Flowable Hemostats Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

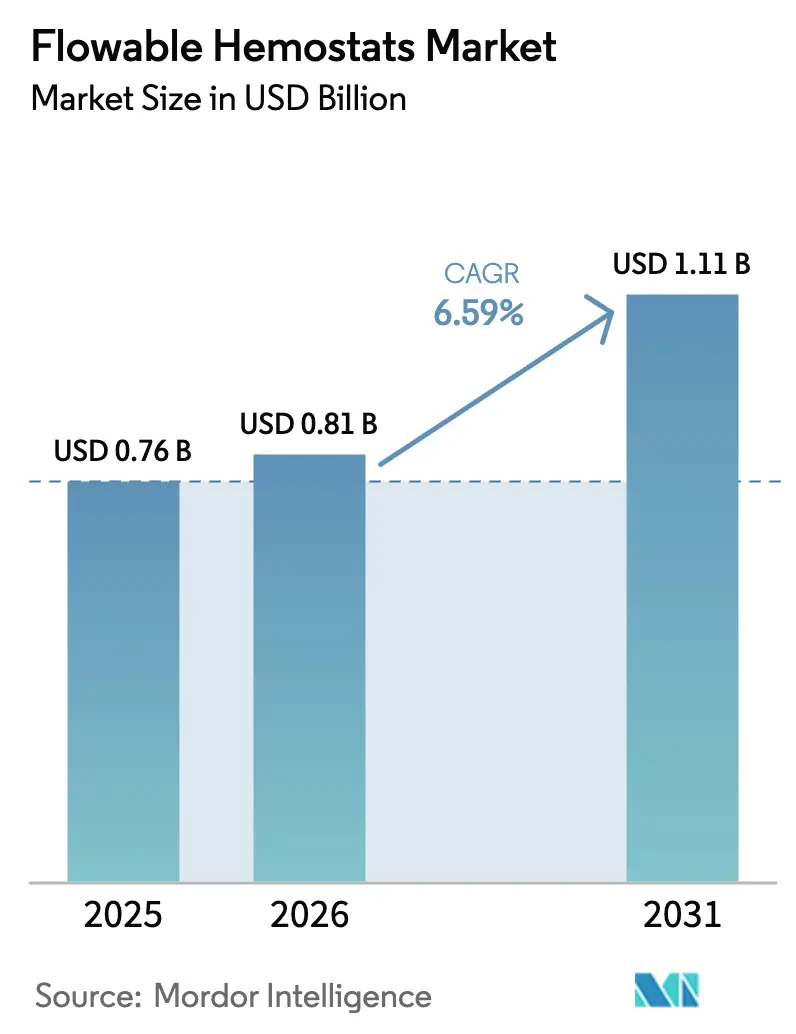

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.11 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flowable Hemostats Market Analysis by Mordor Intelligence

Flowable Hemostats Market size in 2026 is estimated at USD 0.81 billion, growing from 2025 value of USD 0.76 billion with projections showing USD 1.11 billion, growing at 6.59% CAGR over 2026-2031.

Growth is propelled by three durable shifts: larger elderly surgical cohorts, wider use of minimally invasive techniques that still demand rapid bleeding control, and the migration of complex procedures into ambulatory settings that favor ready-to-use hemostatic matrices. Gelatin-based formulations remained dominant, but hybrid and synthetic polymer products are winning share as surgeons prioritize multi-mechanism agents with faster time‐to‐hemostasis benchmarks. Cardiovascular surgery kept its lead in absolute volume, yet neurological procedures are advancing fastest because flowable agents can reach deep parenchymal sites. Hospitals continue to account for most consumption, while ambulatory surgical centers post the steepest growth as payers shift elective cases out of inpatient facilities.

Key Report Takeaways

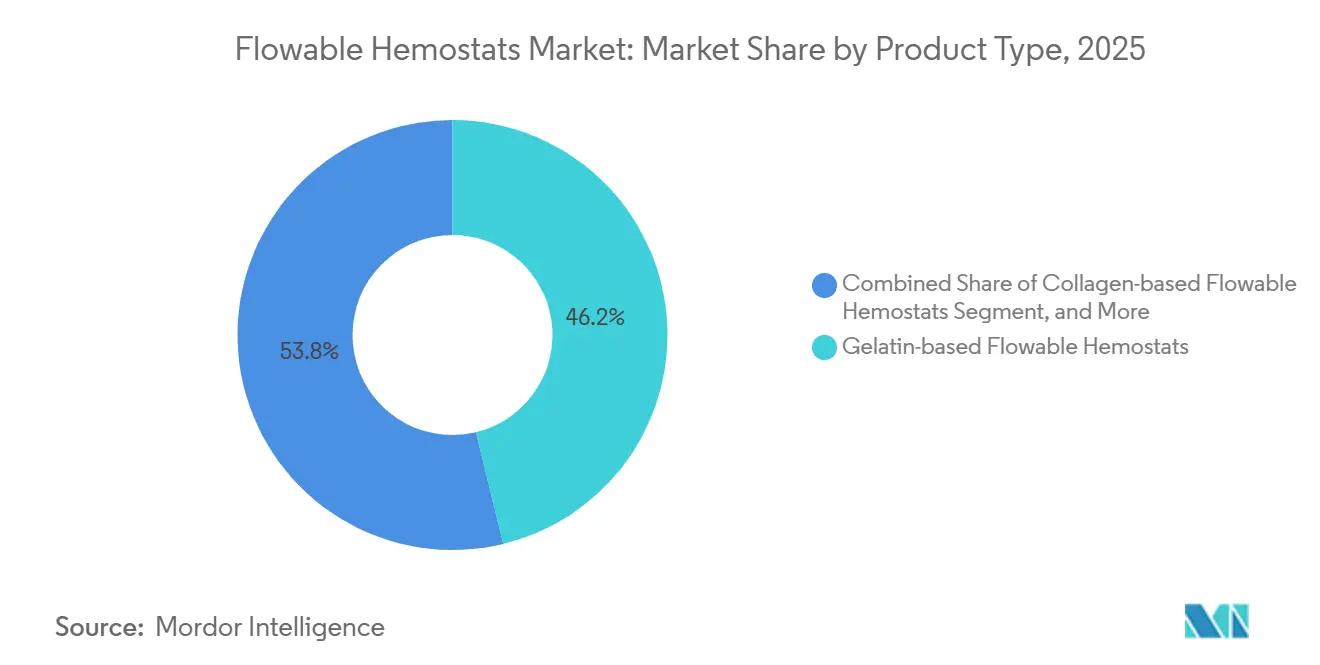

- By product type, gelatin-based systems captured 46.23% of the flowable hemostats market share in 2025, while combination and hybrid matrices are projected to expand at a 7.22% CAGR through 2031.

- By application, cardiovascular surgery led with 31.82% revenue share in 2025; neurological surgery is forecast to grow at 9.87% CAGR to 2031.

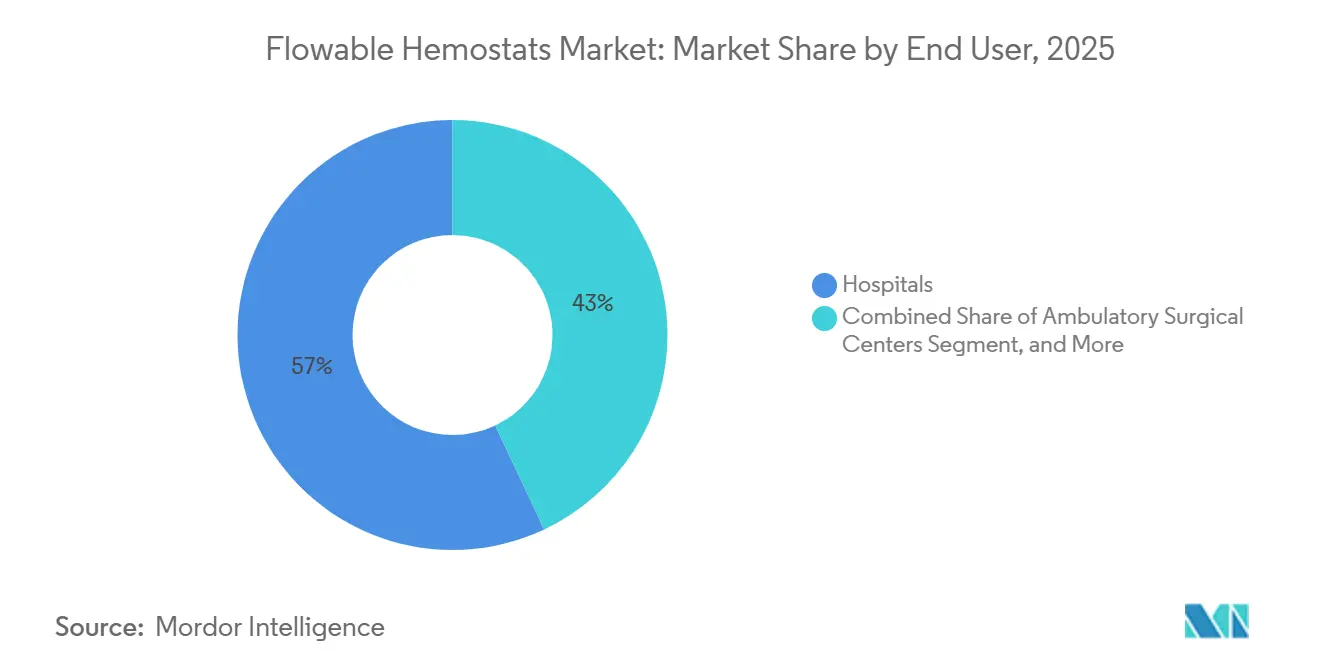

- By end user, hospitals held 57.03% of the flowable hemostats market share in 2025, while ambulatory surgical centers are advancing at an 8.42% CAGR through 2031.

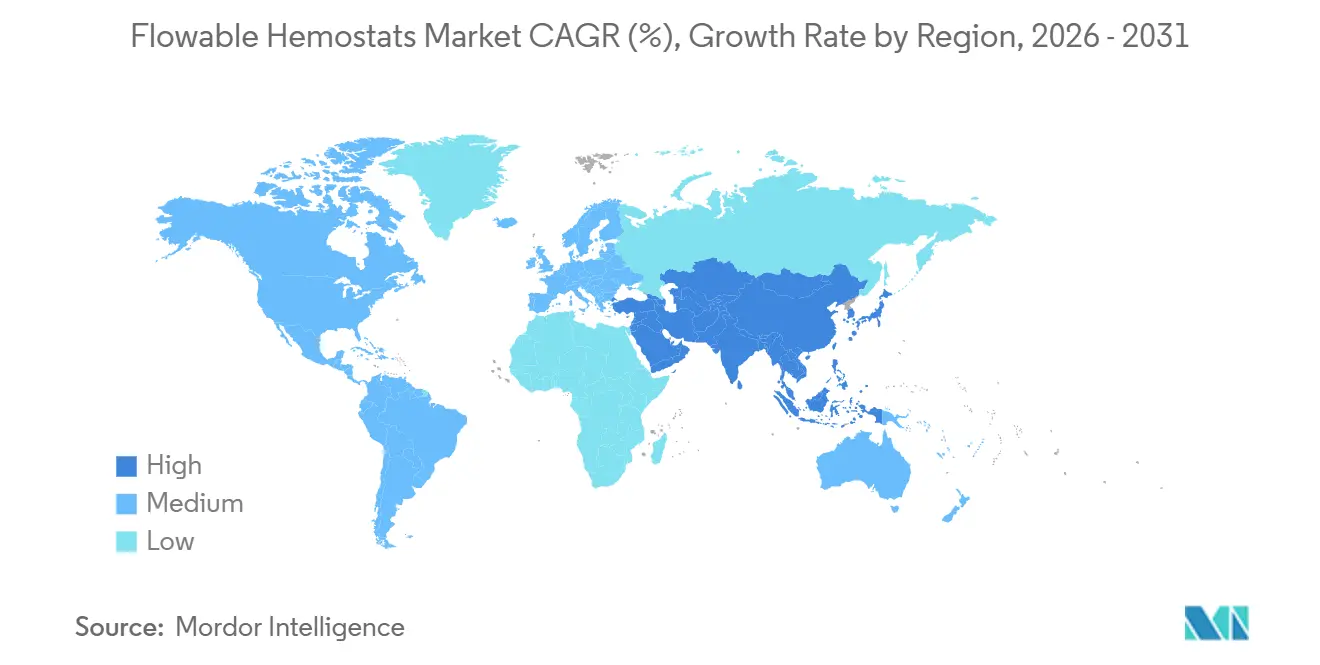

- By geography, North America contributed 36.51% of 2025 revenue; Asia-Pacific is on track to expand at 10.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flowable Hemostats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Surgical Procedure Volume Driven by Aging Populations | +1.8% | Global, acute in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Rising Adoption of Minimally Invasive Surgeries Requiring Effective Hemostasis | +1.5% | North America, EU, expanding into APAC metros | Medium term (2-4 years) |

| Favorable Reimbursement Frameworks and Quick Regulatory Clearances | +1.2% | United States, Germany, United Kingdom, France | Short term (≤ 2 years) |

| Increasing Prevalence of Bleeding Disorders and Anticoagulant Usage | +0.9% | Global, elevated in North America and Western Europe | Medium term (2-4 years) |

| Expansion of Hybrid ORs Demanding Versatile Flowable Hemostats | +0.7% | North America, Western Europe, select APAC metros | Medium term (2-4 years) |

| Value-Based Procurement Favoring Multi-Indication Matrices | +0.6% | United States, United Kingdom, Germany, Nordics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Surgical Procedure Volume Driven by Aging Populations

People aged 65 years and older are projected to reach 1.6 billion by 2050, doubling from 2025 levels.[1]United Nations, “World Population Ageing 2023,” UN.ORG That demographic surge drives higher demand for joint replacements, cardiovascular revascularizations, and oncologic resections, three categories that collectively account for the majority of flowable agent use. Asian nations feel the sharpest pressure; Japan’s median age exceeded 49 in 2025, while China had more than 280 million citizens aged 60 or older. Orthopedic trauma in elderly patients often involves anticoagulant therapy, elevating bleeding risk and prompting routine use of gelatin-thrombin matrices. European health systems expanded day-surgery capacity, adding 1,200 ambulatory operating rooms in Germany between 2024 and 2025 to manage patient throughput. Delayed hemostasis extends anesthesia time and lifts per-case costs by USD 500–800, making effective flowable products a financial imperative for procurement committees.

Rising Adoption of Minimally Invasive Surgeries Requiring Effective Hemostasis

Minimally invasive approaches reached 48% of elective general and gynecologic cases in the United States by 2025.[2]Centers for Medicare & Medicaid Services, “Hospital Outpatient Prospective Payment System,” CMS.GOV Laparoscopic and robotic methods limit surgeons’ ability to apply manual pressure, so flowable Hemostats are deployed through small trocars to quickly seal vascular pedicles. Robotic prostatectomy and nephrectomy volumes climbed 12% year-over-year in 2025, each relying on gelatin-based or synthetic polymer matrices that conform to irregular sites. Off-pump coronary bypass surgeries reported 22% lower transfusion requirements when fibrin-collagen combination agents were used, saving USD 1,200 in blood products per case. The FDA cleared Johnson & Johnson’s TRUFILL n-BCA liquid embolic in December 2025, underscoring regulatory support for innovative hemostatic formats tailored to minimally invasive settings. Ambulatory centers leverage pre-loaded syringes to reduce turnover time by up to 10 minutes, enabling an extra daily case.

Favorable Reimbursement Frameworks and Quick Regulatory Clearances in Major Markets

The dedicated U.S. reimbursement code C1849, effective January 2025, reimburses USD 180–220 per absorbable hemostat used in inpatient orthopedic and cardiovascular procedures. Utilization climbed 15% within six months of launch as hospitals no longer absorbed full device cost. In the European Union, Medical Device Regulation Class III reviews for flowable hemostats take 18–24 months, several months faster than for many implantable devices due to lower systemic risk. Baxter renewed its CE Mark for Hemopatch, with expanded pediatric cardiac indications, in April 2025, following a 96.7% success rate at 4 minutes. Japan’s Sakigake pathway cut review times in half for combination products, lifting early-market access for regional innovators.

Increasing Prevalence of Bleeding Disorders and Anticoagulant Usage

Direct oral anticoagulant prescriptions in the United States surpassed 35 million during 2025, up 9% year over year.[3]Centers for Disease Control and Prevention, “Anticoagulation Therapy,” CDC.GOV These agents prolong intraoperative bleeding time, prompting surgeons to use gelatin-thrombin or fibrin sealants that achieve hemostasis within a 5-minute window. Teleflex’s QuikClot Control+ showed 98.7% success in anticoagulated trauma patients after its March 2025 clearance. Elective surgeries in hemophilia and von Willebrand cohorts are also increasing as prophylactic therapies improve baseline coagulation, yet still require adjunctive mechanical-plus-biologic matrices. Each avoided red-blood-cell transfusion saves about USD 250 and reduces average length of stay by nearly two days, reinforcing economic value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Cost and Limited Reimbursement in Price-Sensitive Regions | -1.0% | Asia-Pacific (excluding Japan, South Korea, Australia), Middle East & Africa, South America | Medium term (2-4 years) |

| Stringent Storage & Handling Requirements Impacting Shelf Life | -0.6% | Global, with acute impact in tropical and sub-tropical regions (Southeast Asia, Sub-Saharan Africa, Latin America) | Short term (≤ 2 years) |

| Supply-Chain Volatility from Animal-Derived Gelatin Sources | -0.5% | Global, with concentrated risk in Europe and North America dependent on bovine/porcine sourcing | Medium term (2-4 years) |

| Surgeon Learning Curve and Perceived Redundancy with Sealants | -0.4% | Global, with higher friction in low-volume specialty clinics across all regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product Cost and Limited Reimbursement in Price-Sensitive Regions

With unit prices ranging from USD 150 to USD 300, many flowable agents exceed surgical consumable budgets in India, Brazil, and South Africa, where allocations average USD 80–120 per case. India’s Ayushman Bharat scheme lacks dedicated hemostat reimbursement, so public hospitals default to oxidized cellulose products that take three times longer to work. Brazil’s SUS flat reimbursement of USD 1,200 for elective orthopedic cases squeezes margins, keeping adoption below 15% in state facilities. Volume-based tenders can trim prices São Paulo hospitals obtained gelatin agents at USD 95 in 2025, but usage remains limited to high-risk surgeries. Import tariffs compound challenges; South Africa’s 15% medical-device duty raises landed prices, creating opportunities for local polysaccharide suppliers offering products at USD 60 per unit.

Stringent Storage and Handling Requirements Impacting Shelf Life

Conventional gelatin-thrombin matrices require refrigeration at 2–8 °C and must be mixed immediately before use, adding two to three minutes of OR time and generating waste when prepared syringes expire within two hours. Hot climates drive higher spoilage; Baxter reported 12–18% product loss in regions where ambient temperatures exceed 30 °C for much of the year. The firm’s 2025 room-temperature Hemopatch reformulation sidesteps cold-chain costs, but many competing collagen-fibrinogen patches still demand frozen storage and lengthy thaw times. Regulators now require rigorous prion and endotoxin testing on animal-derived gelatins, adding as much as USD 300,000 to new submissions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetic Polymers Gain Ground Despite Gelatin Dominance

The flowable hemostats market, by gelatin-based products, accounted for 46.23% of global revenue. Collagen variants provide surgeons with greater tensile strength along suture lines. Synthetic polymer agents represented a smaller base yet advanced at a 6.8% CAGR, propelled by demand for animal-free materials that deliver rapid hemostasis even in irrigated fields. Combination and hybrid matrices are the fastest-growing subset, forecast to outpace the overall flowable hemostats market CAGR through 2031.

Surgeon preference is shifting toward multi-mechanism formats that couple mechanical scaffolds with biologic or mineral procoagulants. Johnson & Johnson’s ETHIZIA patch achieved 80% hemostasis at 30 seconds, six times faster than older collagen-fibrinogen benchmarks, illustrating performance gains that justify premium pricing. Yet cost-conscious hospitals still rely on gelatin products priced at USD 120–180 per unit. Supply-chain volatility from bovine sources, highlighted by 2024 BSE outbreaks, underscores the strategic value of synthetic platforms that avoid animal raw materials altogether.

By Application: Neurological Surgery Outpaces Cardiovascular Growth

Cardiovascular procedures accounted for 31.82% of the flowable hemostats market revenue in 2025, reflecting the high bleeding risk inherent to bypass grafts and valve replacements. Gelatin-thrombin matrices cut transfusion rates by 22% in off-pump CABG cases, saving USD 1,200 per patient. Neurological surgery, while smaller in absolute terms, is projected to rise 9.87% annually through 2031 as agents that respect delicate cortical tissue gain broader adoption.

Johnson & Johnson secured FDA approval for TRUFILL n-BCA in December 2025, opening the door for liquid embolics specifically designed for intracranial bleeding. Orthopedic and trauma rely on collagen fibers that activate platelet adhesion within cancellous bone. General and abdominal surgeries account for 18%, with flowable products used to reinforce hepatic and colorectal anastomoses. Plastic, reconstructive, and other specialty fields take the remainder, expanding at mid-single-digit rates as ambulatory centers diversify case mixes.

By End User: ASCs Leverage Workflow Efficiency

Hospitals retained 57.03% of 2025 unit volume, driven by complex cardiovascular and neuro cases that require multiple SKUs for varied bleeding scenarios. Group purchasing organizations are narrowing formularies to two or three suppliers to reduce inventory complexity, reinforcing scale advantages for market leaders.

Ambulatory surgical centers are growing at an 8.42% CAGR in the flowable hemostats market. Ready-to-use syringes that can be stored at room temperature align with ASC staffing models by eliminating reconstitution delays. Specialty clinics, including orthopedic surgery and catheterization labs, account for about 8% of usage and favor single-step products that fit tight procedure windows. Channel migration toward outpatient settings rewards manufacturers able to supply ambient-stable, multi-indication lines in flexible pack sizes.

Geography Analysis

North America accounted for 36.51% of the flowable hemostats market revenue in 2025, with U.S. facilities accounting for 85% of regional demand following CMS's introduction of reimbursement code C1849. Canada gained momentum as Ontario and Quebec added hemostat coverage, expanding the addressable case base by 12%. Baxter renewed Hemopatch’s CE Mark in April 2025, extending indications into pediatric cardiac surgery after demonstrating a 96.7% four-minute hemostasis rate.

Asia-Pacific is the fastest-growing region, advancing at a 10.45% CAGR, driven by aggressive capacity additions. China built 2,800 tertiary hospitals between 2024 and 2026, many of which were fitted with hybrid ORs that require versatile hemostats. Japan’s Sakigake designation halved review times for novel collagen-thrombin matrices, supporting quick market entry for domestic innovators. India’s growth is constrained by reimbursement gaps, although private chains are adopting premium agents for high-risk cardiovascular cases. Middle East & Africa and South America combined contribute roughly 8%, with adoption limited by tariff and cold-chain hurdles that favor low-cost polysaccharide alternatives.

Competitive Landscape

The flowable hemostats market is moderately concentrated. Baxter cemented its lead by launching room-temperature Hemopatch in April 2025, reducing product loss due to refrigeration lapses by 18% at high-volume sites. Johnson & Johnson pursues a synthetic polymer roadmap, as evidenced by ETHIZIA’s 30-second performance, which shortens OR time and limits allergic risk.

Medtronic retains a strong position in cardiovascular indications, while Integra LifeSciences differentiates through pre-filled FlowSeal syringes that reduce nurse preparation time by 3 minutes per case. Stryker’s USD 4.9 billion acquisition of Inari Medical signals a push into vascular-access hemostasis, a U.S. category valued at USD 6 billion and growing 20% annually.

Smaller entrants like Arch Therapeutics and Biom'Up target fully synthetic platforms that bypass animal sourcing and simplify regulatory review. Regional manufacturers, notably Shandong Success Biological Technology, compete on price in emerging markets by offering polysaccharide products at USD 60 per unit. Filing trends under FDA 510(k) and EU MDR show rising emphasis on room-temperature stability and single-use packaging, underscoring workflow efficiency as a core battleground.

Flowable Hemostats Industry Leaders

Becton, Dickinson and Company

Johnson & Johnson

Integra LifeSciences Holdings Corporation

Teleflex Incorporated

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Johnson & Johnson received FDA approval for TRUFILL n-BCA, the first flowable neurovascular hemostat cleared for intracranial bleeding.

- April 2025: Baxter launched room-temperature-stable Hemopatch in Europe, extending shelf life to three years and removing cold-chain costs.

- April 2025: Teleflex obtained FDA 510(k) clearance for QuikClot Control+ with internal bleeding indication expansion.

- April 2024: Medcura closed USD 22.4 million financing to advance its surgical hemostatic gel pipeline.

Global Flowable Hemostats Market Report Scope

The Flowable Hemostats Market refers to the global industry for hemostatic agents in a flowable (gel-like or paste-like) form, designed to control bleeding during surgical procedures. These products combine absorbable hemostatic materials with carriers that allow them to be applied easily to irregular wound surfaces, making them especially useful in complex or minimally invasive surgeries.

The Flowable Hemostats Market Report is Segmented by Product Type (Gelatin-based, Collagen-based, Synthetic Polymer-based, Combination/Hybrid Matrices), Application (Cardiovascular, Orthopedic & Trauma, Neurological, General & Abdominal, Plastic & Reconstructive, Other), End User (Hospitals, ASCs, Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Value (USD).

| Gelatin-based Flowable Hemostats |

| Collagen-based Flowable Hemostats |

| Synthetic Polymer-based Flowable Hemostats |

| Combination / Hybrid Matrices |

| Cardiovascular Surgery |

| Orthopedic & Trauma Surgery |

| Neurological Surgery |

| General & Abdominal Surgery |

| Plastic & Reconstructive Surgery |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Gelatin-based Flowable Hemostats | |

| Collagen-based Flowable Hemostats | ||

| Synthetic Polymer-based Flowable Hemostats | ||

| Combination / Hybrid Matrices | ||

| By Application | Cardiovascular Surgery | |

| Orthopedic & Trauma Surgery | ||

| Neurological Surgery | ||

| General & Abdominal Surgery | ||

| Plastic & Reconstructive Surgery | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the flowable hemostats market in 2026?

The flowable hemostats market size reached USD 0.81 billion in 2026 and is projected to grow at a 6.59% CAGR to 2031.

Which product segment is expanding fastest?

Combination and hybrid matrices are forecast to rise at 7.22% CAGR through 2031 as surgeons favor multi-mechanism agents.

Why is Asia-Pacific growing more rapidly than other regions?

Aging populations and large-scale hospital expansion in China, India, and Japan fuel double-digit growth despite reimbursement gaps.

What advantage do synthetic polymer hemostats offer?

Synthetic polymers eliminate animal sourcing, reduce allergy risk, and achieve hemostasis in as little as 30 seconds, cutting OR time.

How are ambulatory surgical centers influencing demand?

ASCs prefer room-temperature, ready-to-use syringes that accelerate turnover, driving an 8.42% CAGR in this channel.

Page last updated on: