Size and Share of Fiber Optic Cable Market For Smart Highways and Autonomous Vehicle Infrastructure

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

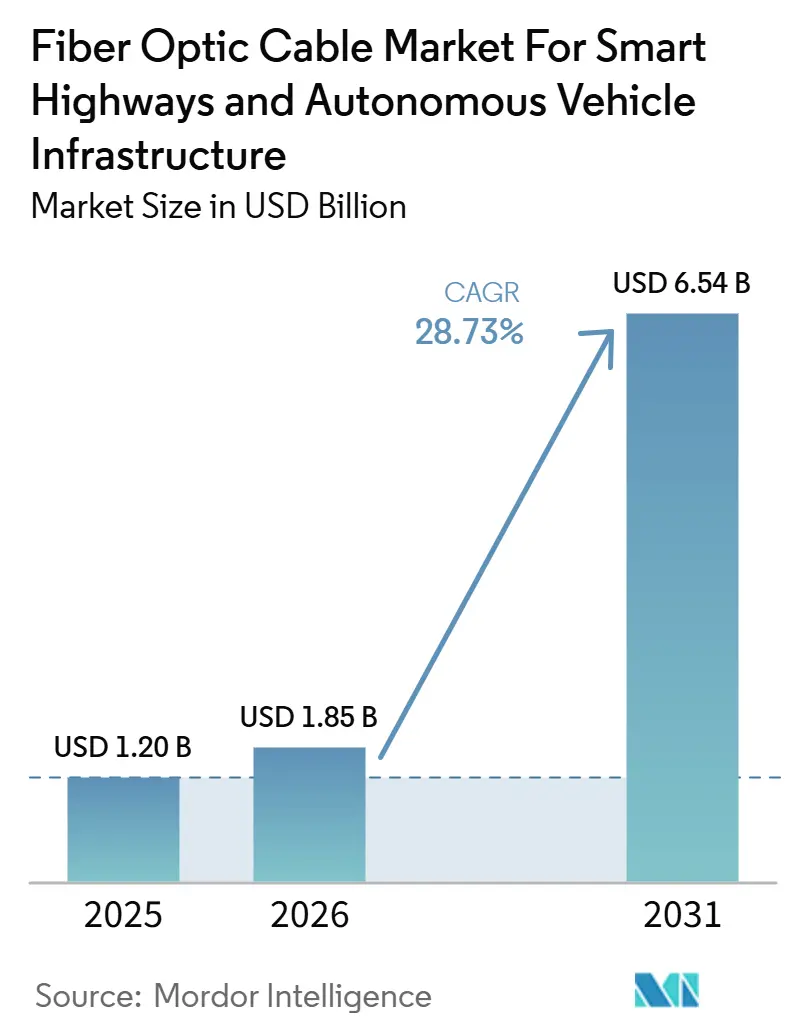

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 28.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Fiber Optic Cable Market For Smart Highways and Autonomous Vehicle Infrastructure by Mordor Intelligence

The fiber optic cable market size for smart highways and autonomous vehicle infrastructure industry is expected to increase from USD 1.2 billion in 2025 to USD 1.85 billion in 2026 and reach USD 6.54 billion by 2031, growing at a CAGR of 28.73% over 2026-2031. The fiber optic cable market for smart highways is expanding as V2X deployment mandates, autonomous corridor programs, and highway digitization plans are moving from pilot activity into funded rollout phases. Fiber is now being specified as the fixed backhaul layer in intelligent transportation networks because legacy wireless links and coaxial systems do not offer the same stability for corridor-scale traffic, sensing, and communication loads. Public investment remains central to demand because many projects are still led by transport ministries, highway authorities, and concession operators that are building digital road systems into broader modernization programs. Competitive conditions remain moderate at the top end, with established global cable suppliers leading revenue while Chinese manufacturers continue to widen their presence through price-led bids in emerging tenders. The main structural brake on the fiber optic cable market for smart highways autonomous vehicle infrastructure remains the cost of excavation, reinstatement, and permitting, which is why deployment models that rely on microduct systems or aerial routes are gaining stronger commercial support.

Key Report Takeaways

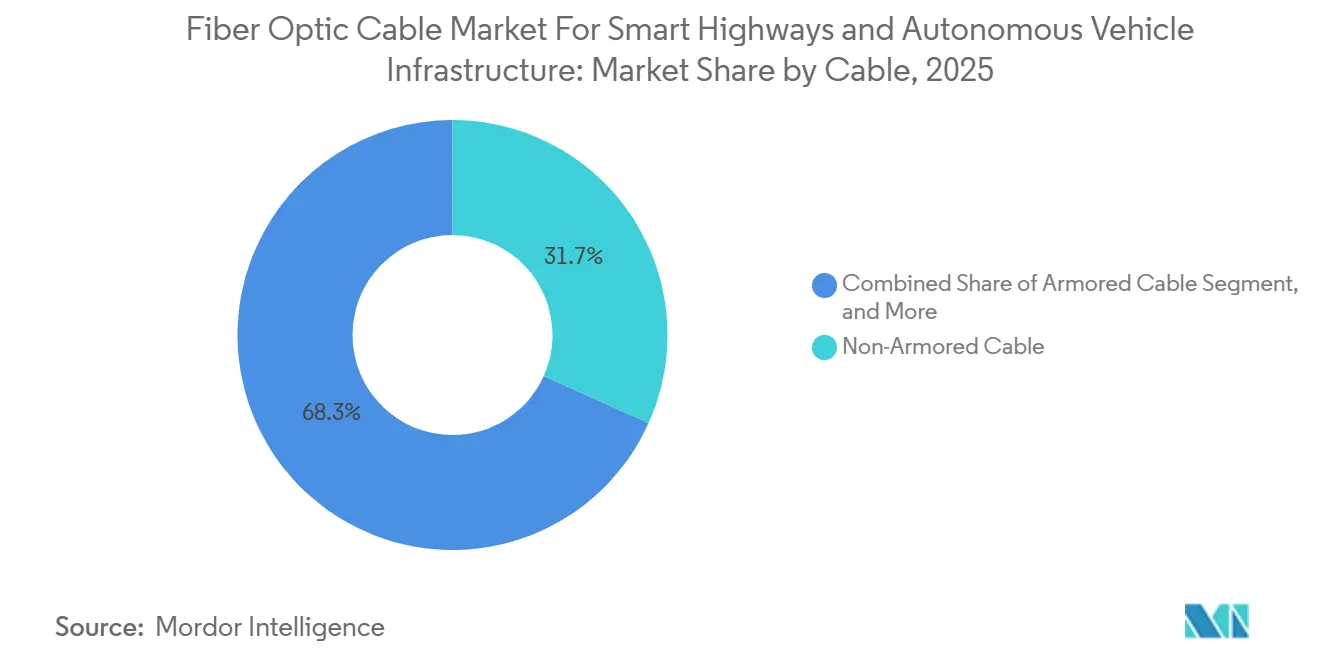

- By cable type, Non-Armored Cable held 31.72% of the fiber optic cable market for smart highways and autonomous vehicle infrastructure in 2025, while Microduct and Blown Fiber Cable are projected to expand at a 28.45% CAGR through 2031.

- By fiber mode, Single-Mode Fiber held 53.34% share in 2025 and is projected to grow at a 27.63% CAGR through 2031.

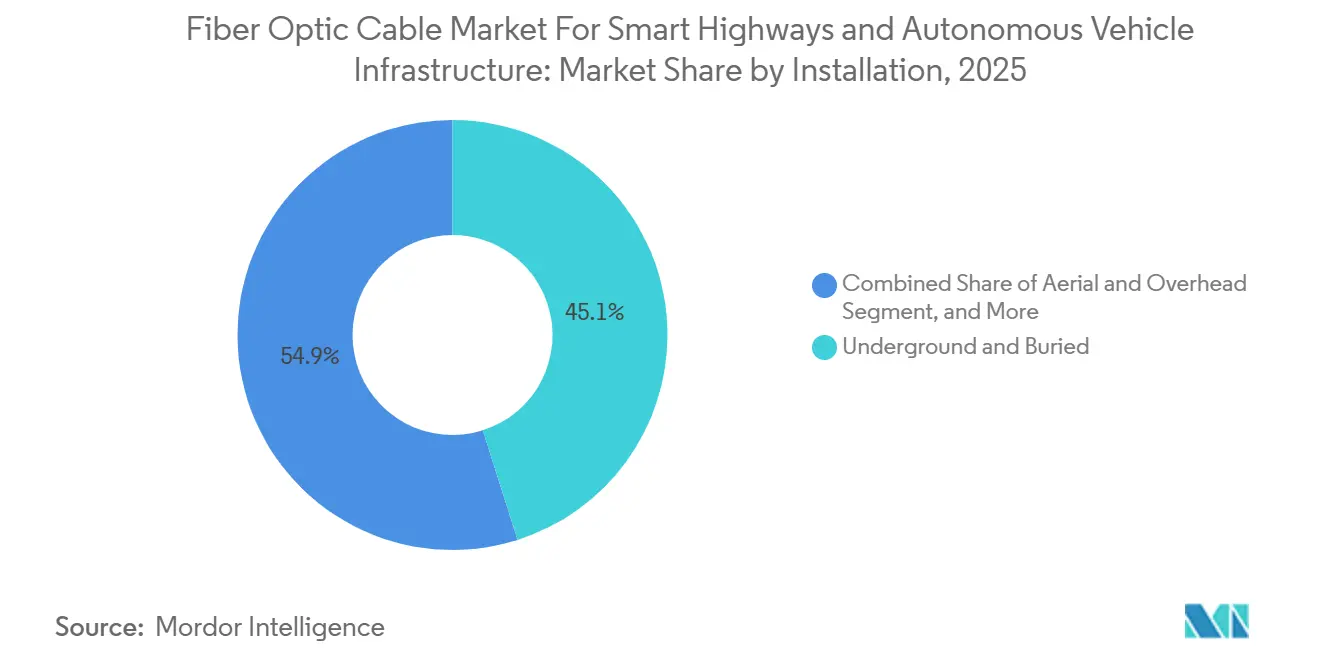

- By installation type, Underground and Buried installations accounted for a 45.10% share in 2025, while Aerial and Overhead installations are expected to expand at a 26.54% CAGR through 2031.

- By application, V2X Backhaul captured 35.98% share in 2025, while Autonomous Vehicle Support Corridors are projected to advance at a 29.45% CAGR through 2031.

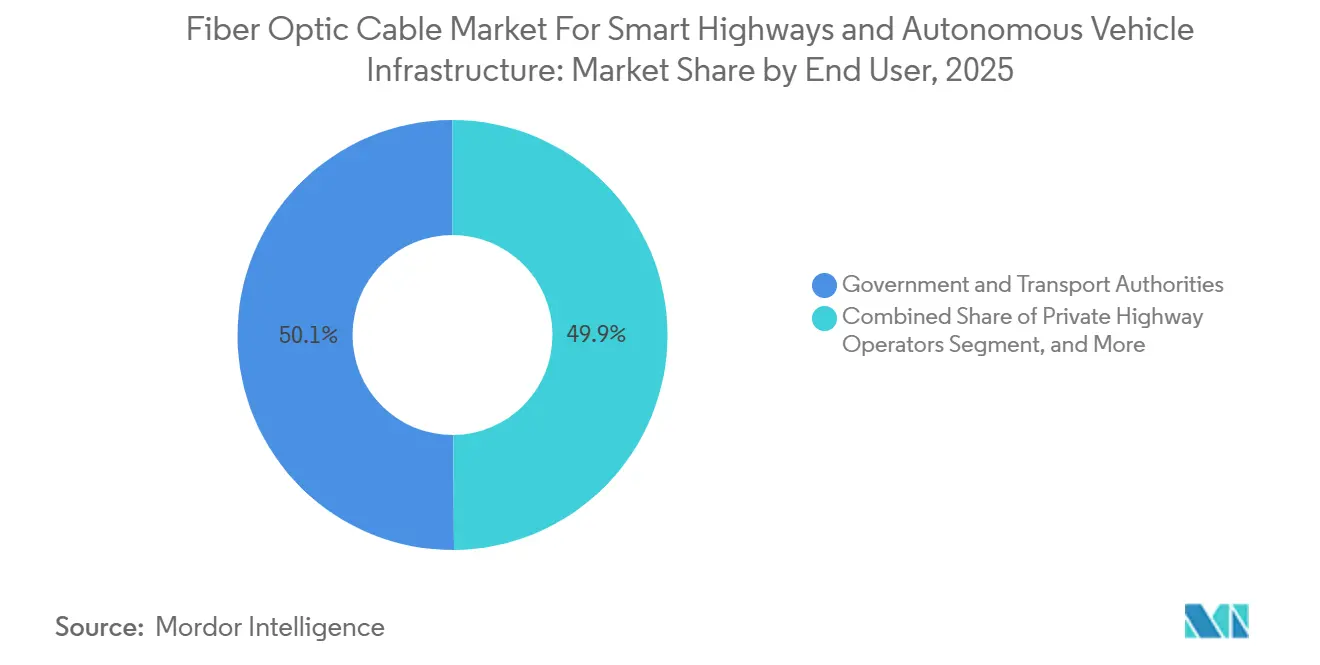

- By end user, Government and Transport Authorities held 50.12% of the fiber optic cable market for smart highways autonomous vehicle infrastructure in 2025, while Logistics and Fleet Operators are projected to record the fastest CAGR of 29.03% through 2031.

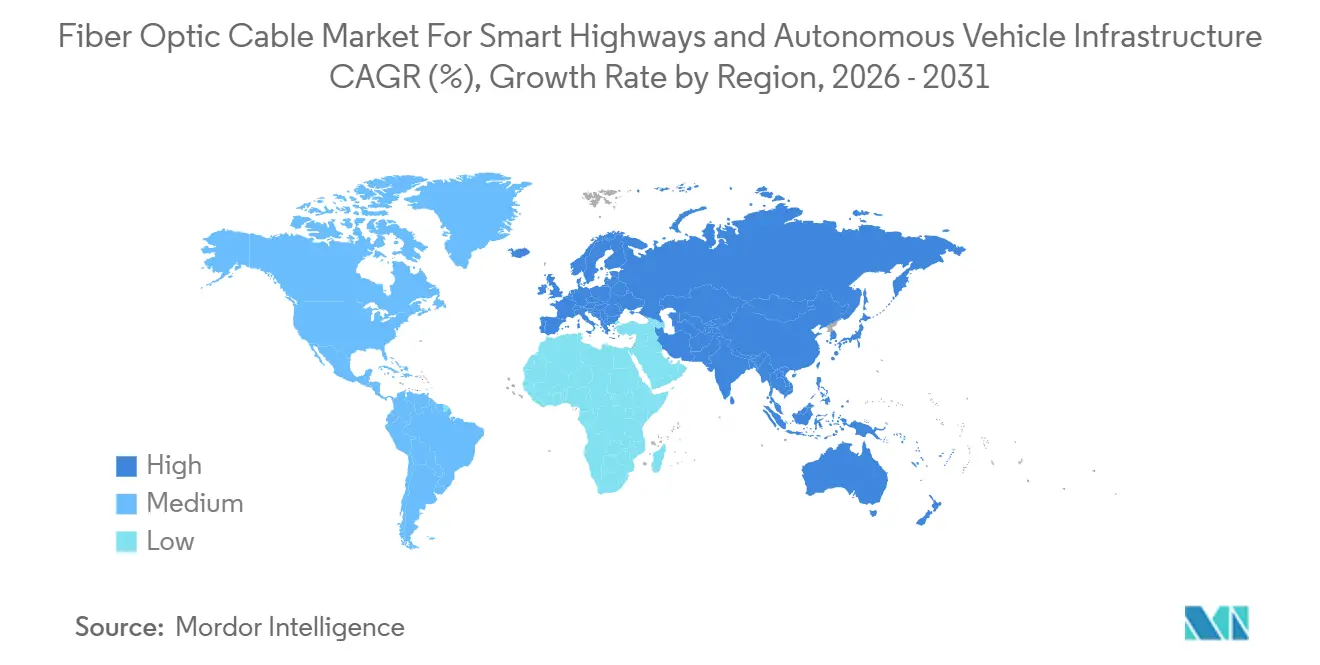

- By geography, Europe led with 32.67% share in 2025, while Asia Pacific is projected to grow at a 28.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Fiber Optic Cable Market For Smart Highways and Autonomous Vehicle Infrastructure

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Smart Corridor Build-Out Programs | +8.2% | Global, with concentration in EU TEN-T corridors, U.S. National Highway System, and China’s national highway grid | Short term (≤ 2 years) |

| Fiber As The Preferred Medium For Intelligent Highway Communication | +6.4% | Global | Short term (≤ 2 years) |

| Government Mandates For Intelligent Transportation Systems | +5.1% | North America and EU core, spill-over to APAC and Middle East and Africa | Medium term (2-4 years) |

| Need For Route Diversity And Resilience In Highway Networks | +3.8% | Global, with early gains in North America and Northern Europe | Medium term (2-4 years) |

| Monetization Of Corridor Data Through Fiber Network Commercialization | +2.9% | EU and North America, with early commercialization in India via NHAI PPP model | Long term (≥ 4 years) |

| Increasing Fiber Density Requirements Along Highway Corridors | +2.3% | APAC core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Smart Corridor Build-Out Programs

State-backed corridor programs are moving from broad transport policy into live procurement schedules, and that shift is giving the fiber optic cable market for smart highways and autonomous vehicle infrastructure a stronger near-term order base. The Federal Highway Administration released USD 58.8 million in V2X grants in 2024 across Arizona, Texas, Wyoming, Michigan, and Virginia, and those projects required fixed backhaul links for roadside unit connectivity. The U.S. national deployment plan also set a target for V2X coverage across 50% of the National Highway System by 2031, which moves corridor fiber demand from a discretionary line item into a more visible infrastructure requirement.[1]U.S. Department of Transportation, “Saving Lives with Connectivity, A Plan to Accelerate V2X Deployment,” U.S. Department of Transportation Once agencies design highway connectivity around dense node placement, every added gantry, cabinet, and edge device raises the need for reliable fiber paths and spare capacity. The fiber optic cable market for smart highways and autonomous vehicle infrastructure is therefore benefiting not only from higher project counts, but also from denser build specifications inside each funded corridor. This pattern also favors scalable cable architectures because operators want assets that can support later upgrades without repeating the heaviest civil works.

Fiber As The Preferred Medium For Intelligent Highway Communication

Wireless-only backhaul has become harder to justify on high-speed road networks where sensor density, latency demands, and continuous data movement all rise together. A 2025 peer-reviewed study in Vehicle Communications found that optical network solutions for roadside unit connectivity materially outperform wireless alternatives in intelligent transportation settings.[2]“Optimizing Road Side Units Connectivity in Intelligent Transportation Systems with Optical Network Solutions,” Vehicle Communications This matters for the fiber optic cable market for smart highways and autonomous vehicle infrastructure because corridor operators are now treating fiber as a design requirement rather than an optional add-on. The move is reinforced by the IEEE 802.3cz standard for automotive multigigabit optical communications over glass fiber, which is being adopted for use cases spanning both vehicle systems and roadside infrastructure.[3]“KD to Integrate Its Transceiver Into ZF ProAI ECU,” Telematics Wire As LiDAR, radar, weather sensing, and camera clusters push higher data loads through each roadside node, the tolerance for unstable or congested backhaul drops sharply. The fiber-optic cable market for smart highways and autonomous vehicle infrastructure benefits from this shift, as higher performance requirements often translate into higher fiber counts, lower attenuation specifications, and more durable long-haul corridor designs.

Government Mandates For Intelligent Transportation Systems

Regulation is playing a direct role in turning connected road programs into mandatory infrastructure upgrades across several major corridors. The 5G-BEAM project on the Brenner route formally launched in December 2025 under the Connecting Europe Facility Digital program to support cooperative and automated mobility across a cross-border highway corridor. In Italy, Smart Road certification requirements under Ministerial Decree 70/2018 have already been translated into live corridor deployment, with Tangenziale di Napoli becoming the first certified Smart Road in June 2026. That certification included fiber-connected traffic detection, weather systems, intelligent cameras, and V2I communication infrastructure, demonstrating how compliance standards directly translate into cable demand. The fiber optic cable market for smart highways and autonomous vehicle infrastructure benefits when mandates clearly define technical baselines, enabling agencies to move faster from planning to specification and tendering. This also reduces some cyclical volatility because spending is tied less to optional modernization and more to formal compliance with road network performance rules.

Need For Route Diversity And Resilience In Highway Networks

Single-route fiber paths are becoming less acceptable where roads carry emergency communications, connected vehicle data, and early autonomous operations. India’s NHAI disclosed plans in November 2024 to build an optical fiber network under a PPP Build-Operate-Transfer model across its 146,000-kilometer highway grid, with pilots active on the Delhi-Mumbai Expressway and the Hyderabad-Bangalore Corridor. The stated network approach focused on route diversity and redundancy, which means future procurement is tied not only to route length but also to resilience design. Turkey also committed to extending its highway fiber network beyond 20,000 kilometers, with 7,931 kilometers complete as of 2025 and construction continuing on the balance. In practice, dual-path and redundant layouts raise cable demand per kilometer above what simple network maps suggest. The fiber optic cable market for smart highways and autonomous vehicle infrastructure therefore gains an additional layer of volume support when network resilience becomes a stated design objective rather than a later-stage enhancement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Civil Works And Right-Of-Way Costs In Highway Corridors | -4.2% | Global, most severe in North America and Western Europe | Short term (≤ 2 years) |

| Long Permitting Cycles For Highway Infrastructure Projects | -2.8% | North America and EU, with secondary impact in APAC | Medium term (2-4 years) |

| Interoperability Challenges Across ITS Platforms And Standards | -1.9% | Global | Medium term (2-4 years) |

| Project Deferrals From Budget Constraints And Funding Gaps | -1.4% | South America and Middle East and Africa, spill-over to Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Civil Works And Right-Of-Way Costs In Highway Corridors

Excavation and reinstatement remain the clearest structural cost burden in the fiber optic cable market for smart highways and autonomous vehicle infrastructure. The Fiber Broadband Association’s annual deployment cost report, produced with Cartesian and released in January 2026, placed median underground installation costs at USD 18 per foot in 2025, up 12% year over year.[4]Fiber Broadband Association and Cartesian, “Fiber Deployment Cost Annual Report 2025,” Fiber Broadband Association The same report showed that labor accounted for 60-80% of total construction spending, leaving limited room for agencies to offset inflation through product purchasing alone. A January 2026 analysis tied 75-90% of fiber installation costs to road excavation and reinstatement, and concluded that missing dig-once policies can multiply costs by 10 times compared with placing conduit during original road construction. IEC TR 63431:2025 supports a move toward microduct systems that can reduce installation costs by 50-75% versus open trenching, but adoption still takes time because procurement cycles do not change overnight. The result is a market where demand stays strong, but delivery timing depends heavily on whether project owners can lower civil intensity.

Long Permitting Cycles For Highway Infrastructure Projects

Permitting is a slower but still meaningful restraint because it delays starts even when funding and technical plans are already in place. Highway fiber projects often require sequential approvals from transport departments, utility authorities, environmental bodies, and corridor managers, which lengthens mobilization timelines before trenching can begin. California uses a statutory environmental exemption to support broadband deployment, yet active 2026 filings still show separate project processing for highway corridor fiber work on routes such as U.S. Highway 50. Cross-border projects in Europe face another layer of variation because right-of-way rules, concession terms, and national transport procedures differ from one jurisdiction to another. The fiber optic cable market for smart highways and autonomous vehicle infrastructure can, therefore, show a healthy pipeline on paper while actual installation activity remains staggered across approval windows. This timing mismatch is especially important when operators are working toward fixed compliance milestones between 2028 and 2031 and cannot easily shift labor or capital across delayed corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable Type: Microduct Architecture Is Reshaping Highway Fiber Procurement

Non-Armored Cable held 31.72% of the fiber optic cable market for smart highways and autonomous vehicle infrastructure share in 2025, making it the leading cable type across smart highway use cases. Its lead position reflects the fact that many highway projects route fiber through conduit, so the duct itself already provides the core mechanical protection required for long corridor runs. In those settings, added armoring can raise cable weight, increase installed cost, and complicate field termination without delivering proportional operating benefit. Microduct and Blown Fiber Cable are projected to grow at a 28.45% CAGR through 2031, as agencies seek modular systems that allow them to add strands later without reopening the entire route. The fiber optic cable market for smart highways autonomous vehicle infrastructure is responding to that preference as lifecycle flexibility now matters almost as much as first-pass installation cost.

The Pennsylvania Turnpike example remains important because its 500-mile microtrench conduit deployment demonstrated documented cost savings of 50-75% compared to conventional open-cut trenching. The same project also demonstrated why spare microduct capacity has real value when operators want to support both transport systems and external broadband leasing demand. Armored Cable still holds relevance in direct-buried greenfield projects across South America and Middle East and Africa, where conduit is less consistently pre-installed. Ribbon Cable remains useful at traffic management hubs where high-count splicing efficiency matters more than route flexibility. Across the fiber optic cable market for smart highways and autonomous vehicle infrastructure industry, IEC TR 63431:2025 has become a useful technical reference because it gives highway agencies a clearer basis for specifying microduct systems with less procurement uncertainty.

By Fiber Mode: Single-Mode Fiber Dominance Reflects The Physics Of Corridor-Scale Connectivity

Single-Mode Fiber accounted for 53.34% of the fiber optic cable market for smart highways and autonomous vehicle infrastructure by fiber mode in 2025 and is projected to grow at a 27.63% CAGR through 2031. That combination of scale and growth reflects the basic physics of corridor networking, because inter-city road links often stretch far beyond the range where multimode systems stay efficient. Long highway paths between traffic centers, toll nodes, and sensing clusters favor lower attenuation and lower regeneration needs over distance. The 2025 roadside connectivity study in Vehicle Communications supports this direction, showing the performance advantage of optical network solutions in intelligent transportation environments. The fiber optic cable market for smart highways autonomous vehicle infrastructure, therefore, continues to anchor its backbone demand in single-mode builds rather than short-reach alternatives.

This preference is becoming more entrenched as LiDAR, radar, imaging, and environmental sensing loads climb on connected corridors. The IEEE 802.3cz standard has also strengthened the case for glass fiber in multigigabit automotive communications tied to road and vehicle infrastructure. Multimode Fiber still retains a practical role inside toll plazas, traffic management buildings, and maintenance depots where link lengths are short and easier termination is useful. Plastic Optical Fiber also keeps a small niche in tight roadside cabinets and in-vehicle proximity links where bend flexibility matters more than long-distance transmission. Across the fiber optic cable market for smart highways and autonomous vehicle infrastructure industry, demand is therefore widening across corridor backhaul and facility-level interconnects, even though single-mode remains the clear performance anchor.

By Installation Type: Cost Pressures Are Expanding Interest In Aerial Options

Underground and Buried installation retained a 45.10% share in 2025, which kept it as the leading method in the fiber optic cable market for smart highways and autonomous vehicle infrastructure. Agencies still prefer buried assets because they are protected, long-lived, and less exposed to accidental damage on busy road corridors. That preference is strongest where highways are already being rebuilt or expanded and where conduit can be installed alongside broader civil works. At the same time, Aerial and Overhead installation is projected to expand at a 26.54% CAGR through 2031, which shows that cost pressure is changing route design choices. The Fiber Broadband Association’s 2025 cost study put average aerial deployment at USD 8 per foot versus USD 18 per foot for underground work, which is too large a gap for planners to ignore.

That cost difference gives existing gantries, sign structures, poles, and lighting assets a larger role in future corridor design. Aerial routes can also shorten installation schedules when compliance deadlines are fixed, and agencies need a faster path to service activation. Submarine and underwater deployment remains a specialized niche tied to river crossings, estuary links, and harbor-adjacent expressway projects. Tunnel and Bridge Integrated Deployment is becoming more visible because new transport structures are increasingly designed with embedded microduct and ITS fiber from the start. The fiber optic cable market for smart highways and autonomous vehicle infrastructure industry is therefore moving toward a more mixed installation model, where buried fiber stays dominant but overhead and structure-integrated routes solve time and cost constraints more directly.

By Application: V2X Backhaul Anchors Revenue While AV Corridors Set The Pace For Growth

V2X Backhaul captured 35.98% share in 2025, making it the largest application in the fiber optic cable market for smart highways and autonomous vehicle infrastructure. Its lead comes from a basic network role, because roadside units, weather systems, traffic gantries, and emergency communications all need dependable aggregation back to control centers. The U.S. national deployment plan targets V2X coverage across 50% of the National Highway System by 2031, with a longer-term objective of 75% by 2036. That target establishes a minimum infrastructure floor across more than 80,000 route miles and provides backhaul fiber with a durable planning base. Traffic Monitoring and Incident Management, along with Smart Tolling and Revenue Collection, also continue to support demand because these functions rely on stable transport links for real-time operations.

Autonomous Vehicle Support Corridors are projected to grow at a 29.45% CAGR through 2031, which makes them the fastest-growing application in the fiber optic cable market for smart highways and autonomous vehicle infrastructure industry. FiberLight’s USD 20 million deployment along Texas State Highway 130 demonstrated how node density, highway length, and autonomous-use-case design can quickly increase corridor fiber requirements. That project installed more than 240 Public Infrastructure Network Nodes at 2,000-foot intervals and provided 10-100 Gb/s corridor connectivity, which gives other agencies a visible reference model. Environmental Monitoring and Weather Sensing is also becoming more important because operators can use the fiber line itself as a distributed sensor rather than depend only on point hardware. On the Joshinetsu Expressway, a live trial confirmed that communication-grade fiber could detect vehicle vibrations, road surface ice-formation temperatures, and structural deformation across a 100-kilometer section without installing additional point sensors at every location.

By End User: Public Authorities Lead Spending While Logistics Buyers Gain Speed

Government and Transport Authorities controlled 50.12% share in 2025, which kept them as the largest buyer group in the fiber optic cable market for smart highways and autonomous vehicle infrastructure. Their lead reflects the fact that national and regional road digitization programs still sit mainly inside public budgets, concession mandates, and transport compliance frameworks. India’s NHAI illustrates the scale of this institutional role, with a nationwide plan that was expected to surpass the combined fiber networks built by RailTel and Power Grid Corporation of India. Private Highway Operators also remain important within this segment because PPP concessionaires in Europe and Australia are directly exposed to smart road performance requirements. The fiber optic cable market for smart highways and autonomous vehicle infrastructure industry, therefore, continues to depend on public-sector planning depth even when execution is shared with private contractors and infrastructure partners.

Logistics and Fleet Operators are projected to grow at a 29.03% CAGR through 2031, which makes them the fastest-rising end-user group. In March 2026, Japan’s T2 autonomous truck program completed a hands-free Level 2 run of nearly 500 kilometers between the Kanto and Kansai regions on national highways. That milestone matters because long-haul automated freight needs corridor consistency, and wireless coverage gaps can become a serious operating weakness on routes intended for scaled deployment. Logistics companies are therefore moving from passive users of digital roads into active co-investors in truck platooning and AV-ready corridor plans. Automotive OEMs and broader mobility ecosystems still shape specifications more than direct cable procurement, but their technical demands continue to influence how the fiber optic cable market for smart highways and autonomous vehicle infrastructure industry evolves.

Geography Analysis

Europe held 32.67% of the fiber optic cable market for smart highways and autonomous vehicle infrastructure share in 2025, which kept it as the largest regional contributor. The region’s lead reflects binding interoperability goals, active concession models, and corridor funding structures under the Connecting Europe Facility Digital framework. Italy’s Tangenziale di Napoli became the country’s first certified Smart Road in June 2026, and the corridor deployed 217 intelligent cameras, 15 traffic detection gantries, 8 weather stations, and 40 V2I and Cellular V2X communication antennas. That project matters because it gives other European operators a practical compliance template rather than a theoretical policy target. Germany, France, and the United Kingdom remain the largest individual national markets because motorway control systems there continue to require steady capacity upgrades as connected vehicle traffic and real-time analytics loads increase.

North America remained the second-largest region in the fiber optic cable market for smart highways and autonomous vehicle infrastructure, supported by the U.S. V2X deployment plan and corridor modernization funding under the Bipartisan Infrastructure Law. California alone had major 2026 activity, including approximately USD 150 million of fiber optic infrastructure work along Highway 101 in Sonoma County and active middle-mile corridor processing on U.S. Highway 50. In April 2026, Cavnue won a Virginia Department of Transportation contract to deploy its Smart Road Platform on Interstate 95 in the Richmond region, which supports a managed service model for lane-level corridor operations data. Canada and Mexico offer moderate opportunities, while South America remains smaller but active, with Brazil and Argentina pursuing smart highway pilots even though fiscal constraints still create a higher risk of project deferral.

Asia Pacific is projected to grow at a 28.76% CAGR through 2031, making it the fastest-expanding region in the fiber optic cable market for smart highways and autonomous vehicle infrastructure industry. India remains a major regional growth anchor because NHAI’s digital highway network plan is already active on flagship pilot corridors and is built around national-scale route coverage. Japan is also testing how mobile and fiber layers can work together, with a 2025 Level 4 autonomous driving trial on the Shin-Tomei Expressway using 5G to evaluate selective complementarity rather than full replacement of dedicated road fiber. Middle East and Africa is moving forward through national vision projects and smart city infrastructure spending, which is pulling road connectivity into broader digital transport programs. Turkey adds a concrete regional benchmark because it committed to a 20,141-kilometer highway fiber target, with 7,931 kilometers completed by 2025 and construction continuing on the rest.

Competitive Landscape

The fiber optic cable market for smart highways and autonomous vehicle infrastructure remains moderately consolidated at the top, with Prysmian Group, Corning Incorporated, and Sumitomo Electric Industries leading global revenues while several regional suppliers compete for project-specific tenders. Competitive pressure has intensified because Asian manufacturers such as Yangtze Optical Fiber and Cable, Hengtong Optic-Electric, and ZTT Group continue to challenge incumbents through pricing and broad product portfolios. In 2026, Corning announced large multiyear supply agreements with Meta, Amazon, and NVIDIA, which indicates that manufacturing capacity is being absorbed by hyperscale optical demand at the same time road infrastructure programs are rising. That capacity competition matters because highway buyers often draw from the same production ecosystem serving data center optical infrastructure. The fiber optic cable market for smart highways and autonomous vehicle infrastructure industry, therefore, faces a competitive dynamic where scale, supply assurance, and qualification status matter as much as raw cable pricing.

Product strategy is also becoming more specialized as AV-ready corridors demand distributed sensing, high fiber counts in smaller duct footprints, and durable roadside connectivity. Suppliers that can support microduct-first designs, long-haul single-mode performance, and corridor monitoring applications are better positioned in premium highway projects. This is one reason the fiber optic cable market for smart highways and autonomous vehicle infrastructure industry is not competing on commodity cable alone, because operators increasingly want a mix of transport capacity, future upgrade flexibility, and compatibility with road sensing architectures. Asian manufacturers are using this transition to move up the value curve, especially where governments want integrated solutions for vehicle-road-cloud connectivity and lower installed cost. At the same time, European and North American suppliers continue to benefit where procurement frameworks place more weight on certification, standards alignment, and domestic or regionally compliant supply chains.

Standards are shaping competition more directly now, especially in microduct and installation design. IEC TR 63431:2025 has become an important reference point because it gives agencies and concessionaires a clearer technical baseline for microduct deployment. Another clear strategic move came in March 2026, when AFL, Corning Incorporated, Lightera, and Prysmian formally committed BABA-compliant fiber and cable supply to the NTIA for the duration of the U.S. BEAD program. Taken together, these moves show that the fiber optic cable market for smart highways and autonomous vehicle infrastructure is being shaped by a combination of plant capacity, standards compliance, and the ability to support long, complex transport corridors with lower execution risk.

Leaders of Fiber Optic Cable Market For Smart Highways and Autonomous Vehicle Infrastructure

Prysmian Group

Corning Incorporated

Sumitomo Electric Industries, Ltd.

Furukawa Electric Co., Ltd.

Yangtze Optical Fibre and Cable Joint Stock Limited Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Corning Incorporated announced a multibillion-dollar multiyear optical fiber and cable supply agreement with Amazon to support Amazon's expanding U.S. data center infrastructure, with plant capacity expansion in Hickory, North Carolina, projected to create 1,000 manufacturing and several hundred construction positions. The deal, following Corning's USD 6 billion Meta agreement and USD 3.2 billion NVIDIA partnership, signals a sustained tightening of Corning's fiber manufacturing capacity with direct procurement implications for highway cable buyers.

- June 2026: Tangenziale di Napoli received official Smart Road certification from Italy's Ministry of Infrastructure and Transport under Ministerial Decree 70/2018, becoming Italy's first certified Smart Road. The 22-kilometer Autostrade per l'Italia corridor, supported technologically by Movyon and the National Center for Sustainable Mobility, deployed 217 smart cameras, 40 V2X communication antennas, and real-time V2I bidirectional communication for connected and autonomous vehicles.

- May 2026: Kajima Corporation, NEXCO East Japan, and NI&C reported results from Japan's first fiber-optic distributed-sensing trial for real-time highway monitoring, which has been active since November 2025 on a 100-kilometer section of the Joshinetsu Expressway. The trial confirmed simultaneous detection of vehicle vibrations, road surface ice-formation temperatures, and structural deformation across bridges, culverts, and embankments using existing communication-grade fiber cables.

- April 2026: Cavnue, a Consor Engineers subsidiary, was awarded a Virginia Department of Transportation contract to deploy its Smart Road Platform on Interstate 95 in the Richmond region, establishing a managed-service model for continuous lane-level, real-time corridor visibility across one of Virginia's most heavily trafficked corridors.

Scope of Report on Fiber Optic Cable Market For Smart Highways and Autonomous Vehicle Infrastructure

The Fiber Optic Cable Market for Smart Highways and Autonomous Vehicle Infrastructure Industry Report is Segmented by Cable Type (Armored Cable, Non-Armored Cable, Ribbon Cable, Microduct and Blown Fiber Cable, Other Cables), Fiber Mode (Single-Mode Fiber, Multimode Fiber, and Plastic Optical Fiber), Installation (Underground and Buried, Aerial and Overhead, Submarine and Under-Water, and Tunnel and Bridge Integrated Deployments), Application (Roadside Communications and V2X Backhaul, Traffic Monitoring and Incident Management, Smart Tolling and Revenue Collection, Autonomous Vehicle Support Corridors, and Environmental Monitoring and Weather Sensing), End User (Government and Transport Authorities, Private Highway Operators, Logistics and Fleet Operators, and Automotive OEMs and Mobility Ecosystem Providers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Armored Cable |

| Non-Armored Cable |

| Ribbon Cable |

| Microduct and Blown Fiber Cable |

| Other Cable Types |

| Single-Mode Fiber |

| Multimode Fiber |

| Plastic Optical Fiber |

| Underground and Buried |

| Aerial and Overhead |

| Submarine and Under-Water |

| Tunnel and Bridge Integrated Deployments |

| Roadside Communications and V2X Backhaul |

| Traffic Monitoring and Incident Management |

| Smart Tolling and Revenue Collection |

| Autonomous Vehicle Support Corridors |

| Environmental Monitoring and Weather Sensing |

| Government and Transport Authorities |

| Private Highway Operators |

| Logistics and Fleet Operators |

| Automotive OEMs and Mobility Ecosystem Providers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Cable Type | Armored Cable | ||

| Non-Armored Cable | |||

| Ribbon Cable | |||

| Microduct and Blown Fiber Cable | |||

| Other Cable Types | |||

| By Fiber Mode | Single-Mode Fiber | ||

| Multimode Fiber | |||

| Plastic Optical Fiber | |||

| By Installation Type | Underground and Buried | ||

| Aerial and Overhead | |||

| Submarine and Under-Water | |||

| Tunnel and Bridge Integrated Deployments | |||

| By Application | Roadside Communications and V2X Backhaul | ||

| Traffic Monitoring and Incident Management | |||

| Smart Tolling and Revenue Collection | |||

| Autonomous Vehicle Support Corridors | |||

| Environmental Monitoring and Weather Sensing | |||

| By End User | Government and Transport Authorities | ||

| Private Highway Operators | |||

| Logistics and Fleet Operators | |||

| Automotive OEMs and Mobility Ecosystem Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the fiber optic cable market for smart highways and autonomous vehicle infrastructure?

The fiber optic cable market for smart highways and autonomous vehicle infrastructure stood at USD 1.85 billion in 2026 and is forecast to reach USD 6.54 billion by 2031 at a 28.73% CAGR.

Which cable type leads deployments on smart highways?

Non-Armored Cable led in 2025 with a 31.72% share because many projects use conduit that already provides the main physical protection.

Why is single-mode fiber dominant on highway corridors?

Single-Mode Fiber held 53.34% share in 2025 because long inter-city routes need lower attenuation and more stable long-distance transmission.

What is the main application for highway fiber networks today?

V2X Backhaul was the largest application in 2025 with a 35.98% share, reflecting its central role in linking roadside units and traffic systems to control centers.

Which buyer group is growing the fastest?

Logistics and Fleet Operators are projected to post the fastest growth through 2031 at a 29.03% CAGR as autonomous freight corridors move closer to practical deployment.

Which region is expanding the fastest?

Asia Pacific is projected to grow at a 28.76% CAGR through 2031, supported by large-scale road digitization activity in countries such as India and ongoing autonomous driving trials in Japan.

Page last updated on: