Europe Recreational Boating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 16.78 Billion |

| Market Size (2026) | USD 17.89 Billion |

| Market Size (2031) | USD 24.67 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Recreational Boating Market Analysis by Mordor Intelligence

The Europe Recreational Boating Market size was valued at USD 16.78 billion in 2025 and estimated to grow from USD 17.89 billion in 2026 to reach USD 24.67 billion by 2031, at a CAGR of 6.64% during the forecast period (2026-2031). The Europe recreational boating market continues to grow despite lingering supply-chain bottlenecks and stricter emissions regulations. Digital boat-sharing platforms, a sharp rise in electric propulsion adoption, and a stream of high-net-worth migrants moving to Mediterranean tech hubs are reshaping demand and encouraging access-based business models.

Key Report Takeaways

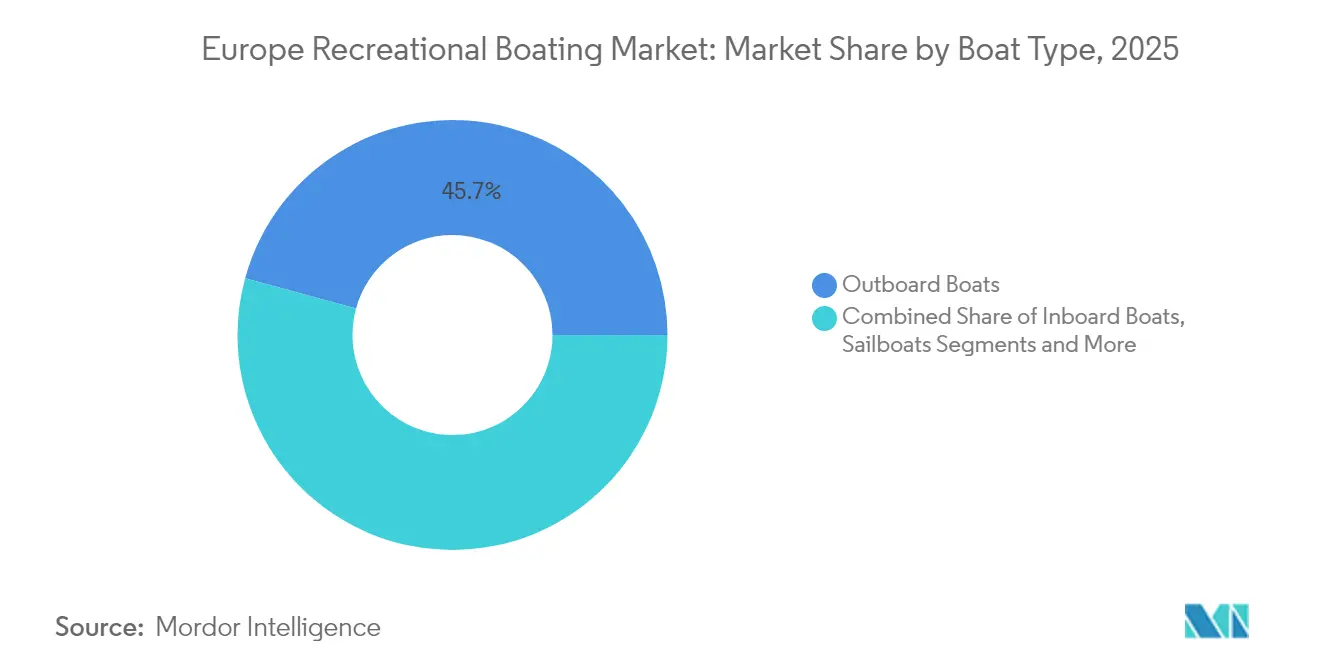

- By boat type, outboard boats led with 45.74% of the Europe recreational boating market share in 2025, whereas inboard boats are forecast to expand at a 6.75% CAGR to 2031.

- By length, the 30-60 feet segment accounted for 45.88% of the Europe recreational boating market size in 2025; vessels under 30 feet are advancing at a 6.69% CAGR through 2031.

- By propulsion system, internal combustion engines dominated with an 86.62% Europe recreational boating market share in 2025, while electric systems are projected to post a 7.05% CAGR over 2026-2031.

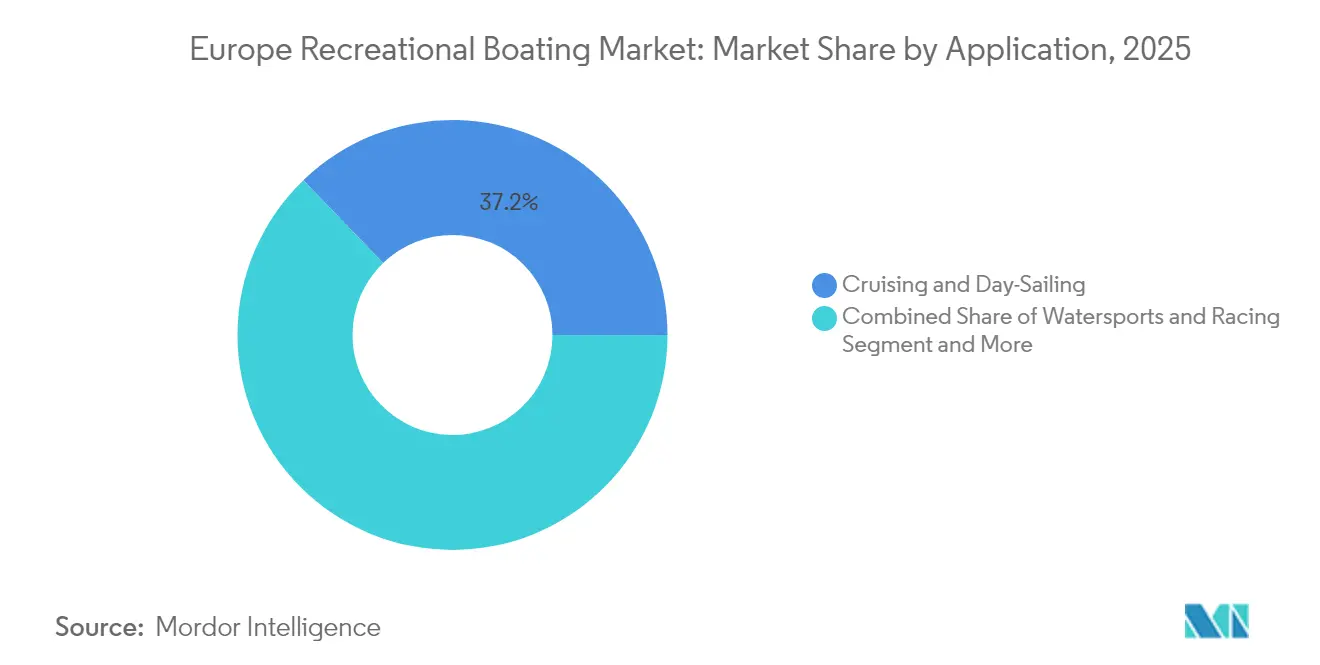

- By application, cruising and day-sailing held 37.20% revenue share in 2025; charter and rental services exhibit the fastest growth at 6.78% CAGR to 2031.

- By distribution channel, dealers and brokers commanded 60.74% revenue share in 2025, yet rental and subscription services are growing at a 6.98% CAGR.

- By country, Italy captured 18.96% revenue share in 2025; Sweden is poised for the highest growth with a 7.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on recreational boating market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Recreational Boating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Participation in Adventure Tourism and Water Sports | +1.2% | Central and Northern Europe, Nordic countries | Medium term (2-4 years) |

| Surge in Charter-Based Fractional Ownership Models | +0.9% | Mediterranean core, expanding to Northern Europe | Short term (≤ 2 years) |

| Expanding Network of Inland Waterways | +0.8% | Germany, Netherlands, France, Poland | Long term (≥ 4 years) |

| OEM Push Toward Low-Noise Electric Outboards | +0.7% | Nordic countries, expanding to Central Europe | Medium term (2-4 years) |

| Digital Boat-Sharing Platforms | +0.6% | Global, with concentration in Mediterranean and Nordic markets | Short term (≤ 2 years) |

| High-Net-Worth Migration to Mediterranean Tech Hubs | +0.5% | Mediterranean, particularly Italy, Spain, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Participation in Adventure Tourism & Water Sports Across Central & Northern Europe

European water-sports tourism is set to grow at a robust CAGR, steering new demand toward group-friendly boats in the 30-60 feet class. Nordic GDP recovery, led by Sweden’s expected rebound to growth in 2026, boosts discretionary spending, while EU-backed inland-waterway investments widen boating access beyond coastal hotspots. The Europe recreational boating market is therefore capturing a new cohort of consumers who favor active itineraries over traditional beach vacations. Operators catering to adventure tourism are increasing fleet renewals, further stimulating sales of mid-size cruisers and performance-oriented water-sports craft.[1]“Monetary Policy Report 2024,” Sveriges Riksbank, riksbank.se

Surge in Charter-Based Fractional Ownership Models Driving First-Time Boaters

GetMyBoat processed USD 75 million in bookings across 150,000 listings, illustrating how peer-to-peer access reduces entry barriers for novice boaters.[2]“Company Fact Sheet,” GetMyBoat Inc., getmyboat.com Groupe Beneteau’s Wiziboat rollout and its Your Boat Club acquisition validate OEM appetite for recurring-revenue models. Marina fees between EUR 1,990 and EUR 9,879 per year for 10-12 meter boats reinforce the economic logic of sharing, while rental channel growth at 7.11% CAGR underscores a structural shift toward access over ownership. These dynamics augment utilization rates of idle private vessels, directly enlarging the addressable Europe recreational boating market.

Expanding Network of Inland Waterways & EU-Funded Marina Upgrades

EU cohesion funds are modernizing docks, electrifying berths, and deepening inland channels. Germany’s Federal Transport Infrastructure Plan earmarks EUR 5.4 billion for waterway enhancement, boosting boat traffic on the Elbe and Oder. Smart-marina concepts that integrate renewable energy and automated waste systems align with EU sustainability directives, making smaller boats under 30 feet increasingly attractive for inland excursions. Improved access is lifting regional dealership revenues and stimulating ancillary service providers in the Europe recreational boating market.

OEM Push Toward Low-Noise Electric Outboards Aligning with Scandinavian Zero-Emission Lakes

ePropulsion shipped nearly 10,000 electric outboards by mid-2024, with more than 50% of its revenue derived from Europe. Scandinavian zero-emission lake policies, coupled with Swedish fuel prices of USD 1.55 per liter, accelerate consumer migration to electric drivetrains. Ferretti’s Riva El-Iseo and Groupe Beneteau’s Oceanis 37.1 electric options confirm a premium segment willing to pay for silent, eco-friendly cruising. Electric propulsion embodies both regulatory compliance and lifestyle appeal within the Europe recreational boating market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Emission and Noise Regulations | -1.1% | EU-wide, particularly affecting smaller manufacturers | Short term (≤ 2 years) |

| Escalating Insurance Premiums | -0.8% | Mediterranean and Northern European coastal regions | Medium term (2-4 years) |

| Skilled-Labour Shortages | -0.6% | Italy and Poland, with spillover effects across EU supply chain | Medium term (2-4 years) |

| Berth Scarcity and Soaring Mooring Fees | -0.4% | Mediterranean core markets, particularly France, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Stage V Emission & Noise Regulations Inflating Compliance Costs

FuelEU Maritime Regulation mandates a 2% greenhouse-gas intensity cut in 2025, rising to 80% by 2050, forcing rapid drivetrain innovation at significant cost. Inclusion of shipping in the EU Emissions Trading System shifts allowance expenses onto charterers through BIMCO clauses, tightening margins for fleet operators. Smaller yards struggle to finance R&D, sparking accelerated consolidation inside the Europe recreational boating market.

Escalating Insurance Premiums After Climate-Driven Loss Events

September 2024 floods in Central Europe produced EUR 1.6-2.1 billion in losses, and UK weather claims pushed premiums up by around two fifth during 2023. Marine insurers pass higher reinsurance and litigation costs to boat owners, especially in storm-prone Mediterranean marinas. Elevated cover charges threaten discretionary purchases and could delay charters, slowing near-term growth in the Europe recreational boating market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Boat Type: Larger Inboard Craft Set the Pace for Premiumization

Current demand skews toward versatile outboards that captured 45.74% revenue in 2025, yet inboard craft are rising fastest at a 6.75% CAGR as affluent buyers pursue performance, space, and integrated luxury features. This shift enlarges the Europe recreational boating market because premium price points lift overall industry value. In 2025, the inboard portion of the Europe recreational boating market size is forecasted to grow exponentially, with Italian builders such as Ferretti and Sanlorenzo introducing hybrid propulsion to entice eco-conscious yacht enthusiasts. Compact personal watercraft retain a niche in Nordic summer cottages, while RIBs supply entry-level charter fleets that funnel new users into ownership pathways.

OEMs are bundling digital navigation, advanced stabilization, and AI-enabled safety into inboard models, increasing appeal among tech-savvy migrants to Mediterranean innovation hubs. Strong charter yields also convince investors to allocate capital toward larger craft, further buoying the Europe recreational boating market. Manufacturers that scale hybrid powertrains across mid-size ranges are likely to win share as regulatory pressure intensifies.

By Length: Sub-30 Feet Vessels Drive Volume, Mid-Size Boats Preserve Value

The 30-60 feet class maintains 45.88% dominance because it balances comfort with marina versatility throughout Europe’s varied coastline. However, sub-30 feet boats will outpace all other lengths at a 6.69% CAGR. High ownership costs motivate urban dwellers to rent smaller craft for weekend trips, boosting turnover at sharing platforms. EU-funded inland-waterway upgrades further stimulate purchases of trailerable models, bolstering the lower-end of the pricing spectrum.

Mid-size craft still capture discretionary upgrades as family cruisers, particularly in France and Spain where multi-day coastal itineraries prevail. Electric conversion economics favor sub-30 feet units because lighter displacement extends battery range, attracting funding from various sources. Conversely, super-yachts over 60 feet remain a luxury niche, adding value rather than volume to the Europe recreational boating market.

By Propulsion System: Electric Gains Momentum

Internal combustion engines remain the baseline, yet their 86.62% share erodes gradually. Electric and hybrid systems achieve 7.05% CAGR as EU climate policies bite. Falling battery prices, improved fast-charging infrastructure, and noise-sensitive Nordic lakes all bolster adoption. Hybrid drives serve as transitional solutions for long-range voyaging, with OEMs like Scania rolling out modular powertrains. Hydrogen remains exploratory, but pilot projects in the Netherlands suggest long-term potential when green hydrogen supply scales.

Manufacturers able to platform electric motors across length categories will capture disproportionate value. Financing programs that bundle battery leasing with charter income further de-risk ownership, widening the appeal of electric craft and reinforcing the growth trajectory of the Europe recreational boating market.

By Application: Charter Expansion Alters Usage Patterns

Cruising and day-sailing held 37.20% revenue in 2025, reflecting Europe’s longstanding leisure habits. Yet charter and rental activities will set the pace at 6.78% CAGR, leveraging digital platforms to optimize fleet utilization. Watersports applications benefit from EU adventure-tourism grants that subsidize operator equipment upgrades, while fishing maintains stable demand amid regulatory quotas.

Charter growth encourages fleets of standardized, sub-30 feet electric boats in urban marinas, which strengthens the business case for infrastructure electrification. Meanwhile, cruising retains its cultural resonance as retirees seek multi-week coastal itineraries, sustaining demand for comfortable mid-size boats within the Europe recreational boating market.

By Distribution Channel: Rental & Subscription Models Reshape Commerce

Traditional dealers and brokers still mediate 60.74% of purchases, but rental subscriptions grow fastest at 6.98% CAGR as consumers prioritize flexibility. Digital contracting, embedded insurance, and AI-driven pricing enable platforms to scale rapidly without owning physical inventory. OEMs respond by launching proprietary services that complement sales, protecting margins in a tightening regulatory landscape.

Direct-to-consumer sales survive in the luxury bracket, where personalized layouts and bespoke interiors remain critical. Hybrid commerce models—combining dealer showrooms, online configuration, and subscription trials—are emerging to capture multiple revenue streams from the expanding Europe recreational boating market.

Geography Analysis

Italy remains the single largest revenue contributor with 18.96% share, aided by globally recognized yacht brands and a robust refit ecosystem that attracts high-net-worth clientele. Fincantieri’s Maestri del Mare program to hire 110 workers by early 2025 highlights the labor shortages that threaten delivery schedules but also underline the sector’s resilience. Luxury-day-cruiser demand is buoyed by Mediterranean tech entrepreneurs seeking leisure outlets, while berth scarcity pushes marina fees upward, reinforcing the shift to charter and fractional models.

Sweden leads growth on the strength of innovation and supportive policy, forecasted to grow at 7.12% CAGR. Electric start-up Candela secured EUR 25 million for production expansion, and Axopar now exports roughly half its output to the US, validating Nordic design appeal. High domestic fuel prices amplify the value proposition of electric propulsion. Denmark and Norway backfill the region’s expertise through zero-emission lake mandates and the Northern Lights Port Alliance, which coordinates alternative-fuel infrastructure.

Germany’s economic headwinds in 2024 dampened discretionary spending, but indications of lower interest rates and a rebound in consumer confidence suggest improved prospects for 2025. Federal water-way investments enlarge the inland boating customer base, especially for trailerable electric craft. France’s dual-coast geography supports both Atlantic and Mediterranean cruising, and Spain’s Balearic Islands sustain charter fleet utilization above 70% during peak season. The UK leverages a deep maritime services ecosystem despite regulatory divergence from EU norms. Poland advances as an export-oriented builder but confronts a tightening labor pool that could curb longer-term capacity additions.

Competitive Landscape

The Europe recreational boating market is moderately fragmented. Groupe Beneteau, Ferretti Group, and Azimut-Benetti are the key players in 2024, yet no single player dominates individually. Market consolidation is underway, Blackstone’s USD 5.65 billion acquisition of Safe Harbor Marinas adds infrastructure depth, while Sanlorenzo purchased Nautor Swan for EUR 48.5 million to sharpen its sailing-yacht portfolio.[3]“Safe Harbor Marinas Acquisition Press Release,” Blackstone Infrastructure Partners, blackstone.com OneWater Marine paid USD 75 million for American Yacht Group, securing exclusive HCB distribution rights.

Technology is a prime differentiator. Brunswick’s Boating Intelligence integrates AI into propulsion and docking systems, and Mercury Marine holds a significant outboard share through constant product refresh.[4]“Consumer Electronics Show Presentation 2025,” Brunswick Corporation, brunswick.com Electric insurgents gain ground, Candela’s hydro-foiling hulls cut energy usage by 80%, and ePropulsion’s European revenue surpassed 50% of total sales.

Digital platforms such as GetMyBoat scale bookings without asset ownership, incentivizing OEM participation in hybrid sales-plus-subscription models. Competitive success will hinge on combining manufacturing excellence with platform economics and low-emission technology leadership.

Europe Recreational Boating Industry Leaders

Groupe Beneteau

Azimut-Benetti Group

Sunseeker International

Ferreti Group

Feadship

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Blackstone Infrastructure completed the USD 5.65 billion acquisition of Safe Harbor Marinas, adding 138 facilities to its portfolio.

- February 2025: OneWater Marine finalized the USD 75 million purchase of American Yacht Group, extending luxury distribution rights.

- January 2025: Brunswick Corporation introduced Boating Intelligence at CES, unveiling autonomous docking and electric concepts.

Europe Recreational Boating Market Report Scope

Recreational boats, commonly known as leisure or pleasure boats, refer to watercraft designed for enjoyment and relaxation. These vessels are not intended for commercial or industrial use but are instead used for activities such as cruising, fishing, water sports, and other recreational purposes.

The scope of the Europe Recreational Boating Market is segmented by Boat Type, Drive Type, Application, and Country. By Boat Type, the market is segmented into Inboard Boats, Outboard Boats, Personal Watercraft Boats, and Other Boat Types. By Drive Type, the market is segmented into IC Engine and Electric Power. By Application, the market is segmented into Water sports and Fishing. By Country, the market is segmented into Germany, United Kingdom, France, Italy, Spain, Denmark, Netherlands, Greece, and the Rest of Europe.

The report offers the market size in value (USD) and forecasts for all the above segments.

| Inboard Boats |

| Outboard Boats |

| Personal Watercraft |

| Sailboats |

| Inflatable & RIBs |

| Other Boat Types |

| Less than 30 Feet |

| 30–60 Feet |

| More than 60 Feet |

| Internal Combustion Engine |

| Hybrid |

| Electric |

| Hydrogen & Alt-Fuels |

| Watersports & Racing |

| Fishing & Angling |

| Cruising & Day-Sailing |

| Charter & Rental |

| Direct OEM Sales |

| Dealers & Brokers |

| Rental & Subscription Services |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Denmark |

| Netherlands |

| Greece |

| Norway |

| Sweden |

| Finland |

| Poland |

| Croatia |

| Russia |

| Rest of Europe |

| By Boat Type | Inboard Boats |

| Outboard Boats | |

| Personal Watercraft | |

| Sailboats | |

| Inflatable & RIBs | |

| Other Boat Types | |

| By Length | Less than 30 Feet |

| 30–60 Feet | |

| More than 60 Feet | |

| By Propulsion System | Internal Combustion Engine |

| Hybrid | |

| Electric | |

| Hydrogen & Alt-Fuels | |

| By Application | Watersports & Racing |

| Fishing & Angling | |

| Cruising & Day-Sailing | |

| Charter & Rental | |

| By Distribution Channel | Direct OEM Sales |

| Dealers & Brokers | |

| Rental & Subscription Services | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Denmark | |

| Netherlands | |

| Greece | |

| Norway | |

| Sweden | |

| Finland | |

| Poland | |

| Croatia | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe recreational boating market?

The market is valued at USD 17.89 billion in 2026 and is set to reach about USD 24.67 billion by 2031.

Which country holds the largest Europe recreational boating market share?

Italy leads with 18.96% revenue share in 2025, driven by its super-yacht manufacturing base.

How fast is electric propulsion growing in the Europe recreational boating market?

Electric systems are forecast to record a 7.05% CAGR between 2026 and 2031 as regulations tighten and battery costs fall.

What segment shows the highest growth by length?

Vessels under 30 feet will expand the quickest at a 6.69% CAGR, buoyed by sharing platforms and inland-waterway upgrades.

How are charter services affecting traditional dealers?

Rental and subscription channels are growing at 6.98% CAGR, prompting dealers to integrate access-based offerings into their models.

What key regulation will impact boat builders from 2025?

The FuelEU Maritime Regulation begins with a 2% greenhouse-gas intensity reduction requirement in 2025, escalating to 80% by 2050, mandating cleaner propulsion solutions.

Page last updated on: