Size and Share of Fiber Optic Sensing Market For Industrial and Infrastructure Monitoring

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.85 Billion |

| Growth Rate (2026 - 2031) | 10.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Fiber Optic Sensing Market For Industrial and Infrastructure Monitoring by Mordor Intelligence

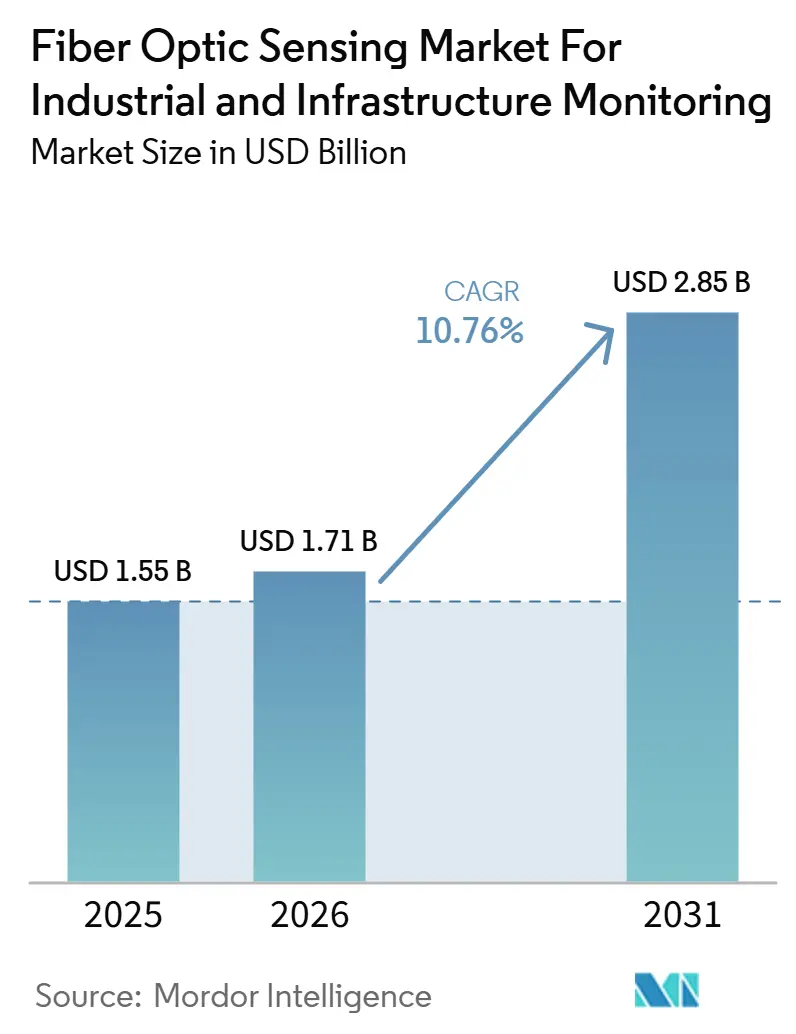

The fiber optic sensing market for industrial and infrastructure monitoring size was valued at USD 1.55 billion in 2025 and estimated to grow from USD 1.71 billion in 2026 to reach USD 2.85 billion by 2031, at a CAGR of 10.76% during the forecast period (2026-2031). The fiber optic sensing market for industrial and infrastructure monitoring is expanding because operators need continuous monitoring across pipelines, power cables, transport corridors, and other long linear assets where electronic sensors often fail under electromagnetic interference or extreme temperatures. The ability to convert existing fiber routes into distributed sensing networks is shortening payback periods and widening adoption beyond new-build projects. Insurance and reinsurance practices are also pushing asset owners toward real-time monitoring because continuous data can lower outage exposure and improve risk visibility. Across energy, civil infrastructure, and defense use cases, the fiber optic sensing market for industrial and infrastructure monitoring is benefiting from the practical value of reducing unplanned outages, limiting third-party liability, and enabling faster operational decisions. A second shift is also underway as AI-enabled edge interrogators begin to reduce the burden of signal interpretation, which should help the fiber-optic sensing market for industrial and infrastructure monitoring expand into mid-tier applications such as water networks, chemical plants, and light rail systems.

Key Report Takeaways

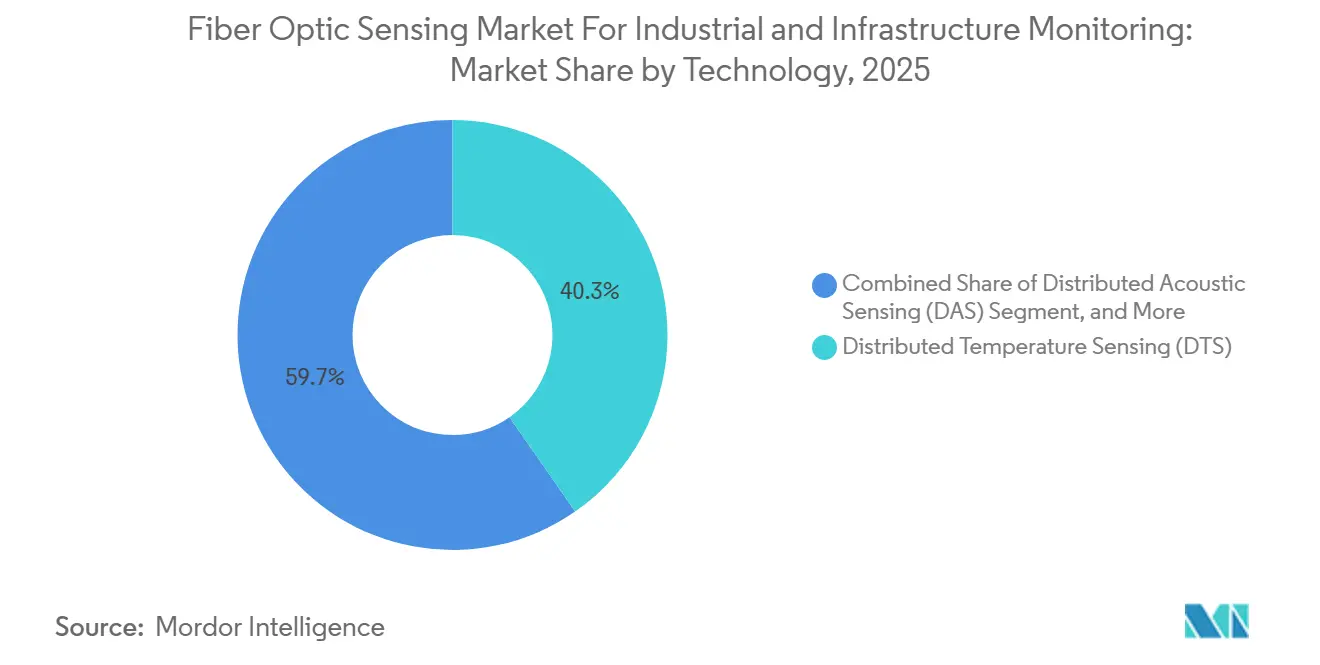

- By technology, Distributed Temperature Sensing held 40.34% of the fiber optic sensing market for industrial and infrastructure monitoring share in 2025, while Distributed Acoustic Sensing is projected to expand at a 10.32% CAGR through 2031.

- By application, pipeline monitoring accounted for 32.45% share in 2025, while perimeter and border security is expected to record the fastest growth at 11.45% CAGR through 2031.

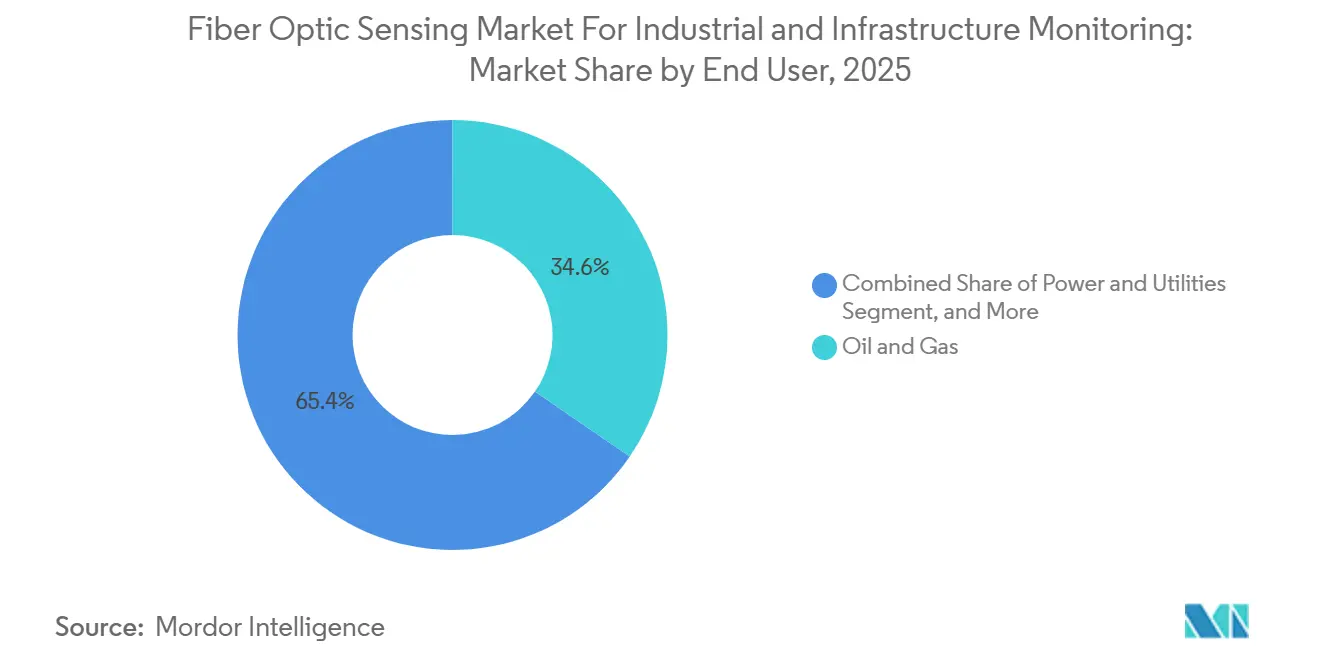

- By end user, oil and gas held 34.56% share in 2025, while defense and border security are projected to grow at a 10.89% CAGR through 2031.

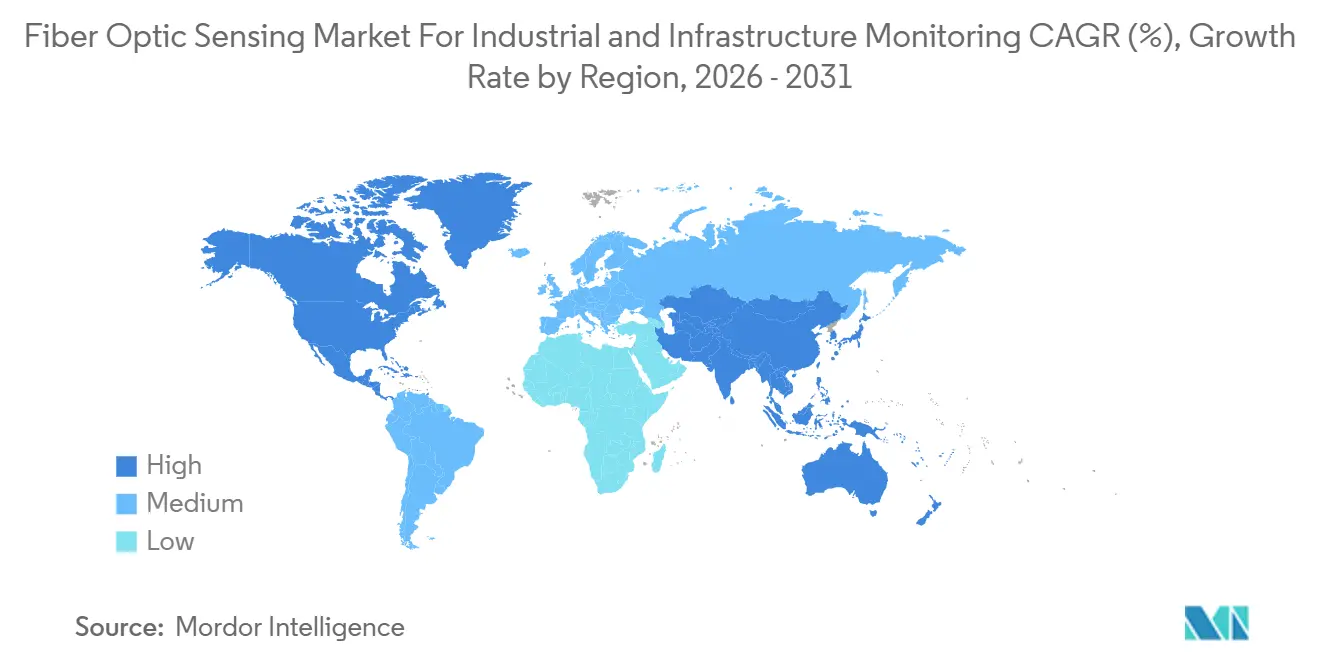

- By geography, North America led with a 31.78% share in 2025, while the Asia-Pacific is expected to advance at a 11.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Fiber Optic Sensing Market For Industrial and Infrastructure Monitoring

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Infrastructure Safety Monitoring | +2.8% | Global | Short term (≤ 2 years) |

| Stricter International Regulations for Critical Asset Integrity | +2.1% | North America and EU, spillover to APAC and MEA | Medium term (2-4 years) |

| Expansion of Oil, Gas, and Renewable Energy Infrastructure | +1.9% | Middle East, North America, Asia Pacific | Medium term (2-4 years) |

| Increasing Integration of Smart Grid and Industrial IoT Systems | +1.5% | APAC core, spillover to North America and EU | Long term (≥ 4 years) |

| Growth in Military, Defense, and Border Security Spending | +1.2% | North America and EU, with early gains in MEA and APAC | Medium term (2-4 years) |

| Shift Toward Predictive Maintenance and Condition-Based Operations | +1.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Real-Time Infrastructure Safety Monitoring

The fiber optic sensing market for industrial and infrastructure monitoring industry is gaining support from a basic operating need, which is to monitor pipelines, power cables, tunnels, and transport assets without interruption. Many long assets still depend on periodic manual inspection, and that creates gaps between inspection cycles when leaks, fires, strain, or vibration can go unnoticed. International standards are helping buyers move faster by reducing uncertainty around technical performance and interoperability. IEEE published IEEE 3461-2025 in February 2026, and that standard set out performance expectations for smart infrastructure applications such as bridges, tunnels, dams, rail lines, power lines, and pipelines.[1]IEEE Standards Association, “IEEE 3461-2025 IEEE Standard for Smart Infrastructure with Fiber Optic Sensors,” IEEE Standards Association The financial case is also strengthening, as insurers and reinsurance underwriters increasingly value real-time condition data when assessing exposure to critical infrastructure. Pipeline monitoring already held 32.45% of the application base in 2025, indicating that this driver has already translated into real deployments across the fiber optic sensing market for industrial and infrastructure monitoring.

Stricter International Regulations for Critical Asset Integrity

The fiber optic sensing market for industrial and infrastructure monitoring is also moving higher as regulations are tightening across pipeline integrity, grid resilience, and infrastructure protection. This matters because distributed sensing spans several compliance areas rather than serving a single, narrow use case. The ITU approved Recommendation G.681 in November 2025, and that framework formally addressed distributed fiber optic sensing systems used with terrestrial optical transmission networks. Europe is also developing more consistent commissioning practices following CIGRE's guidance on site acceptance testing for DTS and DAS systems used in power cable monitoring.[2]AP Sensing, “Fiber Optic Monitoring for Offshore Wind Export Cables,” AP Sensing News China added another layer with GB/T 47547-2026 for optical fiber monitoring systems in direct-buried insulated pipelines, indicating that sensing requirements are moving deeper into civil engineering practice. As these rules become more specific, the fiber optic sensing market for industrial and infrastructure monitoring favors vendors with established compliance records, validated performance histories, and the ability to pass qualification reviews with less friction.

Expansion of Oil, Gas, and Renewable Energy Infrastructure

The fiber optic sensing market for industrial and infrastructure monitoring is benefiting from 2 build cycles that are moving at the same time, which are oil and gas infrastructure growth and renewable power expansion. Pipelines, well monitoring systems, and offshore export cables all require long-distance monitoring in harsh conditions, and distributed sensing fits those needs better than point sensors. AP Sensing delivered integrated distributed fiber optic monitoring across the Fécamp, Saint-Brieuc, and Gruissan offshore wind projects in 2026, showing how DTS and DAS can support hotspot detection and intrusion monitoring along subsea export cables.[3]CIGRE, “Technical Brochure 984 Guidelines for SAT of DTS and DAS Systems When Used for Power Cable Systems Monitoring,” CIGRE That matters because offshore wind projects create service opportunities that continue long after the initial hardware delivery, especially where cable health must be monitored continuously over long marine routes. The same pattern supports energy assets on land because operators want better leak detection, fault detection, and corridor visibility without relying on dense arrays of discrete devices. As a result, the fiber optic sensing market for industrial and infrastructure monitoring is drawing demand from both hydrocarbon infrastructure and energy transition projects, which broadens the revenue base and lowers dependence on any single asset class.

Increasing Integration Of Smart Grid And Industrial IoT Systems

The fiber optic sensing market for industrial and infrastructure monitoring is also gaining from a shift in how utilities and industrial operators use existing fiber assets. In many cases, the cable is already in the ground or on the network, so the main decision is no longer whether to install fiber, but whether to activate it as a sensing layer. AP Sensing and Ampacimon announced a collaboration in February 2026 that combined distributed fiber optic sensing with dynamic line rating for overhead transmission monitoring. That approach uses DAS on optical ground wire to read real-time wind conditions at span level, which can help operators increase corridor capacity without building new transmission infrastructure. The shift is important because it changes the economics of deployment and makes monitoring more viable across a wider set of assets. Over time, the fiber optic sensing market for industrial and infrastructure monitoring should see more competition in software, analytics, and service contracts, as value shifts from the fiber itself to the quality of the operational intelligence built on top of it.

High Initial Capital And Installation Expenditure

The fiber optic sensing market for industrial and infrastructure monitoring still faces a clear barrier in the form of high upfront deployment costs, especially in subsea, underground, and hazardous environments. Ruggedized fiber, trenching, marine-grade connectors, interrogator units, data acquisition systems, and analytics platforms can make the first approval stage difficult for public agencies and mid-sized operators. Even when lifecycle economics are favorable, many buyers still focus on installation cost because that is the number that enters capital budgeting first. VIAVI launched the FTH-DAS in March 2026 with embedded edge AI and machine learning, reducing infrastructure burden by limiting reliance on centralized data processing. That helps, but it does not change the fact that long-distance monitoring across hundreds of kilometers still requires substantial hardware and installation costs. Until standard packages and lower-cost deployment models scale further, this restraint will continue to slow the fiber optic sensing market for industrial and infrastructure monitoring in cost-sensitive regions.

Need For Specialized Technical Expertise In Data Interpretation

The fiber optic sensing market for industrial and infrastructure monitoring also slows when end users struggle to interpret continuous multi-parameter data streams. Installing a sensing cable is often simpler than converting vibration, acoustic, temperature, or strain signals into decisions that operating teams trust. A DAS event on a pipeline corridor, for example, can reflect a leak, an intrusion, or environmental noise, and separating those patterns requires both sensing knowledge and asset-specific context. The same issue applies to structural monitoring, where interpreting strain evolution demands an understanding of both photonics and civil asset behavior. Vendors are responding by packaging analytics and managed services with hardware, but that shifts the business model toward long-term software and service commitments rather than one-time equipment sales. Until automated classification tools mature further and buyers develop more in-house confidence, this skills gap will remain a practical restraint on wider penetration across the fiber optic sensing market for industrial and infrastructure monitoring.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: DTS Anchors The Base As DAS Reshapes Market Dynamics

Distributed Temperature Sensing held 40.34% of the technology base in 2025, which made it the largest contributor to the fiber optic sensing market for industrial and infrastructure monitoring within this segment group. Its position was built over years of use in power cable thermal rating, downhole monitoring, and fire detection across tunnels and data centers. The installed base matters because it creates recurring service, maintenance, and upgrade work long after the first deployment is completed. Utilities that installed DTS systems earlier in the last decade are now moving into refresh cycles as older interrogators near end-of-support and operators seek stronger anomaly detection. This gives the fiber optic sensing market for industrial and infrastructure monitoring a replacement stream that supports demand even in applications that are already well penetrated.

DAS is projected to expand at a 10.32% CAGR from 2026 to 2031, which makes it the fastest-moving technology line in the fiber optic sensing market for industrial and infrastructure monitoring industry. Buyers are responding to the fact that one DAS channel can detect leaks, intrusions, and geohazards along the same corridor, which improves the value case against point-sensor arrays. Distributed Strain Sensing is also gaining traction in bridges, dams, offshore wind foundations, and other structures where long-term strain change provides earlier warning than periodic field inspection. NTT and the University of Tokyo demonstrated a multi-fiber B-OTDR shape sensing technique in March 2026 that improved detection of curvature over long distances and opened additional possibilities in marine, aviation, and urban utility applications.[4]NTT, Inc., “NTT and the University of Tokyo Demonstrate a New Technology for Detecting Invisible Deformation in Large-Scale Structures Using Optical Fiber,” NTT News Release As technical capability improves, the fiber optic sensing market for industrial and infrastructure monitoring is shifting from single-parameter monitoring toward multi-use sensing platforms that can justify broader capital approval.

By Application: Pipeline Monitoring Underpins Revenue As Perimeter Security Accelerates

Pipeline monitoring accounted for 32.45% of the application base in 2025, and that gave it the largest share of the fiber optic sensing market for industrial and infrastructure monitoring among major application categories. This lead reflects the scale of global pipeline networks and the direct cost of leaks, service interruptions, and integrity failures. Operators are also attracted to the ability to use pre-installed fiber running along pipeline corridors, which can reduce civil works and improve the economics of deployment. In this application set, existing telecom routes often become sensing backbones, and that materially improves the practical case for adoption. Pipeline work, therefore, continues to provide the broad commercial base for the fiber optic sensing market for industrial and infrastructure monitoring, especially where compliance pressure is high.

Perimeter and border security is projected to grow at an 11.45% CAGR through 2031, which makes it the fastest-growing application in the fiber optic sensing market for industrial and infrastructure monitoring industry. Defense buyers value the ability of DAS systems to provide long-distance continuous surveillance with lower false alarm rates than many conventional electronic fence systems. The overlap with pipeline protection is also important because the same vendor pool can serve both use cases in the same geography, which shortens qualification cycles and expands account value. Structural health monitoring remains another large application because bridge managers, tunnel operators, and port authorities need integrity data without lane closures or repeated manual inspection. Rail infrastructure and power cable monitoring add further stability because both asset classes benefit from continuous thermal and acoustic data that can reduce unplanned outages and speed maintenance response.

The remaining application mix also shows how the fiber optic sensing market for industrial and infrastructure monitoring is broadening beyond its earlier concentration in energy infrastructure. Rail programs often benefit from lineside fiber that was originally installed for telecoms or signaling, which means the incremental deployment cost can be limited to interrogators and system integration. That model is proving commercially workable in emerging Asian markets where infrastructure modernization budgets are active but still disciplined. The others category includes areas such as carbon capture and storage well monitoring, where long-duration subsurface observation is becoming more important. Luna’s integration of Silixa increased relevance in this space because the combined portfolio brought together acoustic, strain, and temperature capabilities that fit energy transition use cases. These shifts indicate that the fiber optic sensing market for industrial and infrastructure monitoring is becoming more diversified by use case even while pipeline monitoring remains the core revenue anchor.

By End User: Oil And Gas Sustains Dominance While Defense Spending Accelerates

Oil and gas held 34.56% of the end-user base in 2025, which gave it the largest fiber optic sensing market for industrial and infrastructure monitoring share among end-user categories. That position reflects the sector’s need to monitor pipelines, wells, gathering systems, and completions across wide and often harsh operating environments. The business case is clear because real-time data can reduce leak exposure, improve completion quality, and support better production decisions. Regulatory expectations also remain strong, especially where pipeline integrity and environmental risk are closely monitored. As a result, oil and gas continue to provide the most established deployment base in the fiber optic sensing market for industrial and infrastructure monitoring.

Defense and border security are projected to expand at a 10.89% CAGR from 2026 to 2031, which makes it the fastest-growing end-user category. Governments are allocating more capital to persistent perimeter surveillance, and fiber-based sensing fits that need because it can use existing infrastructure while covering long distances. The overlap with pipeline protection in energy-producing regions creates a compounding demand effect because the same corridors often carry both security and asset protection requirements. This is one reason the fiber optic sensing market for industrial and infrastructure monitoring is finding more cross-vertical leverage than many vendors fully captured in earlier planning cycles. In practical terms, a vendor qualified for one security-sensitive use case may gain access to adjacent infrastructure programs faster than before.

Power and utilities form the next large user group because grid operators rely on DTS for cable thermal rating and increasingly use DAS for overhead line vibration sensing and dynamic line rating. Transportation users, including rail operators, road authorities, and port operators, remain at an earlier adoption stage, but the value case is improving as aging infrastructure needs more frequent condition data. Civil infrastructure buyers are also moving steadily because bridges, tunnels, and dams benefit from the ability to track micro-strain over time instead of depending only on periodic inspection. The others category includes water utilities and data center operators, where pilot activity has started around leak detection and cable intrusion monitoring. Together, these patterns show that the fiber optic sensing market for industrial and infrastructure monitoring is retaining its oil and gas center while widening toward public infrastructure and utility applications.

Geography Analysis

North America held 31.78% in 2025, which gave it the largest share of the fiber optic sensing market for industrial and infrastructure monitoring across all regions. The region benefits from a large installed base of regulated pipeline infrastructure and a strong commercial base for DAS in oil-field and well integrity applications. The United States remains the most active deployment market because operators use fiber sensing across hydraulic fracturing optimization, production monitoring, and pipeline protection. Canada adds demand through oil sands pipeline monitoring and civil infrastructure programs, while Mexico is building momentum as pipeline modernization advances. Grid modernization funding is also expanding the addressable base for the fiber optic sensing market for industrial and infrastructure monitoring across power and utility applications.

Europe remained an important regional pillar because energy transition goals and infrastructure monitoring needs are moving in parallel. Germany’s SuedOstLink HVDC corridor is a strong example because it embeds distributed sensing into a major renewable energy transmission route for thermal rating, fault detection, and intrusion monitoring. That kind of project supports the region’s role as a testing ground for high-specification sensing deployments tied to long-life infrastructure. European utilities and infrastructure operators also benefit from clearer commissioning guidance, which lowers uncertainty during procurement and commissioning. For the broader fiber optic sensing market for industrial and infrastructure monitoring, Europe remains important because it links policy goals, grid investment, and validated use cases in a relatively mature procurement environment.

Asia Pacific is projected to grow at an 11.21% CAGR from 2026 to 2031, and that makes it the fastest-growing regional block in the fiber optic sensing market for industrial and infrastructure monitoring. State-backed smart infrastructure programs, offshore wind development, and domestic sensing technology progress are all lifting demand. China is reinforcing that direction through standards tied to oil and gas well monitoring and pipeline applications, which signals policy support for distributed sensing as a strategic technology area. Japan is also contributing at the technology frontier because NTT’s March 2026 work on multi-fiber B-OTDR shape sensing advanced precision for large-scale structural monitoring. South America and the Middle East and Africa region still represent a smaller base, but both are growing. In South America, Lightera and Immer Messen completed DAS trials on a 500kV transmission line in Brazil in January 2026, which marked a meaningful step for utility-focused adoption. In the Middle East and Africa region, oil and gas pipeline monitoring remains the main demand driver, while border-sensitive locations add secondary support through perimeter surveillance needs.

Competitive Landscape

The fiber optic sensing market for industrial and infrastructure monitoring remains moderately fragmented, with established vendors such as AP Sensing, Halliburton, VIAVI Solutions, Bandweaver, Fotech Solutions, Siemens, Silixa, Yokogawa, and others competing across DTS, DAS, and integration work. No single company appears to dominate every major application because the market spans energy, utilities, transport, civil infrastructure, and security needs that require different technical strengths. The practical distinction between leaders increasingly comes from analytics, AI capability, application libraries, and project execution experience rather than from core optical components alone. This means the fiber optic sensing market for industrial and infrastructure monitoring rewards vendors that can turn raw backscatter data into reliable operational alerts with lower interpretation burden for end users. It also explains why specialized firms remain relevant even when larger companies have broader commercial reach.

Strategic moves in 2026 showed this shift clearly. VIAVI launched the FTH-DAS interrogator in March 2026 with embedded AI and machine learning at the edge, which strengthened the push toward localized event classification and reduced dependence on centralized processing. AP Sensing expanded its position in offshore renewables through deployments on 3 French offshore wind projects, which supported its presence in subsea cable monitoring and long-term service work. Luna’s acquisition of Silixa for up to USD 38 million in January 2024 added acoustic, strain, and temperature sensing depth and strengthened carbon capture and subsea monitoring relevance. These actions show that the fiber optic sensing market for industrial and infrastructure monitoring is consolidating around platforms that combine hardware, software, and application-specific know-how.

There is still open space in mid-tier assets such as chemical plants, water networks, and light rail systems, where high-end solutions are often too costly or too customized for broad rollouts. Vendors that package simpler installation models with bundled analytics can capture demand that sits below the large oil and gas and utility projects. Intellectual property also remains part of the competitive equation in subsurface sensing. Halliburton received USPTO grant US 12,578,209 B2 in March 2026 for a distributed acoustic sensing system using a split interrogator, which highlights continued effort to defend specialized positions in high-value well and production applications. Overall, the fiber optic sensing market for industrial and infrastructure monitoring is competitive enough to support specialist entrants, but still selective enough that proven execution and domain knowledge remain hard to replace.

Leaders of Fiber Optic Sensing Market For Industrial and Infrastructure Monitoring

AP Sensing GmbH

Aragon Photonics, S.L.

Bandweaver Technologies Ltd.

Halliburton Company

Hottinger, Brüel & Kjær A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AP Sensing delivered distributed fiber optic monitoring solutions for 3 offshore wind projects in France, Fécamp, Saint-Brieuc, and Gruissan, integrating DTS for real-time hotspot detection, DAS-based third-party intrusion monitoring, and advanced analytics for power cable health along subsea export cable routes. The deployment marks a significant expansion into offshore renewables and is expected to generate long-term O&M service contracts as European wind capacity scales.

- March 2026: VIAVI Solutions launched the FTH-DAS, a true-phase DAS fiber sensing interrogator with an embedded AI and machine learning engine for its NITRO Fiber Sensing platform. The device applies patented phase-stepping interferometry to measure strain, vibration amplitude, and acoustic power in true physical units, running all event classification models locally at the network edge without requiring centralized infrastructure.

- March 2026: NTT, Inc. and the Graduate School of Engineering at the University of Tokyo announced a world-first optical fiber shape sensing technique using a multi-fiber B-OTDR cable, achieving less than 1% error for 10-meter curvature radius detection over distances of several kilometers, an order-of-magnitude improvement over prior systems. The technology enables structural deformation monitoring for offshore wind turbine foundations, underground pipeline networks, and large civil structures, with findings published in the IEEE Journal of Lightwave Technology.

- January 2026: Lightera, Furukawa Electric's global fiber operations arm, and Immer Messen, a Brazilian DAS specialist, completed successful fiber optic sensing trials on a 500kV power transmission line in Brazil, and entered into a strategic partnership to develop and scale distributed fiber optic sensing solutions for the South American power transmission sector.

Scope of Report on Fiber Optic Sensing Market For Industrial and Infrastructure Monitoring

The Fiber Optic Sensing Market for Industrial and Infrastructure Monitoring Industry Report is Segmented by Technology (Distributed Acoustic Sensing (DAS), Distributed Temperature Sensing (DTS), Distributed Strain Sensing (DSS), and Others Technology), Application (Pipeline Monitoring, Structural Health Monitoring, Power Cable and Grid Asset Monitoring, Rail Infrastructure Monitoring, Perimeter and Border Security, and Other Applications), End User (Oil and Gas, Power and Utilities, Transportation and Railways, Civil Infrastructure and Construction, Defense and Border Security, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Distributed Acoustic Sensing (DAS) |

| Distributed Temperature Sensing (DTS) |

| Distributed Strain Sensing (DSS) |

| Others Technology |

| Pipeline Monitoring |

| Structural Health Monitoring |

| Power Cable and Grid Asset Monitoring |

| Rail Infrastructure Monitoring |

| Perimeter and Border Security |

| Other Applications |

| Oil and Gas |

| Power and Utilities |

| Transportation and Railways |

| Civil Infrastructure and Construction |

| Defense and Border Security |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | Distributed Acoustic Sensing (DAS) | ||

| Distributed Temperature Sensing (DTS) | |||

| Distributed Strain Sensing (DSS) | |||

| Others Technology | |||

| By Application | Pipeline Monitoring | ||

| Structural Health Monitoring | |||

| Power Cable and Grid Asset Monitoring | |||

| Rail Infrastructure Monitoring | |||

| Perimeter and Border Security | |||

| Other Applications | |||

| By End User | Oil and Gas | ||

| Power and Utilities | |||

| Transportation and Railways | |||

| Civil Infrastructure and Construction | |||

| Defense and Border Security | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the fiber optic sensing market for industrial and infrastructure monitoring?

The fiber optic sensing market size for industrial and infrastructure monitoring industry was USD 1.55 billion in 2025 and stands at USD 1.71 billion in 2026. It is projected to reach USD 2.85 billion by 2031 at a 10.76% CAGR.

Which technology leads revenue in fiber optic sensing?

Distributed Temperature Sensing led the technology segment with 40.34% share in 2025, supported by its long use in power cable monitoring, fire detection, and downhole applications.

Which application is growing fastest through 2031?

Perimeter and border security is projected to record the fastest application growth at an 11.45% CAGR, driven by long-distance surveillance needs and defense spending.

Why does oil and gas remain the largest end-user segment?

Oil and gas held 34.56% share in 2025 because operators need continuous monitoring for pipelines, wells, and gathering systems where leak risk and integrity requirements are high.

Which region is leading the fiber optic sensing market for industrial and infrastructure monitoring industry today?

North America led with 31.78% share in 2025 due to its large regulated pipeline base, active DAS deployments, and wider use in energy and utility assets.

Which region is expected to grow the fastest in the coming years?

Asia-Pacific is projected to expand at an 11.21% CAGR through 2031, supported by smart infrastructure programs, offshore wind investment, and local sensing technology development.

Page last updated on: