Size and Share of Fiber Optic Market For Defense and Battlefield Communication Networks

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

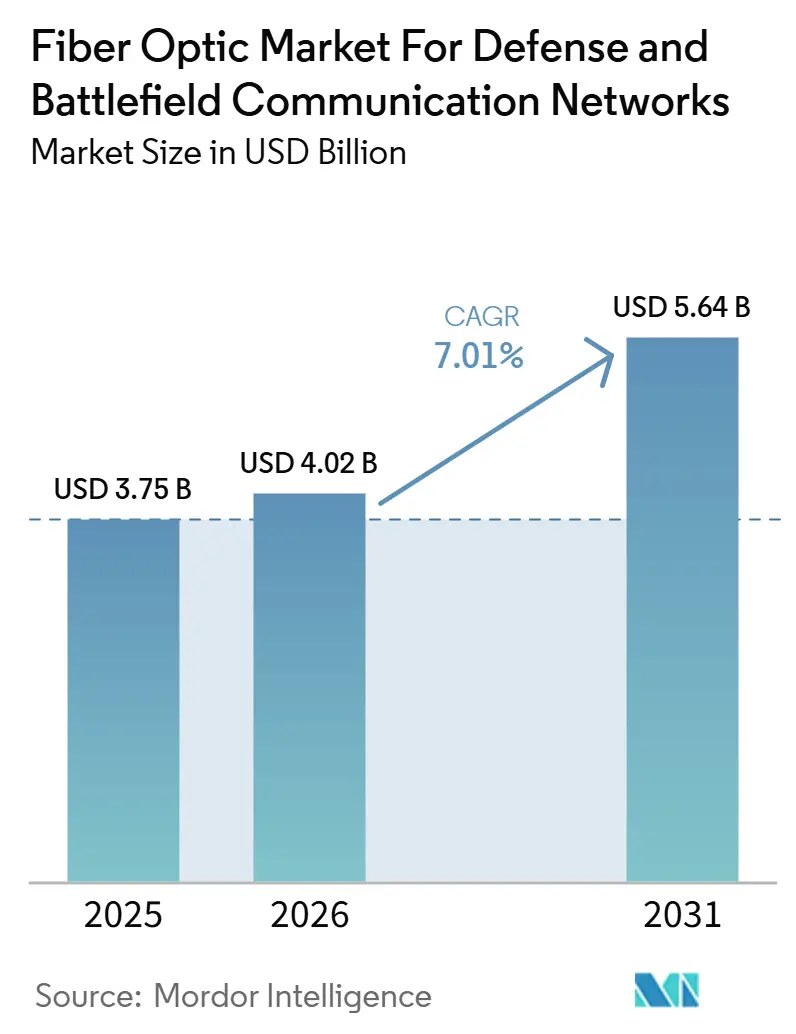

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

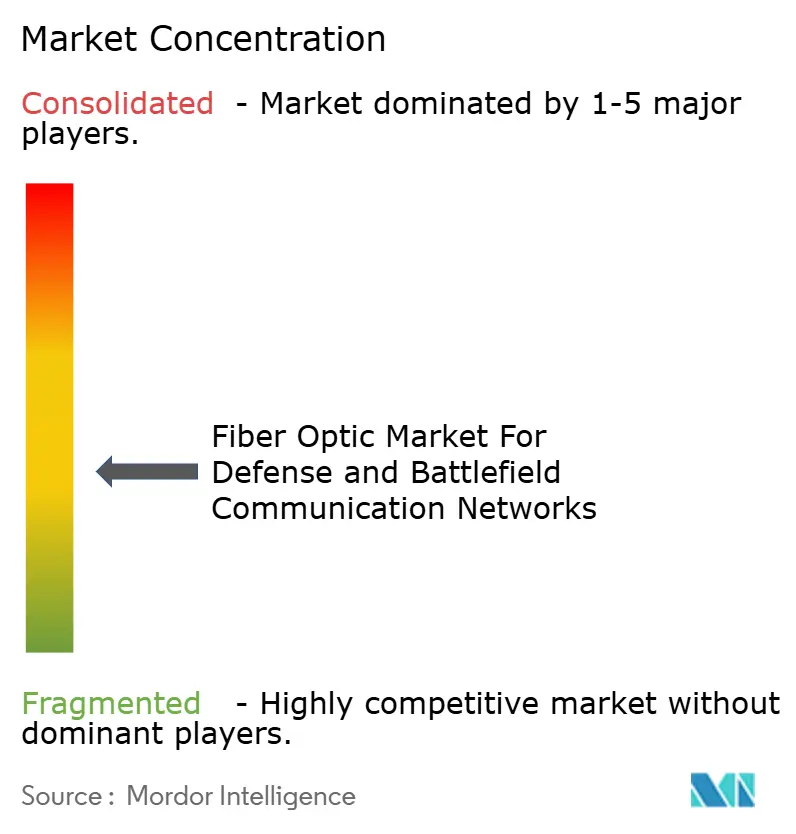

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Fiber Optic Market For Defense and Battlefield Communication Networks by Mordor Intelligence

The fiber optic market for defense and battlefield communication networks is expected to increase from USD 3.75 billion in 2025 to USD 4.02 billion in 2026 and reach USD 5.64 billion by 2031, growing at a CAGR of 7.01% over 2026-2031. Demand is rising because military networks now need secure, high-capacity links that can handle AI-enabled operations, edge computing, and multi-domain command structures without the performance limits of legacy copper systems. The shift is also tied to how armed forces are rebuilding transport layers for network-centric warfare, where data integrity, low latency, and electromagnetic resilience matter across fixed sites, mobile platforms, and forward positions. Procurement decisions are increasingly shaped by a two-layer competitive structure, where qualified cable and component makers compete on ruggedization and certification, while systems integrators compete on program execution and platform-level delivery. Supply chain concentration in specialty materials and limited field repair capacity still slow adoption in some programs, especially where ruggedized assemblies and trained splicing personnel are difficult to scale. Even with those constraints, the fiber optic market for defense and battlefield communication networks continues to gain ground because secure optical infrastructure is difficult to replace in contested operating environments.

Key Report Takeaways

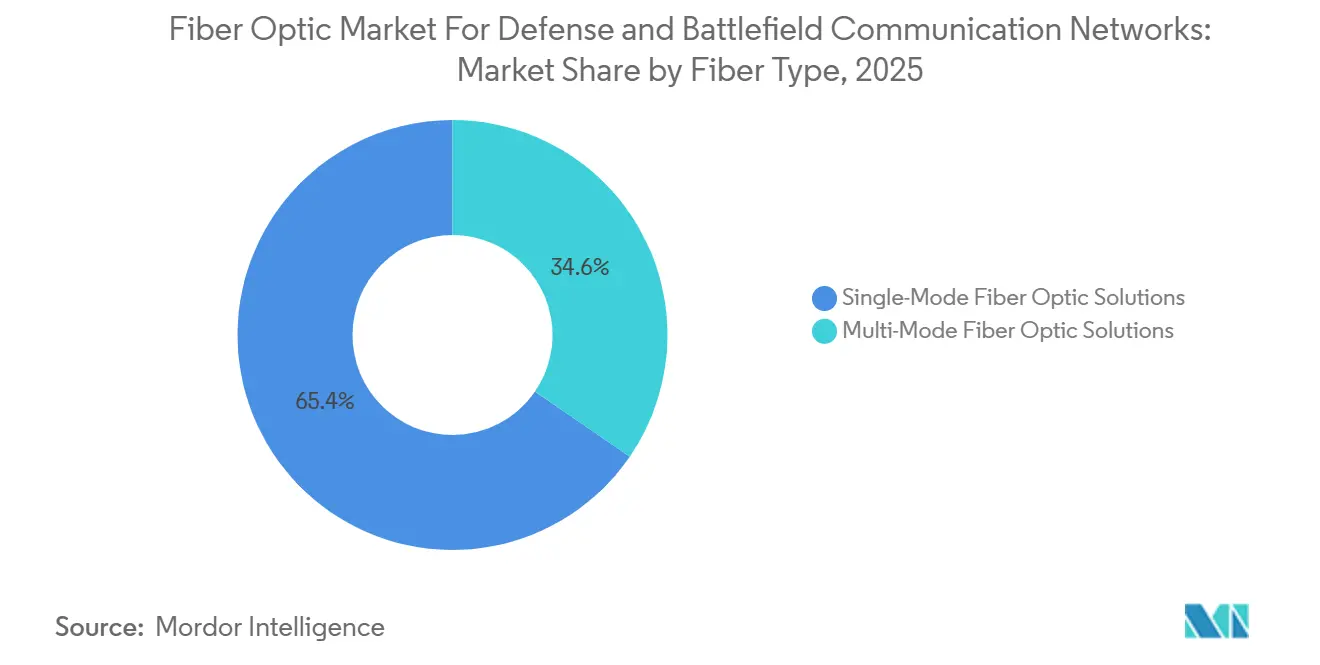

- By fiber type, single-mode solutions held 65.43% share of the fiber optic market for defense and battlefield communication networks in 2025, while multi-mode solutions are projected to expand at a 7.34% CAGR through 2031.

- By product architecture, armored fiber optic cables accounted for 54.67% of the market share in 2025, while tactical field fiber assemblies are expected to grow at a 7.12% CAGR through 2031.

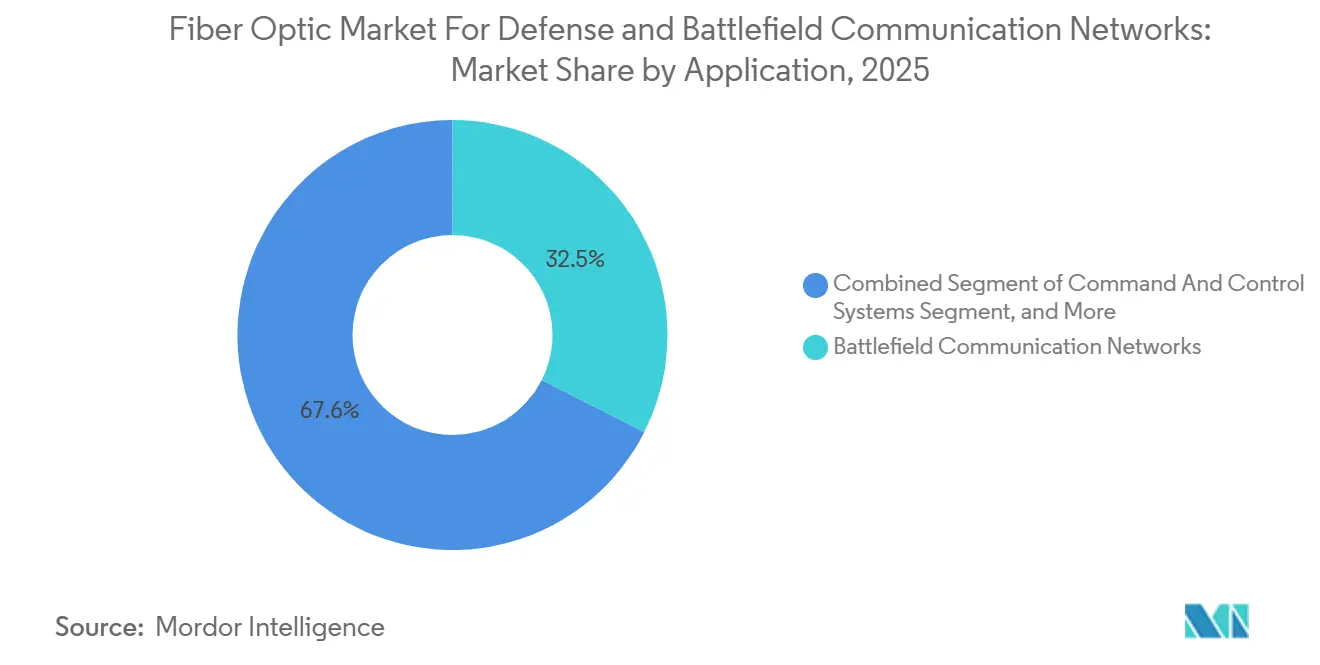

- By application, battlefield communication networks captured 32.45% share in 2025, while ISR networks are projected to advance at a 7.87% CAGR through 2031.

- By platform, land platforms held 37.89% share in 2025, while space-enabled defense networks are expected to expand at an 8.12% CAGR through 2031.

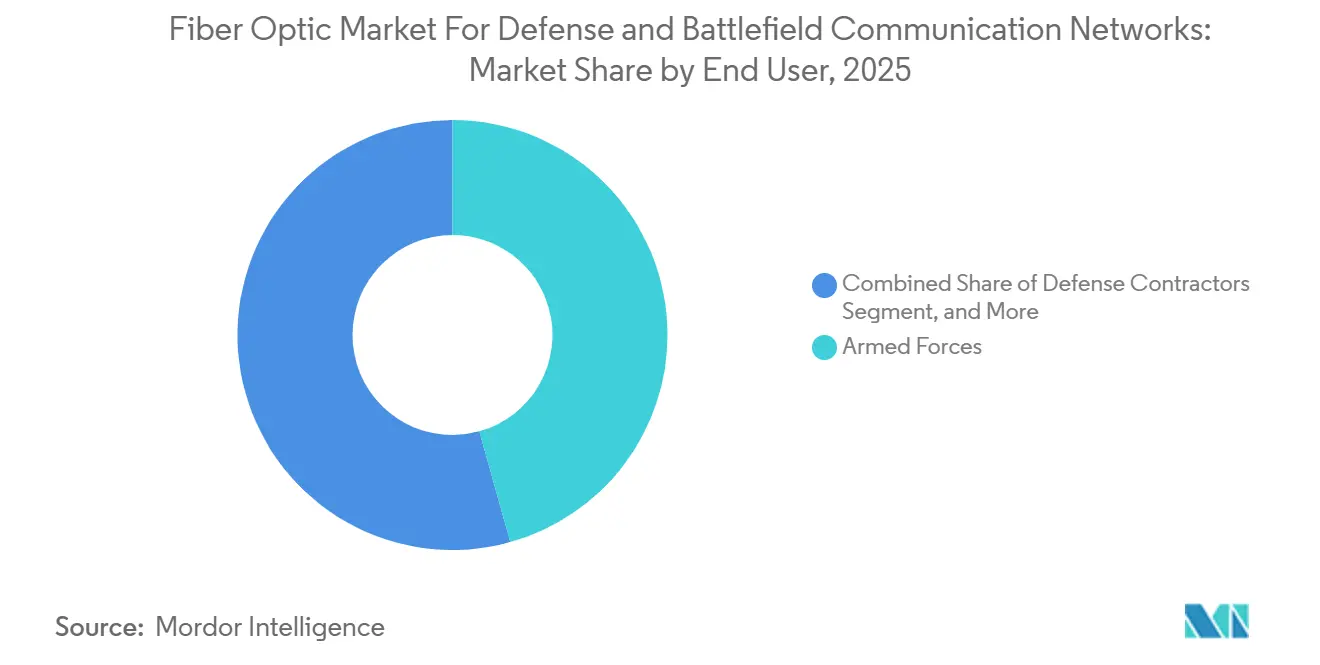

- By end user, armed forces accounted for 45.67% share in 2025, while defense contractors are projected to grow at an 8.34% CAGR through 2031.

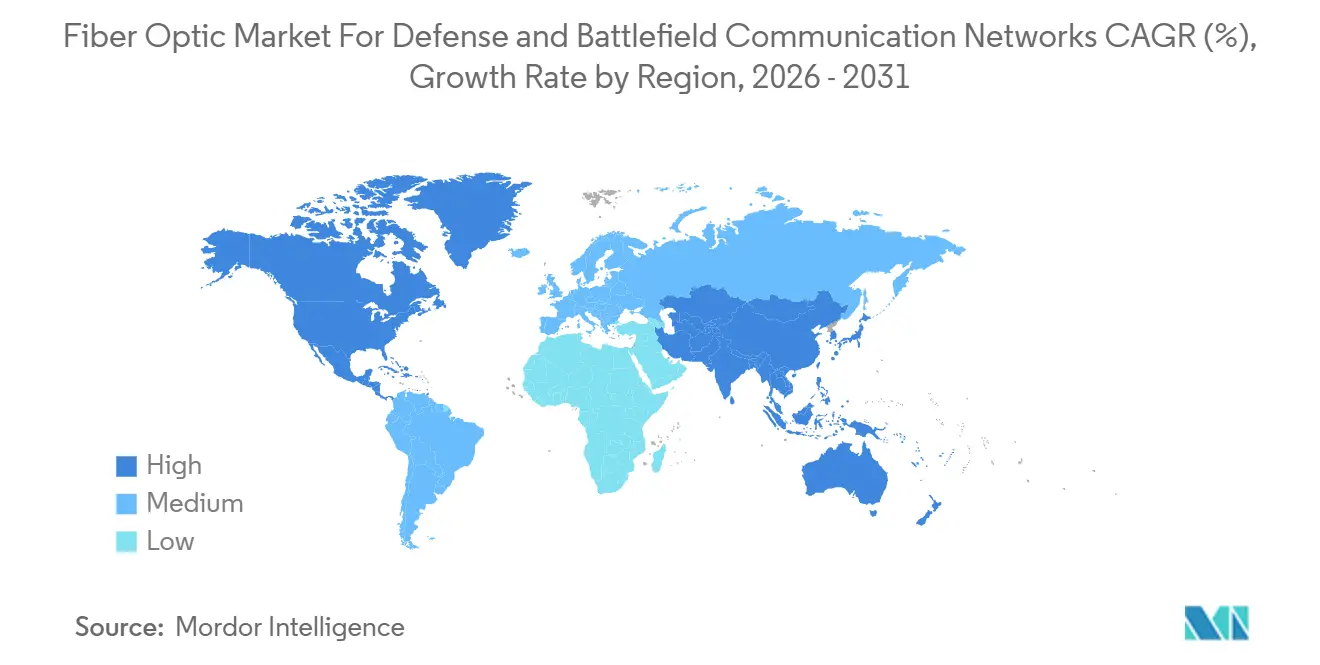

- By geography, North America held a 36.78% share of the fiber optic market for defense and battlefield communication networks in 2025, while Asia-Pacific is expected to expand at an 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Fiber Optic Market For Defense and Battlefield Communication Networks

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Secure, Low-Latency Defense Communication | +2.1% | Global | Short term (≤ 2 years) |

| Modernization of C4ISR Backbone Infrastructure | +1.7% | North America and Europe | Medium term (2-4 years) |

| Electromagnetic Interference Immunity Over Copper and RF | +1.3% | Global, with Asia-Pacific and Middle East and Africa as primary theaters | Short term (≤ 2 years) |

| Higher Data Throughput for Sensor-Heavy Platforms | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growth in Tactical Networks for Multi-Domain Operations | +0.7% | Global, with spillover across all regions | Long term (≥ 4 years) |

| Adoption of Ruggedized Fiber for Harsh Operating Environments | +0.5% | Middle East and Africa, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Secure, Low-Latency Communication in Defense Networks

Secure optical transport is becoming a core requirement because command systems now depend on faster and cleaner data movement across contested operating areas. The fiber optic market for defense and battlefield communication networks benefits from this shift because encrypted transport, low latency, and physical layer monitoring are now treated as mission requirements rather than optional upgrades. Modern fiber systems can carry multiple encrypted data streams on a single strand through dense wavelength division multiplexing, and distributed sensing features can also help detect physical interference on the line. The Indo-Pacific transport buildout described in the source material also shows that strategic geography is driving backbone procurement, not just routine network refresh cycles.[1]Scott Barnett, “The Pentagon's Fiber Future, How DoD Networks Race to Meet New Demands,” Breaking Defense This matters because sensor-to-shooter loops demand stricter latency performance than standard enterprise traffic, so military programs need hardened physical layers that commercial specifications do not fully address. That gap keeps the fiber optic market for defense and battlefield communication networks tied to a distinct procurement channel with higher entry barriers and longer qualification cycles.

Modernization of C4ISR Backbone Infrastructure

C4ISR modernization is a strong demand driver because legacy tactical architectures were not built for the volume and speed of current military data exchange. The U.S. Army's FY2027 request for Next Generation Command and Control and the C2NOW program marks a clear move away from legacy WIN-T structures that relied more heavily on copper and satellite backhaul. In the source material, this program is important because optical distribution is being designed into the transport layer from the beginning rather than added later as a workaround. The fiber optic market for defense and battlefield communication networks is also supported by broader compliance requirements, as physical transmission pathways now face tighter scrutiny under cybersecurity and supply assurance standards. That expands the addressable space for certified assemblies, connectors, and cable systems beyond older program-of-record lists. It also favors suppliers that can combine qualification depth with long production consistency over multiple program years.

Electromagnetic Interference Immunity in Contested Environments

Electromagnetic resilience remains one of the clearest technical reasons for choosing fiber over copper and radio-frequency links in military systems. Fiber-optic links are inherently resistant to electromagnetic pulse effects and jamming, which is why they are increasingly used for intra-platform wiring on armored, naval, and airborne systems. Research published in Photonics in 2025 showed that multi-core fiber architectures for microwave photonic links achieved 27 dB suppression of third-order intermodulation distortion and a noise floor of -167 dBm/Hz at 5 MHz, supporting cleaner signal fidelity under heavy interference conditions.[2]Jian Li, “High-Fidelity Long-Haul Microwave Photonic Links With Composite OPLLs and Multi-Core Fiber for Secure Command and Control Systems in Contested Environments,” Photonics The battlefield relevance is broader than a single platform type, as the same immunity applies to command links, radar transport, electronic warfare synchronization, and tethered unmanned systems. The source material also connects this trend to the use of fiber-optic drones and tactical tethers, where radio-frequency dependence creates a visible vulnerability in contested environments. That gives the fiber optic market for defense and battlefield communication networks a structural advantage that commercial telecom demand drivers cannot replicate.

Higher Data Throughput for Sensor-Heavy Defense Platforms

Modern military platforms now carry radar, lidar, electronic intelligence, hyperspectral imaging, and other sensor loads, creating sustained pressure on transport capacity. The U.S. Air Force award tied to the ABMS Digital Infrastructure Network Developer program explicitly included scalable and resilient optical transport networks for cross-domain data distribution across fixed, mobile, and edge environments. That matters because the throughput problem is not limited to backbone routes; it also affects tactical nodes, remote systems, and platform interiors where sensor fusion has become standard. L3Harris expanded fiber-pack winder capacity through 2025 and 2026 to support unmanned surface and underwater vehicle programs, demonstrating how high-bandwidth tethered operations are moving from niche demand into a repeatable program base.[3]L3Harris Technologies, “Unjammable Lifeline, L3Harris Fiber-Optic Tethers Keep Warfighters Connected,” L3Harris Newsroom The fiber optic market for defense and battlefield communication networks benefits because these payload-heavy systems need dependable capacity with low latency and reduced interception risk. The result is a stronger pull for optical transport that can still function under degraded operational conditions, which is a standard that commercial systems are not designed to meet.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Ruggedization, Qualification, and Lifecycle Costs | -0.9% | North America and Europe, with the highest qualification bar | Long term (≥ 4 years) |

| Field Repair Complexity and Skilled Technician Dependency | -0.5% | Global, especially remote theaters in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Vulnerability of Supply Chains for Specialty Components | -0.3% | Global, concentrated in U.S.-China sourcing channels | Medium term (2-4 years) |

| Procurement Cycles Tied to Defense Budget Cycles | -0.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Ruggedization, Qualification, and Lifecycle Costs

Qualification and lifecycle costs remain significant constraints because defense-grade fiber assemblies must meet stricter environmental and performance standards than commercial cable systems. The source material notes that MIL-STD-810H qualification can take 12 to 24 months and can cost several million dollars per cable configuration, which limits how many suppliers can enter or stay active in approved defense channels. That cost burden persists after initial approval because changes to materials or manufacturing methods can trigger another validation round. The practical effect is that buyers often stick with already-qualified vendors, even when wider competition could lower costs or shorten lead times. The fiber optic market for defense and battlefield communication networks, therefore, grows within a supply structure where technical approval is slow and where pricing remains elevated for long-service platforms. This also explains why the market remains only moderately consolidated rather than fully open, since qualification depth carries as much weight as manufacturing scale.

Field Repair Complexity and Skilled Technician Dependency

Field repair is another restraint because military-grade fiber cannot be serviced as easily as copper in harsh or time-sensitive operating conditions. Fusion splicing in the field demands specialized tools, controlled handling, and trained personnel, and those requirements are not evenly distributed across military units or coalition partners. The problem becomes more serious in airborne and naval platforms where access to cable runs often requires partial disassembly and more time than field crews can spare. Tactical field assemblies with pre-terminated ruggedized connectors help reduce this issue, which supports their projected 7.12% growth path through 2031, but they do not solve the maintenance burden for the installed base. That means the armed forces still have to sustain both older and newer wiring architectures simultaneously, which increases complexity across procurement, training, and maintenance planning. The fiber optic market for defense and battlefield communication networks, therefore, expands with a clear technical case, but not every program can absorb the operational burden at the same pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Single-Mode Solutions Anchor Long-Haul Links, Multi-Mode Gains in Intra-Platform Wiring

Single-mode fiber optic solutions held 65.43% share in 2025, giving them the largest position in this part of the fiber optic market for defense and battlefield communication networks. That lead reflects the long-haul requirements of base-to-base backbone links, shipboard trunk routes, and command node interconnects where attenuation over distance remains a core performance factor. The installed base also matters because NATO-aligned military optical standards have historically leaned toward single-mode specifications, which keeps replacement and upgrade demand tied to existing technical choices. This installed base effect makes single-mode demand more durable than a simple cost comparison would suggest. It also helps explain why buyers continue to prioritize compatibility, qualification history, and long-term reliability when they update core network transport layers.

Multi-mode solutions are projected to grow at a 7.34% CAGR from 2026 to 2031, making them the fastest-growing sub-segment within fiber type. Their role is strongest in short-reach intra-platform wiring for armored vehicles, naval combat systems, and radar environments where distance limits are manageable, and bandwidth needs remain high. Research published in IEEE in 2025 described hybrid fiber-RF communication protocols for anti-jamming resilience in unmanned aerial vehicle systems, showing how fiber can take over critical command paths while redundant RF links preserve broader awareness. That architecture expands the case for multi-mode fiber beyond fixed platforms and into airborne and robotic systems that previously relied more heavily on radio-frequency or copper harnesses. As military standards evolve to accommodate more short-reach optical use cases, multi-mode adoption is gaining institutional support rather than depending only on commercial preference. This mix means the fiber optic market for defense and battlefield communication networks keeps its single-mode base while opening new room for faster-growing intra-platform use cases.

By Product Architecture: Armored Cables Lead the Installed Base, Tactical Assemblies Accelerate at the Edge

Armored fiber optic cables accounted for 54.67% share in 2025, so they remain the dominant product architecture across the installed defense base. Their position is tied to the harsh environments that define defense transport, including tracked vehicles, shipboard cable trays, underground hardened sites, and exposed tactical routes where crush, heat, abrasion, and fragment risk are all real design concerns. This makes armored products a significant part of the fiber optic market for defense and battlefield communication networks at the product level, because survivability requirements raise both unit value and qualification requirements. Their pricing premium is also reinforced by the fact that qualified domestic suppliers with military certification are fewer in number than in commercial cable markets. That combination of rugged use conditions and constrained qualified supply keeps armored cables central to both current deployments and future replacement cycles.

Tactical field fiber assemblies are expected to grow at a 7.12% CAGR through 2031, making them the fastest-growing product architecture sub-segment. Their growth profile is different from armored cable demand because they serve the battlefield edge, where rapid connectorization, lower weight, and easier field replacement matter more than long-haul attenuation. The source material also notes that connectors, splices, and terminations form a third product group that is increasingly specified under military connector standards for dense patching and fixed high-capacity environments. This signals a wider move toward pre-terminated and factory-qualified assembly solutions that shift installation risk away from the field and into controlled production settings. That trend matters because it reduces technician dependency, shortens deployment time, and fits with procurement offices that want predictable installation outcomes across distributed programs. As a result, the fiber optic market for defense and battlefield communication networks is gradually shifting toward assembly formats that balance ruggedness with simpler deployment at the tactical edge.

By Application: Battlefield Networks Lead Volume, ISR Demand Shifts the Mix Toward High-Bandwidth Solutions

Battlefield communication networks captured a 32.45% share in 2025, giving them the largest market position. Their lead reflects the central role they play in linking command posts, artillery, logistics nodes, and forward sensors into a usable operational picture. This part of the fiber optic market for defense and battlefield communication networks is sustained by the fact that these networks serve as the foundation for almost every other mission system. Command and control systems follow closely because they need dependable physical transport for cross-service data distribution that older, incompatible network structures could not support at the same scale. Radar, surveillance, and electronic warfare applications also deepen demand, as they require accurate timing and cleaner signal transport over distances where copper loses effectiveness.

ISR networks are projected to expand at a 7.87% CAGR from 2026 to 2031, making them the fastest-growing application area. That growth is tied to the wider rise of sensor-rich multi-domain operations, where persistent collection and rapid data movement are becoming routine rather than exceptional. The application mix is therefore shifting toward higher-bandwidth optical solutions that can support large sensor loads across land, air, maritime, and subsurface missions. In practical terms, ISR demand also pulls more premium single-mode fiber, ruggedized connector systems, and higher-assurance transport standards into procurement programs that previously had narrower optical requirements. This change matters because ISR scale can be larger than many platform-specific fiber needs once networks extend across distributed sensing areas and longer surveillance routes. The fiber optic market for defense and battlefield communication networks therefore gains not only from battlefield backbone demand, but also from the expanding intensity of sensing, tracking, and data exploitation missions.

By Platform: Land Platforms Dominate the Installed Base, Space Networks Lead Growth

Land platforms held a 37.89% share in 2025, giving them the largest market position. That lead rests on the installed volume of armored fighting vehicles, mobile command posts, self-propelled artillery, and forward operating base infrastructure that still anchor conventional force structures. Intra-vehicle fiber wiring now supports battle management, crew communications, and sensor integration in a growing range of upgraded and newly built ground systems. That installed footprint gives land systems an important role in the fiber optic market for defense and battlefield communication networks, as replacements, retrofits, and subsystem upgrades continue well beyond a platform's original entry into service. Naval platforms also remain a major demand center because shipboard fiber trunk cabling supports combat management, radar, and propulsion monitoring systems that require dependable onboard transport.

Space-enabled defense networks are expected to expand at an 8.12% CAGR through 2031, making them the fastest-growing platform category. This reflects how optical connectivity is moving upward from terrestrial and shipboard systems into space-linked military architectures. The source material connects this shift to the optically interconnected low Earth orbit backbone awarded to SpaceX in 2026, and that project highlights how future military networks will depend on both free-space optical links and supporting ground-segment fiber infrastructure. Airborne platforms also absorb meaningful optical demand through avionics integration and electronic warfare wiring, although airframe weight limits keep total cable count below that of land and naval systems. Even so, the platform mix is widening because military optical communication is no longer confined to traditional fixed installations or heavy ground assets. That widening platform base strengthens the long-run outlook for the fiber optic market for defense and battlefield communication networks, even as qualification and integration demands remain high.

By End User: Armed Forces Anchor Procurement, Defense Contractors Capture the Growth Differential

Armed forces accounted for 45.67% share in 2025, making them the largest end-user group in the market. Their lead reflects direct procurement through program-of-record contracts, base infrastructure upgrades, and longer-term purchasing vehicles that support recurring network and platform requirements. This gives the armed forces the largest direct role in the fiber optic market for defense and battlefield communication networks, as they remain the final operators of the systems and the main drivers of standard-setting. Their buying pattern also tends to reinforce demand for proven suppliers, since field performance, lifecycle support, and compatibility matter more than simple component price. That keeps procurement relatively predictable where modernization programs are active, even if sourcing rules and qualification cycles slow vendor turnover.

Defense contractors are projected to grow at an 8.34% CAGR through 2031, making them the fastest-growing end-user category. The growth gap reflects the larger role contractors now play in subsystem integration, assembly, and delivery under modular and outsourced defense program structures. As defense departments push more responsibility onto specialized integrators, contractors capture a larger share of the value tied to qualified optical assemblies, connectors, and platform-level communications packages. Homeland security and border security also form a smaller end-user tier, using fiber-optic sensing and surveillance networks for perimeter monitoring and critical infrastructure protection. That smaller tier does not displace core defense demand, but it creates an additional use path that can help support qualified manufacturing capacity. The result is a market where end-user demand still starts with armed forces, while growth at the margin is moving faster through contractor-led execution models.

Geography Analysis

North America held a 36.78% share in 2025, making it the largest regional market for fiber optic market for defense and battlefield communication networks. The region's lead is tied to the scale of U.S. defense modernization and the depth of its qualified domestic supply base. The replacement of legacy tactical network structures, the expansion of submarine communication programs, and the buildout of optical transport layers across command systems all keep procurement active across multiple branches. Domestic sourcing requirements also reinforce this position because classified and high-assurance programs often favor or require approved U.S.-based manufacturing. The Indo-Pacific transport buildout described in the source material adds another layer of demand by pointing to strategic-reach infrastructure, not just platform-level integration.

Europe held the second-largest position, supported by Germany, the United Kingdom, and France, as they continue multi-year defense modernization under NATO commitments. Demand in the region is shaped by secure deployable communications, interoperability programs, and certified optical backplanes for command systems rather than only by basic cable replacement. The conflict-driven rise of battlefield fiber-optic drone tether applications has also created a distinct regional pull for ruggedized optical components and assemblies. That pattern matters because it adds newer unmanned use cases to a region already focused on deployable command, control, and secure information systems. Smaller NATO members absorb a more limited share of procurement, but alliance-funded interoperability needs still broaden the regional base.

Asia-Pacific is projected to expand at an 8.01% CAGR from 2026 to 2031, making it the fastest-growing region. Growth is tied to naval modernization in China, defense manufacturing expansion in India, higher defense allocations in Japan, and advanced platform programs in South Korea. This regional profile gives Asia-Pacific the clearest growth role in the fiber optic market for defense and battlefield communication networks outside North America because demand is rising across both procurement volume and local supply chain ambition. Middle East and Africa and South America remain smaller in absolute terms, but they still show strategic activity as countries upgrade naval communications and build indigenous defense manufacturing capability. Australia also stands out as a sub-regional demand node because it participates in qualified defense fiber programs that exceed what its overall economic size might suggest.

Competitive Landscape

The fiber optic market for defense and battlefield communication networks is moderately consolidated at the cable and fiber strand layers, where Corning Incorporated, Prysmian Group, Sumitomo Electric Industries, Nexans S.A., and OFS Fitel LLC have broad qualification depth. Competition at this layer is centered on materials capability, compliance with military specifications, and the ability to sustain domestic or allied sourcing requirements across sensitive programs. These factors matter because new entrants do not compete solely on cost; they must also demonstrate repeatable performance in rugged operating conditions and navigate lengthy approval cycles. TE Connectivity Ltd and Amphenol Corporation hold an important middle position because qualified connectors and assemblies sit between raw cable capability and final system integration. That gives them leverage in approved vendor positions that are difficult to displace once embedded in military platforms and facility standards.

The competitive dynamic changes at the systems level, where L3Harris Technologies, Thales S.A., and General Dynamics Mission Systems compete on integration record, customer access, and delivery of complete communication subsystems rather than only on components. The source material shows a broader shift toward fixed-price, multi-year framework agreements, which puts greater pressure on suppliers to automate, standardize, and manage margins carefully. Patton Electronics' June 2026 subcontract for source-secure transport modules shows how supply chain certification itself is becoming a competitive differentiator in defense optical programs. GPD Optoelectronics' USD 14.5 million STOMPeR award also points to a growing frontier in rugged optical receivers and modem technology, which expands competition beyond cable and connector manufacturing alone. This matters because future value creation is spreading across photonics, transport modules, and platform-specific optical processing as much as across traditional cable supply.

Recent strategic moves also show how suppliers are positioning for long-cycle defense demand. L3Harris expanded fiber pack winder capacity in 2025 and 2026 to support tethered unmanned programs, which reinforced its role in a fast-developing tactical niche. L3Harris also secured its largest full-rate production contract for U.S. Navy submarine communication systems in February 2026, which strengthened its position in platform-level optical communications. Ondas Holdings introduced NDAA-compliant, U.S.-made fiber-optic spools for drones and ground robotics in September 2025, showing how domestic sourcing has become part of product positioning as well as compliance.[4]Ondas Holdings, “Ondas' Apeiro Launches NDAA-Compliant Made-in-the-USA Combat-Proven Fiber-Optic Spools for Drones and Ground Robotics,” Ondas Holdings Press Release Together, these moves support a market structure where concentration is meaningful in qualified niches, but no single company appears to control the full competitive field end to end.

Leaders of Fiber Optic Market For Defense and Battlefield Communication Networks

Prysmian Group

Nexans S.A.

Corning Incorporated

OFS Fitel, LLC

Sumitomo Electric Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Thales S.A. and Leonardo S.p.A., in consortium, won a NATO contract to deliver next-generation secure deployable communication and information systems for the Allied Special Operations Forces Command, covering 6 deployable headquarters capabilities with full lifecycle support.

- June 2026: SAIC was awarded a leading position on the U.S. Air Force's USD 192 million ABMS Digital Infrastructure Network Developer contract. The technical scope explicitly includes scalable and resilient optical transport networks, software-defined wide area networking, and cloud-enabled infrastructure integration across fixed, mobile, and edge environments

- June 2026: Patton Electronics was awarded a subcontract to develop specialized, source-secure fiber optic transport modules for U.S. defense applications, built entirely from U.S.-sourced, source-verified components, as part of a broader DoD initiative to strengthen domestic capability in secure optical communications infrastructure.

- May 2026: The U.S. Space Force awarded SpaceX a USD 2.29 billion firm-fixed-price contract for the Space Data Network Backbone, a resilient, optically interconnected proliferated low Earth orbit satellite constellation delivering worldwide tactical communications. SpaceX is required to deliver a fully operational prototype capability by the end of 2027, with 13 satellites planned for acquisition in 2026 and 21 in 2027.

Scope of Report on Fiber Optic Market For Defense and Battlefield Communication Networks

The Fiber Optic Market for Defense and Battlefield Communication Networks is Segmented by Fiber Type (Single-Mode Fiber and Multi-Mode Fiber), Product Architecture (Armored Fiber Optic Cables, Tactical Field Fiber Assemblies, and Connectors, Splices, and Termination Kits), Application (Battlefield Communication Networks, Command And Control Systems, Radar And Surveillance Networks, Electronic Warfare Systems, and Intelligence, Surveillance, and Reconnaissance Networks), Platform (Land Platforms, Naval Platforms, Airborne Platforms, and Space-Enabled Defense Networks), End User (Armed Forces, Defense Contractors, and Homeland Security And Border Security Agencies), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Mode Fiber Optic Solutions |

| Multi-Mode Fiber Optic Solutions |

| Armored Fiber Optic Cables |

| Tactical Field Fiber Assemblies |

| Connectors, Splices, And Termination Kits |

| Battlefield Communication Networks |

| Command And Control Systems |

| Radar And Surveillance Networks |

| Electronic Warfare Systems |

| Intelligence, Surveillance, And Reconnaissance Networks |

| Land Platforms |

| Naval Platforms |

| Airborne Platforms |

| Space-Enabled Defense Networks |

| Armed Forces |

| Defense Contractors |

| Homeland Security And Border Security Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Fiber Type | Single-Mode Fiber Optic Solutions | ||

| Multi-Mode Fiber Optic Solutions | |||

| By Product Architecture | Armored Fiber Optic Cables | ||

| Tactical Field Fiber Assemblies | |||

| Connectors, Splices, And Termination Kits | |||

| By Application | Battlefield Communication Networks | ||

| Command And Control Systems | |||

| Radar And Surveillance Networks | |||

| Electronic Warfare Systems | |||

| Intelligence, Surveillance, And Reconnaissance Networks | |||

| By Platform | Land Platforms | ||

| Naval Platforms | |||

| Airborne Platforms | |||

| Space-Enabled Defense Networks | |||

| By End User | Armed Forces | ||

| Defense Contractors | |||

| Homeland Security And Border Security Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the fiber optic market for defense and battlefield communication networks in 2026?

The market stands at USD 4.02 billion in 2026 and is projected to reach USD 5.64 billion by 2031, growing at a 7.01% CAGR over 2026-2031.

What is driving demand for fiber optics in military communication networks?

Demand is rising because armed forces need secure, low-latency, high-bandwidth transport for AI-enabled operations, edge processing, sensor fusion, and multi-domain command structures.

Which fiber type holds the largest share in defense and battlefield communication networks?

Single-mode solutions led with 65.43% share in 2025 because they fit long-haul backbone routes, shipboard trunk lines, and command node interconnects.

Which application is growing the fastest in this space?

ISR networks are the fastest-growing application, with a projected 7.87% CAGR through 2031, reflecting the expansion of sensor-heavy, data-intensive military operations.

Which region leads current demand, and which region is expanding the fastest?

North America held the largest share at 36.78% in 2025, while Asia-Pacific is projected to grow the fastest at an 8.01% CAGR through 2031.

What are the main barriers slowing the wider adoption of defense fiber networks?

The main barriers are high ruggedization and qualification costs, plus field repair complexity that depends on trained technicians and specialized tools in harsh operating conditions.

Page last updated on: