EV Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

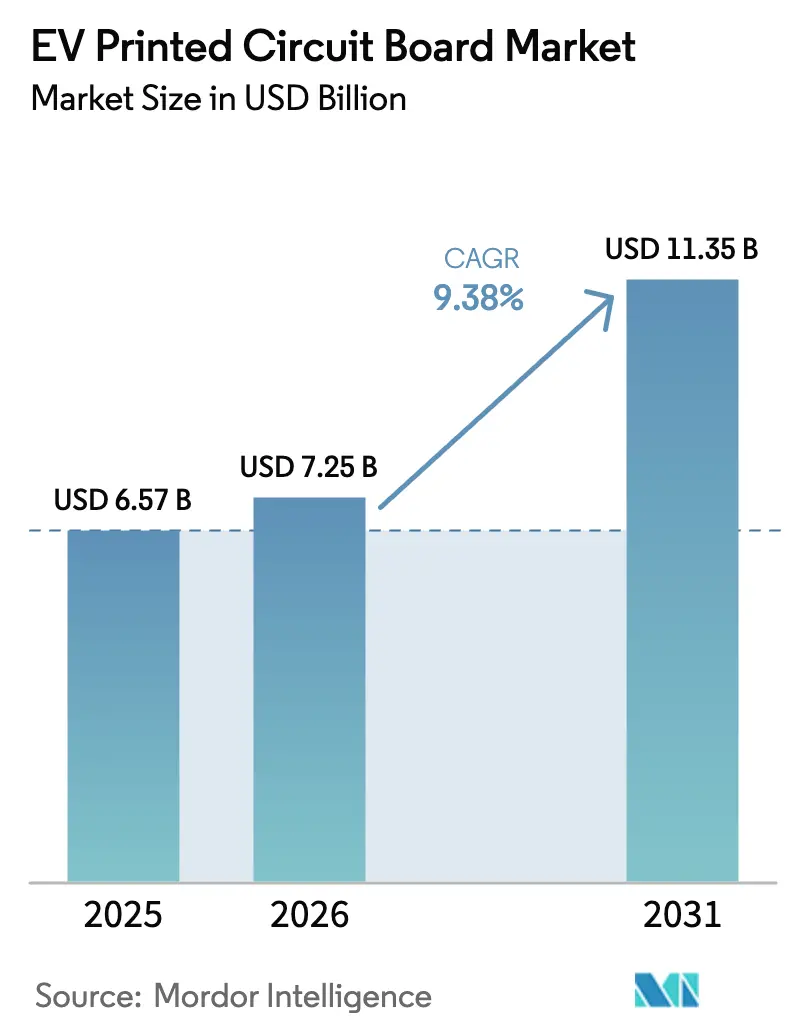

| Market Size (2026) | USD 7.25 Billion |

| Market Size (2031) | USD 11.35 Billion |

| Growth Rate (2026 - 2031) | 9.38% CAGR |

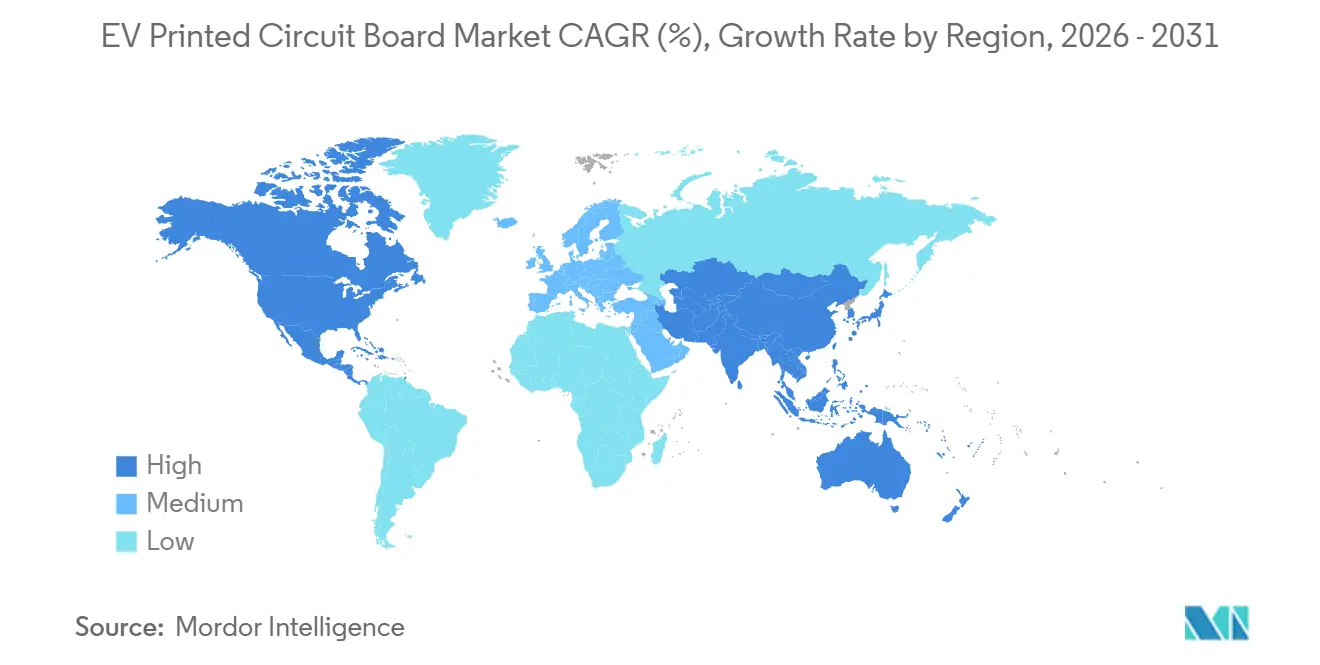

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EV Printed Circuit Board Market Analysis by Mordor Intelligence

The EV Printed Circuit Board Market size is projected to expand from USD 6.57 billion in 2025 and USD 7.25 billion in 2026 to USD 11.35 billion by 2031, registering a CAGR of 9.38% between 2026 to 2031. Strong demand stems from automakers shifting to battery-electric platforms that need larger board area, higher power density, and tighter signal integrity. Adoption of 800-volt vehicle architecture raises average selling prices for multilayer boards, while the parallel build-out of 350-kilowatt public chargers accelerates heavy-copper demand. Government incentive programs in the United States, the European Union, and China are regionalizing supply, pushing fabricators to add capacity closer to end users. At the same time, silicon carbide power modules and embedded-substrate packages are compressing board real estate, forcing traditional suppliers to differentiate through advanced materials and vertically integrated processes.

Key Report Takeaways

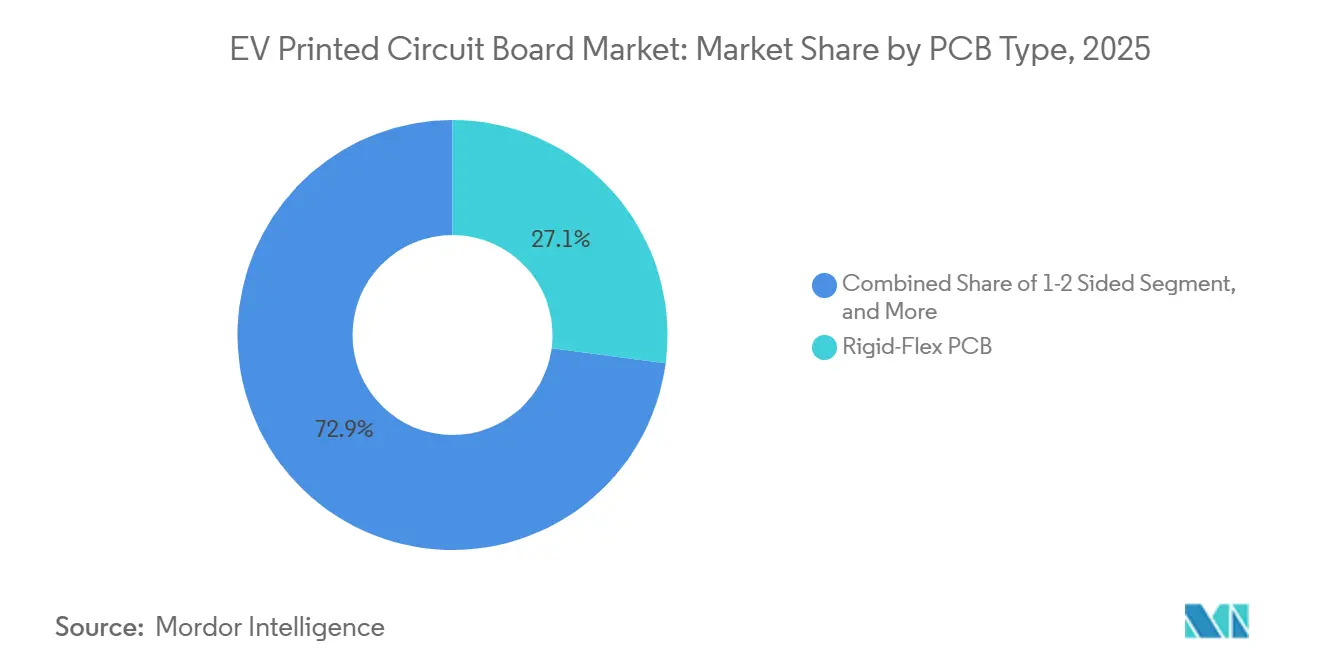

- By PCB type, rigid-flex captured 27.10% of EV PCB market share in 2025, while flexible circuits are forecast to post the fastest 11.21% CAGR through 2031.

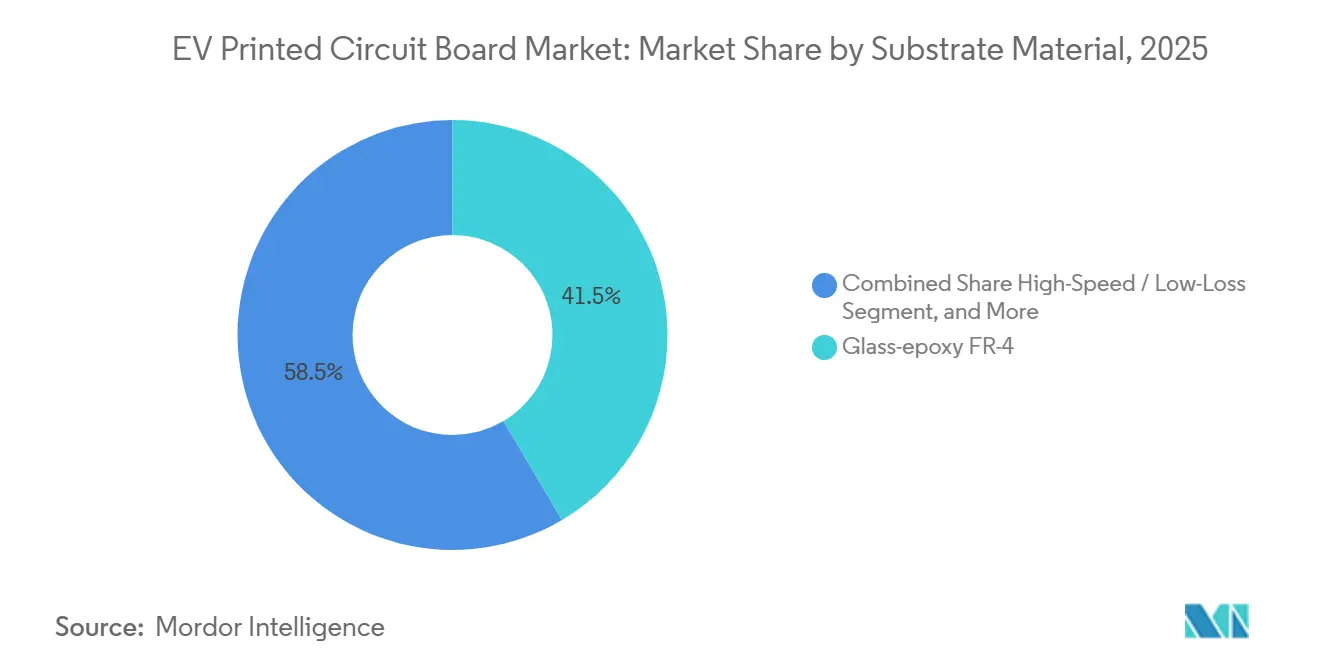

- By substrate material, glass-epoxy FR-4 held 41.50% of the EV PCB market size in 2025, whereas high-speed low-loss laminates are projected to expand at a 10.50% CAGR during the same horizon.

- By geography, Asia Pacific accounted for 82.30% of EV PCB market share in 2025 and is set to grow at a 9.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global EV Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Scale-up of EV Production and Model Variety | +2.8% | Global, strongest in China, Europe, North America | Medium term (2-4 years) |

| Government Incentives Localising PCB Supply Chains | +1.9% | North America, Europe, China | Long term (≥4 years) |

| Shift to High-Voltage 800V Architectures Raising PCB ASP | +2.1% | Global, led by premium segments in Europe and North America | Medium term (2-4 years) |

| Ultra-Fast Public Charging Roll-outs Driving Heavy-Copper Boards | +1.5% | Europe, North America, urban China | Short term (≤2 years) |

| AI-Assisted PCB Design Improving Yield and Time-to-Market | +0.7% | Global, adopted by tier-one fabricators | Short term (≤2 years) |

| Thermal-Management Materials Innovation (Ceramic, IMS) | +0.9% | Global, critical for power electronics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-up of EV Production And Model Variety

Global electric-vehicle sales topped 17 million units in 2024 and are expected to exceed 20 million in 2025, with China producing more than 70% of those vehicles.[1]Source: International Energy Agency, “Global EV Outlook 2025,” iea.org Automakers are converging on skateboard platforms that share battery, inverter, and infotainment electronics across sedans, crossovers, and vans, lifting PCB demand per vehicle to 8-12 square meters. Larger volumes enable once-qualified board designs to be reused across nameplates, yet OEMs use that leverage to push aggressive cost reduction targets. Fabricators counter with automated optical inspection and AI-driven defect classification that keep first-pass yield above 98% while shortening takt time.[2]Source: Siemens Digital Industries Software, “AI-Driven PCB Design and Manufacturing Solutions,” siemens.com The result is a virtuous cycle of higher volume and tighter cost control that supports steady EV printed circuit board market expansion.

Government Incentives Localising PCB Supply Chains

The EU Chips Act mobilized EUR 31.5 billion (USD 35.6 billion) in public-private funding to spur silicon-carbide and substrate production inside the block. The United States CHIPS and Science Act set aside USD 52.7 billion for onshore fabrication, pushing automakers to source boards regionally to capture domestic-content credits. China’s dual-circulation strategy directs subsidies toward PCB plants that meet IATF 16949 and partner with state-owned automakers. These programs fragment a historically Asia-centric supply chain into three blocks, cost-optimized Asia Pacific, prototyping-focused Europe, and localized North America, raising working-capital needs as suppliers stage inventory on multiple continents. In the medium term, localized plants secure demand and improve lead times for domestic OEMs, reinforcing EV printed circuit board market growth in each region.

Shift to High-Voltage 800V Architectures Raising PCB ASP

Models such as the Porsche Taycan and Lucid Air employ 800-volt systems that cut charging times while trimming conductor weight by up to 15 kilograms. Higher voltage tightens creepage and clearance rules, forcing designers to add layers and use 3-ounce copper foil to handle peaks above 400 amperes. A typical 800-volt inverter board costs 30-40% more than its 400-volt predecessor, boosting revenue for fabricators with high-aspect-ratio drilling and controlled-impedance capability. OEMs lock in multiyear pricing agreements to protect margins, shifting material inflation risk to suppliers. Consequently, established fabricators invest in captive laminate lines and drilling automation to secure value and defend share in the EV printed circuit board market.

Ultra-Fast Public Charging Roll-outs Driving Heavy-Copper Boards

The United States NEVI program mandates at least 150 kilowatts per charging port, while many sites deploy 350-kilowatt hardware. CharIN’s high-power charging standard pushes currents to 500 amperes at 1,000 volts, demanding boards clad with 6-10-ounce copper for continuous operation. Heavy-copper PCBs cost up to 60% more than standard designs, yet they enable passive cooling in exposed outdoor cabinets. SAE’s J3400 specification harmonizes Tesla’s connector with CCS, accelerating retrofits of early 50-kilowatt stations. This infrastructure refresh fuels near-term orders for ruggedized boards, expanding the addressable EV printed circuit board market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and Specialty Resin Price Volatility | -1.2% | Global, acute where no long-term contracts | Short term (≤2 years) |

| Automotive-Grade Quality Certification Costs | -0.8% | Global, heavier on new entrants | Medium term (2-4 years) |

| Supply-Chain Fragility for Advanced Substrates | -0.6% | Asia Pacific, Europe | Short term (≤2 years) |

| Competition from Integrated Power Modules (SiC) | -0.5% | Global, premium segments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Copper And Specialty Resin Price Volatility

London Metal Exchange copper futures swung from USD 10,200 per metric ton in May 2024 to USD 9,000 by December 2024, compressing PCB gross margins by up to 300 basis points. Specialty resins such as polyimide and bismaleimide triazine come from a narrow supplier base, limiting price-negotiation leverage. Because automakers lock component pricing 18-24 months ahead, board makers must absorb raw-material swings or hedge, tying up working capital. Smaller shops often lack the balance-sheet strength to ride out sharp commodity cycles, prompting industry consolidation. Cost-plus formulas indexed to LME copper have emerged but remain unpopular among OEMs intent on shielding themselves from volatility.

Automotive-Grade Quality Certification Costs

IATF 16949 audits add USD 50,000-150,000 per facility every three years, while AEC-Q200 reliability testing for passives adds another USD 20,000-40,000 per new design. These fixed costs create a minimum viable scale of roughly 5 million square meters of annual output, discouraging new entrants and favoring established fabricators. Qualification cycles ranging from 12-18 months slow design refreshes, conflicting with software-defined vehicle roadmaps that rely on rapid hardware updates. The certification burden therefore tempers short-term EV printed circuit board market growth while reinforcing the competitive positions of incumbents that already hold multi-site accreditation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Poised for Fastest Expansion

Rigid-flex products led the EV PCB market with 27.10% share in 2025 thanks to their ability to replace connectors inside battery management systems and withstand high vibration. Flexible circuits, however, are projected to deliver the strongest 11.21% CAGR from 2026-2031 as OEMs thread signal paths through cramped doors, dashboards, and seat assemblies. The EV PCB market size for flexible circuits is expected to swell as sensor density rises and assembly lines favor boards that bend without cracking during installation. High-density interconnect (HDI) technology is also gaining ground in radar and camera modules, though elevated cost limits penetration in value-oriented models. Standard multilayer and 1-2-sided rigid boards remain prevalent in low-complexity functions where cost per channel outweighs packaging density.

Advanced IC substrates occupy a niche yet mission-critical role, supporting flip-chip microcontrollers and power-management ICs that drive inverter and charger efficiency. Ajinomoto’s build-up film enables sub-10-micrometer lines, essential for 7-nanometer automotive processors. Metal-core boards bonded to aluminum deliver thermal conductivity above 200 W/m-K for LED headlamps and gate drivers, while ceramic boards serve silicon-carbide power modules operating beyond 175 °C. As architectures consolidate discrete parts into modules, demand for such specialty formats will climb, complementing volume growth in mainstream flexible circuitry.

By Substrate Material: High-Speed Laminates Gain Momentum

Glass-epoxy FR-4 retained 41.50% EV printed circuit board market share in 2025, reflecting its balance of cost, flame resistance, and mechanical strength. Yet radar, lidar, and vehicle-to-everything links depend on laminates with dielectric constants below 3.5 and dissipation factors under 0.005, propelling high-speed low-loss materials toward a 10.50% CAGR through 2031. The EV PCB market size associated with these premium laminates will climb as OEMs prioritize signal integrity that avoids false detections in autonomous driving. Rogers RO4000, Isola Astra MT77, and Panasonic Megtron 7 command prices three-to-five times higher than FR-4 but deliver low insertion loss up to 77 GHz.[3]Source: Panasonic Industry Europe, “Megtron 7 High-Speed Laminates for Automotive Radar Applications,” industry.panasonic.eu

Polyimide, with service temperatures to 260 °C, underpins flexible circuits in battery enclosures that experience continuous thermal cycling. Packaging resins such as bismaleimide triazine and build-up film fuel the high-density packaging substrate segment, which is forecast to grow 9.84% annually as multichip modules proliferate. Aluminum nitride and other ceramic composites fill performance gaps where thermal conductivity and high-frequency dielectric performance converge, although their elevated cost confines usage to luxury and motorsport applications.

Geography Analysis

Asia Pacific dominated the EV printed circuit board market with 82.30% share in 2025 and is projected to expand at a 9.55% CAGR to 2031. China produced more than 12 million electric vehicles in 2024, creating captive demand that Shennan Circuits, Kinwong, and WUS meet with local fabs located near battery and final-assembly plants. Taiwan’s Unimicron and Tripod supply HDI boards and substrates to automotive semiconductor houses, benefiting from proximity to foundries that reduce cycle time. South Korea’s Samsung Electro-Mechanics and Daeduck focus on rigid-flex and multilayer boards for premium EVs, leveraging their ties to Hyundai and LG Energy Solution. Japan’s Meiko and Nippon Mektron lead in flexible and metal-core formats aimed at Western luxury brands.

North America’s EV printed circuit board market is scaling under the CHIPS Act, yet domestic costs remain 15-25% higher than Asian equivalents. TTM Technologies broke ground on a USD 200 million New York expansion in 2025 to supply rigid-flex and heavy-copper boards for 800-volt powertrains. Mexico is emerging as a near-shoring hub aligned with USMCA rules, as Asian fabricators explore new plants to serve Detroit-based OEMs. Europe centers capacity in Germany and Austria, where Schweizer provides embedded-component boards for autonomous-driving ECUs while AT&S channels output from its Malaysian site to European lines, balancing cost and localization needs. The region’s high labor cost restricts competitiveness to low-volume, high-mix programs for motorsport and luxury marques.

In South America, Brazil stands out as the primary player, benefiting from import duties that promote local board assembly and support the domestic market. However, the arrival of laminates from Asia significantly undermines these cost savings, as imported materials continue to play a major role in the supply chain. Meanwhile, the Middle East and Africa, with their still-nascent EV adoption and insufficient board volumes, remain heavily reliant on imports. The low demand in these regions makes greenfield investments economically unviable, further reinforcing their dependence on external suppliers.

Competitive Landscape

In 2025, the top 10 suppliers dominated the EV printed circuit board market, accounting for 45-50% of global revenue. Unimicron, AT&S, and Samsung Electro-Mechanics, through vertical integration, own laminate, fab, and assembly lines, which not only compress lead times but also secure their profit margins. This strategic approach allows these companies to maintain a competitive edge by streamlining production processes and ensuring cost efficiency. TTM and Meiko stand out with their IATF-16949 certifications and strategic co-location with tier-one suppliers, ensuring timely deliveries and fostering strong partnerships with key players in the supply chain. Meanwhile, niche players like Schweizer and Daeduck focus on embedded components and rigid-flex designs, capitalizing on customization for premium pricing. These specialized offerings cater to specific market demands, enabling these firms to carve out a unique position in the competitive landscape.

Technological prowess shapes competitive dynamics in the EV printed circuit board market. AI-driven design tools from Cadence, Altium, and Siemens can reduce engineering hours by as much as 30%, leveling the playing field between midsize and larger fabricators. These advanced tools enhance efficiency and allow companies to allocate resources more effectively, thereby improving overall productivity. Furthermore, automated optical inspections, when paired with machine-learning classifiers, can identify 99.5% of micro-voids and trace defects, significantly reducing the risk of recalls in safety-critical boards. This high level of defect detection ensures reliability and safety, which are critical factors in the automotive industry, particularly for electric vehicles.

However, as silicon-carbide power modules with embedded substrates from Wolfspeed and Infineon begin to replace discrete PCBs in inverters and chargers, board manufacturers are pivoting towards sensing and infotainment assemblies. This shift reflects the evolving demands of the market, where manufacturers must adapt to changing technologies and consumer preferences. Additionally, sustainability initiatives are paving the way for innovative biodegradable substrates, becoming a key differentiator for European OEMs. These environmentally friendly materials align with the growing emphasis on sustainability and regulatory requirements, offering manufacturers an opportunity to meet eco-conscious consumer expectations while gaining a competitive advantage in the market.

EV Printed Circuit Board Industry Leaders

TTM Technologies Inc.

Unimicron Technology Corporation

AT&S AG

Meiko Electronics Co., Ltd.

Nippon Mektron Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron committed USD 300 million to expand automotive IC substrate capacity in Taoyuan, Taiwan, targeting a 40% output increase by Q4 2027.

- December 2025: AT&S completed phase-one of its Kulim, Malaysia, substrate plant, adding 2 million m² of annual capacity for automotive and industrial customers.

- November 2025: Samsung Electro-Mechanics partnered with Hyundai Motor Group to co-develop rigid-flex PCBs that integrate wireless modules, cutting battery-pack weight by 15%.

- October 2025: TTM Technologies secured a USD 150 million contract with a North American automaker to supply heavy-copper boards for 800-volt inverters and chargers.

Global EV Printed Circuit Board Market Report Scope

The EV printed circuit board Market Report is Segmented by PCB Type (Standard Multilayer Rigid, 1-2 Sided, HDI, Flexible Circuits, IC Substrates, Rigid-Flex, and Other PCB Types), Substrate Material (Glass Epoxy FR-4, High-Speed Low-Loss, Polyimide, Packaging Resins, and Other Substrate Materials), PCB Materials (Copper Clad Laminate, and High-Density Packaging Substrate), and Geography (North America, Europe, Asia-Pacific, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (Non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Standard Multilayer (Non-HDI) | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

How large is the EV printed circuit board market in 2026?

The EV printed circuit board market size is USD 7.25 billion in 2026, and it is forecast to climb to USD 11.35 billion by 2031 with a 9.38% CAGR.

Which printed circuit board type is growing fastest in electric vehicles?

Flexible circuits lead growth, advancing at an 11.21% CAGR through 2031 as OEMs route signals through compact door and dashboard spaces.

What is driving higher average selling prices for EV PCBs?

The shift to 800-volt vehicle architectures requires multilayer boards with thicker copper and tighter creepage, increasing ASP by 30-40%.

Why is Asia Pacific dominant in EV PCB supply?

Integrated supply chains, proximity to high-volume EV production, and large domestic fabricators give Asia Pacific 82.30% market share in 2025.

Page last updated on: