Flexible Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

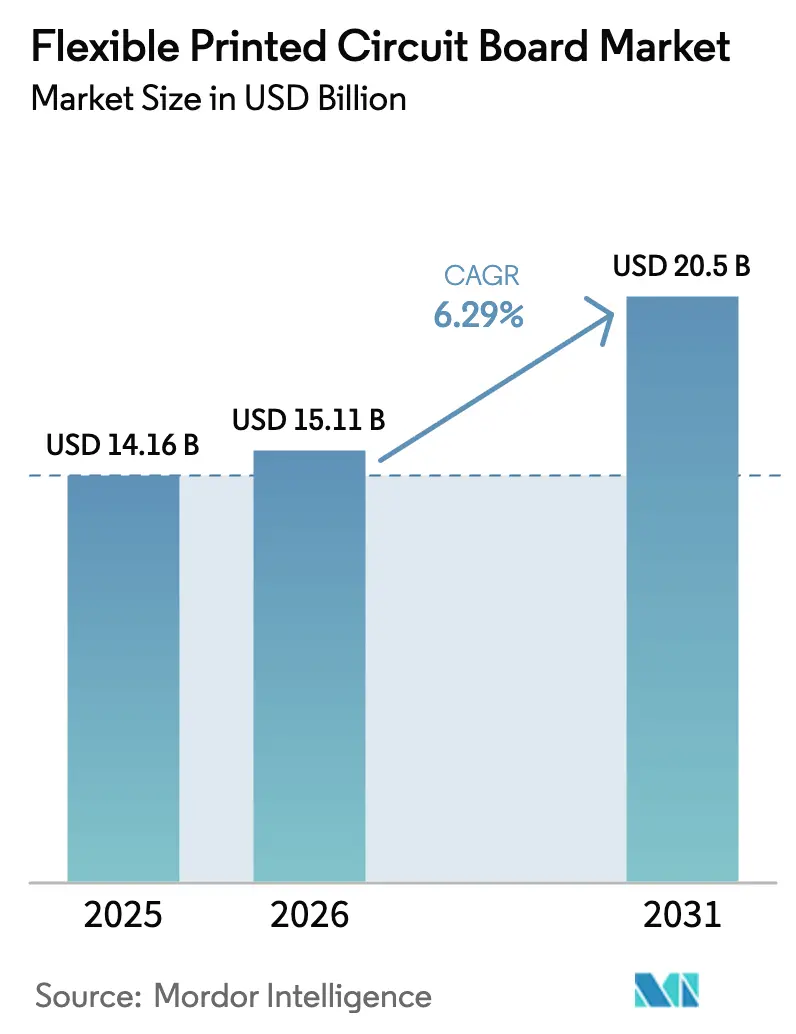

| Market Size (2026) | USD 15.11 Billion |

| Market Size (2031) | USD 20.5 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

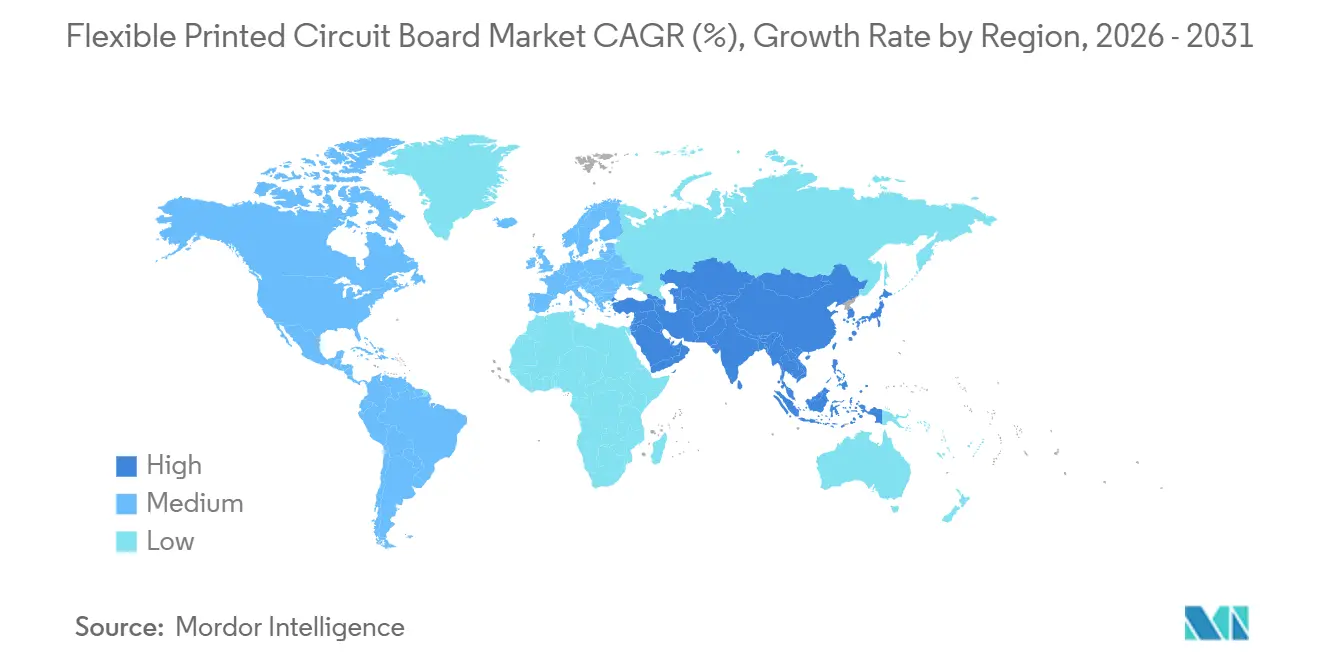

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Printed Circuit Board Market Analysis by Mordor Intelligence

The Flexible Printed Circuit Board Market is expected to grow from USD 14.16 billion in 2025 to USD 15.11 billion in 2026 and is forecasted to reach USD 20.5 billion by 2031 at 6.29% CAGR over 2026-2031. The expansion rides on surging demand for lighter, thinner, and more reliable interconnects in foldable smartphones, 5G base-station radios, advanced driver-assistance systems, and wearable medical sensors. Device makers value the superior bend radius, thermal resilience, and signal integrity that polyimide-based constructions deliver, propelling a structural shift away from rigid boards. Fabricators are widening material portfolios to include liquid-crystal polymer and low-loss modified polyimide for millimeter-wave applications, while additive manufacturing and sub-micrometer copper deposition shorten cycle times for high-layer-count builds. Cost pressures tied to copper and specialty film volatility temper margins, yet investments in automation, optical inspection, and vertical integration sustain profitability as the flexible printed circuit board market rewards suppliers that meet tight tolerance, high-reliability requirements.

Key Report Takeaways

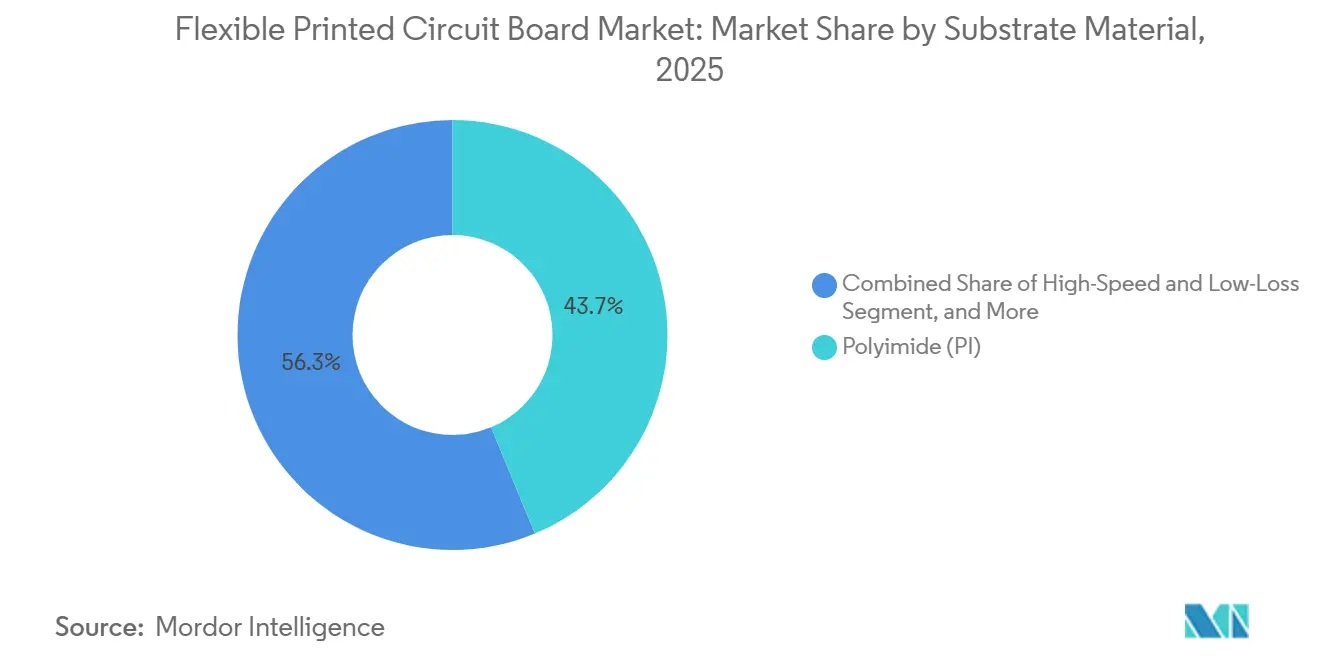

- By substrate material, polyimide captured 43.73% of flexible printed circuit board market share in 2025.

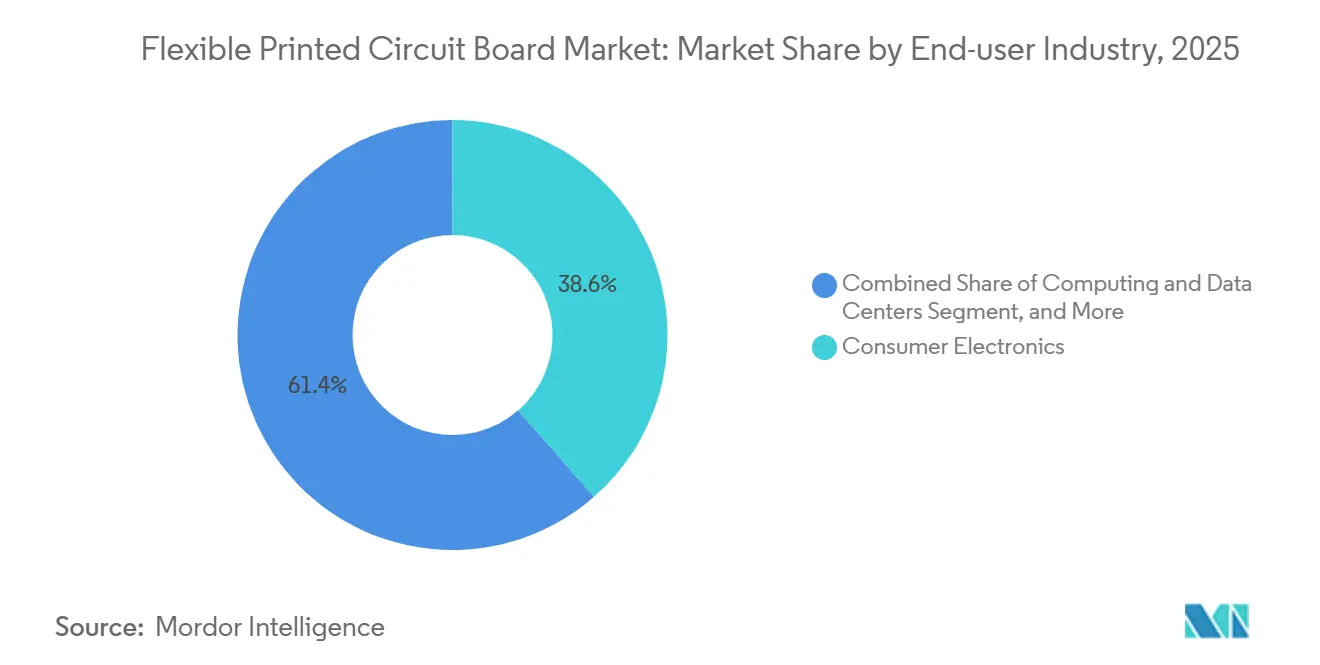

- By end-user, consumer electronics led with 38.62% of flexible printed circuit board (PCB) market revenue share in 2025, while telecommunications registered the fastest 7.11% CAGR to 2031.

- By geography, Asia-Pacific held 68.94% of global revenue in 2025, and is advancing at a 6.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flexible Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Foldable Smartphones | +1.2% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Rising Demand for Advanced Driver-Assistance Systems | +1.4% | Global, early concentration in Europe and North America | Long term (≥ 4 years) |

| Miniaturization of Wearable Medical Devices | +0.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of 5G Base-Station Roll-outs | +1.5% | Asia-Pacific dominance, North America and Europe upgrades | Short term (≤ 2 years) |

| Adoption of LED Lighting in Smart-City Projects | +0.6% | Asia-Pacific and Middle East, pilot deployments in Europe | Medium term (2-4 years) |

| Commercialization of Flexible Solar Panels for IoT Edge Nodes | +0.5% | Global, early adoption in building-integrated photovoltaics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Foldable Smartphones

Foldable handset shipments demand multi-bend circuits that survive 200,000 to 400,000 fold cycles without trace fatigue, multiplying board count per device versus slate phones. Samsung Display branded its MONT FLEX panels in 2025 to standardize stack-up rules, enabling suppliers to reuse tooling across different models and reduce cost per square meter.[1]Samsung Display, “MONT FLEX Foldable OLED Panel Portfolio,” samsungdisplay.com Tri-fold prototypes raise interconnect layers and average selling prices by roughly 35%, cushioning the smartphone segment’s unit softness. Apple’s selection of BH as a primary board vendor pulled smaller Chinese fabricators into qualification programs, widening the supply base. Yet, Taiwan’s third-quarter 2025 output slipped 10.9% year-over-year as delayed model launches exposed the volatility tied to a narrow customer roster.

Rising Demand for Advanced Driver-Assistance Systems

Each Level-2+ vehicle integrates at least a dozen camera, radar, and lidar modules, with flexible printed circuit boards routing differential pairs through tight bumper and mirror cavities. Temperature excursions from -40 °C to +125 °C and the new IPC-A-610JA addendum published in September 2025 impose stricter solder-joint acceptance, forcing fabricators to install automated optical inspection and X-ray imaging.[2]IPC, “IPC-A-610JA Automotive Addendum,” ipc.org Embedded thermistors inside battery-management boards track cell temperatures in 400 V and 800 V packs, an architecture absent in combustion vehicles. Updated USCAR vibration testing at 50 G peak acceleration now favors polyimide-reinforced stiffeners rather than adhesive steel, lengthening validation but widening the moat for certified suppliers.

Miniaturization of Wearable Medical Devices

Continuous glucose monitors and skin-patch ECGs require sub-50 µm traces on circuits that flex with the wearer. Boyd Corporation advises polyimide with a coefficient of thermal expansion below 20 ppm/°C to limit sensor drift, a benchmark consumer-grade films cannot meet. A 2025 study in Nature showed flexible boards cut motion artifacts by 40% versus rigid alternatives. Near-field communication power harvesting eliminated coin-cell batteries, trimming device thickness under 1 mm and doubling wear time . While U.S. FDA 510(k) clearance averages nine months, the European MDR adds post-market surveillance that lifts supplier compliance costs 15-20%.

Expansion of 5G Base-Station Roll-outs

Massive-MIMO radio units deploy 64- or 128-element arrays, each embedding flexible printed circuit boards for 25 Gb/s signal lines spanning 0.5-2 m. TE Connectivity’s 617-6000 MHz antennas unite sub-6 GHz and millimeter-wave bands in one enclosure, slashing tower lease fees.[3]TE Connectivity, “617-6000 MHz Flexible Antenna Datasheet,” te.com Skyworks marries flexible boards with embedded passives, shrinking front-end modules 30% while maintaining thermal headroom for -40 °C to +65 °C climates. Open RAN splits baseband from radios, increasing demand for high-speed jumper boards certified to O-RAN 50 Gb/s interoperability. China surpassed 3.5 million active sites by end-2024, and rural subsidies steer operators toward cost-efficient flexible designs.[4]Ministry of Industry and Information Technology, “5G Base Station Roll-out Status,” miit.gov.cn

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-Management Challenges in High-Layer Count Flexible PCBs | -0.8% | Global, acute in automotive and telecommunications | Short term (≤ 2 years) |

| Volatility in Copper Foil and Polyimide Prices | -1.1% | Global, Asia-Pacific fabricators most exposed | Short term (≤ 2 years) |

| Stringent Automotive Qualification Cycles | -0.6% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| High Tooling Costs for Multi-Generation Smartphone Models | -0.7% | Asia-Pacific concentration, affecting Taiwan and China fabricators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Copper Foil and Polyimide Prices

Copper foil represents roughly one-third of material cost, and spot prices climbed 21.2% from Q4 2024 to Q4 2025 amid supply disruptions in Indonesia and Chile. JPMorgan pegs the 2026 average at USD 12,075 per t, up 8.6% year on year, tightening margins under six- to twelve-month OEM price locks.[5]JPMorgan, “2026 Copper Market Outlook,” jpmorgan.com Polyimide film in China fell 13.42% in Q3 2025 to USD 19,133 per t, yet North American converters raised quotes as fourth-quarter smartphone kitting absorbed excess supply. UBE’s new precursor line will not reach volume until late 2027, sustaining supplier concentration risk.

Thermal-Management Challenges in High-Layer Count Flexible Printed Circuit Boards

Boards exceeding eight layers trap heat in polyimide stacks with 0.12 W/m·K conductivity, one-third that of FR-4, forcing 20-30% de-rating on current-carrying capacity. A 10-layer structure running 10 GHz signaled hot spots above 180 °C in accelerated life tests, lifting insertion loss 0.5 dB per 10 cm after 5,000 h. DuPont’s Pyralux ML cures below 180 °C and improves conductivity, but 25% higher material cost limits adoption to prototypes. Boron-nitride-filled interface sheets reached 3 W/m·K in lab trials, yet commercial yields below 85% stall rollout. The European Space Agency now requires -180 °C to +125 °C thermal-vacuum cycling under ECSS-Q-ST-70-60C Rev.1, exposing delamination in adhesive builds.[6]European Space Agency, “ECSS-Q-ST-70-60C Rev.1,” esa.int

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: Polyimide Leads High-Reliability Deployments

Polyimide accounted for 43.73% of flexible printed circuit board market share in 2025 and is forecast to expand at a 6.68% CAGR through 2031. The material’s 260 °C glass-transition temperature, 3-5% elongation at break, and stable 3.4 dielectric constant at 1 GHz satisfy bend-cycle and millimeter-wave integrity targets in foldable handsets and 28 GHz base-station arrays. These attributes secure the largest slice of the flexible printed circuit board market size for polyimide-based designs. UBE’s fully integrated precursor-to-film chain grants it single-supplier leverage, prompting OEMs to dual-source modified chemistries wherever qualification windows allow.

High-speed low-loss substrates such as liquid-crystal polymer pursue telecommunications backplanes and artificial-intelligence servers that push 56 Gb/s PAM4 links beyond FR-4 loss budgets. IBM’s 1.2-Tb/s optical transceiver routes sixteen 100 Gb/s pairs on a board just 2 mm thick, a mechanical envelope unsustainable for rigid-flex alternatives. Cost-sensitive gadgets still default to FR-4 where bend radii exceed 10 mm and duty temperatures stay under 130 °C. Specialty resins, including bismaleimide-triazine and Ajinomoto build-up film, support chiplet interposers for AI accelerators, though combined revenue sits below 8% as certification hurdles restrict volume.

By End-User Industry: Telecom Surpasses Handsets in Growth Pace

Consumer electronics generated 38.62% of sales in 2025, but telecommunications infrastructure now commands the fastest 7.11% CAGR, turning macro cell sites and remote radio heads into the headline growth vector for the flexible PCB market. A single 5G base-station enclosure may house 20-30 boards, boosting the flexible printed circuit board market size in telecom gear even as smartphone volumes plateau. Computing and data-center hardware absorb high-layer-count circuits for AI server backplanes, with UALink 200 G specification stipulating 212.5 GBd signaling over sub-4 m reaches that favor flexible over optical links.

Automotive boards face 18-24 month AEC-Q200 validation, slowing near-term intake despite rising sensor density. Healthcare devices, from glucose monitors to neurostimulators, promise higher gross margins but add ISO 10993 biocompatibility and FDA 510(k) overhead. Aerospace and defense players source MIL-PRF-55110-qualified circuits for satellites and drones, and OKI’s custom 100 m boards opened low-Earth-orbit prototyping to start-ups needing small lots.[7]OKI Electric Industry, “Custom FPC for New Space,” oki.com Industrial automation and energy storage round out demand but remain fragmented, delivering limited scale for suppliers.

Geography Analysis

Asia-Pacific held 68.94% of flexible printed circuit board market revenue in 2025 and is projected to grow at a 6.53% CAGR to 2031. Taiwan’s Q2 2025 output reached NTD 218.2 billion (USD 7 billion), buoyed by AI server orders that consumed former smartphone capacity. China logged USD 34.18 billion in 2025 production after 22.3% year-on-year expansion, propelled by subsidies for 5G and semiconductor-packaging initiatives that channel domestic board spend toward local vendors. Japan maintained flexible circuits at 51.3% of total board value in 2024, roughly USD 11.53 billion, reflecting its niche in automotive-grade and medical-device builds, in the flexible PCB market, that command 30-40% premiums.

South Korea produced USD 7.86 billion in 2024, with 45% tied to semiconductor substrates, a mix that exposes fabricators to memory-chip cycles. India and Southeast Asia collectively supply below 5% of regional capacity but attract EMS investment for supply-chain diversification. North America and Europe combine for 20% of global revenue, weighted toward high-reliability automotive, aerospace, and medical uses where intellectual-property protection outweighs labor cost. European automakers now mandate IPC-A-610JA traceability, favoring regional board sources. North American data-center demand for AI clusters lifts domestic board spend as design complexity and delivery certainty offset Asia-Pacific price advantages in the flexible printed circuit board market. The rest of world commands under 12%, centered on telecom roll-outs and smart-city projects that select lower-cost glass-epoxy solutions.

Competitive Landscape

The flexible printed circuit board market shows moderate concentration: Zhen Ding Technology, Dongshan Precision, Nippon Mektron, BH, and Flexium Interconnect collectively held 59.3% capacity in 2023. Large players defend share through additive manufacturing, sub-micrometer copper deposition, and rigid-flex vertical integration. Elephantech’s April 2025 launch of ultra-thin 1 µm copper boards cut waste 95% and enabled 10 µm traces, securing medical and aerospace accounts that pay 20-30% premiums.

A bifurcation is evident in the flexible PCB market. Volume-oriented Chinese and Taiwanese fabricators chase smartphone OEMs on price and scale, while specialty houses seek automotive, medical, and defense niches by stacking certifications such as IATF 16949, ISO 13485, and AS9100. Fuji Corporation doubled Okazaki SMT platform output to 1,000 units per month for placement rates above 150 k cph, mirroring assemblers’ throughput needs in miniaturized wearables. Disruptors include low-temperature polyimide developers; DuPont’s Pyralux ML cures below 180 °C but bears a 25% cost premium that confines it to high-reliability prototypes.

Incumbents diversify into service-oriented models. NOK Corporation and MEKTEC began infrastructure-monitoring sensor trials in September 2025, creating recurring revenue streams from data subscriptions.[8]NOK Corporation, “FPC Strain Sensor Trial,” nok.co.jp BIPVco’s 17%-efficient CIGS modules weigh under 3 kg/m² and need 25-year-rated circuits that withstand -40 °C to +85 °C cycling, opening adjacent demand in building-integrated photovoltaics. Rising capital expenditure from CMI Limited and GCE Electronics underscores optimism, yet copper and film volatility still compress gross margins for less-automated plants.

Flexible Printed Circuit Board Industry Leaders

Nippon Mektron Ltd.

Zhen Ding Technology Holding Ltd.

Flexium Interconnect Inc.

Sumitomo Electric Industries Ltd.

Fujikura Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: NOK Corporation and MEKTEC launched field trials of flexible printed circuit board strain sensors for bridge and tunnel monitoring in Shiga Prefecture, Japan.

- July 2025: OKI Electric Industry introduced custom flexible boards up to 100 m for New Space satellite prototypes, cutting lead time to six weeks.

- April 2025: Elephantech started mass production of additive-manufactured boards with sub-1 µm copper foil, reducing etchant waste by 95%.

- January 2025: Sumitomo Electric Industries reported that automotive and industrial uses rose to 45% of flexible board revenue, up from 28% in 2020.

Global Flexible Printed Circuit Board Market Report Scope

The Flexible Printed Circuit Board Market / Flexible PCB Market / Flexible Printed Circuit Board (PCB) Market Report is Segmented by Substrate Material (Glass Epoxy, High-Speed Low-Loss, Polyimide, Packaging Resins, Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Healthcare Medical, Aerospace and Defense, Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Rest of World |

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By End-user Industry | Consumer Electronics | |

| Computing and Data Centers | ||

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Healthcare / Medical | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Region | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the projected value of the flexible printed circuit board market in 2031?

The market is forecast to reach USD 20.5 billion by 2031, advancing at a 6.29% CAGR from 2026.

Which substrate holds the largest share today?

Polyimide substrates lead with a 43.73% share in 2025 thanks to superior thermal and mechanical performance.

Which end-use segment is expanding the fastest?

Telecommunications equipment shows the fastest 7.11% CAGR through 2031 as 5G infrastructure scales globally.

How concentrated is supplier capacity?

The five largest manufacturers control 59.3% of global capacity, reflecting moderate consolidation.

What is the primary raw-material cost risk?

Copper foil price volatility poses the biggest near-term risk, with 2026 averages expected around USD 12,075 per t.

Which region dominates production?

Asia-Pacific accounts for 68.94% of global revenue, driven by Taiwan, China, Japan, and South Korea.

Page last updated on: