Size and Share of Fiber Optic Infrastructure Market For Airports and Seaports Connectivity

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 430.45 Million |

| Market Size (2031) | USD 751.83 Million |

| Growth Rate (2026 - 2031) | 11.80% CAGR |

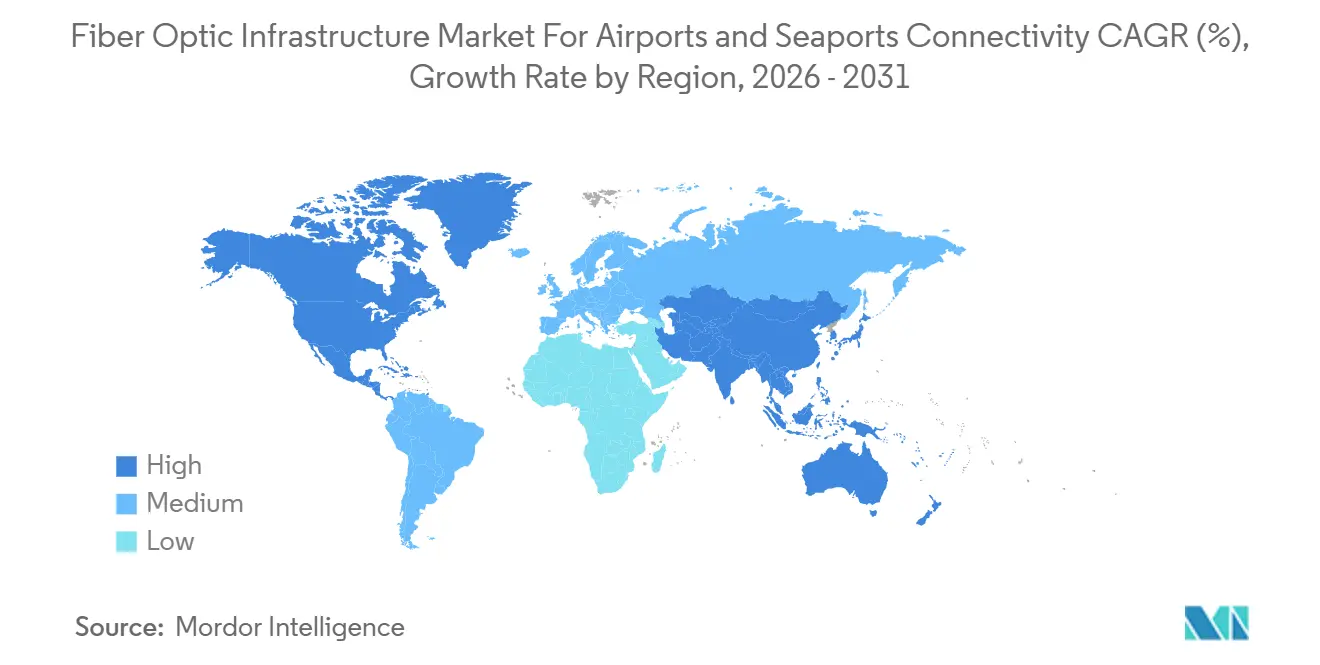

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

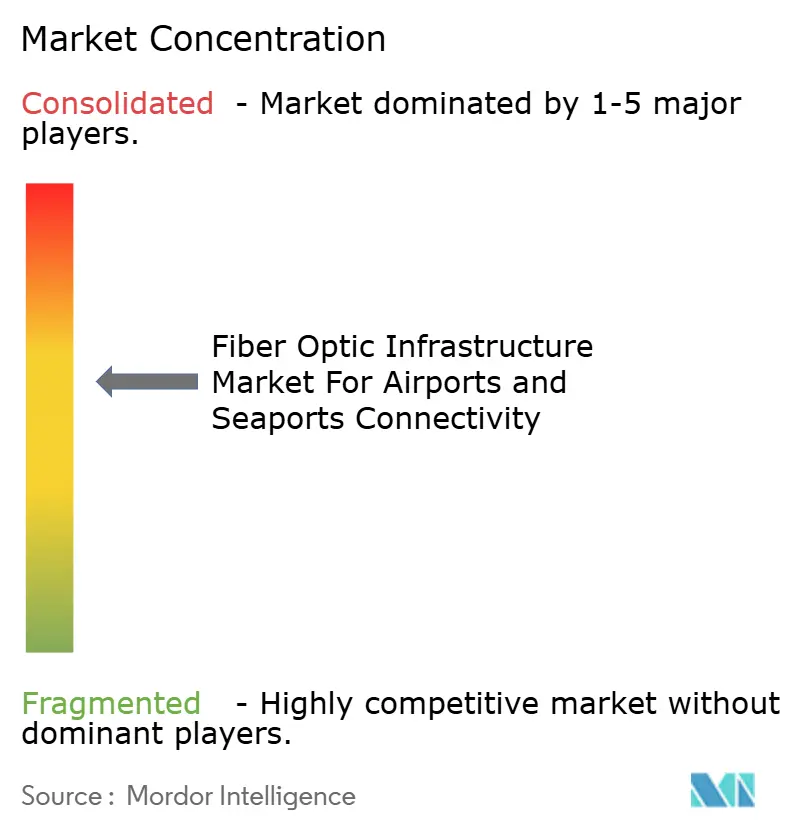

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Fiber Optic Infrastructure Market For Airports and Seaports Connectivity by Mordor Intelligence

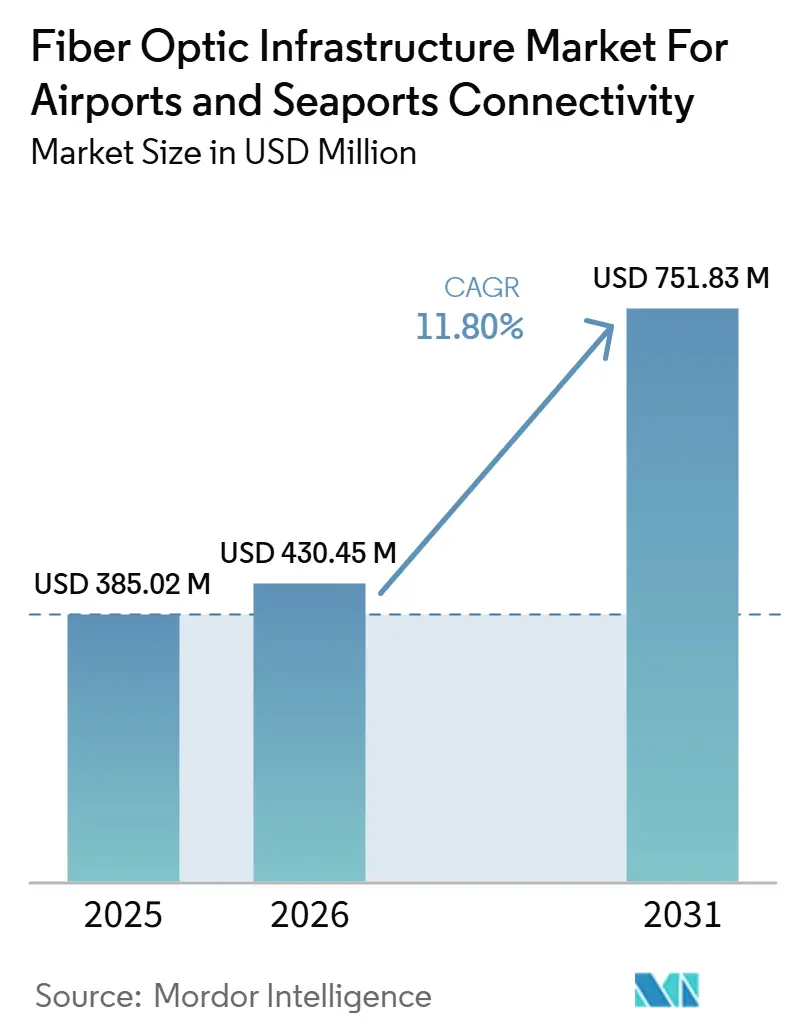

The fiber optic infrastructure market for airports and seaports connectivity is expected to increase from USD 385.02 million in 2025 to USD 430.45 million in 2026 and reach USD 751.83 million by 2031, growing at a CAGR of 11.80% over 2026-2031. The fiber optic infrastructure market for airports and seaports connectivity is expanding as airports and seaports replace legacy networks with unified backbones that support operations, safety, cargo movement, passenger systems, and surveillance on a single physical layer. Demand is also rising because large transport hubs now require greater capacity for digital applications such as real-time monitoring, automated handling systems, biometric processing, and data-intensive security platforms. The fiber-optic infrastructure market for airports and seaports connectivity is also seeing a shift in buying behavior, as operators increasingly prefer bundled deployment, monitoring, and security support rather than managing each network layer separately. Vendor competition is shaped by scale in cable and passive components, but the opportunity is moving toward end-to-end solutions that combine cable, active equipment, campus design, and managed services. Project execution risk still matters because installation inside active airports and seaports is difficult, and cybersecurity requirements are increasing the cost and complexity of each upgrade cycle.

Key Report Takeaways

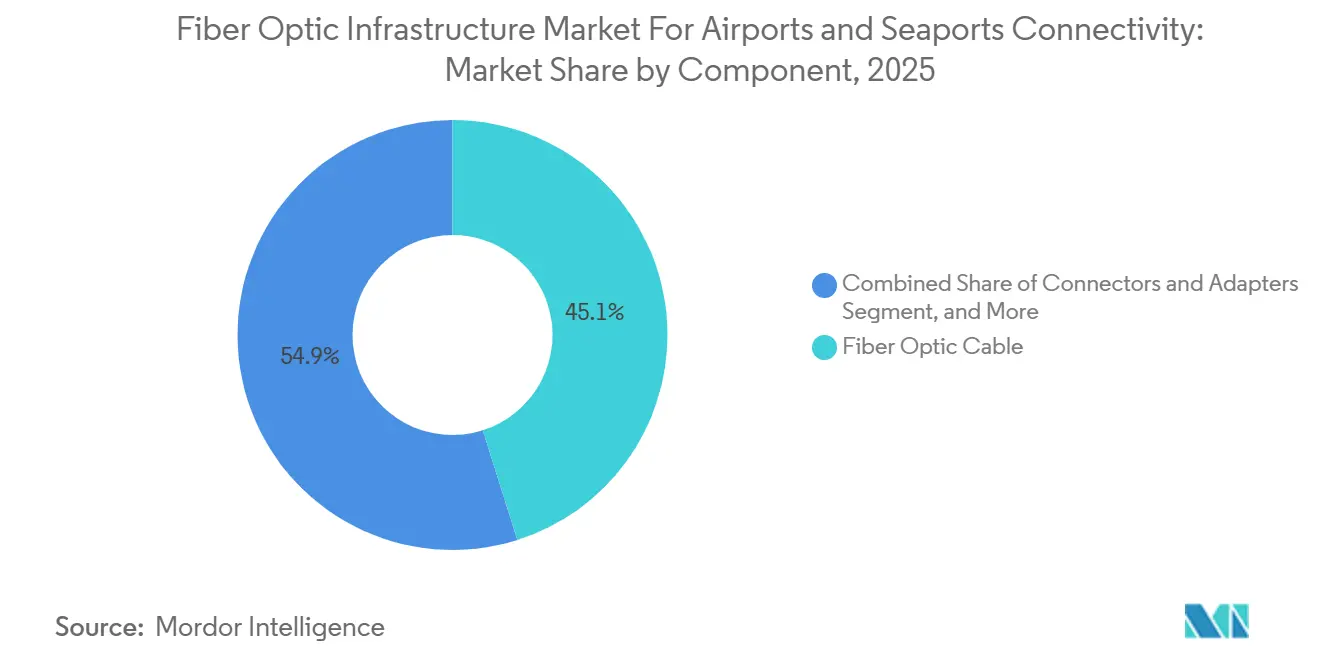

- By component, fiber-optic cable led with a 45.12% revenue share of the fiber optic infrastructure market for airports and seaports connectivity industry in 2025, while transceivers and optical modules are projected to expand at a 11.23% CAGR through 2031.

- By connectivity type, metro and backhaul fiber accounted for 35.03% in 2025, while passive optical LAN is expected to record the highest CAGR of 12.34% through 2031 in the fiber optic infrastructure market for airports and seaports connectivity industry.

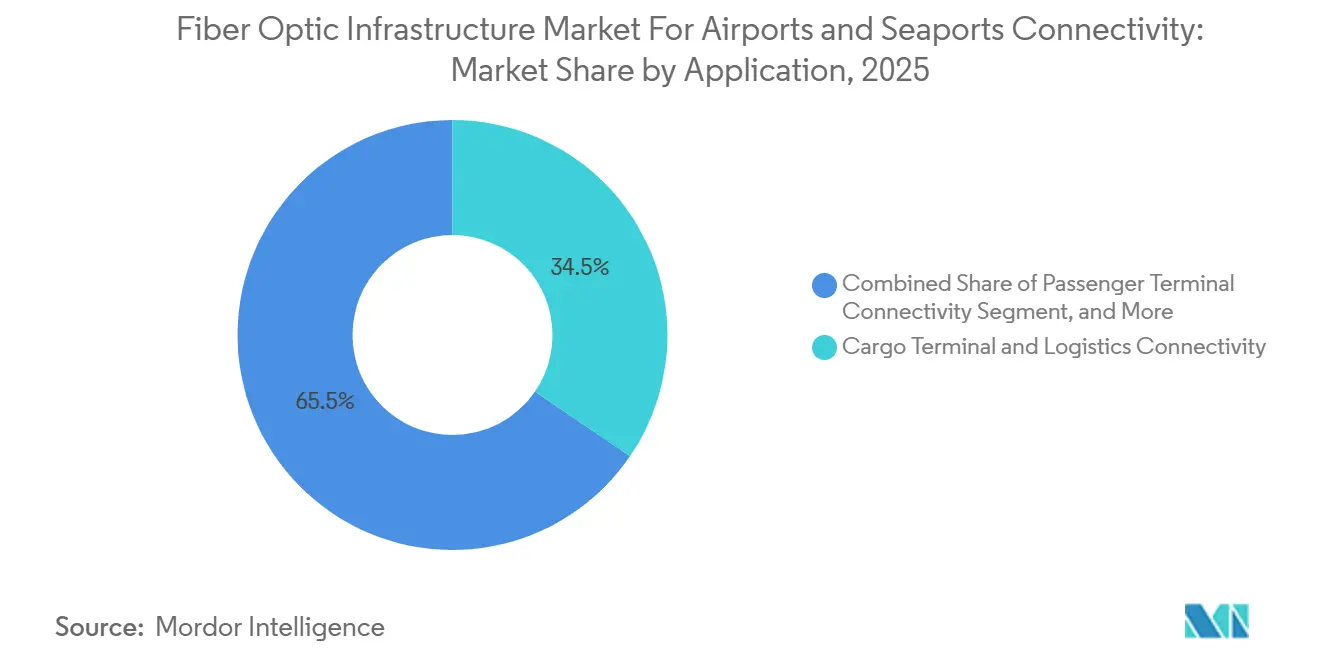

- By application, cargo terminal connectivity accounted for a 34.54% share in 2025, while security and surveillance are projected to grow at a 10.65% CAGR through 2031.

- By end user, airport and port operators held a 40.92% share in 2025, while system integrators and MSPs are expected to post the fastest CAGR at 12.09% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Fiber Optic Infrastructure Market For Airports and Seaports Connectivity

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Airport and seaport digital transformation | +3.0% | Global | Short term (≤ 2 years) |

| Resiliency needs and copper-to-fiber migration | +2.5% | North America and Europe | Short term (≤ 2 years) |

| Private 5G expansion at ports | +1.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Aging copper replacement cycle | +1.5% | North America, with early gains in APAC | Medium term (2-4 years) |

| Network convergence and unified infrastructure demand | +0.8% | Global | Long term (≥ 4 years) |

| Multi-vendor interoperability requirements | +0.6% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Airport and Seaport Digital Transformation Drives Network Investment

The fiber optic infrastructure market for airports and seaports connectivity is benefiting from a broad shift toward connected operations across terminals, cargo areas, and control systems. Airports are moving more services onto shared digital platforms, and this shift raises the value of high-capacity fiber backbones that can support multiple mission-critical functions simultaneously. The same pattern is visible at ports, where digital logistics, equipment monitoring, and smart-port applications depend on stable low-latency connectivity across the site. Valenciaport activated its own private 5G network in January 2025 to support its Smart Port 4.0 framework, showing how digital transformation at ports is tied to stronger underlying connectivity infrastructure.[1]Port Authority of Valencia, “Valenciaport Implements Its Own 5G Connection Network,” Valenciaport In aviation, the FAA's 2026 budget materials placed major emphasis on telecommunications modernization and IP-based infrastructure, which supports the case for broad backbone upgrades across airport environments.[2]Federal Aviation Administration, “FAA FY 2026 Budget Estimates Congressional Justification,” U.S. Department of Transportation Because airport and port operators are modernizing several systems simultaneously, the fiber-optic infrastructure market for airports and seaports connectivity is seeing concentrated procurement activity rather than a slow, steady replacement cycle.

Resiliency Requirements Accelerate Copper-To-Fiber Migration at Aviation Hubs

The fiber optic infrastructure market for airports and seaports connectivity is also being pushed by the need for more resilient communications at major aviation hubs. Legacy copper networks are harder to maintain, and they leave fewer options when operators need higher capacity, cleaner signal performance, and better resistance to interference. FAA budget documents for 2026 highlighted continued investment in telecommunications infrastructure, voice switching, and sustainment of airport cable loops, all of which point to a long runway for backbone modernization. L3Harris stated in May 2026 that it had completed more than 50% of the FAA telecommunications modernization effort and was replacing legacy copper and time division multiplexing technology with high-speed fiber, wireless, and satellite links.[3]L3Harris Technologies, “L3Harris Reaches Over 50% in FAA Telecommunications Modernization,” L3Harris The company also said the program was deploying 150 to 200 new network paths each month and remained on track for completion in 2027, indicating that resiliency-led replacement is already well underway rather than a planning theme. This keeps the fiber-optic infrastructure market for airports and seaports connectivity closely tied to the reliability agenda, not just to bandwidth growth.

Expansion of Private 5G at Ports Creates Sustained Fiber Backhaul Demand

The fiber optic infrastructure market for airports and seaports connectivity is gaining from private 5G adoption at ports because wireless layers still depend on strong fixed backhaul. Port operators are using private 5G to support crane operations, asset visibility, yard movement, and remote operations, but those applications still require reliable data transport between radios, edge systems, and core networks. Valenciaport said its private 5G network was designed to serve the logistics chain with real-time connectivity, edge computing support, and high availability for critical industrial use cases. The same announcement linked the deployment to container tracking, autonomous systems, drones, and equipment monitoring, all of which increase the value of fiber backhaul in dense port environments. This is why the fiber-optic infrastructure market for airports and seaports connectivity continues to benefit, even as operators invest in wireless-heavy architectures inside terminals and container yards. Instead of replacing fiber, private 5G often shifts fiber demand toward aggregation points, rings, and campus backbones.

Lifecycle Replacement of Aging Copper Infrastructure Generates Replacement Wave

The fiber optic infrastructure market for airports and seaports connectivity has a clear replacement driver because much of the installed telecom base at older transport hubs was built for lower data loads. Airports and container ports that were last upgraded in earlier network cycles now need infrastructure that can support denser sensors, modern security systems, and more connected operations. The FAA's 2026 budget request included both Project LIFT and airport cable loop sustainment, which shows that the replacement cycle extends across core telecom systems as well as on-airport cable infrastructure. L3Harris also described the current FAA program as a rebuild of the backbone that connects towers, radar facilities, and air traffic control centers, reinforcing that this is a structural retrofit rather than a limited capacity add-on. For the fiber optic infrastructure market for airports and seaports connectivity, that replacement profile matters because cable wins today can lead to later upgrades in transceivers, switching, and monitoring layers. It also supports repeat spending over several years, since operators rarely refresh both passive and active layers at the same time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High civil works and site preparation costs | -0.8% | Global | Short term (≤ 2 years) |

| Cybersecurity and physical threats to fiber assets | -0.4% | North America and Europe | Medium term (2-4 years) |

| Complex permitting and regulatory approvals | -0.3% | APAC and Middle East | Medium term (2-4 years) |

| Long upgrade cycles and disruption risk | -0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Civil Works and Site Preparation Costs Limit Deployment Velocity

The fiber optic infrastructure market for airports and seaports connectivity still faces a fundamental execution challenge because installation within active airports and seaports is expensive and disruptive. Contractors often need to work around runways, taxiways, container yards, security zones, and sealed surfaces, which slows progress and raises the installed cost far above the cost of cable itself. FAA budget documents show that airport cable loop systems require dedicated sustainment funding, which underlines that underground telecom work at operating airports is a continuing infrastructure burden rather than a one-time event. For smaller regional facilities, those site conditions can delay modernization because capital is usually directed first toward safety, apron, or terminal needs. The fiber optic infrastructure market for airports and seaports connectivity, therefore, expands fastest where operators can combine telecom upgrades with larger redevelopment programs. In cost-constrained settings, the need to stage work around live operations keeps deployment velocity below underlying demand.

Cybersecurity And Physical Threats To Fiber Assets Increase Total Cost Of Ownership

The fiber optic infrastructure market for airports and seaports connectivity also faces higher ownership costs because digital transport networks now carry more operationally sensitive data. Smart-airport systems link passenger services, baggage operations, surveillance, access control, and other connected functions, so a network incident can spread into visible operational disruption. A 2025 article in the Journal of Transportation Security discussed the August 2024 cyberattack on Seattle-Tacoma International Airport and used it as an example of how smart-airport connectivity can expose passenger-facing systems and operational functions to wider disruption. The same article argued that airport environments need defense-in-depth across the cloud, on-premises, IT, OT, vendors, and regulators, meaning network modernization now includes security architecture from the design stage.[4]Journal of Transportation Security, “Smart Airports and the Evolving Cyber Threat,” Springer Nature FAA budget materials also included cybersecurity funding for zero trust, encryption, and information security, showing that security spending is being built into wider telecom modernization plans. For the fiber-optic infrastructure market for airports and seaports connectivity, this raises the cost floor for both new deployments and lifecycle refresh programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Transceivers Drive The Intelligent Network Evolution

In 2025, fiber optic cable accounted for 45.12% share of the fiber optic infrastructure market for airports and seaports connectivity industry, reflecting its role as the base physical layer across airport and seaport systems. The cable segment remains anchored by replacement demand, since older transport hubs still rely on copper-based telecom assets that are harder to maintain and less suitable for present data loads. The fiber-optic infrastructure market for airports and seaports connectivity also favors cable because airports and ports require long-distance signal integrity, immunity to interference, and room for future capacity upgrades. Passive items such as connectors, splitters, and amplifiers hold an important middle position because they determine how efficiently operators can extend links across terminals, perimeters, and equipment zones. Their role becomes more important as operators try to simplify plant design and reduce the number of active touchpoints across large sites.

Transceivers and optical modules are the fastest-growing component group, with an 11.23% CAGR expected from 2026 to 2031. This part of the fiber-optic infrastructure market for airports and seaports connectivity benefits from the shift toward smarter traffic handling, richer surveillance streams, and more connected field assets, all of which raise the value of active optical performance. Operators that already laid fiber in earlier upgrade cycles are now revisiting active layers to unlock additional throughput from their installed plant. Corning and Nokia announced in November 2025 that they were combining passive and active optical LAN offerings in a joint solution for EMEA and APAC, which shows how vendors are targeting customers that want fewer integration gaps across the network stack. Corning also said the combined offer supports speeds from 1 Gbps to 100 Gbps and reduces cabling and total ownership cost against legacy copper, which strengthens the case for active optical upgrades in complex campus environments. As a result, the fiber optic infrastructure market for airports and seaports connectivity is moving beyond cable volume alone and toward a higher-value mix that includes intelligence, management, and lifecycle refresh revenue.

By Connectivity Type: Passive Optical LAN Redefines Terminal Network Architecture

Metro and backhaul fiber held a 35.03% share in 2025, keeping it the largest connectivity layer in the fiber optic infrastructure market for airports and seaports connectivity. That position is logical because airports and seaports depend on strong connections between local operations, metropolitan networks, and external control or logistics systems. The fiber optic infrastructure for airports and seaports connectivity also gives metro and backhaul links a strategic role because they sit underneath cargo coordination, command functions, remote access, and wider enterprise data exchange. Subsea and submarine cable links are gaining strategic visibility around port environments where connectivity assets and logistics infrastructure are starting to overlap. That overlap can strengthen the business case for port-side digital infrastructure because the same location can support operational traffic and wider network interconnection needs.

Passive optical LAN is expected to deliver the fastest growth, with a 12.34% CAGR through 2031. The fiber optic infrastructure market for airports and seaports connectivity is favoring this model because terminal operators want simpler architectures, fewer active floor switches, and easier centralized management across buildings and remote support areas. Corning said its collaboration with Nokia was designed to replace legacy copper with a single high-speed fiber network for Wi-Fi 7, cloud, IoT, and smart-building use cases, which aligns closely with airport terminal and logistics campus needs. The same release said the solution can reduce cabling by 70% and total cost of ownership by 50% against copper-based designs, which explains why optical LAN is attractive in complex transport campuses that want long asset life and lower maintenance load. In practice, passive optical LAN gives the fiber optic infrastructure market for airports and seaports connectivity a route into both new terminal projects and major rewiring programs at older facilities. It also strengthens the position of vendors that can package passive plant, active electronics, and network management under one offer.

By Application: Security And Surveillance Leads Incremental Fiber Demand

Cargo terminal connectivity led with a 34.54% share in 2025, which gave it the largest application position within the fiber optic infrastructure market for airports and seaports connectivity market size. Cargo areas need dependable links for sensors, handling systems, RFID workflows, gate activity, and coordination across multiple parties, so they generate a sustained density of fiber demand. Air traffic control connectivity remains one of the most specification-sensitive areas because reliability, redundancy, and signal quality requirements are especially high. Passenger terminal connectivity also covers a very broad footprint, since it ties together kiosks, signage, boarding tools, Wi-Fi support, and operating systems spread across large buildings. This mix means the fiber-optic infrastructure market for airports and seaports connectivity market is not driven by one use case alone, but by several applications that each need different performance and design choices.

Security and surveillance is projected to grow at a 10.65% CAGR through 2031. The fiber optic infrastructure market for airports and seaports connectivity market is seeing stronger demand here because operators want clearer video flows, more dependable evidence retention, and less congestion on shared networks. The Journal of Transportation Security described how smart-airport connectivity expands the attack surface across surveillance, access control, baggage, flight displays, and other linked systems, which raises the importance of robust network design in security architectures. The same article used the Seattle-Tacoma incident to show that cyber disruption can affect visible passenger systems and operating continuity at the same time. That helps explain why the fiber-optic infrastructure market for airports and seaports connectivity market is allocating more incremental spend toward surveillance and secure operational visibility. It also means security-driven network projects can move ahead even when broader terminal spending is phased over a longer period.

By End User: System Integrators Emerge As The Growth Engine

Airport and port operators held a 40.92% share in 2025, making them the largest end-user group in the fiber optic infrastructure market for airports and seaports connectivity market. Their lead reflects direct control over telecom capital programs and the practical need to align network investment with runway, terminal, berth, and cargo operations. The fiber optic infrastructure for airport and seaport connectivity market also remains operator-led because many upgrades are tied to public infrastructure programs or long-term master plans rather than to short-cycle procurement. FAA budget materials and the ongoing national telecom modernization program show how government-backed aviation operators can create sustained demand across towers, centers, and airport-supporting infrastructure. Port authorities and terminal operators follow a similar pattern when smart-port goals, equipment automation, and logistics visibility all depend on stronger site connectivity.

System integrators and MSPs are projected to expand at a 12.09% CAGR from 2026 to 2031. The fiber optic infrastructure for airports and seaports connectivity market is pushing this group forward because many operators now prefer single-contract accountability for design, deployment, lifecycle management, and security support. That approach reduces coordination burden for facilities that do not want to manage separate suppliers across passive infrastructure, active networking, and monitoring tools. L3Harris described the FAA modernization effort as a nationwide rebuild that uses a build-then-switch approach to avoid operational disruption, which highlights the value of integrator-led execution in live transport environments. Corning and Nokia also framed their joint optical offering around integrated delivery, which supports the wider move toward bundled solutions in complex campus settings. Over time, this should widen the reach of the fiber optic infrastructure market for airports and seaports connectivity industry beyond the largest hubs, since managed delivery is easier for smaller sites to adopt than multi-vendor engineering programs.

Geography Analysis

North America held the largest regional share at 32.13% in 2025, which gave it the largest position in the fiber optic infrastructure market for airports and seaports connectivity share. The region is led by the United States, where aviation telecom modernization is already in active rollout rather than in early planning. FAA budget materials for 2026 highlighted major spending on telecommunications infrastructure, voice switching, and airport cable loop sustainment, all of which support a durable upgrade cycle across aviation assets. L3Harris said in May 2026 that it had surpassed 50% completion in the nationwide FAA modernization effort and was adding 175 positions during the year to keep the program on track for 2027 completion. That progress keeps North America at the center of the fiber optic infrastructure market for airports and seaports connectivity because it combines spending visibility, execution scale, and a strong base of established vendors.

Asia Pacific is expected to post the fastest regional CAGR at 12.34% through 2031. The fiber optic infrastructure market for airports and seaports connectivity industry is expanding quickly in the region because it combines new airport builds, smart-port investment, and a wider willingness to adopt digital operating models across transport infrastructure. Valenciaport is outside the region, but its private 5G example shows the type of container, equipment, and surveillance use cases that Asia Pacific ports are also prioritizing as they modernize operational technology. The region's growth profile is also supported by greenfield infrastructure, which lets operators specify fiber-native architectures from the start instead of retrofitting older facilities.

Europe, the Middle East and Africa, and South America formed the remaining regional base in 2025, with Europe standing out as the most technically mature area outside North America. The fiber-optic infrastructure market for airports and seaports connectivity in Europe benefits from strong standards adoption, large campus environments, and an installed base that is ready for optical LAN and active-layer refresh programs. Corning said its enterprise optical collaboration with Nokia was available across EMEA and APAC, which shows that vendors view Europe and nearby markets as active targets for large campus optical modernization. In Singapore, the Maritime and Port Authority issued Port Marine Notice No. 119 of 2025 for a fiber optic cable laying operation, which points to continuing connectivity work inside one of the world's key port ecosystems. South America and parts of the Middle East and Africa remain more project-driven, but they still add to the fiber optic infrastructure market for airports and seaports connectivity industry where airport expansion, port automation, and digital corridor plans are moving forward. The regional picture therefore combines mature replacement demand in advanced markets with selective build-out demand in developing ones.

Competitive Landscape

The fiber optic infrastructure market for airports and seaports connectivity is moderately consolidated in cable and passive components, where scale, manufacturing depth, and supply reliability matter most. Prysmian, Corning, Furukawa Electric, Nexans, Sterlite Technologies, and AFL compete from a position of product breadth and long-cycle infrastructure relationships. In the active equipment and systems integration layers, the fiber optic infrastructure market for airports and seaports connectivity industry is more fragmented because operators evaluate suppliers by architecture fit, service capability, compliance, and project execution. Nokia, Cisco, SITA, Ciena, Infinera, Juniper Networks, and other specialists compete across different parts of the network stack rather than through a single dominant model. That split between a scale-based passive tier and a fragmented active tier shapes pricing, tender strategy, and partnership behavior across the market.

A clear competitive pattern is vertical integration. The fiber-optic infrastructure market for airports and seaports connectivity increasingly rewards vendors that can offer cable, optical LAN, active electronics, and service support in a single package. Corning and Nokia announced a joint optical offering in November 2025 that combines passive and active layers for enterprise campuses across EMEA and APAC, which is a direct example of this strategy. Corning said the offer supports smart-building, cloud, Wi-Fi 7, and IoT use cases, which fits well with airport terminals, support buildings, and port campuses that want a simpler vendor structure.

Execution scale is another competitive lever. L3Harris stated that it was deploying 150 to 200 new network paths each month in the FAA modernization effort and using a build-then-switch model to limit disruption, which shows how program management capability can matter as much as equipment performance. The fiber optic infrastructure market for airports and seaports connectivity also leaves room for operators and technology partners to shape demand directly, as seen in Valenciaport's private 5G rollout with Cellnex, Lenovo, and Fivecomm around smart-port use cases. That kind of move matters because it creates reference sites for more integrated port connectivity models. The whitespace remains strongest in regional airports and secondary seaports that need modern networks but lack large in-house engineering teams. In those settings, companies that can package delivery, resilience, and ongoing support are likely to capture a larger share of new work in the fiber optic infrastructure market for airports and seaports connectivity.

Leaders of Fiber Optic Infrastructure Market For Airports and Seaports Connectivity

Cisco Systems, Inc.

Nokia Corporation

SITA

Corning Incorporated

Ciena Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: L3Harris disclosed that it has surpassed the 50% completion milestone in the FAA's nationwide telecommunications modernization program, converting copper links to fiber across FAA facilities spanning the United States. The company announced plans to add 175 positions in 2026 to accelerate toward Q3 2027 full completion.

- November 2025: Corning and Nokia announced a strategic collaboration to deliver end-to-end fiber-to-the-edge and optical LAN solutions for enterprises, combining Corning's passive components with Nokia's active elements. The partnership is available across EMEA and APAC, directly addressing modernization requirements for airport and seaport campus networks.

- January 2025: Valenciaport activated its own private 5G network supporting more than 25,000 connected devices at 10 Gbps maximum throughput, with fiber backhaul underpinning the port's Smart Port 4.0 digitalization framework.

Scope of Report on Fiber Optic Infrastructure Market For Airports and Seaports Connectivity

The Fiber Optic Infrastructure Market for Airports and Seaports Connectivity Industry Report is Segmented by Component (Fiber Optic Cable, Connectors and Adapters, Splitters and Couplers, Transceivers and Optical Modules, and Other Components), Connectivity Type (Passive Optical LAN, Active Optical Network, Metro and Backhaul Fiber Connectivity, and Subsea and Coastal Link Connectivity), Application (Passenger Terminal Connectivity, Air Traffic Control and Operational Communications, Cargo Terminal and Logistics Connectivity, Security, Surveillance, and Access Control Connectivity, and Other Applications), End User (Airports, Seaports and Container Terminals, Airport and Port Operators, and System Integrators and Managed Service Providers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fiber Optic Cable |

| Connectors and Adapters |

| Splitters and Couplers |

| Transceivers and Optical Modules |

| Other Components |

| Passive Optical LAN |

| Active Optical Network |

| Metro and Backhaul Fiber Connectivity |

| Subsea and Coastal Link Connectivity |

| Passenger Terminal Connectivity |

| Air Traffic Control and Operational Communications |

| Cargo Terminal and Logistics Connectivity |

| Security, Surveillance, and Access Control Connectivity |

| Other Applications |

| Airports |

| Seaports and Container Terminals |

| Airport and Port Operators |

| System Integrators and Managed Service Providers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Fiber Optic Cable | ||

| Connectors and Adapters | |||

| Splitters and Couplers | |||

| Transceivers and Optical Modules | |||

| Other Components | |||

| By Connectivity Type | Passive Optical LAN | ||

| Active Optical Network | |||

| Metro and Backhaul Fiber Connectivity | |||

| Subsea and Coastal Link Connectivity | |||

| By Application | Passenger Terminal Connectivity | ||

| Air Traffic Control and Operational Communications | |||

| Cargo Terminal and Logistics Connectivity | |||

| Security, Surveillance, and Access Control Connectivity | |||

| Other Applications | |||

| By End User | Airports | ||

| Seaports and Container Terminals | |||

| Airport and Port Operators | |||

| System Integrators and Managed Service Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of fiber optic infrastructure for airport and seaport connectivity?

The sector is valued at USD 430.45 million in 2026 and is projected to reach USD 751.83 million by 2031 at an 11.80% CAGR.

Which component category leads spending across airport and seaport connectivity projects?

Fiber optic cable led in 2025 with a 45.12% share because it remains the base layer for terminal, cargo, control, and surveillance networks.

Which connectivity architecture is growing fastest in airport and port campus networks?

Passive optical LAN is the fastest-growing connectivity type, with a 12.34% CAGR through 2031 as operators look for simpler and more centralized campus designs.

Why are airport operators replacing legacy copper links with fiber?

The main reasons are resiliency, higher throughput, lower maintenance pressure, and the need to support digital operations, security systems, and future upgrades.

Which application area creates the largest demand for fiber links at transport hubs?

Cargo terminal connectivity held the largest application share at 34.54% in 2025 because it supports dense sensor, handling, and logistics data flows.

Which buyers are expanding fastest across new connectivity programs?

System integrators and MSPs are growing fastest, with a 12.09% CAGR through 2031, because many operators now prefer bundled delivery and support models.

Page last updated on: