 2031.

- By content type, domestic matches accounted for 55.34% of the football streaming market size in 2025, while international matches are expected to expand at a 13.76% CAGR through 2031.

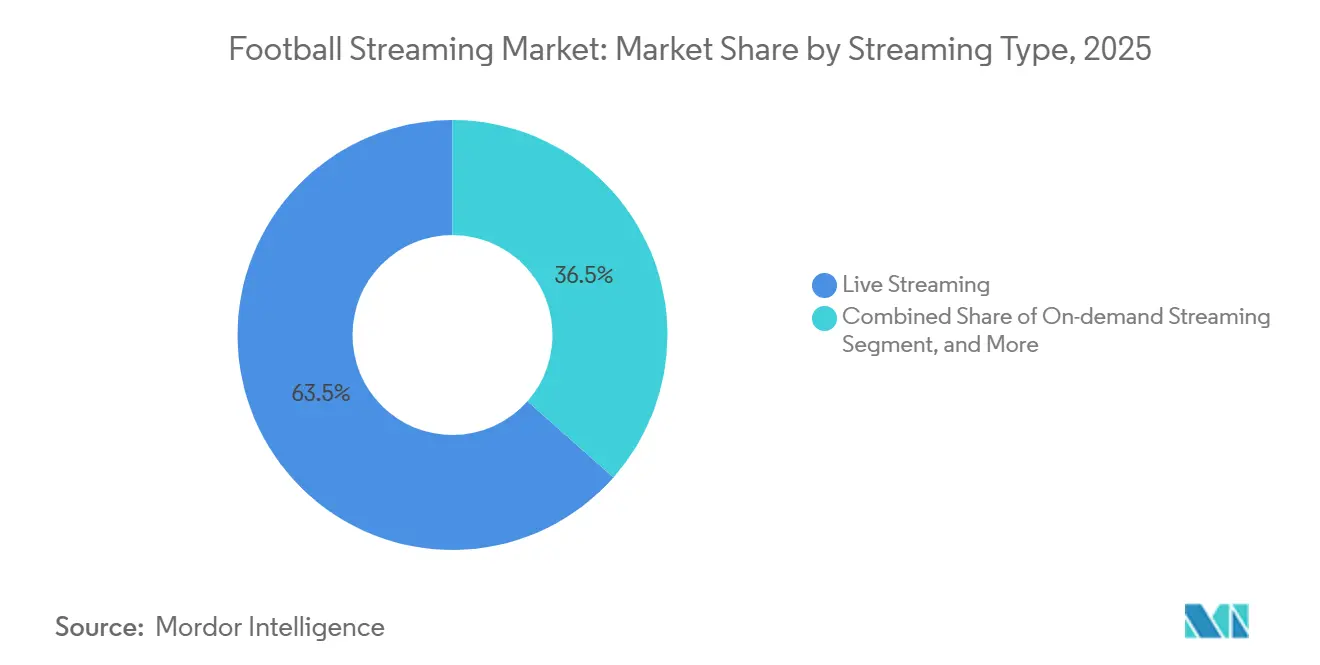

- By streaming type, live streaming represented 63.47% of the football streaming market share in 2025, while on-demand streaming is projected to grow at a 13.88% CAGR through 2031.

- By geography, Europe captured 38.42% of the football streaming market size in 2025, while North America is expected to advance at a 13.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Football Streaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Premium Football Rights Spending by Streamers | +3.2% | Global | Short term (≤ 2 years) |

| Rapid Shift From Pay TV to Direct-to-Consumer Football Viewing | +2.8% | North America, Europe, South America | Medium term (2-4 years) |

| 5G, Low Latency, and Multi-Angle Viewing Expectations | +1.5% | Europe, Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Fan Data Monetization Through First-Party Streaming Ecosystems | +1.2% | Global, early leadership in UK, US, and India | Long term (≥ 4 years) |

| Localized League and Club Streaming in Underserved Markets | +0.9% | Africa, South Asia, South America | Long term (≥ 4 years) |

| Rising Use of Football Streaming for Cross-Sell Into Betting, Commerce, and Memberships | +0.8% | Europe, North America, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Premium Football Rights Spending by Streamers

The football streaming market is moving deeper into a rights-led model, where control of premium competitions increasingly determines which platforms can win attention, hold subscribers, and shape wider fan habits across the year. The football streaming market is showing this pattern clearly through DAZN’s push to strengthen both domestic and international coverage, including its renewal of exclusive Serie A, Coppa Italia, and Supercoppa Italiana rights in France and its position as the sole broadcaster of all 104 FIFA World Cup 2026 matches in Italy.[1]DAZN Group, “FIFA+ Launches on DAZN: A Major Step Towards the Global Home of Football,” DAZN Press Release, dazngroup.com These moves matter because rights depth now influences platform value beyond the live match itself, since a service with broader coverage can reduce cancellation risk and keep football fans inside one environment for more competitions and more months of the year.[2]DAZN Group, “DAZN Renews Exclusive Serie A Rights Through 2029 in France and Reaffirms Its Long-Term Commitment to Football,” DAZN Press Release, dazngroup.com The football streaming market is therefore becoming harder for smaller services to navigate, because rights inflation does not only raise acquisition costs, it also raises the minimum scale needed to remain relevant in top football territories. Premium rights are also concentrating around platforms that can combine league access, tournament coverage, and archived content, which makes each new deal more strategically important than a simple inventory expansion. As a result, the football streaming market is rewarding players that can aggregate high-value football properties across multiple windows and geographies, while weaker operators are pushed toward narrower packages, selective territories, or secondary competitions.

Rapid Shift From Pay TV to Direct-to-Consumer Football Viewing

The football streaming market is gaining momentum from the steady move away from legacy distribution models and toward direct digital access that gives platforms fuller control over pricing, packaging, and the fan relationship. This shift is visible in the way governing bodies and rights holders are backing streaming-first arrangements, including FIFA and DAZN’s launch of FIFA+ on DAZN as a consolidated global destination for live events, archive footage, and original programming. The football streaming market is also moving forward through region-specific distribution choices, such as LaLiga’s exclusive partnership with Begin in Pakistan, Bangladesh, and Sri Lanka, which was designed to create a legal and more commercially workable digital option in a piracy-affected region.[3]LaLiga, “BEGIN Becomes the Exclusive Home of LALIGA in Pakistan, Bangladesh and Sri Lanka,” LaLiga, laliga.com In North America, the 2026 World Cup has already shown that streaming can stand beside, and in some cases outperform, linear viewing for major football audiences, especially in Spanish-language coverage where Peacock passed linear delivery for the first time. The football streaming market benefits from this transition because direct access lets platforms collect user data, adjust price tiers, and bundle football with other digital services more precisely than traditional wholesale television distribution allowed. Over time, the football streaming market is likely to deepen this direct model further, especially in countries where old pay TV structures had limited affordability, weak flexibility, or poor reach among younger users.

Fan Data Monetization Through First-Party Streaming Ecosystems

The football streaming market is becoming more valuable to operators because authenticated viewing environments generate repeat behavioral signals that can support advertising, commerce, personalization, and long-term retention. The football streaming market gains from this shift when platforms move beyond simple match delivery and turn viewing into a logged-in relationship with measurable actions, preferences, and repeat usage patterns across devices and content types. FIFA+ on DAZN reflects this direction because the platform now combines live football events, archive material, and original programming inside one destination, which strengthens the ability to keep users active across more touchpoints and more sessions. The football streaming market is also extending toward more personalized and interactive fan management, as Liverpool FC announced a multi-year partnership with SAS to unify supporter engagement across digital channels and deliver more real-time, tailored experiences. This matters because football subscriptions become more defensible when the platform owns the customer relationship directly and can monetize that relationship through targeted offers, merchandising prompts, membership upsell, or differentiated viewing tools. In that setting, the football streaming market is shifting from a pure content access model toward a commercial model where data depth helps determine platform strength between major rights renewals.

Rising Use of Football Streaming for Cross-Sell Into Betting, Commerce, and Memberships

The football streaming market is opening new revenue paths because football viewers increasingly interact with prediction tools, game formats, and related commercial offers while they watch live content. The football streaming market is showing this clearly through DAZN and Tabcorp’s launch of WorldPlay across five countries, where live streaming is linked with sports gaming infrastructure and a dedicated studio layer in selected markets, including the UK. The football streaming market is also moving toward in-stream prediction and sentiment features, with DAZN and ADI Predictstreet building blockchain-backed free-to-play prediction into FIFA World Cup 2026 live streams to keep fan participation active during the match window itself. These moves matter because they extend the economic value of a match beyond subscription fees and create new reasons for fans to stay inside one platform instead of moving between streaming, betting, social media, and commerce channels separately. The football streaming market gains from this model when engagement becomes deeper and more measurable, since every added interaction increases the chance of repeat use and supports more varied revenue capture. As this pattern expands, the football streaming market is likely to favor operators that can turn football viewing into a broader member experience rather than a limited video transaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rights Inflation and Margin Pressure on Rights Holders and Platforms | -1.8% | Global | Short term (≤ 2 years) |

| Piracy, Illegal Restreaming, and Credential Sharing | -1.5% | Europe, South Asia, Africa | Short term (≤ 2 years) |

| Fragmented Rights Across Leagues, Countries, and Devices | -1.0% | Global, most acute in Europe and North America | Medium term (2-4 years) |

| Event-Scale Latency and Peak Traffic Reliability Risks | -0.6% | Global, concentration in high-density markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rights Inflation and Margin Pressure on Rights Holders and Platforms

The football streaming market faces persistent pressure because premium rights costs keep rising while many services still depend heavily on monthly subscription economics to recover those investments. The football streaming market shows this clearly in the growing importance of exclusive, multi-competition packages, where operators must secure enough football breadth to remain relevant, even when that breadth raises cost exposure and narrows margin flexibility. DAZN’s rights renewals in France, its full World Cup 2026 position in Italy, and its continued expansion of football inventory through FIFA+ all show how competition is moving toward larger, more comprehensive rights stacks rather than isolated event coverage. The football streaming market is especially challenging for specialists because larger digital ecosystems can spread football costs across advertising, commerce, gaming, or other bundled services, while narrower operators often cannot. This imbalance means rights inflation does more than squeeze profits; it also shapes who can keep bidding in future cycles and who must step back into smaller or more local opportunities. Over time, the football streaming market may continue to grow, but rising rights costs can still weaken platform economics, reduce room for product investment, and make competitive positions harder to defend.

Piracy, Illegal Restreaming, and Credential Sharing

The football streaming market continues to lose value to unauthorized access, because live football remains one of the easiest premium content types for illegal redistribution to attract at scale. LaLiga reported that piracy detection in sports and other live events reached record levels through greater investment in resources and technology, with 26.2 million notices issued across an 18-month period and only 6% of infringements acted on within 30 minutes. The football streaming market feels this pressure most directly during premium fixtures, because illegal access weakens the perceived value of paid subscriptions and makes some price-sensitive users less willing to shift into legal platforms. LaLiga’s Begin agreement in South Asia shows that rights holders increasingly see legitimate digital availability as part of the anti-piracy response, not only a distribution decision, especially in territories where access gaps have historically encouraged illegal viewing. The football streaming market is therefore dealing with piracy through both enforcement and product design, since better pricing, easier mobile access, and more localized packages can matter almost as much as takedown speed. Even with improved detection, the football streaming market still faces a structural enforcement gap, and that gap remains a direct brake on monetization in several high-interest football regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smartphones And Tablets Keep The Broadest Audience Base

Smartphones and tablets accounted for 55.22% of the football streaming market in 2025, which kept this category as the main access point for fans in markets where mobile connectivity is stronger than fixed broadband and where screen flexibility matters more than premium home hardware. The football streaming market still leans heavily on handheld devices because football consumption often starts with portability, instant notifications, and social spillover, especially when clips, commentary, and match reactions circulate continuously across messaging and social platforms. This pattern remains strong in South Asia, Southeast Asia, Africa, and South America, where the football streaming industry continues to expand through affordable mobile data, wide smartphone availability, and lower entry barriers for new users. In practical terms, smartphones and tablets keep the football streaming market close to day-to-day fan routines, because users can watch before work, during travel, and around fragmented schedules without depending on a fixed location. That broad accessibility helps explain why this device segment held the largest position even as more premium connected-home experiences continue to develop.

Smart TVs are projected to grow at a 13.42% CAGR from 2026 to 2031, which makes them the fastest-rising large-screen route for premium football access as households shift viewing back into the living room without returning to traditional pay TV bundles. The football streaming market is benefiting from that shift because smart TVs support better picture quality, more immersive match sessions, and stronger co-viewing behavior for marquee fixtures that fans still prefer to watch on a bigger screen. The World Cup audience surge across Fox, FS1, and Tubi also supports the idea that large-event football viewing is scaling across modern connected environments rather than only through legacy television channels. In the same period, Telemundo and Peacock showed that streaming can carry mass football demand at national-event level, which strengthens the long-term case for premium home-based digital viewing in the football streaming market. Laptops and desktops remain useful for office, study, and multitasking situations, while consoles and second-screen formats add incremental engagement value, but the core direction of the football streaming market points to a durable mobile base alongside faster connected-TV growth.

By Content Type: Domestic Matches Remain The Revenue Anchor While International Fixtures Accelerate

Domestic matches held 55.34% of the football streaming market in 2025, which shows that habitual weekly viewing, club allegiance, and league-season continuity still provide the strongest revenue base inside the football streaming market. Domestic league football remains central because it creates recurring viewing behavior across long seasons, keeps fans attached to one service for repeated matchdays, and supports dependable subscription value beyond a few global tournaments. The football streaming market relies on this cadence, since domestic competitions give platforms a stable rhythm of content that is easier to package, promote, and retain than short tournament bursts. For many operators, domestic rights also shape brand relevance in each territory, because top local leagues often decide which platform becomes part of the fan’s weekly routine rather than an occasional destination. That is why domestic football continues to anchor the football streaming market even while international fixtures are rising faster.

International matches are projected to advance at a 13.76% CAGR from 2026 to 2031, reflecting the growing pull of FIFA and UEFA properties, wider global fan reach, and platform strategies built around event concentration and cross-border aggregation. DAZN’s June 2026 integration of FIFA+ into its platform illustrates this trend well, because it combines live FIFA events, full archive access, and original football programming inside one environment that can serve both casual tournament viewers and year-round fans. The football streaming market gains from this model because international content can travel across borders more easily than some domestic properties, which increases the commercial value of consolidated rights and deepens platform relevance in non-traditional football territories. The football streaming market also sees stronger subscriber acquisition during major tournaments, then tries to convert that temporary attention into longer use through replays, archives, and related international content layers. Other content, including women’s football, youth competitions, and club-originated programming, remains smaller, but it is becoming more useful in the football streaming market as a lower-cost way to extend engagement between premium match windows.

By Streaming Type: Live Viewing Holds The Core Position While On-Demand Usage Builds Depth

Live streaming represented 63.47% of the football streaming market in 2025, confirming that real-time access remains the central product in a category where timing, shared reaction, and synchronized conversation still define much of the fan experience. The football streaming market depends on live delivery because goals, officiating moments, tactical swings, and fan response all carry their highest value when watched together and discussed immediately across social and messaging platforms. This is why live streaming continues to lead the football streaming market size conversation in practical commercial terms, since subscription value is still tied most directly to major fixtures and uninterrupted real-time access. The dominance of live coverage also means platform performance matters strongly, because lag, outages, or poor stream quality can damage trust faster in football than in less time-sensitive entertainment categories. Even with broader content libraries now available, the football streaming market still turns on the strength of the live match experience.

On-demand streaming is projected to grow at a 13.88% CAGR from 2026 to 2031, which shows that the football streaming market is becoming less dependent on a single live-event use case and more dependent on continuous content engagement. FIFA+ on DAZN supports this transition because it brings archive programming and original football content together with live events, giving fans reasons to return between tournaments or outside local match windows. The football streaming market benefits when on-demand usage grows, because replays, documentaries, highlights, and multilingual packages can attract viewers who do not follow every match live but still remain commercially valuable to the platform. This category also supports retention, since a service with more off-cycle content can keep users engaged after major tournaments end and can reduce the all-or-nothing behavior that often follows a single-event subscription decision. Other streaming formats, including highlights-only or short-form access, remain smaller today, but they could become more relevant in the football streaming market where affordability, mobile behavior, and advertiser-led models matter more than full-match subscriptions.

Geography Analysis

Europe accounted for 38.42% of the football streaming market in 2025, giving the region the largest position globally because its domestic leagues are commercially dense and its rights environment supports multiple competing platforms across major football territories. The football streaming market in Europe is defined by layered competition, where Sky, DAZN, Amazon Prime Video, Canal+, and beIN Sports operate through different rights bundles, different countries, and different competition tiers rather than through one simple winner-take-all model. DAZN’s renewal of exclusive Serie A rights in France through the 2028-29 season shows how platforms are trying to build long-term relevance through multi-league portfolios that can hold fans inside one subscription for more of the calendar. In Italy, DAZN’s exclusive control of all 104 FIFA World Cup 2026 matches adds another example of how the football streaming market is consolidating premium visibility around digital-first aggregators that can combine domestic and international reach. Europe still offers strong monetization potential, but the football streaming market here remains operationally complex because rights fragmentation, regulatory oversight, and piracy all affect platform economics at the same time.

North America is projected to grow at a 13.91% CAGR from 2026 to 2031, making it the fastest-growing regional bloc in the football streaming market as the 2026 World Cup expands audience familiarity, platform adoption, and commercial confidence. Fox Sports reported strong World Cup 2026 group-stage results, with average English-language viewership of 5.05 million viewers per match and a 92% increase versus the 2022 tournament, which highlights how mainstream football demand is broadening in the region. Comcast also stated that Telemundo and Peacock reached record viewership during the tournament, and that Peacock exceeded linear audience for the first time in this context, which is a major signal for the football streaming market in multilingual and streaming-first households. The football streaming market in North America is still fragmented across several subscription services, but that fragmentation also leaves room for bundling, aggregation, and cross-platform upsell as football becomes a more regular consumer category. With the United States, Canada, and Mexico all tied to the 2026 event cycle, the football streaming market in North America now has stronger foundations for sustained expansion than it had in earlier tournament periods.

Asia-Pacific, South America, the Middle East, and Africa together hold the longest runway for the football streaming market, although monetization still depends on rights affordability, local distribution fit, mobile access, and the ability to reduce piracy through legal convenience. In Asia-Pacific, LaLiga’s multi-year Begin deal in Pakistan, Bangladesh, and Sri Lanka shows how the football streaming market is using regional digital partnerships to improve legal access in price-sensitive territories where football demand is high but traditional premium distribution has been uneven. In South America, the football streaming market continues to benefit from deep football culture and strong event intensity, which means the commercial upside is significant when platforms can match pricing and access with local realities. Across Africa and parts of the Middle East, the football streaming market has strong audience potential, but growth still depends heavily on mobile-first distribution models and practical affordability because those factors often matter more than the theoretical popularity of elite global leagues.

Competitive Landscape

The football streaming market is moderately concentrated at a global level, but it remains structurally fragmented when viewed through geography, league rights, competition windows, device behavior, and the difference between specialist and generalist platform models. The football streaming market, therefore, does not operate like a simple global subscription race, because leadership can be strong in one country or one league package while remaining weak elsewhere. DAZN remains one of the clearest strategic examples in the football streaming market, as it has combined tournament rights, domestic league rights, archive integration, and platform expansion into a more complete football proposition across several territories. The football streaming market also shows a widening split between operators that can absorb rights spending through broader ecosystems and operators that must recover most of the cost directly from sports subscribers, which shapes bidding behavior and long-term resilience. That divide is likely to remain one of the most important competitive features in the football streaming market through the next major rights cycles.

A second clear pattern in the football streaming market is aggressive aggregation, where platforms try to reduce churn and strengthen value perception by keeping more football properties under one roof. DAZN’s renewal of French Serie A rights and its full World Cup 2026 position in Italy support this model, because each move raises the breadth of football access and makes the platform harder to replace for certain fan groups. The football streaming market is also seeing competition move into infrastructure and service capability, not only rights ownership, as shown by DAZN’s acquisition of ViewLift to deepen its position in U.S. local sports media rights and direct-to-consumer solutions. That acquisition matters because the football streaming market increasingly rewards platforms that can offer leagues, clubs, and regional rights holders both distribution reach and technical operating support. In effect, the football streaming market is becoming more competitive across the full stack, including rights, delivery, fan data, advertising options, and partner services.

A third competitive theme in the football streaming market is monetization beyond subscription, especially through gaming, prediction, and localized access models. DAZN and Tabcorp’s WorldPlay launch, along with DAZN’s Predictstreet integration, shows how the football streaming market is turning live match windows into broader engagement environments where betting-adjacent activity and interactive features deepen usage. LaLiga’s partnership with Begin points to another route, where the football streaming market uses local OTT alliances to enter underserved territories with a legal product that is better matched to regional economics and anti-piracy needs. Taken together, these moves show that the football streaming market is no longer shaped only by who owns the biggest match package, but also by who can package football into the most durable, localized, and commercially layered user experience.

Football Streaming Industry Leaders

DAZN Group Limited

Amazon.com, Inc.

YouTube LLC

Sky Limited

Paramount Skydance Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: DAZN and Tabcorp launched WorldPlay, an integrated sports gaming and betting platform, across five countries, combining live football streaming on DAZN with Tabcorp's global sports games infrastructure and a dedicated studio broadcast, WorldPlayHQ, in selected markets including the UK.

- June 2026: FIFA and DAZN launched FIFA+ exclusively on DAZN, consolidating 8,500 live football events annually, FIFA's full archive content, and original programming into a single global streaming destination, operationalizing both parties' stated ambition to create the "Global Home of Football".

- June 2026: DAZN signed a multi-year agreement with DSPORTS to distribute three DSPORTS channels to subscribers in Chile, Colombia, Ecuador, Peru, and Uruguay, integrating Copa America, CONMEBOL Sudamericana, and FIFA World Cup 2026 coverage into DAZN's South American footprint.

- April 2026: DAZN announced its acquisition of ViewLift, a U.S.-based streaming solutions provider serving 15 major U.S. professional sports teams and 5 regional sports networks, to accelerate its penetration of the U.S. local sports media rights market and build comprehensive direct-to-consumer solutions for clubs and leagues.

Global Football Streaming Market Report Scope

Football Streaming Market refers to the segment of digital sports media focused on delivering live and on-demand football matches over internet-based platforms. It includes OTT apps, broadcaster-owned services, and streaming platforms that distribute league matches, tournaments, highlights, and related programming across mobile, web, and connected TV devices.

The Football Streaming Market Report is Segmented by Device Type (Smartphones and Tablets, Smart TVs, and Laptops and Desktops), Content Type (International Matches, and Domestic Matches), Streaming Type (Live Streaming, and On-demand Streaming), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Type |

| International Matches |

| Domestic Matches |

| Other Content Type |

| Live Streaming |

| On-demand Streaming |

| Other Streaming Type |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Type | ||

| By Content Type | International Matches | |

| Domestic Matches | ||

| Other Content Type | ||

| By Streaming Type | Live Streaming | |

| On-demand Streaming | ||

| Other Streaming Type | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future size of the football streaming space?

The football streaming market was valued at USD 10.11 billion in 2025, stands at USD 11.67 billion in 2026, and is forecast to reach USD 21.65 billion by 2031 at a 13.16% CAGR.

Which region leads football streaming revenue today?

Europe leads with 38.42% share in 2025, supported by dense domestic league economics and a highly active multi-platform rights environment.

Which region is growing fastest through 2031?

North America is the fastest-growing region, with a projected CAGR of 13.91% from 2026 to 2031, helped by World Cup-driven audience formation and stronger streaming adoption.

Which device category is most important for football viewing?

Smartphones and tablets held 55.22% share in 2025, showing that mobile access remains the main gateway in many football-heavy and mobile-first markets.

Why do domestic leagues still matter more than international tournaments for revenue?

Domestic matches accounted for 55.34% in 2025 because they create weekly viewing habits, stronger club loyalty, and more stable subscription value across a full season.

How is on-demand viewing changing platform economics?

On-demand streaming is expected to grow at a 13.88% CAGR through 2031, and it helps platforms hold users between live matches through archives, highlights, documentaries, and replay viewing.

Page last updated on: