Finland Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

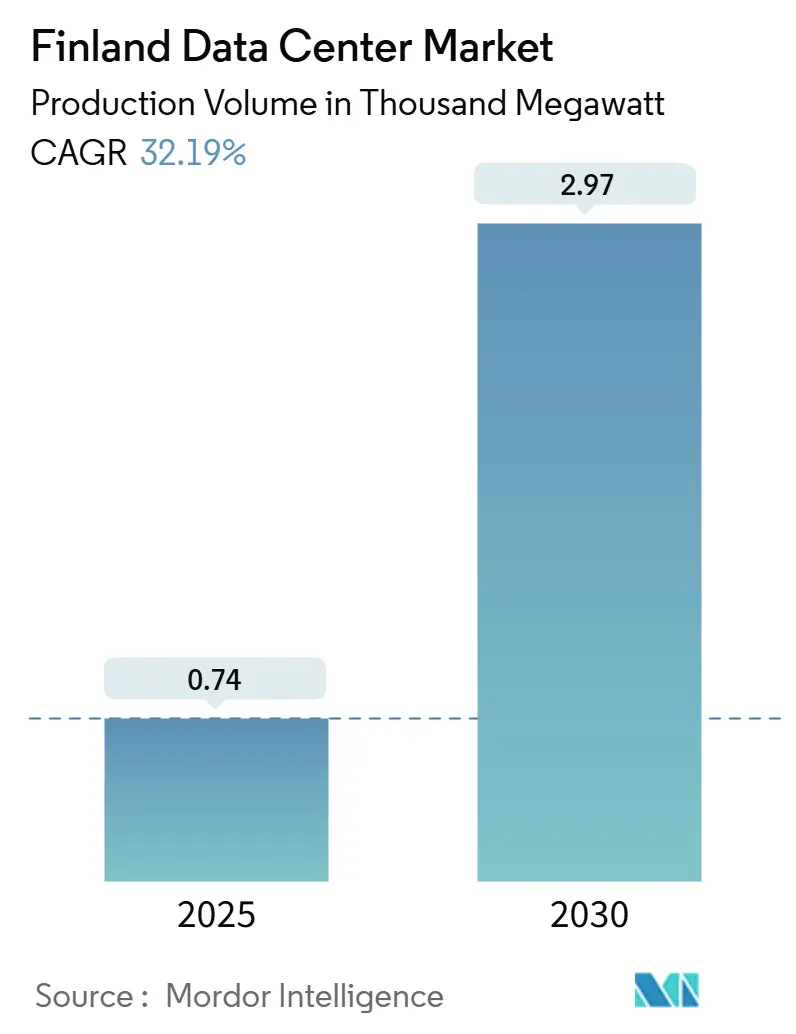

| Market Volume (2025) | 0.74 Thousand megawatt |

| Market Volume (2030) | 2.97 Thousand megawatt |

| Growth Rate (2025 - 2030) | 32.19% CAGR |

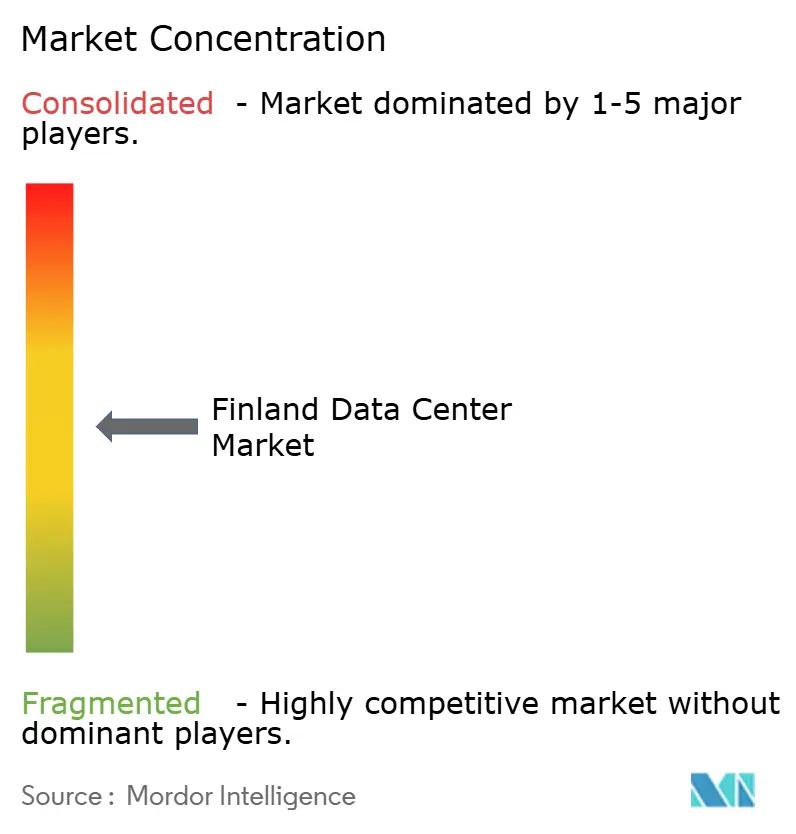

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Data Center Market Analysis by Mordor Intelligence

The Finland Data Center Market size in terms of production volume is expected to grow from 0.74 thousand MW in 2025 to 2.97 thousand MW by 2030, at a CAGR of 32.19% during the forecast period (2025-2030). Finland’s cold climate, abundant renewable energy sources, and supportive fiscal incentives continue to compress operating costs, drawing hyperscale investors who regard the country as a low-risk, carbon-efficient node within the European cloud backbone. Mega-scale builds are accelerating as AI training and inference workloads demand rack densities that align naturally with Finland’s free-air cooling envelope. New submarine cable routes strengthen cross-regional latency profiles, while waste-heat monetization agreements improve project economics and advance municipal decarbonization goals. Together, these factors reinforce the Finland data center market as the Nordic region’s fastest-growing digital infrastructure cluster, outpacing neighboring hubs on both capacity additions and sustainability metrics.

Key Report Takeaways

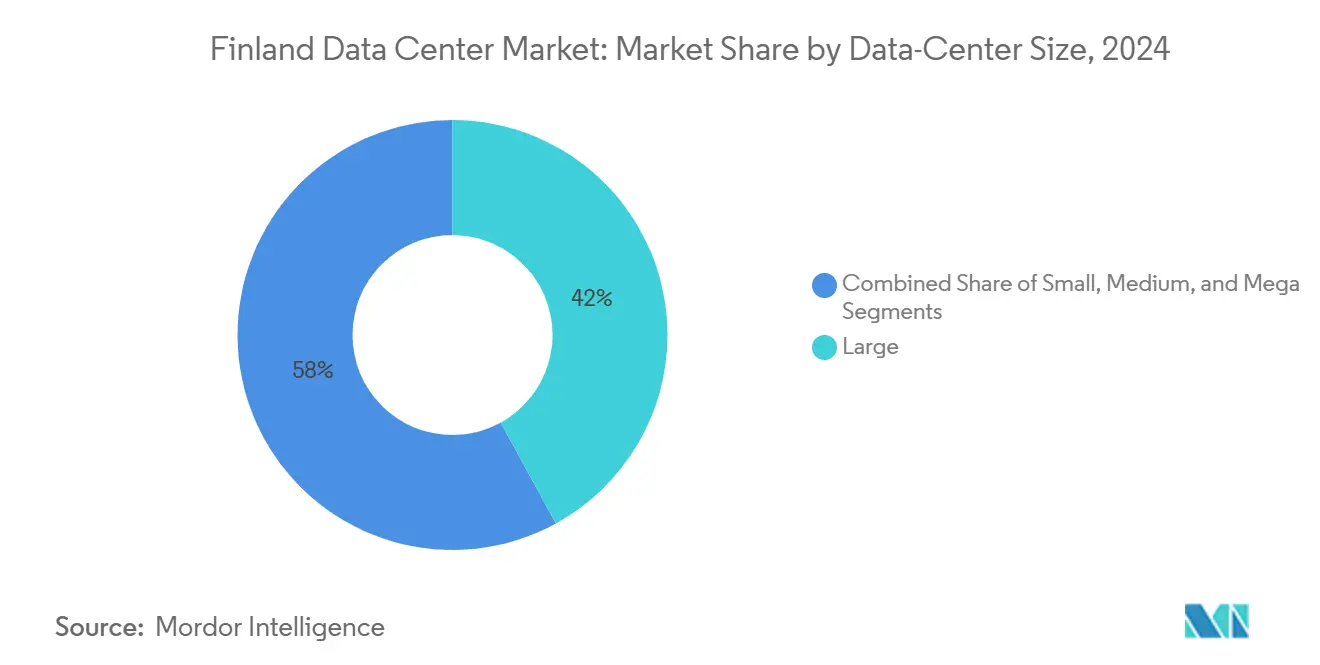

- By data-center size, large facilities led with 42% of Finland data center market share in 2024; the Mega segment is projected to register a 31.5% CAGR to 2030.

- By tier standard, Tier III configurations captured 68% of Finland data center market share in 2024, while Tier IV deployments are set to expand at a 22% CAGR through 2030.

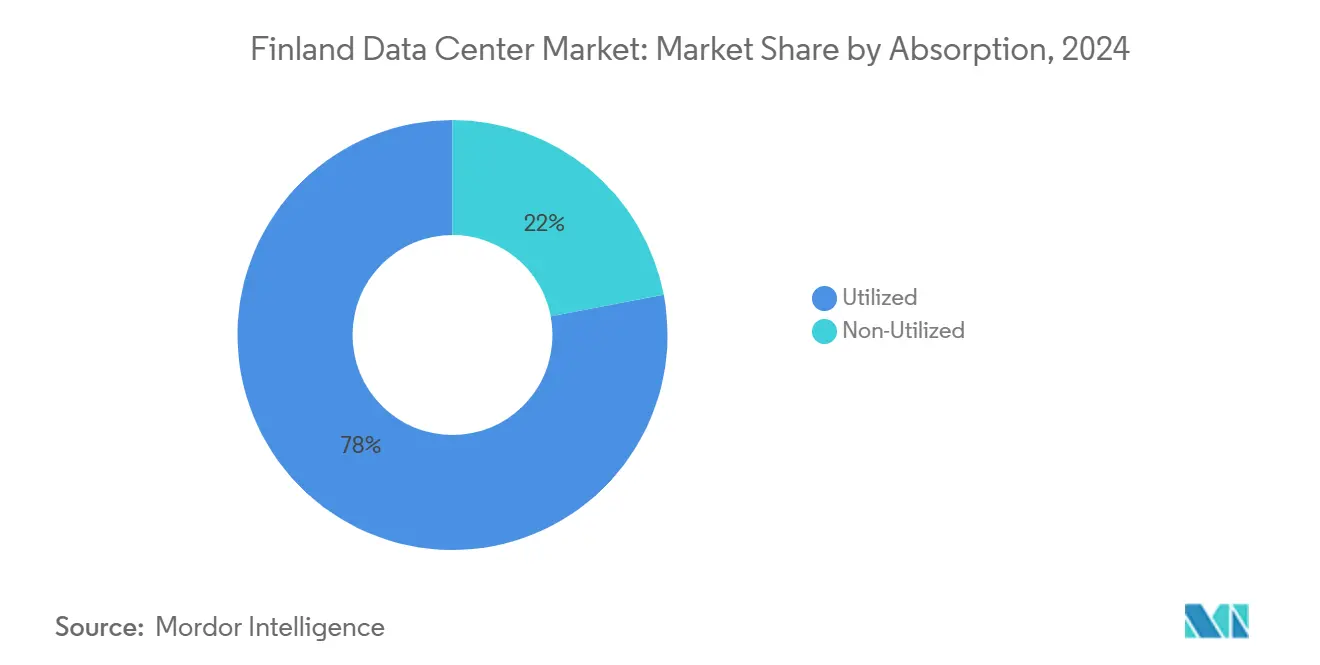

- By absorption, utilized capacity accounted for 78% of the Finland data center market size in 2024, whereas non-utilized capacity is advancing at a 30.5% CAGR on the back of pre-build strategies.

- By hotspot, the Helsinki metropolitan area held 81% of total installed capacity in 2024; Oulu is forecast to record a 29% CAGR between 2025-2030.

Finland Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold climate enables free-air cooling efficiencies | +8.50% | National, concentrated in northern regions | Long term (≥ 4 years) |

| Abundant renewable (wind and hydro) electricity supply | +7.20% | National, strongest in coastal and Lapland regions | Long term (≥ 4 years) |

| Growing Nordic subsea cable mesh (C-Lion1, Far North Fiber) | +6.80% | Helsinki Metropolitan Area, extending to Oulu | Medium term (2-4 years) |

| Surging cloud and AI / HPC workloads in Europe | +5.90% | Global impact, concentrated in Helsinki region | Short term (≤ 2 years) |

| Government's reduced electricity-tax class for data centers | +2.10% | National | Medium term (2-4 years) |

| District-heating heat-reuse incentives in Helsinki and Espoo | +1.40% | Helsinki Metropolitan Area, Espoo, Tampere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold Climate Enables Free-Air Cooling Efficiencies

Finland’s average annual temperature of 4.6 °C enables data centers to operate free-air systems for approximately 94% of their operating hours, reducing mechanical cooling electricity use by up to 60% compared to temperate European locations.[1].Telia Company, “A Data Center in Finland Is Safe, Stable and Energy-Efficient,” telia.fi Google's Hamina campus consistently records a PUE of 1.09 by harnessing Baltic Sea water for indirect seawater cooling, underlining the country’s ability to host high-density AI racks without proportional HVAC investment. Lower heat-rejection overhead means operators can productively fill cabinets at 40–100 kW without breaching critical thermal envelopes, maximizing revenue per square meter. The prolonged cool season also lowers the risk of thermally induced downtime, an attribute valued by financial-trading platforms and HPC tenants. Over the long term, this climatic edge scales linearly with rising chip-level TDPs, reinforcing Finland data center market competitiveness as processors move beyond 1 kW per package.

Abundant Renewable (Wind and Hydro) Electricity Supply

Renewables contributed 52% of Finland’s total power mix in 2024, anchored by hydropower (45% of green output) and onshore wind (23%), supplying operators with cost-stable, low-carbon electricity that satisfies corporate net-zero mandates.[2]Statistics Finland, “Over One-Half of Finland’s Electricity Was Produced with Renewable Energy Sources in 2024,” stat.fi Yandex’s fixed-price, five-year PPA with Ilmatar Energy for its Mäntsälä site exemplifies how hyperscalers are locking in 100% green supply at predictable tariffs. Grid resilience is underpinned by an 18% nuclear baseload, ensuring Tier IV power continuity even during periods of low wind. The availability of certified renewable energy guarantees (RECs) enables colocation providers to offer carbon-neutral service-level agreements that fetch premium pricing. As EU sustainability disclosure regulations tighten, the alignment of clean generation and competitive tariffs will continue to pull incremental hyperscale capacity northward, cementing Finland data center market leadership in sustainable compute.

Growing Nordic Subsea Cable Mesh

The 1,175 km C-Lion1 cable linking Helsinki and Rostock introduced the first direct fiber path between Finland and continental Europe, eliminating prior detours through Sweden and Denmark and trimming RTT by 20% for Frankfurt-bound traffic. Far North Fiber, a planned 15,000 km trans-Arctic project, promises 25-40% latency reduction for Asia-Europe routes while avoiding geopolitical chokepoints in the Suez and Malacca corridors. These investments, totaling more than EUR 1 billion (USD 1.14 billion), reposition Finland as a strategic interconnection hub, enabling local facilities to serve both European low-latency zones and trans-polar transit traffic. Enhanced path diversity has already prompted CDNs and FinTech firms to adopt dual-homed deployments in Helsinki for business-continuity planning. As fresh fiber pairs come online, incremental bandwidth supply is expected to lower wholesale IP transit costs, further improving the cost structure of the Finnish data center market.

Surging Cloud and AI / HPC Workloads in Europe

LUMI-Europe’s pre-exascale supercomputer, located in Kajaani-operates entirely on hydroelectric energy and has become a showcase for running 40-140 kW per rack GPU clusters within PUE-1.2 envelopes, validating Finland’s suitability for AI and HPC at scale. Heightened European data-sovereignty expectations, codified under the EU AI Act, require model training and inference to remain within EU borders, steering demand toward compliant, climate-optimized sites. Major cloud service providers are increasingly placing high-density pods in Finnish colocation suites to alleviate thermal constraints in legacy central European regions. The proliferation of generative-AI inference endpoints with 20 ms latency targets is also spurring distributed edge builds in second-tier Finnish cities. Microsoft’s agreement with Fortum to recycle 100% of data-center waste heat into district networks illustrates how AI power demand can dovetail with municipal decarbonization, giving operators a differentiated sustainability narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction costs and limited specialized labor | -4.20% | National, acute in Helsinki Metropolitan Area | Short term (≤ 2 years) |

| Latency distance from Central European user hubs | -3.10% | National, most significant for southern Finland | Medium term (2-4 years) |

| Financing uncertainty for Arctic Connect cable | -1.80% | Northern Finland, Oulu region | Long term (≥ 4 years) |

| Strict permitting on wind farms near reindeer ranges | -1.30% | Lapland region, northern Finland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Construction Costs and Limited Specialized Labor

Finnish building activity contracted 11% in 2024 and is forecast to decline another 5% this year, compressing contractor availability for large-format data center projects. [3].FIEC, “Finland Construction Outlook 2025,” fiec-statistical-report.euScarcity of mission-critical electricians and BMS engineers pushes wage premiums 15-20% above EU averages, elongating build schedules and inflating capex. Simultaneously, copper and steel prices remain elevated due to global demand for electrification, adding roughly 18% to material budgets compared with pre-2024 benchmarks. Smaller entrants without established EPC relationships face financing challenges as banks weigh the costs of overruns against their risk appetites. While hyperscalers can absorb these premiums via purchasing power and standardized design templates, the constraint limits the pace at which diverse providers can expand, tempering overall Finland data center market growth in the near term.

Latency Distance from Central European User Hubs

Round-trip latency from Helsinki to Frankfurt averages 35-45 ms, roughly quadruple that of intra-German paths, which restricts its suitability for ultra-low-latency use cases such as high-frequency trading and real-time multiplayer gaming. Although C-Lion1 and forthcoming Polar routes shave milliseconds, physical distance imposes an immutable floor that forces some workloads to remain in central-European metros. Content platforms often backhaul traffic through German IXPs for peering density, diminishing Finland’s addressable market share for latency-critical services. Enterprises prioritizing cost and carbon footprint can tolerate the delta; yet, segments that monetize immediacy, such as ad-tech bidding and electronic markets, continue to favor Frankfurt or Amsterdam racks. Until edge nodes or latency-tolerant architectures proliferate further, this constraint will subtract momentum from the Finland data center market CAGR over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Size: Hyperscale Deployments Drive Mega Facility Growth

Large sites retained a 42% foothold in 2024, representing the single largest slice of the Finnish data center market size and accommodating gradual, modular expansions by incumbent cloud tenants. Simultaneously, the Mega cohort projects, exceeding 50 MW of power, lead the growth curve at a 31.5% CAGR through 2030, as capital-intensive AI clusters seek contiguous floorplates for 100 kW racks. The Finland data center market benefits from utility-grade land parcels in Kajaani and Oulu, where purchase prices average 30% below Helsinki levels while grid headrooms exceed 100 MW.

Google’s EUR 1 billion (USD 1.14 billion) Hamina phase-four extension exemplifies the Large segment’s steady cadence and underlines confidence in Finland’s renewable supply guarantees. At the other end of the spectrum, XTX Markets’ forthcoming 22.5 MW Kajaani campus showcases the Mega playbook: bespoke, water-cooled halls feeding GPU-dense financial modeling clusters. With multiple municipalities marketing 200-hectare industrial plots, industry experts anticipate the first Massive facility (>150 MW) to break ground before 2027, further inflating Finland data center market capacity.

By Tier Standard: AI Workloads Accelerate Tier IV Adoption

Tier III facilities dominated 2024 with 68% of installed capacity, balancing reliability and capital efficiency for mainstream SaaS and enterprise colocation. However, Tier IV builds are scaling at a 22% CAGR as AI budgets justify redundant distribution paths, concurrently lifting the overall Finland data center market size. Telia’s EN 50600-certified Helsinki complex illustrates cost-optimized Tier III engineering that still attains sub-1.3 PUE via free-air cooling.

Conversely, Microsoft’s planned Azure region is expected to launch with Tier IV architecture, complete 2N power trains, and on-site battery energy storage systems sized for seven minutes at full load, reflecting hyperscaler appetite for zero downtime. The steady drift toward Tier IV creates demand for specialized commissioning talent and raises entry thresholds, potentially tilting Finland data center industry dynamics toward well-capitalized operators.

By Absorption: Pre-Building Strategies Drive Non-Utilized Capacity Growth

Utilized halls made up 78% of the Finland data center market size in 2024, underscoring healthy take-up despite aggressive builds. Yet Non-Utilized shells are ballooning at a 30.5% CAGR because operators prefer “turnkey in 90 days” propositions for hyperscale contracts that materialize with minimal notice. Equinix’s EUR 180 million (USD 205.47 million) two-phase Helsinki expansion doubled its white-space reserve without pre-signed anchor leases, betting on sustained demand from AI-inference clusters.

This forward-build approach moderates provisioning risk as grid-connection and permitting timelines lengthen. Successful absorption hinges on continued European cloud repatriation trends and regulatory pushes for local data processing. Should demand decelerate, oversupply could pressure rack rates, but present forecasts maintain a tight vacancy window, keeping the Finland data center market resilient.

By End-User: Cloud Service Providers Lead Enterprise Transformation

Hyperscale cloud vendors occupy the lion’s share of live megawatts, drawn by Finland’s 100% renewables pathways and competitive PUE metrics. BFSI institutions make increasing use of Finnish racks for analytics, archiving, and regulatory sandboxes compliant with EU data-residency mandates.

Manufacturing conglomerates leverage proximity to Nokia-led 5G testbeds in Oulu for edge prototyping, while public-sector digitalization programs ensure a steady baseline of sovereign workloads. Media and Entertainment firms exploit emerging Arctic fiber to trunk Nordic content toward Asian POPs, diversifying beyond conventional Frankfurt-Amsterdam-London routes. Collectively, these customer verticals reinforce the Finland data center industry pivot from bandwidth-centric colocation to compute-intensive, sustainability-focused services.

Geography Analysis

The Helsinki Metropolitan Area delivered 81% of the installed IT load in 2024, reflecting its dense carrier hotels, multiple submarine cable landings, and district heating integrations that monetize exhaust heat for up to 20,000 apartments via Helen Oy’s network. The region’s ecosystem advantages create virtuous cycles: more carriers attract more enterprises, which in turn justify further power-feed upgrades that enlarge the Finland data center market.

Oulu, historically a telecom R&D nucleus, posts the fastest expansion at a 29% CAGR as Arctic route projects elevate its connectivity status and land prices remain one-third of those in Helsinki. Municipal incentives include expedited zoning and a 90% discount on connection fees for renewable backup generation, positioning the city to capture a double-digit share of the Finland data center market by 2030.

Secondary nodes, such as Tampere, Jyväskylä, and Mantsala, capture niche uses, including underground secure sites, university HPC clusters, or regional edge caching, balancing national capacity distribution. The Saimaa Data Park initiative promotes lakeside plots with cooling water rights, further diversifying geographic risk and supporting grid-balancing objectives through staggered renewable draw profiles.

Competitive Landscape

Finland data center arena features a concentrated yet heterogeneous mix of global hyperscalers and Nordic specialists. Google, Microsoft, and Equinix anchor the market with multi-billion-euro asset bases, leveraging scale to negotiate PPA pricing and fast-track utility upgrades. Domestic incumbents such as Telia, Ficolo, and Digita capitalize on local knowledge, offering turnkey heat-recovery integrations that resonate with municipal planners. XTX Markets and TikTok exemplify a new wave of self-built, single-tenant campuses, focusing on algorithmic finance and social media content governance, respectively.

Competitive vectors revolve around sustainability certifications, district heat revenue shares, and readiness for rack densities exceeding 100 kW, rather than price undercutting. Strategic alliances-Microsoft-Fortum on waste heat, Google-Helen on district heating-signal co-opetition models where energy-system synergies trump conventional leasing battles.

Although deal flow favors large balance sheets, mid-tier players can differentiate through sovereign cloud offerings and edge colocation in underserved northern municipalities. The net effect is a Finland data center market that tilts toward moderate concentration, yet leaves room for innovative entrants targeting specialized workloads or geographic whitespace.

Finland Data Center Industry Leaders

Equinix Finland Oy

Ficolo Oy

Telia Helsinki Data Center (Telia Company)

Digita Oy

Cinia Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TikTok committed EUR 1 billion (USD 1.13 billion) to construct a Kouvola data center under Project Clover, with HyperCo Oy leading delivery and NCC Group providing independent oversight.

- April 2025: Equinix posted USD 2.225 billion in Q1 revenue and confirmed 56 active build projects, including a major Helsinki expansion integrating NVIDIA’s latest AI systems.

- March 2025: Fortum and Microsoft unveiled the world’s largest data-center heat-recovery partnership, cutting district-heating CO₂ emissions by 400,000 t per year in the Helsinki area.

- January 2025: GlobalConnect inaugurated a triple-route terrestrial fiber link between Sweden and Finland, adding 3 Pbit/s of capacity to Nordic backbones.

Finland Data Center Market Report Scope

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I-II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Helsinki Metropolitan Area |

| Oulu |

| Rest of Finland |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I-II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Helsinki Metropolitan Area | ||

| Oulu | |||

| Rest of Finland | |||

Key Questions Answered in the Report

What is the current installed IT load of the Finland data center market?

Installed capacity stood at 736.56 MW in 2025 and is on track for 2,972.7 MW by 2030, equating to a 32.19% CAGR.

Why do hyperscalers favor Finnish sites for AI workloads?

Free-air cooling for 94% of the year, 100% renewable PPAs, and new Arctic cables create low-carbon, low-latency conditions suited to 40-100 kW AI racks.

Which Finnish region is expanding fastest for new facilities?

Oulu leads growth with a projected 29% CAGR through 2030, aided by Arctic fiber projects and lower land prices.

How are data centers monetizing waste heat in Finland?

Operators pipe exhaust heat into district-heating grids; Microsoft-Fortum’s collaboration will offset 400,000 t of CO₂ annually while generating recurring revenue.

What is the major construction-related barrier facing new entrants?

Elevated material costs and a shortage of mission-critical engineers inflate capex and elongate build schedules, pressuring smaller developers.

How does the submarine cable roadmap affect Finland’s role in European connectivity?

C-Lion1 and planned Far North Fiber reduce round-trip times to Germany and Asia, transforming Finland into a strategic interconnection hub.

Page last updated on: