Fiber Backbone For Network Densification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.89 Billion |

| Market Size (2031) | USD 41.77 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Backbone For Network Densification Market Analysis by Mordor Intelligence

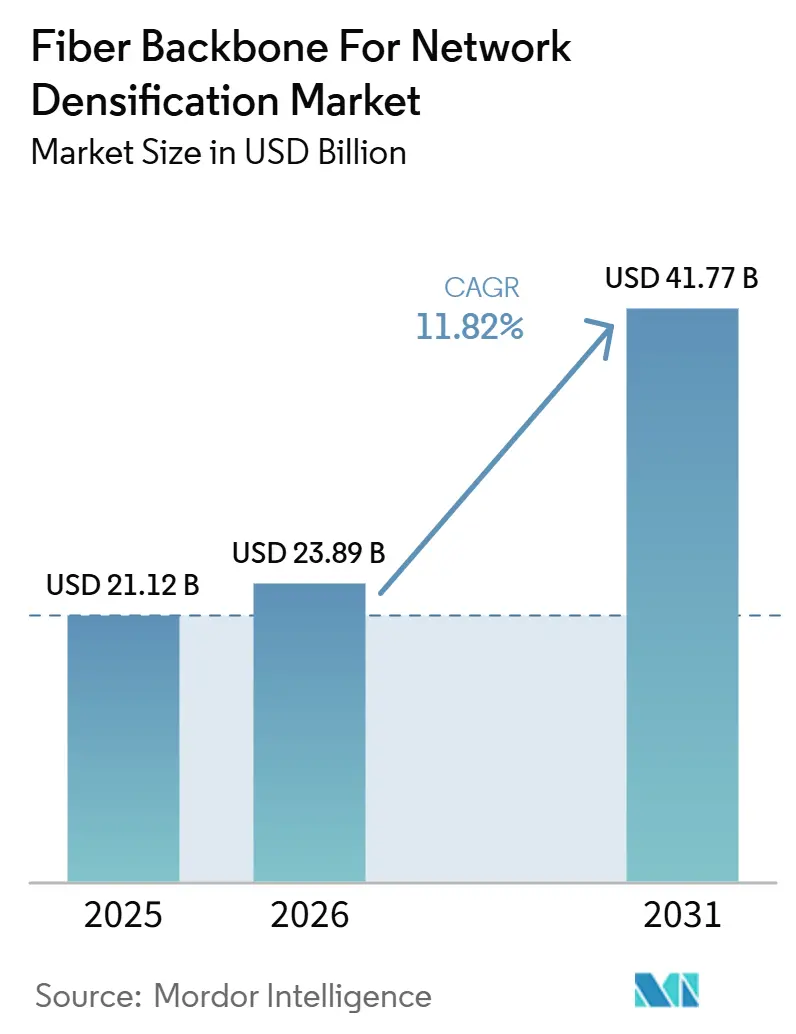

The fiber backbone for network densification market size was USD 21.12 billion in 2025 and is forecast to reach USD 41.77 billion by 2031, growing at a CAGR of 11.82% over 2026-2031. Growth is being shaped by 3 infrastructure cycles moving simultaneously: 5G radio access densification, AI-ready data center expansion, and publicly funded broadband buildouts. Demand is no longer tied mainly to telecom spending, because telecom operators and hyperscale cloud operators are now driving capacity needs together across the same transport corridors. That mix is widening the gap between installed backbone capacity and expected bandwidth demand, especially as AI workloads spread from centralized training sites to distributed edge locations. The fiber backbone for the network densification market is also benefiting from a narrower execution window, as public funding supports broader coverage while hyperscalers commit capital to major routes years in advance. This is pushing suppliers and network operators toward multi-year agreements, faster route planning, and manufacturing expansion, while cost inflation and physical security risks remain the main checks on project pace.

Key Report Takeaways

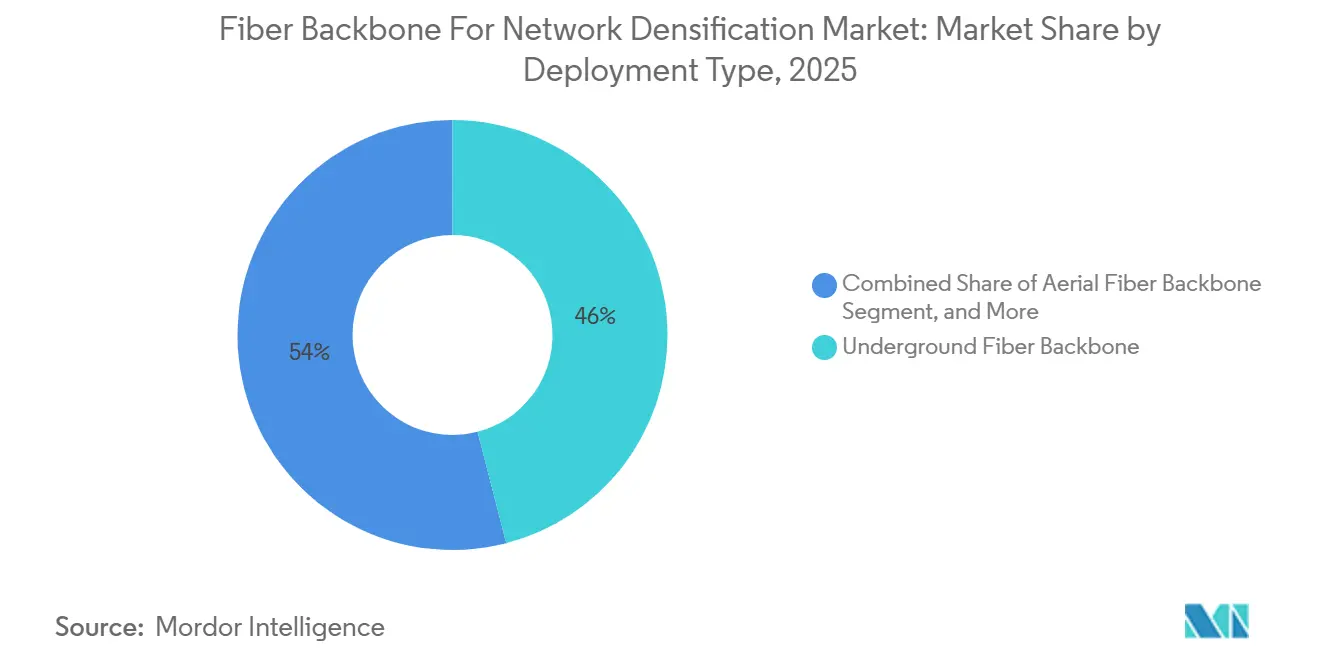

- By deployment type, underground fiber backbone held 45.98% of the fiber backbone market share for network densification in 2025, while submarine and intercity fiber backbone are projected to expand at a 12.87% CAGR through 2031.

- By fiber type, single-mode fiber led with an 89.96% revenue share in 2025, while multi-mode fiber is projected to grow at a 9.99% CAGR through 2031.

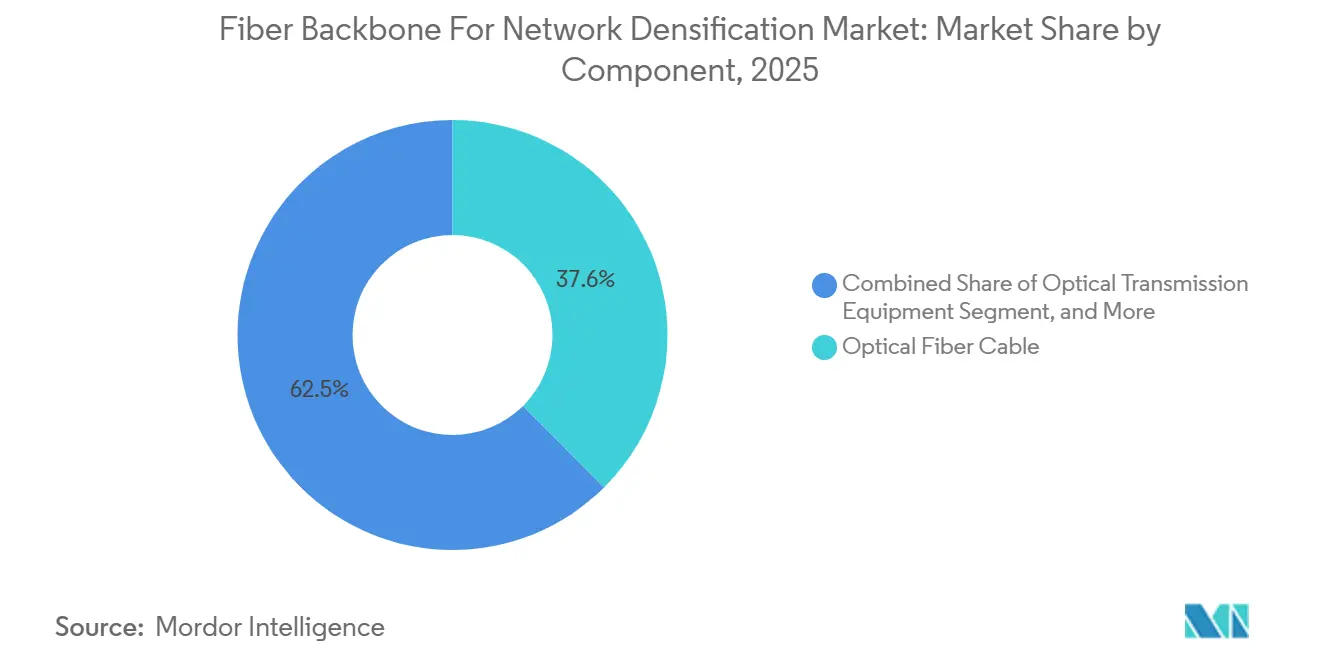

- By component, optical fiber cable accounted for 37.55% of the fiber backbone for network densification market size in 2025, while optical transmission equipment is projected to expand at a 14.10% CAGR through 2031.

- By end user, telecom operators accounted for 52.81% of revenue in 2025, while cloud and hyperscale data center operators are projected to record the highest CAGR of 16.96% through 2031.

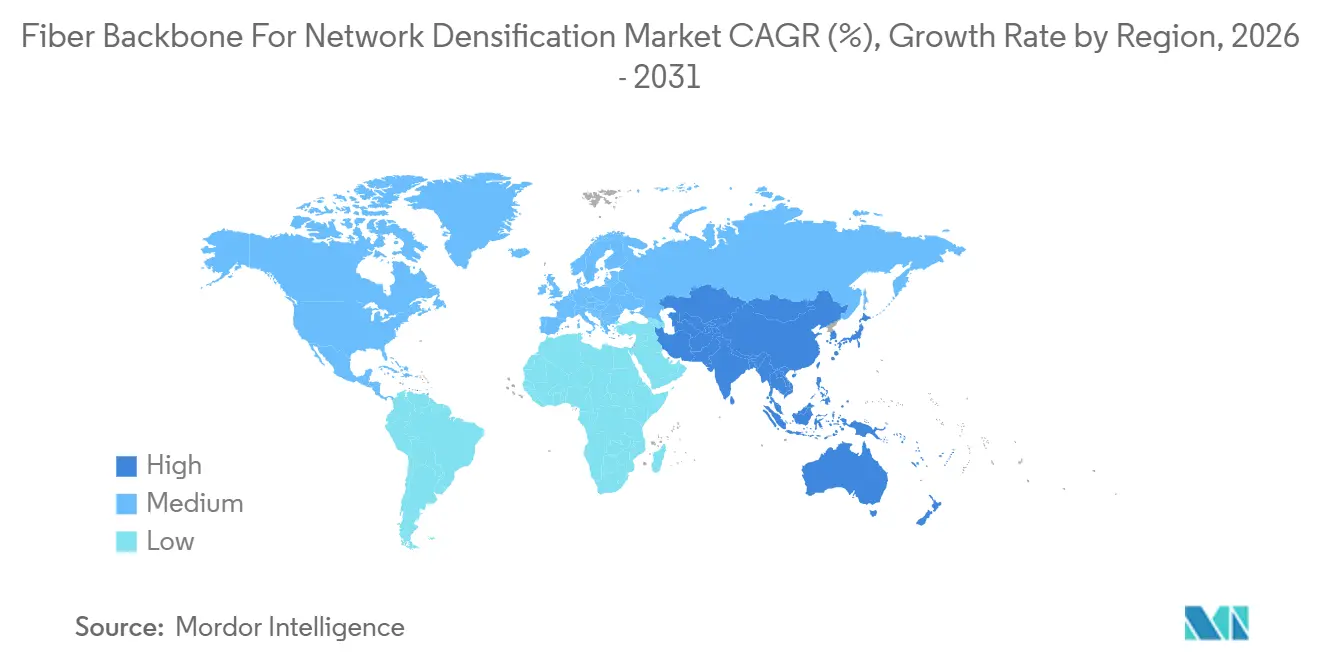

- By geography, North America accounted for 33.12% of the fiber backbone market for network densification in 2025, while Asia-Pacific is projected to expand at a 13.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fiber Backbone For Network Densification Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| 5G Small Cell Densification and Capacity Expansion | +2.8% | Global, with the highest intensity in North America, the Asia Pacific, and Europe | Short term (≤ 2 years) |

| AI-Driven Traffic Growth and East-West Backbone Congestion | +2.5% | North America and the Asia Pacific core spill over to Europe | Medium term (2-4 years) |

| Hyperscale And Edge Data Center Interconnect Expansion | +2.1% | Global, anchored in North America and the Asia Pacific | Medium term (2-4 years) |

| Government Fiberization Programs and Public Funding | +1.5% | North America, Europe, the Middle East and Africa, and parts of the Asia Pacific | Medium term (2-4 years) |

| Open RAN and Cloud-RAN Transport Upgrades | +1.0% | North America, Europe, and the Asia Pacific | Medium term (2-4 years) |

| Fiber Route Sharing, Micro-Trenching, and Utility Corridor Design Innovations | +0.6% | Global, most pronounced in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Small Cell Densification and Capacity Expansion

Mobile network densification is the most immediate near-term demand lever for the fiber backbone market. Standalone 5G and cloud-RAN layouts require highly reliable fronthaul and aggregation links, which keep fiber at the center of dense radio site buildouts. As operators add more small cells and raise transport capacity, network planning is moving from isolated site upgrades toward broader regional backbone commitments. That matters because denser urban footprints need tighter latency control, higher route diversity, and more stable transport between radio clusters and core layers. It also reduces the practical room for wireless substitutes in fronthaul rings, where service-quality requirements are harder to relax. The result is a steadier build cycle for the fiber backbone for the network densification market, even before later AI and enterprise traffic gains become fully visible.

AI-Driven Traffic Growth and East-West Backbone Congestion

AI workloads are reshaping the fiber backbone for the network densification market in ways that differ from earlier traffic growth cycles. Traditional internet growth was driven mainly by user-to-server traffic, whereas AI training and inference generate large east-west flows within and across compute clusters. That shift changes where congestion appears, because routes connected to major AI data center hubs are seeing traffic strain earlier than broad national networks. It also raises the fiber requirement per site, since AI campuses need greater density, more route redundancy, and more optical headroom than legacy server facilities. Large route orders from hyperscalers are therefore becoming longer in duration and larger in fiber count, which is changing cable manufacturing economics and procurement timing. In the fiber backbone for network densification market, this is driving long-haul and metro backbone investment along selected corridors before demand normalizes across the rest of the network.

Hyperscale and Edge Data Center Interconnect Expansion

Data center interconnect is becoming one of the most structurally durable demand pools in the fiber backbone for the network densification market. Corning and Meta announced a multiyear agreement of up to USD 6 billion in January 2026 for optical fiber, cable, and connectivity solutions tied to advanced US data center buildouts, which showed how hyperscalers are anchoring supply years ahead of use.[1]Corning Incorporated, “Corning and Meta Announce Multiyear, up to USD 6 Billion Agreement to Accelerate US Data Center Buildout,” Corning, corning.com Corning and NVIDIA then announced a multi-year partnership in May 2026 to expand US-based optical connectivity manufacturing capacity tenfold and increase fiber production capacity by more than 50%, reinforcing that supply security has become part of infrastructure strategy.[2]Corning Incorporated, “NVIDIA and Corning Announce Long-Term Partnership to Strengthen U.S. Manufacturing for AI Infrastructure,” Corning, corning.com Zayo completed its acquisition of Crown Castle's fiber solutions business in April 2026, adding 90,000 route miles of fiber and expanding its reach to more than 40,000 on-net locations, highlighting that route ownership is also being scaled through acquisition rather than solely through new construction. These moves show that hyperscalers and infrastructure operators are shifting from episodic purchases toward supply frameworks tied to long-term manufacturing and route availability. That shift is giving the fiber backbone for the network densification market a more predictable demand base across both metro and long-haul segments.

Government Fiberization Programs and Public Funding

Public funding is acting as a demand stabilizer for the fiber backbone for network densification market, especially where private returns remain less attractive or more delayed. The European digital connectivity agenda still requires substantial incremental investment to close gigabit coverage gaps, which keeps public support central to deployment planning across multiple member states.[3]ConnectEurope and GSMA, “State of Digital Communications 2025,” ConnectEurope, connecteurope.org National funding programs in the United States and Europe are also shortening the time between policy approval and route execution, which is helping support trunk and feeder expansion alongside access-layer targets. Public capital matters here because it does not simply add more projects, it lowers the demand volatility that would normally appear when private carrier and data center spending move on different cycles. It also helps operators justify backbone investment in regions that need route resilience and transport redundancy before traffic levels fully mature. In the fiber backbone for network densification market, this makes sovereign funding a structural support rather than a temporary supplement.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Civil Works Cost and Right-Of-Way Delays | -1.5% | North America, Europe | Short term (≤ 2 years) |

| Limited Duct and Pole Availability In Dense Urban Corridors | -0.9% | Global, with the highest pressure in legacy urban cores of North America, Europe, and East Asia | Medium term (2-4 years) |

| Fiber Route Security, Vandalism, And Sabotage Risk | -0.4% | North America, the Middle East and Africa | Medium term (2-4 years) |

| Long Payback Periods and Lease Rate Pressure in Secondary Cities | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Civil Works Cost and Right-Of-Way Delays

Civil works and permitting costs are the largest near-term drag on the fiber backbone for the network densification market. The Fiber Broadband Association reported that 92% of US fiber deployers faced cost increases in 2025, while median underground deployment costs reached USD 18.00 per foot and aerial deployment costs reached USD 8.00 per foot. The same industry feedback showed that 88% of respondents expected further cost increases in 2026, with labor, materials, permitting, and make-ready work remaining the main drivers. These pressures matter because backbone routes require high up-front civil spending before a single revenue-generating service goes live. Delays in right-of-way approvals also weaken project sequencing, since a single blocked crossing can disrupt the economics of an entire corridor. In the fiber backbone for network densification market, this restraint is slowing route activation more through timing and cost discipline than through any drop in long-term demand.

Limited Duct and Pole Availability in Dense Urban Corridors

Limited access to ducts and poles is narrowing the practical build window for the fiber backbone for the network densification market in mature urban cores. Many of the highest-value corridors lie within conduit systems laid decades ago, which means new capacity often requires re-entry into already crowded pathways rather than a simple route extension. That creates more dependence on pavement restoration, utility coordination, and infrastructure sharing, all of which raise execution complexity even when demand is clear. Prysmian's Sirocco Ultra design, which places 288 fibers in a 6.1 mm cable compatible with standard 8 mm ducts, reflects how the industry is responding by increasing capacity per duct rather than relying solely on new civil works.[4]Prysmian, “Prysmian Boosts Efficiency for High Density Broadband, Data Centers and 5G Roll-Out with Sirocco Ultra Cables,” Prysmian, prysmian.com In dense urban areas, this kind of design matters because route scarcity can be as limiting as capital availability. The fiber backbone for the network densification market, therefore, depends not only on laying more fiber but also on extracting more usable capacity from existing conduit infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Underground Backbone Anchors Urban Densification Spend

Underground fiber backbone accounted for 45.98% of deployment-type revenue in 2025, making it the largest deployment format in the fiber backbone for network densification market share. That lead reflects the operator's preference for buried infrastructure in high-density corridors, where route security, asset life, and lower long-term maintenance costs carry more weight than initial build cost. Metro rings and major intercity backbone sections also continue to favor underground placement because 5G fronthaul and data center interconnect traffic leave less tolerance for route instability. Aerial routes remain relevant where speed and lower up-front cost matter most, but they face more timeline risk in dense zones because access and permitting can delay installation. The submarine and intercity fiber backbone is projected to grow at a 12.87% CAGR from 2026 to 2031, indicating that long-haul route creation is gaining momentum alongside metro infill in the fiber backbone, driving network densification and market size.

The mix is also changing because many new AI facilities are being placed in power-rich greenfield locations outside legacy fiber rights-of-way. That placement is creating fresh demand for intercity segments that connect new compute locations to existing exchange points and cloud regions. Lumen's NorthLine route between Seattle and Minneapolis clearly shows this pattern, as it was designed around emerging northern US data center corridors and is expected to be available by the end of 2026.[5]Lumen Technologies, “Lumen Expands Its U.S. Network with NorthLine, a New Northern Fiber Route Built for AI Data Movement,” Lumen Technologies, lumen.com At the same time, micro-trenching is becoming increasingly important in metropolitan infill because it reduces disruption and shortens deployment time on sealed urban surfaces. This combination of new intercity demand and faster urban installation methods is broadening the role of deployment engineering in the fiber backbone for the network densification market. It also means route design is becoming more location-specific, with underground strength in core corridors and rising opportunities across newly connected long-haul paths.

By Fiber Type: Single-Mode Fiber Dominates High-Capacity Transport

Single-mode fiber accounted for 89.96% of revenue in 2025, keeping it firmly dominant in the fiber backbone for network densification market size. Its lead reflects the fact that backbone, metro ring, and 5G fronthaul networks depend on longer reach and coherent optical compatibility, where single-mode remains the standard choice. Standard references such as ITU-T G. 652. D still anchors mainstream backbone deployment, while G. 654. E is gaining relevance in higher-capacity long-haul and submarine applications that need lower attenuation over longer distances. China is also pushing backbone upgrades toward 400 Gbps and 800 Gbps network capabilities, supporting continued procurement of high-performance single-mode infrastructure for dense transport layers. Multi-mode fiber is still projected to grow at a 9.99% CAGR through 2031, but that growth remains centered on short-reach campus and data center interconnect use rather than core transport.

Single-mode fiber is also extending its competitive reach through denser cable design. Prysmian launched BendBrightXS 160µm single-mode fiber in October 2025, enabling more fibers per cable and per duct without requiring new civil works. That kind of design matters because duct space is becoming a strategic constraint in urban and campus environments. As cable density improves, single-mode solutions can enter use cases that once relied more on multi-mode due to physical packing constraints. In the fiber backbone for network densification market, this keeps the overall fiber type mix from shifting quickly, even as short-reach applications grow. It also reinforces the view that capacity density, not only transmission reach, is shaping procurement decisions across the broader fiber backbone for the network densification industry.

By Component: Transmission Equipment Leads the Next Capex Wave

Optical fiber cable held 37.55% of component revenue in 2025, while optical transmission equipment is projected to record the fastest growth at a 14.10% CAGR through 2031 in the fiber backbone for network densification market. Networks are no longer built only to add strands; they are being upgraded to support higher wavelength rates and more flexible software-defined traffic management. That is why coherent optics, denser transport shelves, and disaggregated backbone architectures are gaining strategic importance alongside raw fiber deployment. Passive components continue to scale with cable buildout, but they do not define procurement direction as much as transmission platforms do.

Open and disaggregated transport design is becoming a key competitive filter inside the fiber backbone for the network densification market. KDDI launched a large-scale commercial deployment of cluster-based, distributed, disaggregated backbone routers in June 2026, demonstrating that operators are willing to separate hardware and software choices when they need greater flexibility to support AI-driven traffic growth. SoftBank also moved forward with its all-optical metro network deployment with Cisco, targeting nationwide coverage by 2027 and reporting energy consumption that is more than 90% lower than conventional configurations. These moves matter because they lift the importance of software control, optical automation, and open interfaces in backbone procurement. In the fiber backbone for network densification industry, vendors that align with open transport standards are gaining a stronger place in future upgrade cycles. The component mix is therefore moving from a cable-only growth story toward a combined cable and intelligence buildout.

By End User: Hyperscaler Demand Reshapes the Demand Mix

Telecom operators accounted for 52.81% of end-user revenue in 2025, but cloud and hyperscale data center operators are projected to grow at a 16.96% CAGR through 2031 in the fiber backbone for network densification market. Telecom operators still anchor present demand because they own wide portions of existing route infrastructure and remain central to 5G backhaul and wholesale transport. Even so, hyperscaler requirements are changing how projects are defined, as AI infrastructure needs higher fiber density, dedicated paths, and more predictable lead times than conventional cloud expansion. This is encouraging shared build models that enable a route to serve mobile backhaul, enterprise connectivity, and hyperscaler transport simultaneously. It is also changing supplier priorities, since cable makers and equipment vendors increasingly treat hyperscaler programs as anchor demand rather than a secondary layer.

The end-user mix is widening beyond carriers and hyperscalers as demand for localized private networks and neutral-host services grows. Enterprise 5G deployments in industrial sites, ports, and logistics hubs are generating targeted backbone procurement tied to campus and regional transport needs. Public utilities and government-linked infrastructure programs are also expanding route footprints through co-deployment and dig-once approaches, thereby lowering marginal build costs over time. Uniti Wholesale's January 2026 announcement of a 1,100-route-mile dark fiber expansion, supported by a 20-year customer contract valued at more than USD 500 million, showed that neutral-host economics can support large backbone commitments in their own right. In the fiber backbone for network densification market, which broadens demand sources beyond traditional carrier capex cycles. It also gives the long-term revenue base a more diversified profile across wholesale, enterprise, and AI-linked infrastructure use cases.

Geography Analysis

North America accounted for 33.12% of revenue in 2025, giving the region the largest market share in the fiber backbone for network densification market. The region combines active 5G densification, large hyperscale AI infrastructure spending, and public broadband support, which keeps both metro and long-haul route demand elevated. The United States remains the core driver because hyperscalers are expanding compute and interconnect capacity at a scale that pulls forward fiber procurement, construction, and transport upgrades. Canada is also becoming more relevant as data center investment follows power availability and stable operating conditions, which extends backbone demand beyond the main US hubs.

Asia-Pacific is projected to expand at a 13.87% CAGR from 2026 to 2031, making it the fastest-growing regional block in the fiber backbone for network densification market. China is pushing the region through backbone modernization plans that emphasize higher-capacity optical transport and stronger links between major computing hubs. Japan is advancing on a parallel path, with KDDI launching commercial disaggregated backbone routers in June 2026 and SoftBank pursuing nationwide all-optical metro deployment by 2027. NTT and NTT East also demonstrated rapid optical wavelength-path switching for all-photonics networking, which supports the region's push toward more agile AI-era transport. India and South Korea add incremental momentum through continued 5G expansion and rising data center interconnect needs, keeping Asia-Pacific broadly based rather than concentrated in a single national market.

Europe remains strategically important because regulatory and policy support are helping sustain backbone investment even when private operator returns are under pressure. The region's digital connectivity agenda still points to a major investment requirement for gigabit-capable infrastructure across member states, which supports continued route expansion and modernization. The United Kingdom, Germany, France, and Italy remain the main deployment markets, while Central and Eastern Europe still offer room for greenfield-style route economics in underpenetrated areas. The Middle East and Africa are smaller contributors, but national broadband plans and urban connectivity programs are supporting backbone demand in Saudi Arabia, the UAE, Egypt, and South Africa. South America is seeing focused growth in Brazil as hyperscale and interconnection activity rise, while wider regional development remains more selective and corridor-based.

Competitive Landscape

The fiber backbone for the network densification market is moderately concentrated in optical fiber cable manufacturing and more fragmented in optical equipment, creating 2 distinct competitive layers. A relatively small group of global cable producers, including Corning, Prysmian, Sumitomo Electric, Fujikura, YOFC, and Hengtong, controls a large share of manufacturing capability and has become central to hyperscaler supply planning. Multi-year supply agreements reinforce that position by reserving production capacity well before routes are fully engineered or activated. This gives scale players an advantage in lead time, customer commitment, and plant utilization across the fiber backbone for the network densification market.

Prysmian reported 9.0% organic growth in its Digital Solutions segment in Q1 2026, while EBITDA margin expanded to 20.6%, demonstrating the anchored demand from broadband, data center, and 5G programs supporting both volume and pricing power. Corning used a broader strategy by pairing long-term customer agreements with manufacturing expansion, including its Meta agreement in January 2026 and its NVIDIA partnership in May 2026. Corning also expanded its Stryków facility in Poland, which is set to become the EU's largest optical cable and connectivity manufacturing campus in the second half of 2026. These moves show that leading cable suppliers are competing through capacity reservation, local manufacturing scale, and deeper alignment with hyperscaler build programs. In the fiber backbone for network densification market, this creates entry barriers for smaller regional manufacturers that lack the same balance sheet or customer visibility.

The optical equipment layer remains more open because operators still choose among Nokia, Ciena, Infinera, Huawei, ZTE, and FiberHome for transport platforms and backbone routing systems. Even so, disaggregated architecture is reducing switching costs, which means incumbents cannot rely only on proprietary stacks to protect their share. KDDI's deployment of disaggregated backbone routers and SoftBank's all-optical network program both showed that vendors aligned with open, automated transport models are gaining greater procurement relevance. Corning's OFC 2026 multicore fiber and AI data center connectivity launch also signals that the next differentiation cycle is moving toward higher density and more capacity per fiber rather than simple route expansion alone. That leaves the fiber backbone for network densification market competitive, but with clear structural advantages for firms that can pair manufacturing scale, route relevance, and transport innovation.

Fiber Backbone For Network Densification Industry Leaders

Corning Incorporated

Prysmian S.p.A.

Sumitomo Electric Industries, Ltd.

Fujikura Ltd.

YOFC (Yangtze Optical Fibre and Cable Joint Stock Limited Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: KDDI Corporation launched commercial deployment of Disaggregated Distributed Backbone Router (DDBR) clusters across major backbone sites in Japan, built to TIP open standards with DriveNets NOS software, to address AI-driven traffic growth. This is the first large-scale commercial deployment of open, disaggregated backbone routing architecture in Japan's national network, establishing a replicable template for operators globally.

- May 2026: Corning and NVIDIA announced a multi-year commercial and technology partnership to expand US-based manufacturing of advanced optical connectivity solutions, increasing Corning's optical connectivity manufacturing capacity tenfold and fiber production capacity by more than 50%. The partnership includes 3 new facilities in North Carolina and Texas, and the creation of more than 3,000 new jobs.

- April 2026: Zayo Group completed its acquisition of Crown Castle's fiber solutions business, adding approximately 90,000 route miles of fiber and expanding total reach to more than 40,000 on-net locations, as part of a combined fiber and small cells transaction valued at USD 8.5 billion. Concurrent with the acquisition, Zayo and the newly formed Arium Networks, Crown Castle's small cells business under EQT, entered into a long-term commercial fiber supply agreement.

- April 2026: Corning announced an expansion of its manufacturing facilities in Stryków, Poland, slated for the second half of 2026, which, upon completion, will make the Stryków campus the largest optical cable and connectivity manufacturing facility in the Europe. The expansion is expected to create approximately 2,500 high-quality jobs in Poland to meet accelerating demand for AI data center and micro-optics products across the EMEA region.

Global Fiber Backbone For Network Densification Market Report Scope

The Fiber Backbone for Network Densification Market is Segmented by Deployment Type (Underground, Aerial, and Submarine and Intercity), Fiber Type (Single-Mode and Multi-Mode), Component (Optical Fiber Cable, Transmission Equipment, Passive Components, and Other Components), End User (Telecom Operators, Hyperscale, Enterprises, Public Sector, Other End users), and Geography (North America, South America, Europe, Asia-Pacific, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Underground Fiber Backbone |

| Aerial Fiber Backbone |

| Submarine and Intercity Fiber Backbone |

| Single-Mode Fiber |

| Multi-Mode Fiber |

| Optical Fiber Cable |

| Optical Transmission Equipment |

| Passive Components |

| Other Components |

| Telecom Operators |

| Cloud and Hyperscale Data Center Operators |

| Enterprises and Private Network Operators |

| Public Sector and Utilities |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Type | Underground Fiber Backbone | ||

| Aerial Fiber Backbone | |||

| Submarine and Intercity Fiber Backbone | |||

| By Fiber Type | Single-Mode Fiber | ||

| Multi-Mode Fiber | |||

| By Component | Optical Fiber Cable | ||

| Optical Transmission Equipment | |||

| Passive Components | |||

| Other Components | |||

| By End User | Telecom Operators | ||

| Cloud and Hyperscale Data Center Operators | |||

| Enterprises and Private Network Operators | |||

| Public Sector and Utilities | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the fiber backbone market for network densification?

The fiber backbone for network densification market was valued at USD 21.12 billion in 2025 and is projected to reach USD 41.77 billion by 2031 at an 11.82% CAGR.

What is driving backbone fiber demand the most right now?

The strongest demand drivers are 5G small cell densification, AI-related east-west traffic growth, and hyperscale data center interconnect expansion. These 3 forces are raising both metro and long-haul route requirements.

Which deployment type leads current spending?

Underground fiber backbone led deployment-type revenue with a 45.98% share in 2025, supported by stronger route security, longer asset life, and better fit for dense urban corridors.

Which end users are expanding the fastest?

Cloud and hyperscale data center operators are projected to grow the fastest, at a 16.96% CAGR through 2031, even though telecom operators remained the largest end-user group in 2025, with a 52.81% share.

Which region is growing the fastest?

Asia-Pacific is projected to post the highest regional CAGR at 13.87% through 2031, supported by backbone upgrades in China and transport modernization programs in Japan and other major regional markets.

What is the main challenge for project execution?

Civil works inflation and right-of-way delays remain the biggest near-term restraints, because they raise route costs, slow activation timelines, and make dense urban deployment harder to scale.

Page last updated on: