Europe Plus Size Clothing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 22.64 Billion |

| Market Size (2026) | USD 23.77 Billion |

| Market Size (2031) | USD 31.63 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Plus Size Clothing Market Analysis by Mordor Intelligence

The Europe plus size clothing market size is expected to grow from USD 22.64 billion in 2025 to USD 23.77 billion in 2026 and is forecast to reach USD 31.63 billion by 2031 at 5.88% CAGR over 2026-2031. The Europe plus size clothing market benefits from a large adult population that falls outside standard apparel grading, keeping demand tied to structural fit needs rather than short-term fashion cycles. Digital fashion platforms have improved the discoverability of larger sizes through filters, fit tools, and broader assortment depth, reducing the historical visibility gap that once limited category growth. At the same time, premium demand is expanding as shoppers place greater value on fit quality, fabric performance, and design relevance than the category traditionally received. Compliance costs associated with sustainability regulations and the rise of fit-sensitive return behavior continue to pressure margins; however, these factors also favor retailers that can manage technology, sourcing, and customer retention more effectively.

Key Report Takeaways

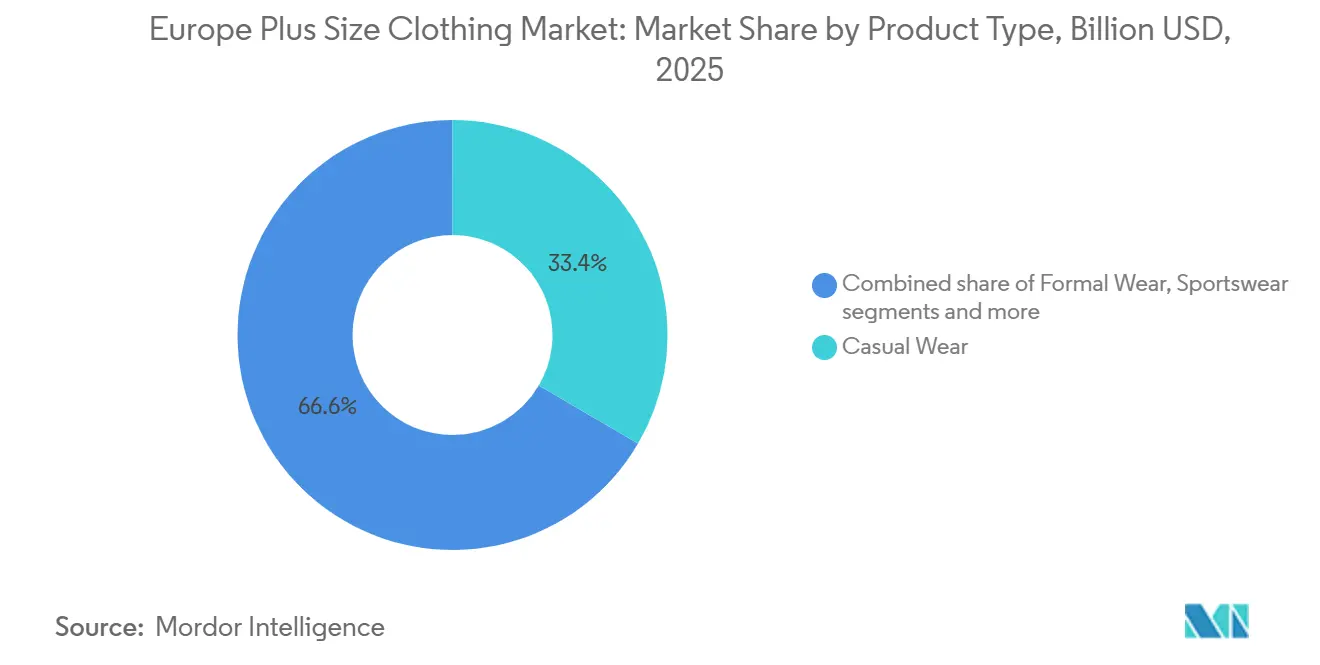

- By product type, casual wear held 33.42% share in 2025, while sportswear is projected to grow at 6.01% CAGR through 2031.

- By end user, men held 72.16% of the Europe plus size clothing market share in 2025, while women are projected to expand at 6.58% CAGR through 2031.

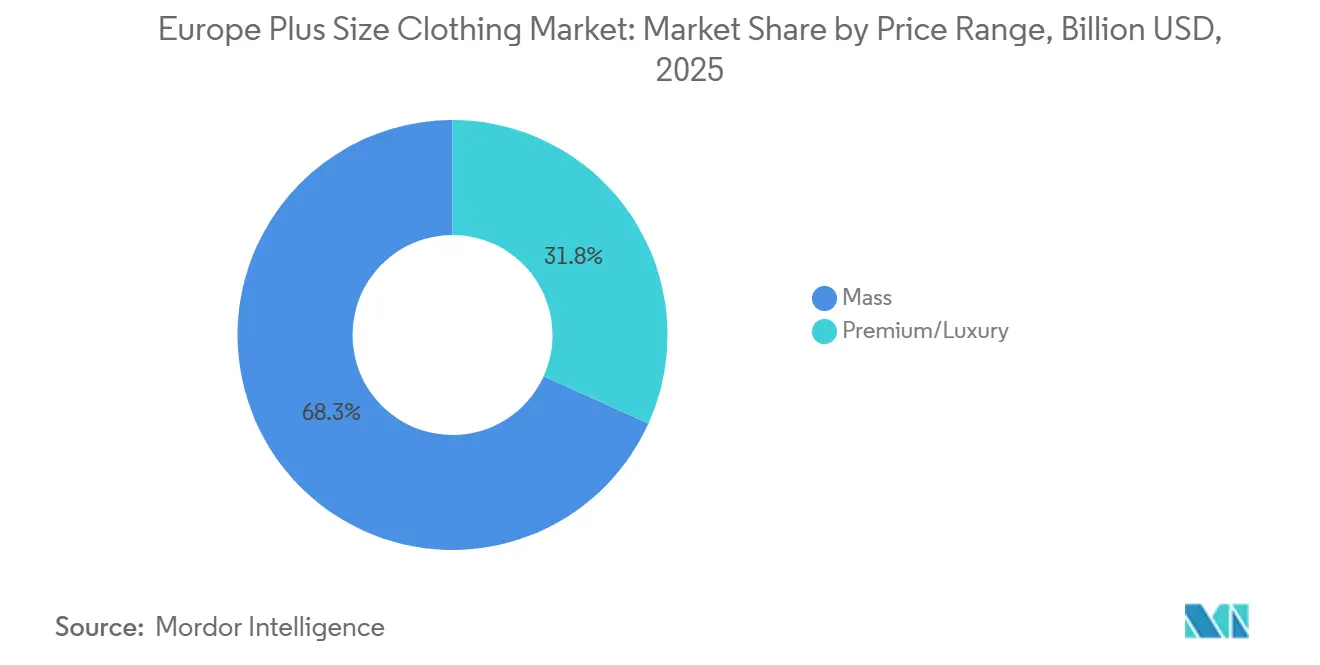

- By price range, mass products captured 68.25% share in 2025, yet premium and luxury offerings are growing at 6.11% CAGR as consumers pay for superior fabrics and precise grading.

- By distribution channel, online retail stores accounted for 84.51% of the Europe plus size clothing market size in 2025, while offline retail stores are projected to expand at 7.34% CAGR through 2031.

- By geography, the United Kingdom held 43.28% share in 2025, while Germany is projected to grow at 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Plus Size Clothing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing body positivity and demand for size inclusivity | +1.0% | United Kingdom and Germany strongest adoption | Medium term (2-4 years) |

| Rising prevalence of overweight and obesity | +1.5% | Central and Eastern Europe accelerating | Long term (≥ 4 years) |

| Influence of social media and plus-size fashion influencers | +1.0% | United Kingdom, Germany, and France core markets | Short term (≤ 2 years) |

| Increasing demand for personalized fit and extended size options | +0.8% | United Kingdom and Germany core, spillover to Benelux | Medium term (2-4 years) |

| Demand for premium denim and bottom wear | +0.5% | United Kingdom, Germany, and France | Medium term (2-4 years) |

| Adoption of inclusive intimate apparel | +0.4% | United Kingdom core, expanding to France and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing body positivity and demand for size inclusivity

Body positivity has become a practical retail factor, as demand for inclusive sizing remains steady even when fashion imagery moves in the opposite direction. The Europe plus size clothing market, therefore, no longer depends on editorial validation to support consumer demand. The commercial impact is clear: brands that limit their size architecture risk losing repeat shoppers to retailers with broader and more visible assortments. This shift has made size inclusion part of customer retention strategy, rather than only a branding choice. The category also benefits as consumers shift spending across borders to find better size availability, strengthening digital specialists and large omnichannel operators. As a result, conversion and loyalty behavior are shaping merchandising decisions in the Europe plus size clothing market more than seasonal runway positioning.

Rising prevalence of overweight and obesity

The rising prevalence of overweight and obesity is a major driver of the Europe plus size clothing market, as it continues to expand the consumer base requiring size-inclusive apparel. According to the World Health Organization (WHO) Regional Office for Europe, almost 60% of adults in the WHO European Region were living with overweight or obesity in 2024, highlighting the growing demand for clothing that offers improved fit, comfort, and style[1]Source: World Health Organization, “The challenge of obesity”, who.int. This demographic shift has encouraged apparel manufacturers and retailers to broaden their extended-size collections across casual wear, formal wear, sportswear, and intimate apparel. Consumers are increasingly seeking fashionable garments rather than limited functional options, prompting brands to invest in inclusive sizing and better pattern grading. The growing emphasis on body positivity and greater representation of diverse body types in fashion campaigns has further strengthened market demand.

Influence of social media and plus-size fashion influencers

The growing influence of social media and plus-size fashion influencers is a significant driver of the Europe plus size clothing market, as digital platforms increasingly shape consumer purchasing decisions and fashion trends. According to the Eurostat March 2024 survey, 59% of individuals in the European Union used social networking sites, highlighting the extensive reach of digital platforms that enable fashion brands and influencers to promote size-inclusive clothing and engage consumers across Europe[2]Source: Eurostat, “59% of EU individuals using social networks in 2023”, ec.europa.eu. Fashion influencers and content creators are helping normalize body diversity by showcasing stylish plus-size apparel, boosting consumer confidence and brand visibility. Social media platforms also allow brands to launch new collections, collaborate with influencers, and interact directly with target audiences through personalized content and campaigns.

Increasing demand for personalized fit and extended size options

Fit inconsistency has become a direct trigger for technology spending because it raises return risk and weakens platform economics. Zalando stated that its Size & Fit AI used real body measurements from more than 1 million customers and reduced size-related returns by more than 8% in 2025[3]Source: Zalando, “Zalando delivers strong 2025 results, expects further acceleration in 2026 through scaling AI innovations and announces a share buy-back of up to 300 million”, corporate.zalando.com. That result matters for the Europe plus size clothing market because sizing friction is more costly when shoppers have fewer reliable in-store alternatives. It also shows that fit technology is moving from a helpful feature into a core operating requirement for large digital fashion platforms. Retailers that cannot improve accuracy are likely to face higher reverse logistics costs and weaker customer retention. The Europe plus size clothing market is therefore seeing technology serve both growth and margin protection at the same time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs due to complex sizing and pattern grading | -0.8% | United Kingdom, Germany | Medium term (2-4 years) |

| Higher product return rates in online plus-size apparel purchases | -0.6% | United Kingdom and Germany core, expanding with e-commerce penetration | Short term (≤ 2 years) |

| Supply chain challenges in managing broader size inventories | -0.5% | Germany, Italy, France | Medium term (2-4 years) |

| Premium pricing of fashionable plus-size garments compared to standard sizes | -0.4% | Southern Europe, limited spillover elsewhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher production costs due to complex sizing and pattern grading

Higher production costs associated with complex sizing and pattern grading are a significant restraint on the Europe plus size clothing market. Unlike standard apparel, plus-size garments require specialized pattern development, multiple fit trials, and precise grading to ensure comfort, durability, and consistent fit across a wider range of body shapes. Manufacturers must also use additional fabric, reinforced stitching, and modified garment construction techniques, increasing material and production costs. These added complexities often result in longer product development cycles and higher manufacturing expenses compared to standard-size clothing. Maintaining extensive size inventories further increases warehousing and inventory management costs for retailers. Consequently, higher production costs can reduce profit margins and slow the expansion of affordable, size-inclusive apparel across the European market.

Supply chain challenges in managing broader size inventories

Supply chain challenges associated with managing broader size inventories present a significant restraint on the Europe plus size clothing market. Offering extended-size collections requires manufacturers and retailers to maintain a larger number of stock-keeping units (SKUs) across multiple sizes, styles, and colors, increasing inventory complexity. Accurately forecasting demand for each size is challenging, often resulting in overstocking of slower-moving sizes or shortages of high-demand products. These inventory imbalances lead to higher warehousing, logistics, and inventory holding costs while reducing operational efficiency. Retailers must also coordinate production and distribution across multiple European markets with varying consumer preferences and size requirements. The complexity of managing wider assortments can increase lead times and limit the flexibility to respond quickly to changing fashion trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Casual Wear Anchors the Market, Sportswear Leads Upside

Casual wear accounted for 33.42% of the Europe plus size clothing market in 2025, making it the largest product type segment. Its leadership is driven by strong consumer preference for comfortable, versatile, and everyday apparel suitable for both work and leisure. The growing adoption of hybrid working models and changing fashion preferences have further increased demand for casual plus-size clothing across Europe. Retailers are continuously expanding their casual wear portfolios by introducing trend-focused collections with improved fit, inclusive sizing, and seasonal styles. As a result, casual wear continues to dominate the market owing to its high purchase frequency, extensive product variety, and widespread consumer acceptance.

Sportswear is projected to register the fastest CAGR of 6.01% during 2026–2031. The segment is benefiting from the rising popularity of athleisure, increasing health awareness, and growing participation in fitness and recreational activities among plus-size consumers. Manufacturers are investing in performance fabrics, moisture-wicking materials, and ergonomic designs to improve comfort and functionality for extended-size apparel. The expansion of inclusive activewear collections by both established sportswear brands and specialized plus-size fashion companies is further accelerating market growth.

By End User: Men Dominate by Value, Women Propel Premium Expansion

Men accounted for 72.16% of the Europe plus size clothing market in 2025, making them the largest end-user segment. The segment's dominance is supported by the widespread availability of plus-size apparel across casual wear, formal wear, sportswear, and everyday essentials. Growing awareness among retailers about the demand for extended-size menswear has led to broader product assortments and improved accessibility through both physical stores and e-commerce platforms. Consumers are increasingly seeking garments that combine comfort, functionality, and contemporary styling, encouraging brands to expand their offerings.

Women are projected to register the fastest CAGR of 6.58% during 2026–2031. The segment is being driven by the growing body positivity movement and increasing consumer demand for fashionable, size-inclusive clothing across all age groups. Fashion brands are rapidly expanding their women's plus-size collections by introducing trend-led designs, premium fabrics, and seasonal product launches. The rapid growth of online retail has also improved access to a wider variety of styles, encouraging higher purchasing frequency among female consumers.

By Price Range: Mass Segment Holds Volume, Premium Rewrites the Value Equation

The mass price range accounted for 68.25% of the Europe plus size clothing market in 2025, making it the dominant pricing segment. Its leadership is primarily attributed to the strong consumer preference for affordable apparel that offers a balance between quality, style, and value. Major fashion retailers have significantly expanded their mass-market plus-size collections, ensuring broad availability across physical stores and online platforms. Frequent product launches, promotional campaigns, and competitive pricing have further strengthened demand within this category. In addition, consumers continue to prioritize everyday clothing at accessible price points, particularly amid inflationary pressures and changing household spending patterns.

The premium and luxury segment is projected to register the fastest CAGR of 6.11% during 2026–2031. Growth in this segment is being driven by increasing consumer willingness to invest in premium-quality plus-size apparel that offers superior fabrics, craftsmanship, and fit. Luxury and premium fashion brands are expanding their inclusive sizing strategies to cater to a broader customer base seeking stylish and high-end clothing options. Improvements in garment construction, precise grading techniques, and premium materials are enhancing product appeal and encouraging repeat purchases.

By Distribution Channel: Digital Commands Share, Offline Channels Recover Fastest

Online retail stores accounted for 84.51% of the Europe plus size clothing market in 2025, making them the dominant distribution channel. Their leading position is driven by the extensive product assortment, convenient shopping experience, and easy access to a wide range of sizes that are often unavailable in physical stores. Consumers increasingly prefer online platforms because they allow them to compare products, prices, and brands while offering discreet and convenient purchasing. The availability of detailed size guides, customer reviews, flexible return policies, and home delivery services has further strengthened consumer confidence in online shopping.

Offline retail stores are projected to register the fastest CAGR of 7.34% during 2026–2031. Growth in this segment is being supported by retailers expanding dedicated plus-size sections and improving the in-store shopping experience. Consumers continue to value the opportunity to try on garments, assess fabric quality, and receive personalized assistance before making a purchase. Apparel brands are also redesigning store layouts and introducing broader size ranges to better serve the growing plus-size consumer base. Omnichannel retail strategies, including click-and-collect services and seamless integration between online and physical stores, are further driving store traffic.

Geography Analysis

The United Kingdom accounted for 43.28% of the Europe plus size clothing market in 2025, making it the largest regional market. The country's leadership is supported by a highly developed fashion retail sector, strong consumer spending on apparel, and widespread acceptance of size-inclusive fashion. The presence of leading retailers and specialized plus-size brands has resulted in an extensive product portfolio across casual wear, formal wear, sportswear, and occasion wear. In addition, the United Kingdom has one of Europe's most mature e-commerce markets, enabling consumers to access a broad range of plus-size clothing through digital platforms.

Germany is projected to register the fastest CAGR of 6.57% during 2026–2031. Market growth is being driven by increasing demand for premium-quality plus-size apparel, rising consumer awareness of inclusive fashion, and continuous expansion of omnichannel retail networks. German apparel brands and international fashion companies are investing in broader size ranges, advanced fit technologies, and sustainable product offerings to meet evolving consumer expectations. The country's strong purchasing power and well-established textile and apparel industry also support the introduction of innovative plus-size collections.

Other countries like Spain, Italy, France, and the Netherlands also represent important contributors to the Europe plus size clothing market. France benefits from its influential fashion industry, with both luxury and mainstream brands increasingly incorporating inclusive sizing into their collections to meet changing consumer preferences. Italy is witnessing steady growth as domestic apparel manufacturers and premium fashion labels expand their plus-size offerings while emphasizing style, quality, and tailored fits. Spain continues to experience healthy demand through the expansion of international fashion retailers, growing online apparel sales, and increasing acceptance of body-positive fashion trends.

Competitive Landscape

The Europe plus size clothing market remains fragmented, with competition spread across specialists, large digital fashion platforms, and mass retailers expanding their extended-size offers. This structure means no single company defines the category across all countries, price points, and end users. The first competitive tier includes dedicated specialists such as Ulla Popken, Yours Clothing, Evans, JD Williams, Simply Be, and Marina Rinaldi. The second tier includes digital generalists such as Zalando, ASOS, H&M, Bonprix, and boohoo that use traffic scale and search visibility to compete. The third tier includes mass retailers such as Marks & Spencer, C&A, KIABI, El Corte Inglés, and Primark that add extended sizing to protect customer reach.

Competition in the Europe plus size clothing market is increasingly centered on product innovation, inclusive sizing, and omnichannel retail strategies. Companies are investing in advanced pattern grading, body-shape analysis, and fit technologies to improve garment comfort while reducing online return rates. Many brands are also expanding their collections beyond basic essentials to include premium fashion, activewear, occasion wear, and seasonal apparel, enabling them to appeal to a broader consumer base.

Digital transformation continues to reshape the competitive landscape as companies enhance their e-commerce capabilities and integrate online and offline shopping experiences. Retailers are leveraging artificial intelligence for personalized product recommendations, virtual fitting tools, and data-driven inventory management to improve customer engagement and conversion rates. Collaborations with plus-size influencers, fashion designers, and social media creators have also become an important strategy for increasing brand visibility and connecting with younger consumers.

Europe Plus Size Clothing Industry Leaders

H & M Hennes & Mauritz AB

Zalando SE

ASOS Plc

NEXT plc

Yours Clothing Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Ulla Popken introduced the Beatrice Egli × Ulla Popken fashion collaboration to promote exclusive plus-size collections and advance inclusive fashion across Europe. The collaboration highlighted the brand’s focus on offering stylish apparel options for plus-size consumers.

- July 2025: Happy Size, a leading German plus-size retailer owned by Popken Fashion Group, partnered with Mirakl, a leading provider of e-commerce software solutions, to launch a specialized marketplace platform for plus-size customers across the DACH region and Europe. Through this partnership, Happy Size expanded its digital retail capabilities and strengthened its product offering for the plus-size customer segment.

- May 2025: Yours Clothing launched a premium underwire swimwear range and became the only European retailer to offer underwired swimsuits with bra cup sizing up to 44G for under GBP 50. The range used a composition of more than 80% elastane to improve stretch and color saturation and addressed a structurally unmet need in inclusive swimwear at accessible price points.

Europe Plus Size Clothing Market Report Scope

The Europe plus-size clothing market caters to individuals whose body measurements exceed standard sizing. The market is segmented by product type, end-user, price range, distribution channel, and geography. By product type, the market is segmented into formal wear, casual wear, sportswear, nightwear and loungewear, intimate and shapewear, and maternity wear. By end user, the market is segmented into women, men, and unisex. By price range, the market is segmented into mass-market and premium or luxury offerings. By distribution channel, the market is segmented into online retail platforms and offline retail stores. By geography, the market is segmented into Germany, United Kingdom, Italy, France, Spain, Netherlands, Poland, Belgium, Sweden and Rest of Europe. The report offers market size and forecasts in value (USD billion) for the above segments.

| Formal Wear |

| Casual Wear |

| Sportswear |

| Nightwear and Loungewear |

| Intimate and Shapewear |

| Maternity Wear |

| Men |

| Women |

| Unisex |

| Mass |

| Premium/Luxury |

| Online Retail Stores |

| Offline Retail Stores |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Formal Wear |

| Casual Wear | |

| Sportswear | |

| Nightwear and Loungewear | |

| Intimate and Shapewear | |

| Maternity Wear | |

| By End User | Men |

| Women | |

| Unisex | |

| By Price Range | Mass |

| Premium/Luxury | |

| By Distribution Channel | Online Retail Stores |

| Offline Retail Stores | |

| By Country | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the expected value of Europe plus size clothing by 2031?

The Europe plus size clothing market is forecast to reach USD 31.63 billion by 2031, rising from USD 23.77 billion in 2026 at a 5.88% CAGR.

Which country currently leads regional demand?

The United Kingdom led with 43.28% share in 2025 because it has a deeper specialist retail base, broader online assortment, and stronger consumer familiarity with dedicated plus-size platforms.

Which country is growing the fastest through 2031?

Germany is projected to expand at 6.57% CAGR through 2031, supported by large digital fashion infrastructure, specialist brands, and scalable marketplace models.

Which product category is growing the fastest in extended-size apparel?

Sportswear is the fastest-growing product type at a 6.01% CAGR through 2031.

Why does online retail dominate this space?

Online retail held 84.5% share in 2025 because it offers deeper assortment, broader size ranges, and better discovery tools than most physical stores historically provided.

Page last updated on: