Europe Milk Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.18 Billion |

| Market Size (2026) | USD 8.57 Billion |

| Market Size (2031) | USD 11.07 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Milk Powder Market Analysis by Mordor Intelligence

The Europe milk powder market size is projected to reach USD 8.18 billion in 2025 and USD 8.57 billion in 2026, before rising to USD 11.07 billion by 2031, registering a CAGR of 5.26% from 2026 to 2031. Demand remains supported by infant and follow-on formula, bakery processing, ready meals, sports supplements, and functional dairy beverages, which reduces dependence on a single end use. EU milk production is estimated to decline to 149.4 million metric tons in 2025 from 150.2 million metric tons in 2024, keeping raw milk supply tight. Processors are shifting more milk to higher-margin cheese and premium whey proteins, supporting value growth in specialty powder grades despite tighter commodity powder volumes. Convenience food manufacturers also use dry dairy solids to improve texture, protein content, and storage efficiency. Stricter infant nutrition standards are raising demand for traceable, specification-grade powders. Competition remains moderate, as large cooperatives expand through mergers and ingredient investments, while smaller producers face compliance costs and supply constraints.

Key Report Takeaways

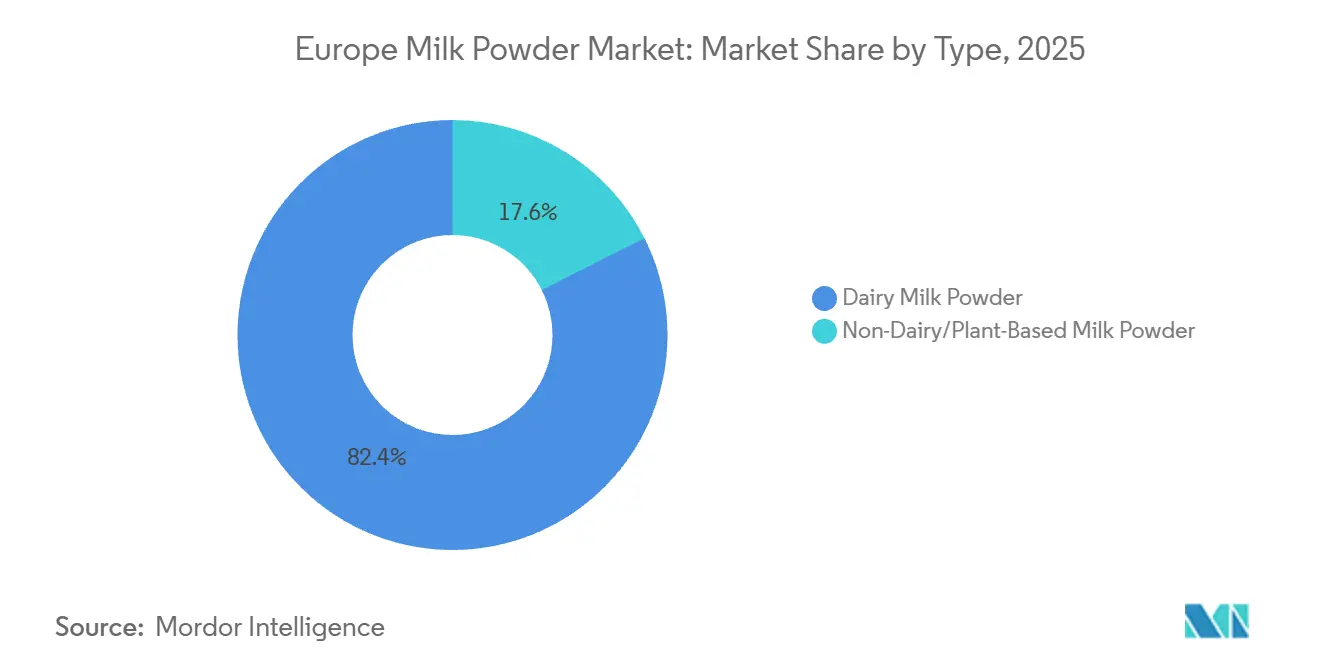

- By type, Dairy Milk Powder led with 82.43% revenue share in 2025, while Non-Dairy and Plant-Based Milk Powder is forecast to expand at a 6.76% CAGR through 2031.

- By distribution channel, Retail held 46.34% of the Europe milk powder market in 2025, while Foodservice recorded the highest projected CAGR at 7.72% through 2031.

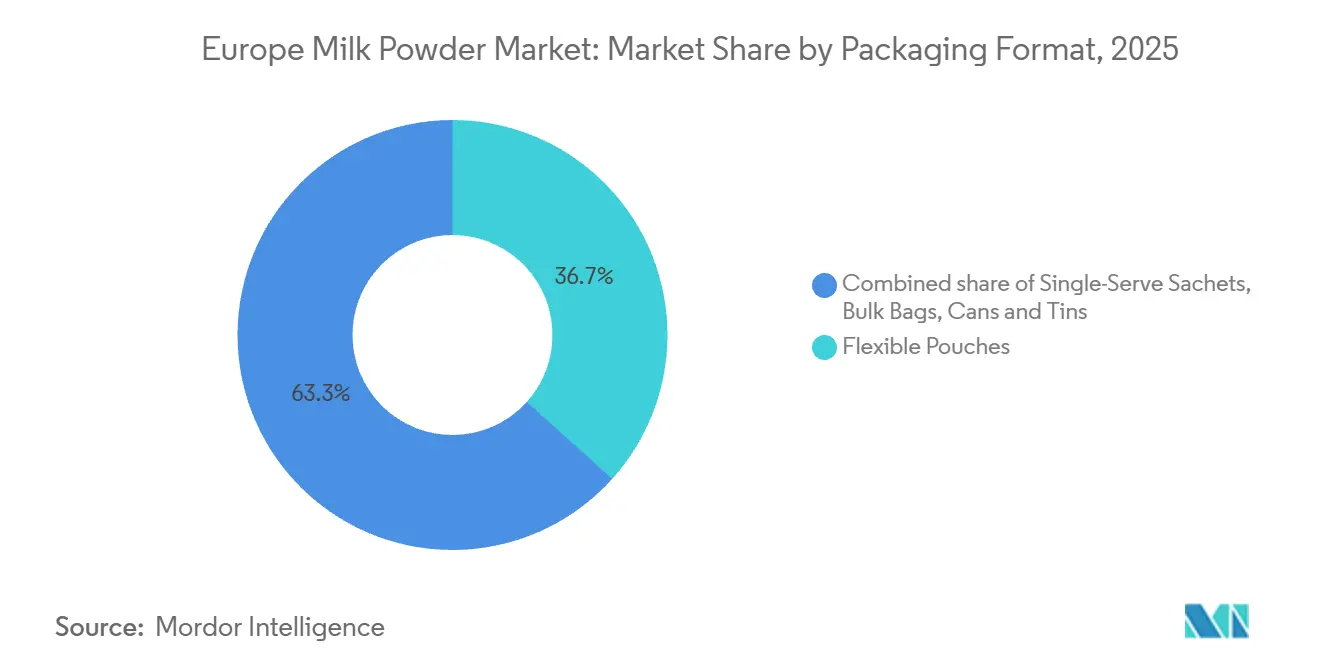

- By packaging format, Flexible Pouches accounted for 36.67% of the Europe milk powder market in 2025, while Single-Serve Sachets are advancing at a 6.98% CAGR through 2031.

- By geography, the United Kingdom held 27.45% of regional value in 2025, while Spain is forecast to grow at the fastest CAGR of 7.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Milk Powder Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Greater Use In Convenience Food Applications | +1.2% | Western and Southern Europe, particularly Germany, France, and Italy | Medium term (2-4 years) |

| Rising Preference For Health-Focused Consumption | +0.8% | Broad European demand, with early gains in the UK, Nordics, and Germany | Long term (≥ 4 years) |

| Increasing Demand Across Infant Nutrition Applications | +1.0% | Strongest in the UK, Germany, and France | Short term (≤ 2 years) |

| Robust Demand From The Food And Feed Industries | +0.7% | Broad European demand, strongest in Eastern Europe and food-processing hubs | Medium term (2-4 years) |

| Extended Shelf-Life Benefit | +0.6% | Broad European demand, with stronger relevance in logistics-constrained Eastern European markets | Long term (≥ 4 years) |

| Increasing Access Through E-commerce And Modern Retail Channels | +0.9% | Western Europe core, with early gains in Spain, Poland, and the Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Greater Use in Convenience Food Applications

The Europe milk powder market gets one of its most stable sources of demand from convenience food manufacturing, where dry dairy solids are easy to store, transport, and use in large-scale production. Bakery and starch-based product manufacturing accounted for 17.7% of the total value added by EU food and beverage processors, showing the strong role of this industrial base in supporting milk powder demand[1]Source: European Parliament, “The EU Dairy Sector”, europarl.europa.eu. Food manufacturers are using more milk powder in ready meals, soups, sauces, bakery fillings, and other processed foods because it reduces dependence on cold-chain logistics while helping maintain texture, flavor, shelf life, and protein content. This trend is especially important in growing processing markets such as Poland and Romania, where industrial output is increasing and cold-chain infrastructure remains less consistent than in Western Europe. As manufacturers continue to replace fresh dairy ingredients with milk powder in selected applications, the Europe milk powder market benefits from steady repeat industrial demand that is less affected by short-term changes in household consumption.

Increasing Demand Across Infant Nutrition Applications

Infant and follow-on formula remains one of the highest-value application areas in the Europe milk powder market because specification standards are strict and product consistency is critical. The European Commission adopted Delegated Regulation (EU) 2025/2017 in October 2025 and Delegated Regulation (EU) 2026/743 in March 2026, and both measures tightened protein-related requirements for infant and follow-on formula made from protein hydrolysates. These updates make it harder for commodity-grade suppliers to compete in formula applications because buyers need traceable inputs with tighter composition control[2]Source: European Commission, “Regulation (EU) No 1169/2011 on the Provision of Food Information to Consumers”, eur-lex.europa.eu. The Europe milk powder market therefore gains more value from premium dairy powders even when birth rates stay relatively stable. This supports suppliers that already operate with strong quality systems, protein fraction expertise, and long-established customer relationships in regulated nutrition categories.

Rising Preference for Health-Focused Consumption

Health-focused consumption is expanding the Europe milk powder market beyond standard household and bakery uses into nutritional products with higher functional value. Demand from the nutritional and sports nutrition segment accounts for 25% to 30% of total dairy ingredient demand by value in the EU, and whey protein isolates and hydrolysates remain preferred formats in this space. Interest in protein-enriched, lactose-free, and fortified dairy products is creating stronger pull for specialty powders that can deliver clean mixing, stable texture, and reliable nutritional claims. The same pattern is widening demand beyond specialist sports formats because medical nutrition and hospital meal support increasingly use high-purity dairy proteins in practical powder form. As this overlap grows, the Europe milk powder market gains a wider premium segment that relies on formulation quality rather than volume alone.

Increasing Access Through E-commerce and Modern Retail Channels

The European milk powder market is also benefiting from broader digital access and better product visibility across organized retail channels. European B2C e-commerce turnover reached EUR 842 billion in 2024 after 7% year-on-year growth, which shows how fast online purchasing has become a regular consumer habit across the region. Online channels are especially useful for premium, specialty, and plant-based powder products that do not always secure wide shelf space in major supermarkets. The retail segment already held 46.34% of market value in 2025, and the online sub-channel is making repeat purchases of infant formula and nutrition powders easier through subscription and direct-to-consumer models. EU food information rules also support this shift because they require consistent product information across channels, which helps consumers compare formats and buy with more confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality And Safety Compliance Obligations | -0.6% | EU-wide, with greater pressure on smaller producers in Eastern Europe | Long term (≥ 4 years) |

| Climate-Related Limitations Affecting Dairy Farming | -0.8% | Southern and Central Europe, with spillover into Belgium and Germany | Medium term (2-4 years), Long term (≥ 4 years) |

| Exposure To Supply Chain Disruption Risks | -0.5% | Cross-border dairy and ingredient supply chains across Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Competitive Pressure From Fresh And Other Dairy Formats | -0.4% | Strongest in higher-income urban markets in Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-Related Limitations Affecting Dairy Farming

Climate-related supply pressure is a structural restraint on the Europe milk powder market because it affects the raw milk base before processors make any product mix decisions. EU dairy herds are projected to shrink by 13% by 2035 under stricter environmental standards, and milk production is forecast to decline by 0.2% annually between 2023 and 2035 despite gradual yield gains per cow. Heat stress adds a second layer of pressure because research shows that milk yields fall once temperature and humidity pass critical thresholds, and cooling technology only offsets part of those losses. When milk becomes scarcer, processors tend to favor cheese and butter before directing residual volumes to powder drying, which places skim and whole milk powder output at a disadvantage. That pattern was already visible in 2025, when USDA data showed a 6% decline in EU whole milk powder production and a 3% decline in NFDM output.

Quality and Safety Compliance Obligations

Quality and safety compliance remains a meaningful restraint in the Europe milk powder market because the burden rises sharply in infant nutrition, clinical use, and export-oriented categories. Directive (EU) 2024/1438 updated harmonized compositional and labeling standards for partly or totally dehydrated milk across EU member states, and Ireland implemented it through the European Union (Dehydrated Preserved Milk) (Amendment) Regulations 2025. The EU Deforestation Regulation, as amended by Regulation 2024/3234, also adds traceability and due diligence requirements for supply chains tied to deforestation-risk jurisdictions, with compliance timelines extending through June 2026 for SMEs. These obligations are easier for large cooperatives to absorb because they already run broader testing, traceability, and certification systems. Smaller producers therefore face a heavier cost burden, and that increases the likelihood that the Europe milk powder market will keep consolidating around scale players with stronger compliance infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dairy Origins Anchor Market, Plant-Based Accelerates

Dairy milk powder is projected to hold 82.43% of the Europe milk powder market share in 2025, keeping the category central to value creation across food manufacturing, infant nutrition, and foodservice. Whole milk powder and skim milk powder remain key inputs for confectionery, bakery, and formula production because they provide standard quality, storage stability, and formulation flexibility. This dairy base continues to benefit from established cooperative collection networks across Germany, France, Ireland, and the Netherlands. However, whole milk powder faces tighter supply as processors shift milk toward cheese and butter, and USDA data indicate a 6% decline in EU whole milk powder production in 2025. Stricter infant formula regulations also support demand for high-purity dairy powders that meet tighter protein and traceability requirements.

The Europe milk powder market size for non-dairy and plant-based milk powder is projected to grow at a CAGR of 6.76% between 2026 and 2031, making it the fastest-growing type category. Oat-based powder is gaining traction in Northern and Western Europe, supported by its neutral taste, sustainability positioning, and foodservice use. Almond powder holds a stable shelf-stable position in Southern Europe, while soy powder remains relevant for food manufacturers focused on familiarity and cost control. Spray-dried and agglomerated plant-based formats are growing faster than liquid alternatives in many business settings because they are easier to store, last longer, and cost less to transport. This shift is expanding the Europe milk powder market and moving the industry toward more functional dry formats.

By Distribution Channel: Retail Anchors the Market, Foodservice Outpaces

Retail is expected to account for 46.34% of the Europe milk powder market share in 2025, making it the largest distribution route across supermarkets, hypermarkets, convenience stores, grocery stores, and online retail. Household demand for infant formula supports this channel, as parents need regular replenishment and reliable availability in stores and online. Private-label products also remain important in Western Europe, where they secure shelf space and maintain price competition, especially in pouches and cans. Online retail is gaining importance in the Europe milk powder market by improving access to premium, organic, and specialty stock keeping units with limited in-store placement. EU food information rules support this channel by keeping core product details consistent across digital and physical points of sale.

The foodservice segment of the Europe milk powder market is projected to register a CAGR of 7.72% between 2026 and 2031, outpacing retail and industrial growth. Cafés, quick-service restaurants, hotels, rail catering services, offices, and institutional kitchens use dry dairy formats to avoid refrigeration and reduce waste in lower-volume service settings. Instant-grade and portion-ready powders help operators prepare beverages faster while maintaining consistency and simple storage. Industrial customers continue to use large volumes in formula manufacturing, bakery, confectionery, and supplement production, giving the distribution structure a strong business-to-business base. As a result, the Europe milk powder market does not depend on one outlet model, as household retail demand and professional foodservice demand grow for different but complementary reasons.

By Packaging Format: Flexible Pouches Lead While Single-Serve Sachets Emerge

Flexible pouches are expected to hold 36.67% of the Europe milk powder market in 2025, staying ahead of rigid formats due to shelf-space efficiency, resealability, and lower packaging cost. They remain widely used in retail infant formula and household products, where buyers prefer medium-volume packs that are easy to store after opening. Cans and tins continue to support premium and organic lines, as strong closures and product protection build trust in sensitive nutrition products. Bulk bags meet industrial needs, as buyers focus on transport efficiency, easy handling, and large-batch procurement. As a result, packaging choice depends on channel economics as well as consumer preference.

The Europe milk powder market size for single-serve sachets is projected to grow at a CAGR of 6.98% between 2026 and 2031, driven by demand for portion control and non-refrigerated use. Foodservice operators use these packs to simplify beverage preparation and reduce waste in hotels, offices, and travel settings. Retail adoption is also rising as urban consumers seek convenient packs for mobile routines and smaller purchases. Across the Europe milk powder industry, sustainability and convenience now guide packaging decisions, with recyclable mono-material structures gaining attention. The packaging mix is shifting toward formats that improve logistics, support portion accuracy, and strengthen environmental positioning.

Geography Analysis

The United Kingdom is expected to hold 27.45% of the regional value in 2025, making it the largest national market in the Europe milk powder market. Strong retail networks, steady infant formula demand, and wider use of online grocery channels support this position. Germany and France remain the largest producing countries in the regional dairy system. Germany accounts for 22% of total EU milk deliveries to dairies, while France contributes 16.6%, based on the cited European Parliament baseline. The Netherlands, Belgium, and Ireland strengthen the Western European cluster through spray-drying capacity and export links. The December 2024 EU-Mercosur political agreement includes a 10,000 metric ton zero-duty quota for EU milk powder exports, improving access for established suppliers.

The Europe milk powder market size in Spain is projected to expand at a CAGR of 7.25% between 2026 and 2031, making Spain the fastest-growing geography in the region. Spain is growing from a less-saturated base and remains attractive for packaged and processed powder because domestic milk production does not fully meet demand. FeNIL estimated Spain’s milk production deficit at 30% of national needs, supporting imports and processed dairy supply. Poland is becoming a key processing center in Eastern Europe, as its growing food manufacturing base creates steady demand for whole and skim milk powder. Denmark and Sweden add premium demand through organic and grass-fed certified products.

Belgium, the Netherlands, and the rest of Europe form an important secondary layer of the Europe milk powder market by combining processing, transit, and emerging demand roles. Belgium serves as both a processor and a logistics node for cross-border powder flows, giving it importance beyond domestic consumption. Emerging Eastern European processing markets add depth as convenience food manufacturing and retail diversification expand. The CAP 2023-2027 framework supports the market through direct payments and rural development funding. However, OECD-FAO still expects overall EU milk production to stagnate as dairy cow numbers decline and yield growth slows.

Competitive Landscape

The Europe milk powder market remains moderately consolidated, with large cooperatives and multinational dairy groups shaping supply, quality standards, and customer access. Arla Foods, Royal FrieslandCampina, Groupe Lactalis, and Danone maintain strong positions through farm linkages, processing assets, and long customer relationships in regulated nutrition categories. Their advantages are strongest where supply security, traceability, and protein specifications matter more than price. The planned June 2026 merger of Arla Foods and DMK Group would strengthen scale in Northern Europe and Germany by creating Europe’s largest farmer-owned dairy cooperative, with a combined milk pool of 19.4 billion kg annually. The planned January 2026 merger between FrieslandCampina and Milcobel would also expand cooperative scale and production in Belgium and the Netherlands.

Competitive strategy in the Europe milk powder market is moving from commodity exposure toward higher-value protein ingredients, formulation support, and application-specific powders. FrieslandCampina Ingredients’ planned March 2026 expansion of its Borculo facility would double capacity for whey protein isolate and milk fat globule membrane ingredients. This investment supports higher-margin uses in infant nutrition, functional foods, sports nutrition, and medical nutrition, instead of relying only on bulk powder sales. Fonterra’s planned February 2026 trial production runs of advanced protein ingredients at its Studholme facility also show how major dairy companies are building advanced powder capabilities beyond Europe. This shift toward specialty proteins helps companies manage tighter raw milk supply and lower returns in commodity grades.

Smaller players still have opportunities in organic, grass-fed, and plant-based niches, but barriers to entry continue to rise. Compliance systems, traceability, drying capacity, and access to stable milk pools increasingly favor larger operators that can spread fixed costs across higher volumes. Major cooperatives are also using precision livestock farming and data-driven milk quality tools to protect yields and improve efficiency amid climate and regulatory pressure. As consolidation advances, the Europe milk powder market should remain open to niche innovation, but scaled players are expected to lead regulated, export-oriented, and high-specification categories.

Europe Milk Powder Industry Leaders

Arla Foods amba

Royal FrieslandCampina N.V.

Groupe Lactalis

Danone S.A.

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Arla Foods and DMK Group completed their merger, creating Europe's largest farmer-owned dairy cooperative with a combined milk pool of 19.4 billion kg annually across 11,200 dairy farmers in seven countries and a pro forma revenue exceeding EUR 20 billion. The merger materially consolidates Northern European milk powder and dairy ingredients capacity and is expected to reshape competitive dynamics in Germany and Scandinavia.

- March 2026: FrieslandCampina Ingredients completed a strategic expansion of its Borculo facility in the Netherlands, doubling production capacity for both whey protein isolate (WPI) and milk fat globule membrane (MFGM) ingredients. The expanded site entered commercial operation in March 2026 and reduces CO₂ emissions in alignment with FrieslandCampina's 2030 climate targets

- February 2026: Fonterra completed trial production runs of advanced protein ingredients at its Studholme facility in New Zealand following a USD 50.1 million investment, with first advanced protein concentrate outputs off the line and commercial scale-up targeting European and Asian customers.

Europe Milk Powder Market Report Scope

| Dairy Milk Powder | Whole Milk Powder (WMP) |

| Skim Milk Powder (SMP) | |

| Others | |

| Non-Dairy/Plant-Based Milk Powder | Soy Milk Powder |

| Almond Milk Powder | |

| Coconut Milk Powder | |

| Oat and Other Cereal-Based Powders |

| Retail | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | |

| Online Retail | |

| Other Distribution Channel | |

| Foodservice | |

| Industrial | Infant and Follow-on Formula |

| Bakery and Confectionery | |

| Dairy-based Beverages and Recombination | |

| Nutritional and Sports Supplements | |

| Others (Ready-Made Meals, cosmetics, etc.) |

| Flexible Pouches |

| Cans and Tins |

| Bulk Bags |

| Single-Serve Sachets |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Poland |

| Denmark |

| Sweden |

| Rest of Europe |

| By Type | Dairy Milk Powder | Whole Milk Powder (WMP) |

| Skim Milk Powder (SMP) | ||

| Others | ||

| Non-Dairy/Plant-Based Milk Powder | Soy Milk Powder | |

| Almond Milk Powder | ||

| Coconut Milk Powder | ||

| Oat and Other Cereal-Based Powders | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | ||

| Online Retail | ||

| Other Distribution Channel | ||

| Foodservice | ||

| Industrial | Infant and Follow-on Formula | |

| Bakery and Confectionery | ||

| Dairy-based Beverages and Recombination | ||

| Nutritional and Sports Supplements | ||

| Others (Ready-Made Meals, cosmetics, etc.) | ||

| By Packaging Format | Flexible Pouches | |

| Cans and Tins | ||

| Bulk Bags | ||

| Single-Serve Sachets | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Denmark | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of Europe milk powder demand in 2026?

The Europe milk powder market is valued at USD 8.57 billion in 2026 and is forecast to reach USD 11.07 billion by 2031 at a 5.26% CAGR.

Which product type is leading Europe milk powder sales?

Dairy milk powder leads with 82.43% share in 2025, supported by its entrenched role in food manufacturing, infant nutrition, and foodservice.

Which channel is growing fastest across Europe milk powder sales?

Foodservice is the fastest-growing channel with a 7.72% CAGR through 2031, driven by cafés, hotels, QSRs, offices, and institutional catering.

Why is Spain expanding faster than other countries in this space?

Spain is forecast to grow at a 7.25% CAGR through 2031, helped by a less-saturated base and a structural milk production deficit equal to 30% of national needs.

Page last updated on: