Fiber Mobile Backhaul System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.65 Billion |

| Market Size (2031) | USD 25.13 Billion |

| Growth Rate (2026 - 2031) | 11.40% CAGR |

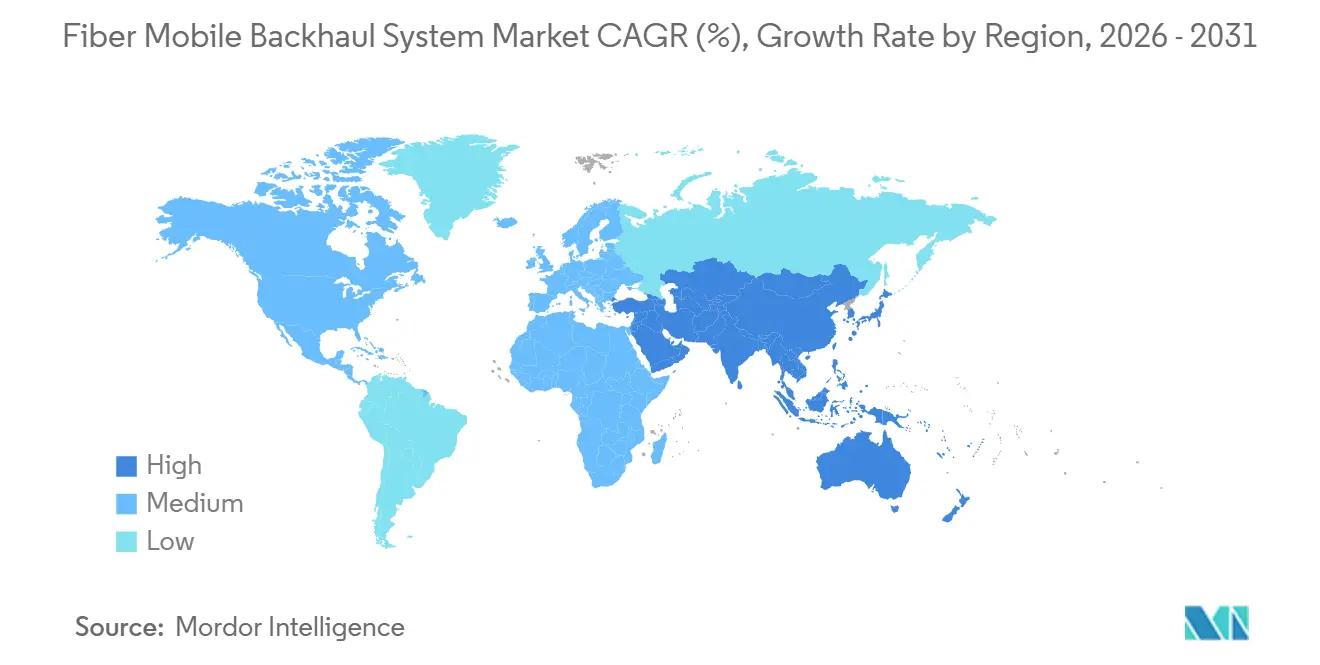

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

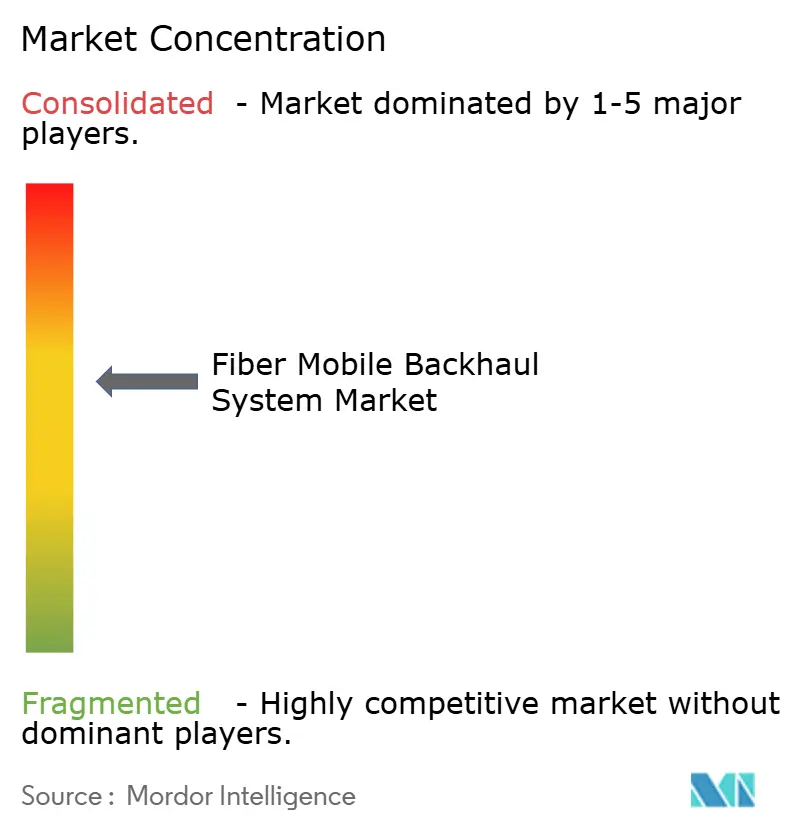

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Mobile Backhaul System Market Analysis by Mordor Intelligence

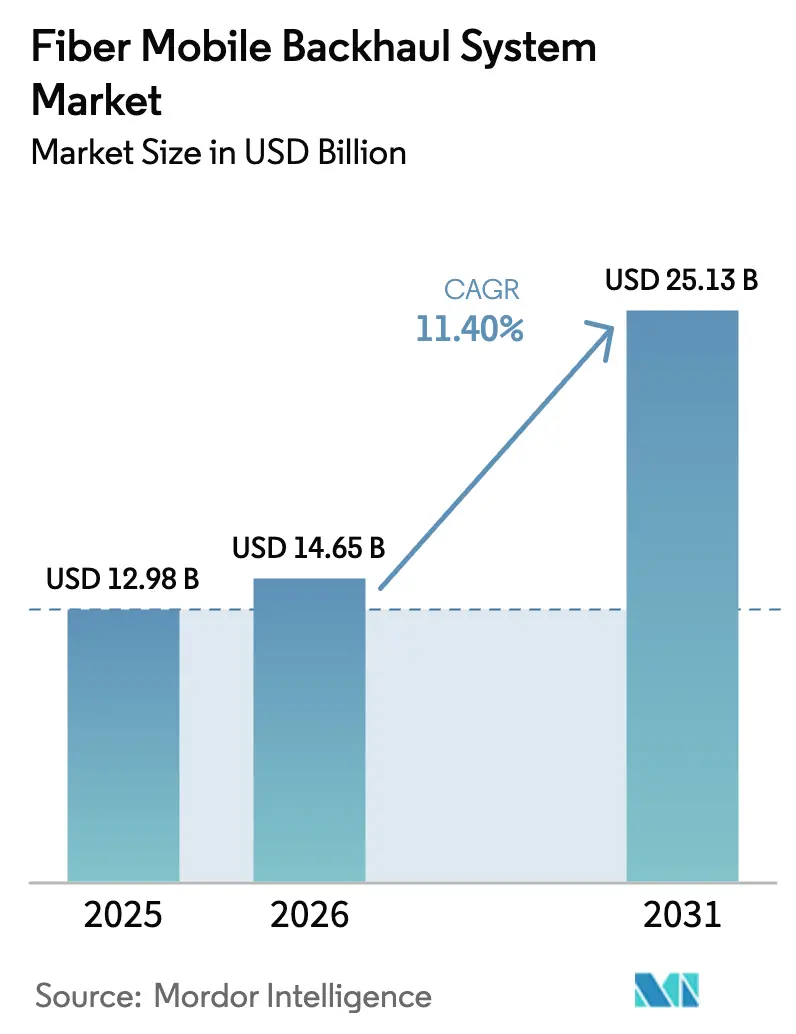

The Fiber Mobile Backhaul System Market size is projected to expand from USD 12.98 billion in 2025 and USD 14.65 billion in 2026 to USD 25.13 billion by 2031, registering a CAGR of 11.40% between 2026 to 2031. Momentum is accelerating because operators are upgrading constrained microwave links to fiber routes that can aggregate multi-terabit traffic generated by dense 5G clusters. Asia-Pacific carriers now budget more for transport than for radio, a reversal of the 4G era, while North American tier-1s are standardizing 100 Gbps wavelengths for every new macro site. The fiber mobile backhaul system market is also being reshaped by coherent pluggable optics that merge IP and optical layers inside a single chassis, trimming power bills by more than half and shortening service-activation cycles to minutes. Tower companies and neutral-host providers are buying dark fiber directly, eroding incumbent vendors’ managed-service margins, and open transport specifications published by the Telecom Infra Project are accelerating multi-vendor deployments.

Key Report Takeaways

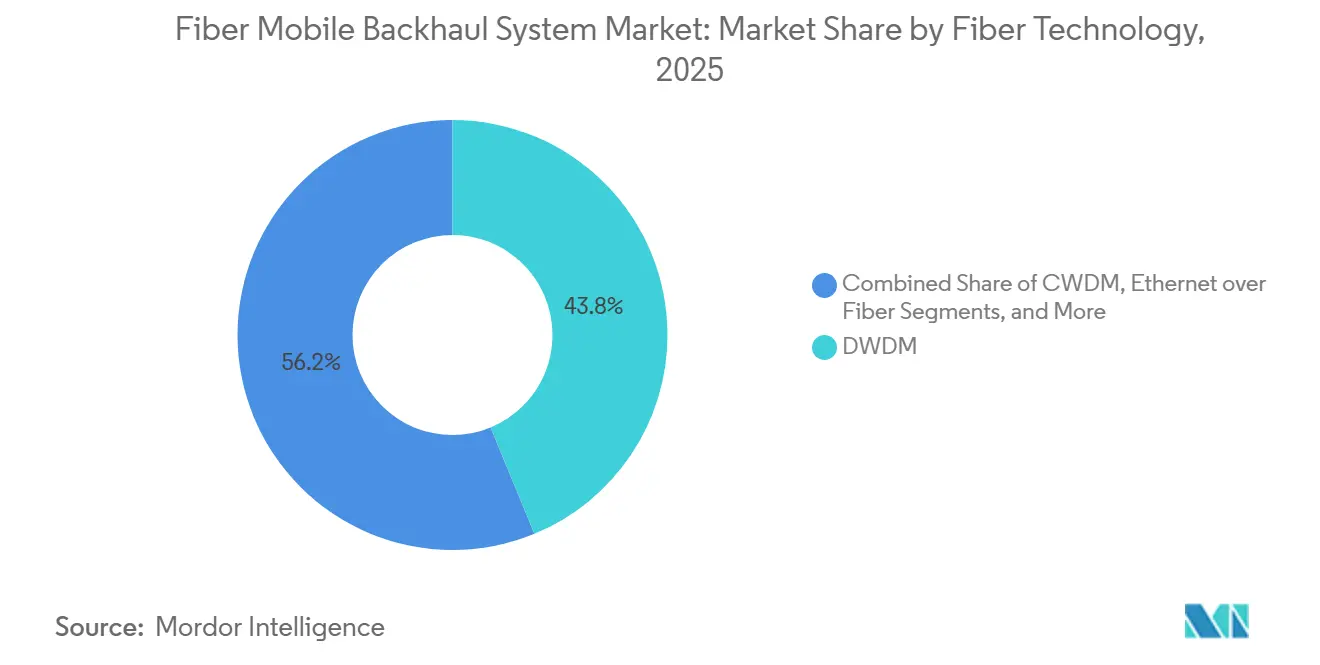

- By fiber technology, dense wavelength division multiplexing (DWDM) accounted for 43.78% of the fiber mobile backhaul system market share in 2025, while passive optical network (XGS-PON / NG-PON2) platforms are expanding at a 12.01% CAGR through 2031.

- By bandwidth capacity tier, links exceeding 100 Gbps are forecast to grow at 12.57% through 2031, outpacing the 25-100 Gbps segment, which led with a 32.49% market share in 2025.

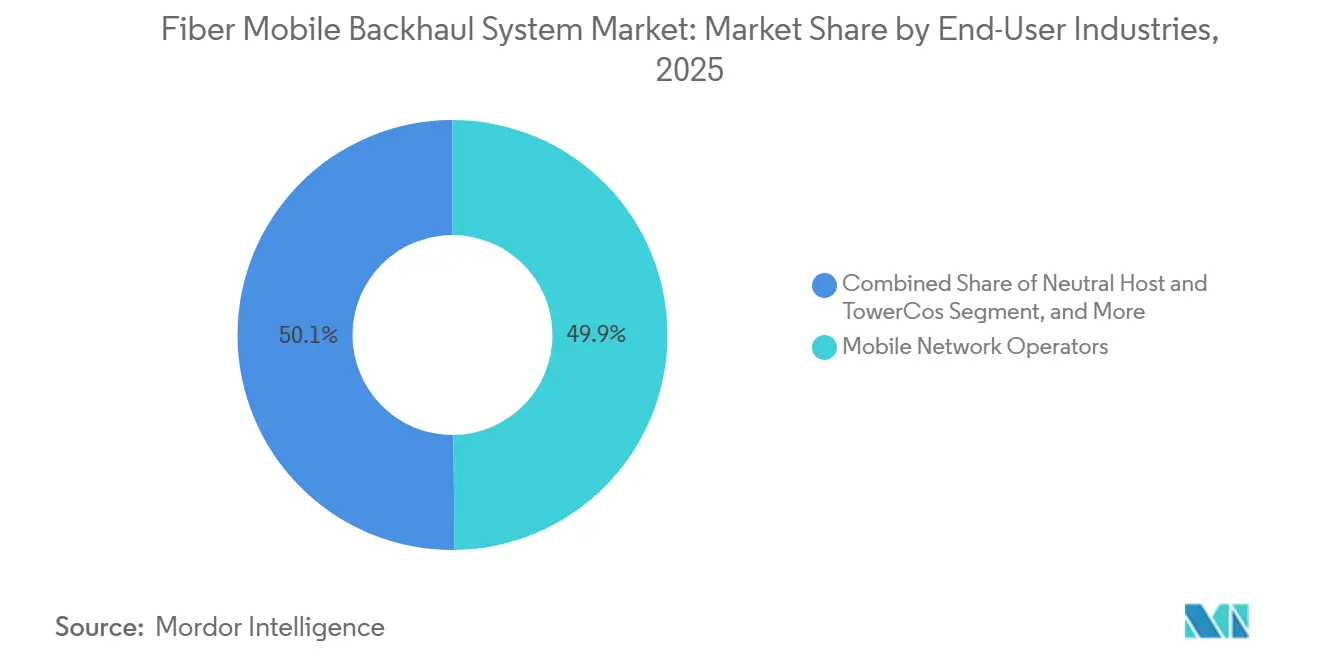

- By end-user industry, mobile network operators accounted for 49.85% of spending in 2025, while enterprises and private 5G networks are advancing at a 11.69% CAGR through 2031.

- By geography, the Asia-Pacific region accounted for 29.67% of the fiber mobile backhaul system market in 2025 and is expected to grow at 13.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fiber Mobile Backhaul System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Densification and Exponential Data Traffic Growth | +3.2% | Global, highest in Asia–Pacific and North American metros | Medium term (2-4 years) |

| Proliferation of Small-Cell and C-RAN Architectures | +2.1% | North America, Europe, tier-1 Asian cities | Medium term (2-4 years) |

| Government-Funded Rural Fiber Initiatives | +1.8% | U.S., EU, India | Long term (≥4 years) |

| Adoption of Coherent Pluggable Optics (400 G/800 G ZR/ZR+) | +2.4% | Early in North America and Europe, rising in Asia–Pacific | Short term (≤2 years) |

| Open and Disaggregated Transport Ecosystems (TIP OOPT, OpenZR+) | +1.3% | North America, Europe | Medium term (2-4 years) |

| Sustainability-Linked Financing Replacing Microwave with Energy-Efficient Fiber | +1.1% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

5G Densification and Exponential Data Traffic Growth

Mobile data traffic jumped 28% year-on-year in 2025, and 5G subscribers are already consuming a median of 42 GB monthly, triple the 4G baseline. Urban operators routinely deploy 8-12 small cells per city block, each demanding peak-hour throughput above 10 Gbps, a load that microwave cannot support once aggregate capacity tops 25 Gbps. Verizon reported 34% lower latency and 19% higher uplink throughput after migrating congested microwave links to fiber in dense metros. China Mobile earmarked USD 8.2 billion for fiber transport in its 2025 budget, reflecting the strategic primacy of backhaul within 5G economics. Operators now default to 100 Gbps wavelengths for new macro sites and plan to exceed 50 Gbps per site by 2028. Continuous traffic growth, therefore, locks in multi-year demand for the fiber mobile backhaul system market.

Adoption of Coherent Pluggable Optics (400G/800G ZR/ZR+)

Coherent pluggable transceivers, such as 400 G ZR and ZR+, reduce the cost and footprint of long-haul transport. Cisco’s Routed Optical Networking platforms recorded a 62% reduction in power consumption per transported terabit compared with separate transponders. The optics extend metro DWDM links by 120 km without amplification, eliminating regeneration sites and reducing right-of-way costs by roughly 30%. Juniper said 18% of its routers shipped in Q1 2026 already carry embedded ZR+ optics, up from 4% a year earlier. Lumentum shipped more than 50,000 coherent modules in Q4 2025 and faces a backlog into late 2026. These advances allow operators to converge IP and optical layers, automate wavelength activation in under 10 minutes, and scale capacity by swapping optics rather than overhauling shelves, a paradigm that sustains double-digit growth for the fiber mobile backhaul system market.

Proliferation of Small-Cell and C-RAN Architectures

Centralized RAN designs pool baseband resources but impose strict sub-1 ms fronthaul latency budgets that only fiber can guarantee. The ITU’s IMT-2020 framework limits timing error to 10 µs, effectively excluding microwave in C-RAN deployments. [1]International Telecommunication Union, “ITU-R M.2150,” ITU.INT Deutsche Telekom uses 25 Gbps Ethernet over fiber to connect up to 60 small cells per C-RAN hub, slashing the number of per-site fiber pairs by 75%. [2]Deutsche Telekom, “C-RAN Architecture Whitepaper 2025,” TELEKOM.COM The GSMA counted 1.8 million small-cell shipments in 2025, up 41% over 2024. [3]GSMA, “GSMA Intelligence Small-Cell Market Tracker 2025,” GSMA.COM Nokia won USD 340 million in neutral-host small-cell contracts in North America during 2025. Without low-latency fiber, the economic gains of C-RAN collapse, so each new hub adds incremental pull on the fiber-based mobile backhaul system market.

Government-Funded Rural Fiber Initiatives

Public programs are extending fiber into territories that once failed to clear commercial hurdle rates. The U.S. BEAD program released USD 6.8 billion in 2025 first-wave grants, including mandatory backhaul upgrades. [4]U.S. Department of Commerce, “BEAD Program State Allocations,” COMMERCE.GOV India’s BharatNet III aims to reach 250,000 villages with fiber capable of aggregating mobile traffic at regulated tariffs. The EU Gigabit Infrastructure Act cut permitting delays by an estimated 22% and lowered per-kilometer costs by up to EUR 18,000. Corning reported that government programs accounted for 27% of its 2025 optical-fiber sales. These subsidies de-risk investment, bringing fresh demand to the fiber mobile backhaul system industry in sparsely populated regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Right-of-Way Hurdles for Fiber Deployment | −1.9% | Global, acute in dense urban areas | Long term (≥4 years) |

| Terrain Constraints Favoring Wireless Alternatives in Remote Areas | −0.8% | Mountainous and archipelagic regions | Medium term (2-4 years) |

| Supply-Chain Volatility for Specialty Fiber and Coherent DSPs | −1.4% | Global, shortages worst in North America and Europe | Short term (≤2 years) |

| Escalating Cyber-Physical Threats to Critical Fiber Routes | −0.6% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Right-of-Way Hurdles for Fiber Deployment

Deploying urban fiber often costs USD 80,000-150,000 per route-kilometer, with permitting accounting for up to half of that total. Many U.S. cities levy linear-foot fees of USD 2.50-6.00 and require performance bonds of USD 500,000 or more before trenching, a burden that delays neutral-host builds. AT&T disclosed 24-month average approval cycles for tower-fiber projects in key states, forcing reliance on interim microwave links. Environmental reviews under national statutes can push timelines past 3 years, while an 18% rise in installation labor costs in 2025 squeezed project margins. Such frictions temper the otherwise robust expansion of the fiber mobile backhaul system market.

Supply-Chain Volatility for Specialty Fiber and Coherent DSPs

High-speed coherent DSP production is concentrated among three suppliers, and lead times lengthened to 42 weeks in Q1 2026 as carriers and hyperscalers vied for the same foundry slots. Infinera cut its H1 2026 shipment forecast by 12% because of DSP shortages. Specialty G.654.E fiber is booking nine-month deliveries as Corning and Prysmian approach 90% utilization. Export controls on advanced lithography slow capacity additions, while rare-earth supply risks threaten erbium-doped amplifier output. Operators therefore adopt dual sourcing and accept longer rollout timelines, modestly restraining the fiber mobile backhaul system market's CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Technology: Coherent Optics Reshape DWDM Dominance

DWDM secured 43.78% of the fiber mobile backhaul market share in 2025 by aggregating hundreds of cell-site wavelengths on a single pair. The segment is migrating from 10×10 Gbps grids to 400 Gbps ZR+ pluggables that fit into QSFP-DD slots, collapsing three rack units of legacy transponders into a single module. Ciena’s WaveLogic 6 Extreme pushes 1.6 Tbps per wavelength over metro spans, quadrupling capacity without laying new fiber. Operators overlay fresh DWDM layers on dark fiber acquired years earlier, deferring costly trenching and lifting the fiber, and boosting the mobile backhaul system market size for coherent optics platforms.

Passive optical network solutions, led by XGS-PON and NG-PON2, are growing at 12.01% through 2031 as rural builds exploit split ratios of up to 1:64 to minimize stranded capex. Nokia’s Lightspan delivered 25 Gbps symmetrical PON to 8,000 rural towers in Southeast Asia under a USD 120 million deal. Ethernet over fiber stays dominant in enterprise private 5G because deterministic latency matters more than spectral efficiency, and CWDM persists in fiber-abundant suburbs. Regulatory overhead is low because the spectrum is unlicensed, but obtaining permits for new routes remains a local hurdle. The competition between coherent DWDM and PON illustrates the bifurcated demand profile that propels the broader fiber mobile backhaul system market.

By Bandwidth Capacity Tier: Hyperscale Demand Propels >100 Gbps Links

The 25-100 Gbps tier accounted for 32.49% of revenue in 2025 as carriers upgraded legacy 10 Gbps backhaul. However, the fiber mobile backhaul system market size for links above 100 Gbps is forecast to expand at 12.57% because millimeter-wave and mid-band carrier aggregation routinely push per-site traffic beyond 50 Gbps. Verizon upgraded 68% of its C-band locations to 100 Gbps links during 2025, investing more than USD 1.2 billion. Juniper’s ACX7000 routers combine 100 Gbps and 400 Gbps ports in a single 1RU chassis, letting operators future-proof their investment without over-provisioning.

The ≤10 Gbps tier is shrinking in developed markets but endures in low-density regions where peak demand sits below 5 Gbps. The 10-25 Gbps slice serves as a staging zone for operators that overlay additional CWDM wavelengths before committing to coherent optics. Broadcom’s Tomahawk 5 switch silicon delivers 51.2 Tbps on a 7 nm die, enabling aggregation hubs with thousands of 100 Gbps ports without chassis swaps. Momentum above 100 Gbps, therefore, underpins the long-term growth profile of the fiber mobile backhaul system market.

By End-User Industries: Private 5G Accelerates Enterprise Adoption

Mobile network operators retained 49.85% of 2025 spending, capitalizing on volume discounts for DWDM shelves and fiber leases. Yet enterprises deploying private 5G networks are expanding at an 11.69% CAGR, pulled by manufacturing plants, ports, and logistics hubs that require latency below 5 ms and symmetrical uplinks. BMW’s Regensburg factory runs 600 autonomous guided vehicles, supported by private 5G backed by dedicated fiber backhaul links to an on-prem core. Neutral-host firms such as American Tower secure 18% of segment revenue by selling backhaul-as-a-service that unbundles transport from radio access.

Government and public-safety agencies hold 8% of spending and specify dual-homed fiber routes with physical-layer encryption to meet mission-critical uptime targets. Cloud providers are emerging buyers as they deploy edge nodes co-located at cell sites. Calix’s AXOS converges residential broadband and mobile backhaul, signing nine regional fiber overbuilders in 2025. By 2030, enterprise and private-network demand could approach one-fifth of the fiber mobile backhaul system market, prompting operators to launch managed private-5G offers that keep transport within their operational perimeter.

Geography Analysis

Asia-Pacific generated 29.67% of 2025 global revenue and will post a 13.32% CAGR to 2031, the fastest of any region. China Mobile spent USD 18.4 billion on transport in 2025, upgrading 580,000 base stations in tier-2 and tier-3 cities with 100 Gbps coherent backhaul. Bharti Airtel committed USD 2.1 billion to fiberize 120,000 rural towers under BharatNet III, leveraging state co-funding to extend reach. NTT Docomo finished a nationwide 100 Gbps rollout in March 2025 and is trialing 800 Gbps ZR+ optics to support latency-sensitive XR services in 2026. South Korean carriers are testing holographic calling that requires 1 Gbps per user, reinforcing the long-term pull on the fiber mobile backhaul market in the region.

North America captured 26% of 2025 revenue and is forecast to expand at 10.8%. Verizon and AT&T invested USD 4.7 billion combined in fiber backhaul during 2025, focusing on C-band sites that exceed 30 Gbps peak traffic. Rogers and Telus earmarked more than CAD 1 billion (USD 740 million) to fiberize towers across Ontario and British Columbia. Tower specialists American Tower and Crown Castle boosted fiber route-miles by double digits, offering neutral-host transport that accelerates 5G densification for smaller carriers. These moves sustain a sizable share of the fiber mobile backhaul system market in the United States and Canada.

Europe represented 23% of 2025 revenue and is expanding at 10.2% on the back of sustainability mandates and open transport. Deutsche Telekom found that fiber backhaul consumes 58% less energy per transported terabit than microwave backhaul, helping it meet its net-zero pledge. Vodafone is rolling out Open RAN across 2,500 sites in the UK and Germany with disaggregated Ciena and ADVA transport to curb vendor lock-in. Orange devoted EUR 1.2 billion in 2025 to upgrade 45,000 cell sites with 100 Gbps coherent links. Middle Eastern carriers such as STC ordered USD 280 million in DWDM gear for Riyadh and Jeddah smart-city corridors. African rollouts remain uneven; South Africa and Nigeria lead with fiberized urban cores, while microwave endures elsewhere, keeping the regional fiber mobile backhaul system industry at an earlier stage of maturity.

Competitive Landscape

The fiber mobile backhaul system market shows moderate concentration as the top five suppliers, Huawei, Nokia, Ericsson, Cisco, and Ciena, held a significant share of global revenue in 2025. Huawei remains dominant in Asia-Pacific and the Middle East by bundling radio, transport, and core gear, although Western restrictions have narrowed its accessible spend to roughly 60% of global operator capex. Nokia and Ericsson counter with open, software-defined transport that works with third-party optics, meeting operators’ multi-vendor policies. Cisco’s Routed Optical Networking collapses IP and optical into one operational plane, trimming the total cost of ownership by up to 30% in published case studies.

Ciena and Infinera exploit long-haul and submarine sweet spots, where their WaveLogic 6 and ICE6 engines top competitor spectral efficiency tables. Ciena’s Blue Planet orchestrator secured eleven tier-1 wins in 2025, automating wavelength turn-ups and supporting pay-as-you-grow opex models. ADVA, now part of Adtran, targets neutral-host and enterprise buyers who need open APIs and incremental scalability.

Ribbon and Tejas win cost-sensitive deals by discounting packet-optical gear by 20-30%, though their service footprints remain regional. The Telecom Infra Project’s Open OOPT specs, published March 2025, intensify competition by certifying interoperability among white-box switches, third-party optics, and incumbent platforms. Patent filings show Broadcom, Marvell, and Acacia racing toward 1.6 Tbps DSPs, underlining silicon as the critical differentiator over the forecast horizon.

Fiber Mobile Backhaul System Industry Leaders

Huawei Technologies Co., Ltd.

Telefonaktiebolaget LM Ericsson (Ericsson)

Nokia Corporation

Cisco Systems, Inc.

ZTE Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Nokia, in partnership with authorized collaborators, upgraded RailTel's DWDM NLD network and deployed CG-NAT and metro optical transport networks across India, addressing rising demand for high-speed, reliable connectivity while enhancing efficiency and reducing costs.

- March 2025: Sivers Semiconductors AB has partnered with WIN Semiconductor to scale the production of its high-power DFB lasers and laser-array technology, enabling mass manufacturing for CWDM and DWDM applications.

Global Fiber Mobile Backhaul System Market Report Scope

The Fiber Mobile Backhaul System Market Report is Segmented by Fiber Technology (DWDM, CWDM, Ethernet over Fiber, Passive Optical Network, Others), Bandwidth Capacity Tier (≤10 Gbps, 10–25 Gbps, 25–100 Gbps, >100 Gbps), End-user Industries (Mobile Network Operators, Neutral Host and TowerCos, Enterprises and Private 5G Networks, Government and Public Safety, Cloud and OTT Providers, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| DWDM |

| CWDM |

| Ethernet over Fiber |

| Passive Optical Network (XGS-PON, NG-PON 2) |

| Other Fiber Technologies |

| ≤10 Gbps |

| 10–25 Gbps |

| 25–100 Gbps |

| >100 Gbps |

| Mobile Network Operators |

| Neutral Host and TowerCos |

| Enterprises and Private 5G Networks |

| Government and Public Safety |

| Cloud and OTT Providers |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Fiber Technology | DWDM | ||

| CWDM | |||

| Ethernet over Fiber | |||

| Passive Optical Network (XGS-PON, NG-PON 2) | |||

| Other Fiber Technologies | |||

| By Bandwidth Capacity Tier | ≤10 Gbps | ||

| 10–25 Gbps | |||

| 25–100 Gbps | |||

| >100 Gbps | |||

| By End-user Industry | Mobile Network Operators | ||

| Neutral Host and TowerCos | |||

| Enterprises and Private 5G Networks | |||

| Government and Public Safety | |||

| Cloud and OTT Providers | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the fiber mobile backhaul system market be by 2031?

It is forecast to reach USD 25.13 billion by 2031, rising from USD 14.65 billion in 2026 at an 11.4% CAGR.

Which fiber technology is growing fastest in mobile backhaul?

Passive optical network platforms such as XGS-PON and NG-PON2 are expanding at a 12.01% CAGR through 2031, the fastest among fiber options.

What bandwidth tier is seeing the highest growth rate?

Links above 100 Gbps are projected to grow at 12.57% as operators migrate to 400 Gbps ZR+ optics for 5G densification.

Why are enterprises investing in fiber mobile backhaul?

Private 5G networks in manufacturing, ports, and logistics need deterministic sub-5 ms latency that wireless alternatives cannot guarantee, driving an 11.69% CAGR for enterprise spending.

Which region is leading growth?

Asia–Pacific is the fastest-growing region, expected to post a 13.32% CAGR to 2031 on the back of large-scale fiber programs in China and India.

How does coherent pluggable optics benefit operators?

400 G ZR/ZR+ modules lower power per transported terabit by roughly 60% and remove expensive regeneration sites, cutting total transport costs by around 30%.

Page last updated on: