Europe Mobile Broadband Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 161.81 Billion |

| Market Size (2030) | USD 176.21 Billion |

| Growth Rate (2025 - 2030) | 1.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mobile Broadband Market Analysis by Mordor Intelligence

The European Mobile Broadband Market size is estimated at USD 161.81 billion in 2025, and is expected to reach USD 176.21 billion by 2030, at a CAGR of 1.72% during the forecast period (2025-2030). Maturity in Western Europe means that revenue growth now hinges on service differentiation rather than net-new subscriber additions, while the transition from 4G to fully-fledged 5G standalone (SA) networks remains the single largest lever for value creation. Household 5G coverage already reaches 94.3% across the EU, yet only 40% of that footprint is SA-enabled, exposing a short-term upgrade cycle that favors operators willing to invest in core-network virtualization. [1]GSMA, “5G Implementation Guidelines,” GSMA.COM Central and Eastern European (CEE) countries benefit from EU Digital Decade funding, whereas high spectrum costs in Germany, Italy, and the UK constrain capital budgets. Operators recognize energy efficiency as a new competitive axis, because electricity accounts for up to 20% of network operating expenses, and green-power commitments influence both cost structure and brand perception.

Key Report Takeaways

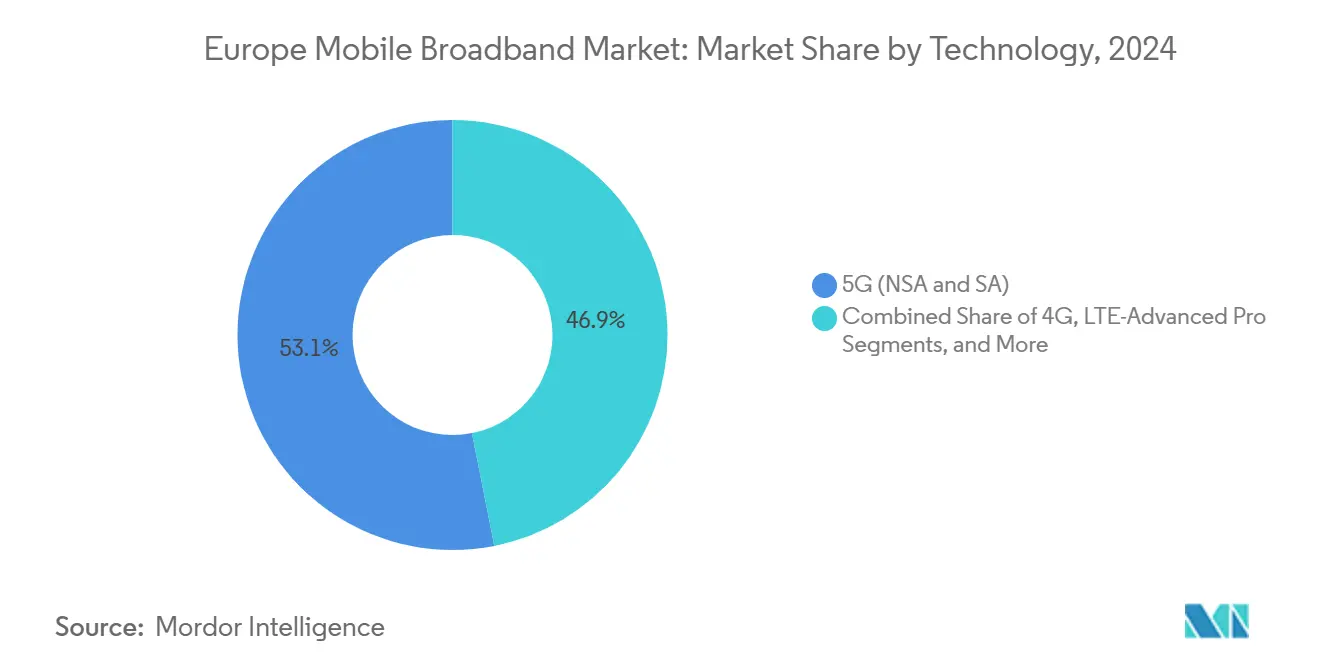

- By technology, 5G commanded 53.11% of the European mobile broadband market share in 2024, and is forecasted to expand at a 2.68% CAGR through 2030.

- By service type, mobile data plans commanded 70.31% of the European mobile broadband market share in 2024, and are forecasted to expand at a 2.19% CAGR through 2030.

- By end-user, consumers accounted for 74.24% of the European mobile broadband market share in 2024; however, the business/enterprise segment is projected to advance at a 3.13% CAGR through 2030.

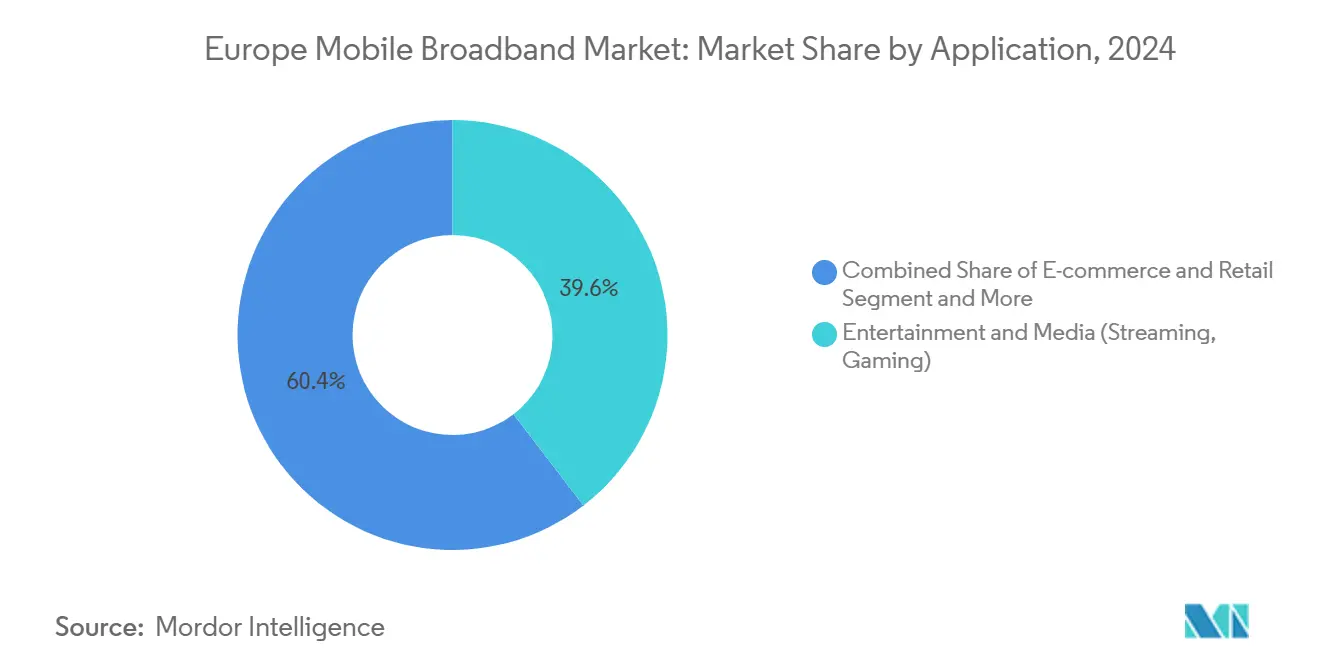

- By application, entertainment and media dominated the market with a 39.57% market share in 2024, while e-commerce and retail applications are poised to grow at the highest CAGR of 4.52% to 2030.

- By spectrum band, the 1-6 GHz mid-band captured 56.97% of the European mobile broadband market size in 2024 and is projected to grow at a 3.52% CAGR to 2030.

- By country, Germany led with a 32.34% revenue share in 2024, while the Rest of Europe is forecast to record the fastest growth, at a 5.92% CAGR, through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Europe includes both locally based firms and those operating across multiple regions. The market landscape in the global mobile broadband industry research shows how these players are arranged internationally.

Europe Mobile Broadband Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G SA Roll-outs and Mid-band Spectrum Awards | +0.8% | Germany, France, UK, wider EU | Medium term (2-4 years) |

| Exponential Mobile-data Growth from Streaming and Gaming | +0.6% | Urban centers EU-wide | Short term (≤ 2 years) |

| 5G FWA Uptake in Austria, Germany and UK | +0.3% | Austria, Germany, UK | Medium term (2-4 years) |

| EU Digital Decade and CEF-Digital Corridor Funding Surge | +0.4% | Strongest in CEE | Long term (≥ 4 years) |

| Utility and Public-safety Private LTE/5G on 450 MHz | +0.2% | Critical-infrastructure corridors | Long term (≥ 4 years) |

| 3G/2G Sunsets Releasing Low-band Capacity for 5G | +0.3% | Accelerated in Nordics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid 5G SA roll-outs and mid-band spectrum awards

By 2024, 40% of European 5G coverage areas had migrated to standalone architecture, providing operators with access to network-slicing functions that generated EUR 2.3 billion in new enterprise revenue for Deutsche Telekom alone. [2]Deutsche Telekom, “Annual Report 2024,” TELEKOM.COMAwarding operators 80-100 MHz of contiguous 3.4-3.8 GHz bandwidth enables sustained 1 Gbps speeds in dense locations, meeting the premium-tier expectations of industrial IoT and cloud gaming clients. ETSI Release 16 compliance has effectively turned network slicing from a technical upgrade into a regulatory necessity, compressing deployment timelines and reinforcing first-mover advantages. [3]ETSI, “5G Technologies and Standards,” ETSI.ORGCapital intensity remains high because a 5G SA base station costs roughly EUR 150,000, compared to EUR 80,000 for a non-standalone upgrade; therefore, operators concentrate their spending in high-value corridors. Early adopters are already bundling SA performance guarantees, latency, and uptime SLAs into managed-service contracts, letting connectivity evolve into a quality-driven product rather than a volume commodity.

Exponential mobile-data growth from streaming and gaming

Monthly mobile traffic reached 15.2 exabytes in 2024, a 17% increase year-over-year, with video and cloud gaming collectively occupying 65% of peak-hour capacity. Gaming alone fills 23% of those peaks, driven by platforms such as Xbox Cloud Gaming that require sub-20 millisecond latency. Compression gains from AV1 video coding reduce bandwidth per stream by 30%, yet higher resolutions neutralize much of that efficiency, creating a sustained demand spiral. Operators answer with small-cell densification in stadiums, transport hubs, and shopping centers, where a 50-meter cell radius guarantees throughput yet adds incremental opex. Premium unlimited data tiers aimed at gamers command an average 14% price uplift, showing how usage intensity can align with revenue despite flat-rate competition.

5G FWA uptake in Austria, Germany, and the UK

Fixed-wireless access (FWA) is expected to add 1.2 million subscribers across the three countries by 2024, providing incumbent mobile operators with an alternative when fiber rollouts remain cost-prohibitive. Deutsche Telekom’s Magenta Zuhause service delivers 100 Mbps in rural communities at one-third the cost of fiber-to-the-home. Austrian operator A1 covers 85% of rural premises with 5G FWA and reports customer acquisition costs 60% lower than those of fiber equivalents. Operators must control at least 80 MHz of mid-band spectrum to maintain consistent broadband-class performance, making spectrum policy a key factor in FWA economics. The segment’s early success presses fixed-line incumbents to accelerate fiber builds or partner on wholesale terms.

EU Digital Decade and CEF-Digital funding surge

The EUR 865 million 2024-2027 CEF-Digital budget subsidizes cross-border 5G road corridors, with EUR 323 million earmarked for autonomous-vehicle connectivity. Poland and the Czech Republic together receive more than EUR 120 million, incentivizing multi-operator consortia that lower individual capex. Funding milestones force compliance with ETSI interface standards, which accelerates technical harmonization and reduces roaming frictions. The long-term carrot of grant disbursement thus converts what might have been fragmented national deployments into a quasi-federal infrastructure map, supporting pan-European logistics and industrial platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Spectrum Prices Limiting Operator CAPEX | -0.4% | Germany, Italy, UK | Medium term (2-4 years) |

| Fragmented Regulation and Slow 26 GHz Authorizations | -0.3% | EU-wide | Long term (≥ 4 years) |

| Rising Energy Costs and Green-network Mandates | -0.2% | Pan-European, acute in Nordics | Short term (≤ 2 years) |

| Short Supply of Affordable 5G-SA Devices in CEE | -0.2% | CEE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High spectrum prices limiting operator capex

European auctions extracted EUR 52.4 billion between 2019 and 2024; Germany alone paid EUR 6.55 billion, exceeding initial forecasts by 180%. [4]Bundesnetzagentur, “Mobile Communications Frequencies,” BUNDESNETZAGENTUR.DESuch outlays soak up 15-20% of annual operator capex, squeezing budgets earmarked for rural build-outs and small-cell densification. Vodafone Germany amortizes its EUR 1.9 billion license over 20 years, diverting EUR 95 million annually that could otherwise be used to fund 1,200 new 5G sites. Smaller challengers are disproportionately hit, nudging markets toward consolidation or network-sharing pacts that erode competitive intensity.

Fragmented regulation delays mmWave deployment

Only 12 EU members had released commercial 26 GHz licenses by 2024, resulting in patchy coverage for latency-sensitive applications. Interference-protection thresholds differ by up to 10 dB across borders, necessitating bespoke radio planning and driving per-country compliance costs to nearly EUR 2.5 million. The European Electronic Communications Code aims for harmonization by 2025; however, national politics suggest a gradual approach, potentially leading to ultra-low-latency industrial automation relying on mid-band or private-spectrum solutions in the interim.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: 5G Captures Early Majority While LTE Holds Revenue Ground

The 5G family, including NSA and SA variants, accounted for 53.11% of the European mobile broadband market share in 2024 and is on track for a 2.68% CAGR to 2030, decisively outpacing legacy systems. Operator playbooks pair 5G SA for enterprise slicing with NSA for broad consumer coverage, enabling a phased migration that preserves cash flow. LTE-Advanced Pro continues to monetize carrier aggregation and 4x4 MIMO in suburban markets, where 5G device penetration remains below 40%, ensuring asset longevity even as spectrum refarming accelerates.

Operators pursue a technology-agnostic orchestration model in which traffic dynamically rides the best-fit radio, maximizing spectral efficiency. Wi-Fi offload is increasingly integrated into transport-level policy engines, reducing RAN congestion in public venues. NB-IoT and LTE-M retain niche roles for smart metering and logistics tags, but private 5G is gradually absorbing those segments once latency or deterministic performance becomes a material concern.

By Service Type: Data Plans Dominate but Quality-of-Service Upsells Emerge

Mobile data plans generated 70.31% of 2024 revenue and are expected to grow at a 2.19% CAGR, aligning with the topline of the European mobile broadband market. The commoditization of voice drove VoLTE to an 89% penetration rate, freeing up spectrum for packet data and enabling operators to sunset their 3G assets. Unlimited tiers, combined with video-streaming partnerships, reinforce loyalty but compress the average revenue per user, prompting the introduction of new quality-of-service add-ons.

Network-slicing SLAs guarantee bandwidth or latency for gaming, livestreaming, or tele-surgery, commanding premiums up to 25% over standard plans. Regulatory guardrails from BEREC prohibit application-specific throttling, so differentiation must stem from virtualized network partitions rather than packet-inspection tricks. Mobile hotspot and tethering revenues are fading as the prevalence of multi-SIM device ownership and generous data buckets renders them redundant.

By End-User: Enterprises Fuel Premium Growth

Consumers still represented 74.24% of the European mobile broadband market size in 2024, yet enterprise lines are growing faster at a 3.13% CAGR. Manufacturing, automotive, and pharma verticals champion private 5G, valuing deterministic uptime and on-premises data sovereignty. German automotive plants, for example, run dedicated 100 MHz slices that synchronize robotic welding lines within 1 millisecond jitter budgets.

SME adoption in CEE receives subsidy boosts from the Digital Decade, but sustainability beyond grant cycles remains an open question. Consumer ARPU remains largely flat as fierce competition favors bundle discounts over headline price increases, reinforcing the strategic pivot toward enterprise-managed services, edge platforms, and vertical-specific apps.

By Application: Entertainment Dominates, E-Commerce Accelerates

Entertainment and media accounted for 39.57% of the 2024 value, confirming the primacy of video in the European mobile broadband market. Cloud gaming joins 4K streaming as bandwidth heavyweights, raising the floor for baseline network performance. Yet, e-commerce and retail applications are forecasted to have a 4.52% CAGR, the fastest among peer groups, as 5G supports real-time inventory, AR shopping, and instant payment flows.

Healthcare and education, once pandemic stop-gaps, mature into ongoing service pillars featuring tele-diagnostics and hybrid classrooms. GDPR-driven privacy expectations give operators an edge in edge-compute offerings that minimize data travel, monetizing compliance as a service element rather than a cost center.

By Spectrum Band: Mid-Band Balances Capacity and Coverage

The mid-band (1-6 GHz) segment held 56.97% of the value in 2024 and is growing at a 3.52% CAGR, the highest among spectrum classes. Its sweet-spot propagation lets operators meet both rural obligations and urban throughput demands. Sub-1 GHz remains essential for wide-area coverage, but yields limited incremental revenue due to the constrained channel size.

mmWave (> 6 GHz) promises multi-gigabit service in stadiums and downtown cores, yet dense small-cell architectures lift opex. Dynamic spectrum sharing allows low-band LTE channels to host 5G, accelerating rural upgrade economics without wholesale refarming. National regulators in the Nordics have pioneered contiguous 100 MHz blocks at 3.5 GHz, providing a template for other markets to follow.

Geography Analysis

Germany maintained a commanding 32.34% share of the European mobile broadband market in 2024, as Deutsche Telekom invested EUR 17 billion in 5G rollouts that prioritized automotive and manufacturing corridors. High spectrum fees and volatile energy prices temper future growth, nudging leading operators toward network-sharing pacts such as the Vodafone-Telefónica tower collaboration that aims to trim redundant capex.

The United Kingdom and France together accounted for just over 40% of 2024 revenue. UK operators deal with post-Brexit regulatory overhead, including EUR 15 million in annual compliance costs to maintain EU roaming parity, while simultaneously fulfilling their rural coverage commitments. France’s Orange achieved 85% population coverage by earning municipal goodwill through transparent environmental reporting on antenna sites. Both jurisdictions see enterprise slices outpacing consumer growth as corporates seek deterministic mobile connectivity.

The rest of Europe, heavily skewed towards CEE, logs the fastest 5.92% CAGR, owing to EU-funded corridor projects that sidestep the need for legacy 4G densification. Poland and the Czech Republic leverage grant-backed spectrum and cross-border road corridors to attract logistics and manufacturing tenants to private 5G campuses. Southern peripheral markets, such as Italy and Spain, grow more slowly due to macroeconomic drag, although Digital Decade subsidies still underwrite rural infill projects.

Mordor Intelligence tracks the mobile broadband market across other major regions such as Asia, North America, and Middle East.

Competitive Landscape

Vodafone, Deutsche Telekom, Orange, and Telefónica collectively control a significant share of regional revenue, resulting in a moderate-concentration structure within the European mobile broadband industry. Profit pools, however, are shifting from subscriber additions to network-quality premiums and managed-service bundles. Infrastructure-sharing deals, Vodafone and Orange in Spain, Vodafone and Telefónica in Germany, cut overlapping tower opex by up to 35% while preserving brand-level competition on retail plans.

Equipment suppliers Nokia and Ericsson are competing for Open-RAN contracts that promise multi-vendor flexibility; Nokia recently secured a pan-European private wireless framework that covers 40 airlines and 600 manufacturing sites. Cloud-native core software entrants, such as Mavenir and Parallel Wireless, chip away at incumbent vendor margins by offering pay-as-you-grow models aligned with edge compute rollouts.

Green-network mandates spur partnerships with renewable-power providers; Vodafone pledged 100% renewable sourcing by 2025, while Orange is piloting on-site hydrogen fuel cells for remote base stations. AI-enabled energy-savings algorithms reduce the annual RAN power draw by 15%, illustrating how sustainability becomes both a compliance requirement and a cost-saving lever.

Europe Mobile Broadband Industry Leaders

Vodafone Group plc

Deutsche Telekom AG

BT Group plc

Iliad SA

Telia Company AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: M Group Telecom won a GBP 11 billion, five-year contract with Vodafone-Three to build nationwide 5G SA infrastructure across the United Kingdom.

- February 2025: Vodafone announced plans to establish Europe’s first research hub dedicated to integrating low-Earth-orbit satellite and terrestrial mobile broadband services. This will enable seamless switching between satellite and 4G/5G networks using existing smartphones.

Europe Mobile Broadband Market Report Scope

| 4G |

| 5G (NSA and SA) |

| LTE-Advanced Pro |

| Wi-Fi |

| Other Technologies (NB-IoT, LoRaWAN etc.) |

| Mobile Data Plans |

| Voice-over-LTE (VoLTE) |

| Mobile Hotspot / Tethering |

| Consumers |

| Businesses / Enterprises |

| Entertainment and Media (Streaming, Gaming) |

| E-commerce and Retail |

| Social Media and Communication |

| Healthcare and Education |

| Other Applications |

| Sub-1 GHz (Coverage bands) |

| 1–6 GHz (Mid-band) |

| >6 GHz mmWave and Terahertz |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Technology | 4G |

| 5G (NSA and SA) | |

| LTE-Advanced Pro | |

| Wi-Fi | |

| Other Technologies (NB-IoT, LoRaWAN etc.) | |

| By Service Type | Mobile Data Plans |

| Voice-over-LTE (VoLTE) | |

| Mobile Hotspot / Tethering | |

| By End-User | Consumers |

| Businesses / Enterprises | |

| By Application | Entertainment and Media (Streaming, Gaming) |

| E-commerce and Retail | |

| Social Media and Communication | |

| Healthcare and Education | |

| Other Applications | |

| By Spectrum Band | Sub-1 GHz (Coverage bands) |

| 1–6 GHz (Mid-band) | |

| >6 GHz mmWave and Terahertz | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe mobile broadband market in 2025?

It is valued at USD 161.81 billion, on course to reach USD 176.21 billion by 2030.

What growth rate is expected for 5G within Europe?

5G revenue is projected to rise at 2.68% CAGR through 2030, faster than the overall market’s 1.72%.

Which country leads European mobile broadband revenues?

Germany holds the lead with 32.34% share thanks to EUR 17 billion in 5G investment by Deutsche Telekom.

Why are energy costs a concern for operators?

Power now makes up 15–20% of network opex, prompting 75% of operators to commit to renewable sourcing by 2030.

What is driving enterprise demand for private 5G?

Industry 4.0 automation needs guaranteed latency and on-premises data control, fueling a 3.13% CAGR in enterprise lines.

How does EU funding influence CEE growth?

EUR 865 million in CEF-Digital grants subsidizes 5G corridors, pushing Rest-of-Europe CAGR to 5.92% through 2030.

Page last updated on: