Foley Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

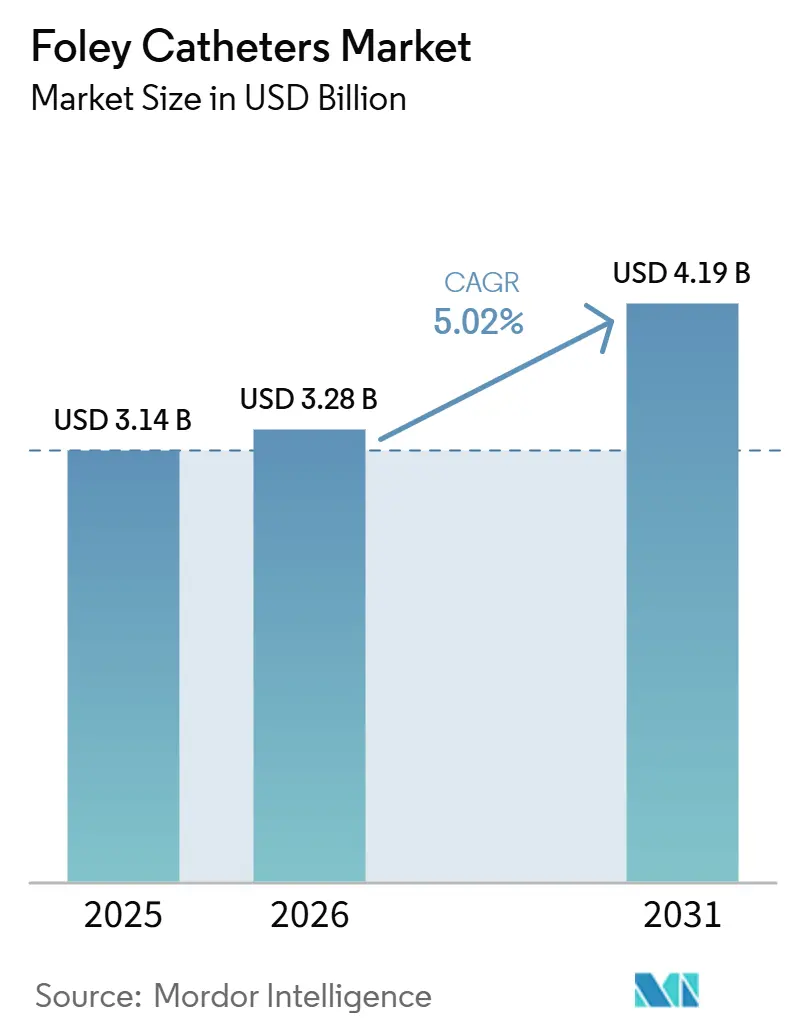

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foley Catheters Market Analysis by Mordor Intelligence

The Foley Catheters Market size is expected to increase from USD 3.14 billion in 2025 to USD 3.28 billion in 2026 and reach USD 4.19 billion by 2031, growing at a CAGR of 5.02% over 2026-2031.

The foley catheters market is being supported by an older patient base, a larger urology disease burden, and tighter hospital focus on infection control, especially as global benign prostatic hyperplasia cases rose from 50.7 million in 1990 to 112.5 million in 2021 and are projected to reach 1,563 per 100,000 people by 2035. The Foley catheters market is also tied to routine care needs because 15% to 25% of hospitalized patients receive urinary catheters, and 75% of hospital-acquired urinary tract infections are linked to catheter use. That infection burden is pushing hospitals toward better materials and coating choices, while the added cost of each CAUTI event at USD 13,793 makes device-level prevention a firm buying criterion in mature care systems. Competitive activity in the Foley catheters market is centered on coating technology, clinical support, regulatory reach, and portfolio changes, especially after Teleflex announced the sale of its acute care and interventional urology businesses for USD 2.03 billion. The foley catheters market is also seeing a clear shift toward home-based use, where comfort, supply continuity, and simpler follow-up matter as much as acute care performance.

Key Report Takeaways

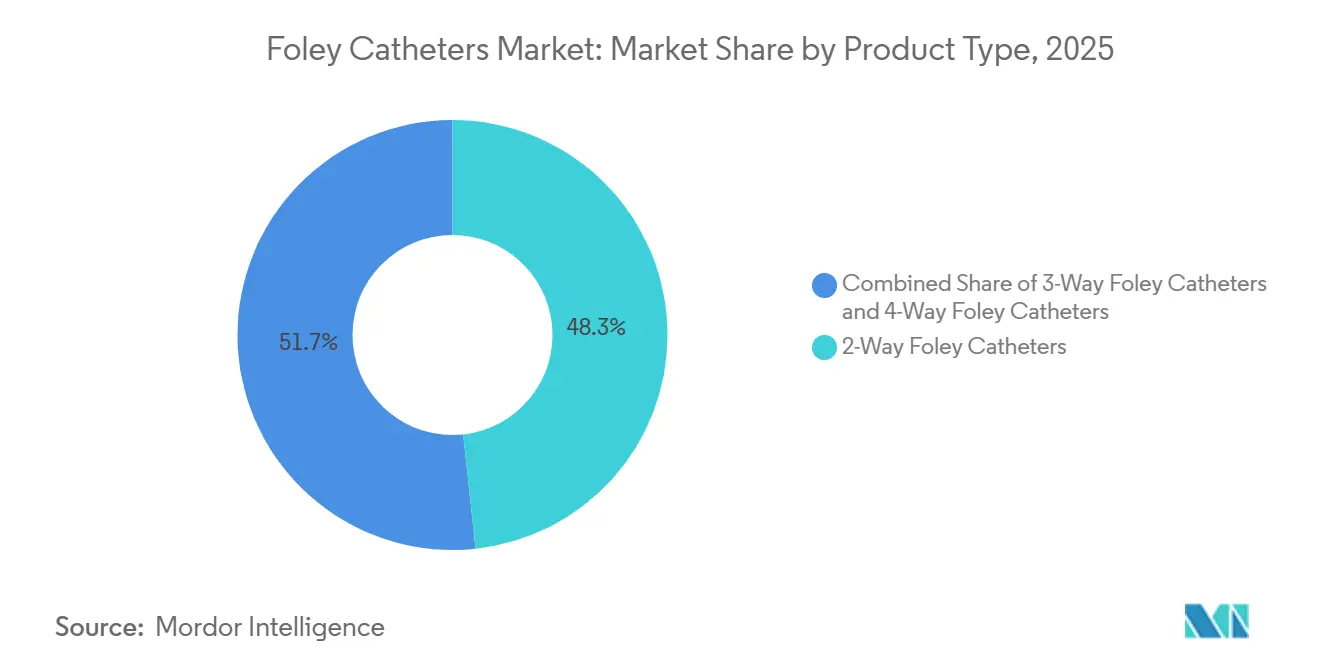

- By product type, 2-Way Foley Catheters led with 48.27% share in 2025, while 3-Way Foley Catheters are projected to expand at 5.49% CAGR through 2031.

- By material type, silicone accounted for 39.38% of the Foley catheters market size in 2025, while silicone elastomer-coated latex is forecast to grow at 6.72% CAGR through 2031.

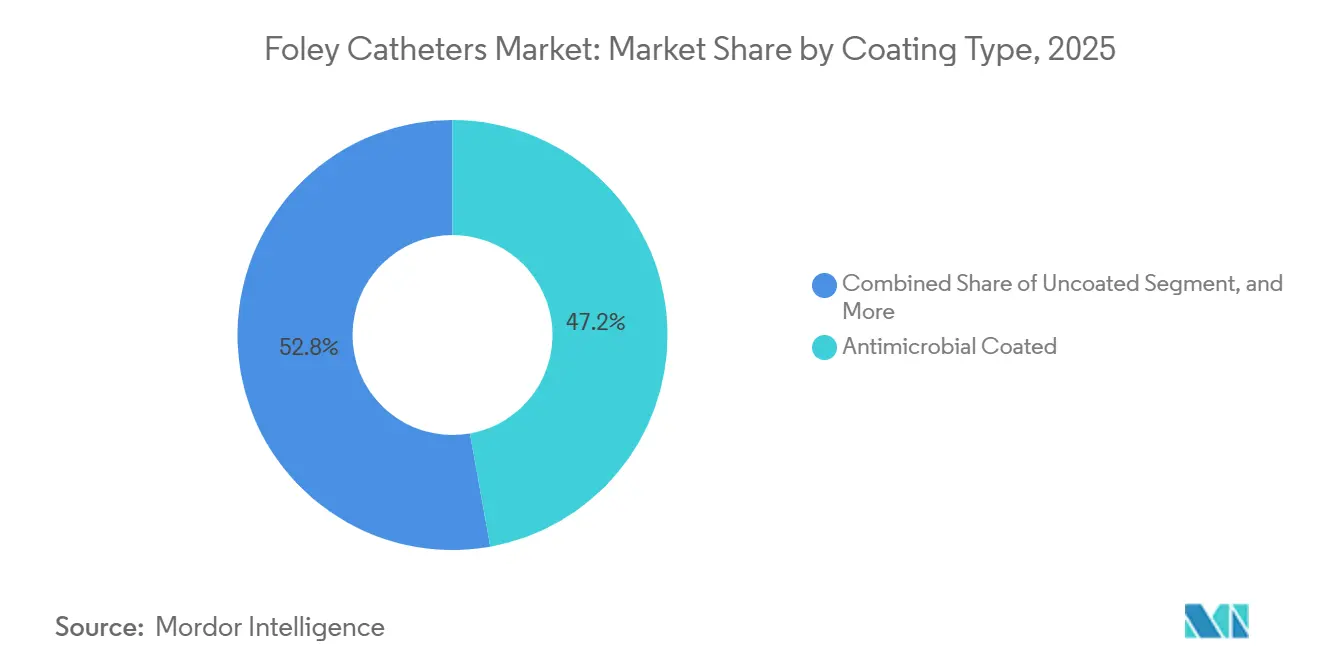

- By coating type, antimicrobial coated catheters held 47.16% share in 2025, while hydrophilic or lubrication coated catheters are projected to grow at 7.53% CAGR through 2031.

- By end user, hospitals captured 39.63% share in 2025, while home care settings are projected to expand at 5.89% CAGR through 2031.

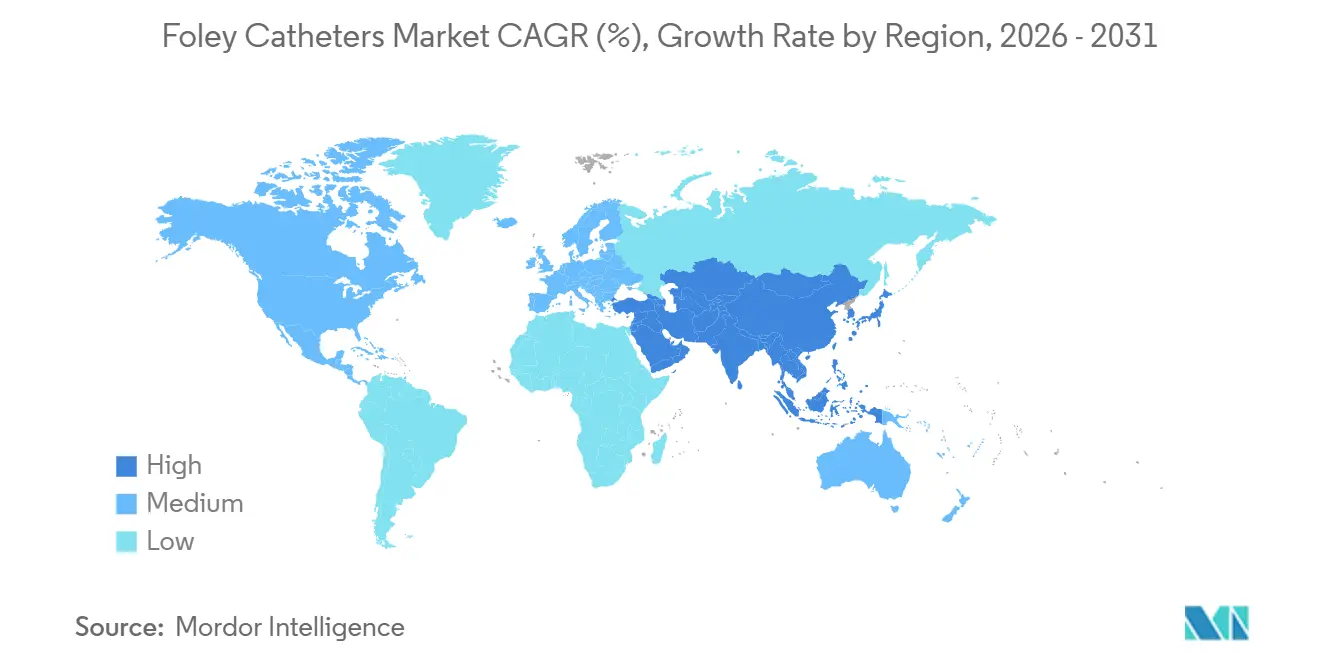

- By geography, North America held 37.63% of the Foley catheters market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 6.09% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Foley Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urological Disorders and Benign Prostatic Hyperplasia | +1.4% | Global, highest absolute burden in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Aging Population and Longer-Term Bladder Management Needs | +1.2% | Global, Asia-Pacific fastest-growing due to demographic acceleration | Long term (≥ 4 years) |

| Rising Surgical Volumes Requiring Post-Operative Urinary Drainage | +0.9% | North America and Europe, expanding in core Asia-Pacific markets | Medium term (2-4 years) |

| Shift Toward Infection-Preventive Silicone and Antimicrobial-Coated Catheters | +0.8% | North America, Europe, with spillover to Asia-Pacific and Middle East & Africa | Medium term (2-4 years) |

| Expansion of Home-Based Catheter Care and Remote Follow-Up Workflows | +0.7% | North America and Europe, nascent in Asia-Pacific | Medium term (2-4 years) |

| Hospital Antibiotic Stewardship Pressure Accelerating Device-Level Infection Control | +0.6% | Global, highest compliance in North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Urological Disorders and Benign Prostatic Hyperplasia

The foley catheters market is being pushed by the growing burden of benign prostatic hyperplasia, which remains the largest long-duration demand source in this category. Global prevalent BPH cases rose from 50.7 million in 1990 to 112.5 million in 2021, and the projected prevalence rate is expected to reach 1,563 per 100,000 people by 2035.[1]Scientific Reports, “Comprehensive Analysis of the Global, Regional, and National Burden of Benign Prostatic Hyperplasia From 1990 to 2021,” Scientific Reports, nature.com The burden is especially strong in older men, and prevalence reaches 80% among men older than 70, which keeps indwelling catheter use closely tied to disease progression when drug treatment is no longer enough. The geographic spread also matters because the UAE recorded a 1,381% increase in BPH prevalence between 1990 and 2021, which points to stronger future demand in Gulf markets that are still underdeveloped from a commercial standpoint. In the United States, BPH and LUTS affected 29% to 35% of men aged 65 and older in Medicare fee-for-service between 2015 and 2021, which keeps catheter use tied to the largest single-payer population in the country.

Aging Population and Longer-Term Bladder Management Needs

The foley catheter market is being shaped by aging in a way that changes not just volume, but also the pattern of use. Older patients are more likely to need longer dwell times, easier care transitions, and more dependable supply over several years rather than short, acute episodes. The foley catheters market therefore, shifts toward products that reduce irritation, limit encrustation risk, and fit home care routines more easily. The same age-linked disease burden that lifts BPH prevalence also enlarges the pool of patients who need repeat or long-term bladder management support. In practical terms, long-term users create a steadier demand for comfortable materials, infection control features, and distribution systems that can support repeat ordering and follow-up.

Rising Surgical Volumes Requiring Post-Operative Urinary Drainage

The foley catheters market continues to rely on post-operative urinary drainage as a stable demand base across hospitals. Catheter use remains routine in colorectal, gynecological, and urological procedures, even as early removal protocols become more structured. Among patients undergoing robotic-assisted radical prostatectomy, post-operative catheterization still remains standard while clinical work continues on the best timing for catheter removal.[2]Baihe Zeng, “Do All Patients Need a Urethral Catheter After Robotic-Assisted Radical Prostatectomy?” Journal of Robotic Surgery, doi.org Rising procedural volumes across China, India, and South Korea are adding new demand, especially as hospital networks expand and urology capacity deepens. As more care systems adopt standardized perioperative protocols, procurement is moving toward fewer suppliers that can meet quality, consistency, and clinical support requirements.

Shift Toward Infection-Preventive Silicone and Antimicrobial-Coated Catheters

The foley catheters market is seeing coating technology move from an optional premium feature to a routine buying standard in higher-compliance settings. A 2026 multicenter randomized controlled trial found that poly-L-lysine-coated catheters reduced bacteriuria incidence to 6.9% from 10.1% in the control group and reduced abnormal urine white blood cell rates to 6.2% from 12.8%.[3]Lei Zhang, “Antimicrobial Catheters Coated With Poly-L-Lysine for the Prevention of Bacteriuria in Adults Requiring Short-Term Catheterization, A Multicenter Randomized Controlled Trial,” BMC Medicine, link.springer.com That evidence supports the case for next-generation coatings that offer measurable infection-related performance rather than just marketing differentiation. Material selection is also being shaped by ISO 10993 biocompatibility expectations, which favor manufacturers that can support testing and documentation at scale. The foley catheters market is also moving toward layered designs where hydrophilic coatings and antimicrobial surfaces are combined, which raises both performance thresholds and cost thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Catheter-Associated Urinary Tract Infection Risk and Liability Exposure | -0.5% | Global, most pronounced in North America and Europe with stronger liability frameworks | Short term (≤ 2 years) |

| Patient Discomfort, Stigma, and Self-Removal Risk | -0.2% | Global, higher impact in home care settings | Long term (≥ 4 years) |

| Higher Cost of Silicone and Advanced Coated Catheters | -0.3% | Core Asia-Pacific, Middle East & Africa, and South America | Medium term (2-4 years) |

| Inconsistent Insertion Training and Maintenance Protocols in Resource-Constrained Settings | -0.2% | Middle East & Africa, South America, and lower-income Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Catheter-Associated Urinary Tract Infection Risk and Liability Exposure

The foley catheters market faces a direct restraint from CAUTI risk because infection control programs reduce unnecessary catheter use and shorten dwell times. U.S. healthcare facilities reported 21,525 CAUTIs to the CDC National Healthcare Safety Network in 2023, and each event carried an average added cost of USD 13,793 with 36 excess deaths per 1,000 events. These figures support premium product demand, but they also push hospitals to narrow insertion indications and remove catheters sooner. In the United States, acute-care CAUTI rates fell 11% between 2022 and 2023, which shows that compliance-based reduction is possible and can reduce unit use in high-surveillance settings. A multi-center study in 8 Chinese tertiary hospital ICUs also showed that bundle interventions reduced CAUTI rates from 3.8 to 1.3 per 1,000 catheter days and reduced catheter utilization from 71.3% to 62.7% of patient days, which shows how infection control can directly limit volume growth.

Higher Cost of Silicone and Advanced Coated Catheters

The foley catheters market also faces a cost barrier because silicone and advanced coated products remain more expensive than standard latex options. More complex raw materials, added process steps, and multi-layer coating systems keep premium product pricing above what many public and lower-income health systems can absorb. This gap slows adoption in parts of Asia-Pacific, Sub-Saharan Africa, and Latin America, where procurement still favors basic products even when infection risk is higher. The cost challenge is made harder by natural rubber latex supply concentration in Southeast Asia, which exposes coated-latex lines to commodity swings and weather-related disruption. As a result, the foley catheters market often sees the strongest clinical products adopted first in wealthier systems, while cost-sensitive settings move at a slower pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 3-Way Catheter Demand Rising on Surgical Back

2-Way Foley Catheters held 48.27% of the Foley catheters market share in 2025, supported by broad use across surgical care, intensive care, and long-term drainage. Their leading position comes from clinical flexibility and lower procurement cost, which fit standardized hospital formularies well. In the Foley catheters market, this segment remains more established than fast moving, especially in higher-income regions where replacement demand is steadier than expansion demand. Growth still continues through hospital build-out in Asia-Pacific and Middle East & Africa, where installed care capacity is still rising.

3-Way Foley Catheters are the fastest-growing product type with a 5.49% CAGR from 2026 to 2031, driven by higher use in procedures that need both drainage and irrigation. Transurethral resection of the prostate and other endoscopic urology procedures continue to support that pattern because continuous irrigation remains a routine need after surgery. The Foley catheters market therefore gives this segment a stronger growth profile than the larger 2-way category, even though the installed base is smaller. 4-Way Foley Catheters remain a narrow specialty segment used mainly in tertiary settings and academic centers for suprapubic and thermometric applications, which keeps demand limited but stable.

By Material Type: Silicone Elastomer Blends Fill the Cost-Performance Gap

Silicone held 39.38% of the Foley catheters market size in 2025, reflecting preference for long-term indwelling use, lower encrustation risk, and fit with latex-free care protocols. That position is strongest in patients who need longer use durations and in settings where pediatric or immunocompromised care makes latex avoidance more important. In the Foley catheters market, silicone also benefits from hospital efforts to reduce irritation and improve tolerance over extended use periods. Its drawback remains price, which slows full penetration in cost-sensitive systems even when clinical preference is clear.

Silicone elastomer-coated latex is the fastest-growing material category with a 6.72% CAGR from 2026 to 2031 because it balances part of silicone's performance with latex's cost advantage. That mix gives mid-tier hospitals, especially in Asia-Pacific, a practical route to move beyond basic latex without taking on the full cost of all-silicone conversion. Standard latex still carries meaningful volume in lower-cost settings because the supply chain is established, and buying budgets remain tight. Hydrophilic polymer-coated latex and PTFE-coated latex continue to serve specific needs linked to easier insertion, lower trauma, and reduced bacterial adhesion. The Foley catheter industry is therefore not moving away from latex in a single step, but rather through a staged shift toward higher-grade coated and blended materials.

By Coating Type: Hydrophilic Coatings Leading the Next Innovation Wave

Antimicrobial-coated catheters held 47.16% share in 2025, which shows how firmly infection prevention standards have shaped buying decisions in critical care and other high-acuity settings. This segment built its position through years of clinical use and through hospital policies aimed at reducing CAUTI incidence. In the Foley catheters market, antimicrobial surfaces still carry strong relevance where surveillance is strict and liability exposure is high. The installed base remains meaningful because many hospitals treat coating performance as part of routine risk control rather than a premium add-on.

Hydrophilic or lubrication coated catheters are the fastest-growing coating type with a 7.5% CAGR from 2026 to 2031, which is the highest growth rate among all segments in the report. A 2026 pilot randomized study of the LubriShield Foley catheter found no serious adverse events and no statistically significant difference in urinary culture outcomes between coated and uncoated devices. The same study also reported lower pain scores with the standard catheter after insertion, which means the evidence base is still developing even though safety was supported. Uncoated products remain present in short-duration and cost-sensitive use cases where the added spend on advanced coating systems is harder to justify. The foley catheters industry is therefore seeing two parallel paths, with antimicrobial coatings defending installed share and hydrophilic coatings opening a separate comfort-led growth lane.

By End User: Home Care Becomes the Market's Structural Frontier

Hospitals accounted for 39.63% of the market in 2025 because acute procedures, intensive care use, and post-surgical monitoring remain concentrated inside institutional settings. Their scale also reflects established purchasing systems and routine catheter use across several inpatient pathways. In the foley catheters market, hospitals still set product standards that later influence use in ambulatory and community settings. That keeps hospital demand central even as the mix of care settings changes.

Home care settings are the fastest-growing end-user category with a 5.89% CAGR from 2026 to 2031, supported by payer pressure to reduce inpatient use and by patient preference for care at home. The foley catheters market is therefore shifting toward products that are easier to handle, more comfortable over time, and better suited to repeat delivery and remote follow-up. Ambulatory surgery centers are also gaining volume as outpatient urology procedures expand under value-based care models. Long-term care facilities continue to generate steady demand because the institutionalized elderly population remains a stable source of chronic catheter use. Other end users, including clinics and research centers, add smaller but relevant volume through trials, specialist care, and follow-up services.

Geography Analysis

North America accounted for 37.63% of the foley catheters market share in 2025, with the United States remaining the main revenue contributor. Claims-based prevalence for BPH and LUTS in U.S. men aged 65 and older ranged from 31% to 35% between 2015 and 2021, which supports steady underlying demand in the Medicare population. Strong infection surveillance and accreditation expectations also keep antimicrobial and hydrophilic coated products well-positioned in hospital buying patterns. Canada adds support through aging-related long-term catheter needs, while Mexico contributes incremental volume through hospital expansion and continued use of conventional latex and entry-level coated products.

Asia-Pacific is the fastest-growing region in the Foley catheters market with a 6.09% CAGR from 2026 to 2031. China carries the largest absolute BPH burden in the region, with 3.2 million incident cases and 23.1 million prevalent cases in 2021, which gives the region a large long-term patient base for catheter use. Growth is also supported by hospital expansion in India, stronger reimbursement structures in South Korea, and broader infection-control awareness across large urban systems. Australia and Southeast Asian markets add incremental demand as surgical volumes rise and institutional procurement becomes more standardized.

Europe held a significant position in the foley catheters market in 2025, led by Germany, the United Kingdom, France, Italy, and Spain. The region is being shaped by stricter clinical evidence expectations under the EU Medical Device Regulation, which raises barriers for weaker catheter offerings and supports manufacturers with stronger documentation. Home-based care in Europe is expected to expand faster than other regional end-user settings through 2031 as tele-urology and community care models continue to develop. The Middle East and Africa remain smaller, but Gulf states are important because imported device demand is rising faster than local supply and the UAE recorded a 1,381% increase in BPH prevalence between 1990 and 2021. South Africa anchors the African market, while the rest of the region remains constrained by infrastructure and reimbursement limits. South America, led by Brazil and Argentina, stays cost-sensitive, but hospital accreditation efforts are gradually improving demand for mid-tier coated catheter products.

Competitive Landscape

The foley catheters market is moderately consolidated at the global tier and fragmented below that level. A small group of multinational companies, including Becton, Dickinson and Company, Coloplast A/S, B. Braun SE, and Cardinal Health, competes through wider portfolios, long-standing clinical relationships, stronger regulatory coverage, and larger distribution systems. Regional manufacturers in China, India, and Eastern Europe continue to contest price-sensitive demand with latex and entry-level silicone products. Teleflex's planned sale of its Acute Care, Interventional Urology, and OEM businesses for USD 2.03 billion is an important shift because it can redistribute competitive weight across product lines where the company has been a long-standing participant.

Competitive pressure in the Foley catheters market is strongest in coating technology, where evidence, patent position, and manufacturing scale all shape pricing power. In May 2026, Bactiguard AB and BD restated and extended their global agreement, and the partnership has now distributed more than 245 million Bactiguard-coated Foley catheters worldwide under BD exclusivity outside China. That move shows how leading companies are tying proprietary coating technology more closely to global commercial reach. The Foley catheters market also still has open space in home-compatible and connected systems that can support monitoring and earlier infection detection, but no major company has yet established a broad commercial scale in that area.

Recent regulatory activity also keeps the competitive door open for well-funded entrants in the Foley catheters market. In January 2026, the U.S. FDA granted 510(k) clearance to Teleflex Medical Sdn. Bhd. for Rusch SoftSimplastic Foley Catheters under 21 CFR 876.5130, which reinforces the importance of regulatory continuity during portfolio restructuring. Geographic expansion into Gulf Cooperation Council states and parts of Sub-Saharan Africa also remains a practical path for companies that can build distribution before local manufacturing catches up. Firms that pair strong quality systems with pricing discipline are likely to gain faster in emerging markets than companies relying only on brand history. Technology-based differentiation in coatings, monitoring features, and home-use ergonomics is becoming a more decisive factor as the lower tier of the Foley catheters market stays fragmented and price pressure remains active.

Foley Catheters Industry Leaders

B. Braun SE

Cardinal Health, Inc.

Cook Medical LLC

Medtronic plc

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bactiguard AB and Becton, Dickinson and Company signed a restated long-term global agreement modernizing and extending their partnership across the full value chain from technology licensing to market execution. BD holds worldwide exclusivity, excluding China, for Bactiguard-coated Foley catheters, and the restated agreement expands scalable global access following the 2025 launch in India and BD's receipt of regulatory clearances enabling future European market launches. The partnership has distributed over 245 million Bactiguard-coated Foley catheters globally since its establishment.

- January 2026: The U.S. FDA granted 510(k) substantial equivalence clearance, K252537, to Teleflex Medical Sdn. Bhd. for Rusch SoftSimplastic Foley Catheters, confirming regulatory compliance under 21 CFR 876.5130. The clearance, based on a device submitted in August 2025, reinforces Teleflex's catheter regulatory portfolio ahead of the announced business restructuring.

Global Foley Catheters Market Report Scope

The Foley catheters market encompasses the global production, distribution, and use of indwelling urinary catheters designed to facilitate continuous bladder drainage in patients experiencing urinary retention, urinary incontinence, or requiring perioperative urinary management. Foley catheters are flexible tubes inserted into the bladder through the urethra and retained in place by an inflatable balloon. They are widely used across hospitals, long-term care facilities, ambulatory surgery centers, and home care settings for both short-term and long-term urinary management.

The foley catheters market is segmented by product type, material type, coating type, end user, and geography. Based on product type, the market is categorized into 2-way Foley catheters, 3-way Foley catheters, and 4-way Foley catheters. By material type, the market is segmented into latex, silicone, hydrophilic polymer-coated latex, silicone elastomer-coated latex, and PTFE-coated latex. Based on coating type, the market comprises antimicrobial-coated, hydrophilic or lubrication-coated, and uncoated Foley catheters. By end user, the market is divided into hospitals, ambulatory surgery centers, long-term care facilities, home care settings, and other end users, including clinics and medical research centers. Geographically, the market is analyzed across North America (United States, Canada, and Mexico), Europe (Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific), the Middle East & Africa (GCC, South Africa, and the Rest of the Middle East & Africa), and South America (Brazil, Argentina, and the Rest of South America).

| 2-Way Foley Catheters |

| 3-Way Foley Catheters |

| 4-Way Foley Catheters |

| Latex |

| Silicone |

| Hydrophilic Polymer Coated Latex |

| Silicone Elastomer Coated Latex |

| PTFE Coated Latex |

| Antimicrobial Coated |

| Hydrophilic or Lubrication Coated |

| Uncoated |

| Hospitals |

| Ambulatory Surgery Centers |

| Long-Term Care Facilities |

| Home Care Settings |

| Other End Users (Clinics, Medical Research Centers, among others) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | 2-Way Foley Catheters | |

| 3-Way Foley Catheters | ||

| 4-Way Foley Catheters | ||

| By Material Type | Latex | |

| Silicone | ||

| Hydrophilic Polymer Coated Latex | ||

| Silicone Elastomer Coated Latex | ||

| PTFE Coated Latex | ||

| By Coating Type | Antimicrobial Coated | |

| Hydrophilic or Lubrication Coated | ||

| Uncoated | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Long-Term Care Facilities | ||

| Home Care Settings | ||

| Other End Users (Clinics, Medical Research Centers, among others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 value expected for foley catheters?

The foley catheters market is projected to reach USD 4.19 billion by 2031, up from USD 3.28 billion in 2026, with a 5.02% CAGR over 2026-2031.

Which region leads current demand and which region grows fastest?

North America led with 37.63% share in 2025, while Asia-Pacific is projected to grow fastest at a 6.09% CAGR through 2031.

Which product type has the strongest current position?

2-Way Foley Catheters held the leading product share at 48.27% in 2025 because of broad use across hospital, ICU, and long-term drainage settings.

Which coating segment is expanding the fastest?

Hydrophilic or lubrication coated catheters are projected to grow at 7.53% CAGR through 2031, which is the highest segment growth rate in the report.

Why are hospitals still the largest end user?

Hospitals held 39.63% share in 2025 because acute procedures, ICU catheterization, and post-surgical monitoring are still concentrated in institutional care.

What is the main commercial risk for suppliers?

CAUTI risk remains the main commercial constraint because infection control programs shorten dwell time and raise product scrutiny, while each CAUTI event adds USD 13,793 in cost.

Page last updated on: