Fish Collagen Peptides Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 443.49 Million |

| Market Size (2031) | USD 774.29 Million |

| Growth Rate (2026 - 2031) | 11.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fish Collagen Peptides Market Analysis by Mordor Intelligence

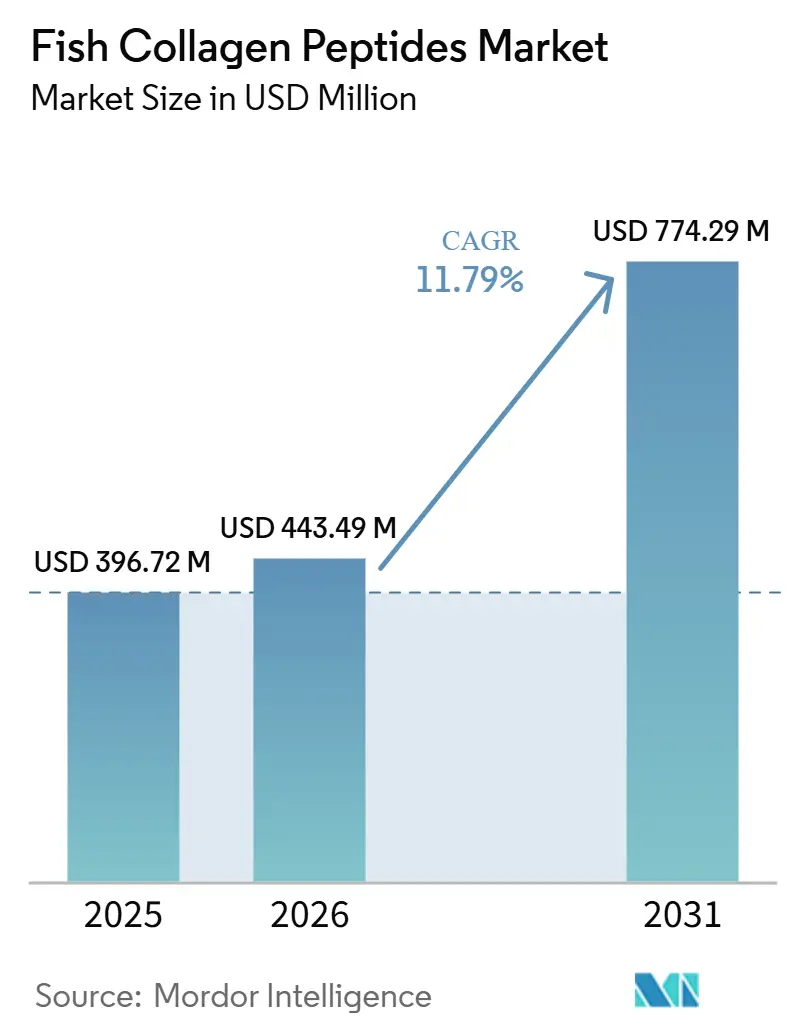

The Fish Collagen Peptides Market size is projected to be USD 396.72 million in 2025, USD 443.49 million in 2026, and reach USD 774.29 million by 2031, growing at a CAGR of 11.79% from 2026 to 2031.

The fish collagen peptides market is expanding as preventive wellness spending, clean-label preferences, and pharmaceutical-grade use cases move demand toward higher-value collagen formats rather than bulk commodity supply. The fish collagen peptides market also benefits from its raw material base because skin, scales, bones, and fins from finfish processing create a supply stream that rises with seafood output and supports a more favorable cost structure than terrestrial collagen sources. Demand is moving further toward clinically positioned products as practitioners in parts of Asia increasingly recommend fish collagen peptide regimens for skin health, which supports stronger pricing and brand differentiation in the fish collagen peptides market. Competitive intensity is rising, but scale, clinical validation, certification, and purification capabilities continue to shape who can defend premium positioning in the fish collagen peptides market. Regulatory scrutiny on label claims, traceability, and sustainability is also pushing the fish collagen peptides market toward suppliers that can document efficacy, sourcing, and product consistency across regions.

Key Report Takeaways

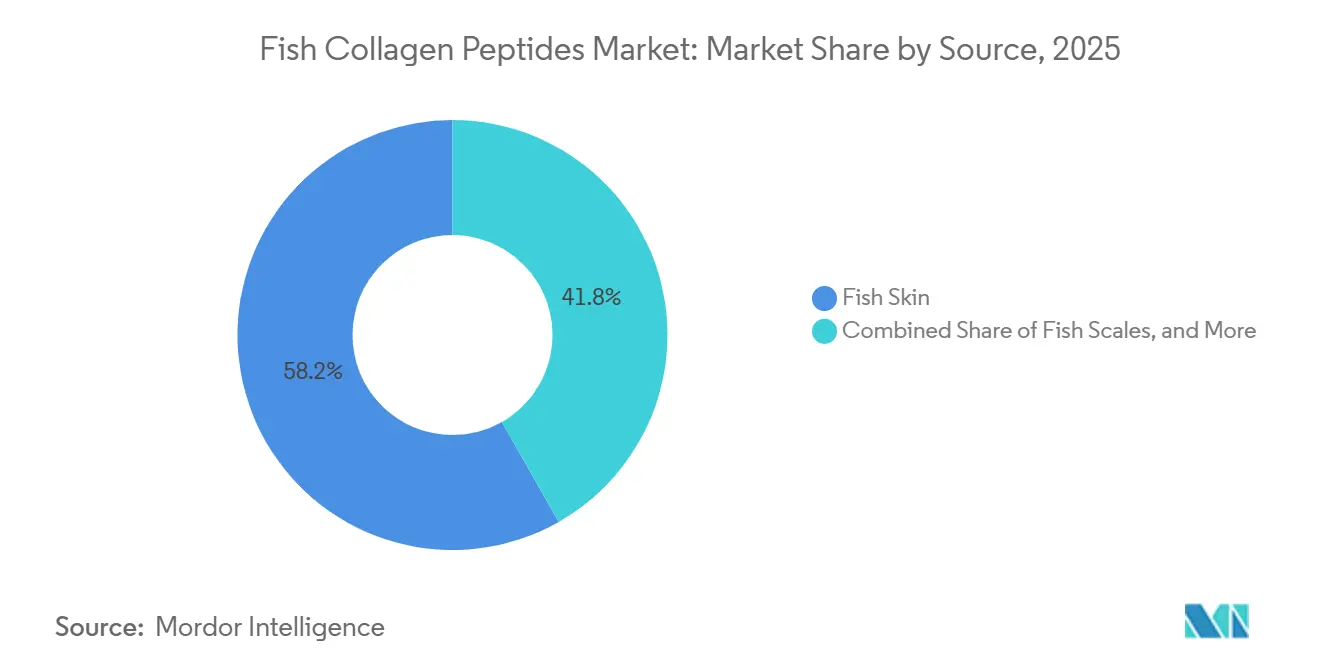

- By source, fish skin held 58.23% share in 2025, while fish scales will expand at a 12.45% CAGR through 2031 in the fish collagen peptides market.

- By form, powder held 60.56% share in 2025, while liquid will expand at a 14.93% CAGR through 2031.

- By application, dietary supplements held 48.74% share in 2025, while cosmetics and personal care will expand at a 13.87% CAGR through 2031 in the fish collagen peptides market.

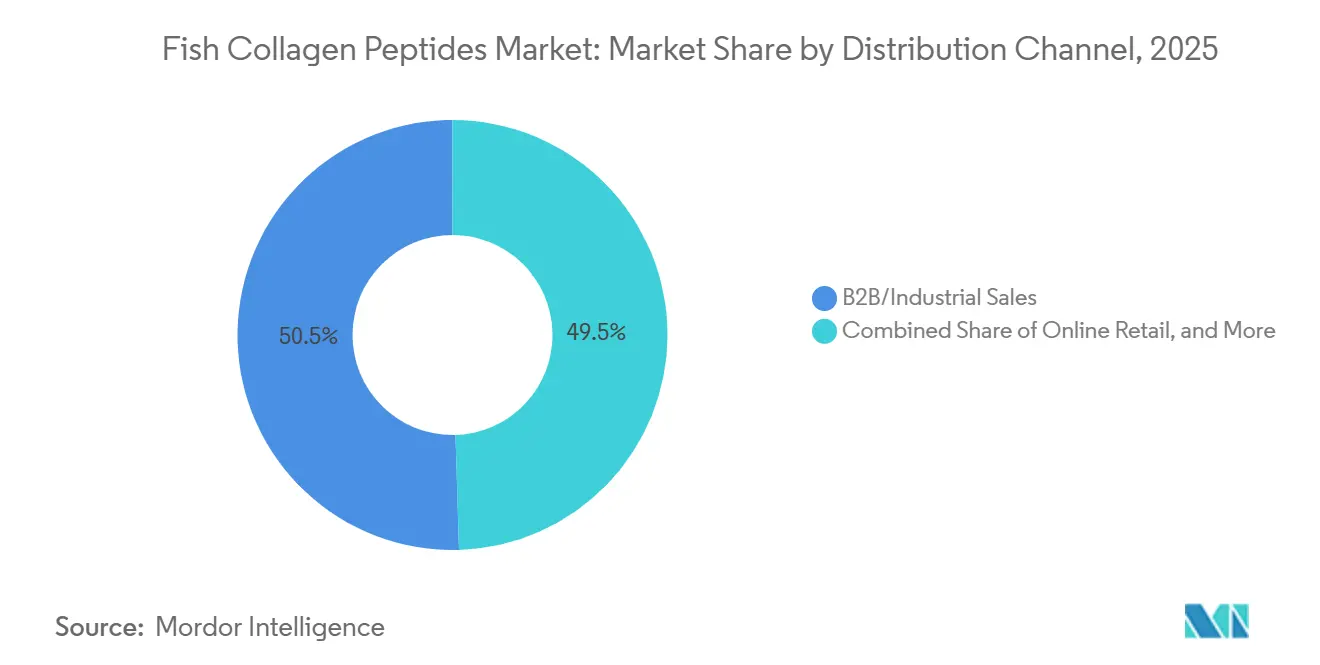

- By distribution channel, B2B and industrial sales held 50.48% share in 2025, while online retail will advance at a 15.84% CAGR through 2031.

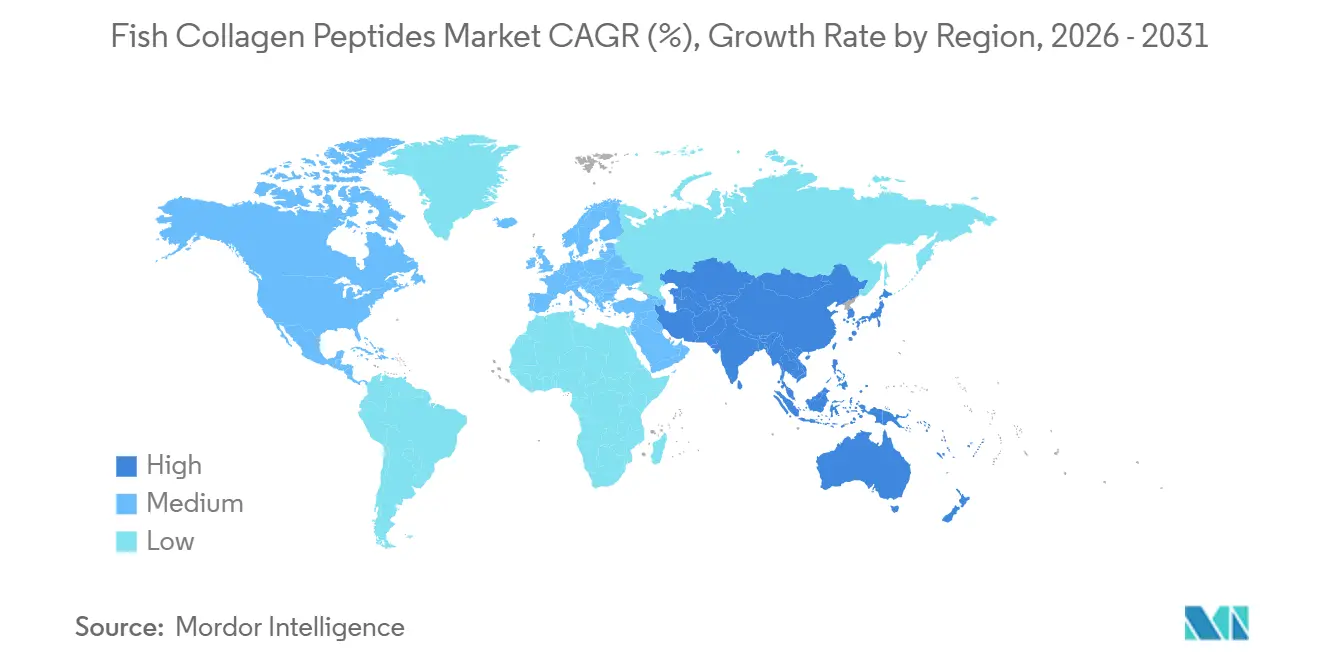

- By geography, North America held 38.47% of the fish collagen peptides market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 17.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fish Collagen Peptides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Beauty from Within Nutricosmetics | +2.8% | Global, strongest in Asia-Pacific, North America, and Western Europe | Short term (≤ 2 years) |

| Superior Bioavailability Versus Mammalian Collagen | +1.6% | Global, strongest in North America, the EU, and Japan | Medium term (2-4 years) |

| Expansion of Halal, Kosher, and Pescatarian Formulations | +1.2% | Southeast Asia, GCC, and wider Muslim and Jewish consumer groups | Medium term (2-4 years) |

| Circular Economy Use of Seafood By-Products | +0.7% | EU, Norway, Japan, China, Australia, with spillover elsewhere | Long term (≥ 4 years) |

| Growth of Medical and Wound-Healing Use Cases | +1.0% | North America and Europe, emerging in China and Japan | Medium term (2-4 years) |

| Enzymatic Hydrolysis and Peptide Tailoring for Premium Claims | +0.9% | Global, with R&D hubs in Germany, Japan, France, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Beauty From Within Nutricosmetics

The fish collagen peptides market is seeing demand shift from bulk ingredient trade toward premium ingestible beauty formats that are sold on clinical positioning, ingredient traceability, and finished-product claims. Buyers in this category increasingly look for species provenance and molecular weight information, which supports fish-derived Type I collagen over less transparent alternatives. This shift is also changing the route to market because dermatology clinics in Japan and South Korea are directing patients toward fish collagen peptide regimens paired with hyaluronic acid, which gives the category a practitioner-backed route rather than a simple shelf presence. Clinical supplementation studies over 8 to 12 weeks linked daily fish collagen intake with better skin hydration, improved elasticity, and reduced wrinkle appearance, which gives branded products the evidence base needed for premium pricing.[1]“Valorisation of Fish Scales and Bones: A Sustainable Source of Bioactive Proteins and Collagen for Nutraceuticals,” The fish collagen peptides market, therefore, gains not only volume from beauty demand but also stronger margins because brands with medical affairs, formulation depth, and claim support can separate themselves from generic suppliers.

Superior Bioavailability Versus Mammalian Collagen

The fish collagen peptides market continues to benefit from the smaller peptide size achieved through enzymatic hydrolysis, which supports faster passage through the intestinal barrier and better systemic availability. Fish collagen peptides are produced in the 3 to 10 kDa range, while native bovine collagen chains sit much higher, which helps explain why marine collagen is often positioned on absorption and usability grounds.[2]“Absorption of Bioactive Peptides Following Collagen Hydrolysate Intake: A Randomized, Double-Blind Crossover Study in Healthy Individuals,” Reviews cited in the source material indicate marine collagen can reach up to 1.5 times the absorption efficiency of bovine collagen at equal dosing, which keeps the efficacy narrative favorable for premium fish-derived products. An important commercial effect is that suppliers can focus differentiation on religious compliance, pescatarian fit, and cleaner label positioning without needing to give up performance-based messaging. In regulated markets, access to human clinical data is also becoming more important because health-claim rules shape what can be said on labels and what B2B buyers are willing to pay for validated ingredients. The fish collagen peptides market is therefore gaining from a mix of physiological performance, formulation flexibility, and regulatory alignment rather than from a single clinical argument alone.

Expansion of Halal, Kosher, and Pescatarian Formulations

The fish collagen peptides market is opening demand pools that mammalian collagen cannot fully access because fish-derived inputs fit halal, kosher, and pescatarian formulation needs more naturally. Nippi obtained halal certification for its fish-derived CQT series and its Collagenomics GFF-01 peptide, which shows how certification has become part of growth strategy rather than a minor compliance step.[3]“Fish-Derived Collagen CQT Series, Halal Certification and Product Information,” This is not only a substitution story because certified fish collagen can bring new consumers into the category who had previously avoided collagen products on faith or dietary grounds. The barrier is documentation, since credible halal or kosher approval increasingly depends on traceability back through the sourcing chain, and that is harder for lower-cost commodity producers to maintain consistently. Producers in Norway, France, and Japan that invested in full-chain audit systems are therefore in a better position to defend premium contracts in the fish collagen peptides market. As GCC and other regulated buyers place more weight on approved sourcing systems, certification becomes both a demand driver and a competitive filter.

Circular Economy Use of Seafood By-Products

The fish collagen peptides market gains long-term support from the conversion of fish skins, scales, bones, and fins from waste streams into higher-value ingredients with stronger unit economics. Fish processing waste accounts for 50% to 75% of total fish weight, so recovery into collagen removes the disposal burden while creating an additional revenue stream for processors.[4]“Unlocking the Potential of Marine Sidestreams in the Blue Economy: Lessons Learned from the EcoeFISHent Project on Fish Collagen,” Fish scales are especially useful because they contain a dense Type I collagen matrix within a mineral framework, and optimized extraction conditions can deliver strong recovery yields from discarded material. Hainan Huayan Collagen Biotech used this model at scale in Haikou, where its 2 lines and 9,000 metric tons of annual capacity supported nearly 100% overseas sales growth in the first half of 2025. That commercial result matters because it shows circular sourcing is not only a sustainability message, but also a workable production and export model in the fish collagen peptides market. As more processors look to improve raw material economics, the fish collagen peptides market should continue to benefit from recovery systems that link waste reduction with premium ingredient production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited and Seasonal Marine Raw Material Supply | -1.4% | Global, most acute in Norway, Iceland, Russia, and Japan | Short term (≤ 2 years) |

| Higher Cost of Extraction and Purification Versus Bovine Alternatives | -1.1% | Global, especially limiting in South America and the rest of Asia-Pacific | Medium term (2-4 years) |

| Labeling and Health-Claim Scrutiny in Supplements and Cosmetics | -0.8% | North America & EU core; spill-over to APAC (Japan, South Korea, Australia) | Medium term (2–4 years) |

| Lower Thermal Stability and Processing Constraints in Certain Formulations | -0.5% | Global; most acute in high-temperature food and beverage processing applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited and Seasonal Marine Raw Material Supply

The fish collagen peptides market remains exposed to seasonal catch patterns, species-specific yield swings, and the limited geographic concentration of large fish processing hubs. Pollock, cod, tilapia, and salmon are among the major collagen-yielding species, so weather shocks, quota changes, overfishing controls, or disease outbreaks can move quickly into raw material prices. Supply is also pressured by competing uses for the same by-products because fishmeal, fish oil, and biogas operators are also investing in recovery capacity. Weishardt renewed Friend of the Sea certification for its Naticol marine collagen brand in December 2024, which shows that even established players face growing compliance expectations around traceable and legally sourced marine inputs. Norwegian fisheries research also pointed to dried and salted cod skins as an underused but promising collagen source, which suggests the fish collagen peptides market still has room to reduce supply risk if more by-product streams are commercialized. Even so, supply limitations continue to cap how quickly the fish collagen peptides market can scale in premium and regulated applications.

Higher Cost of Extraction and Purification Versus Bovine Alternatives

The fish collagen peptides market also faces a cost disadvantage because fish-derived raw materials require more intensive extraction, purification, and refinement than many bovine alternatives. Multi-step processing typically includes pretreatment, hydrolysis, purification, and membrane filtration, and the user-supplied content states that unit costs can run 20% to 40% above bovine collagen for comparable pharmaceutical-grade outputs. Fish skins and scales carry higher pigment, odor, and lipid contamination loads, so the production line must work harder to reach clean, neutral, and consistent finished material. Nippi noted that odor-free and tasteless fish collagen peptide powder requires low-temperature extraction and high-level refinement in a dedicated CQT facility, which shows why smaller producers often struggle to match premium specifications. New encapsulation and nanoemulsion work may improve delivery performance, but it also raises processing cost and limits commercial rollout to suppliers with stronger scale or pricing power. When standard-grade output rises and pricing softens, mid-tier suppliers in the fish collagen peptides market face margin pressure because their input costs do not fall in the same proportion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Fish Skin Leads While Scales Gain Speed

Fish skin held 58.23% of the fish collagen peptides market share in 2025, making it the most established raw material source within the fish collagen peptides market. Its position reflects mature extraction protocols, broad commercial familiarity, and a strong clinical link with skin-health formulations that already have traction in supplements and beauty products. In 2026, fish skin continues to benefit from integrated processing systems in large tilapia and pollock hubs, which helps suppliers maintain quality control and output scale. Solubility performance and cleaner purification pathways also make fish skin more attractive for finished-goods manufacturers that need dependable ingredient behavior across formats. These advantages keep fish skin at the center of mainstream supply in the fish collagen industry, especially where large-volume supplements and beauty formulations depend on reliable sourcing.

Fish scales are projected to grow at a 12.45% CAGR through 2031, showing that the segment is moving from an underused by-product to a stronger commercial source in the fish collagen peptides market. Recovery technologies are improving, and ultrasound-coupled natural deep eutectic solvent methods are now supporting native Type I collagen extraction from discarded seabass scales with competitive yields and lower solvent waste. This matters because scale material is abundant and was historically overlooked despite its dense collagen content. Fish bones still contribute meaningful volume in pharmaceutical-grade products because hydroxyapatite co-extraction supports dual positioning for bone-health formulas. Fish fins and the others category, including swim bladders, cartilage, and heads, remain niche but are drawing research attention as medical and technical applications broaden. Commercial growth in those smaller categories will still depend on better scale-up economics and more consistent collagen quality across batches.

By Form: Powder Holds Volume While Liquid Builds Premium Demand

Powder held 60.56% share in 2025, showing that the fish collagen peptides market still leans heavily on ingredient trade and scalable dry formats. Powder remains attractive because it fits high-volume hydrolysis output, stores well, and moves easily into capsules, sachets, and functional food systems without heavy downstream handling. These characteristics keep it central to B2B supply and explain why large manufacturers continue to rely on powder for mainstream wellness and beauty positioning. The format also supports cost discipline because it limits packaging complexity and aligns well with industrial blending operations. For these reasons, powder remains the volume anchor even as the fish collagen peptides market moves toward more differentiated delivery systems.

Liquid is projected to expand at a 14.93% CAGR through 2031, and this makes it one of the clearest premiumization channels in the fish collagen peptides market. The source material notes that liquid collagen products can command retail premiums of 3 times to 5 times versus equivalent powder dosing, which reflects the higher perceived convenience and efficacy of ready-to-drink formats. A 2026 clinical study on hydrolyzed collagen from sea bass skin showed measurable gains in hydration, roughness, and elasticity after 30 days, which supports liquid collagen as a clinically credible delivery method. Capsules and tablets continue to serve pharmacy and clinical nutrition channels, where standardized dosing remains important for practitioner recommendation and repeat use. The others category, which includes gummies, films, and hydrogels, is still smaller but is moving quickly because easier dosing can improve acceptance among pediatric and older users. As consumer products become more brand-driven, the fish collagen peptides market size for liquid and other convenient formats is likely to rise faster than bulk dry powder demand.

By Application: Supplements Lead While Personal Care Moves Faster

Dietary supplements held 48.74% share in 2025, which made them the main application channel across the fish collagen peptides market. The segment covers skin health, joint support, bone support, sports recovery, and an emerging metabolic wellness area that is pulling fish collagen into more science-led positioning. Rousselot’s Nextida GC received U.S. Patent No. US12636339 in June 2026 for a collagen peptide ingredient linked with GLP-1 and GIP stimulation, which shows how supplement demand is broadening beyond traditional beauty and mobility use. Supplement formats also remain the easiest route for premium claims because they allow flexible dosing, combination formulas, and direct consumer storytelling. These advantages keep supplements at the center of revenue generation while the fish collagen peptides market expands into new health-positioned niches.

Cosmetics and personal care are expected to grow at a 13.87% CAGR through 2031, which reflects the strength of ingestible beauty reformulation and premium anti-aging positioning. Beauty brands are increasingly using fish collagen peptides with proprietary molecular weight designations to support product distinction and pricing. Pharmaceuticals are smaller in broad volume, but they represent a high-value area because wound care matrices, acellular fish skin grafts, and cross-linked fish collagen membranes are gaining attention in clinical settings. The THOR trial interim analysis in 2025 reported preliminary superiority over standard care in venous leg ulcer closure, which supports the medical relevance of fish-derived wound applications. Food and beverages are also gaining from ready-to-drink collagen shots, fortified soups, and snack bars, although health-claim limits keep this channel more measured in some regions. The others category includes animal nutrition and technical uses, which remain smaller but still add breadth to the application base of the fish collagen peptides market.

By Distribution Channel: B2B Keeps Scale While Online Retail Expands Fastest

B2B and industrial sales held 50.48% share in 2025, which shows that the fish collagen peptides market still runs first through ingredient supply rather than through branded consumer ownership. Manufacturers, private-label blenders, and cosmetic formulators continue to account for much of the total volume because they purchase by collagen content, molecular weight, and certification profile. This structure favors suppliers that can deliver consistent technical specifications at a commercial scale. It also means the fish collagen peptides market remains strongly influenced by contract relationships and formulation pipelines rather than only by consumer shelf visibility. The broad channel base keeps industrial sales central even as higher-margin retail formats gain momentum.

Online retail is projected to grow at a 15.84% CAGR through 2031, which makes it the fastest-moving distribution route in the fish collagen peptides market. Direct-to-consumer collagen beauty and wellness brands are performing strongly across the United States, South Korea, China, and the United Kingdom because digital channels support education, clinical storytelling, and repeat purchase models. The online route also reduces intermediary margin pressure and gives brands better access to engagement data. Pharmacies and drug stores remain important where consumers look for more clinically grounded supplement choices, and the source material points to Japan as a market where pharmacist-guided recommendation holds strong trust. The others category includes specialty health retailers, direct clinical sales, and practitioner-dispensed lines, which are useful for targeted premium positioning. As channel strategies diversify, the fish collagen peptides market is likely to keep its industrial base while shifting more value capture toward digitally led branded sales.

Geography Analysis

North America held 38.47% of the fish collagen peptides market share in 2025, which made it the largest regional contributor within the fish collagen peptides market. The region benefits from a well-capitalized supplement manufacturing base, high health and wellness spending, and a strong direct-to-consumer ecosystem for collagen products. The United States remains the largest national market and is also distinct because demand extends beyond supplements into wound care, hospital supply, and medical device pathways. Clinical interest in acellular fish skin grafts for diabetic wounds and venous leg ulcers supports this broader use profile in 2026. Canada adds volume through natural health products, while Mexico supports demand through food processing applications. Europe remains important because the marine ingredient manufacturing strength in France and Germany supports both product development and regulatory positioning. Copalis SEA continues to valorize Atlantic catch by-products into branded marine ingredients, which keeps Europe relevant in premium collagen supply.

Asia-Pacific is projected to grow at a 17.62% CAGR through 2031, giving it the fastest regional expansion in the fish collagen peptides market. The region combines unmatched supply potential with rising consumer demand, which few other regions can replicate at the same time. China generates large volumes of collagen-rich by-products through fish processing, and Hainan Huayan’s Haikou facility has become a major export-oriented production base with 9,000 metric tons of annual capacity across 2 lines. Japan remains one of the most demanding fish collagen peptides markets because companies such as Nippi and Nitta Gelatin compete on patented compositions, anti-doping certification, and premium clinical positioning. South Korea, India, and Australia add further momentum through beauty supplements, dietary supplements, and functional foods, which helps keep regional growth above the global average.

The Middle East and Africa and South America still represent smaller shares, but both carry strategic relevance for future expansion in the fish collagen peptides market. In the Gulf states, halal certification is moving from a premium feature toward a category requirement for wider supplement distribution. Saudi Arabia’s domestic pharmaceutical investment is beginning to create downstream demand for pharmaceutical-grade collagen inputs, while South Africa serves as a distribution gateway for parts of sub-Saharan Africa. In South America, Brazil’s cosmetics manufacturing base and Argentina’s nutraceutical development create early-stage volume opportunities, while wider supplier coverage from global collagen producers should improve access over time. These regions are still smaller today, but certification, pharmaceutical expansion, and regional supply coverage can gradually raise their role in the fish collagen peptides market.

Competitive Landscape

The fish collagen peptides market remains moderately fragmented at the overall level, but competition is tightening in the premium tier where clinical evidence, patents, purification technology, and sustainability credentials matter most. This means volume competition and premium competition do not operate in the same way, and suppliers that succeed in one layer do not always lead in the other. Large-scale groups can defend supply reliability and broader regional reach, while specialized players compete through application-specific science and branded ingredients. The proposed merger of Rousselot and PB Leiner, announced by Darling Ingredients and Tessenderlo Group in May 2026, stands out as the biggest structural move in the current fish collagen peptides market because it targets USD 1.5 billion in annual revenue and 22 global facilities. That combination would strengthen pricing discipline, technical depth, and customer access across multiple collagen end uses, even though regulatory approval was still pending at the time of announcement.

Fish Collagen Peptides Industry Leaders

BioCell Technology LLC

Copalis SEA

Nippi Inc.

Norland Products Inc.

Gelita AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Darling Ingredients' health brand Rousselot received US Patent No. US12636339 for Nextida GC, a collagen peptide ingredient demonstrating GLP-1 and GIP stimulation for post-meal glucose regulation; complementary patents were simultaneously active in Europe (EP4498839B1), Japan (JP7751755B2), Australia (AU2023279850B2), and China (CN119212574B), establishing a multi-jurisdiction proprietary platform in the metabolic health collagen segment.

- May 2026: Darling Ingredients and Tessenderlo Group announced the merger of Rousselot and PB Leiner into a new collagen company projected to generate approximately USD 1.5 billion in annual revenue, operating 200,000 metric tons of gelatin and collagen capacity across 22 global facilities, with Darling Ingredients holding an 85% stake and Tessenderlo Group retaining 15%; regulatory approvals were pending at the time of announcement, with closing targeted for 2026.

- May 2026: Hofseth BioCare ASA signed an exclusive license and supply agreement with US-based Fission for its ProGo bioactive collagen peptide ingredient, valued at over USD 5 million, targeting the US metabolic health and performance supplement market.

Global Fish Collagen Peptides Market Report Scope

As per the scope of the report, fish collagen peptides are short-chain bioactive fragments are produced by enzymatically hydrolyzing type I fish collagen from skin, scales, or bones. They offer high absorption, low molecular weight, and strong biocompatibility, making them ideal for nutraceutical, cosmetic, and biomedical applications. Their smaller peptide size enhances skin repair, joint support, and tissue regeneration compared with native collagen.

The fish collagen is segmented by source, form, application, distribution channel, and geography. By source, the market is segmented into fish skin, fish scales, fish bones, fish fins, and others. By form, the market is segmented into powder, liquid, capsules, tablets, and others. By application, the market is segmented into dietary supplements, pharmaceuticals, food and beverages, cosmetics and personal care, and others. By distribution channel, the market is segmented into B2B and industrial sales, online retail, pharmacies and drug stores, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Fish Skin |

| Fish Scales |

| Fish Bones |

| Fish Fins |

| Others |

| Powder |

| Liquid |

| Capsules and Tablets |

| Others |

| Dietary Supplements |

| Pharmaceuticals |

| Food and Beverages |

| Cosmetics and Personal Care |

| Others |

| B2B and Industrial Sales |

| Online Retail |

| Pharmacies and Drug Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Fish Skin | |

| Fish Scales | ||

| Fish Bones | ||

| Fish Fins | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Capsules and Tablets | ||

| Others | ||

| By Application | Dietary Supplements | |

| Pharmaceuticals | ||

| Food and Beverages | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Distribution Channel | B2B and Industrial Sales | |

| Online Retail | ||

| Pharmacies and Drug Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of fish collagen by 2031?

The fish collagen peptides market is forecast to reach USD 774.29 million by 2031, rising from USD 443.49 million in 2026 at an 11.79% CAGR.

Which application generates the most revenue for fish collagen?

Dietary supplements led with 48.74% share in 2025, supported by skin health, joint support, sports recovery, and emerging metabolic wellness uses.

Which region is growing fastest for fish collagen demand?

Asia-Pacific is projected to grow at a 17.62% CAGR through 2031, helped by large by-product availability, export capacity, and strong supplement demand.

Why does fish skin remain the leading source material?

Fish skin held 58.23% share in 2025 because extraction methods are mature, purification is easier, and it already has strong use in skin-focused formulations.

Which sales channel is expanding the fastest?

Online retail is forecast to grow at a 15.84% CAGR through 2031 as brands use direct digital channels for education, repeat purchase, and premium storytelling.

What are the main barriers for new entrants in fish collagen?

The main barriers are traceable raw material access, higher purification cost versus bovine collagen, clinical validation needs, and tighter certification demands in regulated markets.

Page last updated on: