Europe Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

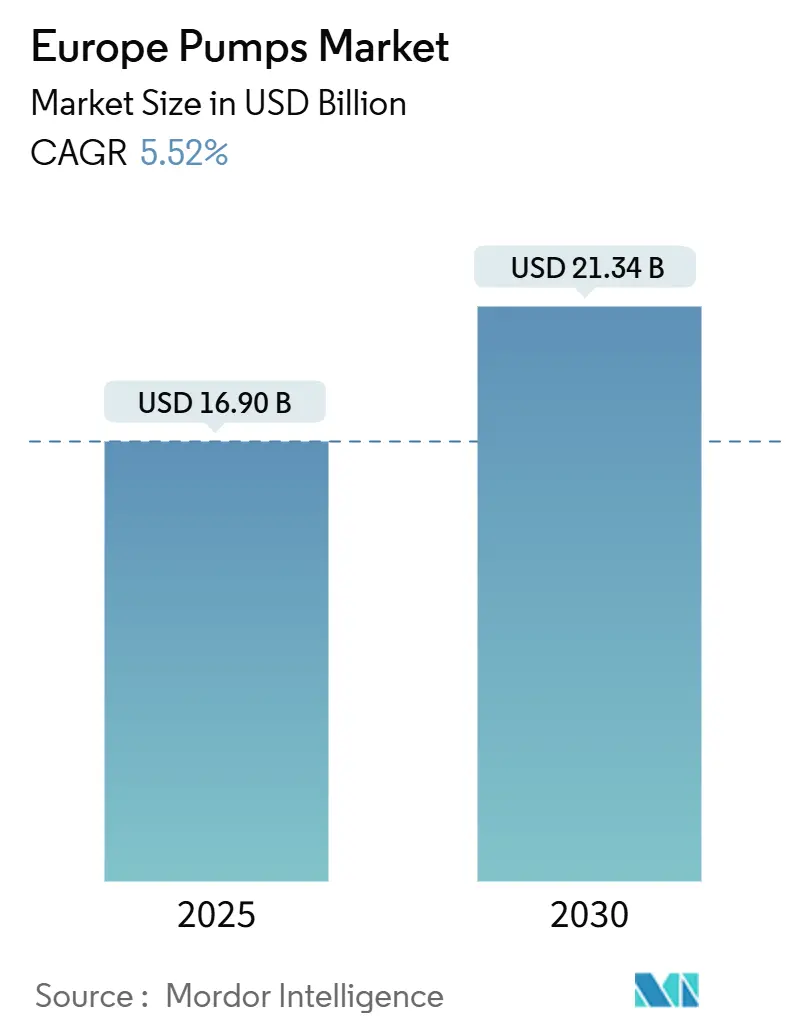

| Market Size (2025) | USD 16.90 Billion |

| Market Size (2030) | USD 21.34 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pumps Market Analysis by Mordor Intelligence

The Europe Pumps Market size is estimated at USD 16.90 billion in 2025, and is expected to reach USD 21.34 billion by 2030, at a CAGR of 5.52% during the forecast period (2025-2030).

Energy-efficiency mandates, an unprecedented wave of water-infrastructure renewal, and decarbonization programs are stretching performance specifications beyond the pace of normal replacement. Germany, holding 24.6% of 2024 revenue, is on track for an 8.2% growth curve as Energiewende upgrades sweep power, district heating, and chemical installations.[1]Eurostat, “Manufacturing Workforce Age Structure,” ec.europa.eu The United Kingdom’s GBP 104 billion AMP8 plan (USD 132.1 billion) earmarks USD 111.8 billion for leakage reduction and storm-overflow mitigation, setting up multi-year tenders for wastewater and potable-water pumps. Solar-driven and other renewable propulsion systems now show the fastest expansion, while predictive analytics is slashing unplanned downtime across asset-intensive sectors. Consolidation among leading vendors continues, yet niche specialists still thrive in sealless, progressive-cavity, and single-use segments.

Key Report Takeaways

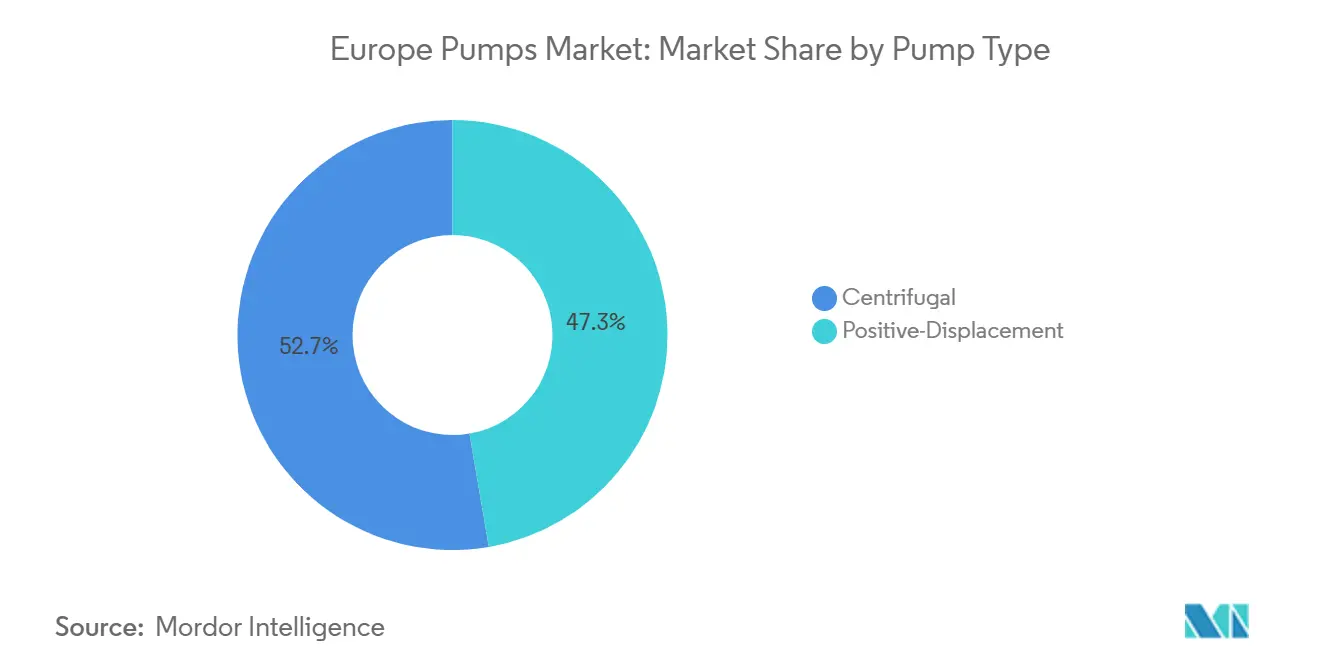

- By pump type, centrifugal models captured 52.7% of the European pumps market share in 2024 and are set for a 6.2% CAGR through 2030.

- By drive technology, solar and other renewable drives represent the fastest-growing segment, advancing at an 8.4% CAGR to 2030, while electric motors held a 72.5% revenue share in 2024.

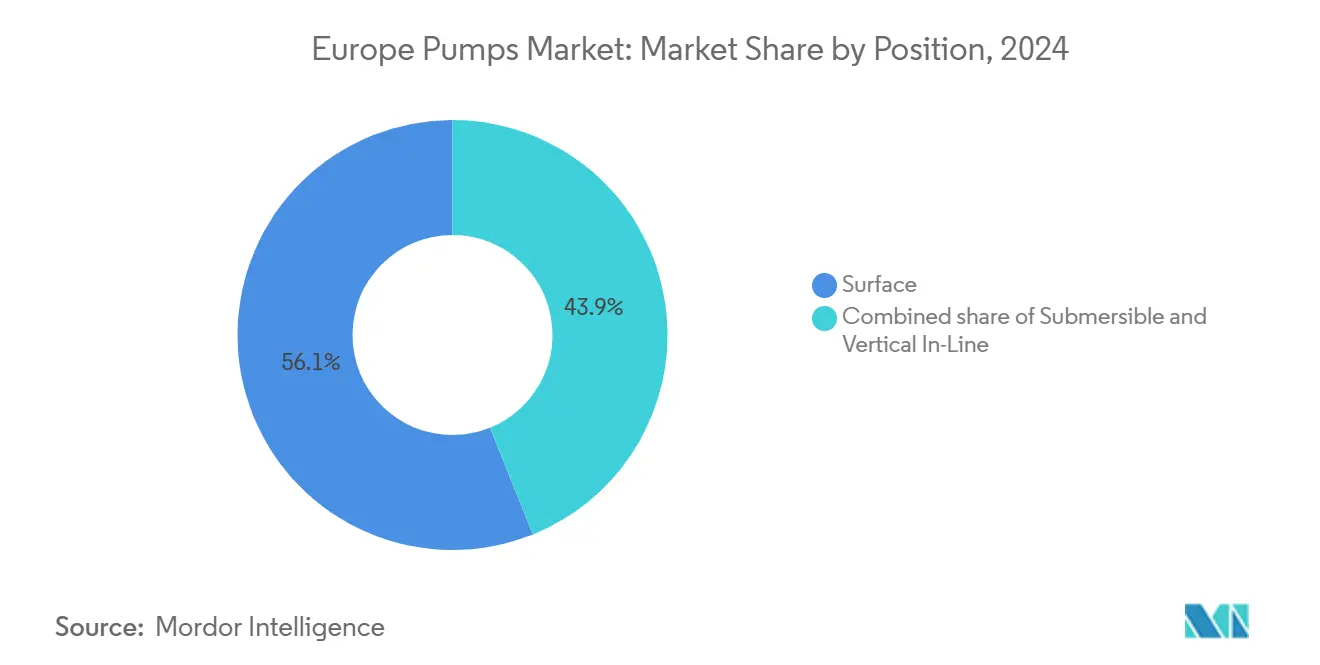

- By position, surface configurations secured 56.1% of 2024 revenue; submersible models record the quickest growth at 6.5% through 2030.

- By application, water and wastewater plants supplied 34.5% of 2024 sales and are forecast to post a 6.1% CAGR, the swiftest among end uses.

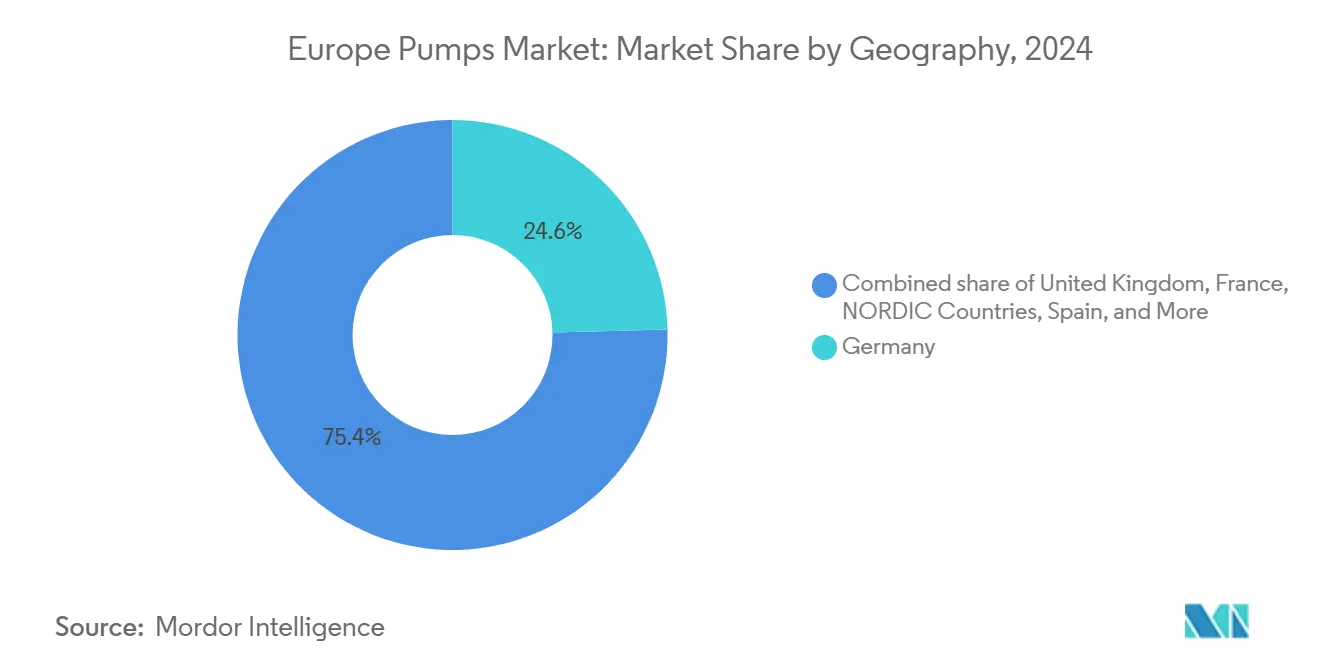

- By geography, Germany led the European pumps market with a 24.6% slice in 2024 and is expected to grow at 8.2% to 2030.

Europe Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Water & Waste-Water CAPEX | +1.2% | UK, Germany, France, Spain (Thames Valley, Barcelona metro) | Medium term (2-4 years) |

| Hydrogen & CCUS Project Pipeline | +0.8% | Northwest Europe, North Sea basin | Long term (≥ 4 years) |

| EU Fit-for-55 Energy-Efficiency Mandates | +0.9% | Pan-European, led by Germany and Nordics | Medium term (2-4 years) |

| Digitisation of Process Industries | +0.6% | Germany, France, Netherlands chemical and pharma hubs | Short term (≤ 2 years) |

| Revival of Brown-Field Refinery Upgrades | +0.4% | Spain, Netherlands, France | Medium term (2-4 years) |

| Demand for Micro-Utility Heat Pumps | +0.5% | Sweden, Denmark, Norway; pilot sites in Germany and Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Water & Waste-Water CAPEX

European utilities must invest EUR 255 billion in renewals by 2030, driving sustained orders for leak-reduction, sludge-handling, and desalination pumps. The UK’s AMP8 budget alone allocates USD 111.8 billion to capital works, pushing Thames Water to specify thousands of variable-speed units to meet new performance targets. Spain’s 765 desalination plants scaled Barcelona output to 240,000 m³ per day in 2024, creating steady demand for 60-80 bar reverse-osmosis feed pumps. France’s Grand Paris Express tunnels need dewatering systems rated at 200,000 m³ per day, favoring abrasion-resistant submersibles. Rural sewage expansion financed by the EUR 476 billion Recovery & Resilience Facility is opening green-field pump installations in Poland and Romania.[2]European Commission, “Recovery and Resilience Facility Allocations,” ec.europa.eu

Hydrogen & CCUS Project Pipeline

Northwest Europe plans 30-40 GW of electrolyser capacity, each site requiring high-pressure circulation pumps for alkaline and PEM stacks running up to 80 bar.[3]Hydrogen Europe, “European Hydrogen Valleys Roadmap,” hydrogeneurope.eu The Porthos CO₂ network in Rotterdam will inject 2.5 million t annually beneath the North Sea and calls for 110 bar multistage centrifugal boosters. The EU Innovation Fund granted EUR 1.8 billion to decarbonization projects in 2024, including amine scrubbing at Brevik cement works that needs 95 °C solvent-circulation pumps. ITT opened a German test center in 2024 to validate seals for CO₂ service between –50 °C and 120 °C, accelerating material qualification. Duplex-stainless and nickel-alloy wetted parts add 20-30% to cost but double mean time between failures, a premium operators accept to maintain 90% uptime covenants.

EU Fit-for-55 Energy-Efficiency Mandates

The recast Energy Efficiency Directive requires an 11.7% cut in final energy use by 2030, propelling the replacement of fixed-speed pumps in buildings and factories. The Renovation Wave targets 35 million structures, with variable-frequency drives trimming pump power between 30% and 50% during part-load operation. Europump’s Extended Product Approach has already saved 226 million MWh and avoided 158 million t CO₂ since 2016. Germany’s EUR 13.5 billion Federal Funding for Efficient Buildings covers up to 40% of pump retrofits, cutting payback to under 2.5 years. Ecodesign 2025 widens MEI thresholds to industrial pumps above 0.75 kW, forcing factories to retool impellers and stators, which tightened supply in early 2024.

Digitisation of Process Industries

Xylem’s Concertor smart system at Heathrow cut servicing costs by 88% and energy by 53% by predicting fouling events 72 hours in advance. Alfa Laval’s Analytics subscription reduced unplanned downtime by 25% at Danish and Dutch pilot plants by spotting vibration anomalies days before failure. BASF and Covestro embed pump telemetry in ISO 55000 asset platforms, underpinning an 8% annual rise for intelligent centrifugal units. Retrofit packages cost EUR 5,000-50,000 per pump, a hurdle for SMEs that still account for 60% of European manufacturing employment. ENISA found 42% of operators delaying connectivity over ransomware fears, prompting on-premise analytics that avoid cloud dependence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Smart Retro-fits | –0.4% | Germany, France, Italy, where small and medium manufacturers dominate production bases | Short term (≤ 2 years) |

| Raw-Material and Freight Price Volatility | –0.6% | Pan-European, with the sharpest exposure in Southern EU states dependent on imported steel | Short term (≤ 2 years) |

| Fragmented National Standards and Certifications | –0.3% | UK (UKCA), Germany (TÜV), France (NF) posing hurdles for cross-border capital projects | Medium term (2-4 years) |

| Ageing Maintenance Workforce Gap | –0.5% | Germany, Italy, Spain, each with more than 30 % of technicians older than 55 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Smart Retro-fits

Retrofitting a legacy pump with sensors, edge gateways, and analytics software costs EUR 5,000-50,000, which translates into paybacks of 2-5 years, well outside the cash-approval windows of many SMEs. A Fraunhofer study in 2024 showed 38% of German chemical-plant deployments required an extra EUR 10,000-20,000 of middleware to bridge vintage programmable logic controllers with MQTT platforms, inflating budgets further. Vendors have started offering outcome-based leases that bundle hardware, software, and service, yet uptake stays muted because CFOs remain cautious after pandemic liquidity shocks. Cybersecurity anxiety compounds hesitation, as 42% of operators surveyed by ENISA feared ransomware infiltration of production networks.[4]ENISA, “ICS Cybersecurity Survey,” enisa.europa.eu The fledgling on-premise analytics model partially eases those fears, although it forfeits the scale benefits of cloud processing.

Raw-Material & Freight Price Volatility

Copper averaged USD 9,638 t in 2024, peaking at USD 11,104 t and forcing motor OEMs to levy quarterly surcharges that complicate long-term project quotes. Hot-rolled coil rebounded from EUR 550 t to EUR 630 t between January and Q3, eroding margins on fixed-price frameworks in power and desalination plants. Nickel slid to USD 16,500-17,000 t yet remains 60% above 2019 levels, prompting a shift toward duplex steels that deliver comparable corrosion resistance at a 20% lower alloy surcharge.[5]London Metal Exchange, “Non-Ferrous Metals Monthly Report,” lme.com The Baltic Dry Index fell 26% in 2024 but is still vulnerable to Red Sea and Panama Canal disruptions that add two weeks to lead times. Budget buffers of 5-7% are now customary in the European pumps market, bids to hedge against these oscillations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Retrofit Momentum Keeps Centrifugal at the Forefront

Centrifugal designs delivered 52.7% of 2024 revenue and are forecast to grow 6.2% through 2030, reflecting entrenched positions in water distribution, power-plant cooling, and chemical recirculation. Their simple casing and ease of seal change keep lifecycle cost attractive even as energy standards tighten. Germany’s coal-to-gas conversions specify variable-frequency centrifugal units that trim auxiliary power 15-25% during part-load operation. Spain’s Barcelona desalination upgrade favored 60-80 bar multistage centrifugal pumps for reverse-osmosis because of proven reliability under brackish conditions.

Positive-displacement models still hold a 47.3% share and earn premium margins in high-viscosity, sanitary, or metering niches. Repsol’s USD 1.21 billion Cartagena biofuel plant chose progressive-cavity pumps to move 500 centipoise feedstocks. Supermarket ammonia retrofits, driven by the F-Gas phase-down, lean on leak-tight diaphragm pumps to keep fugitive emissions below 500 ppm. Smart sensor retrofits on progressive-cavity pumps at BASF Ludwigshafen now predict stator wear six weeks out, avoiding unscheduled downtime.

By Drive Technology: Solar and Battery Combinations Accelerate Adoption

Electric motors powered 72.5% of installations in 2024 and will remain the backbone of the European pumps market size as Renovation Wave subsidies favor variable-speed retrofits. Average electric tariffs of EUR 0.12-0.18 kWh keep motor OPEX advantageous against internal-combustion alternatives. Deutsche Bahn’s district-heating substations replaced 1,200 fixed-speed motors with IE4 drives in 2024, cutting kWh use by 32% in the first winter season.

Solar and other renewable drives represent only 4% of horsepower today but grow at an 8.4% CAGR. Andalusian farmers are installing photovoltaic pump kits that deliver 40 m head without grid access, avoiding EUR 50,000 connection fees. Grundfos added solar reverse-osmosis skids via the Culligan purchase, creating a subscription service that bundles PV panels, pumps, and cloud monitoring. Diesel and gas engines drop to a 20% share by 2030 as Stage V after-treatment costs squeeze their total cost of ownership.

By Position: Submersibles Edge Up in Space-Constrained Sites

Surface pumps held a 56.1% share in 2024, thanks to easy inspection in chemical refineries and power stations. BASF keeps horizontals for secondary loops so technicians avoid confined-space rules during seal swaps. Surface equipment in Neste’s Rotterdam biorefinery will push hot esters at 180 °C, where external cooling jackets aid maintenance.

Submersible units, however, expand 6.5% annually as urban wastewater networks add lift stations beneath roads and parks where land is scarce. Thames Water will deploy 4,200 submersibles during AMP8, each rated 500-2,000 m³ h to handle peak rainfall. Spanish drought mitigation led to hundreds of new deep wells in Catalonia using 200 m submersible turbines. Vertical in-line pumps, growing 5.9%, satisfy compact HVAC retrofits; Stockholm Exergi’s 180 MW heat pump circulates 10,000 m³ h via vertical turbines that keep NPSH above 3 m.

By Application: Water Programs Deliver the Fastest Growth

Water and wastewater plants commanded 34.5% revenue in 2024 and expanded 6.1% through 2030, buoyed by a USD 280.5 billion EU renewal pipeline and Barcelona’s 240,000 m³ day desalination expansion. United Utilities is upgrading 12,000 existing sites with telemetry and VFD drives, underscoring steady aftermarket pull.

Chemical and petrochemical facilities hold 18% of demand and climb 5.4%. BASF Ludwigshafen’s EUR 1.2 billion digital overhaul replaces 800 legacy units with smart pumps, while Neste’s biofuel push lifts orders for corrosion-resistant gear designs. HVAC services, 16% share, grow 5.7% on the Renovation Wave as circulators convert to variable-speed class IE4. Pharmaceuticals rise 6.3%, the second-fastest pace, with Irish and Swiss biosimilar lines adopting single-use polymer pumps that eliminate clean-in-place downtime.

Geography Analysis

Germany accounted for 24.6% of 2024 turnover and is forecast to grow 8.2% through 2030, outpacing the European pumps market average. Energiewende conversions in coal plants, district-heating loops in Munich and Hamburg, and chemical process digitization at BASF and Covestro together require roughly 120,000 pump replacements. The EUR 14.85 billion Federal Funding for Efficient Buildings subsidy pays up to 40% of variable-speed retrofits, shaving payback below 30 months and accelerating replacement timelines. To counter labor shortages, KSB extended its Mechatronics Academy intake to 600 apprentices annually.

The United Kingdom held a 13.9% share in 2024 and advanced at 5.9%. The GBP 104 billion AMP8 framework obliges leakage cuts from 24% to 16% and mandates telemetry on every sewage pump by 2030. Post-Brexit UKCA rules add four to six months of testing for new designs, nudging some EU-based vendors to prioritize continental orders. Scottish Water’s highland catchments favor solar-hybrid booster stations to avoid grid extensions, driving niche demand for battery-coupled submersibles.

France captured a 12.9% share in 2024 and tracks a 4.7% growth slope. Its 56-reactor nuclear fleet orders seismic-qualified coolant pumps that cost USD 8-12 million each and require 18-24 months of lead time. Six planned EPR2 reactors will prolong this demand curve into the mid-2030s. Grand Paris Express builds six tunnel-boring sites that each need 20 submersible dewatering pumps, adding near-term volume.

Spain contributes 7% revenue and grows 4.5%. Its 765 desalination plants, 17% of global capacity, are adding energy-recovery turbines that cut power use 40%, but still require 60-80 bar primary pumps. Drought-driven boreholes in Andalusia expand submersible sales. The Nordics hold 4.9% and grow 3.6% on district-heating heat-pump rollouts. Turkey, Russia, and the rest of Europe make up 36.7% with mixed prospects: Turkey expands 3.3% on automotive exports, while sanctions shrink Russian imports, leading suppliers to shift attention toward Balkan and Baltic customers.

Competitive Landscape

The European pumps market remains moderately fragmented. Grundfos, KSB, Wilo, and Sulzer share about 37% of revenue, leaving room for regional specialists like DESMI in marine duty, Seepex in progressive-cavity designs, and Fristam in sanitary dairy lines. Honeywell bought Sundyne for USD 2.16 billion in March 2025, adding high-speed centrifugal and diaphragm lines for LNG and hydrogen duty. Georg Fischer spent USD 220 million on VAG valves in May 2025, bundling flow-control portfolios that simplify tendering for water utilities.

Veolia closed a USD 1.75 billion deal for the final 30% of Water Technologies, gaining full control over a membrane and dosing-pump portfolio with EUR 3.2 billion turnover. Atlas Copco’s January 2024 acquisition of Kracht added USD 79.2 million in hydraulic pumps and broadened compressor-division sales channels. Valuations ranged 9-15× EV/EBITDA in 2024, with water-focused targets fetching the upper band because regulatory clarity supports resilient cash flows.

Digital differentiation is now the main competitive lever. Xylem’s Concertor, deployed at Heathrow, saved 88% in service costs and 53% in energy, validating predictive maintenance in mission-critical sites. Alfa Laval’s Analytics subscription lowered downtime 25% for Danish food processors running centrifugal hygienic pumps. CP Pump Systems won a EUR 15 million cryogenic CO₂ order by delivering ASME Section VIII and DNV-GL certified units rated –50 °C, underlining how material pedigree and test validation remain vital for CCUS contracts. Incumbents with accredited labs expedite CE, TÜV, NF, and UKCA files, making entry steep for new challengers.

Europe Pumps Industry Leaders

Grundfos Holding A/S

KSB SE & Co. KGaA

Wilo SE

Sulzer Ltd.

Xylem Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dover Corporation announced its acquisition of ipp Pump Products GmbH, integrating it into the Pump Solutions Group ("PSG") business unit of Dover's Pumps & Process Solutions segment.

- June 2025: Honeywell acquired Sundyne for USD 2.16 billion, adding high-speed centrifugal and diaphragm pumps to its Process Solutions division.

- May 2025: Veolia signed a deal to acquire the remaining 30% minority stake in its subsidiary, Water Technologies and Solutions (WTS), from the Caisse de dépôt et placement du Québec (CDPQ) for $1.75 billion.

- September 2024: Grundfos, a global frontrunner in advanced pump solutions and water technologies, has acquired the commercial and industrial (C&I) division of Culligan, marking its expansion in Italy, France, and the UK.

Europe Pumps Market Report Scope

Pumps, mechanical devices, convert energy to elevate, transport, or compress fluids, be it liquids or gases. By transforming mechanical energy into hydraulic or pneumatic energy, pumps generate a pressure difference, propelling fluids from lower to higher pressure zones.

The European pumps market is segmented by pump type, drive technology, position, application, and geography. By pump type, the market is segmented into centrifugal and positive-displacement. By drive technology, the market is segmented into electric motor, diesel/gas engine, solar/renewable, and magnetically-driven/sealless. By position, the market is segmented into surface, submersible, and vertical in-line. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market sizes and forecasts for the European pumps market across major countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Centrifugal |

| Positive-Displacement |

| Electric Motor |

| Diesel/Gas Engine |

| Solar/Renewable |

| Magnetically-Driven/Sealless |

| Surface |

| Submersible |

| Vertical In-Line |

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

| United Kingdom |

| Germany |

| France |

| Spain |

| NORDIC Countries |

| Russia |

| Turkey |

| Rest of Europe |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By Drive Technology | Electric Motor |

| Diesel/Gas Engine | |

| Solar/Renewable | |

| Magnetically-Driven/Sealless | |

| By Position | Surface |

| Submersible | |

| Vertical In-Line | |

| By Application | Water and Wastewater |

| Chemical and Petrochemical | |

| HVAC and Building Services | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Food and Beverage | |

| Mining and Metals | |

| Power Generation (Thermal, Nuclear, Renewables) | |

| Pharmaceuticals and Biotech | |

| Others | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Turkey | |

| Rest of Europe |

Key Questions Answered in the Report

What revenue will the Europe pumps market generate by 2030?

Sales are projected to reach USD 21.34 billion, reflecting a 5.52% CAGR for 2025-2030.

Which pump type holds the highest Europe pumps market share?

Centrifugal pumps led with 52.7% in 2024 and will keep first position through 2030.

Why are solar-powered pumps gaining ground?

PV panel prices below EUR 0.20 W and battery costs of EUR 100 kWh have made off-grid pumping economical for farms and islands.

What is driving Germany’s above-average growth rate?

Energiewende conversions, district-heating upgrades, and chemical-plant digitization together trigger about 120,000 pump replacements.

How is digitalization changing service models?

Predictive systems like Xylem Concertor cut unplanned downtime up to 53% and let OEMs sell subscription analytics.

Which recent merger reshaped competition?

Honeywell’s USD 2.16 billion purchase of Sundyne in 2025 added high-speed hydrogen and LNG units to its portfolio.

Page last updated on: