Size and Share of Fiber Optic Network Infrastructure Market For Emergency Communication Systems

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.49 Billion |

| Market Size (2031) | USD 6.57 Billion |

| Growth Rate (2026 - 2031) | 7.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Fiber Optic Network Infrastructure Market For Emergency Communication Systems by Mordor Intelligence

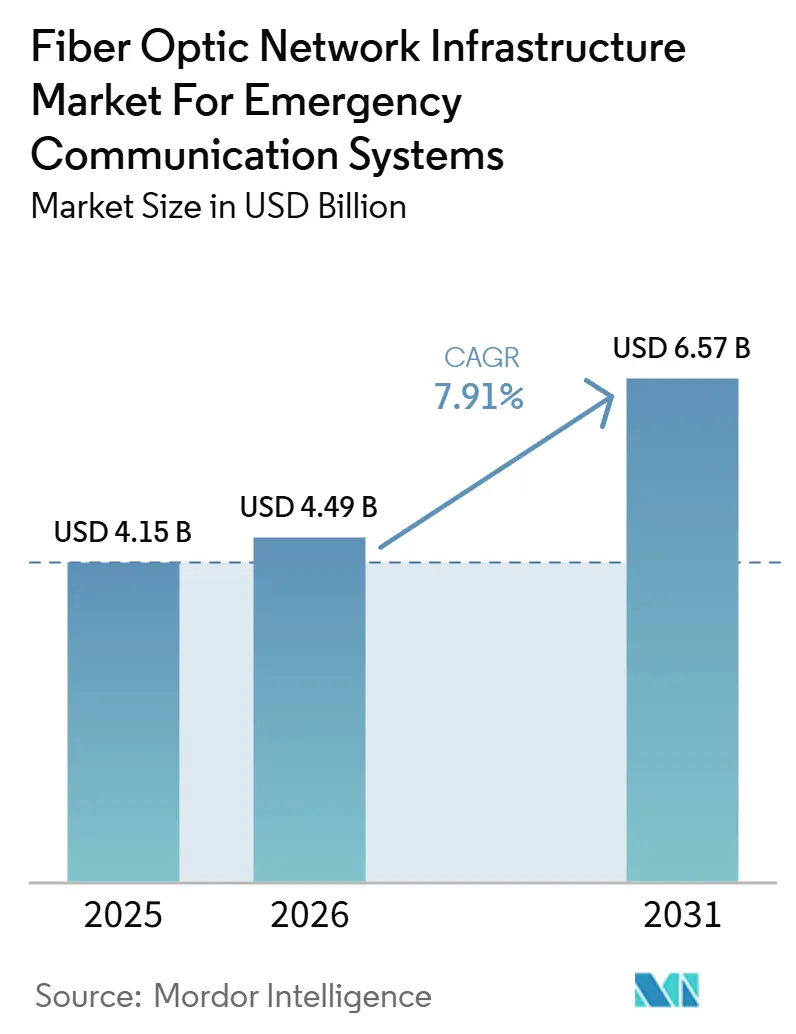

The fiber optic network infrastructure market for emergency communication systems industry is expected to increase from USD 4.15 billion in 2025 to USD 4.49 billion in 2026 and reach USD 6.57 billion by 2031, growing at a CAGR of 7.91% over 2026-2031. The fiber optic network infrastructure market for emergency communication systems is advancing as regulators push agencies to replace aging copper and narrowband systems with higher-capacity optical networks. Agencies are also finding that one fiber backbone can carry voice, video, and sensor data more efficiently than separate communication systems, which supports broader modernization plans. Public funding programs in North America, Europe, and the Asia Pacific are expanding conduit access and network reach, which makes dedicated emergency deployments easier to scale. Vendors are responding by combining transport hardware, management software, and support services into integrated offerings that align with multi-year public procurement cycles. The main limits remain civil works costs, permitting delays, legacy radio integration, and technician shortages, yet these issues are slowing deployment rather than weakening the long-term case for modernization.

Key Report Takeaways

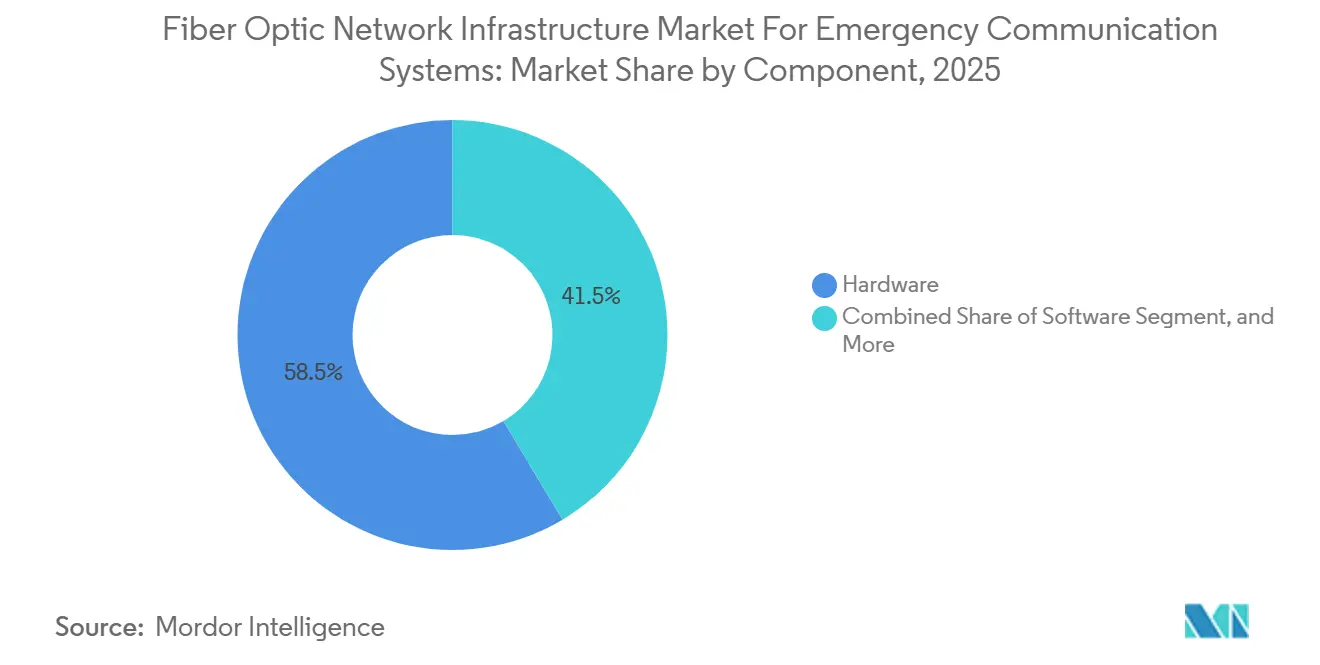

- By component type, hardware held 58.54% share in 2025, and software is projected to expand at an 8.13% CAGR through 2031 in the fiber optic network infrastructure market for emergency communication systems.

- By fiber and cable type, single-mode fiber accounted for 62.69% of the market in 2025, and plastic optical fiber is expected to expand at a 7.65% CAGR through 2031.

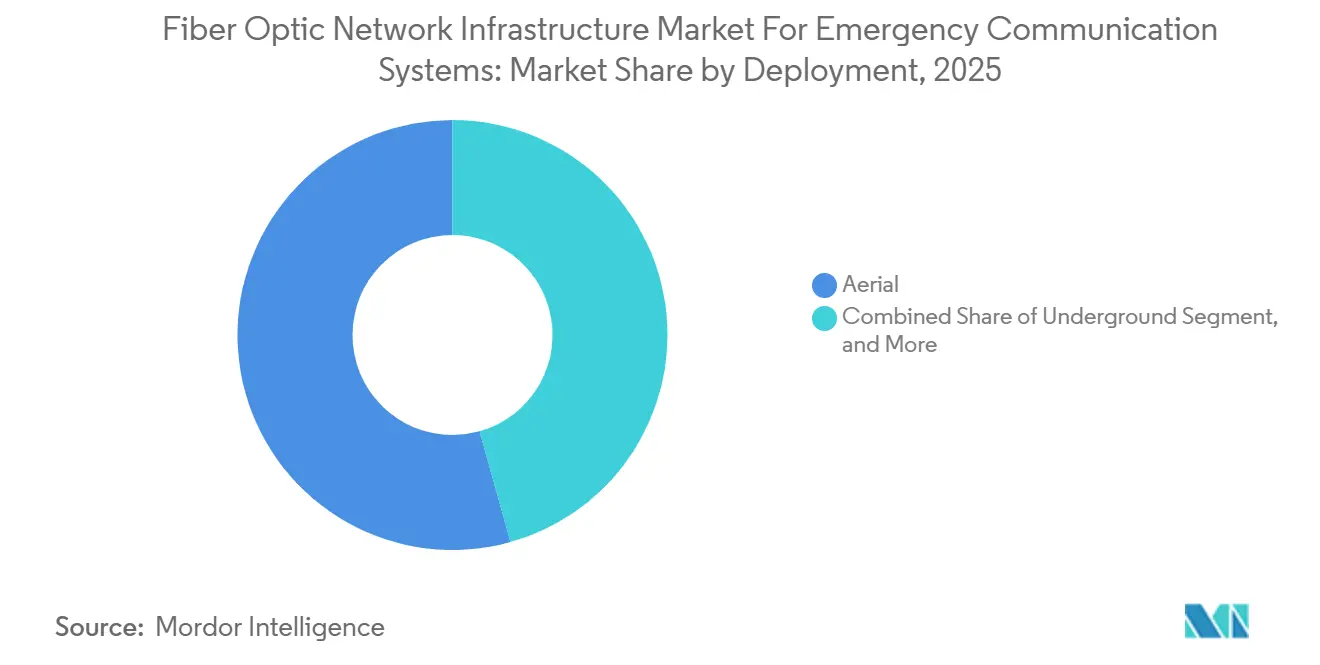

- By deployment type, aerial deployment led with 54.34% share in 2025, and underwater deployment is projected to grow at a 7.32% CAGR through 2031.

- By end user, public safety agencies held 43.50% share in 2025, and critical infrastructure operators are expected to advance at an 8.11% CAGR through 2031.

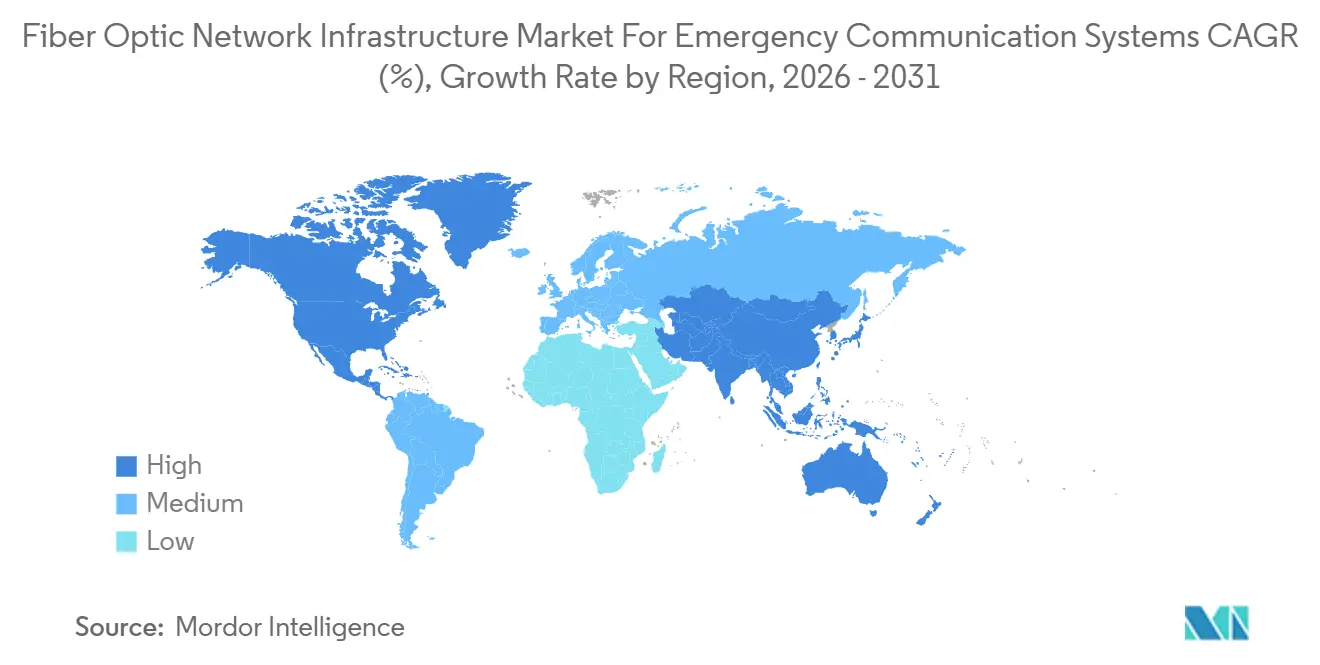

- By geography, North America captured 35.43% share in 2025, and the Asia Pacific is projected to expand at a 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Fiber Optic Network Infrastructure Market For Emergency Communication Systems

Rising Mandates for Resilient Public Safety Networks

Government mandates are translating directly into procurement activity across the fiber optic network infrastructure market for emergency communication systems. In March 2026, U.S. policymakers advanced the First Responder Network Authority Reauthorization Act, and the related agreement with AT&T added USD 2 billion to the national public safety broadband network, including USD 1 billion for new site builds, in-building coverage, and the dedicated public safety 5G core.[1]First Responder Network Authority, “Secretary Lutnick and AT&T Agree to 2 Billion Deal Benefitting First Responders, Public Safety Under FirstNet Contract,” FirstNet Germany already operates a national core transport network for public safety agencies spanning more than 9,600 km of exclusive fiber pairs, providing other governments with a working model for secure national backbones. As policy moves from broad resilience guidance to network redundancy requirements, procurement decisions are becoming less optional for public agencies. That shift is shortening decision cycles and supporting steady demand across the fiber optic network infrastructure market for emergency communication systems.

Fiber Backbone Expansion for Mission-Critical Applications

Dedicated fiber backbones for emergency use are driving sustained demand across the cable, optical transport, and control layers of the fiber optic network infrastructure market for emergency communication systems. The FirstNet Authority and AT&T announced in February 2024 that they planned to invest more than USD 8 billion over 10 years to move the network to 5G, a step that relies on dense fiber fronthaul and backhaul.[2]Congressional Research Service, “First Responder Network Authority Reauthorization and Selected Issues,” Congress In December 2025, NTT East Japan demonstrated automatic optical transmission-layer control that could reroute optical wavelength paths in under 10 minutes during major disasters, raising the service restoration benchmark for this category.[3]East Nippon Telegraph and Telephone Company, “World’s First Successful Demonstration of Automatic Optical Transmission Layer Control for Rapid Path Switching During Major Disasters,” NTT East Japan The current demand for single-mode fiber reflects its fit with long-reach, high-bandwidth backbone requirements that agencies expect to keep in service for many years. Commercial fiber buildouts in broadband, utilities, and smart grid projects are also expanding conduit and easement access for emergency networks to later share, lowering the incremental cost of dedicated circuits.

5G Fronthaul, Backhaul, And Edge Computing Integration

Public safety 5G expansion is increasing fiber consumption because each new small cell or edge location requires a reliable transport layer in the fiber optic network infrastructure for emergency communication systems. Research published in 2026 confirmed that optical transport network (OTN) multiplexing supports the deterministic latency and low jitter required for mission-critical 5G fronthaul, reinforcing fiber over OTN as the preferred architecture. Verizon launched its Frontline Network Slice coast to coast in 2025, and that service depends on fiber-dense metro infrastructure to support priority communications for first responders. Deutsche Telekom also demonstrated an interface in 2025 that linked MCx communications with TETRA digital radio over 5G, showing how fiber remains central even as radio access evolves.[4]Deutsche Telekom, “Telekom Unifies 5G and Emergency Services Radio with T Mission,” Deutsche Telekom As agencies add video, data, and mission-critical voice to the same transport environment, fiber is becoming the fixed layer that supports changing access technologies.

Smart City Emergency Command Infrastructure Growth

Municipal smart city programs are creating direct demand for command-and-control fiber networks in the fiber optic network infrastructure market for emergency communication systems. Japan’s Ministry of Internal Affairs and Communications earmarked JPY 123.4 billion (USD 865 million) in its FY2025 supplementary budget for next-generation all-optical network research and early implementation, which reflects state support for optical infrastructure in high-priority services SOUMU.GO.JP. City emergency command networks usually require ring designs and N+1 redundancy, so cable use per site rises beyond what point-to-point layouts would require. That design choice supports specialty fiber demand by enabling long buildout cycles, especially where surveillance, public address, and command applications converge onto a single backbone. The result is a steady expansion path for the fiber optic network infrastructure market for emergency communication systems in urban public safety programs and other state-backed digital infrastructure projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Civil Works and Rights-of-Way Costs | -1.4% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Legacy Emergency Systems and Integration Challenges | -0.9% | Global, concentrated in developed markets with aging infrastructure | Medium term (2-4 years) |

| Cybersecurity and Interoperability Risks | -0.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Skilled Installation, Testing, and Maintenance Shortage | -0.6% | Global, acute in South America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Civil Works And Rights-Of-Way Costs

Civil works remain the strongest practical restraint on deployment speed in the fiber optic network infrastructure market for emergency communication systems. The Fiber Broadband Association’s 2025 annual cost study found that median underground deployment reached USD 18.00 per foot, aerial deployment rose to USD 8.00 per foot, and labor accounted for 72% of underground deployment expenses. The same study found that permitting delays extended project timelines by 20% in 2025, with some projects delayed by up to 18 months. Emergency-grade designs often require physically separate redundant routes, which raises both easement costs and exposure to permit bottlenecks. The FCC moved to improve pole attachment timelines in 2025, but that mainly benefits aerial projects and does not address the higher cost burden in dense urban underground builds. Budget pressure is therefore likely to remain a drag on the fiber optic network infrastructure market for emergency communication systems, even as core demand stays intact.

Legacy Emergency Systems and Integration Challenges

Legacy TETRA, P25, and analog radio systems are slowing transition programs across the fiber optic network infrastructure market for emergency communication systems. These systems still carry active life-safety traffic, so agencies cannot interrupt them during cutover and often need long parallel operating periods. That raises program cost and extends implementation schedules, especially in mature markets with large installed bases. Many agencies also need middleware or gateway layers because older platforms do not connect cleanly with fiber-native and IP-based architectures. As a result, phased migration on existing conduit is often more practical than full replacement, even though it slows modernization in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Software Intelligence Closes The Hardware Lead

Hardware accounted for 58.54% of the fiber optic network infrastructure market for emergency communication systems in 2025, as physical deployment still drives most capital spending. Agencies needed fiber-optic cables, amplifiers, multiplexers, optical line terminals, and other core nodes to connect dispatch centers, substations, and field locations. That lead reflected the high cost of extending fixed networks over wide service territories rather than a lack of software demand. In many mature programs, the first priority remained physical expansion to remote and underserved public safety locations.

This pattern also showed that agencies were moving from earlier planning stages into multi-year construction programs across the fiber optic network infrastructure market for emergency communication systems. Services became more important inside these contracts because vendors increasingly bundled deployment, integration, and lifecycle support with equipment supply. Software is projected to grow at a 8.13% CAGR through 2031 as more value shifts toward network orchestration, fault prediction, and encryption management. Compliance-driven NG9-1-1 upgrades are also widening demand for applications that sit above the transport layer, which gives software a faster growth path than hardware even though hardware remains the larger base.

By Fiber And Cable Type: Single-Mode Dominance Meets Plastic Optical Fiber Niche Growth

Single-mode fiber commanded 62.69% share in 2025 because it fit the long-haul and high-bandwidth needs that define the fiber optic network infrastructure market for emergency communication systems. It remains the preferred option for backbone links between major command centers, hospitals, relay nodes, and other critical facilities. Its low attenuation and high data-rate ceiling also align with procurement cycles that assume long service lives. Multi-mode fiber kept its role in short-reach environments such as emergency operations centers and public safety answering points, where distances are limited.

Plastic optical fiber is projected to expand at a 7.65% CAGR through 2031 because it serves a different installation need inside the fiber optic network infrastructure market for emergency communication systems. It is well-suited to in-building systems, fire stations, and vehicle-mounted communication rigs where flexibility and installation speed matter more than maximum bandwidth. Its larger core diameter also handles tighter bends more easily than glass fiber in complex building layouts. Germany’s VDE Leitlinie 0800-730, which took effect in February 2026, established a uniform national framework for fiber installations in safety-critical buildings and removed an adoption barrier for such uses.

By Deployment Type: Aerial Coverage Leads While Underwater Routes Add Resilience

Aerial deployment held a 54.34% share in 2025 because it offered the lowest-cost, fastest route to broad network coverage in the fiber optic network infrastructure market for emergency communication systems. The input showed a median aerial deployment cost of USD 8.00 per foot, compared with USD 18.00 per foot for underground builds, which explains its strong role in rural and suburban expansions. Existing utility poles also shortened construction time where public safety networks needed a large geographic reach. Underground deployment remained important in urban systems where storm exposure, planning requirements, and resilience goals favored buried infrastructure.

Underwater deployment is expected to grow at a 7.32% CAGR through 2031, as coastal and disaster-prone cities increasingly need physically diverse paths within the fiber optic network infrastructure market for emergency communication systems. The FCC’s disaster reporting rules have raised the bar for hardened routes that can remain functional during major disruptions. Japan’s resilience planning also identified submarine cable development as a priority for maintaining communications when terrestrial links fail. NTT East Japan’s under-10-minute optical rerouting demonstration added weight to that need because diverse route options make rapid rerouting materially more effective. This made underwater routes a smaller but strategically important growth pocket in the fiber optic network infrastructure market for emergency communication systems.

By End User: Public Safety Agencies Lead While Critical Infrastructure Scales Faster

Public safety agencies accounted for 43.50% share in 2025 because they remained the main institutional buyers in the fiber optic network infrastructure market for emergency communication systems. Police, fire, emergency medical services, and public safety answering points require extremely high uptime and therefore need ring topology, path diversity, and automatic protection switching. Those design standards raise fiber use per connected location and support steady long-term replacement cycles. Enterprises also represent a meaningful customer base as campus emergency systems and continuity networks move toward higher reliability standards.

Critical infrastructure operators are projected to grow at a 8.11% CAGR through 2031, making them the fastest-scaling end-user group in the fiber optic network infrastructure market for emergency communication systems. Regulatory pressure on utilities, transport systems, water assets, and financial facilities is increasing demand for hardened communication backbones. Motorola Solutions and Nokia announced in September 2025 that they were developing a containerized tactical communications network for U.K. defense agencies, combining deployable TETRA infrastructure with Nokia’s 5G AirScale radio and optical transport. Japan’s National Institute of Information and Communications Technology also began collaborative development tied to NerveNet in April 2026 to help municipal agencies maintain secure communications during disruptions. These examples show that defense and infrastructure users are raising specification levels beyond the civilian baseline, which supports faster expansion in this part of the market.

Geography Analysis

North America held 35.43% of the fiber optic network infrastructure market for emergency communication systems in 2025, making it the largest regional base. The United States led this position through the FirstNet program, which remains the largest dedicated public safety broadband effort in the market. In March 2026, FirstNet and AT&T added USD 2 billion in value to the network program, including USD 1 billion tied to new site builds, in-building coverage, and the dedicated public safety 5G core. Canada also provided a practical model through the Ontario pilot, demonstrating that a fiber-based commercial mobile core could meet public-safety quality-of-service requirements.

Europe remained a mature yet still active part of the fiber optic network infrastructure market for emergency communication systems. Germany, the United Kingdom, France, and Scandinavia continued to lead emergency fiber deployment, while Southern and Eastern European markets stayed in earlier buildout stages. The U.K. Emergency Services Network continued to support optical transport demand, and Motorola Solutions and Nokia’s 2025 tactical communications collaboration for U.K. defense agencies demonstrated how TETRA, 5G, and fiber are integrated into a single architecture. BEREC’s 2025 civil works coordination guidelines under the Gigabit Infrastructure Act also supported lower deployment friction across member states.

Asia Pacific is projected to expand at a 7.98% CAGR through 2031, which gives it the fastest growth path in the fiber optic network infrastructure market for emergency communication systems. The region is seeing active public safety digitization in India, China, Australia, Japan, and South Korea, supported by both national programs and local network upgrades. Japan backed this direction through JPY 123.4 billion (USD 865 million) in FY2025 supplementary budget support for next-generation all-optical network development and early implementation. Australia also showed private-sector network investment momentum when Vocus announced an AUD 500 million (USD 344.5 million) ducted long-haul fiber route between Sydney and Melbourne with emergency communications identified as a core use case. South America and the Middle East and Africa remained earlier-stage regions, yet the urgency around resilient state communications was rising, which points to a larger future role in the fiber optic network infrastructure for emergency communication systems market.

Competitive Landscape

The fiber optic network infrastructure market for emergency communication systems is moderately concentrated, with a leading group of suppliers active in cable, optical transport equipment, and network systems. Motorola Solutions, Inc., Honeywell International Inc., Siemens AG, Johnson Controls International plc, and Eaton Corporation plc formed the main hardware layer, while Everbridge and BlackBerry competed more directly in emergency communication software and application integration. This split is still useful, but the boundary is narrowing as buyers increasingly prefer integrated solutions over separate point products. The fiber optic network infrastructure market for emergency communication systems is therefore moving toward bundled offers that combine transport, management, analytics, and support services in one contract structure.

Strategic moves in 2025 and 2026 showed that suppliers were seeking to expand their roles within the fiber optic network infrastructure market for emergency communication systems. Prysmian entered a long-term production partnership with Relativity Networks in March 2025 for hollow-core optical fiber and cable, a move aimed at ultra-low-latency use cases with premium technical requirements. Motorola Solutions and Nokia also announced a next-generation containerized tactical communications network for U.K. defense agencies in September 2025, which combined deployable radio infrastructure with optical backhaul. Nokia separately partnered with Leonardo in 2025 to deliver mission-critical private wireless networks for public safety and critical infrastructures, reinforcing the move toward broader platform offerings around secure connectivity. These actions showed that vendors were competing on integration depth as much as on standalone hardware performance.

Open space remains strongest in areas where the fiber optic network infrastructure market for emergency communication systems still lacks many full-stack providers. Underwater deployment is one example because few suppliers combine subsea installation, hardened connectors, and emergency-grade redundancy in one offer. Compliance capability is also becoming a competitive factor as agencies place more value on network architectures that support resilience reporting and rapid restoration. Vendors that can connect optical transport, NG9-1-1 functions, and tactical or temporary field deployment are better placed to win multi-layer projects. This keeps competition active even though the leading names still carry clear weight across the fiber optic network infrastructure market for emergency communication systems.

Leaders of Fiber Optic Network Infrastructure Market For Emergency Communication Systems

Motorola Solutions, Inc.

Honeywell International Inc.

Siemens AG

Johnson Controls International plc

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Comtech Telecommunications Corp. introduced Allerium Coral, a network-native NG9-1-1 capability extending Emergency Services IP Networks beyond transport to support secure, standards-based information coordination across the public safety ecosystem, including first responders, healthcare providers, and dispatch centers, advancing the fiber-layer NG9-1-1 software market.

- March 2026: The U.S. NTIA and AT&T secured an additional USD 2 billion in value for the FirstNet Nationwide Public Safety Broadband Network, approximately USD 1 billion in cost savings reallocated to network investment, and approximately USD 1 billion in new network and coverage enhancements guided by public safety users, including accelerated build-out of the Dedicated Public Safety 5G Core.

- September 2025: Motorola Solutions and Nokia announced a strategic collaboration to deliver a next-generation containerized tactical communications network for U.K. defense agencies, combining Motorola Solutions' deployable TETRA infrastructure with Nokia's 5G AirScale radio portfolio, an integration requiring dedicated optical backhaul.

Scope of Report on Fiber Optic Network Infrastructure Market For Emergency Communication Systems

The Fiber Optic Network Infrastructure Market for Emergency Communication Systems Report is Segmented by Component (Hardware, Software, and Services), Fiber and Cable Type (Single-Mode Fiber, Multi-Mode Fiber, and Plastic Optical Fiber), Deployment (Underground, Aerial, and Underwater), End User (Public Safety Agencies, Critical Infrastructure Operators, Enterprises, Military and Defense, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Single-Mode Fiber |

| Multi-Mode Fiber |

| Plastic Optical Fiber |

| Underground |

| Aerial |

| Underwater |

| Public Safety Agencies |

| Critical Infrastructure Operators |

| Enterprises |

| Military and Defense |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Fiber and Cable Type | Single-Mode Fiber | ||

| Multi-Mode Fiber | |||

| Plastic Optical Fiber | |||

| By Deployment Type | Underground | ||

| Aerial | |||

| Underwater | |||

| By End User | Public Safety Agencies | ||

| Critical Infrastructure Operators | |||

| Enterprises | |||

| Military and Defense | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and forecast for fiber optic network infrastructure market for emergency communication systems?

The sector stood at USD 4.15 billion in 2025, is at USD 4.49 billion in 2026, and is projected to reach USD 6.57 billion by 2031 at a 7.91% CAGR.

Which component category leads demand today?

Hardware leads with 58.54% share in 2025 because most spending still goes into cables, optical transport equipment, and physical network nodes.

Which component is expanding the fastest through 2031?

Software is growing the fastest at an 8.13% CAGR as agencies add network management, fault prediction, and secure communications applications on top of the fiber backbone.

Why is single-mode fiber dominant in emergency communications?

Single-mode fiber held 62.69% share in 2025 because it supports long reach, high bandwidth, and long service life requirements for backbone links between critical locations.

Which deployment model is seeing the strongest long-term growth?

Underwater deployment is projected to grow at a 7.32% CAGR as coastal and disaster-prone areas add diverse routes that can keep traffic moving when terrestrial links fail.

Which regions are setting the pace for adoption?

North America led with 35.43% share in 2025 because of FirstNet, while the Asia Pacific is growing the fastest at a 7.98% CAGR through 2031 as public safety digitization programs expand.

Page last updated on: