Event Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

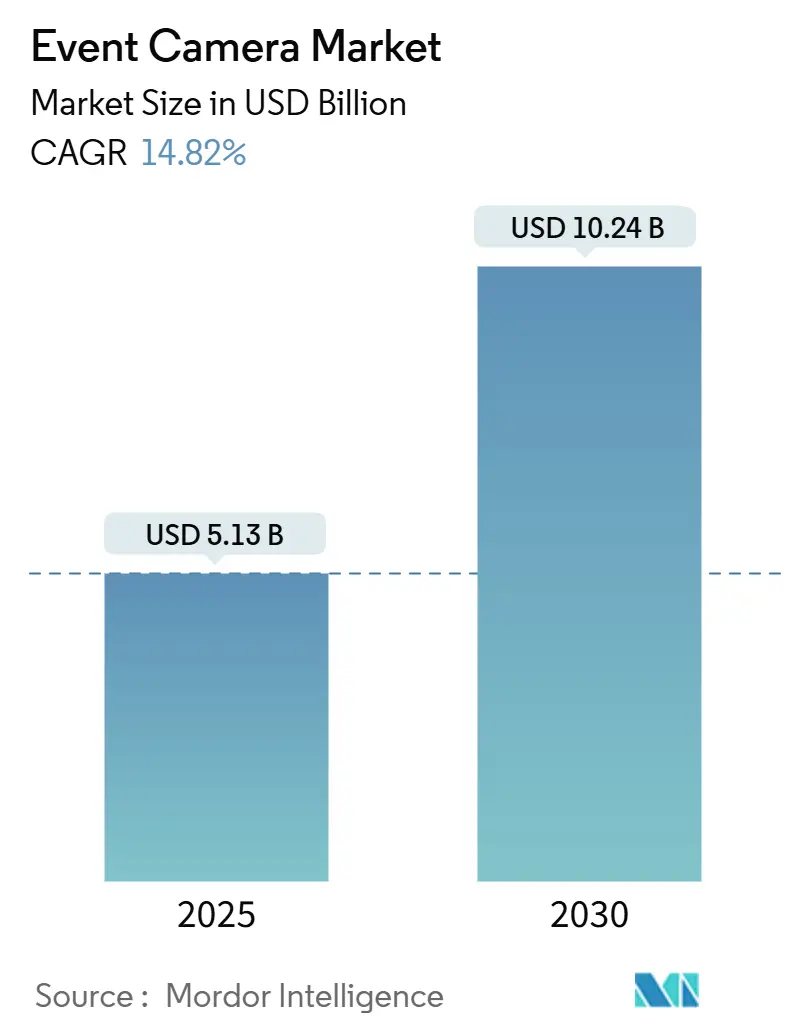

| Market Size (2025) | USD 5.13 Billion |

| Market Size (2030) | USD 10.24 Billion |

| Growth Rate (2025 - 2030) | 14.82% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Event Camera Market Analysis by Mordor Intelligence

The event camera market size stands at USD 5.13 billion in 2025 and is projected to reach USD 10.24 billion by 2030, growing at a 14.82% CAGR. Momentum stems from regulatory pushes in autonomous vehicle safety, demand for microsecond-level industrial inspection, and the need for always-on vision in edge artificial intelligence devices. Venture investment climbed in 2024, and the cost curve is beginning to bend as large foundries shift neuromorphic sensors onto 300 mm wafers. Competitive dynamics are shifting from pure hardware supply to integrated chip-plus-software offerings, with regional opportunities being strongest in the Asia-Pacific and the Middle East. Market participants that combine low-power sensing with spiking-network processing remain best placed to capture incremental design wins.

Key Report Takeaways

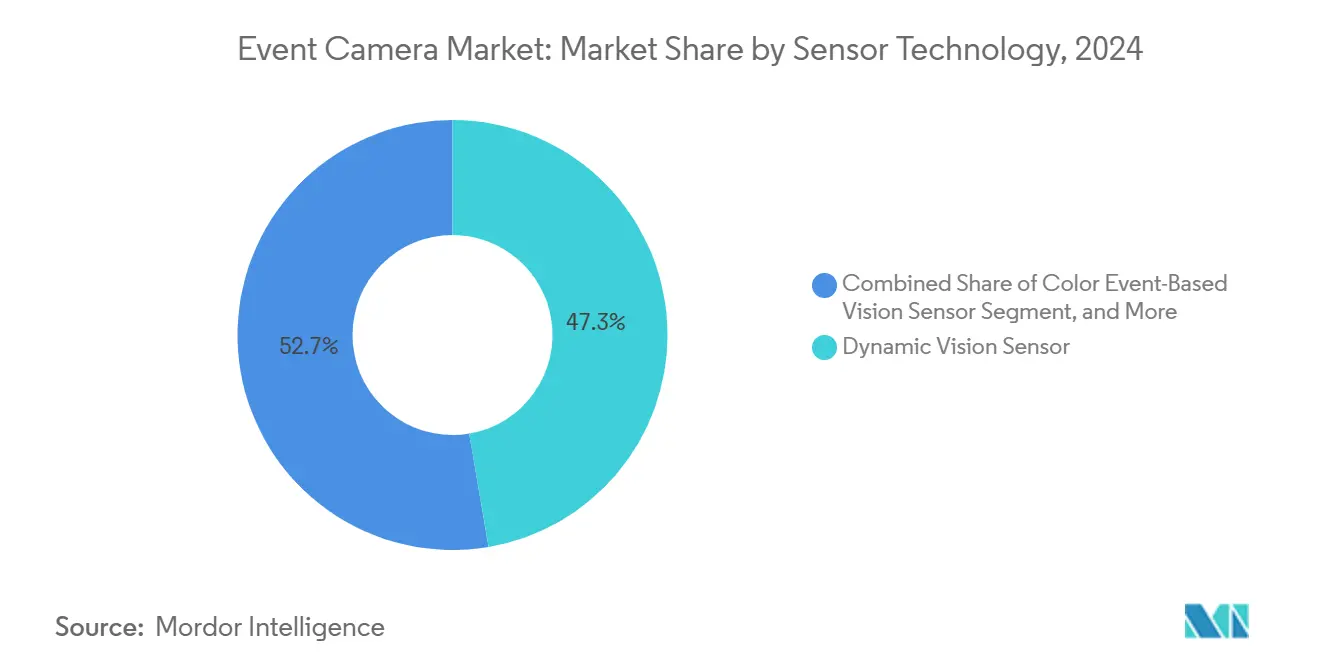

- By sensor technology, Dynamic Vision Sensor designs held 47.32% revenue share in 2024, while Hybrid Event plus Frame architectures are forecast to expand at a 15.36% CAGR through 2030.

- By application, Industrial Automation and Robotics accounted for 33.61% of the event camera market share in 2024, whereas Augmented and Virtual Reality Devices are expected to grow at a 15.66% CAGR through 2030.

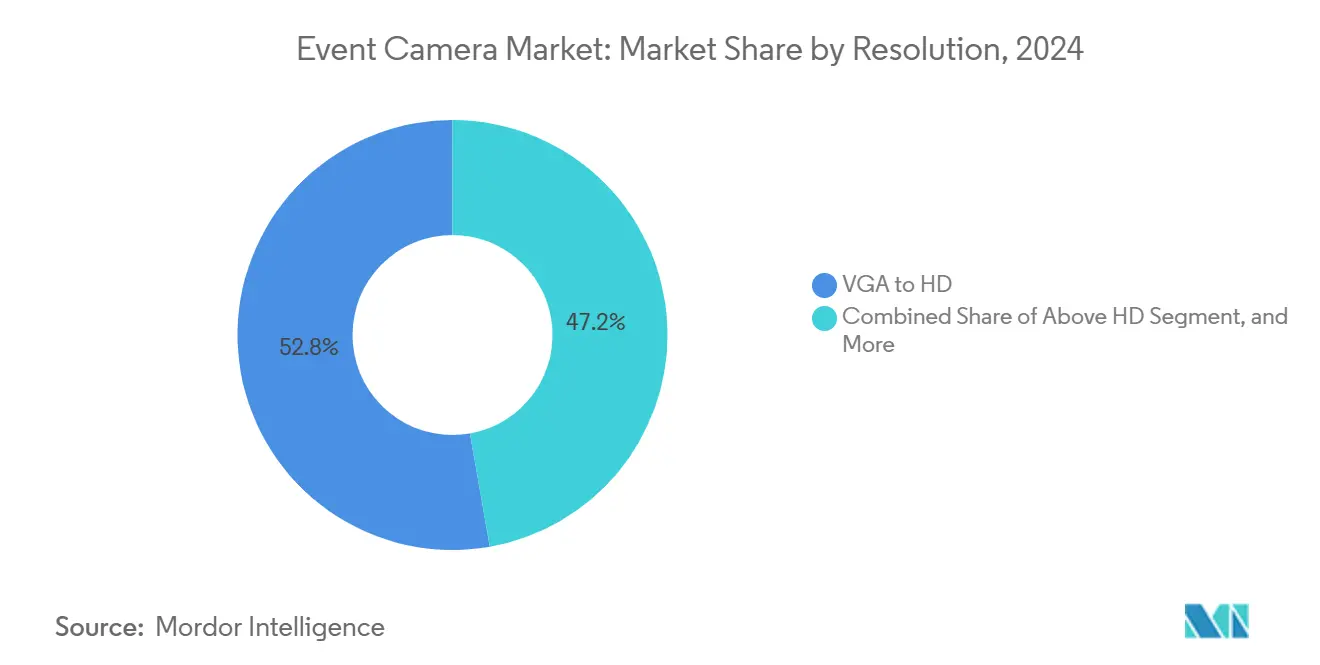

- By resolution, VGA to HD formats captured a 52.78% share of the event camera market size in 2024; above-HD resolutions are projected to rise at a 15.17% CAGR.

- By end-use industry, the Automotive Sector dominated with a 42.74% revenue share in 2024, and the Healthcare and Life Sciences Sector is advancing at a 15.71% CAGR through 2030.

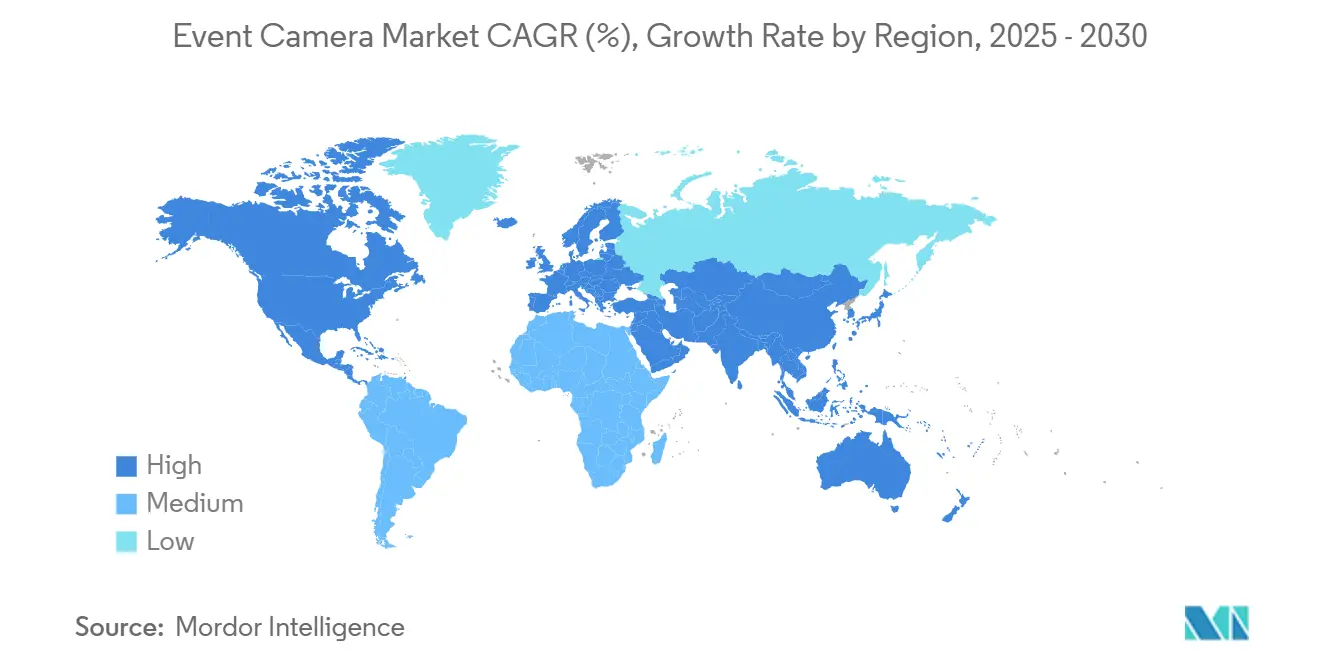

- By geography, the Asia-Pacific region led with 45.87% of 2024 revenue, while the Middle East is expected to be the fastest-growing region at a 15.79% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Event Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption in Autonomous Vehicles Safety Systems | +3.2% | Global, with concentration in North America, Europe, China, Japan | Medium term (2-4 years) |

| Demand for High-Speed Industrial Inspection and Automation | +2.8% | Asia-Pacific manufacturing hubs, Germany, United States | Short term (≤ 2 years) |

| Rising Deployment in Augmented and Virtual Reality Headsets | +2.4% | North America, Europe, South Korea | Medium term (2-4 years) |

| Surge in Low-Power Always-On Vision for Edge AI IoT Devices | +2.1% | Global, early traction in smart-city projects across Middle East and Asia-Pacific | Long term (≥ 4 years) |

| Integration of Event Sensors with Neuromorphic Processors Reducing System Latency | +1.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Regulatory Push for High Dynamic Range Sensors in Adverse-Lighting Surveillance | +1.6% | Middle East, North Africa, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Autonomous Vehicles Safety Systems

Automakers are integrating event cameras into advanced driver-assistance systems to meet looming regulatory deadlines for nighttime pedestrian detection. The 2024 U.S. mandate for automatic emergency braking underscores the need for sensors that can maintain performance under headlight glare and at tunnel exits. Sony and Prophesee plan to start 300 mm wafer production in 2026, promising sub-USD 15 automotive-grade units.[1]Sony Semiconductor Solutions, “Sony and Prophesee Announce Joint Development of Event-Based Vision Sensors,” sony.com Euro NCAP’s 2025 protocol will reward systems that operate effectively in extreme lighting conditions, further increasing design-win activity. The combination of high dynamic range and microsecond latency positions the technology as an enabling component of next-generation safety stacks.

Demand for High-Speed Industrial Inspection and Automation

Manufacturing lines moving faster than 10 m/s create motion blur for conventional imagers; however, event cameras capture edge transitions without the need for strobed lighting. A 2024 deployment in European electronics cut false rejects by 34% and lowered illumination power by 80%. Functional-safety standards now reference asynchronous vision for hazardous environments, accelerating its uptake in the chemicals and oil and gas industries.[2]International Electrotechnical Commission, “IEC 61508 Functional Safety Standard,” iec.ch Collaborative robots respond to human motion within 5 milliseconds, removing the need for safety cages and increasing throughput. Early successes are prompting machine-vision vendors to embed event modules into standard industrial cameras.

Rising Deployment in Augmented and Virtual Reality Headsets

Motion-to-photon delays above 20 ms induce simulator sickness. By sending only pixel-level changes, event cameras enable headsets to deliver sub-10 ms updates, freeing the main processor for rendering tasks.[3]Meta, “Meta Quest 3 Integrates Event Camera Technology for Enhanced Hand Tracking,” meta.com The approach cuts battery drain, a critical limit for untethered devices. Apple’s next headset is expected to follow suit, widening the supplier pipeline. As consumer giants prioritize comfort and run time, component volumes should scale quickly.

Surge in Low-Power Always-On Vision for Edge AI IoT Devices

Remote IoT nodes often operate on harvested energy. Event cameras reduce average draw to single-digit milliwatts, enabling multi-year deployments on primary cells. U.S. Geological Survey field tests increased the life of monitoring stations eightfold by switching from frame sensors to other types. Neuromorphic processors, such as SynSense Speck, consume 1.2 mW while handling gesture recognition. The combination opens doors in agriculture, wildlife observation, and smart buildings where wiring or frequent battery replacement is infeasible.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sensor Cost and Limited Manufacturing Scale | -2.3% | Global, acute in price-sensitive consumer electronics and small-to-medium enterprise industrial segments | Short term (≤ 2 years) |

| Complexity of Event-Based Data Processing Expertise Shortage | -1.8% | Global, particularly acute in North America and Europe where spiking neural network talent is concentrated in academia | Medium term (2-4 years) |

| Absence of Unified Standards for Event Data Interfaces | -1.4% | Global, with heightened impact in automotive supply chains spanning North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Burst-Bandwidth Spikes Overloading Legacy Vehicle Networks | -1.2% | Automotive-focused, concentrated in North America, Europe, China, and Japan where controller area network architectures dominate | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Sensor Cost and Limited Manufacturing Scale

Event camera units are priced between USD 800 and USD 3,500 in 2024, which restricts their adoption to high-value niches. Only a handful of foundries can build the mixed-signal pixels, which limits wafer starts and keeps die costs above USD 20. Until Sony’s 300 mm line ramps up, industrial and consumer applications will rely on smaller suppliers, keeping prices elevated. Consultancy estimates indicate parity with the demands of global-shutter imagers at a die cost below USD 8. Many small manufacturers are waiting for sub-USD 500 modules before retooling their inspection lines.

Complexity of Event-Based Data Processing Expertise Shortage

Address-event streams require spiking neural network skills, which are rare outside academia. An IEEE survey found just 11% of embedded-vision developers had production experience with spiking networks versus 68% for convolutional models. Universities offer limited coursework in neuromorphic engineering, so companies must either retrain their staff or compete for a small talent pool. Toolkits such as Metavision SDK shorten ramp-up time but do not remove the need for temporal-coding expertise. Incompatible timestamp conventions across vendors deepen integration overhead, lengthening development cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Technology: Hybrid Architectures Build Momentum

Dynamic Vision Sensor platforms led revenue growth at 47.32% in 2024, largely driven by maturity in factory inspection and robotics. Hybrid Event plus Frame designs are forecast to grow at a 15.36% CAGR as automotive suppliers retrofit asynchronous capability into legacy electronic control units. The event camera market size for hybrid designs is expected to roughly double during the forecast period, driven in part by the DAVIS346 sensor’s 12,000-unit shipments to research groups and tier-one automotive labs.

Hybrid sensors overlay frame output on event data, allowing object-recognition algorithms to reuse existing convolutional pipelines while adding motion cues. Color Event-Based variants gained traction after CelePixel introduced a 640 × 480 Bayer device, though extra circuitry enlarges die area by 40%. Pure Dynamic Vision Sensor modules still dominate cost-sensitive tasks where monochrome edge detection suffices, but carmakers and consumer electronics firms value backward compatibility enough to pay the premium. As wafer volumes increase, the cost gap between architectures should narrow, broadening the event camera market.

By Application: VR Headsets Accelerate Past Factory Lines

Industrial Automation and Robotics retained 33.61% of the application revenue in 2024, while Augmented and Virtual Reality devices are poised for faster growth at a 15.66% CAGR. Meta’s Quest 3 validation demonstrated that event cameras can achieve sub-10 ms hand-tracking latencies, which 90 fps frame imagers cannot. The event camera market share for AR and VR remains small today, but is expanding rapidly as headset producers prioritize comfort and battery life.

Factory inspection growth is moderating as the installed base matures, shifting the focus toward advanced automotive driver-assistance systems undergoing Euro NCAP certification. Surveillance users appreciate the 120 dB dynamic range that maintains tracking from bright deserts to shaded parking decks. Drone makers value milliwatt operation for longer flight times in obstacle-avoidance tasks. These cross-segment needs ensure a diversified demand mix, insulating the event camera market from end-use cyclicality.

By Resolution: Above-HD Advances With Neuromorphic Chips

VGA to HD formats captured 52.78% demand in 2024, balancing pixel density with 100 Mbps automotive Ethernet limits. Above-HD streams are expected to grow at a 15.17% CAGR once 2.5-Gbps IEEE 802.3ch links reach mass production, thereby increasing the event camera market size in high-resolution tiers. Intel’s Loihi 2 processed 1280 × 720 event streams at 10 µs latency, proving that compute no longer constrains resolution.

Automakers still select VGA sensors for pedestrian detection at 50 m range because they fit existing compute budgets. Healthcare microscopes and precision agriculture will be early adopters of megapixel-class devices where detail trumps bandwidth. As neuromorphic processors reach production silicon from BrainChip and SynSense, sensor resolution is likely to rise further, shifting debate toward cost and power envelopes.

By End-Use Industry: Healthcare Gains Momentum

Automotive users generated 42.74% of 2024 revenue thanks to global safety mandates. The event camera market now benefits from healthcare growing at a 15.71% CAGR, as ophthalmology clinics and neurological monitors exploit microsecond temporal precision. Trials in Zurich hospitals showed earlier detection of diabetic neuropathy using event-based slit-lamp attachments.

Manufacturing and electronics accounted for 28% of shipments in high-speed inspection lines, while defense programs are exploring radiation-tolerant event sensors for satellites. Consumer electronics makers use milliwatt eye-tracking technology to extend the run time of smart glasses. Each vertical value represents distinct combinations of power, latency, and dynamic range, sustaining a multi-industry pull that underpins the broader event camera market.

Geography Analysis

Asia-Pacific generated the largest share at 45.87% of 2024 revenue, buoyed by China’s driver-monitoring mandate and Japan’s airport shuttle pilots. Original equipment manufacturers in the region scale quickly, pushing component volumes and accelerating learning curves. China’s BYD and Geely have begun specifying event cameras in export models headed for Europe, reinforcing their leadership in the Asia-Pacific region.

North America captured roughly 32% of the revenue, driven by compliance programs ahead of the 2029 U.S. emergency braking deadline. Semiconductor clean-room investments also spur demand for microsecond inspection in U.S. fabs. Europe held 18%, with German automakers collaborating with sensor startups on prototypes featuring surround view. While adoption spreads, fragmented standards slow cross-border rollouts until the IEEE P2020 group settles on common event-stream formats.

The Middle East is the fastest-growing region, with a 15.79% CAGR, as Saudi Arabia’s NEOM project embeds event-based surveillance across desert corridors and the United Arab Emirates equips unmanned aerial vehicles for border patrol. Harsh lighting swings make 120 dB dynamic range indispensable, and sovereign wealth funds are willing to underwrite early adoption. South America and Africa remain nascent, with a combined share of under 5%, but infrastructure upgrades tied to smart-city grants could unlock latent demand later in the decade.

Competitive Landscape

Fewer than 25 suppliers shipped commercial event sensors in early 2025, resulting in a moderate market concentration. Prophesee, iniVation, and CelePixel together supplied roughly 60% of units in 2024, yet incumbents such as IDS Imaging and Lucid Vision Labs have begun integrating event modules, raising fragmentation. Prophesee’s USD 50 million Series D secures capital for large-scale automotive production through Sony’s wafer line, signaling imminent cost reductions.

The strategy is shifting toward system-on-chip solutions that integrate sensing with neuromorphic computing. SynSense’s 5 mm Speck chip tailors spiking acceleration to milliwatt budgets, while BrainChip’s Akida 2 focuses on driver monitoring. Patent filings increased to 47 in 2024, primarily focusing on compression and spike coding. Lack of standardization remains a hurdle, but vendors view proprietary ecosystems as customer lock-in moats.

New entrants often emerge from university labs. Opteran raised USD 14 million to commercialize insect-inspired algorithms that slash compute needs by 70%. Defense contracts such as the U.S. Air Force’s space-sensor program give smaller players room to specialize. As barriers to analog pixel design persist, differentiation will come from vertical integration, algorithmic IP, and support ecosystems rather than raw sensor fabrication alone.

Event Camera Industry Leaders

Prophesee SA

iniVation AG

CelePixel Technology Co., Ltd.

Lucid Vision Labs, Inc.

IDS Imaging Development Systems GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Meta launched the Quest 4 headset featuring dual color event cameras and an updated neuromorphic coprocessor, cutting hand-tracking latency to 8 ms while extending battery life by 25% compared with the prior generation.

- June 2025: The International Electrotechnical Commission released an interim guideline defining a common timestamp and polarity convention for event-stream data, a precursor to the planned 2027 IEC 62941-1 standard for neuromorphic vision interchange.

- April 2025: Bosch began series production of driver-monitoring systems that integrate BrainChip Akida 2 neuromorphic processors paired with event cameras, marking the first Tier-One rollout of full spike-based perception in passenger vehicles.

- February 2025: Sony and Prophesee commenced pilot runs on the 300 mm wafer line, delivering the first automotive-grade event sensor samples to Continental for validation in night-time pedestrian detection modules.

Global Event Camera Market Report Scope

The Event Camera Market Report is Segmented by Sensor Technology (Dynamic Vision Sensor, Dynamic and Active Pixel Vision Sensor, Color Event-Based Vision Sensor, Hybrid Event plus Frame Sensor), Application (Autonomous Vehicles and ADAS, Industrial Automation and Robotics, Surveillance and Security, AR and VR Devices, Drones and UAVs), Resolution (QVGA and Below, VGA to HD, Above HD), End-Use Industry (Automotive, Manufacturing and Electronics, Consumer Electronics, Defense and Aerospace, Healthcare and Life Sciences), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Dynamic Vision Sensor (DVS) |

| Dynamic and Active Pixel Vision Sensor (DAVIS) |

| Color Event-Based Vision Sensor |

| Hybrid Event + Frame Sensor |

| Autonomous Vehicles and ADAS |

| Industrial Automation and Robotics |

| Surveillance and Security |

| AR and VR Devices |

| Drones and UAVs |

| QVGA and Below |

| VGA to HD |

| Above HD |

| Automotive |

| Manufacturing and Electronics |

| Consumer Electronics |

| Defense and Aerospace |

| Healthcare and Life Sciences |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Technology | Dynamic Vision Sensor (DVS) | ||

| Dynamic and Active Pixel Vision Sensor (DAVIS) | |||

| Color Event-Based Vision Sensor | |||

| Hybrid Event + Frame Sensor | |||

| By Application | Autonomous Vehicles and ADAS | ||

| Industrial Automation and Robotics | |||

| Surveillance and Security | |||

| AR and VR Devices | |||

| Drones and UAVs | |||

| By Resolution | QVGA and Below | ||

| VGA to HD | |||

| Above HD | |||

| By End-Use Industry | Automotive | ||

| Manufacturing and Electronics | |||

| Consumer Electronics | |||

| Defense and Aerospace | |||

| Healthcare and Life Sciences | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the event camera market in 2025?

The event camera market size is USD 5.13 billion in 2025 and is projected to double by 2030.

What is driving adoption in autonomous vehicles?

Regulations that demand reliable pedestrian detection at night are steering automakers toward high-dynamic-range event cameras able to respond within microseconds.

Which region will grow the fastest through 2030?

The Middle East is forecast to post a 15.79% CAGR, fueled by smart-city surveillance and unmanned-aerial-vehicle deployments.

Which application segment shows the highest growth rate?

Augmented and Virtual Reality devices are expanding at 15.66% CAGR thanks to sub-10 ms motion-to-photon performance and lower headset power draw.

What are the main barriers to wider adoption?

High sensor costs and a shortage of engineers skilled in spiking-neural-network development remain the chief obstacles.

How do event cameras reduce power consumption in IoT devices?

They transmit only pixel-change data, allowing always-on vision at single-digit milliwatt levels that support multi-year battery life.

Page last updated on: