Flexible Spinal Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.48 Billion |

| Market Size (2031) | USD 7.06 Billion |

| Growth Rate (2026 - 2031) | 9.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Spinal Implants Market Analysis by Mordor Intelligence

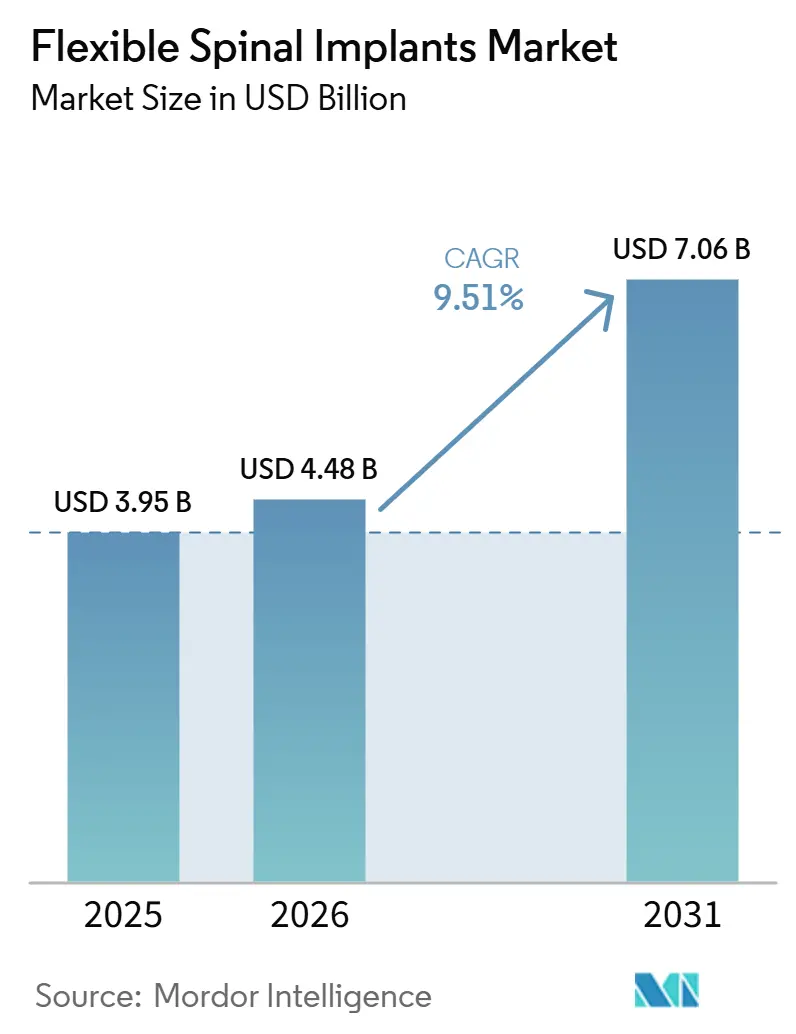

The Flexible Spinal Implants Market size is projected to be USD 3.95 billion in 2025, USD 4.48 billion in 2026, and reach USD 7.06 billion by 2031, growing at a CAGR of 9.51% from 2026 to 2031.

The current shape of the flexible spinal implants market reflects a demand base that is being supported by population aging, a rising burden of degenerative spine conditions, and a larger pool of patients who now need treatment after years of delayed or incomplete care for musculoskeletal disorders. Clinical practice is also moving away from rigid fusion alone and toward constructs that preserve motion, reduce stiffness, and improve functional recovery in selected cases, which is strengthening the case for dynamic fixation and arthroplasty across the flexible spinal implants market. Competitive positioning in the flexible spinal implants market is increasingly shaped by ecosystem depth rather than implant design alone, as planning software, navigation, robotics, and implant compatibility now influence surgeon choice and hospital adoption at the same time. Recent portfolio realignment among larger companies has opened room for mid-sized vendors that can serve community hospitals and outpatient settings with simpler workflows, while premium technology platforms continue to raise the capital threshold for smaller stand-alone implant suppliers. Growth opportunities remain strongest where outpatient spine procedures are expanding and where hospitals are upgrading surgical infrastructure, although procedure cost, evidence requirements for newer motion-preserving devices, and uneven payer support still limit the pace of adoption across several healthcare systems.

Key Report Takeaways

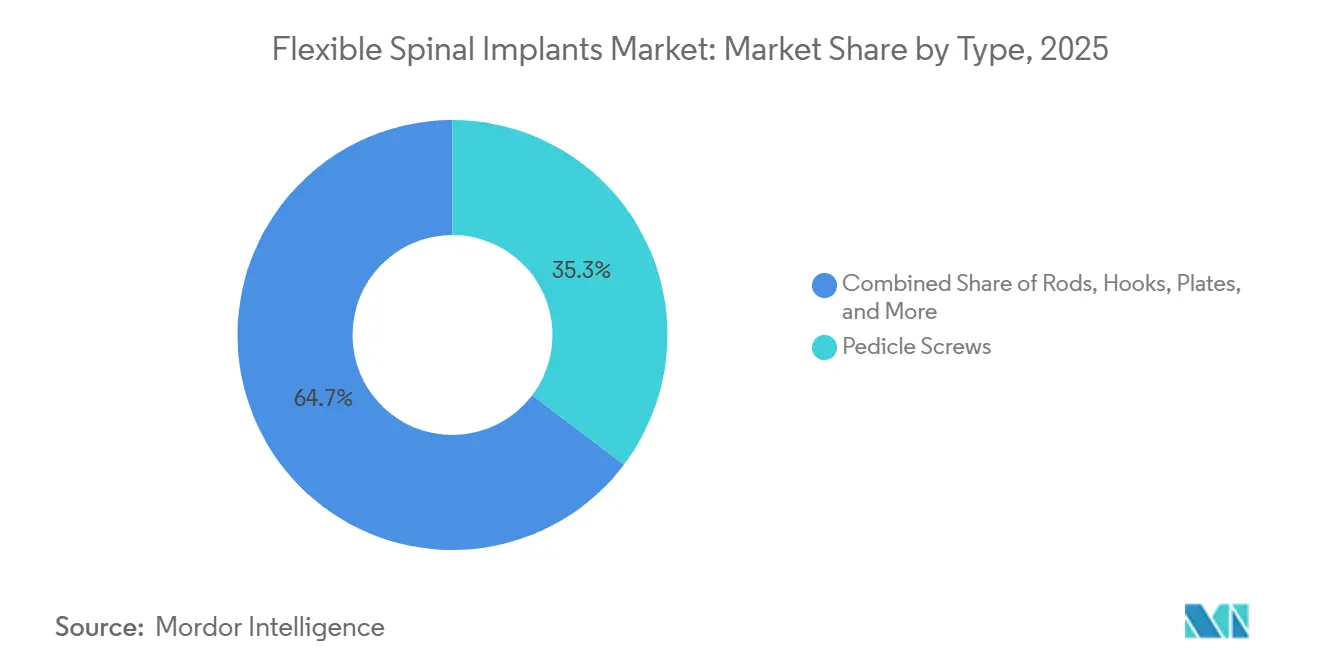

- By type, pedicle screws led with 35.31% revenue share in 2025, while rods are expected to have the highest projected CAGR at 10.38% through 2031.

- By product type, dynamic stabilization devices held 45.24% revenue share in 2025, while motion preservation devices are forecast to expand at a 10.52% CAGR through 2031.

- By material, titanium accounted for 56.64% revenue share in 2025, while PEEK is expected to post the fastest projected CAGR at 11.62% through 2031.

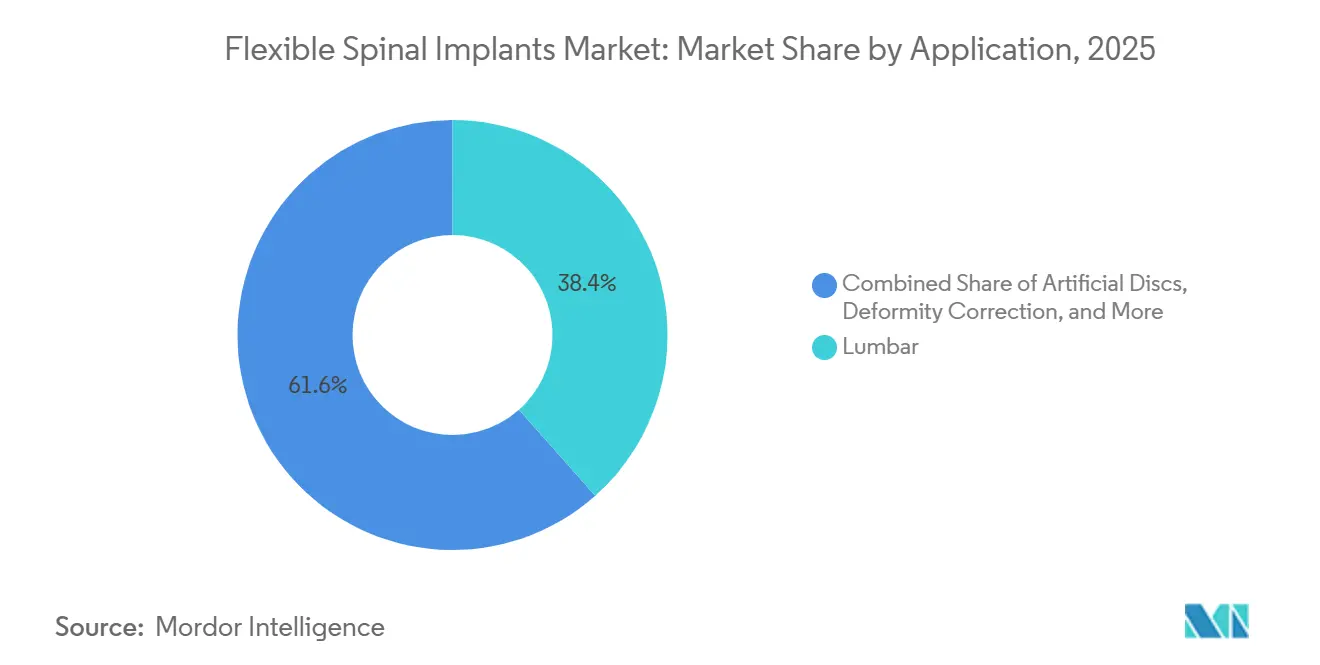

- By application, lumbar procedures captured 38.44% revenue share in 2025, while artificial discs are expected to advance at a 10.63% CAGR through 2031.

- By end user, hospitals commanded 52.26% revenue share in 2025, while ambulatory surgical centers are projected to grow at a 10.95% CAGR through 2031.

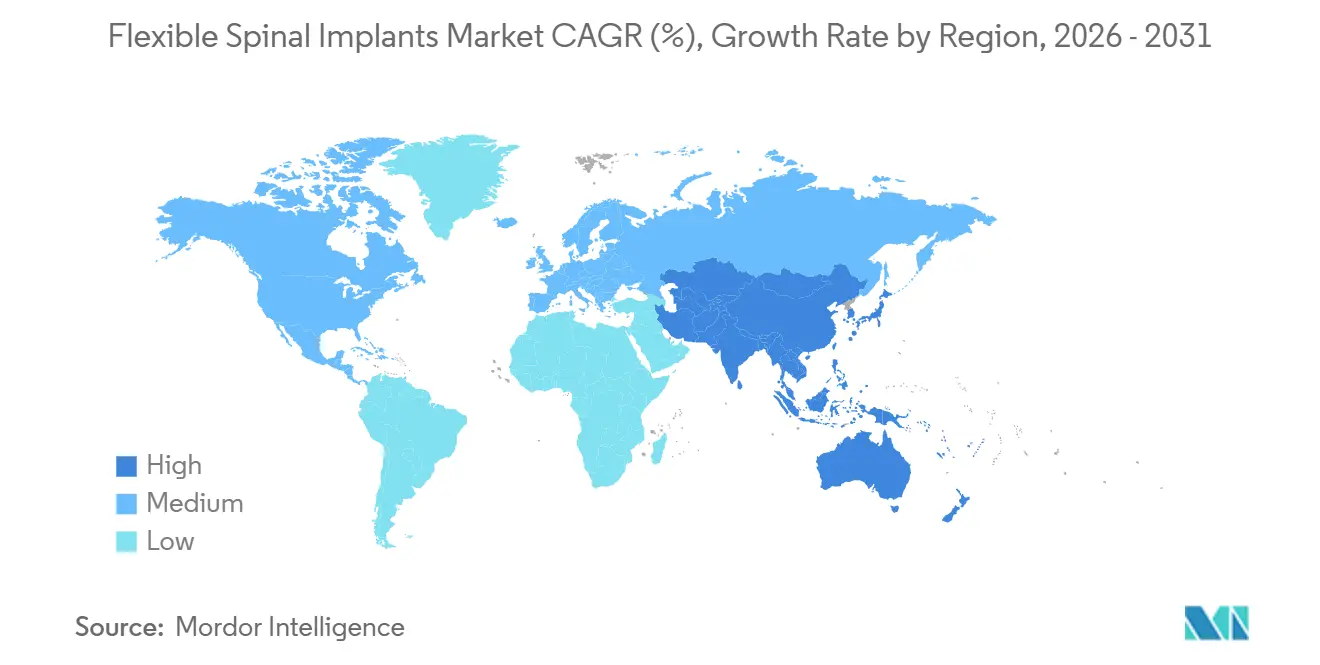

- By geography, North America held 41.61% revenue share in 2025, while Asia-Pacific is expected to expand at a 10.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flexible Spinal Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Spine Disease Burden and Revision Backlog | +2.8% | Global, concentrated in North America, Western Europe, and East Asia | Long term (≥ 4 years) |

| Shift Toward Motion Preservation | +2.1% | North America and Western Europe, with early adoption in Asia-Pacific | Medium term (2-4 years) |

| Expanded Use in Ambulatory Surgical Centers | +1.5% | North America primarily, Western Europe secondarily | Medium term (2-4 years) |

| Patient-Specific Implant Design and Navigation Planning | +1.0% | North America, Germany, and Australia | Long term (≥ 4 years) |

| Reimbursement Support for Procedure Efficiency and Recovery | +0.8% | North America and Western Europe | Medium term (2-4 years) |

| Under-Served Degenerative and Deformity Cases in Emerging Markets | +0.7% | China, India, Brazil, and GCC countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Spine Disease Burden And Revision Procedure Backlog

The flexible spinal implants market is being supported by a durable rise in the number of older patients living with chronic degenerative spine disorders, and that demand base is likely to stay in place through the forecast period. The burden figures across 204 countries show that musculoskeletal disease is rising with aging populations, which directly strengthens the procedure pipeline for devices used in stabilization, decompression support, and motion-preserving repair. A second layer of demand comes from revision cases, because many patients who received rigid fusion earlier are now reaching the stage where adjacent segment stress and long-term mechanical limitations require new intervention. That revision pool matters because repeat procedures often call for more nuanced fixation choices, and those cases support higher-value use of dynamic systems rather than a simple repeat of traditional rigid constructs. This also changes revenue mix inside the flexible spinal implants market, because growth is being shaped not only by a larger patient base, but also by a higher share of complex and clinically selective procedures. The result is a market where demand is becoming deeper and more persistent, even when procedure growth and hospital budgeting do not move at the same speed.

Shift From Rigid Fusion Toward Motion Preservation

The flexible spinal implants market is also benefiting from a clear clinical shift toward devices that protect motion and reduce the long-term drawbacks seen with rigid fusion in selected patient groups. Published 2025 evidence showed that dynamic fixation systems produced lower postoperative stiffness, better range of motion preservation, and stronger paraspinal muscle outcomes than rigid fusion in the studied cohort, which gives surgeons a stronger evidence base when deciding between fixation strategies. Long-term review literature also supported lower reoperation rates at adjacent segments for motion-preserving techniques in several follow-up comparisons, which matters because payers and providers are placing more weight on downstream revision risk and long-term function. As more preoperative planning systems incorporate alignment modeling and dynamic construct behavior, the discussion with patients is becoming more focused on functional recovery rather than only on short-term stabilization, and that is helping the flexible spinal implants market move further toward non-fusion options. This shift is still selective and does not replace fusion in every indication, but it is widening the commercial path for arthroplasty and dynamic stabilization across both cervical and lumbar procedures. Over time, companies with complete motion-preservation portfolios should benefit more than companies that remain centered only on rigid hardware.

Expanded Use In Ambulatory Surgical Centers

The flexible spinal implants market is being reshaped by the steady movement of spine procedures into ambulatory surgical centers, especially in the United States where reimbursement and workflow efficiency increasingly favor outpatient care. CMS expanded the framework for outpatient spine work in 2025 by adding 32 new separately payable procedures, and that policy move continues to support migration away from inpatient settings for suitable cases[1]Centers for Medicare & Medicaid Services, “Ambulatory Surgical Center Payment Update, January 2025,” CMS, cms.gov. In 2026, robotic-assisted spine surgery in an ASC setting also moved from a theoretical possibility to a real operating example, which matters because technology barriers are one of the main limits on outpatient case complexity. New center launches and dedicated orthopedic and spine facilities are reinforcing this direction by adding operating capacity that is built around specialist throughput and more standardized procedure flow. For suppliers, this changes purchasing behavior because ASC administrators are more sensitive to tray count, setup time, and instrument simplicity than large inpatient procurement teams. That means the flexible spinal implants market is rewarding vendors that design for outpatient compatibility from the start, rather than vendors that try to scale down hospital systems after launch.

Patient-Specific Implant Design And Navigation-Enabled Planning

The flexible spinal implants market is moving into a stage where software, navigation, and patient-specific design carry more strategic weight, because they directly affect reproducibility, implant fit, and procedural confidence. Medtronic’s Stealth AXiS system, cleared by the FDA in February 2026, brought planning, navigation, and robotics into one integrated platform and introduced real-time alignment visibility during surgery, which makes workflow integration a more important commercial lever in the flexible spinal implants market. Clinical work in 2025 also showed favorable fusion outcomes for 3D-printed titanium patient-specific interbody cages, with fewer than 2% of patients requiring reoperation for mechanical issues within one year, which supports the use of customized implants in anatomically demanding cases. That evidence matters because it shifts attention upstream, away from the implant as a stand-alone item and toward the planning environment that determines what implant is selected and how it is placed. As that shift continues, companies that control the planning layer can create stronger surgeon retention and better pull-through for downstream implant sales. The flexible spinal implants market therefore faces a competitive model where data, workflow, and customization increasingly matter as much as traditional hardware breadth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implant and Procedure Cost | -1.2% | Global, most acute in emerging Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Regulatory and Clinical Evidence Burden for Novel Devices | -0.9% | Global, with concentrated impact in North America and Europe | Long term (≥ 4 years) |

| Surgeon Learning Curve and Technique Sensitivity | -0.5% | Global, especially where advanced training infrastructure is limited | Medium term (2-4 years) |

| Long-Term Durability and Revision Uncertainty for Non-Fusion Constructs | -0.4% | Global, with payer sensitivity highest in North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implant And Procedure Cost

The flexible spinal implants market still faces a clear adoption barrier from procedure cost, especially in health systems where premium implants, navigation tools, and robotic support sit well above budget limits for routine spine care. Advanced motion-preserving systems already carry high device costs, and the total episode cost rises further when capital-intensive enabling technologies are added to the procedure stack. That cost issue matters most in emerging growth regions, because those are the markets expected to add new procedure volume, yet they are also the places where price sensitivity is strongest and payer support is least consistent. Cost pressure is not evenly distributed across the flexible spinal implants market, because mature regions can absorb premium pricing more easily while many faster-growing systems still depend on lower-cost conventional fixation pathways. This creates a structural tension where companies need global growth but cannot assume that premium product economics will transfer smoothly outside established reimbursement environments. Vendors with modular product lines, flexible pricing architecture, and a practical path into lower-cost care settings are therefore better positioned than vendors that rely only on high-ASP technology bundles.

Regulatory And Clinical Evidence Burden For Novel Motion-Preserving Devices

The flexible spinal implants market also remains constrained by the long regulatory and evidence path required for novel motion-preserving devices, because these products carry higher scrutiny than incremental updates to existing fixation systems. In the United States, Medtronic’s path from Breakthrough Device Designation for INFUSE in 2024 to FDA approval in February 2026 shows that accelerated routes exist, but they still depend on strong clinical justification and well-supported trial evidence[2]Medtronic, “Medtronic Announces FDA Approval of Infuse Bone Graft for TLIF Spine Procedures,” Medtronic News, medtronic.com. In Europe, the more demanding device environment for Class III implants extends certification work, increases clinical follow-up requirements, and adds cost for manufacturers that want to scale flexible or non-fusion technologies across multiple markets. This matters because a company can clear a product in one region and still face a long wait before full commercial access opens elsewhere, which delays revenue capture during the period when the product is still new and strategically important. The evidence burden also affects smaller companies more sharply, because they usually have narrower clinical databases and less capacity to fund multi-market approval programs. As a result, the flexible spinal implants market often favors larger vendors that can absorb long approval cycles while maintaining surgeon engagement and post-market data generation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pedicle Screws Anchor Volume, Rods Lead Growth

Pedicle screws retained the largest position in the flexible spinal implants market by type with 35.31% revenue share in 2025, reflecting their central role across lumbar, thoracic, and cervical fixation pathways where posterior instrumentation remains the base of surgical stability. Their leadership is tied to clinical versatility, because the same screw platform can be used with rigid or dynamic constructs and can support a wide range of deformity, degenerative, and trauma procedures. That breadth keeps pedicle screws deeply embedded in surgeon workflow and hospital inventory strategy, which makes them harder to displace than more specialized device categories. The same aging-related disease burden that is increasing overall procedure volumes also reinforces demand for these systems, since posterior fixation often remains necessary even when the broader treatment philosophy shifts toward motion preservation. In practice, pedicle screws benefit from being both clinically foundational and commercially adaptable, which explains why this segment remains the scale anchor inside the flexible spinal implants market.

Rods are projected to record the fastest type-level expansion at a 10.38% CAGR through 2031, which reflects material innovation and a broader move toward load-sharing systems that reduce excessive segment stiffness. Much of this growth is linked to the substitution of conventional rod configurations with PEEK and hybrid titanium-PEEK designs that aim to improve biomechanics around adjacent levels. The flexible spinal implants market is also seeing continued use of hooks in selected pediatric and thoracic deformity cases where anatomy or construct strategy limits screw placement. Plates remain important in anterior cervical fixation, while cages across ALIF, TLIF, and PLIF procedures continue to evolve through porous titanium and hybrid material formats that improve osseointegration and imaging compatibility. Stryker’s Spine Guidance 5 software with Copilot adds another layer to this segment, because AI-assisted screw trajectory support reduces placement variability and strengthens the value of compatible fixation workflows rather than only the implant itself. Taken together, these shifts show that the type mix in the flexible spinal implants market is changing less through replacement of pedicle screws and more through smarter integration of the hardware around them.

By Product Type: Dynamic Stabilization Scales, Motion Preservation Accelerates

Dynamic stabilization devices held 45.24% of the flexible spinal implants market size in 2025, which shows that the largest revenue base still sits in systems designed to stabilize the spine without imposing the full motion restriction associated with rigid fusion. These devices have built an established clinical position in lumbar stenosis and early degenerative disease, where surgeons often want a middle path between conservative care and full arthrodesis. Their commercial strength also comes from procedural familiarity, because dynamic systems have been part of surgeon decision-making longer than some of the newer arthroplasty pathways. North America and Western Europe remain the most mature settings for this product category, while adoption in several newer regions is still shaped by training access and local reimbursement design. That maturity gives dynamic stabilization a stable base inside the flexible spinal implants market even as newer motion-preserving technologies attract a larger share of future attention.

Motion preservation devices are projected to expand at a 10.52% CAGR through 2031, making them the fastest-growing product category as evidence continues to support better function and lower adjacent segment stress in appropriately selected patients. Comparative literature in 2025 found that cervical and lumbar motion-preserving procedures often delivered stronger range of motion outcomes and more favorable reoperation patterns than conventional fusion, which supports broader surgeon confidence for these devices. The flexible spinal implants market is therefore moving toward a product mix where non-fusion systems no longer sit at the edge of adoption but increasingly shape center-stage competitive strategy. Other categories such as interspinous implants and facet replacement systems still hold a narrower role, especially where simplicity, speed, and outpatient suitability matter more than full platform breadth. Over time, product winners in the flexible spinal implants market are likely to be those that combine strong clinical outcomes with workflow ease, rather than those that rely only on a premium technology position.

By Material: Titanium Leads, PEEK Momentum Reshapes Material Economics

Titanium accounted for 56.64% of the flexible spinal implants market share in 2025, which reflects the material’s long clinical history, strong biocompatibility, and continued relevance across fixation hardware and interbody systems. Titanium remains the default choice in many operating environments because surgeons trust its long-term behavior and manufacturers can adapt it to both standard and advanced designs. Additive manufacturing is reinforcing that lead, especially through porous titanium cages that aim to improve bone ingrowth and better serve complex revision or deformity cases where anatomy does not fit conventional geometries. The flexible spinal implants market also benefits from titanium’s flexibility in product design, because it works across core fixation systems, patient-specific implants, and hybrid surface technologies. Evidence published in 2025 further supported this direction by showing earlier fusion for titanium-coated PEEK cages than for uncoated PEEK in lumbar procedures, which highlights how titanium-based performance features continue to influence material choice even beyond all-metal implants.

PEEK is forecast to grow at an 11.62% CAGR through 2031, making it the fastest-rising material segment as surgeons place more value on radiolucency and an elastic modulus that is closer to bone behavior. Postoperative imaging clarity remains a major commercial advantage for PEEK, because it can simplify fusion assessment and reduce interpretive limits that arise with more opaque materials. In March 2025, Globus Medical launched the COHERE ALIF Spacer as the first porous PEEK interbody spacer for anterior lumbar interbody fusion, showing how suppliers are directly addressing the material’s historical osseointegration weakness through surface and structural innovation. Stainless steel still retains some presence in lower-acuity trauma work and in price-sensitive settings, but its role continues to narrow as titanium and advanced polymer systems offer stronger clinical and workflow advantages. A 2025 meta-analysis found no statistically significant difference in adjacent segment disease rates between PEEK and titanium rods after posterior lumbar fusion, which suggests that material choice in the flexible spinal implants market is increasingly shaped by imaging needs and surgical preference rather than by a clear long-term superiority signal. This means material competition is becoming less about replacement of one class by another and more about how each material can be engineered to fit specific procedural priorities.

By Application: Lumbar Dominates, Artificial Disc Demand Builds

Lumbar procedures captured 38.44% of the flexible spinal implants market size in 2025, which reflects the large global burden of lumbar degenerative disease and the broad use of instrumentation across decompression, stabilization, fusion, and motion-preserving treatment paths. The lumbar spine remains the largest treatment field because it carries a heavy share of chronic pain, disability, and structural degeneration across aging and working-age populations, which keeps surgical need elevated over time. It also offers a wider set of surgical approaches, including ALIF, TLIF, PLIF, LLIF, and lateral corpectomy, which gives providers more flexibility to match anatomy, setting, and instrumentation strategy. Cervical procedures hold the next major position, supported by rising cervical disc arthroplasty volumes and by an evidence base that continues to expand around non-fusion care. Thoracic applications remain more specialized, but they still matter because deformity correction and trauma treatment often involve technically demanding instrumentation with higher average selling prices than routine cases.

Artificial discs are forecast to expand at a 10.63% CAGR through 2031, making them the fastest-growing application area as surgeon confidence, clinical evidence, and reimbursement support continue to improve. The strongest momentum has come from cervical disc replacement, where modeling published in early 2026 projected robust long-term utilization growth for single-level procedures in the U.S. Medicare population. That pattern matters for the flexible spinal implants market because it normalizes disc arthroplasty in mainstream care rather than limiting it to select specialist centers. Deformity correction and spinal fusion surgery remain high-volume and clinically necessary applications, but their growth is more mature and less disruptive to the competitive mix. Trauma treatment continues to provide a stable procedural base, particularly where road accident burden and acute care demand support steady instrumentation needs. The broader direction across applications shows a gradual but meaningful shift toward function-preserving care, which benefits companies that can cover both conventional and motion-preserving procedure pathways.

By End User: Hospitals Stay Central, ASCs Expand Access

Hospitals held 52.26% revenue share in the flexible spinal implants market in 2025, reflecting their continued importance in complex deformity, revision, multi-level reconstruction, and high-acuity trauma cases that still require broader postoperative support. Large hospital systems and academic medical centers also remain the primary entry point for newly cleared technologies, because they have the staff depth, capital base, and case complexity needed to validate advanced navigation, robotics, and patient-specific implant workflows. This makes hospitals a strategic reference channel even when overall case migration is moving toward outpatient care. The flexible spinal implants market still depends on hospitals to establish procedure credibility for new technologies before those technologies spread more widely into smaller facilities. That role is especially important for solutions that combine implants with planning software or robotic navigation, because early adoption depends as much on training and protocol development as on the hardware itself.

Ambulatory surgical centers are projected to grow at a 10.95% CAGR through 2031, making them the fastest-growing end-user channel as reimbursement support, specialist workflows, and lower-cost care models keep strengthening. The 2025 CMS update widened the outpatient reimbursement framework, and that continues to support more spine procedures in the ASC setting. In 2026, new ASC openings dedicated to orthopedic and spine care showed how providers are adding procedure capacity around focused workflows rather than around broader hospital service lines[3]Ascension, “Ascension St. Vincent’s and Southeast Orthopedic Specialists Open Ambulatory Surgery Center in St. Augustine,” Ascension, ascension.org. Robotic-assisted spine surgery performed in an ASC in 2026 also signals that the outpatient ceiling for case complexity is moving upward, which will widen the addressable opportunity for ASC-ready implant systems. Specialty spine clinics remain a useful niche in the flexible spinal implants market because their consultation depth and imaging focus can improve conversion into elective deformity and motion-preserving procedures.

Geography Analysis

North America held 41.61% of the flexible spinal implants market share in 2025, giving it the leading regional position through a combination of high procedure volumes, established reimbursement, and dense concentration of advanced spine centers. The United States accounted for the largest part of that regional base because it combines trained surgeon availability, broad use of navigation tools, and a strong shift toward outpatient spine care. The flexible spinal implants market in North America also benefits from regulatory momentum that supports product visibility, as shown by the FDA clearance of Medtronic’s Stealth AXiS system in February 2026 and the region’s continued role as a first commercialization step for many advanced platforms. CMS policy is reinforcing that demand by widening the outpatient spine reimbursement framework, which strengthens implant pull-through in ASCs and other efficient elective settings. Canada and Mexico add smaller but relevant volumes, with Canada constrained more by public budgeting and Mexico supported more by private hospitals and medical tourism.

Europe remains the next major regional pillar in the flexible spinal implants market, supported by Germany, France, and the United Kingdom where aging populations and established surgeon training keep procedure demand stable. The region’s stricter device environment increases the evidence threshold for flexible and motion-preserving implants, which raises lifecycle management costs but also benefits larger companies with stronger clinical datasets and compliance infrastructure. Germany stands out because its evidence-driven reimbursement structure supports measured adoption of non-fusion technologies when clinical support is strong. Other European countries, including Spain, Italy, and the Nordic markets, continue to build demand through aging demographics and ongoing investment in robotic and navigation-assisted surgical capability.

Asia-Pacific is projected to grow at a 10.65% CAGR through 2031, making it the fastest-growing regional segment in the flexible spinal implants market as China and India continue to expand tertiary care capacity and spine surgery access. The region’s growth case is strengthened by a large aging population base and by a broader shift toward advanced surgical infrastructure in major urban centers. China’s largest city hubs are likely to remain the first point of adoption for navigation-integrated and motion-preserving procedures before those approaches spread into a wider hospital network. Japan, South Korea, and Australia provide a more stable high-value layer of demand where advanced procedure standards and reimbursement support already exist, even if adoption growth is less dramatic than in China or India. Outside Asia-Pacific, GCC countries continue to build tertiary hospital capability, and South America still offers room for selective expansion where provider infrastructure and affordability align with product positioning. Overall, regional growth in the flexible spinal implants market is likely to be uneven, with North America setting the technology pace, Europe shaping the evidence standard, and Asia-Pacific driving the strongest volume expansion.

Competitive Landscape

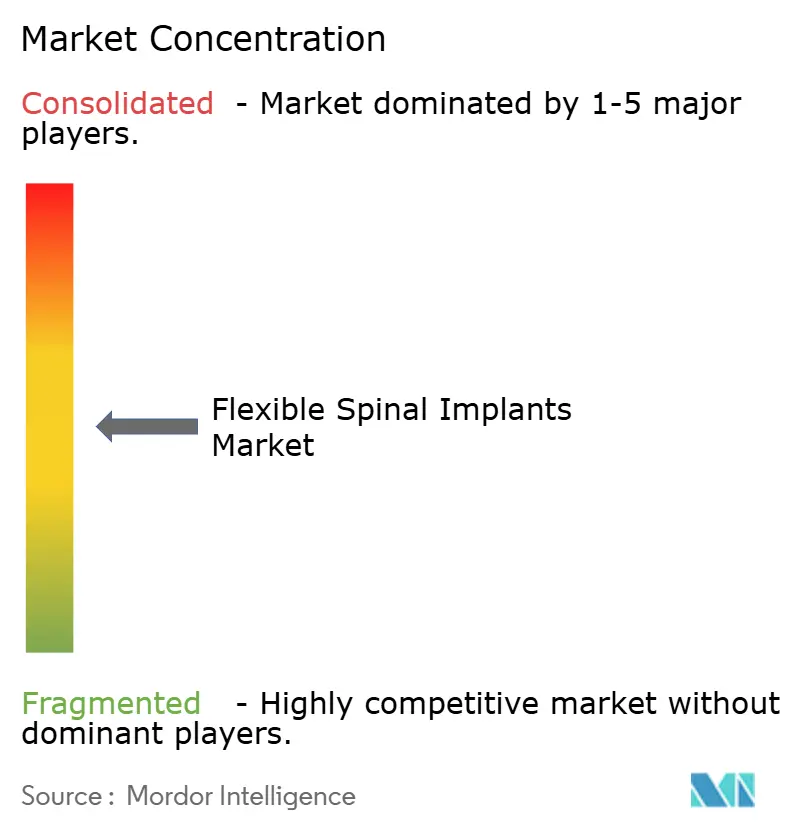

The flexible spinal implants market operates with moderate consolidation, where scale matters, but where a full lock on demand remains limited by the number of established companies that compete across fixation, arthroplasty, navigation, and biologic adjacencies. Medtronic and Globus Medical remain the strongest competitive reference points in the United States, especially in navigation-linked fixation systems and posterior thoracolumbar instrumentation. Stryker’s completed sale of its U.S. spinal implants business in April 2025 changed the competitive structure by moving those assets into VB Spine and by concentrating more attention on which companies can fill the next tier below the largest leaders. That shift matters because it creates fresh room in community hospitals and ASC-focused channels, where product simplicity and workflow fit can matter more than sheer breadth of installed capital systems. DePuy Synthes, Centinel Spine, B. Braun Melsungen, Orthofix Medical, and Highridge Medical continue to occupy important middle positions through portfolio depth, geographic reach, and the ability to support different surgeon preferences across core procedure categories.

The flexible spinal implants market is also seeing a sharper divide between ecosystem players and hardware-only players, because planning software, navigation, and data integration are becoming more central to long-term account control. Medtronic’s June 2025 launch of the CD Horizon ModuLeX spinal system within the AiBLE ecosystem is a good example, since it ties implant selection more closely to digital workflow and makes switching less attractive once surgeons are trained inside that environment. Alphatec has built a differentiated position through its PTP approach and continued procedure innovation, including the 2025 launch of PTP Corpectomy, which strengthens its visibility among surgeons seeking workflow differentiation in lateral access surgery. Its January 2026 strategic partnership with Theradaptive also shows how companies are trying to extend value beyond core implants and into adjacent regenerative solutions that may improve procedure pull-through over time. Personalized Spine adds another competitive signal because its patient-specific planning and implant model is built around measurable surgical fit and low reoperation expectations, which speaks directly to provider and payer interest in better downstream outcomes. These examples show that competition in the flexible spinal implants market now extends across clinical design, workflow control, surgeon training, and proof of economic value.

A large share of open opportunity sits in lumbar motion preservation, ASC-oriented implant systems, and solutions that match the capital realities of emerging healthcare systems. Smaller and mid-sized vendors can still gain ground if they build around these gaps instead of trying to match the broadest portfolio players head to head. The flexible spinal implants market therefore rewards selective strategy more than generic scale, especially where outpatient migration and planning-led surgery are changing how purchase decisions are made. At the same time, larger companies still hold an advantage in evidence generation, regulatory endurance, and integrated platform adoption, which means the competitive field remains active but not fully open.

Flexible Spinal Implants Industry Leaders

Medtronic plc

Globus Medical, Inc.

Stryker Corporation

Orthofix Medical Inc.

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Moscow Aviation Institute (MAI) announced progress in the development of a new generation of flexible spinal implants designed to preserve natural spinal mobility after surgery while improving reliability, service life, and biocompatibility.

- January 2026: Nivalon Medical Technologies Inc. produced the world's first fully patient-specific, motion-preserving spinal implant built entirely without metal, using AI-driven design and advanced ceramic 3D printing. The breakthrough device combines a proprietary zirconia-toughened alumina (ZTA) ceramic architecture that behaves like bone with a flexible elastomeric core to mimic natural spinal motion, creating a new category of spinal implant engineered to match both human anatomy and natural biomechanics.

Global Flexible Spinal Implants Market Report Scope

As per the scope of the report, flexible spinal implants are medical devices designed to provide support and stabilization to the spine while allowing a degree of flexibility and movement. They are typically used in spinal fusion procedures, disc replacement, or deformity correction to maintain spinal alignment and promote natural motion, reducing stress on adjacent segments. These implants are made from biocompatible materials and are engineered to mimic the spine's natural flexibility, thereby enhancing patient comfort and functional mobility.

The flexible spinal implants market is segmented by type into hooks, rods, plates, pedicle screws, cages, and other types; by product type into dynamic stabilization devices, motion preservation devices, and other product types; by material into titanium, PEEK, stainless steel, and other materials; by application into lumbar, cervical, thoracic, artificial discs, deformity correction, spinal fusion surgery, trauma treatment, and other applications; by end user into hospitals, ambulatory surgical centers, specialty spine clinics, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Hooks |

| Rods |

| Plates |

| Pedicle Screws |

| Cages |

| Others Types |

| Dynamic Stabilization Devices |

| Motion Preservation Devices |

| Others Product Types |

| Titanium |

| PEEK |

| Stainless Steel |

| Other Materials |

| Lumbar |

| Cervical |

| Thoracic |

| Artificial Discs |

| Deformity Correction |

| Spinal Fusion Surgery |

| Trauma Treatment |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Spine Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Hooks | |

| Rods | ||

| Plates | ||

| Pedicle Screws | ||

| Cages | ||

| Others Types | ||

| By Product Type | Dynamic Stabilization Devices | |

| Motion Preservation Devices | ||

| Others Product Types | ||

| By Material | Titanium | |

| PEEK | ||

| Stainless Steel | ||

| Other Materials | ||

| By Application | Lumbar | |

| Cervical | ||

| Thoracic | ||

| Artificial Discs | ||

| Deformity Correction | ||

| Spinal Fusion Surgery | ||

| Trauma Treatment | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Spine Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the flexible spinal implants market?

The flexible spinal implants market is valued at USD 4.48 billion in 2026 and is projected to reach USD 7.06 billion by 2031 at a 9.51% CAGR.

Which product category leads revenue today?

Dynamic stabilization devices lead product revenue with 45.24% share in 2025, showing that stabilization without full motion restriction still holds the largest commercial base.

Which material is growing the fastest for spinal implant use?

PEEK is the fastest-growing material segment, with an 11.62% CAGR through 2031, supported by radiolucency and imaging advantages after surgery.

Why is North America still the leading region?

North America held 41.61% share in 2025 because of higher procedure volumes, stronger reimbursement support, and faster uptake of navigation and outpatient spine care.

What is driving faster growth in Asia-Pacific?

Asia-Pacific is projected to grow at a 10.65% CAGR through 2031, supported by expanding tertiary hospital capacity, aging populations, and wider access to spine procedures.

Which end-user channel is expanding the fastest?

Ambulatory surgical centers are the fastest-growing end-user segment at a 10.95% CAGR through 2031, helped by outpatient reimbursement support and growing specialist infrastructure.

Page last updated on: