Extremity Tissue Expanders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

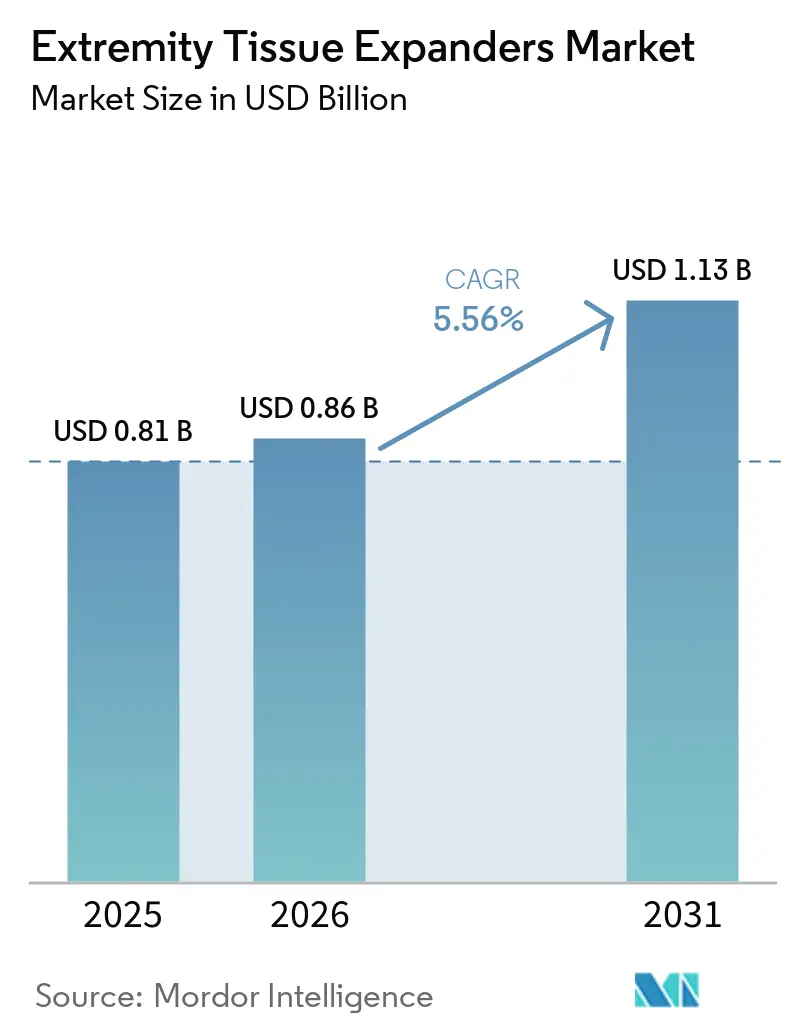

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.13 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

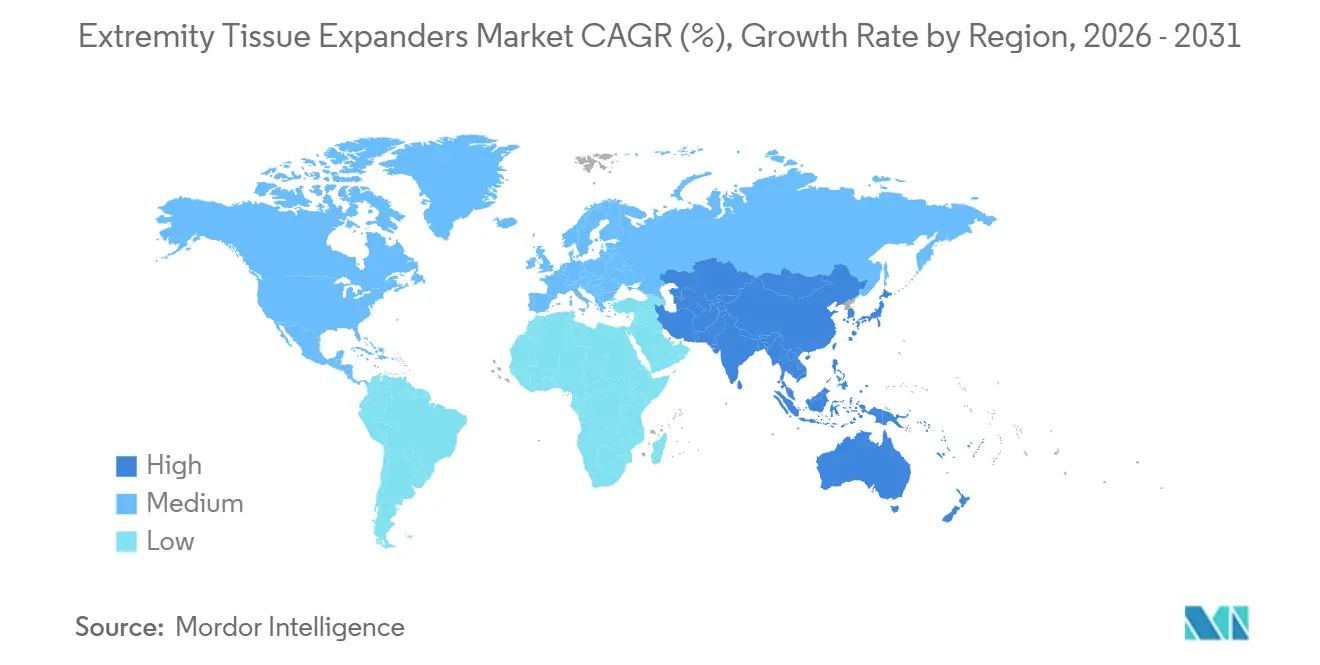

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extremity Tissue Expanders Market Analysis by Mordor Intelligence

The Extremity Tissue Expanders Market size is projected to be USD 0.81 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.13 billion by 2031, growing at a CAGR of 5.56% from 2026 to 2031.

Sustained demand arises from reconstruction after oncologic surgery, high-energy trauma, and burns, while newer polymer shells and antimicrobial coatings are lowering complication rates and shortening expansion schedules. North America remains the revenue anchor, yet capital expenditures on tertiary care in China, India, and South Korea are positioning Asia-Pacific as the fastest riser. Device pricing remains under negotiation pressure as payers steer staged reconstructions to ambulatory settings where bundled payments dominate. Meanwhile, product differentiation has moved beyond volume ranges to MRI compatibility and surface engineering, encouraging surgeons to switch platforms when real-world data confirm lower explant rates.

Key Report Takeaways

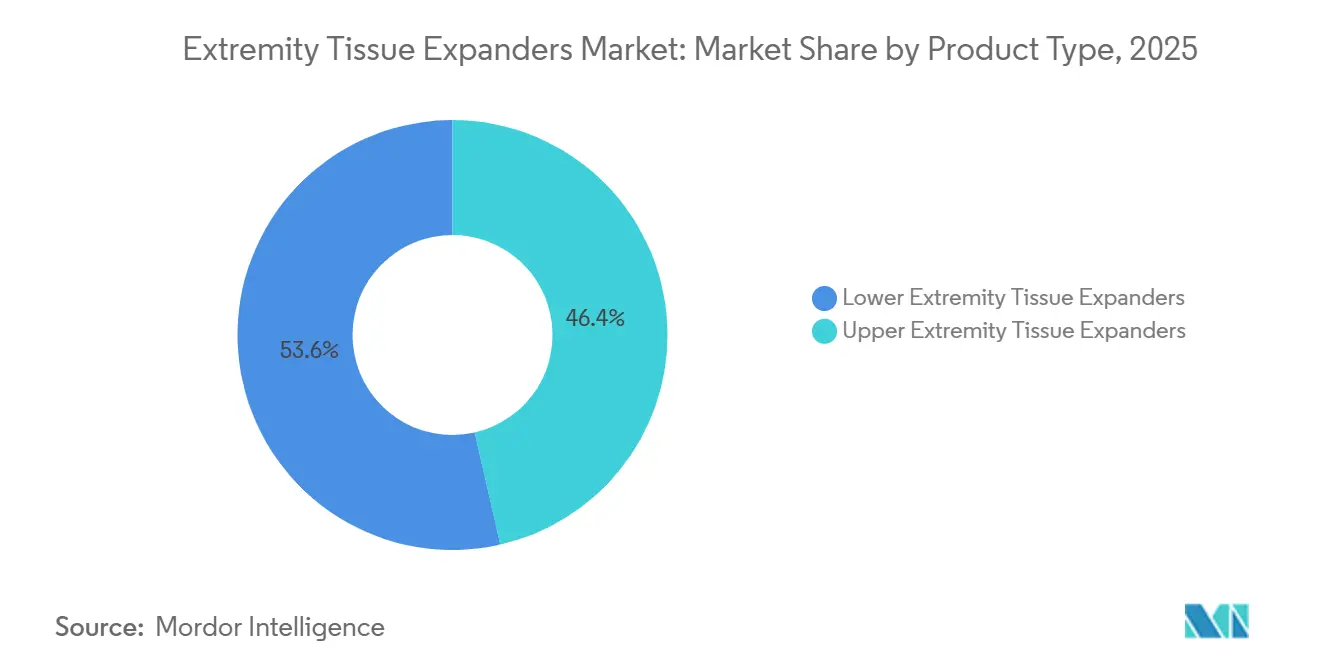

- By product type, upper extremity devices led with a 46.43% revenue share in 2025. Lower extremity devices are expected to expand at a 7.65% CAGR between 2026 and 2031.

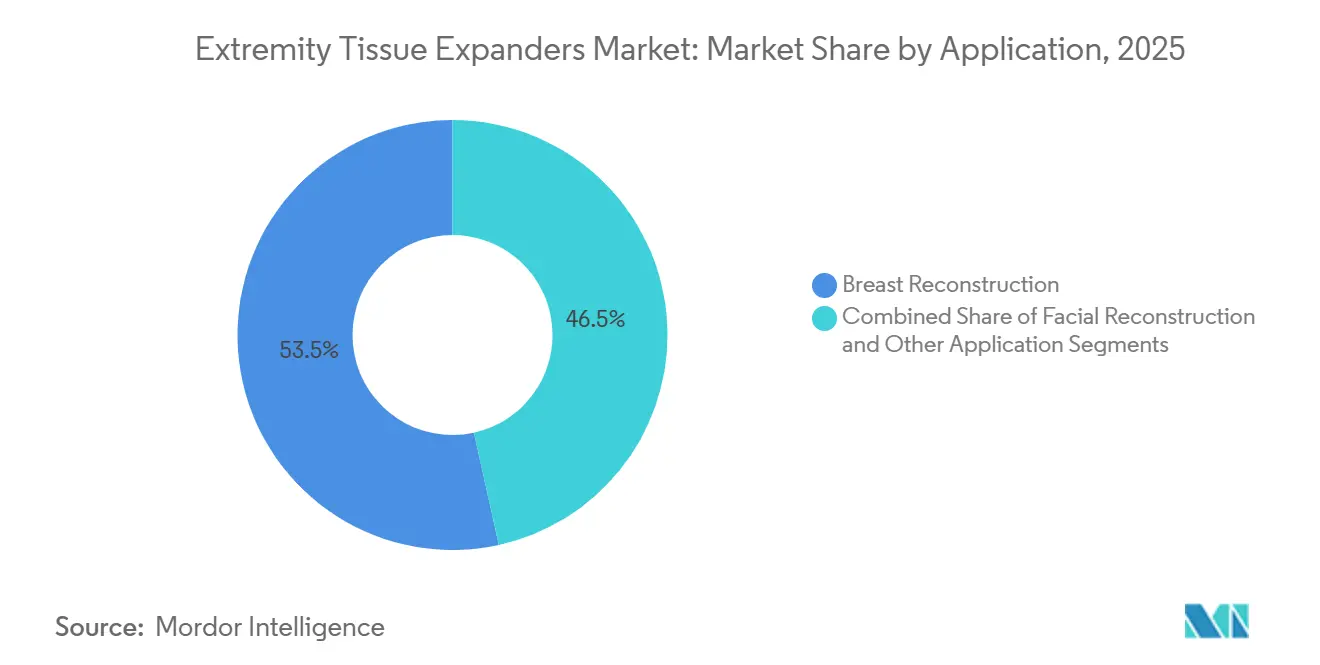

- By application, breast reconstruction commanded 53.45% of revenue in 2025. Facial reconstruction is forecast to progress at a 7.88% CAGR from 2026 to 2031.

- By end user, hospitals accounted for 62.45% of revenue in 2025. Ambulatory surgical centers are expected to advance at an 8.65% CAGR through 2031.

- By geography, North America commanded 42.56% of revenue in 2025. Asia-Pacific is forecast to progress at a 6.54% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Extremity Tissue Expanders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing incidence of reconstructive trauma and oncology procedures | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Advancements in tissue expander materials and design technologies | +1.0% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Rising acceptance of minimally invasive reconstructive techniques | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Expanding access to reimbursement for reconstructive surgeries | +0.7% | North America, select European markets | Medium term (2-4 years) |

| Growth in cosmetic and aesthetic enhancement demand | +0.6% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of healthcare infrastructure in emerging economies | +0.9% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Reconstructive Trauma and Oncology Procedures

Worldwide trauma volumes and oncologic resections continue to push patients into staged soft-tissue reconstruction pathways. The American Society of Plastic Surgeons recorded 162,579 breast reconstruction procedures in 2024, underscoring stable procedural throughput despite reimbursement fluctuations. The World Health Organization estimates up to 50 million non-fatal injuries annually, many requiring extremity or craniofacial expansion before flap coverage[1]World Health Organization, “Global Burden of Disease 2020,” who.int. Oral cancer resections exceeded 377,000 global cases in 2020, each creating soft-tissue defects amendable to expander placement. U.S. workplace accidents resulted in 2.1 million non-fatal injuries in 2020, and bicycle injuries rose to 425,910, further feeding the reconstructive pipeline. Improved survival in breast oncology widens the eligible pool for delayed or prophylactic reconstruction, reinforcing baseline growth in the extremity tissue expanders market.

Advancements in Tissue Expander Materials and Design Technologies

Regulatory clearances for larger-volume and MRI-compatible devices have raised the standard of care. Mentor secured FDA approval in December 2024 for MemoryGel Enhance implants and matching CPX4 PLUS Enhance expanders (930–1,445 cc), filling a gap for the 15% of mastectomy patients with larger chests. A 400-patient study showed 97% satisfaction at three-year follow-up, with complication rates comparable to those of autologous options. Sientra’s AlloX2Pro received FDA clearance in June 2023 as the first MRI-compatible expander, eliminating pre-imaging explant procedures. Establishment Labs’ Motiva Flora features a nanosurface that inhibits bacterial adhesion, aiming to reduce capsular contracture rates. These technologies allow manufacturers to defend premium pricing even as tenders tighten, helping the extremity tissue expanders market sustain margin.

Rising Acceptance of Minimally Invasive Reconstructive Techniques

Prepectoral placement accelerated from 88,043 cases in 2022 to 106,380 in 2023, thanks to the routine use of acellular dermal matrices (ADM) that obviate muscle dissection. ADM procedures rose to 79,747 in 2023, and Integra LifeSciences will restart PriMatrix and SurgiMend production at a Massachusetts facility in 2026 to meet demand. Same-day discharge protocols dovetail with ambulatory center economics, while shorter anesthesia times and lower narcotic use improve patient scores. Surgeons report fewer animation deformities and faster expansion cycles when the device sits above the pectoralis. These clinical wins reinforce payer efforts to migrate staged reconstruction out of hospital outpatient departments, sustaining volume growth in the extremity tissue expanders market.

Expanding Access to Reimbursement for Reconstructive Surgeries

The Women’s Health and Cancer Rights Act requires private plans that cover mastectomy to fund reconstruction, yet claims adjudication varies by state. CMS revised Billing & Coding Article A58573 in October 2024, clarifying CPT codes and supportive ICD-10 diagnoses, which has reduced denial rates for tissue expander claims. However, Fair Health data show commercial allowed amounts for expander pathways ranging from USD 9,300 to USD 18,000, reflecting site-of-service variation. Payers are piloting episode-based bundles that pay a flat fee for placement, expansions, and exchange, which could widen access if set near median costs. Clearer guidance and bundled initiatives are expected to lift procedure volumes, reinforcing demand within the extremity tissue expanders market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure And Device Costs | -0.9% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Post-Operative Complication Risks | -0.6% | Global, amplified in irradiated and immunocompromised patients | Medium term (2-4 years) |

| Limited Specialist Surgeon Availability | -0.5% | North America, parts of Europe, rural Asia-Pacific | Medium term (2-4 years) |

| Stringent Regulatory Approval Processes | -0.4% | United States, European Union, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure and Device Costs

Total costs for staged expander reconstruction can surpass USD 50,000 when performed out of network, and Fair Health data places in-network payments between USD 9,300 and USD 18,000 in Austin for identical CPT codes. Medicare payments for breast reconstruction fell 13.32% in real terms between 2000 and 2019, forcing surgeons to favor faster, lower-margin expander pathways over autologous options[2]Mayo Clinic, “Historical Medicare Payment Trends in Breast Reconstruction,” mayoclinic.org. The debate over retiring temporary S-codes that increased payments for microsurgical flaps illustrates payer pushback against high-resource reconstructions. Device list prices remain opaque under group purchasing contracts, hindering patient price transparency. In emerging economies, out-of-pocket financing limits uptake, dampening the growth trajectory of the extremity tissue expanders market.

Post-Operative Complication Risks

Infection rates range from 2% to 35% and are higher in irradiated fields, often necessitating explantation and delayed reconstruction. Capsular contracture affects up to 20% of cases and drives the need for revision surgery. The 2019 FDA request that Allergan recall BIOCELL textured devices heightened awareness of breast-implant-associated anaplastic large cell lymphoma, prompting many surgeons to switch to smooth expanders[3]U.S. Food and Drug Administration, “BIOCELL Device Recall,” fda.gov. Expander extrusion remains more common in lower limb sites that endure shear forces, complicating diabetic and burn reconstructions. Manufacturers fund registries such as NBIR to monitor real-world outcomes, but complications remain a concern, slowing momentum in the extremity tissue expanders market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Upper Extremity Dominance, Lower Limb Momentum

Upper extremity devices held a 46.43% market share of extremity tissue expanders in 2025, reflecting broad use in chest wall and scalp reconstruction, as well as in staged breast procedures. Mentor’s December 2024 approval of CPX4 PLUS Enhance, which scales to 1,445 cc, exemplifies a shift toward shape-stable shells that accommodate larger thoracic defects. Lower extremity units are projected to grow at a 7.65% CAGR from 2026 to 2031, buoyed by burn-center protocols and diabetic limb salvage programs. National Safety Council data show more than 425,000 bicycle injuries annually in the United States, underscoring continuous trauma demand.

Design challenges for lower-limb applications include weight-bearing stress and the risk of joint infections. Reinforced shells and antimicrobial silicone blends are in pilot use, while modular ports enable bedside inflation, reducing outpatient visits. As payers reward home-based expansion, companies are beta-testing smartphone apps that guide injection volumes and flag over-pressure events. These enhancements, combined with stable reimbursement for limb salvage, support forecast outperformance for lower extremity devices and diversify revenue within the extremity tissue expanders market.

By Application: Breast Reconstruction Anchor, Facial Uptick

Breast reconstruction accounted for 53.45% of revenue in 2025, anchored by 85,970 U.S. expander-to-implant cases in 2023. This cohort benefits from federal mandates that guarantee coverage after mastectomy, sustaining baseline unit flow. Facial reconstruction is positioned to expand at a 7.88% CAGR through 2031, supported by 377,713 global oral and mandibular cancer diagnoses in 2020 and increased maxillofacial trauma referrals.

Crescent- and anatomically contoured expanders now account for about half of facial sales, minimizing distortion during inflation. Surgeons pair these devices with intraoral flaps and 3D-printed guides to shorten operating time. Real-world evidence suggests that MRI-compatible shells ease oncologic surveillance in head-and-neck cancer survivors. With more insurers approving staged facial reconstruction for functional impairment, growth in this niche will offset plateauing volumes in traditional breast workflows, sustaining diversity in the extremity tissue expanders market.

By End-User: Hospitals Hold Ground, Ambulatory Centers Surge

Hospitals retained 62.45% of 2025 revenue, reflecting their role in complex microsurgical reconstructions and pediatric care. Nonetheless, ambulatory surgical centers are on track for an 8.65% CAGR to 2031 as CMS site-neutral payment policies incentivize lower-cost venues. Prepectoral placement suits ASC workflow because patients can ambulate within hours, and bundled supplies reduce inventory overhead.

Manufacturers now market “ASC kits” that bundle an expander, fill tubing, and ADM patches, reducing SKU counts and negotiating leverage. Remote wound-monitoring platforms feed data to the surgeon’s dashboard, reducing post-op visits by up to 40%. Cosmetic clinics, which captured near 20% of placements in 2025, entice self-pay patients with staged augmentation packages. Taken together, outpatient migration and consumer cash spending should lift procedure counts even if hospital volumes stay flat, supporting stable mid-single-digit growth for the extremity tissue expanders market.

Geography Analysis

North America accounted for 42.56% of global revenue in 2025, driven by 162,579 breast reconstructions and statutory coverage mandates. Reimbursement erosion, including a 13.32% fall in real Medicare payments since 2000, intensifies margin pressure but has not reversed volume growth. Domestic manufacturing is rising: Tiger Aesthetics Medical broke ground in 2025 on a USD 50 million plant in Wisconsin to de-risk supply chains and win federal sourcing contracts.

Europe accounted for a significant portion of 2025 sales, led by Germany, France, Italy, Spain, and the United Kingdom, where public health systems reimburse oncologic reconstruction. CE-certified smooth expanders have gained share since the Allergan BIOCELL recall, while MDR surveillance obligations favor companies with established quality systems. Eastern European uptake is rising as EU cohesion funds modernize surgical centers, offering a steady if modest tailwind to the extremity tissue expanders market.

Asia-Pacific is forecast to lead growth at a 6.54% CAGR through 2031 as China, India, South Korea, and Japan expand tertiary beds and attract medical tourists. China’s NMPA has trimmed review cycles for Class III devices, speeding approvals for imported expanders. India’s Ayushman Bharat scheme now reimburses burn and trauma reconstructions, reducing patients' out-of-pocket costs. South Korea’s aesthetic clinics rely on MRI-safe shells to manage rigorous postoperative imaging, while Japan’s aging population lifts mastectomy rates. Local producers such as HansBiomed compete on price, but multinationals dominate through training programs that build surgeon loyalty, ensuring that the extremity tissue expanders market will remain globally diversified.

Competitive Landscape

Five manufacturers capture a significant share of revenue: AbbVie’s Allergan Aesthetics, Mentor Worldwide, Establishment Labs, Sientra, and GC Aesthetics. Establishment Labs posted USD 50.6 million in Q3 2024 revenue, up 20% year over year, driven by Motiva implant and expander penetration across 90 countries. Sientra logged USD 23.8 million in the same quarter despite restructuring, buoyed by MRI-compatible AlloX2Pro shipments. Mentor’s MemoryGel Enhance line widened the anatomic envelope, while Allergan continues to distribute smooth-shell systems following the BIOCELL withdrawal.

Mid-tier firms, including POLYTECH Health & Aesthetics and PMT Corporation, compete via regional approvals and lower capital intensity, whereas Asian entrants such as Kangning Medical leverage cost advantages. Differentiation now concentrates on MRI labeling, nanosurfaces, and integration with ADM or biologic matrices. Regulatory rigor under 21 CFR 878.3510 and the EU MDR increases compliance costs, driving consolidation. Investment in 3D-printed patient-specific expanders and Bluetooth-enabled pressure sensors suggests a pipeline pivot toward smart reconstruction solutions, which could reset pricing power within the extremity tissue expanders market.

Extremity Tissue Expanders Industry Leaders

Mentor Worldwide LLC

AbbVie Inc.

GC Aesthetic

Sientra, Inc.

POLYTECH Health & Aesthetics GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tiger Aesthetics Medical committed USD 50 million to a 120,000-square-foot plant in Franklin, Wisconsin, aiming to double its workforce by 2028 and localize implant and expander production

- December 2024: Mentor Worldwide gained FDA clearance for MemoryGel Xtra implants and CPX4 PLUS Enhance expanders sized 850–1,445 cc.

Global Extremity Tissue Expanders Market Report Scope

As per the scope of the report, extremity tissue expanders are devices used in reconstructive surgery to gradually stretch the skin and soft tissues of limbs. They are inserted under the skin and periodically filled with saline to promote tissue growth. This process creates additional skin for use in reconstructing defects or injuries in the extremities.

The Extremity Tissue Expanders Market Report is Segmented by Product Type (Upper Extremity and Lower Extremity), Application (Breast Reconstruction, Facial Reconstruction, and Other Applications), End-User (Hospitals, Ambulatory Surgical Centers, Cosmetic Clinics, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Upper Extremity Tissue Expanders |

| Lower Extremity Tissue Expanders |

| Breast Reconstruction |

| Facial Reconstruction |

| Others |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Cosmetic Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Upper Extremity Tissue Expanders | |

| Lower Extremity Tissue Expanders | ||

| By Application | Breast Reconstruction | |

| Facial Reconstruction | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Cosmetic Clinics | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the extremity tissue expanders market?

The market is valued at USD 0.86 billion in 2026 and is forecast to reach USD 1.13 billion by 2031.

Which region is growing fastest for extremity tissue expanders?

Asia-Pacific is projected to post a 6.54% CAGR through 2031, outpacing all other regions.

Which product segment holds the largest share?

Upper extremity devices lead with a 46.43% revenue share as of 2025.

Why are ambulatory surgical centers important to growth?

Site-neutral payments and same-day discharge protocols favor ASCs, driving an expected 8.65% CAGR through 2031.

How are manufacturers differentiating new expanders?

They focus on MRI compatibility, nanosurface technology that reduces infection, and size ranges that fit larger patients.

What are the main cost barriers for patients?

Wide variation in commercial payments, high out-of-network charges, and declining Medicare reimbursement increase out-of-pocket exposure.

Page last updated on: