Fibrin Sealants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

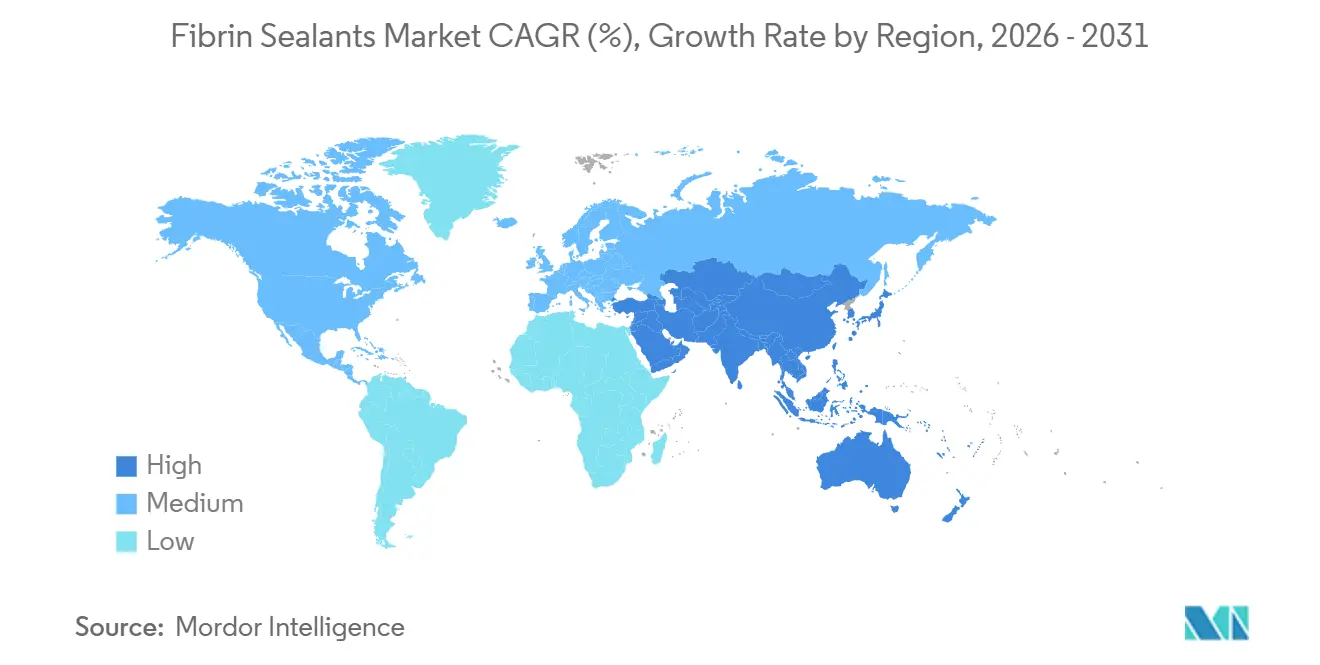

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fibrin Sealants Market Analysis by Mordor Intelligence

The Fibrin Sealants Market size is expected to grow from USD 1.17 billion in 2025 to USD 1.26 billion in 2026 and is forecast to reach USD 1.92 billion by 2031 at 8.74% CAGR over 2026-2031.

Robust growth reflects a structural pivot in surgical hemostasis, as biologic sealants displace sutures and electrocautery in procedures that demand rapid, atraumatic tissue sealing. Accelerated adoption is driven by three converging forces: the spread of robotic surgery platforms that need spray-compatible adjuncts, hospital blood-management protocols that reward fibrinogen supplementation over transfusion, and widening regulatory approvals that now cover pediatric cardiovascular and neurosurgical cases where conventional techniques carry elevated risk [1]Centers for Medicare & Medicaid Services, “OPPS Final Rule,” CMS.gov. North America leads usage because bundled-payment models financially penalize transfusion-related complications, while Asia-Pacific is scaling fastest as China and India roll out surgical-capacity expansions and universal health-coverage schemes. Capital investment by plasma-fractionation incumbents and device specialists further anchors the Fibrin sealants market, yet headline risks include spray-application safety warnings, reimbursement scrutiny, and plasma-supply volatility.

Key Report Takeaways

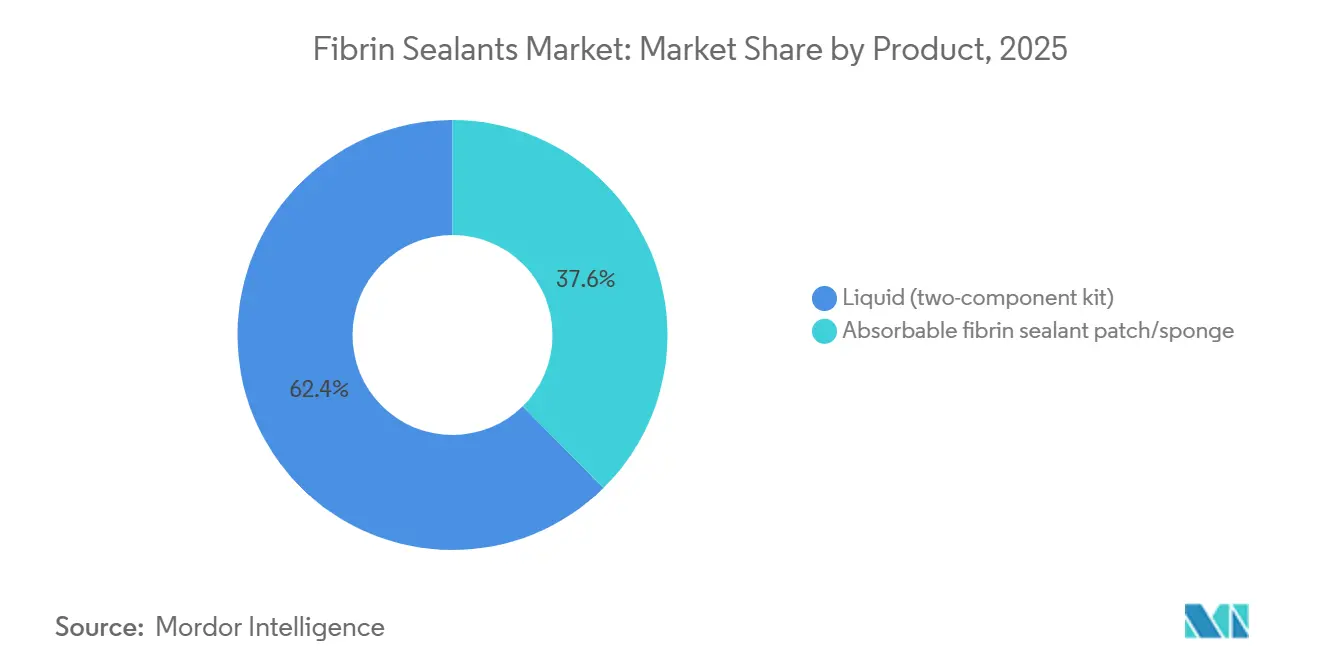

- By product, liquid two-component kits held 62.4% of the Fibrin sealants market share in 2025, while absorbable patches are advancing at a 8.94% CAGR to 2031.

- By source, autologous systems commanded 58.39% share of the Fibrin sealants market size in 2025 and are forecast to expand at 8.96% CAGR through 2031.

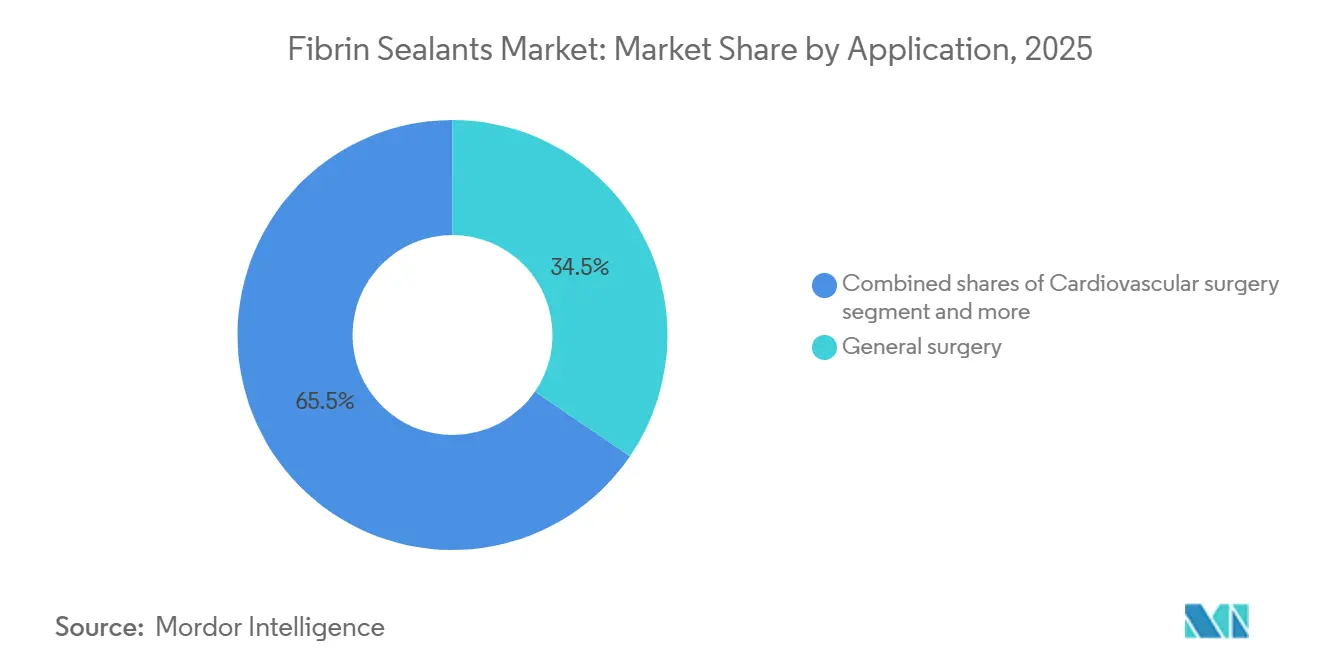

- By application, general surgery led with 34.55% revenue share in 2025; orthopedic surgery posts the highest projected CAGR at 9.12% to 2031.

- By end user, hospitals captured 37.56% share in 2025, whereas ambulatory surgical centers are growing at a 9.45% CAGR through 2031.

- By geography, North America accounted for 45.87% of 2025 revenue, and Asia-Pacific is on track to expand at a 9.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fibrin Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical volumes in cardiovascular and general surgery | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Wider adoption in minimally invasive and robotic procedures | +2.5% | North America, Europe, APAC core markets (Japan, South Korea, Australia) | Short term (≤ 2 years) |

| Hospital protocols favoring blood conservation and hemostasis adjuncts | +1.8% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Product approvals expanding indications and pediatric use | +1.2% | North America, Europe, with spillover to APAC | Long term (≥ 4 years) |

| Shift toward autologous fibrin systems in centers prioritizing pathogen-risk mitigation | +0.9% | North America, Western Europe | Long term (≥ 4 years) |

| Optimized delivery systems for endoscopic/robotic ports and gasless spray applicators | +1.1% | North America, Europe, APAC advanced markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes in Cardiovascular and General Surgery

Cardiovascular and general surgery together drive the highest per-case consumption of fibrin sealants because large anastomotic areas require rapid, diffuse hemostasis. The United Kingdom aims to perform 500,000 robotic surgeries annually by 2035, a policy that increases sealant demand in high-bleed procedures. In the United States, the decline in open-heart volumes has stabilized, thanks to transcatheter valve replacements that still require topical adjuncts. General surgery retained 34.55% of 2025 revenue and continues to benefit from bariatric, hepatobiliary, and colorectal cases that prioritize early discharge, an outcome improved by sealant use. According to a 2025 report by the National Library of Medicine, fibrin sealants are already widely used due to their advantageous properties, such as in situ polymerization, high adhesion, biocompatibility, biodegradability, and biological activity. Fibrin sealants are in high demand in almost all areas of surgery: general surgery, neurosurgery, vascular and nephron-sparing surgery, traumatology and orthopedics, ophthalmic surgery, and reconstructive plastic surgery. Collectively, rising procedure counts provide a dependable volume floor for the Fibrin sealants market.

Wider Adoption in Minimally Invasive and Robotic Procedures

Intuitive Surgical logged 2.4 million da Vinci procedures in 2024, up 17% year over year, with general surgery representing half of all robot-assisted cases [2]Intuitive Surgical, “FY 2024 Results,” Intuitive.com. Sealant formulators now engineer catheters sized for 5 mm and 8 mm ports, while patch suppliers pre-cut matrices to fit robotic graspers. Spray applicators face headwinds after European Medicines Agency advisories linked pressurized gas to embolism; manufacturers are therefore commercializing gasless devices that use mechanical atomization. Reimbursement also boosts uptake: the U.S. decision to cover total-knee arthroplasty in ambulatory surgical centers accelerates outpatient orthopedic work, a setting that depends on fast, clean hemostasis delivered by fibrin sealants. These forces collectively enlarge the addressable case mix for the Fibrin sealants market.

Hospital Protocols Favoring Blood Conservation and Hemostasis Adjuncts

Patient-blood-management guidelines from the American Association of Blood Banks and the American Society of Anesthesiologists endorse restrictive transfusion thresholds and focus on hemostatic optimization [3]American Association of Blood Banks, “Standards for Patient Blood Management,” AABB.org. Topical fibrin sealants fit seamlessly because they cap diffuse oozing that systemic agents cannot reach. Bundled-payment schemes further reward facilities that cut transfusion-related complications, creating direct financial incentives for sealant procurement. The WHO framework recommends fibrinogen concentrate when viscoelastic testing shows deficiency and explicitly extends this logic to topical fibrin formulations. Consequently, formulary committees increasingly place fibrin sealants on mandatory-stock lists for cardiac, orthopedic, and trauma suites.

Product Approvals Expanding Indications and Pediatric Use

Grifols secured FDA approval for VISTASEAL in pediatric populations in October 2024 after achieving 95% hemostasis within four minutes in Phase 3 trials. Baxter updated TISSEEL labeling for neonates in September 2025, closing a key clinician concern on dose precision. Health Canada mirrored the U.S. authorization a month later, and European regulators maintain Plasma Master Files that certify viral safety across suppliers. These milestones open large tertiary pediatric centers that previously restricted sealants to compassionate use. Over the long term, expanded labels translate into steady incremental volume for the Fibrin sealants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spray application safety constraints (air/gas embolism risk) require training and limit use | -1.4% | Global, with heightened scrutiny in Europe | Short term (≤ 2 years) |

| High product cost and reimbursement variability versus alternatives | -1.7% | North America, Europe, with emerging pressure in APAC | Medium term (2-4 years) |

| Plasma-derived input constraints and stringent viral-inactivation/testing steps | -0.8% | Global, most acute in Europe | Long term (≥ 4 years) |

| Mixed clinical benefit across certain indications limits routine use | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spray Application Safety Constraints Require Training and Limit Use

Surgeons must now use devices at defined pressures and distances, and many centers demand formal credentialing. In practice, these stipulations fragment usage because operating-room staff often rotate between multiple specialties and cannot maintain device-specific competencies. Absorbable patches have therefore gained share in laparoscopic, thoracic, and neuro cases where spray is either impractical or contraindicated. Manufacturers are countering with gasless systems and pre-filled syringes, but regulatory review adds time, limiting near-term market penetration.

High Product Cost and Reimbursement Variability Versus Alternatives

Typical U.S. list prices range from USD 400 to 800 per kit, owing to the complexity of plasma fractionation and cold-chain distribution. Ambulatory surgical centers, which collect a notable share of hospital outpatient reimbursement, face acute margin pressure and, when possible, substitute cheaper gelatin sponges or topical thrombin. In Europe, Germany offers separate cardiac-surgery reimbursement, but the United Kingdom caps prices under national framework deals that thin manufacturer margins. Mixed outcomes in peer-reviewed cost-effectiveness analyses add further uncertainty, keeping some formularies on the fence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Liquid Kits Remain Dominant While Patches Accelerate

Liquid two-component kits accounted for 62.4% of 2025 revenue, giving them the largest single slice of the Fibrin sealants market share. They excel in cardiovascular and hepatobiliary surgery because intraoperative mixing preserves thrombin activity until the moment of application, maximizing clot strength. The segment also benefits from delivery flexibility: dual-syringe guns can drip, spray, or stream, enabling surgeons to coat large, irregular surfaces. Yet cold-chain storage, thawing protocols, and setup time challenge ambulatory centers with lean staff. Absorbable patches and sponges are forecast to log a 8.94% CAGR, the fastest within the product category. Patches ride the robotic-surgery wave because 5 mm ports restrict spray-gun maneuvering. Ethicon’s EVARREST, which couples fibrin with oxidized cellulose, underscores physicians' appetite for shelf-stable, ready-to-use products that avoid gas-propulsion risks.

Longer term, the patch subcategory may raise its Fibrin sealants market size share as manufacturers pair fibrin with growth factors or antimicrobials, creating multifunctional matrices for infection-prone patients. However, kit manufacturers defend incumbency by rolling out gasless applicators that meet EMA safety guidance and by miniaturizing nozzles for 5 mm trocars. Evidence from large cardiac centers continues to favor liquid kits in redo sternotomies where broad coverage outperforms patches. Consequently, the market is unlikely to witness wholesale substitution, but rather a pragmatic procedural split: liquids for open and large-field surgery, patches for endoscopic and robotic cases.

By Source: Autologous Systems Surge in Pathogen-Averse Centers

Autologous formulations captured 58.39% of source-based revenue in 2025, aligning with hospitals that prioritize zero viral-transmission risk and immunologic compatibility. Vivostat’s platform processes 120 ml of the patient’s blood to yield 5 ml of sealant with stable fibrinogen content, eliminating donor-pool exposure. Adoption is particularly strong in orthopedic revisions and cardiac cases involving Jehovah’s Witness patients. The autologous segment is expected to post a 8.96% CAGR, bolstered by new compact centrifuges that cut prep time below 20 minutes.

Human plasma-derived products still underpin global supply because vertically integrated giants Grifols, CSL Behring, Takeda, Octapharma control donor pools and fractionation plants. Rigorous solvent-detergent, nanofiltration, and pasteurization regimes meet EMA Plasma Master File standards, sustaining clinician trust. Pricing pressure looms as immunoglobulin demand rises 8-9% annually, competing for the same plasma pool. Animal-derived offerings remain niche because equine or bovine proteins raise immunogenicity flags; Baxter’s collagen-based TachoSil, therefore, finds use mainly in situations where human plasma access is constrained.

By Application: Orthopedic Surgery Emerges as the Fastest-Growing Segment

General surgery generated 34.55% of 2025 revenue, maintaining the biggest slice of the Fibrin sealants market. Use cases span bariatric gastric sleeves, colorectal resections, and hepatic tumor ablations, all of which benefit from reduced drain output and earlier discharge. Cardiovascular surgery follows, driven by valve replacements and aortic repairs conducted under systemic anticoagulation. Orthopedics, however, will deliver the highest growth, advancing at an 9.12% CAGR through 2031. The Fibrin sealants market size for orthopedic applications is projected to climb materially as total-knee arthroplasty relocates to ambulatory surgical centers after CMS added the procedure to the covered list in 2020, unlocking USD 73.4 billion in projected Medicare savings by 2028. Sealants curb postoperative hematomas, speeding rehabilitation and aligning with same-day discharge goals.

Neurosurgery represents a high-value, low-volume niche where sealants reinforce dural closures and curb cerebrospinal fluid leaks. Urology, especially partial nephrectomy and robotic prostatectomy, captures incremental volume as da Vinci cases fall under this specialty. Trauma and transplant centers adopt sealants in damage-control and graft reperfusion settings, respectively, yet overall shares remain modest relative to the big three categories.

By End User: Ambulatory Surgical Centers Outpace Hospitals in Growth

Hospitals absorbed 37.56% of end-user revenue in 2025, reflecting their dominance in complex cardiac and neurosurgical volumes where per-case consumption is highest. Bulk purchasing allows them to negotiate favorable contracts and lock in supplier exclusivity, reinforcing incumbent positions for Baxter, Ethicon, and Grifols. Yet, ambulatory surgical centers projected to grow at 9.45% CAGR, are the nimblest demand node in the Fibrin sealants market. ASCs run lean staff models and need products that shave minutes off turnover; patches and ready-mixed kits thrive here. Value-based payment also drives ASC demand because postoperative bleeds trigger costly readmissions under 90-day bundles.

Specialty clinics in ophthalmology, dermatology, and oral surgery extend product reach beyond the traditional operating theater. Mini-kit launches containing sub-2 ml volumes match the hemostatic needs of micro-incision settings. Regulatory oversight is lighter in ASCs and clinics compared with Joint Commission-accredited hospitals, easing inventory hurdles. Nonetheless, cold-chain obligations remain a barrier for plasma-derived liquids, an issue that autologous systems and room-temperature patches sidestep entirely.

Geography Analysis

North America retained 45.87% of global revenue in 2025, underwritten by the region’s 9,539-unit da Vinci installed base and bundled-payment models that penalize transfusion-related complications. FDA pediatric approval for VISTASEAL in 2024 and Baxter’s neonatal label update in 2025 have opened high-acuity children’s hospitals to commercial sales. Canada and Mexico trail in absolute volumes but are catching up as aging populations swell cardiovascular caseloads.

Europe is more fragmented. Germany reimburses sealants separately in cardiac DRGs, but the U.K. imposes price ceilings under centralized procurement. Chronic plasma deficits. Octapharma’s EUR 200 million expansion in Vienna and its NHS contract to process domestic plasma mark strategic moves to buffer supply shocks. The National Health Service's aim of 500,000 robotic surgeries per year by 2035 furnishes a long-term tailwind for sealants compatible with endoscopic ports.

Asia-Pacific is the fastest-growing region with a projected 9.98% CAGR. Regional healthcare expenditure jumped from USD 3.2 trillion in 2020 to USD 4.2 trillion in 2024 and is on pace for USD 5.7 trillion by 2030. China and India direct public funds into tertiary surgical centers, and local players like Shanghai RAAS and Guangzhou Bioseal are broadening product lines. Japan and South Korea boast high robotic-surgery density, mirroring utilization patterns seen in the United States. While the Middle East, Africa, and South America collectively hold smaller shares, Gulf Cooperation Council investments in medical tourism and Brazil’s push to manage non-communicable diseases are slowly enlarging the addressable base. Cold-chain gaps and reimbursement limitations keep adoption concentrated in private hospitals, but rising trauma volumes linked to road-traffic injuries provide an unserved need that fibrin sealants meet.

Competitive Landscape

The Fibrin sealants market is moderately concentrated. Four plasma-fractionation giants—Grifols, CSL Behring, Takeda, and Octapharma control most fibrinogen and thrombin feedstock through vertically integrated donor networks. Grifols doubled Barcelona plasma capacity to 3.3 million liters in 2025, while Takeda invested USD 230 million in its Los Angeles site to expand fibrinogen lines. Octapharma’s EUR 200 million Vienna upgrade and its U.K. NHS contract mark hedges against import bottlenecks. Device specialists Baxter and Ethicon differentiate on applicator ergonomics; both race to commercialize gasless spray guns that satisfy EMA safety criteria.

White-space innovation targets biosynthetic or recombinant fibrin to bypass plasma supply; early programs combine sealant matrices with antimicrobial peptides for infection-prone wounds. Vivostat and Hemarus court pathogen-averse hospitals via point-of-care autologous platforms, undermining pooled-plasma incumbents. Potential new entrants include Stryker, which logged USD 22.6 billion in revenue in 2024 and signals interest in biologics, and Corza Medical, which has acquired multiple specialty hemostat assets. Barriers remain formidable: EMA Plasma Master Files act as regulatory moats, and raw-plasma inflation narrows margins for smaller firms lacking donor infrastructure.

Competitive tactics increasingly hinge on contracting. U.S. health systems consolidate purchasing under Integrated Delivery Networks that award multi-year, volume-based deals. European tenders prioritize cost and viral safety, advantaging suppliers that can certify domestic plasma sourcing. In Asia-Pacific, joint ventures with regional blood-collection agencies secure feedstock and win political goodwill. Overall, scale, vertical integration, and device innovation remain the cornerstones of share defense in the Fibrin sealants market.

Fibrin Sealants Industry Leaders

Grifols, S.A.

CSL Behring

Takeda Pharmaceutical Company

Octapharma AG

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: A study published in MDPI Medicina found that combining TISSEEL fibrin sealant with sutures in a rat model significantly increases neovascularization during tubal reconstructive surgery

- June 2025: Johnson & Johnson rolled out a refined version of its EVICEL fibrin sealant, engineered for improved stability and faster hemostasis in cardiovascular, orthopedic, and trauma surgeries.

- April 2025: CSL Behring announced that the European Commission has authorized the use of Tissucol in neurosurgery, expanding its application for managing surgical bleeding.

Global Fibrin Sealants Market Report Scope

As per the scope of the report, fibrin sealants are a class of biological surgical glues and hemostatic agents that mimic the final stages of the natural human blood coagulation cascade. They are typically two-component systems consisting of fibrinogen (a protein) and thrombin (an enzyme). When these components are mixed, typically in the presence of calcium and Factor XIII, thrombin converts fibrinogen into insoluble fibrin strands that form a stable, physiological clot.

The Fibrin Sealants Market is segmented by product, source, application, end users, and geography. By product, the market is segmented into liquid (two-component kit), and Absorbable fibrin sealant patch. By source, the market is segmented into human, autologous, and animal-derived. By Application, the market is segmented into cardiovascular surgery, general surgery, neurosurgery, orthopedic surgery, urology, and others. By end users, the market is segmented into hospitals, ambulatory surgical centers (ASCs), and specialty clinics.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Liquid (two-component kit) |

| Absorbable fibrin sealant patch |

| Human |

| Autologous |

| Animal-derived |

| Cardiovascular surgery |

| General surgery |

| Neurosurgery |

| Orthopedic surgery |

| Urology |

| Others |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Liquid (two-component kit) | |

| Absorbable fibrin sealant patch | ||

| By Source | Human | |

| Autologous | ||

| Animal-derived | ||

| By Application (Surgery) | Cardiovascular surgery | |

| General surgery | ||

| Neurosurgery | ||

| Orthopedic surgery | ||

| Urology | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the fibrin sealants market be by 2031?

Forecasts point to USD 1.92 billion, implying a CAGR of 8.74% from 2026

Which product type holds the biggest share today?

Liquid two-component kits account for 62.4% of 2025 revenue Liquid two-component kits account for 62.4% of 2025 revenue .

What segment is growing fastest?

Orthopedic surgery is projected to post an 9.12% CAGR to 2031, aided by outpatient joint-replacement growth

Why is Asia-Pacific a focus region?

Health-care spending there is expected to reach USD 5.7 trillion by 2030, driving a 9.98% CAGR in regional sales.

Page last updated on: