Europe Quantum Computing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.10 Billion |

| Market Size (2030) | USD 3.28 Billion |

| Growth Rate (2025 - 2030) | 24.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Quantum Computing Market Analysis by Mordor Intelligence

The Europe quantum computing market size stands at USD 1.1 billion in 2025 and is projected to reach USD 3.28 billion by 2030, translating into a 24.42% CAGR over the forecast period. National and EU-level public funding, notably the Digital Europe Programme and Horizon Europe, underpins a rapid scale-up of infrastructure and skills pipelines. Hardware remains the biggest revenue contributor, but demand for quantum-as-a-service models is expanding even faster as enterprises tap cloud platforms hosted in Frankfurt, Dublin, Amsterdam and Zurich. Photonic systems gain traction because they sidestep cryogenic cooling, while gate-based architectures continue to dominate high-fidelity research workloads. Regulatory push for quantum-safe cryptography, combined with early proofs of value in portfolio optimization and molecular simulation, align the region’s academic strength with distinct industrial use cases in automotive, finance and life sciences.

Key Report Takeaways

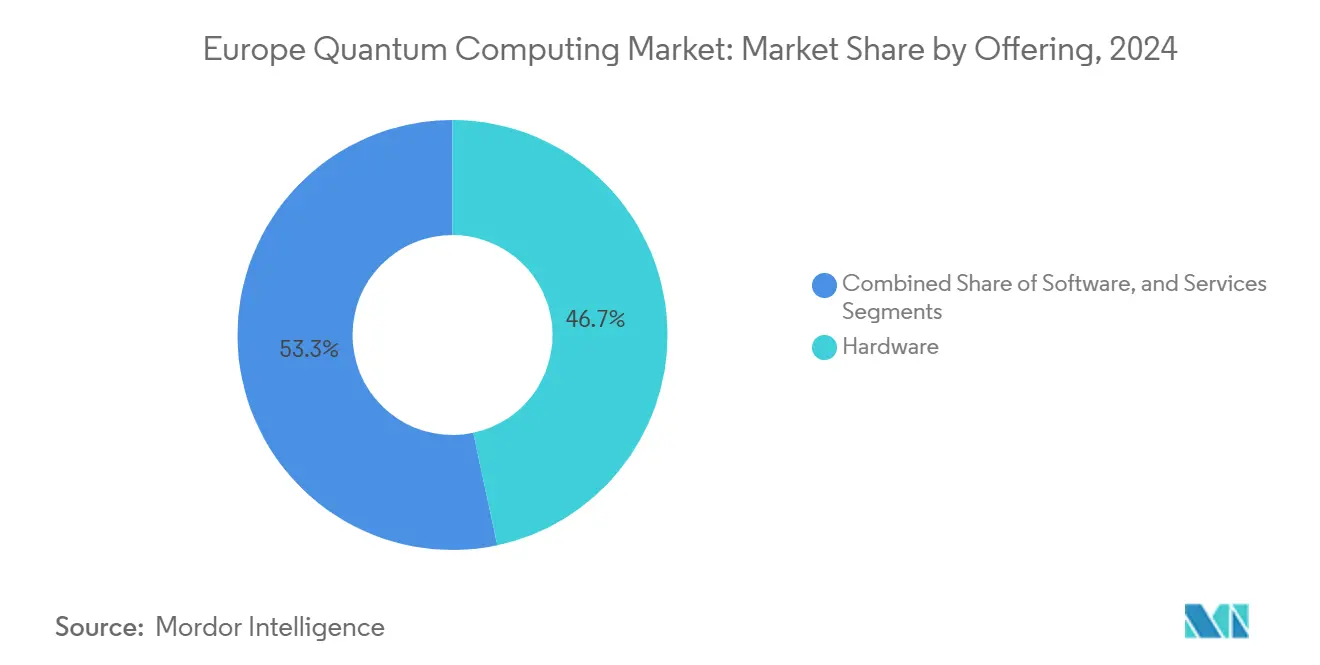

- By offering, hardware held 46.66% of Europe quantum computing market share in 2024, while services is forecast to expand at a 26.11% CAGR to 2030.

- By technology, gate-based systems led with 54.39% revenue share in 2024, whereas photonic platforms are set to grow at a 25.29% CAGR through 2030.

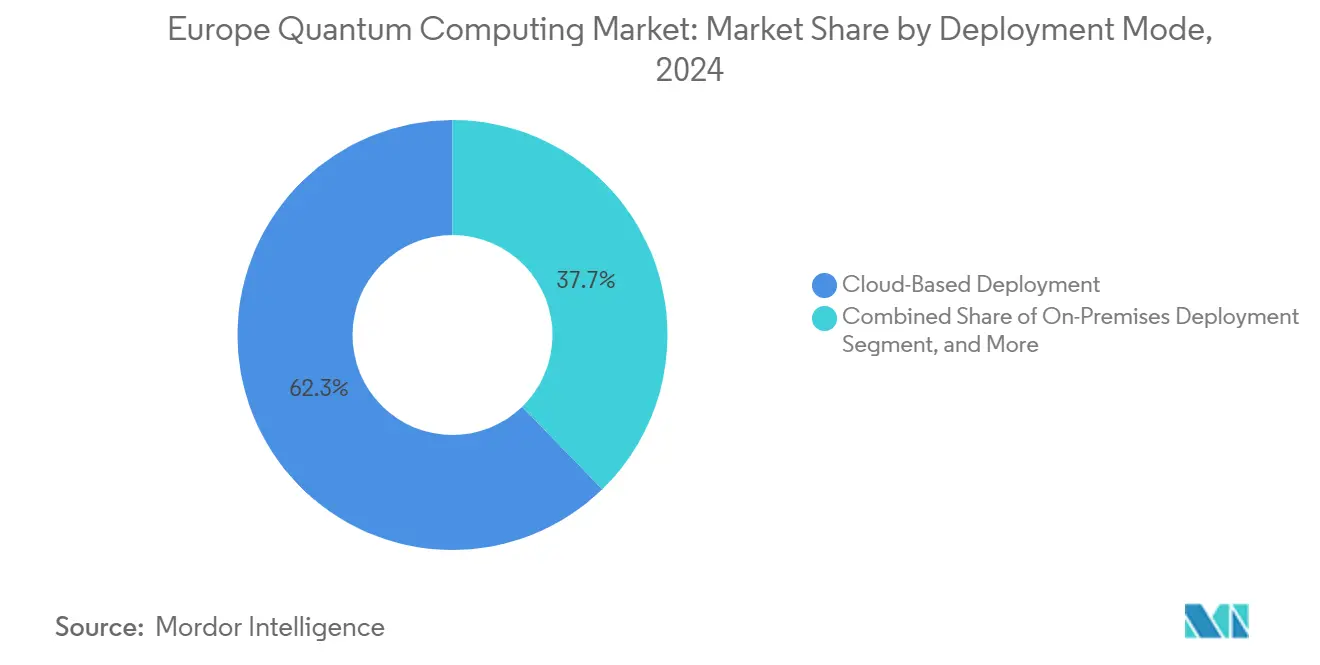

- By deployment mode, cloud-based solutions captured 62.27% share of the Europe quantum computing market size in 2024 and hybrid models are projected to advance at 24.93% CAGR between 2025-2030.

- By application, cryptography and cybersecurity accounted for 28.73% share of the Europe quantum computing market size in 2024; drug discovery and life sciences is moving ahead at a 25.01% CAGR.

- By geography, Germany commanded 21.85% of Europe quantum computing market share in 2024, while Spain is expected to register the fastest 25.55% CAGR through 2030.

Europe Quantum Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Digital Europe Programme quantum funding surge | +4.20% | Germany, France, Netherlands core with spillover to Nordic countries | Medium term (2-4 years) |

| Rapid enterprise adoption for financial risk modeling | +3.80% | Germany, United Kingdom, France financial centers | Short term (≤ 2 years) |

| Local quantum-cloud availability in European data centres | +3.50% | Global with concentration in Germany, Netherlands, Ireland | Medium term (2-4 years) |

| Rising venture capital inflow to European hardware start-ups | +2.90% | Germany, France, United Kingdom, with emerging activity in Spain | Long term (≥ 4 years) |

| Quantum-safe cryptography mandates from European Banking Authority | +2.10% | European Union wide with focus on financial hubs | Short term (≤ 2 years) |

| Cryogenic CMOS control electronics lowering total cost of ownership | +1.80% | Germany, Netherlands, Switzerland manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Digital Europe Programme Quantum Funding Surge

Digital Europe allocates EUR 1.38 billion (USD 1.56 billion) to quantum projects between 2024-2027, creating dedicated calls for cloud testbeds, qubit manufacturing facilities and skills academies.[1]European Commission, “Digital Europe Programme,” digital-strategy.ec.europa.eu Grants awarded to Pasqal, IQM and other European vendors subsidize pilot installations, effectively shortening commercial deployment cycles. The program also co-funds regional competence centers that channel research prototypes into industrial demonstrators, an approach that keeps intellectual property inside the bloc. As a result, enterprises receive direct incentives to trial optimization and simulation workloads on Europe-based hardware, reinforcing the 62.27% cloud deployment share. Taken together, the funding surge contributes the single-largest incremental uplift to the projected CAGR for the Europe quantum computing market.

Rapid Enterprise Adoption for Financial Risk Modelling

Basel III capital rules force banks to improve stress-testing accuracy, driving experiments with quantum Monte Carlo and portfolio optimization. Deutsche Bank, BNP Paribas and Santander have each executed proofs of concept on cloud-resident superconducting back-ends hosted in European data centers.[2]European Banking Authority, “ICT and Security Risk Management Guidelines,” eba.europa.eu Early trials show runtime reductions that shorten overnight risk cycles, a gain that management teams view as directly monetizable. Because most proofs run on pay-as-you-go services, banks sidestep capital expenditure, accelerating time to value. This momentum elevates the cryptography-centric workload share and funnels service revenue to cloud operators, reinforcing the 26.11% CAGR in Europe quantum computing market services.

Local Quantum-Cloud Availability in European Data Centres

New quantum regions in Frankfurt, Dublin, Amsterdam, and Zurich address latency and data-sovereignty constraints for highly regulated verticals. Amazon, IBM, and Microsoft co-locate classical HPC nodes with trapped-ion, superconducting, and photonic processors, enabling hybrid execution paths that keep customer data within EU borders.[3]Amazon Web Services, “European Quantum Regions,” aws.amazon.com Enterprises integrate these endpoints through standard SDKs, blending quantum kernels with existing AI pipelines. Lower latency and GDPR alignment lift utilization rates, favouring subscription models over capex-heavy on-premises builds. Consequently, cloud remains the default entry point for most newcomers, reinforcing the 24.93% CAGR expectation for hybrid configurations.

Rising Venture Capital Inflow to European Hardware Start-ups

Press releases from Pasqal, planqc, and Universal Quantum announced cumulative equity inflows exceeding EUR 280 million (USD 317.9 million) in 2024-2025, financed by sovereign funds and deep-tech investors.[4]Pasqal, “Neutral-Atom Roadmap,” pasqal.com Capital is earmarked for fab expansion, qubit-control electronic, and room-temperature photonics, reducing Europe’s historic dependence on U.S. supply chains. Larger seed rounds allow start-ups to offer quantum-as-a-service early, blurring lines between hardware and managed services. Funding momentum, therefore, widens the addressable market base for European quantum computing and adds resilience to the regional supply network.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of quantum engineering talent | -3.20% | Germany, United Kingdom, France with spillover across EU | Medium term (2-4 years) |

| High capital cost of dilution refrigeration infrastructure | -2.40% | European Union wide, particularly affecting smaller markets | Long term (≥ 4 years) |

| Post-2025 EU export controls on specialised cryogenic components | -1.90% | European Union with impact on non-EU partnerships | Short term (≤ 2 years) |

| Lack of hardware interface standards for multi-vendor integration | -1.50% | Global with particular impact on European enterprise adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Quantum Engineering Talent

Universities graduate fewer than 1,500 quantum-specialized engineers per year, while advertised roles exceed 4,000 across Munich, Paris, Amsterdam and Oxford. Salary premiums of 50% over traditional software roles are now typical, stretching start-up burn rates. Government scholarship schemes exist, but most take several years to translate into workforce supply. The talent gap slows roadmap execution schedules and forces companies to outsource specialized firmware or fabrication tasks outside Europe, undercutting strategic autonomy goals.

High Capital Cost of Dilution Refrigeration Infrastructure

Superconducting processors operate below 20 millikelvin, necessitating dilution refrigerators priced at EUR 500,000-2 million (USD 565,000-2.26 million) per unit. Facilities must also budget for vibration-isolated floors, RF shielding, and helium recovery systems. Such upfront costs lock smaller research labs and SMEs out of on-premises deployments, thereby reinforcing their reliance on the cloud. While photonic platforms promise room-temperature operation, those products remain in early-stage trials, leaving high capital cost as a near-term brake on Europe quantum computing market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Leads but Services Scale Faster

Hardware generated the largest revenue in 2024 as fabrication expansions in Finland, France, and Germany positioned Europe-based fabs to supply regional demand. IQM’s new Helsinki line, funded by EUR 128 million (USD 144.6 million), raised output beyond 5,000 qubits per year. These volumes accounted for a 46.66% share of the European quantum computing market in terms of hardware. Services, however, are forecasted to have the highest 26.11% CAGR as enterprises transition from pilot programs to managed subscriptions. The Europe quantum computing market size tied to services is expected to surpass USD 1 billion by the end of the decade, driven by integration, algorithm design, and training packages. Hardware suppliers are increasingly bundling consulting services to retain customer stickiness, blurring traditional value-chain boundaries.

Processor subsegments show superconducting arrays leading shipments, followed by trapped-ion setups optimized for high-fidelity gate research. Photonics, although smaller, competes on total cost of ownership by eliminating the need for cryogenics. Consulting services grew alongside as banks, pharma majors, and automotive OEMs issued quantum readiness assessments. Application-specific middleware, such as Quantinuum’s TKET and Cambridge Quantum’s cybersecurity suite, drives incremental license revenue. Collectively, these trends accelerate ecosystem maturation and open adjacent revenue pools for cloud providers.

By Technology: Gate-Based Dominance under Photonic Pressure

Gate-based architectures accounted for 54.39% revenue in 2024, thanks to established toolchains and cross-vendor benchmarks. The Europe quantum computing market size derived from gate-based systems remains the anchor for public research grants focusing on error correction and logical qubit scale-out. Photonic processors, led by Pasqal, Orca Computing, and Xanadu, show a powerful 25.29% CAGR outlook as they offer room-temperature operation and fiber compatibility. Neutral-atom and trapped-ion solutions stay attractive for academic consortia that need high gate fidelity over extended coherence windows.

Quantum annealers have established a niche in combinatorial optimization and have found applications in logistics and energy. Topological qubits are still in the pre-commercial stage, but research institutions in the Netherlands and Germany are prototyping Majorana-based devices with backing from the European Commission. Each technology variant influences software stack designs, prompting middleware vendors to deliver abstraction layers that shield users from hardware idiosyncrasies.

By Deployment Mode: Cloud First, Hybrid Next

Cloud-based instances captured 62.27% of revenue in 2024, reflecting a proven pay-per-use model that aligns with the budgets of early-stage experimentation. European expansions by AWS, IBM, and Microsoft guarantee GDPR-compliant processing, which remains a non-negotiable for regulated sectors. Hybrid configurations, where quantum resources interoperate with on-premises HPC clusters, are projected to grow at a 24.93% CAGR as firms integrate quantum kernels into existing AI and simulation workflows. This strategy mitigates data-transfer latency and retains sensitive datasets within local secure zones.

On-premises deployments are rare outside major research centers due to the high cost of infrastructure, but they remain vital for sovereign defense programs. Reference architectures featuring modular cryostats and rack-mount control electronics aim to lower barriers, yet widespread uptake depends on future cost curves. In the meantime, cloud operators collaborate with telecom carriers to deliver dedicated links that ensure sub-10 ms round-trip times, a crucial requirement for near-real-time financial workloads.

By Application: Cryptography Leads, Life Sciences Accelerates

Cryptography and cybersecurity represented 28.73% revenue share in 2024, driven by European Banking Authority directives that compel institutions to adopt quantum-safe standards. Quantum key distribution pilots along major fiber corridors in Germany and France validate readiness for production rollouts. Drug discovery and life sciences are projected to hold the highest 25.01% CAGR outlook, as companies such as Roche and Sanofi utilize quantum simulation to evaluate molecular conformations more efficiently than classical methods. Optimization applications remain widespread across manufacturing scheduling and supply chain routing, while financial modelling benefits directly from variance reduction in Monte Carlo simulations.

Material science research leverages quantum algorithms to study battery cathode chemistries, supporting the EU’s Green Deal objectives. Government and defense projects focus on satellite-based quantum communication and inertial navigation. Collectively, these workloads diversify revenue streams, ensuring that no single vertical dominates demand over the forecast period.

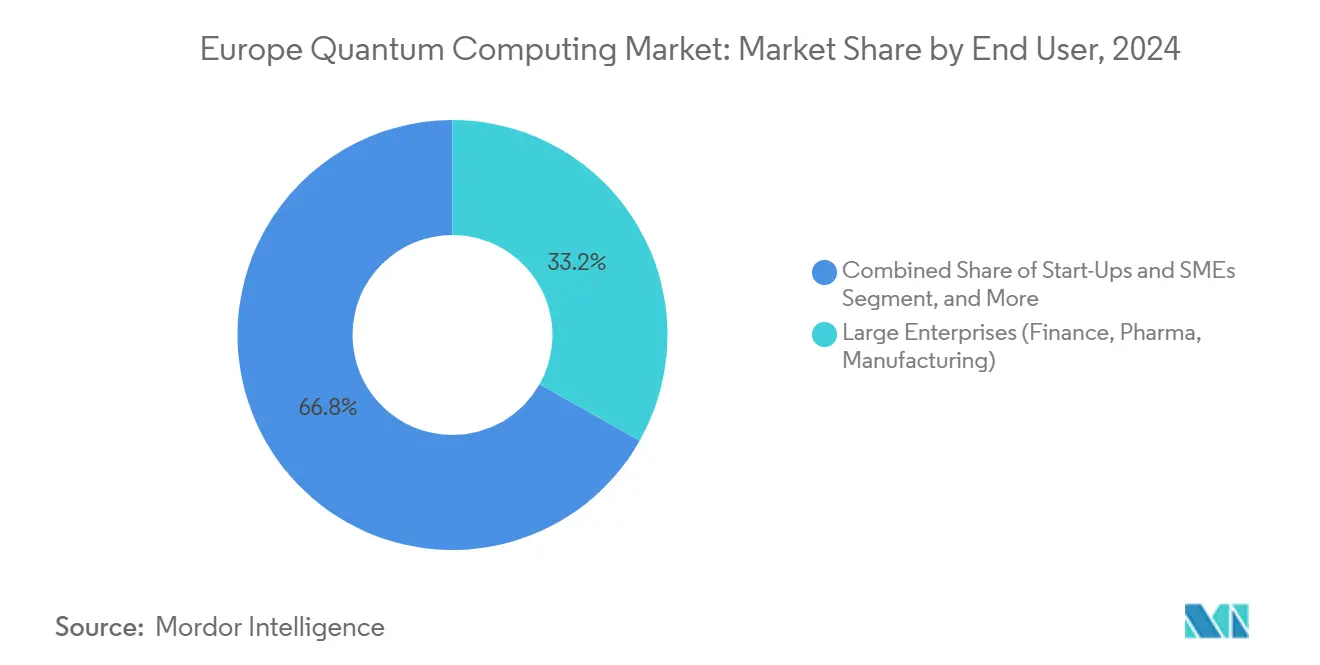

By End User: Enterprises Hold Share, SMEs Drive Growth

Large enterprises in finance, pharmaceuticals, and automotive secured a 33.19% revenue share in 2024 as they transitioned proof-of-concepts into limited production on cloud platforms in the Europe quantum computing market. Start-ups and SMEs boast the fastest 25.89% CAGR, empowered by quantum-as-a-service models that remove capex hurdles. Academic and government research labs continue to play a foundational role by nurturing talent and delivering early algorithmic proofs. Defense agencies maintain strategic projects in secure communication and quantum radar, supported by the European Defence Fund’s EUR 245 million allocation.

Corporate participation is deepening through joint development agreements. BMW collaborates with Pasqal on battery research, while BASF works with Quantinuum on catalysis. These cross-sector alliances shorten learning curves for SMEs that integrate into larger supply chains, reinforcing ecosystem density around flagship industry clusters.

Geography Analysis

Germany generated the largest revenue share at 21.85% in 2024, anchored by a EUR 2 billion national program that funds full-stack development from qubit fabrication to software toolchains. Partnerships between Max Planck institutes and OEMs such as Volkswagen yield early commercial pilots in supply chain optimization. Munich hosts the Federal Quantum Computing Hub, a facility that houses multisource hardware, providing pay-per-use access to universities and corporations alike. International collaboration agreements with Finland and the Netherlands broaden the supply network for cryogenics and control electronics.

Spain registers the highest 25.55% CAGR, propelled by Barcelona Supercomputing Center’s quantum division and a dynamic start-up scene in Catalonia. Qilimanjaro’s coherent annealing prototypes attract logistics and finance pilots, while national grants subsidize SME experimentation vouchers. The favorable growth trajectory stems from a tight loop between academic researchers, local investors and industrial anchor clients in aerospace and tourism. Spain’s progress demonstrates that smaller economies can leapfrog through cloud and shared infrastructure models.

The United Kingdom remains a heavyweight with Oxford and Cambridge universities feeding talent into spinouts such as Oxford Quantum Circuits and Universal Quantum. Post-Brexit funding continuity is ensured via the GBP 1 billion National Quantum Strategy, sustaining collaborations with European counterparts on joint Horizon Europe calls. France benefits from the EUR 1.8 billion France Quantum Plan that prioritizes neutral-atom research, while Italy, the Netherlands and Nordic states specialize in quantum networking and sensing niches. Collectively, the diversity of national strategies creates a mosaic of competency centers that, when interconnected, elevate the overall competitiveness of the Europe quantum computing market.

Competitive Landscape

The Europe quantum computing market exhibits moderate concentration as hyperscale cloud providers coexist with regional hardware champions. IBM, Google, and Microsoft leverage their global R&D capabilities to maintain first-mover advantages in gate-based and error-corrected roadmaps. European firms, such as IQM and Pasqal, counter this trend by maintaining geographic proximity to automotive, pharmaceutical, and energy clients, and tailoring their systems to workload-specific performance metrics. Photonic entrants, such as Orca Computing and Xanadu, challenge incumbents by eliminating cryogenic bottlenecks and aligning with existing telecom infrastructure.

Strategic alliances proliferate. IQM partners with Ato to integrate superconducting processors into classical HPC centres, while Pasqal teams with Siemens on industrial optimization software. Patent analytics from the European Patent Office indicate that Europe generated 1,247 quantum-related filings in 2024, accounting for 23% of global filings related to quantum technology.

The pipeline spans error correction, quantum interconnects, and cryogenic control, signalling future competition beyond raw qubit counts. Overall, suppliers tend to lean toward vertical integration to secure differentiation; however, the open-source nature of many software tools prevents lock-in, keeping switching costs manageable for end-users.

Europe Quantum Computing Industry Leaders

IBM Corporation

Quantinuum Ltd.

IonQ Inc.

D-Wave Quantum Inc.

Pasqal SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Nordic quantum initiative QuNorth was launched with an investment of USD 88 million to deploy and operate a commercial-scale quantum computer in Denmark, in partnership with Microsoft and Atom Computing.

- March 2025: The EuroHPC Joint Undertaking signed a procurement contract for a new quantum computer to be installed in Italy, representing an investment of approximately USD 150 million, with Pasqal selected to deliver a neutral-atom quantum system starting at 140+ qubits.

- January 2025: Alice & Bob, a France-based quantum computing startup specializing in fault-tolerant superconducting qubits, raised USD 110 million in a Series B funding round to accelerate development of a commercially useful quantum computer by 2030.

- January 2025: The EQUSPACE consortium received USD 3.5 million in funding from the European Innovation Council Pathfinder Open program to advance scalable silicon-based quantum computing technologies across multiple EU research institutions.

Europe Quantum Computing Market Report Scope

The Europe Quantum Computing Market Report is Segmented by Offering (Hardware, Software, and Services), Technology (Quantum Annealing, and More), Deployment Mode (On-Premises, Cloud-Based, and Hybrid), Application (Cryptography and Cybersecurity, and More), End User (Government Research Institutions, Academic and Research Universities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Quantum Processors | Superconducting Qubits |

| Trapped Ions | ||

| Quantum Dots | ||

| Other Quantum Processor Hardwares | ||

| Quantum Annealers | ||

| Quantum Sensors and Devices | ||

| Software | Quantum Algorithms | |

| Quantum Simulation Software | ||

| Quantum Cryptography Software | ||

| Middleware and Development Tools | ||

| Services | Consulting | |

| Integration | ||

| Quantum-As-A-Service (QaaS) |

| Quantum Annealing | |

| Gate-Based Quantum Computing | Superconducting |

| Trapped IoN | |

| Topological Qubits | |

| Photonic Quantum Computing | |

| Other Emerging Technologies |

| On-Premises Deployment |

| Cloud-Based Deployment |

| Hybrid Deployment |

| Cryptography and Cybersecurity |

| Optimization Problems |

| Drug Discovery and Life Sciences |

| Material Science |

| Financial Modeling and Risk Analysis |

| Artificial Intelligence and Machine Learning |

| Government and Defense Applications |

| Government Research Institutions |

| Academic and Research Universities |

| Large Enterprises (Finance, Pharma, Manufacturing) |

| Start-Ups and SMEs |

| Defense Agencies |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Offering | Hardware | Quantum Processors | Superconducting Qubits |

| Trapped Ions | |||

| Quantum Dots | |||

| Other Quantum Processor Hardwares | |||

| Quantum Annealers | |||

| Quantum Sensors and Devices | |||

| Software | Quantum Algorithms | ||

| Quantum Simulation Software | |||

| Quantum Cryptography Software | |||

| Middleware and Development Tools | |||

| Services | Consulting | ||

| Integration | |||

| Quantum-As-A-Service (QaaS) | |||

| By Technology | Quantum Annealing | ||

| Gate-Based Quantum Computing | Superconducting | ||

| Trapped IoN | |||

| Topological Qubits | |||

| Photonic Quantum Computing | |||

| Other Emerging Technologies | |||

| By Deployment Mode | On-Premises Deployment | ||

| Cloud-Based Deployment | |||

| Hybrid Deployment | |||

| By Application | Cryptography and Cybersecurity | ||

| Optimization Problems | |||

| Drug Discovery and Life Sciences | |||

| Material Science | |||

| Financial Modeling and Risk Analysis | |||

| Artificial Intelligence and Machine Learning | |||

| Government and Defense Applications | |||

| By End User | Government Research Institutions | ||

| Academic and Research Universities | |||

| Large Enterprises (Finance, Pharma, Manufacturing) | |||

| Start-Ups and SMEs | |||

| Defense Agencies | |||

| By Geography | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

Key Questions Answered in the Report

How large is the Europe quantum computing market in 2025?

The Europe quantum computing market size is USD 1.1 billion in 2025.

What CAGR is expected for quantum computing revenue in Europe through 2030?

Revenue is forecast to grow at a 24.42% CAGR between 2025 and 2030.

Which deployment model generates most spending today?

Cloud-based quantum-as-a-service models hold 62.27% revenue share as of 2024.

Which European country currently leads adoption rates?

Germany leads with 21.85% market share, helped by a EUR 2 billion federal program.

What segment is expanding the fastest?

Services is projected to record the highest 26.11% CAGR through 2030.

Why are photonic processors attracting interest?

They operate at room temperature, removing costly cryogenic systems and accelerating practical deployments.

Page last updated on: