Europe VR Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

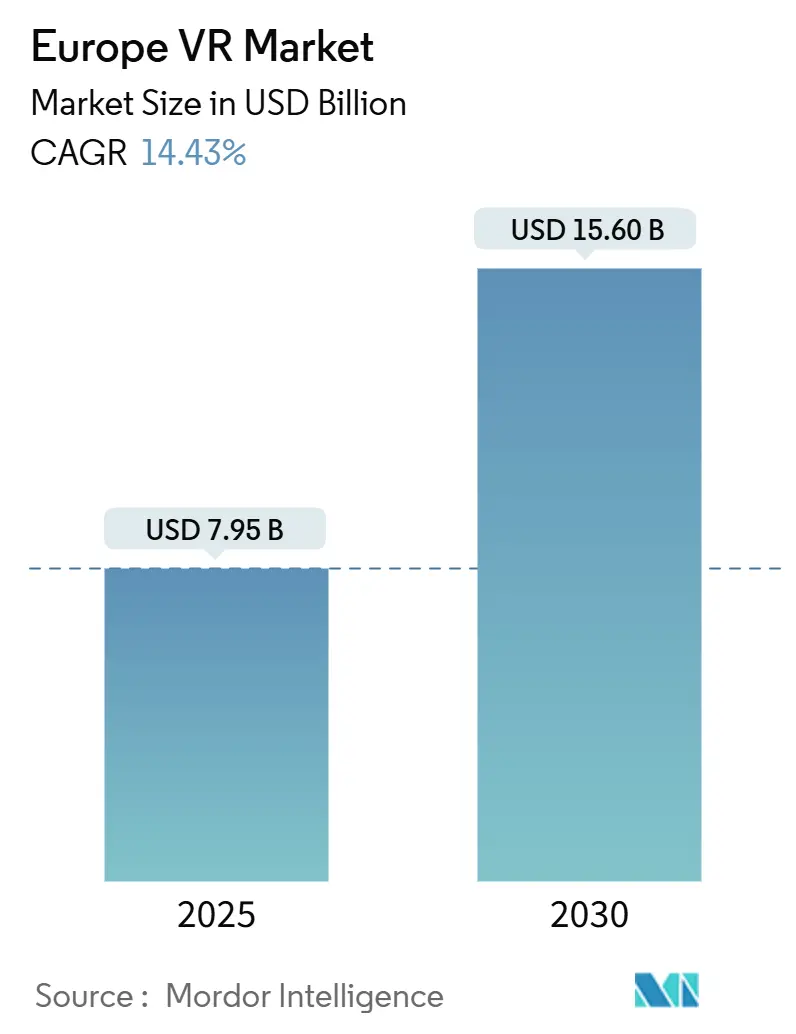

| Market Size (2025) | USD 7.95 Billion |

| Market Size (2030) | USD 15.60 Billion |

| Growth Rate (2025 - 2030) | 14.43% CAGR |

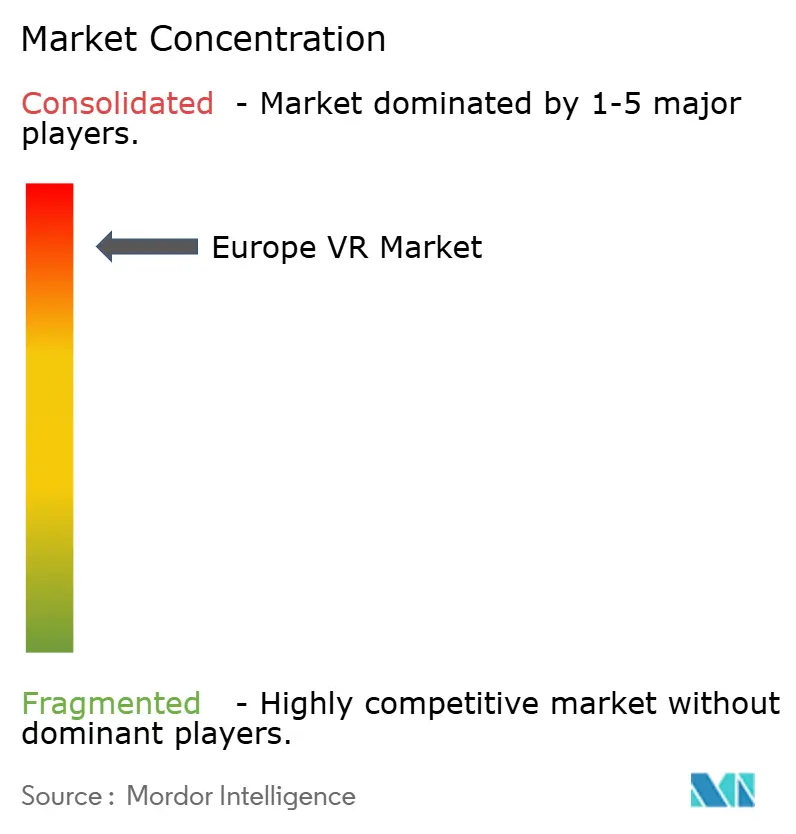

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe VR Market Analysis by Mordor Intelligence

The Europe VR Market size is estimated at USD 7.95 billion in 2025, and is expected to reach USD 15.60 billion by 2030, at a CAGR of 14.43% during the forecast period (2025-2030). Hardware remains the largest revenue contributor, yet accelerated platform monetization and enterprise simulation spending are reshaping value capture. National digitalization grants, mixed-reality productivity suites, and AI-enabled volumetric video pipelines shorten the time-to-market for localized content, boosting developer economics. Declining headset prices below EUR 400 (USD 435) widen consumer access, while mid-range enterprise devices with inside-out tracking achieve procurement preference. Supply-chain fragility tied to non-EU semiconductor vendors persists, but Horizon Europe and the Digital Europe Program channel public funds into home-grown XR components and interoperability frameworks that temper geopolitical risk.

Key Report Takeaways

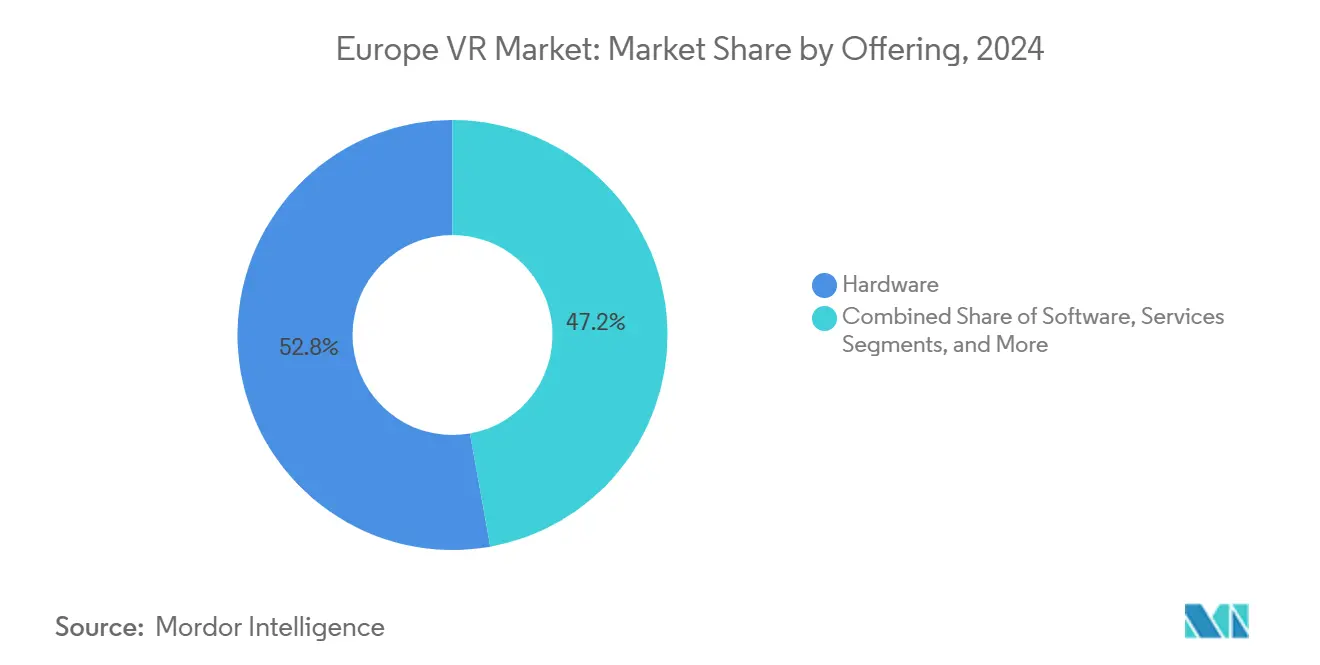

- By offering hardware, 52.8% of the revenue share in the European VR market was captured in 2024, while content platforms are projected to post the fastest growth rate of 17.6% CAGR through 2030.

- By device form factor, stand-alone HMDs accounted for 57.89% of the European VR market in 2024; smart-glasses hybrids are forecast to expand at a 16.98% CAGR through 2030.

- By immersion level, fully immersive solutions accounted for 62.7% of the European VR market in 2024, whereas semi-immersive deployments are projected to advance at a 14.78% CAGR through 2030.

- By distribution channel, online sales accounted for 72.1% of the European VR market in 2024, but offline/retail is projected to grow at a 15.12% CAGR through 2030.

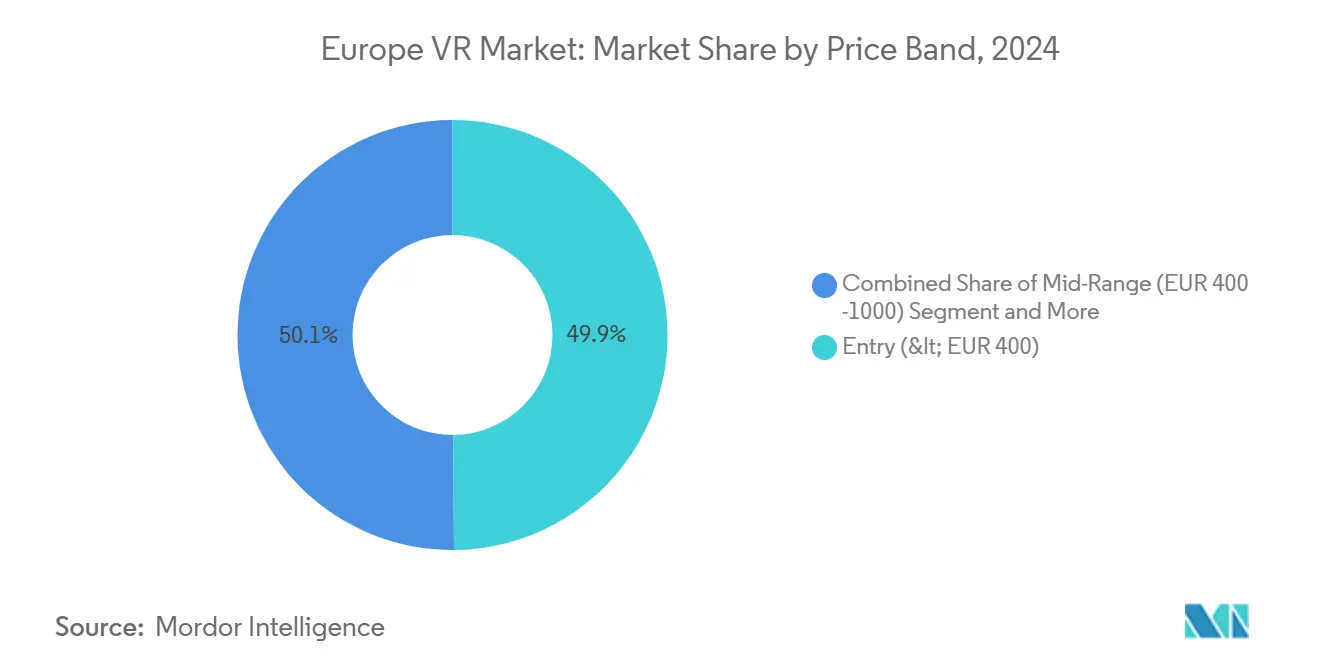

- By price band, entry-tier headsets (< EUR 400) accounted for 49.88% of the European VR market in 2024, while mid-range units (EUR 400–1,000) are climbing at a 15.34% CAGR through 2030.

- By end-user industry, gaming led the European VR market with 46.23% in 2024; education and training are progressing at a 16.11% CAGR through 2030.

- By country, Germany contributed 24.7% in the European VR market in 2024, whereas Spain is the fastest-growing geography, with a 15.4% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe VR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gaming-Led Demand for Affordable Standalone Headsets | +3.2% | Pan-European, strongest in Germany, UK, France | Short term (≤ 2 years) |

| Enterprise Training and Simulation Uptake (Manufacturing, Healthcare) | +2.8% | Germany, France, Italy, Nordics | Medium term (2-4 years) |

| EU Digital-Transformation Funding (Horizon Europe, Digital Europe) | +1.9% | All EU member states, concentrated in Horizon Europe beneficiaries | Long term (≥ 4 years) |

| AI-Driven Volumetric-Video Workflows Cut Content Costs | +2.4% | Content hubs in UK, France, Spain, Poland | Medium term (2-4 years) |

| Mixed-Reality Productivity Apps Localized for EU Languages | +1.7% | Germany, France, Spain, Italy, Netherlands | Medium term (2-4 years) |

| VR-Enabled Cultural-Heritage Tourism Backed by Recovery Funds | +1.3% | Italy, Greece, Spain, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gaming-Led Demand for Affordable Stand-Alone Headsets

Meta’s Quest 3S launch at USD 299 catalyzed a replacement cycle, eliminating the need for EUR 800–1,200 gaming PCs and driving first-time adoption among price-sensitive households in Spain and Poland. [1]Meta Platforms, “Introducing Meta Quest 3S,” meta.com AAA ports now run natively on Snapdragon XR2 Gen 2, pushing publishers to prioritize mobile SoCs. Sony’s PSVR2 shipments fell 25% after the PlayStation install base plateaued, underscoring the shift toward cable-free ecosystems. HTC’s EUR 1,229 Vive Focus Vision lacks consumer content at its price, leaving the sub-EUR 400 tier largely to Meta and rising Chinese vendors.

Enterprise Training and Simulation Uptake (Manufacturing, Healthcare)

German automotive suppliers using Microsoft Dynamics 365 Guides recorded 20–24% productivity gains, validating ROI for immersive work instructions. [2]Microsoft Corporation, “Dynamics 365 Guides Productivity Gains,” microsoft.com EIT Health’s VR Champions program spans 15 countries, reduces surgical error rates, and grants credentials recognized across EU borders. [3]EIT Health, “VR Champions Programme,” eithealth.eu Siemens Healthineers cut technician classroom time by 40% by embedding VR modules, prompting similar rollouts by Philips and GE HealthCare. Enterprise demand has flipped shipment mixes for DPVR and Pico toward B2B.

AI-Driven Volumetric-Video Workflows Cut Content Costs

Volumetric capture once required arrays of 50 or more synchronized cameras and budgets exceeding EUR 100,000 per finished minute, which kept most European studios on the sidelines. Start-ups such as Volograms and Lifecast now utilize neural-radiance-field models to transform standard DSLR footage into photorealistic 3D assets, reducing production costs by up to 70% and enabling mid-tier teams to pitch immersive projects to enterprise clients. Epic Games pushed the trend further in 2024 by integrating MetaHuman Creator into Unreal Engine 5, allowing developers to rig and animate a lifelike avatar in minutes instead of days. Telecom operator Orange applies the same AI up-scaling to convert 2D concert archives into 180-degree experiences that it resells to music labels, which turns dormant footage into fresh subscription revenue. Localization hurdles also shrink because voice-cloning services from Synthesia enable teams to dub a module into German, French, and Italian for one-tenth of the prior costs, allowing a single training app to reach 70% of the European workforce. The upshot is a rapid fall in unit economics that widens the content funnel and feeds device demand across both consumer and enterprise channels.

EU Digital-Transformation Funding Catalyzes Local Ecosystems

Brussels is channeling over EUR 62 million towards home-grown XR stacks through Horizon Europe and the Digital Europe Program, with funding allocated for virtual-world research and skills academies until 2027. These grants target open-source rendering engines, haptic standards, and avatar frameworks, aiming to minimize license fees to non-EU vendors and retain intellectual property within the bloc. The Virtual Worlds Skills Academy, which trains 5,000 developers annually, focuses on GDPR-compliant data handling and accessibility features, set to become mandatory under the European Accessibility Act from June 2025. National digital-innovation agencies match these EU funds, leading to the establishment of XR incubators in mid-sized cities like Lille and Valencia, which cater to local manufacturing clusters. Early indicators reveal a growing presence of European languages in app stores, bridging a cultural nuance gap that previously favored North American publishers. A brief from the London School of Economics suggests that with proactive policy, the EU's GDP could increase by EUR 400 billion by 2031. This potential underscores the strategic importance member states place on VR, viewing it as essential digital infrastructure rather than merely a niche gadget.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Headset Cost and Limited AAA Content Library | -2.1% | Southern and Eastern Europe, price-sensitive segments | Short term (≤ 2 years) |

| Motion-Sickness and Ergonomic Concerns | -1.4% | Pan-European, acute in first-time users and elderly demographics | Medium term (2-4 years) |

| Fragmented EU Language Localization Inflates Dev. Budgets | -1.6% | All EU member states, acute in smaller language markets | Long term (≥ 4 years) |

| Non-EU Semiconductor Reliance Risks Supply Continuity | -1.8% | Supply-chain dependent markets, Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Headset Cost and Limited AAA Content Library

Premium devices costing over EUR 1,000 remain out of reach for many households in Southern Europe, while only 12 AAA VR titles were shipped in 2024 as publishers shifted their budgets to flat-screen live-service games. Ubisoft’s Assassin’s Creed Nexus VR sold just 180,000 units in its first month, reinforcing risk aversion among studios. Fragmented backward compatibility between headset generations further discourages early adopters and hinders the growth of the European virtual reality market.

Motion-Sickness and Ergonomic Concerns

Up to 40% of first-time users experience nausea despite 90 Hz refresh rates, leading developers to deploy teleport locomotion that degrades immersion. A headset mass of 500-600 grams causes neck fatigue after 45 minutes, while the European Accessibility Act requires vendors to accommodate users with balance disorders starting from June 2025. Non-compliance risks fines and narrows the addressable base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Content Platforms Accelerate Monetization

Hardware dominated 52.8% of 2024 revenue, yet subscription-led content hubs are on track for a 17.6% CAGR that will lift their share of the European virtual reality market size. Meta’s Horizon Worlds began revenue-sharing with creators, mimicking Roblox’s flat-screen success. Software licensing from Unity and Unreal added a mid-20s share as European studios ramped up their mixed-reality pipelines. Services such as systems integration grew in the low double digits, with Accenture embedding VR in Industry 4.0 transformations. Hardware margins are compressing as vendors subsidize headsets, whereas platforms earn recurring 30% store commissions and sell in-experience ads.

Content platforms also unlock value in smaller language markets. AI voice cloning reduces localization spend by 90%, letting mid-tier studios profitably address German, French, Italian, and Polish users. HTC’s Viveport Infinity reached 80,000 European subscribers at EUR 12.99 monthly, proving the appetite for all-you-can-consume libraries. Over the forecast period, market power will migrate from device makers to platform operators that aggregate creators, advertisers, and data, reshaping the competitive core of the European virtual reality market.

By Device Form Factor: Smart-Glasses Hybrids Gain Enterprise Traction

Stand-alone HMDs accounted for 57.89% of revenue in 2024, as Quest and Pico units replaced cable-bound predecessors. PC-tethered rigs retained niche simulation roles, while screenless viewers faded to novelty status. CAVE rooms persisted in high-ticket automotive design, and Barco’s six-sided system averaged above EUR 500,000 per installation. The European virtual reality market size for smart-glasses hybrids is projected to grow at the fastest rate, with a 16.98% CAGR, driven by logistics pilots at DHL that have reduced pick-and-pack times by 25%.

Qualcomm’s 2024 Snapdragon AR2 SOC enables sub-50-gram eyewear with on-device AI, pushing eight-hour battery life. Procurement teams now rank weight, passthrough quality, and mobile-device-management compatibility ahead of pure resolution, signaling a structural shift that will redirect R&D dollars toward enterprise-grade smart glasses.

By Immersion Level: Semi-Immersive Gains in Collaborative Workflows

Fully immersive experiences accounted for 62.7% of 2024 spend, but semi-immersive mixed-reality modes are rising at a 14.78% CAGR as automotive and architectural teams demand eye contact during virtual reviews. BMW’s Munich studio blended clay models with Meta Quest Pro passthrough, reducing prototyping time by one-third. The European virtual reality market share for semi-immersive systems will therefore expand, especially as ISO ergonomic guidelines steer enterprises toward ambient-aware solutions.

Passthrough cameras, once exclusive to USD 1,500 headsets, now ship in USD 299 devices, democratizing mixed-reality workflows. Non-immersive 360-degree video remains a lightweight marketing tool but generates marginal revenue. Regulation remains relatively lenient, yet insurance premiums favor semi-immersive deployments that reduce collision risk in shared spaces, thereby reinforcing demand outside of entertainment.

By Distribution Channel: Offline Retail Addresses Trial Barriers

Online portals captured 72.1% of 2024 sales through Amazon and operator bundles, but offline retail is projected to grow at a 15.12% CAGR as demo pods mitigate motion sickness fears. Meta opened permanent Quest trial zones in MediaMarkt and Fnac, converting up to 22% of walk-ins within 30 days. Apple’s appointment-only Vision Pro fitting exemplifies the premium store model, although limited content availability curbed uptake.

Enterprise buyers also demand tactile evaluation under factory noise and lighting. HTC and Varjo operate European showrooms where procurement teams validate data sovereignty and cleaning protocol compliance. As headset ASPs fall, experiential retail will imitate the early smartphone cycle, anchoring brand differentiation and fueling incremental growth for the European virtual reality market.

By Price Band: Mid-Range Expands as Enterprise Standardizes

Entry-tier devices priced under EUR 400 accounted for 49.88% of the 2024 turnover, driven by Quest 3S discounts. Enterprises, however, favor mid-range headsets priced at EUR 400–1,000 because they strike a balance between cost and the required features, including inside-out tracking and fleet-management APIs. This tier is forecast to grow at a rate of 15.34% annually, reinforcing procurement hubs in Germany and France. Premium rigs above EUR 1,000, such as Varjo XR-4, remain vital in defense and medical simulation but form a narrower niche.

HTC’s Vive Business bundle adds EUR 200 per unit yearly for support, turning capex into opex and smoothing budgeting cycles. Apple’s Vision Pro lacks CAD integrations, limiting its premium appeal. Thus, the mid-range becomes the de facto standard for broad-based enterprise rollouts, shaping future economies of scale in the European virtual reality market.

By End-User Industry: Education and Training Surges on Simulation ROI

Gaming retained a 46.23% share in 2024, yet quantifiable benefits in training will propel that segment at a 16.11% CAGR. Clinicians in EIT Health’s VR Champions cohort cut surgical errors 30%, convincing national health services to fund VR labs. Manufacturing uses Microsoft Guides to onboard line workers 24% faster, while logistics teams employ smart glasses to raise throughput.

Healthcare, media, and industrial applications each contribute high single-digit shares, with regulations such as the EU Medical Device Regulation mandating validated competency tools. Retail trials by IKEA and Zara illustrate emerging but still modest revenue. Because simulation yields measurable KPI improvements, procurement committees allocate larger budgets despite macro headwinds, amplifying the non-gaming trajectory of the European virtual reality market.

Geography Analysis

Germany contributed 24.7% of 2024 revenue, driven by automotive design, Industrie 4.0 grants, and a strong R&D spend that equals 3.1% of GDP. Headset vendors tailor GDPR-compliant telemetry that enables manufacturers to log training performance under legitimate interest clauses. Germany’s skill shortage further incentivizes immersive instruction.

Spain is the fastest-growing geography, with a 15.4% CAGR through 2030, as developers digitize UNESCO sites and real estate stakeholders adopt virtual tours, financed by EU Recovery funds. Barcelona-based Immersium has raised EUR 3 million to reconstruct Gaudí landmarks for hotels and cruise lines, underscoring the synergies in tourism. National digital plans also earmark EUR 4 billion for public-sector tech upgrades that include VR kiosks in museums.

The United Kingdom maintains a high teen share due to London’s studio concentration and 25% video-game tax relief, which offsets Brexit-related talent leakage. France leverages CNC subsidies and Orange Immersive Video to scale French-language content across Europe and Africa. Italy combines luxury fashion virtual storefronts with cultural digitization projects, such as the Vatican Museum archive. Collectively, the Nordics, the Netherlands, Belgium, and Poland bring niche strengths that rival those of larger economies in logistics, defense, and gaming IP.

Competitive Landscape

Meta captured 77% of global headset shipments in 2024 and 84% in Q4, solidifying its dominance through sub-USD 300 pricing and exclusive titles. The firm’s Reality Labs has lost more than USD 70 billion since 2021, yet the subsidy model continues to expand its advertising and app-store ecosystem. Competitors pivot toward enterprise niches: HTC bundles device-management subscriptions, Varjo serves aerospace with 60 pixels-per-degree fidelity, and Lynx offers open-source firmware for GDPR-compliant data localization.

Sony’s PSVR2 adapter opened SteamVR access but failed to halt shipment declines amid a limited exclusive catalog. Apple’s USD 4,350 Vision Pro shipped 43% fewer units quarter-over-quarter in Europe due to the lack of native apps under 200, revealing the limits of its premium spatial-computing positioning. Chinese entrants such as DPVR and XREAL post 30% annual growth by undercutting incumbents while matching mixed-reality features.

Technology differentiation now revolves around AI. Meta’s Codec Avatars generate near-photoreal presence from selfies, while Microsoft’s Azure Spatial Anchors enable persistent annotations across devices. Meta filed 147 VR-related patents in Europe during 2024, primarily in eye-tracking and foveated rendering, whereas Qualcomm lodged 63 patents related to wireless streaming. Vendors that align roadmaps with the European Accessibility Act will gain first-mover compliance advantages once the regulation becomes enforceable in June 2025.

Europe VR Industry Leaders

-

Meta Platforms, Inc. (Meta Quest)

-

Sony Interactive Entertainment LLC (PlayStation VR)

-

HTC Corporation

-

Apple Inc.

-

Varjo Technologies Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Meta launched Quest 3S at USD 299, shipping 1.2 million units globally in Q4, with Europe accounting for 30% of volumes.

- September 2024: HTC introduced Vive Focus Vision at EUR 1,229, adding a rear-mounted battery to reduce neck strain in enterprise training.

- July 2024: Apple launched Vision Pro in the UK, Germany, and France at €3,999, but shipments fell 43% quarter-over-quarter.

- June 2024: Sony released a PC adapter for PSVR2, extending compatibility to SteamVR titles at USD 59.99.

Europe VR Market Report Scope

The Europe Virtual Reality Market Report is Segmented by Offering (Hardware, Software, Services, and Content Platforms), Device Form Factor (PC-Tethered HMD, Stand-Alone HMD, Screenless Viewer, CAVE/Immersive Rooms, and Smart-Glasses Hybrid), Immersion Level (Non-Immersive, Semi-Immersive, and Fully-Immersive), Distribution Channel (Online, and Offline/Retail), Price Band (Entry [<EUR 400], Mid-Range [EUR 400-1000], and Premium [>EUR 1000]), End-User Industry (Gaming, Media and Entertainment, Healthcare, Education and Training, Military and Defense, Retail and eCommerce, Real-Estate and Architecture, Automotive and Transportation, Manufacturing and Industrial, and Other End-User Industries), and Country (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Content Platforms |

| PC-Tethered HMD |

| Stand-Alone HMD |

| Screenless Viewer |

| CAVE / Immersive Rooms |

| Smart-Glasses Hybrid |

| Non-Immersive |

| Semi-Immersive |

| Fully-Immersive |

| Online |

| Offline /Retail |

| Entry (< EUR 400) |

| Mid-Range (EUR 400 -1000) |

| Premium (> EUR 1000) |

| Gaming |

| Media and Entertainment |

| Healthcare |

| Education and Training |

| Military and Defense |

| Retail and eCommerce |

| Real-Estate and Architecture |

| Automotive and Transportation |

| Manufacturing and Industrial |

| Other End-User Industries |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Offering | Hardware |

| Software | |

| Services | |

| Content Platforms | |

| By Device Form Factor | PC-Tethered HMD |

| Stand-Alone HMD | |

| Screenless Viewer | |

| CAVE / Immersive Rooms | |

| Smart-Glasses Hybrid | |

| By Immersion Level | Non-Immersive |

| Semi-Immersive | |

| Fully-Immersive | |

| By Distribution Channel | Online |

| Offline /Retail | |

| By Price Band | Entry (< EUR 400) |

| Mid-Range (EUR 400 -1000) | |

| Premium (> EUR 1000) | |

| By End-User Industry | Gaming |

| Media and Entertainment | |

| Healthcare | |

| Education and Training | |

| Military and Defense | |

| Retail and eCommerce | |

| Real-Estate and Architecture | |

| Automotive and Transportation | |

| Manufacturing and Industrial | |

| Other End-User Industries | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe virtual reality market in 2025?

The Europe virtual reality market size is USD 7.95 billion in 2025.

What is the projected growth rate for VR headsets in Europe?

Shipments and revenue are forecast to expand at a 14.43% CAGR from 2025 to 2030.

Which segment will grow fastest through 2030?

Content platforms are expected to post the highest 17.6% CAGR as recurring subscriptions scale.

Why is Spain the fastest-growing geography?

EU recovery grants for heritage tourism and real-estate virtual tours are propelling a 15.4% CAGR.

How does enterprise adoption compare with gaming?

Training and simulation demand now rivals consumer gaming, especially in healthcare and manufacturing.

Which companies dominate the European headset landscape?

Meta leads with 77% of shipments, while Sony, HTC, Pico, and Apple compete in niche enterprise and premium tiers.

Page last updated on: