Size and Share of Fiber Optic Cable Market For Railway and Metro Infrastructure

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

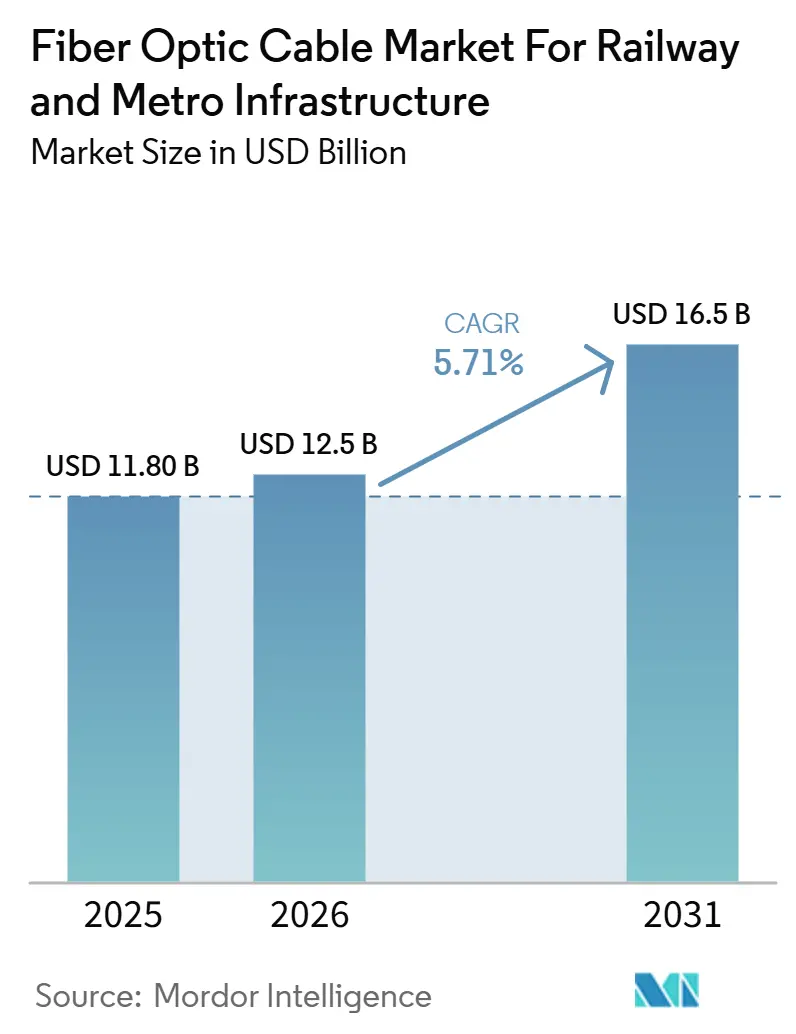

| Market Size (2026) | USD 12.5 Billion |

| Market Size (2031) | USD 16.5 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

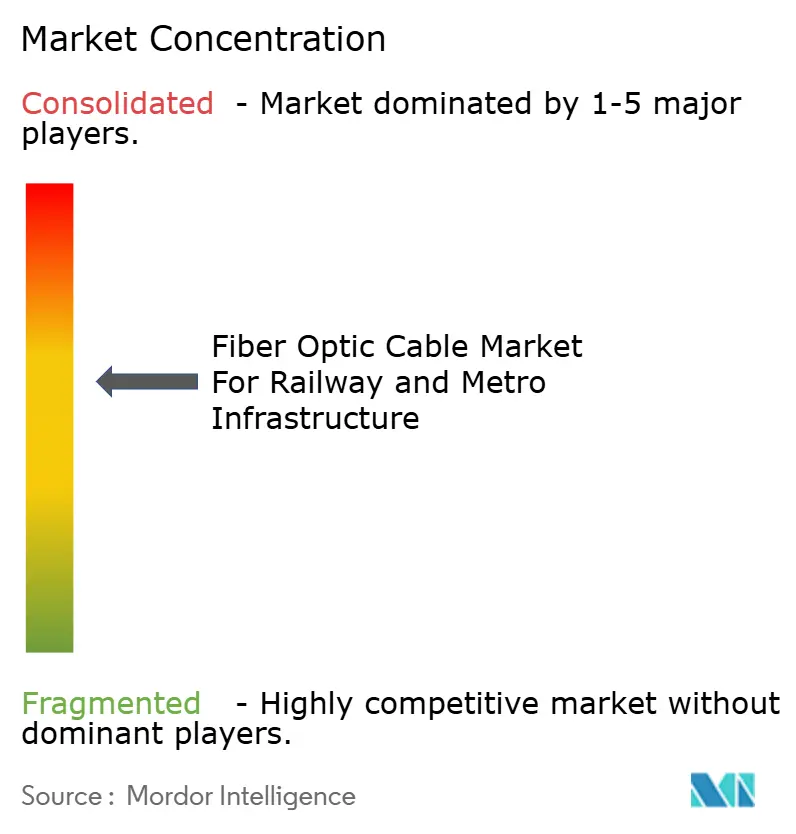

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Fiber Optic Cable Market For Railway and Metro Infrastructure by Mordor Intelligence

The fiber optic cable market for railway and metro infrastructure industry size is expected to increase from USD 11.8 billion in 2025 to USD 12.50 billion in 2026 and reach USD 16.50 billion by 2031, growing at a CAGR of 5.71% over 2026-2031. Growth in the market is tied to the same structural shift seen across modern rail systems, where network expansion now moves together with heavier spending on digital signaling, passenger communication, and control networks that need higher bandwidth and stronger immunity to electromagnetic interference than copper can usually deliver. The demand profile is also changing because each new metro corridor needs far more than route-side cable, as operators now build fiber rings for control centers, communication layers for stations and depots, and resilient links for public information and safety systems across the same project footprint. The fiber optic cable market for railway and metro infrastructure is also being shaped by a clear specification shift, with new rail projects favoring fiber for command, control, and monitoring functions while legacy corridors continue to sustain demand for copper communication cable and armored products in selected use cases. Regional momentum remains uneven, with North America supported by corridor modernization and public funding cycles, while Asia-Pacific continues to draw growth from new urban rail construction and large railway digitalization programs. Competition in the market remains centered on certification depth, supply security, and technical support capacity, and that gives an edge to suppliers with integrated production, railway-grade product portfolios, and the ability to manage longer lead times in a tighter global fiber supply environment.

Key Report Takeaways

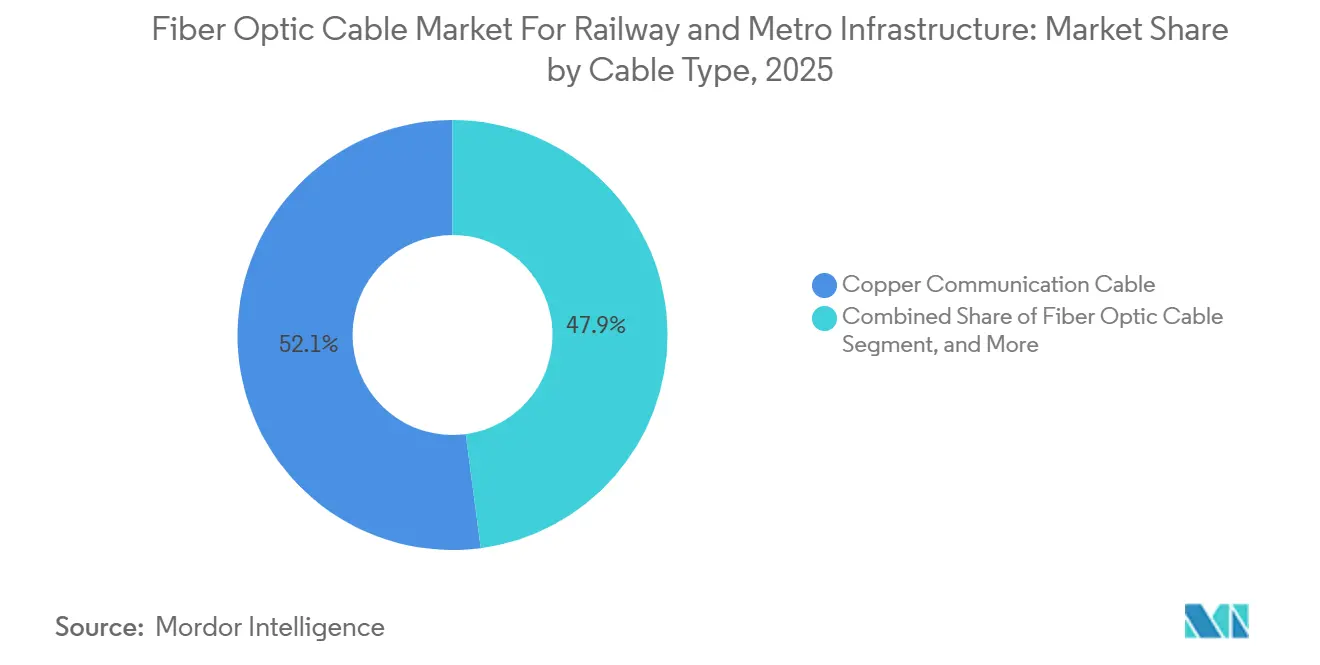

- By cable type, copper communication cable held a 52.10% share in 2025 across the fiber optic cable market for railway and metro infrastructure, while fiber-optic cable is projected to record the fastest 6.12% CAGR through 2031.

- By application, signaling systems accounted for 45.67% share in 2025, while communication networks are expected to expand at the fastest 5.43% CAGR through 2031.

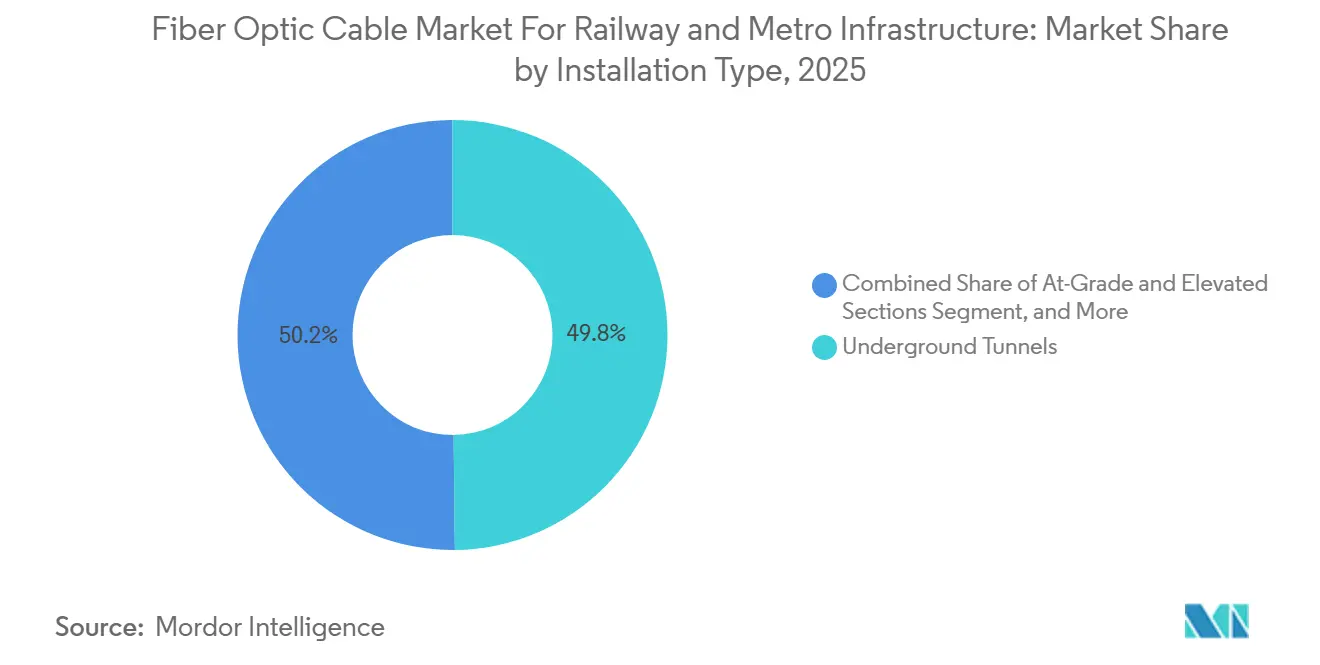

- By installation type, underground tunnels represented 49.82% share in 2025, while station and depot infrastructure is projected to advance at a 5.69% CAGR through 2031.

- By end user, metro operators captured 32.14% share in 2025, while system contractors and EPC firms are projected to post the fastest 5.12% CAGR through 2031.

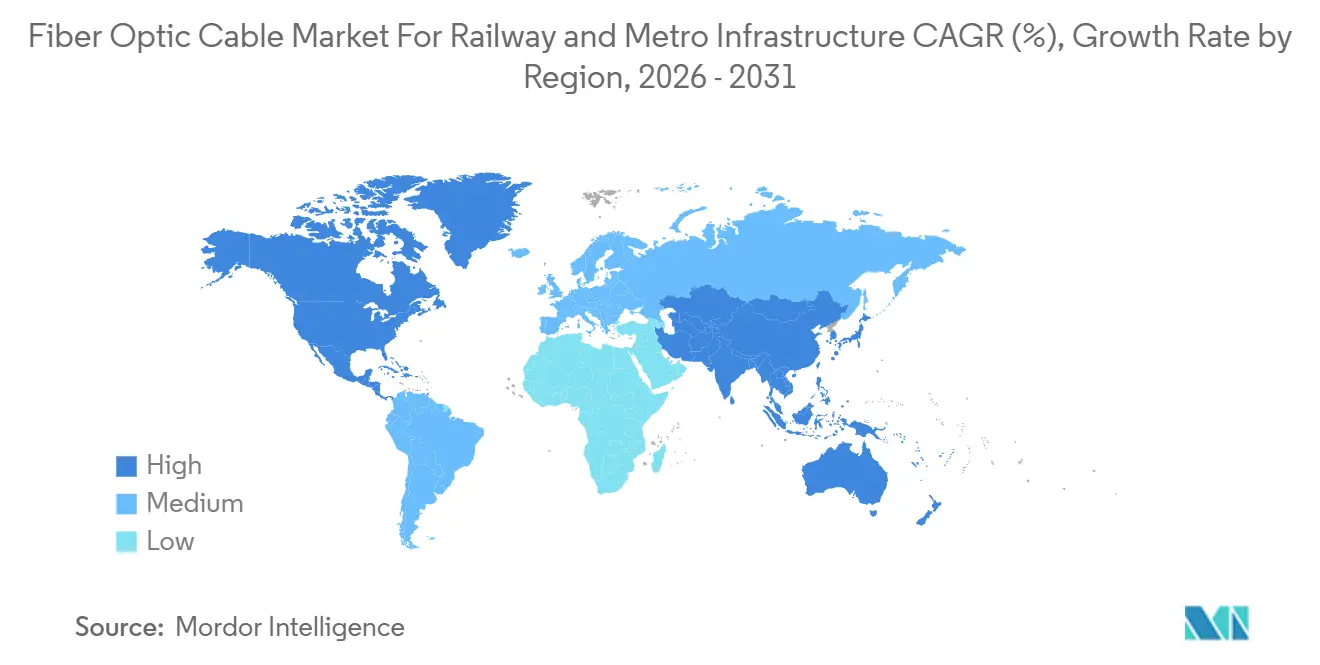

- By geography, North America held 33.56% share in 2025, while Asia-Pacific is expected to deliver the fastest 6.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Fiber Optic Cable Market For Railway and Metro Infrastructure

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urbanization And Metro Network Expansion | +2.1% | Global, concentrated in Asia-Pacific, South America, and Middle East | Medium term (2-4 years) |

| Digital Signaling Adoption Requiring Dense Fiber Backbones | +1.5% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Higher Bandwidth Demands From Data-Intensive Rail Operations | +1.2% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Fire Safety Standards Mandating Low-Smoke, Halogen-Free Cable Specifications | +0.8% | Europe, Asia-Pacific, North America | Short term (≤ 2 years) |

| Fiber Embedment In Rail Infrastructure For Structural Sensing And Condition Monitoring | +0.6% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Hybrid Route Fiber Integration Across Mixed Copper-Fiber Corridor Architectures | +0.4% | North America, South America, India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization And Metro Network Expansion

Urban transit expansion remains the largest volume driver of the fiber optic cable market for railway and metro infrastructure, as every new metro line now carries a large communication and control layer alongside civil construction. The cable requirement no longer stops at route alignment, since operators also need fiber networks for operations control centers, platform systems, depots, emergency communication, and station connectivity across the same project. That makes revenue per route kilometer higher than in older rail programs, where cable scope was narrower and much of the installed base remained tied to simpler signaling or voice networks. The effect is strongest in greenfield metro systems, where designers can specify a fiber-first architecture from the start rather than preserving mixed legacy systems that slow procurement and complicate performance standards. The fiber-optic cable market for railway and metro infrastructure also benefits, as metro expansion typically occurs in phases, meaning an initial cable order for one corridor often extends into later packages for stations, depots, interchanges, and control-room upgrades. This creates a steadier demand cycle for railway-grade cable suppliers than one-time track construction alone would suggest.

Digital Signaling Adoption Requiring Dense Fiber Backbones

The shift toward digital signaling has become one of the most durable demand supports for the fiber optic cable market for railway and metro infrastructure market because high-frequency train control depends on stable, low-latency, and interference-resistant communication links. Operators moving from conventional fixed-block systems to CBTC and ETCS architectures are not simply replacing signaling equipment; they are also rebuilding the communications backbone that supports train movement authority, supervision, diagnostics, and system resilience. This is evident in major signaling deployments where the control platform and the transmission layer are designed together, as in Hitachi Rail’s Taipei-Keelung Metropolitan MRT contract in 2025, which combined advanced signaling, telemetry, and cloud-linked operational functions that require dense fiber connectivity between trains, stations, and supervision nodes.[1]Hitachi Ltd., “Hitachi Rail Awarded Contract To Deliver Advanced Signalling And SCADA Solutions In Taipei Keelung Metropolitan MRT,” Hitachi The same pattern appeared in Australia when Alstom placed the Melbourne Metro Tunnel brownfield CBTC installation into passenger service in December 2025, reinforcing the role of fiber-intensive signaling architecture in capacity upgrades on active urban systems.[2]Alstom, “Alstom Delivers Australia’s First Brownfield CBTC Installation For Melbourne’s Metro Tunnel Project,” Alstom The fiber optic cable market for railway and metro infrastructure, therefore, gains not only from new lines but also from signal modernization on existing lines, where service frequency, safety, and real-time control requirements continue to rise. Even where wireless layers are introduced for train communication, the need for high-capacity fiber backhaul at trackside and station level remains intact.

Higher Bandwidth Demands From Data-Intensive Rail Operations

The fiber optic cable market for railway and metro infrastructure is also moving with wider changes in railway operations, where video surveillance, passenger information, predictive maintenance, and asset monitoring generate far more traffic than older transport networks were designed to handle. Rail operators now treat the communication backbone as a continuous operating layer rather than a support utility, because service reliability depends on stable data transmission between trains, stations, depots, and centralized management systems. This shift is visible in corridor upgrades such as the New Haven Line communications modernization, where legacy copper circuits were replaced with fiber across all 22 stations to support signaling, train control, and passenger information functions on a heavily used commuter route. The same direction is evident in the United Kingdom, where Project Reach was launched to deploy a large ultra-fast fiber network along major rail corridors and to reserve part of that capacity for operational rail use.[3]Government of the United Kingdom, “On Track And Online, Landmark Deal To End Mobile Dead Zones,” GOV.UK In the fiber optic cable market for railway and metro infrastructure, this means bandwidth growth is no longer tied solely to route additions, as installed networks are also being deepened to handle richer data loads on existing systems. It also raises the value of higher-count cables, resilient network design, and products that can support future overlay applications without repeated civil intervention.

Fire Safety Standards Mandating Low-Smoke, Halogen-Free Cable Specifications

Compliance requirements are driving up specification quality in fiber-optic cable for the railway and metro infrastructure market, as tunnel, rolling stock, and enclosed-station environments now place greater emphasis on flame resistance, smoke behavior, and toxic emission performance. The June 2025 publication of IEC 60332-1-2 reinforced the test framework used for electrical and optical fiber cables under fire conditions, and this continues to affect how suppliers position railway-grade cable portfolios for tender participation. In practice, that shifts procurement away from lower-grade products and toward LSZH and other certified formulations that can more consistently clear railway approval processes. The effect is not limited to Europe, as suppliers serving Asia-Pacific and North American metro systems also face tighter customer expectations for pre-validated compliance with fire behavior and operating safety. The fiber optic cable market for railway and metro infrastructure, therefore, sees a faster mix shift than volume growth alone would imply, as more tenders specify premium cable classes rather than leaving material formulation open to supplier choice. This improves pricing potential in compliant product categories, while narrowing the commercial space for products that cannot demonstrate railway-grade testing depth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Civil Infrastructure And Trenching Costs For Underground Cable Installation | -0.5% | Global, most pronounced in dense urban European and East Asian markets | Medium term (2-4 years) |

| Long Certification And Type-Testing Cycles For Railway-Grade Cable Products | -0.4% | Europe, North America, and markets with multi-standard compliance requirements | Short term (≤ 2 years) |

| Copper And Legacy Infrastructure Competition Slowing Fiber Migration Timelines | -0.3% | South America, Middle East and Africa, parts of Asia-Pacific | Medium term (2-4 years) |

| Skilled Labor Shortage For Specialized Railway Cable Installation And Splicing | -0.2% | Global, most acute in Sub-Saharan Africa, South Asia, and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Civil Infrastructure And Trenching Costs For Underground Cable Installation

Underground installation remains one of the most persistent barriers to faster adoption of fiber optic cable market for railway and metro infrastructure markets because trenching, ducting, drilling, traffic management, and restoration often cost more than the cable hardware itself. This burden is particularly strong in dense urban settings where construction windows are short, utility congestion is high, and surface disruption carries both financial and political costs for project owners. Even where the long-term operating case for fiber is clear, near-term procurement can still be delayed if route design requires complex civil packages before the cable network can be installed. The issue also affects retrofit programs more than greenfield corridors, because legacy rail systems must fit new cable pathways into built environments that were never designed for modern communication loads. In the fiber optic cable market for railway and metro infrastructure, this means project timing is often shaped as much by civil readiness as by cable availability or equipment specifications. Suppliers with products suited to hybrid deployment models, existing ducts, or staged corridor upgrades are therefore better placed to help operators reduce upfront disruption.

Long Certification And Type-Testing Cycles For Railway-Grade Cable Products

Certification timelines slow the pace of change in the fiber-optic cable market for railway and metro infrastructure, as railway buyers rarely accept new cable designs without extensive testing against fire, safety, durability, and application-specific standards. IEC 60332-1-2 remains a benchmark in this process, and its 2025 edition underscores how formal test compliance continues to shape which products can enter approved railway procurement channels. Suppliers serving multiple regions also face overlapping requirements, which raises testing cost, documentation complexity, and the time needed to commercialize even technically attractive product improvements. That dynamic favors larger, integrated manufacturers that can fund repeated certification programs and maintain broader approval portfolios across metro, mainline, and rolling stock applications. In the fiber-optic cable market for railway and metro infrastructure, the result is slower adoption of new cable formulations and a higher barrier to entry for smaller entrants with capable products but limited certification capacity. It also means railway operators often stay with familiar approved vendors when project schedules leave little room for qualification risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable: Fiber Optic Uptake Reshapes A Copper-Led Market

Copper communication cable held 52.10% of the fiber-optic cable market share for railway and metro infrastructure in 2025, reflecting its continued role in legacy signaling environments, its lower per-meter cost, and its broad availability across rail projects that still use established communication layouts. The category remains relevant because many rail systems do not replace their entire communication architecture at once, and that keeps copper in service across retrofit work, lower-bandwidth functions, and corridors where procurement budgets remain tightly controlled. Even so, the fiber-optic cable market for railway and metro infrastructure is steadily shifting away from copper in performance-critical use cases, especially in energized rail environments where electromagnetic interference is a recurring operational concern. Fiber products address that exposure more effectively, which is why new-build metro systems increasingly specify fiber for backbone communication and command functions instead of treating it as an optional upgrade path. Armored rail cable continues to hold a complementary position in the fiber optic cable for the railway and metro infrastructure industry, since mechanically exposed sections still need protection features that track closely with greenfield construction and route conditions.

Fiber optic cable is projected to expand at a 6.12% CAGR through 2031, and that makes it the fastest-moving category within the fiber optic cable market for railway and metro infrastructure industry as signaling migration, surveillance needs, and wider data traffic reshape procurement priorities. The category also benefits from the way national rail projects are being designed for long-lived communication capacity, as seen in Project Reach in the United Kingdom, where Network Rail, Neos Networks, and Freshwave launched a 1,000 km ultra-fast fiber rollout with operational rail use embedded in the architecture from the outset. That kind of specification signals a move toward higher-capacity corridor design, where operators size fiber networks not only for current control and communication tasks but also for future commercial, operational, and digital service layers. Compliance pressure adds another tailwind because certified LSZH fiber variants are becoming the safer procurement choice in enclosed and high-criticality rail settings, especially as the fiber optic cable for railway and metro infrastructure market places more weight on tested performance rather than nominal specification alignment alone.

By Application: Signaling Systems Anchor Demand While Communication Networks Gain Pace

Communication networks are projected to grow at a 5.43% CAGR through 2031, reflecting the fiber-optic cable market for railway and metro infrastructure moving toward dedicated, high-capacity transmission layers that connect stations, depots, operations centers, and route-side assets in real time. Demand in this segment is tied to a broader move toward IP-based architecture, where voice, data, video, and supervisory traffic increasingly share resilient backbone infrastructure rather than relying on isolated, lower-capacity legacy systems. Passenger information systems also form an expanding demand base because real-time displays, onboard connectivity, and dynamic operational messaging all rely on stable, low-latency links to centralized data environments. The others category remains smaller, but it covers technical use cases such as traction power monitoring and industrial Ethernet connections that can still carry strict performance and reliability requirements in active rail environments. Taken together, these shifts show how the fiber-optic cable market for railway and metro infrastructure is expanding beyond train control alone and becoming more closely linked to the full operating technology layer of rail networks.

Signaling systems accounted for 45.67% of the fiber optic cable market for railway and metro infrastructure industry size in 2025, and that lead position reflects their status as the highest-criticality application across metro and railway infrastructure. In this application, buyers focus less on cable unit price and more on network availability, because a communication failure inside a signaling loop can affect service continuity across multiple stations or an entire corridor. That is why operators increasingly specify dual-path or otherwise resilient fiber architectures in the fiber optic cable market for railway and metro infrastructure market, using redundant route design to preserve network uptime when one path is compromised. The category also benefits from new signaling contracts that combine telemetry, analytics, and control functions, such as Hitachi Rail’s 2025 Taipei-Keelung Metropolitan MRT award, which pointed to a deeper and denser communications requirement than conventional signal replacement programs usually carried.

By Installation Type: Tunnel Volume Leads While Station And Depot Work Accelerates

Station and depot infrastructure is projected to advance at a 5.69% CAGR through 2031, indicating that the fiber-optic cable market for railway and metro infrastructure is not driven solely by line-side installations but also by the growing technical complexity of station and maintenance environments. Each new station fit-out requires communication layers across concourse, platform, equipment rooms, access control, and public information functions, while depots increasingly need digital links for diagnostics, monitoring, and operational coordination. This creates a broad installation base that extends beyond the route itself and often arrives in later project packages, giving the market an additional source of follow-on demand after core civil works move forward. At-grade and elevated track installations remain important for suburban rail and light rail systems, which benefit from easier access and lower civil costs than tunnel-heavy urban alignments. Hybrid corridors also matter in the fiber-optic cable market for railway and metro infrastructure because extensions that move from dense city cores to open suburban sections require careful transitions between tunnel-grade, outdoor, and armored cable specifications at multiple interface points.

Underground tunnels accounted for 49.82% of the fiber optic cable market for railway and metro infrastructure industry size in 2025, which reflects both the physical volume of cable installed in enclosed networks and the higher specification level demanded by tunnel environments. Tunnel sections need LSZH performance, stronger mechanical protection, dense splice management, and dependable enclosures, which raises both technical complexity and average value per installed route segment. The direction of future tunnel specifications can already be seen in the Lisbon Metro LUMIRing project, where a multicore fiber terrestrial testbed was deployed under live operating conditions to validate next-generation optical cable performance in a real underground environment. For the fiber optic cable market for railway and metro infrastructure industry, that matters because operators building tunnel assets for decades of service increasingly want cable systems that can carry more data in the same duct space while standing up to vibration, humidity, and thermal stress.

By End User: Metro Operators Lead While EPC Contractors Drive Contract Growth

System contractors and EPC firms are projected to record the fastest 5.12% CAGR through 2031, indicating that the fiber optic cable market for railway and metro infrastructure is seeing procurement authority move steadily toward turnkey project structures. In these models, the contractor often controls cable specification, sourcing, installation planning, and coordination with signaling and communications packages, giving large project integrators greater influence over product selection than in older authority-led procurement formats. This shift matters commercially because suppliers that secure preferred status with EPC groups can gain access to a wider project scope early in the build cycle, rather than competing only at later material purchase stages. It also rewards manufacturers that can support design coordination, approval paperwork, and on-site execution rather than simply offering compliant cable products. Rolling stock integrators remain a smaller part of the fiber-optic cable market for railway and metro infrastructure, but they still represent a specialized demand pool for onboard communication harnesses and fire-compliant cable assemblies linked to trainset procurement cycles.

Metro operators held 32.14% share in 2025, underscoring the fact that the fiber optic cable market for railway and metro infrastructure is still anchored by the scale, density, and recurring upgrade needs of urban transit networks. Their demand is recurring rather than one-time, because expansion projects, replacement cycles, signaling upgrades, and station technology refreshes continue to generate procurement even after the original line enters operation. Railway infrastructure authorities represent the next large demand center, especially where national digitalization, safety compliance, and network harmonization programs require multi-year communication upgrades across long corridors. In the fiber optic cable market for railway and metro infrastructure industry, suppliers with a strong certification base and long program support capability are better aligned with these end users, since they can serve both immediate installation needs and the longer operating life expected from railway communications assets.

Geography Analysis

North America held 33.56% of the fiber optic cable market for railway and metro infrastructure industry share in 2025, and that lead position reflected the region’s steady corridor modernization cycle, commuter rail communication upgrades, and institutional support for high-reliability operating networks. The region continues to generate demand from projects that replace legacy communication links with fiber for signaling, train control, and passenger information, which keeps retrofit activity commercially important alongside new transit work. This was visible on Metro-North’s New Haven Line, where a multi-phase upgrade replaced older copper circuits with fiber across all 22 stations and strengthened the communications base for control and passenger systems. The fiber-optic cable market for railway and metro infrastructure in North America also benefits from the fact that operators often extend modernization over several phases, which smooths demand rather than concentrating it in a single procurement cycle. South America remains smaller, but the region still adds relevance through metro expansions, commuter rail electrification, and communications upgrades that gradually expand the installed base for railway-grade fiber solutions.

Europe remains one of the most specification-driven parts of the fiber optic cable market for railway and metro infrastructure industry because procurement is closely tied to ETCS rollout, network reliability targets, and strict fire safety expectations. The United Kingdom’s Project Reach is a strong example of this direction, with a large national rail fiber rollout designed to improve connectivity along major corridors while preserving operational capacity for rail use within the same infrastructure. Cross-border projects are also relevant, as Rail Baltica moved forward with fiber-related duct supply awards that show how large regional rail builds create layered demand beyond track and civil packages alone.[4]Estonian Public Broadcasting, “Estonian Firms Win Tender To Supply Rail Baltica With Fiber Optic Cabling Ducts,” ERR The Middle East is following a different pattern, where greenfield metro development is setting up a longer future procurement cycle for tunnel-grade, armored, and communications cable across large urban rail systems.

Asia-Pacific is projected to grow at a 6.43% CAGR through 2031, giving it the fastest regional trajectory in the fiber optic cable market for railway and metro infrastructure as urban transit buildout and railway digitalization move in parallel. The region’s demand base is broad, since it spans dense metro development, new signaling deployment, national telecom upgrades inside railway systems, and a stronger preference for turnkey execution on major transport programs. In India, the Ministry of Railways approved a July 2026 project to deploy 48-fiber OFC across 1,696.2 route km on South Eastern Railway, reinforcing the scale at which public rail systems in the region are building higher-bandwidth communication backbones. The region also continues to influence future specification direction for the fiber optic cable for railway and metro infrastructure market through signaling-led upgrades such as Hitachi Rail’s Taipei-Keelung MRT program and through capacity-oriented operating models such as Alstom’s CBTC activation in Melbourne.

Competitive Landscape

The fiber-optic cable market for railway and metro infrastructure remains moderately concentrated, with Prysmian Group, Nexans S.A., Sumitomo Electric Inc., Furukawa Electric Co., and LS Cable and System forming the core group of large suppliers with broad manufacturing depth and established credibility in rail-grade applications. Their competitive position rests less on simple unit pricing and more on the ability to offer compliant product portfolios, familiarity with railway approvals, dependable delivery, and technical support across signaling, communication, tunnel, and station installations. The fiber-optic cable market for railway and metro infrastructure also rewards suppliers that control more of the production chain, as tighter global fiber supply conditions have increased the value of captive capacity, better planning visibility, and stronger resilience against input disruptions. Regional challengers such as Hengtong Group, KEI Industries, Polycab India, Riyadh Cables Group, and ACOME are gaining traction where localization, domestic access, or regional project familiarity matters more than global footprint alone. This leaves the market competitive but not fragmented, because large approved vendors still hold the strongest position when rail buyers prioritize certification depth and operational reliability over price alone.

The next layer of competition in the fiber optic cable market for railway and metro infrastructure market is forming around specialized solutions rather than basic cable supply, especially in cybersecure rail communication architectures and self-diagnostic cable systems that can help operators monitor network integrity on live corridors. The LUMIRing testbed in Lisbon matters in this context because it places multicore fiber under real tunnel operating conditions and could influence how future metro projects think about duct efficiency, capacity scaling, and long-life communication design. At the same time, certification continues to act as a practical barrier to entry, since products still need documented compliance under formal fire and performance test regimes before they can move into railway approval pipelines. The fiber optic cable for railway and metro infrastructure market therefore gives an advantage to suppliers that combine product innovation with fast and repeatable qualification capacity, rather than relying on technical novelty alone.

Strategic moves in the wider competitive field show how demand is increasingly tied to integrated rail communications programs rather than isolated cable purchases. In June 2025, Network Rail, Neos Networks, and Freshwave launched Project Reach to deploy 1,000 km of ultra-fast fiber along major UK rail corridors, with part of the network reserved for operational rail use and the balance opened to commercial deployment, a structure that may influence other corridor modernization programs. In July 2025, Hitachi Rail secured the Taipei-Keelung Metropolitan MRT contract for advanced signaling and SCADA functions, reinforcing the link between signaling awards and higher-performance station-to-train fiber requirements. In December 2025, Alstom brought Australia’s first brownfield CBTC installation into passenger service on the Melbourne Metro Tunnel program, showing how major signaling suppliers continue to shape future cable specification and communication architecture choices across active urban rail networks.

Leaders of Fiber Optic Cable Market For Railway and Metro Infrastructure

Prysmian Group

Nexans S.A.

Sumitomo Electric Industries, Ltd.

LS Cable & System Ltd.

Furukawa Electric Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Ministry of Railways, Government of India, approved an INR 200 crore (USD 24 million) project to deploy 48-fiber OFC across 1,696.2 route km spanning all four divisions of South Eastern Railway, establishing a high-bandwidth, redundant fiber backbone to support next-generation signaling and operational data transmission systems.

- December 2025: Alstom delivered Australia's first brownfield CBTC installation for Melbourne's Metro Tunnel Project, with its Urbalis Flo system entering passenger service on December 1, 2025, enabling reduced headways and higher service frequency and establishing the fiber-intensive CBTC architecture that Sydney and Perth networks are expected to adopt.

- July 2025: Hitachi Rail secured a contract to deploy SelTrac CBTC with private, cloud-based signaling and advanced telemetry for the Taipei-Keelung Metropolitan MRT, incorporating data analytics features that require dense fiber-optic cable infrastructure between stations, trains, and cloud supervision systems.

- June 2025: Network Rail, Neos Networks, and Freshwave signed Project Reach, deploying 1,000 km of ultra-fast fiber optic cable along the East Coast Main Line, West Coast Main Line, and Great Western Main Line, with an ambition to expand to 5,000 km nationally, while Network Rail retains half the fiber capacity for operational use and Neos Networks commercializes the remainder.

Scope of Report on Fiber Optic Cable Market For Railway and Metro Infrastructure

The Fiber Optic Cable Market for Railway and Metro Infrastructure Industry Report is Segmented by Cable Type (Fiber Optic Cable, Hybrid Fiber Copper Cable, Copper Communication Cable, and Armored Rail Cable), Application (Signaling Systems, Communication Networks, Passenger Information and Surveillance Systems, and Other Applications), Installation Type (Underground Tunnels, At-Grade and Elevated Tracks, Station and Depot Infrastructure, and Hybrid Corridor Deployments), End User (Metro Operators, Railway Infrastructure Authorities, Rolling Stock Integrators, and System Contractors and EPC Firms), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fiber Optic Cable |

| Hybrid Fiber Copper Cable |

| Copper Communication Cable |

| Armored Rail Cable |

| Signaling Systems |

| Communication Networks |

| Passenger Information and Surveillance Systems |

| Other Applications |

| Underground Tunnels |

| At-Grade and Elevated Sections |

| Station and Depot Infrastructure |

| Hybrid Corridor Deployments |

| Metro Operators |

| Railway Infrastructure Owners |

| Rolling Stock Integrators |

| System Contractors and EPC Firms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Cable Type | Fiber Optic Cable | ||

| Hybrid Fiber Copper Cable | |||

| Copper Communication Cable | |||

| Armored Rail Cable | |||

| By Application | Signaling Systems | ||

| Communication Networks | |||

| Passenger Information and Surveillance Systems | |||

| Other Applications | |||

| By Installation Type | Underground Tunnels | ||

| At-Grade and Elevated Sections | |||

| Station and Depot Infrastructure | |||

| Hybrid Corridor Deployments | |||

| By End User | Metro Operators | ||

| Railway Infrastructure Owners | |||

| Rolling Stock Integrators | |||

| System Contractors and EPC Firms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the fiber optic cable market for railway and metro infrastructure space?

The fiber optic cable market for railway and metro infrastructure industry report states that the market size stood at USD 11.8 billion in 2025, reached USD 12.50 billion in 2026, and is forecast to reach USD 16.50 billion by 2031 at a 5.71% CAGR.

Which cable type is growing the fastest in rail and metro communication networks?

Fiber optic cable is projected to post the fastest 6.12% CAGR through 2031, while copper communication cable still held the largest 52.10% share in 2025.

Why do signaling systems account for the largest application demand?

Signaling systems held 45.67% share in 2025 because train control requires the highest level of communication reliability, redundancy, and availability across metro and railway corridors.

Which installation environment creates the biggest cable demand?

Underground tunnels led with 49.82% share in 2025 because enclosed rail environments require more cable volume and higher-specification products such as LSZH and protected assemblies.

Which end users are driving the fastest contract growth?

System contractors and EPC firms are projected to grow the fastest at 5.12% CAGR through 2031 as turnkey delivery models give them more control over cable specification and sourcing.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to expand at a 6.43% CAGR through 2031, supported by ongoing metro buildout, signaling upgrades, and railway digitalization programs across major regional markets.

Page last updated on: