Facial Cleanser Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

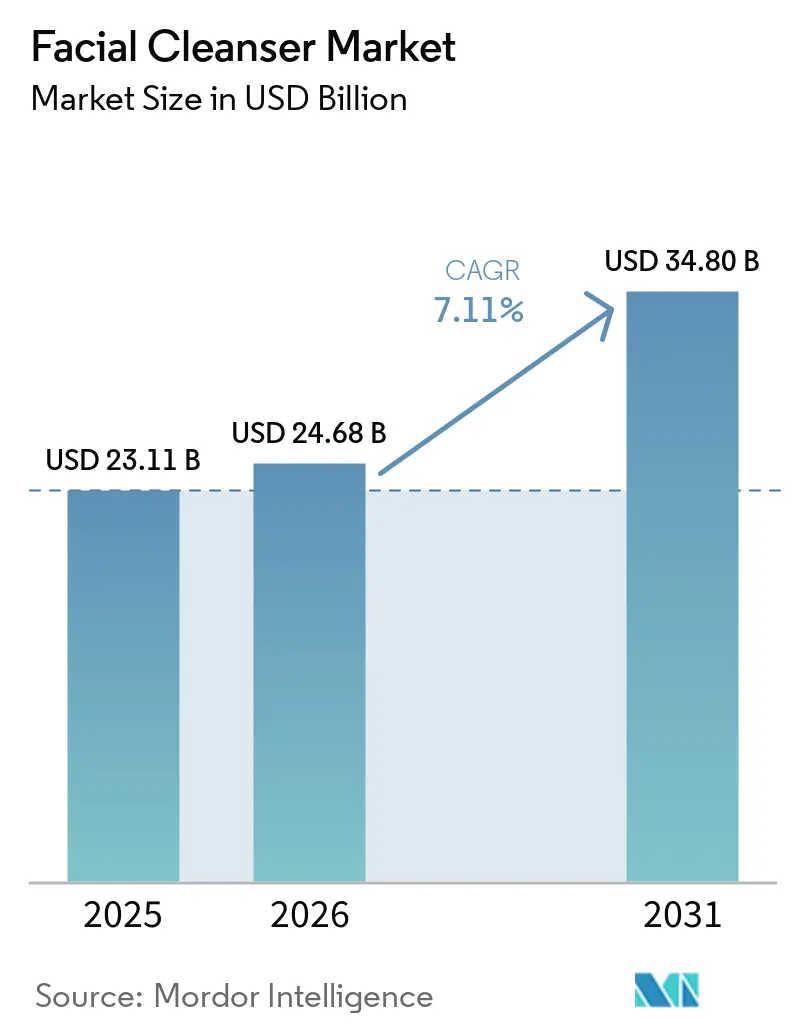

| Market Size (2026) | USD 24.68 Billion |

| Market Size (2031) | USD 34.80 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Facial Cleanser Market Analysis by Mordor Intelligence

The face cleanser market size is expected to increase from USD 23.11 billion in 2025 to USD 24.68 billion in 2026 and reach USD 34.80 billion by 2031, growing at a CAGR of 7.11% over 2026–2031. The category has evolved from a basic cleansing step into the foundation of a more informed and skincare-focused routine, increasing the emphasis on ingredient efficacy, skin barrier protection, and clinically backed formulations in the facial cleanser market. This transition is creating greater pressure for innovation, as brands can no longer rely solely on factors such as lather, fragrance, or affordability to maintain consumer interest. Demand is also becoming more consistent as concerns related to acne, sensitivity, and overall skin health increasingly influence repeat purchasing behavior across diverse consumer groups and regions. At the same time, the market is witnessing intensified competition driven by science-backed product launches, dermatologist-associated positioning, and portfolio expansion through acquisitions as companies seek to accelerate innovation and strengthen their market presence. However, supply chain risks and heightened scrutiny around ingredient safety and compliance continue to pose challenges, increasing reformulation requirements and making sourcing strategies more critical across the facial cleanser market.

Key Report Takeaways

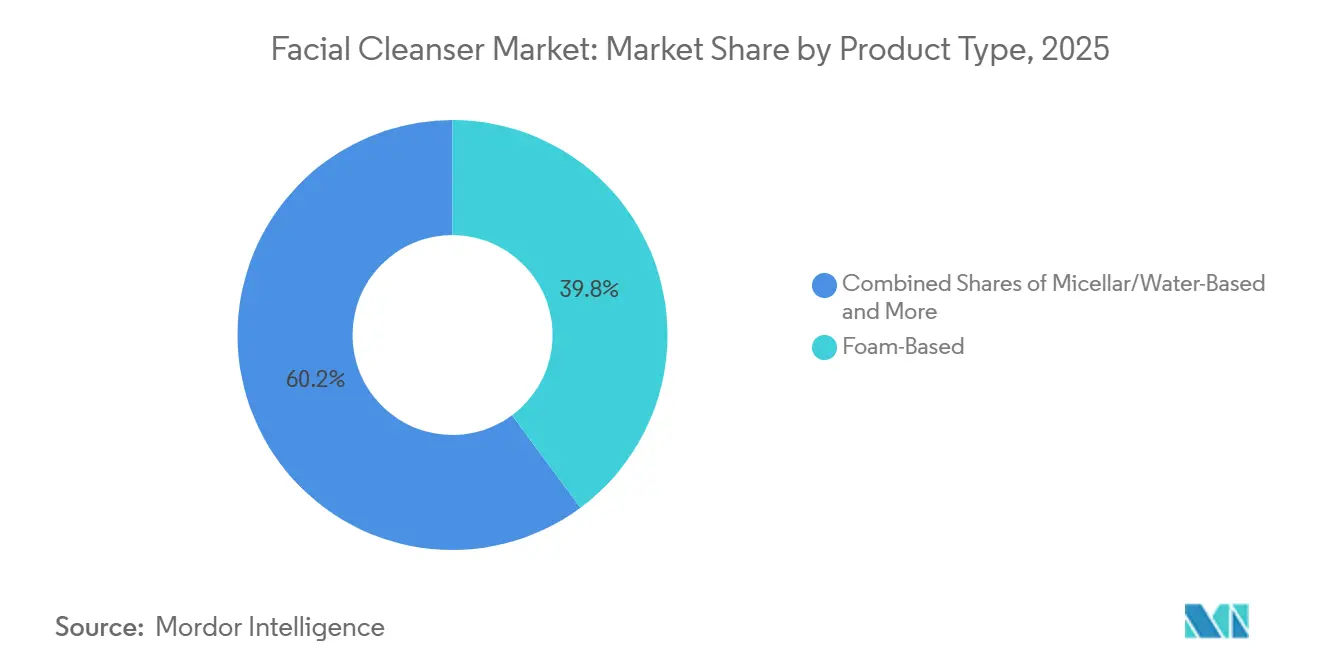

- By product type, foam-based cleanser held 39.84% of facial cleanser market share in 2025, while micellar/water-based cleanser is forecast to expand at 8.54% CAGR through 2031.

- By category, conventional segment accounted for 82.73% of the market in 2025, while natural/organic segment is projected to grow at 7.95% CAGR through 2031.

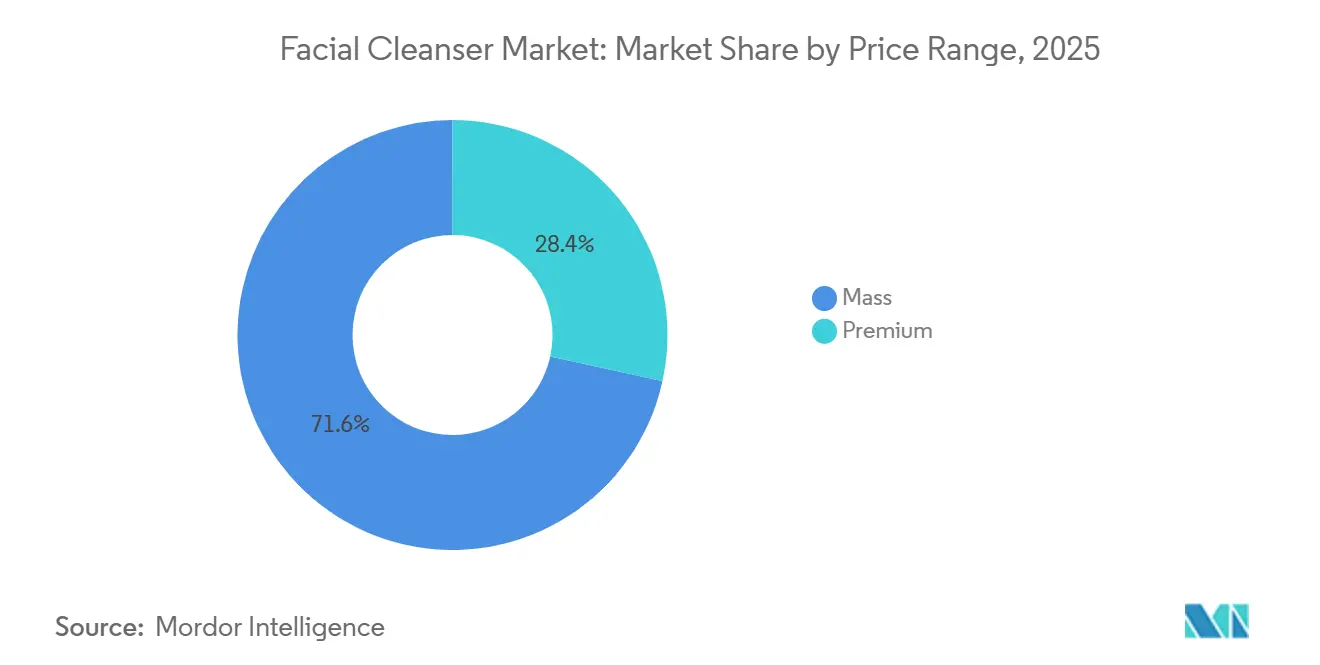

- By price range, mass segment represented 71.56% of the face cleanser market size in 2025, while premium segment is expected to advance at 7.83% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets captured 36.28% of the market in 2025, while online Retail Stores are set to grow at 8.05% CAGR through 2031.

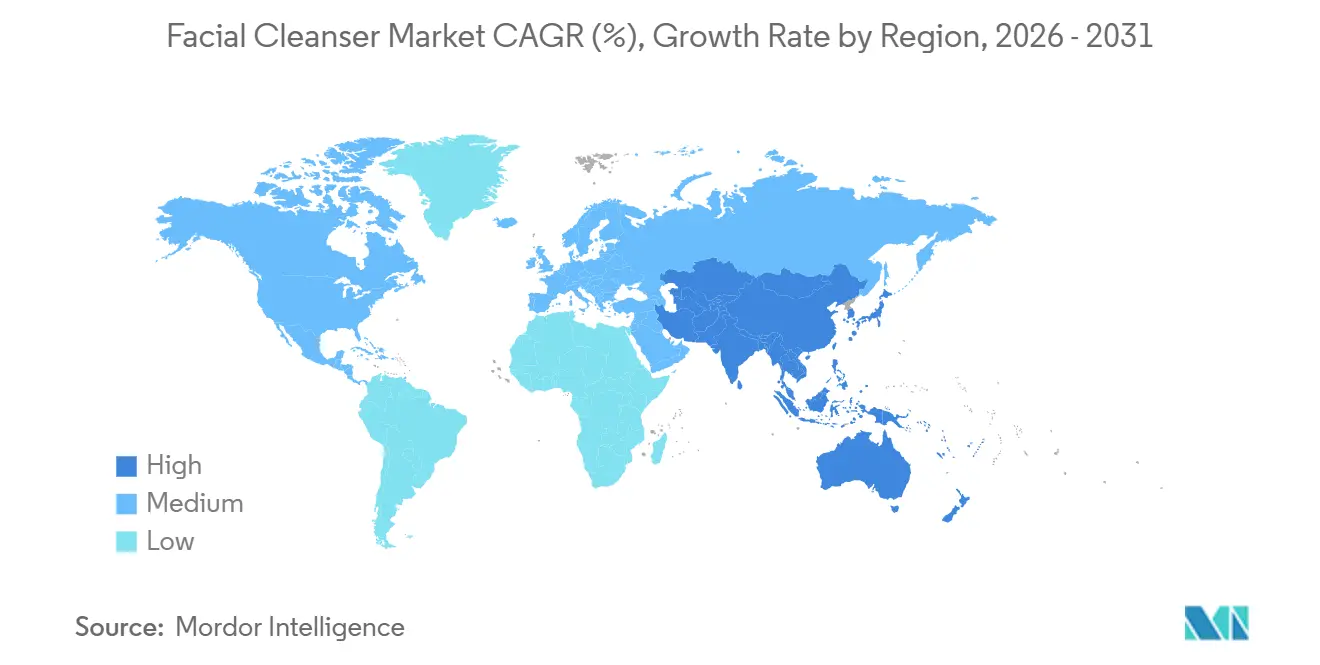

- By geography, Asia-Pacific held 41.37% of face cleanser market share in 2025, and the same region is projected to expand at 8.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Facial Cleanser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on skincare and facial hygiene | +1.5% | Global, concentrated in Asia-Pacific, North America, and Western Europe | Medium term (2-4 years) |

| Increasing demand for personalized and skin-specific formulations | +1.2% | Global, with highest traction in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Rising male grooming and gender-inclusive skincare adoption | +1.0% | North America, Western Europe, India, and East Asia | Medium term (2-4 years) |

| Increasing prevalence of acne, sensitivity, and other skin conditions | +1.2% | Global, with highest burden in Latin America, East Asia, and Africa | Short term (≤ 2 years) |

| Influence of social media, beauty influencers, and celebrity endorsements | +0.8% | Global, with stronger impact in China, the United States, and Southeast Asia | Short term (≤ 2 years) |

| Increasing preference for natural, organic, and clean-label products | +0.9% | North America, Western Europe, and premium Asia-Pacific segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on skincare and facial hygiene

Consumer expectations from face washes and facial cleansers have evolved significantly, with the category moving beyond basic cleansing to become an essential part of daily skincare routines. Cleansers are increasingly viewed as the foundation of skincare regimens, with consumers seeking products that address concerns such as hydration, acne management, and skin barrier protection. This has elevated the importance of face washes as an entry point into broader skincare routines and strengthened their role in influencing brand loyalty and long-term consumer engagement with skincare brands. For example, consumers who adopt a hydrating or barrier-repair cleanser from brands such as CeraVe or Neutrogena often extend their routines to include moisturizers, serums, and treatment products from the same portfolio. Supporting this trend, consumer spending on personal care products in the United Kingdom increased from GBP 36,132 million in 2023 to GBP 38,290 million in 2025, according to the Office for National Statistics, reflecting the growing prioritization of skincare and wellness among consumers [1]Source: Office for National Statistics (United Kingdom), "Consumer trends: Q4 2025", ons.gov.uk. Consequently, efficacy and skin compatibility have become key purchase drivers, encouraging manufacturers to invest further in advanced formulations, dermatological testing, and ingredient innovation.

Increasing demand for personalized and skin-specific formulations

The increasing demand for personalized and skin-specific formulations is reshaping the facial cleanser market, as consumers increasingly expect products that address their unique skin biology rather than broad skin-type categories. This trend extends beyond conventional "for oily skin" or "for dry skin" positioning toward formulations tailored to individual factors such as age, lifestyle, climate, pollution exposure, hormonal changes, and skin sensitivity. For example, PROVEN Skincare offers AI-driven personalized cleansers that analyze more than 40 individual parameters, including skin concerns, environmental conditions, and lifestyle factors, to create unique formulations for each consumer rather than assigning them to a standard product segment. Similarly, Prose Skincare develops made-to-order facial cleansers based on over 80 variables, including geographic location, humidity levels, and skincare goals, with formulations that evolve over time as consumer needs change. These developments illustrate the industry's shift from demographic segmentation toward precision skincare, creating opportunities for brands with strong data analytics, dermatological expertise, and formulation capabilities.

Increasing prevalence of acne, sensitivity, and other skin conditions

Clinical skin conditions continue to serve as one of the strongest and most enduring demand drivers in the face wash market. According to a 2024 global study by Pierre Fabre Laboratories, acne affects approximately 20.5% of the global population, with prevalence reaching 23.9% in Latin America, 20.2% in East Asia, and 18.5% in Africa, regions that also represent key growth markets for facial cleansers [2]Source: Pierre Fabre Laboratories, "Pierre Fabre Laboratories presents the first global study on the epidemiology of acne", pierre-fabre.com. Further, the American Academy of Dermatology further estimates that up to 50 million Americans experience acne annually, with around 85% of cases occurring among individuals aged 12 to 24 years. Such widespread and persistent skin concerns support consistent demand for cleansers targeting acne, excess sebum, and skin sensitivity. Unlike discretionary beauty purchases, these products are closely tied to long-term skin management needs, creating recurring consumption patterns. This dynamic strengthens the market foundation for clinically positioned and dermatologist-recommended face wash products. Additionally, growing consumer awareness around preventive skincare and early intervention for skin issues is further increasing the adoption of specialized cleansing solutions. Manufacturers are responding by expanding portfolios with science-backed formulations featuring active ingredients such as salicylic acid, niacinamide, and ceramides to address specific dermatological concerns.

Increasing preference for natural, organic, and clean-label products

The clean beauty trend has evolved from a niche preference into a mainstream expectation, particularly among higher-income consumer groups. Consumer interest in organic and naturally derived ingredients continues to strengthen, with a significant share of buyers placing importance on ingredient transparency and certification in personal care products. Younger consumers, especially those in the 18–29 age group, demonstrate a higher willingness to pay premium prices for certified organic formulations. At the same time, the market faces a growing trust deficit, as many consumers remain skeptical of self-declared "natural" or "organic" claims. This has increased the importance of independent certification bodies and recognized standards that provide greater transparency and credibility. As a result, certified brands are benefiting from stronger consumer confidence and premium positioning, while uncertified brands face increasing challenges in competing within the clean beauty segment. A recent example is Sky Organics, which launched a facial skincare collection in July 2025 featuring products certified to the United States Department of Agriculture (USDA) Organic standard, illustrating how brands are increasingly leveraging third-party certifications to build trust, support premium pricing, and differentiate themselves in the competitive clean beauty market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity among consumers in developing markets | -1.5% | South Asia, Sub-Saharan Africa, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Stringent regulations on cosmetic ingredients and labeling | -1.0% | Europe primary, spill-over to North America, Asia-Pacific with evolving frameworks | Medium term (2-4 years) |

| Supply chain disruptions affecting ingredient availability | -0.8% | Global; concentrated exposure in South Asia, Middle East, and Europe | Short term (≤ 2 years) |

| Rising concerns over harsh chemicals and skin irritation | -0.7% | Global; highest sensitivity in markets with elevated sensitive-skin consumer prevalence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on cosmetic ingredients and labeling

Ingredient regulations are increasing pressure on the facial cleanser market by shortening reformulation timelines and raising compliance requirements. Stricter restrictions on fragrances, preservatives, and other cosmetic ingredients are prompting companies to reassess product portfolios, particularly those reliant on traditional foaming systems. Regulatory momentum continues to intensify, with the European Union introducing restrictions on an additional 15 chemicals classified as carcinogenic, mutagenic, or toxic to reproduction (CMR) in April 2026, underscoring the increasing pace of compliance changes facing personal care manufacturers [3]Source: European Union, "Commission Regulation (EU) 2026/78", europa.eu. This challenge is especially significant for foam-based products, as consumers continue to associate rich lather with effective cleansing. Reformulation efforts are both time-intensive and costly, involving extensive testing, packaging revisions, inventory management, and sourcing changes. As a result, manufacturers must carefully balance maintaining the sensory experience consumers expect while transitioning to cleaner and gentler ingredient profiles. This trade-off is expected to remain a key challenge shaping the facial cleanser market in the coming years.

Rising concerns over harsh chemicals and skin irritation

Consumer awareness of the stripping and irritant potential of conventional sulfate surfactants in foaming cleansers is creating a reformulation imperative that adds cost without guaranteed short-term revenue uplift. The shift from sulfate-based to amino acid or alkyl glucoside surfactant systems, which deliver milder cleansing profiles compatible with barrier-sensitive skin, is progressing fastest in East Asian markets where ingredient-literate consumers have developed precise sensory benchmarks for gentleness. This transition complicates the formulation economics of mass-market foam-based cleansers, which depend on sulfate systems for cost efficiency, high-volume lather, and the "skin-tightness post-wash" sensory cue that a significant portion of mass-market consumers still equate with effective cleansing. Reformulating for gentleness risks eroding the sensory signals that drive repeat purchase at mass price points, creating a strategic dilemma between clinical positioning and commercial sensory delivery that is particularly acute for brands operating simultaneously across premium and mass distribution tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foam-Based Leads While Micellar/Water-Based Drives Premium Growth.

Foam-based cleansers accounted for the largest share of the market in 2025, representing 39.84% of total value, supported by their broad appeal across consumer groups, suitability for multiple skin types, and strong presence across retail channels. Their leadership is reinforced by long-standing consumer perceptions linking foam textures with superior cleansing performance, resulting in high repeat purchase rates. Gel-based cleansers continue to cater primarily to oily and acne-prone skin, while cream and lotion formats remain preferred for dry and sensitive skin due to their moisturizing properties.

Micellar and water-based cleansers are projected to register the fastest growth, expanding at a CAGR of 8.54% during 2026–2031, driven by rising demand for convenient, no-rinse products that cleanse while preserving the skin barrier. Growing adoption of multifunctional skincare routines and increasing awareness of sensitive skin needs are accelerating this shift. Oil-based cleansers continue to benefit from the popularity of the K-beauty-inspired double-cleansing routine, particularly in East Asian markets, while texture innovation across formats is emerging as a key premiumization strategy for brands.

By Category: Conventional Holds Scale While Natural/Organic Segment Drives Value

The conventional segment held the largest share of the facial cleanser market in 2025, accounting for 82.73% of total market value, supported by its affordability, widespread retail penetration, and strong consumer trust in established surfactant-based cleansing technologies. While conventional formulations are expected to remain dominant in the near term, their share is gradually moderating in premium consumer segments as demand shifts toward higher-value and ingredient-conscious alternatives. The expansion of clean-label and certified formulations is also contributing to an increase in category average selling prices.

The natural/organic segment is projected to record the fastest CAGR of 7.95% during 2026–2031, driven by rising consumer preference for ingredient transparency, sustainability, and certification-backed claims. Growth in this segment is increasingly supported by demand for products that combine natural ingredients with clinically proven efficacy rather than relying solely on "natural" positioning. This trend is encouraging both emerging and established brands to reformulate products and adopt certification-led strategies, strengthening the premiumization of the facial cleanser market.

By Price Range: Mass Supports Reach While Premium Lifts Value Creation

Mass-priced face wash products accounted for the largest share of the global market in 2025, representing 71.56% of total value due to their high purchase frequency and extensive availability across retail channels and income groups. The segment benefits from strong penetration in supermarkets, pharmacies, and traditional retail formats, supporting sustained sales volumes worldwide. However, it continues to face strong price competition, growing private-label penetration in developed markets, and margin pressure arising from fluctuations in surfactant and packaging costs.

Premium face wash products are projected to register the fastest growth, expanding at a CAGR of 7.83% during 2026–2031, supported by increasing consumer willingness to spend on advanced skincare solutions. Growth is being fueled by rising demand for clinically positioned and benefit-led products among younger consumers in developed markets and affluent urban populations in Asia-Pacific. The segment is also benefiting from premiumization trends and rising preference for dermatologist-endorsed and ingredient-focused formulations. While masstige brands are broadening access to premium skincare, luxury brands continue to command higher price realizations, reinforcing premiumization as a key trend shaping the category.

By Distribution Channel: Offline Retains Leadership as Online Accelerates Growth

Supermarkets/Hypermarkets accounted for the largest share of global face wash distribution in 2025, representing 36.28% of total market value. Their dominance is driven by their role as the primary replenishment channel for mass-market cleansers across both developed and emerging economies. Health and beauty stores continue to serve as important premium discovery destinations, while pharmacies and drug stores maintain relevance through strong consumer trust in dermatologist- and pharmacist-recommended formulations for targeted skin concerns. The broad geographic reach and high product visibility offered by modern retail formats further reinforce their leadership position in the category.

Online retail stores are projected to register the fastest growth, expanding at a CAGR of 8.05% during 2026–2031. The rapid shift toward digital purchasing is being fueled by rising e-commerce penetration, social commerce adoption, and increasing consumer engagement with online beauty platforms. Social media-driven product discovery and the growing influence of creator-led recommendations are accelerating online conversion rates across skincare categories. For face wash brands, this evolution is making product visibility increasingly dependent on digital shelf optimization, content-driven marketing, and influencer-led consumer acquisition strategies.

Geography Analysis

Asia-Pacific accounted for 41.37% of the facial cleanser market in 2025 and is expected to register the fastest regional growth through 2031 at a CAGR of 8.32%. Despite its large market size, the region continues to expand as consumers increasingly prioritize ingredient transparency and skin compatibility in cleansing products. China remains the largest value contributor, while South Korea continues to influence global cleansing routines through its skincare-led culture. Premium skincare habits in Japan and rising demand for herbal and Ayurvedic products in India further strengthen regional growth prospects.

The facial cleanser market in North America and Europe represents the largest concentration of value outside Asia-Pacific, although growth drivers differ across the two regions. In the United States, demand is supported by strong consumer interest in acne-focused and dermatologist-recommended products. Canada shows similar preferences for quality and safety, while affordability plays a more prominent role in purchasing decisions in Mexico. Across Europe, consumers increasingly favor clean-label and dermocosmetic cleansers, encouraging manufacturers to adopt gentler ingredient systems and reformulate existing products.

South America, the Middle East, and Africa are emerging as important long-term growth regions due to urbanization, youthful populations, and expanding retail access. Demand in Latin America is supported by a growing need for targeted skincare solutions, particularly for acne management. The Middle East reflects a mix of premium demand in affluent urban markets and value-oriented purchasing in more price-sensitive economies. In Africa, companies are increasingly introducing localized offerings, highlighted by launches such as Garnier’s tailored cleanser products in markets such as Kenya.

Competitive Landscape

The facial cleanser market remains moderately concentrated, with major multinational players such as L'Oréal, Unilever, Beiersdorf, Estee Lauder Companies, amd Amorepacific Corporation, among others, accounting for significant market presence without fully dominating the category. This leaves room for regional brands, pharmacy-led players, and digital-native entrants to address local preferences and niche skin concerns. Competition increasingly depends on formulation credibility, pricing strategy, and channel relevance rather than brand recognition alone. While large companies continue to benefit from strong distribution and research and development capabilities, these advantages no longer ensure market leadership across all segments.

Recent developments highlight targeted innovation as a key competitive strategy in the facial cleanser market. Companies are increasingly focusing on science-backed formulations, barrier-support benefits, and dermatology-led positioning to differentiate their offerings. For instance, in March 2026, Kenvue showcased the expansion of Neutrogena's BarrierCare technology at AAD 2026, underscoring the industry's growing emphasis on cleansers that support skin barrier health alongside effective cleansing. These trends reflect the increasing convergence of formulation credibility, clinical validation, and commercialization strategy in the facial cleanser segment.

White space opportunities persist across both premium and value segments of the facial cleanser market. Premium growth is being driven by clinically backed cleansers featuring advanced actives and skin barrier support, while value opportunities continue to favor affordable offerings from regional brands and private labels. Increasing adoption of Asian skincare concepts in Western markets is further shaping innovation in facial cleansers. Going forward, success will depend on balancing scientific efficacy, sensory experience, and price competitiveness.

Facial Cleanser Industry Leaders

-

L'Oréal S.A.

-

Unilever PLC

-

Beiersdorf AG

-

The Estée Lauder Companies Inc.

-

Amorepacific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Premium skincare brand KASS expanded its portfolio with the launch of the Pore Minimizer Serum and Evergoing Face Wash, targeting concerns such as enlarged pores, excess oil, and daily cleansing needs. The products emphasize science-backed, barrier-friendly formulations aimed at improving skin texture and supporting long-term skin health.

- June 2025: Glowbar, a facial membership studio brand, expanded into skincare with the launch of its first product, Expert Cleanser, translating its in-studio expertise into an at-home skincare solution. The cleanser is a concentrated foaming formula featuring ingredients such as white willow bark, glycolic acid, and gluconolactone to deliver deep cleansing and gentle exfoliation without stripping the skin barrier.

- February 2025: Starface expanded beyond its signature acne patches by launching its first facial cleanser and moisturizer, marking a strategic move into the broader skincare category. The launch supports the brand's growth ambitions by encouraging consumers to adopt a full skincare routine within the Starface ecosystem.

Global Facial Cleanser Market Report Scope

| Gel-Based |

| Foam-Based |

| Cream-Based |

| Micellar/Water-Based |

| Oil-Based |

| Other Product Types |

| Conventional |

| Natural/Organic |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Gel-Based | |

| Foam-Based | ||

| Cream-Based | ||

| Micellar/Water-Based | ||

| Oil-Based | ||

| Other Product Types | ||

| By Category | Conventional | |

| Natural/Organic | ||

| By Price Range | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for the facial cleanser market through 2031?

The facial cleanser market is expected to grow from USD 24.68 billion in 2026 to USD 34.80 billion by 2031 at a 7.11% CAGR, supported by stronger skincare adoption, clinical positioning, and premium format expansion.

Which region leads global demand for facial cleansers?

Asia-Pacific led with 41.37% share in 2025 and is also the fastest-growing region at 8.32% CAGR through 2031, helped by scale in China, innovation in South Korea, and rising urban demand in India.

Which product type is growing the fastest in facial cleansing?

Foam-based remained the largest type with 39.84% share in 2025, but micellar/water-based products are growing the fastest at 8.54% CAGR because they match demand for gentler and more convenient cleansing.

How are digital channels changing brand competition in this category?

Online retail stores are projected to grow at 8.05% CAGR through 2031, and digital-first approaches show that platform visibility now shapes product discovery and premium positioning.

Page last updated on: