Europe Machining Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.93 Billion |

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2031) | USD 6.04 Billion |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Machining Centers Market Analysis by Mordor Intelligence

The Europe Machining Centers Market size was valued at USD 4.93 billion in 2025 and is estimated to grow from USD 5.11 billion in 2026 to reach USD 6.04 billion by 2031, at a CAGR of 3.40% during the forecast period (2026-2031). A steady headline growth rate masks an accelerated shift toward five-axis and multitasking platforms, as electric-vehicle battery-housing work, sovereign semiconductor programs, and near-shored aerospace blades all demand one-setup machining that compresses lead times and minimizes re-fixturing. Policy liquidity is also pivotal; the European Union’s Important Projects of Common European Interest (IPCEI) framework continues to unlock vast funding for advanced microelectronics and digital infrastructure, steering buyers toward control-rich models capable of 0.5-millisecond block processing.[1]European Commission, “IPCEI AI Communication 2025,” europa.eu Parallel headwinds shape the same landscape. Industrial electricity prices averaged USD 0.19 per kilowatt-hour in Aragón during 2025, 50% above the French mean, forcing factories to adopt regenerative drives and off-peak production schedules. At the same time, a severe shortage of skilled machinists is widening; an overwhelming majority of medium-sized builders report deep hiring difficulties, prompting vendors to roll out conversational human-machine interfaces that cut setup steps in half and enable less experienced staff to run simultaneous-contouring work cells.

Key Report Takeaways

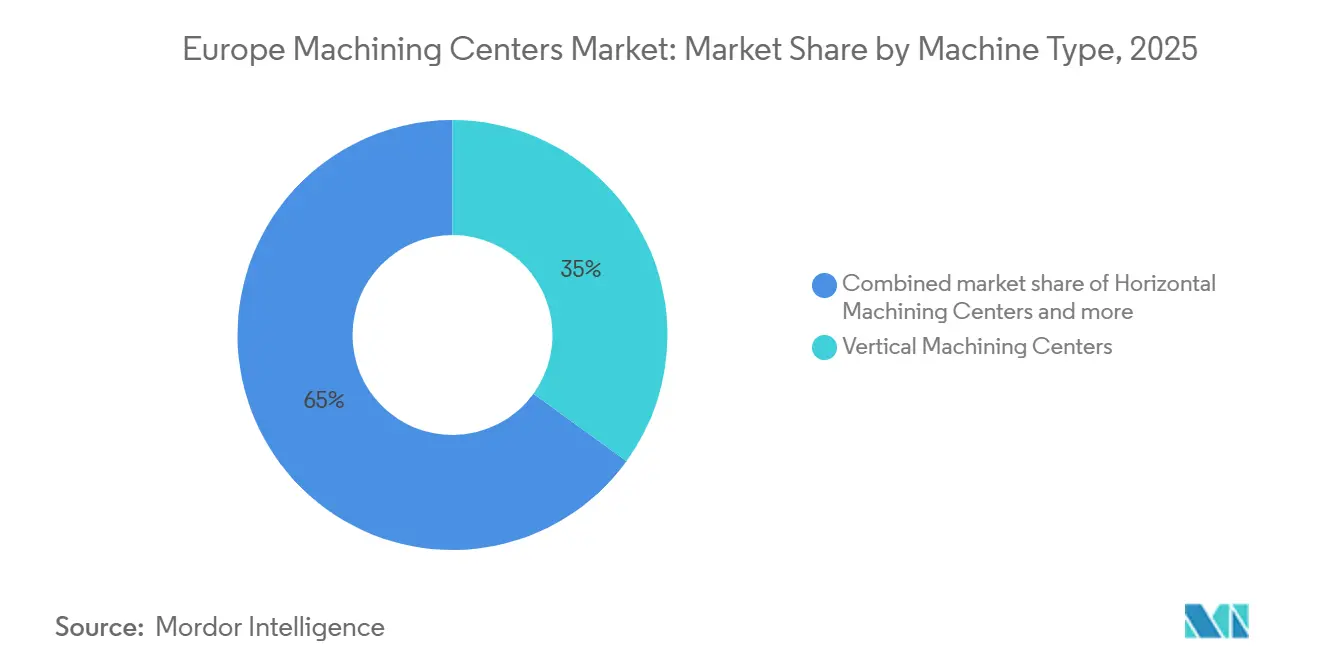

- By machine type, vertical machining centers held 35% of the Europe machining centers market share in 2025, while universal/5-axis machining centers are projected to post a 5.80% CAGR to 2031.

- By axis configuration, 3-axis equipment accounted for 42% of the Europe machining centers market size in 2025 and 5-axis & above machines are advancing at a 6.20% CAGR through 2031.

- By spindle orientation, vertical spindles led with a 48% of the Europe machining centers market share in 2025; multi-spindle designs recorded the highest projected CAGR of 6.00% to 2031.

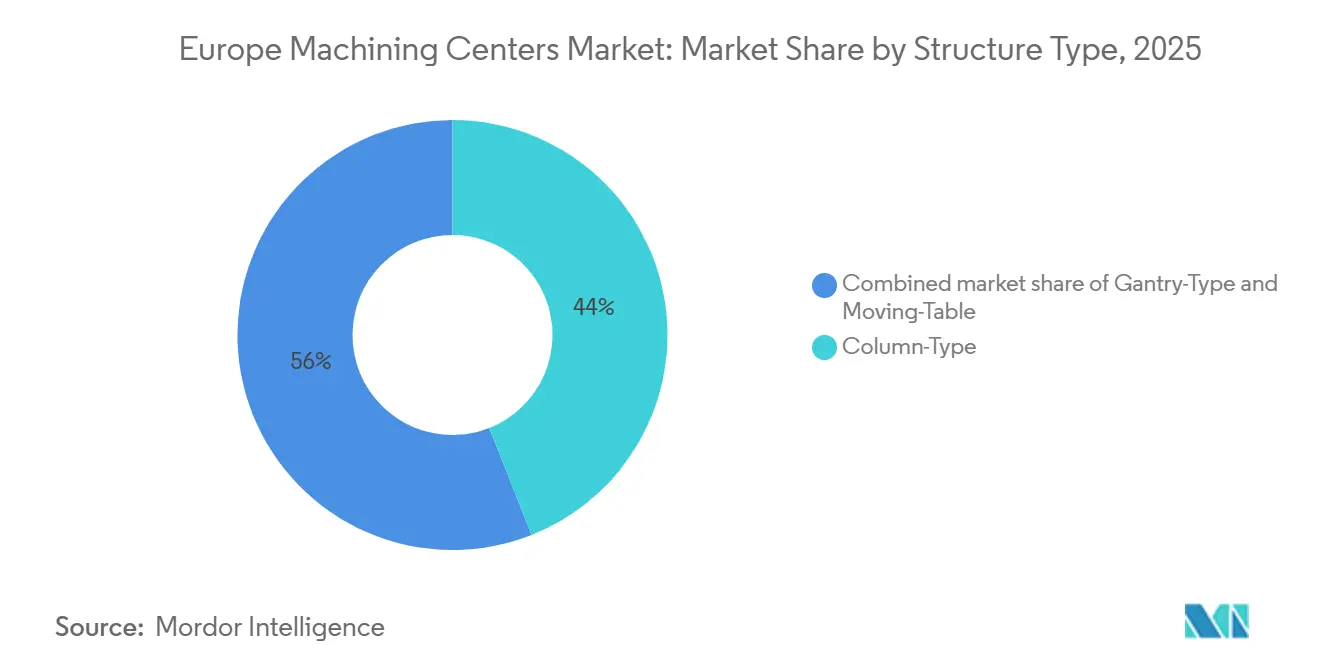

- By structure type, column machines accounted for 44% of the Europe machining centers market size in 2025, whereas gantry platforms are forecast to expand at a 5.70% CAGR.

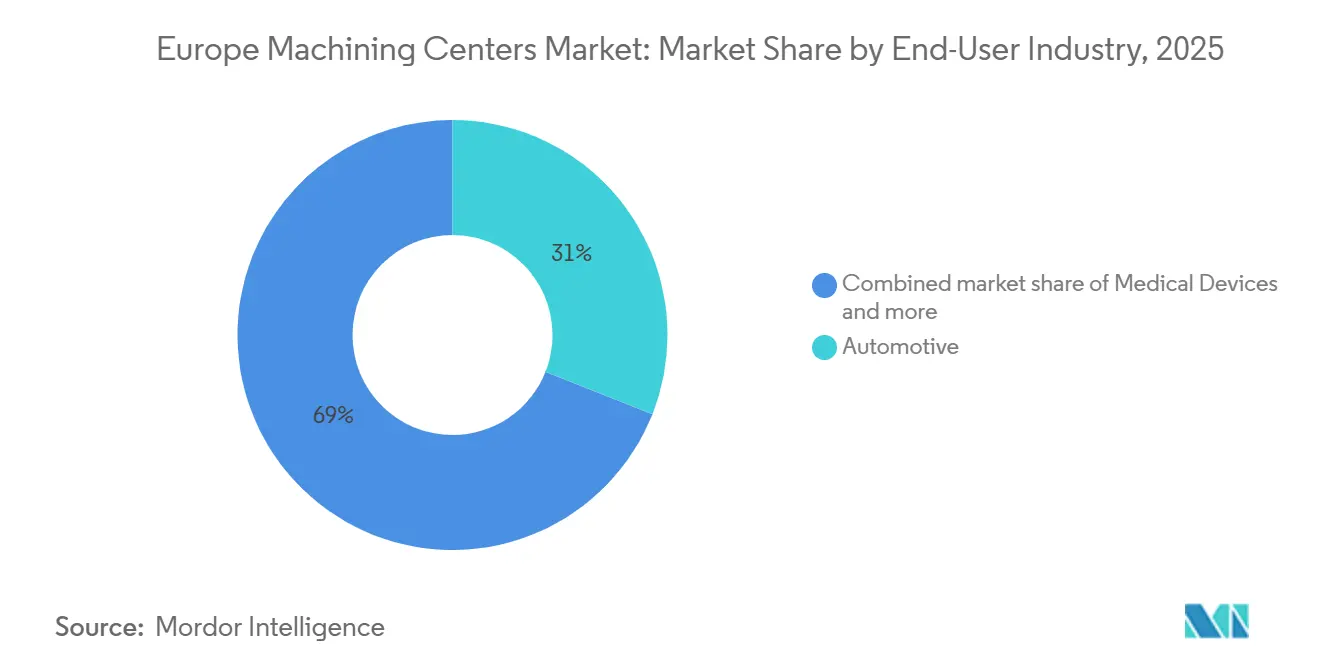

- By end-user industry, automotive manufacturers accounted for 31% of the Europe machining centers market share in 2025, but medical devices are expected to grow fastest at a 5.60% CAGR.

- By country, Germany accounted for 28% of the Europe machining centers market size in 2025, and Spain is the fastest-rising market with a 4.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Machining Centers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-driven lightweight component machining demand accelerates multi-axis machine adoption | +0.8% | Germany, Spain, France, Eastern European battery hubs | Medium term (2-4 years) |

| Industry 4.0-ready HMC/VMC retrofits expand smart machining capabilities across factories | +0.6% | Germany, Italy, the United Kingdom, Czech Republic | Short term (≤2 years) |

| EU IPCEI funding boosts strategic investment in advanced machine-tool capacity | +0.5% | Pan-European, concentrated in Germany, France, the Netherlands, and Belgium | Medium term (2-4 years) |

| Near-shoring of aerospace titanium machining to Eastern Europe increases precision-machining demand | +0.4% | Poland, the Czech Republic, and Romania | Long term (≥4 years) |

| Hybrid additive–subtractive machining-center rollout enhances production flexibility and efficiency | +0.3% | Germany, the United Kingdom, France, Italy | Long term (≥4 years) |

| Rising demand for micro-machining in medical implants drives ultra-precision machine adoption | +0.3% | Germany, Switzerland, Ireland, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV-Driven Lightweight Component Machining Demand Accelerates Multi-Axis Machine Adoption

Battery-electric vehicles swap cast-iron engine blocks for aluminum e-motor housings and CFRP body parts that require simultaneous five-axis contouring to avoid thermal distortion. BMW’s USD 216 million upgrade in Landshut added 17 industrial printers to supply 4,500 sand cores daily, cutting casting cycle time and energy use. Stellantis is directing massive capital investments toward its Zaragoza gigafactory, triggering a large-scale hiring demand that severely outpaces the local talent pool. This profound labor gap is pushing builders to embed AI-assisted tool-path optimization to compensate for the scarcity of master machinists. Chery-Ebro’s Barcelona joint venture aims to reach 150,000 units annually by 2029 and is sourcing multi-axis centers capable of finishing aluminum battery trays with cooling channels in a single setup. Seat’s 64,000-square-meter battery plant will ship 300,000 systems per year once operational in 2026, each calling for ISO 9001-certified machining of tight-tolerance housings. Altogether, the migration from three-axis horizontals to universal centers shortens changeovers, lowers scrap, and accelerates payback on high-precision machinery.

Industry 4.0-Ready HMC/VMC Retrofits Expand Smart-Machining Capabilities Across Factories

Machine parks across Germany and Italy average 10 to 15 years in age, yet they retain rigid iron foundations capable of performing for another decade when upgraded with modern controls. HEIDENHAIN’s TNC7 Generation 3, released in 2025, supports 24 control loops and 0.5-millisecond block times, unlocking real-time feed-rate adaptations based on spindle-load telemetry. Demonstrating this potential, a VDW case study showed significant cycle-time reductions and productivity lifts after a 12-year-old horizontal machine was retrofitted with a Siemens SINUMERIK 840D sl and condition-monitoring sensors. To support these upgrades, vast EU IPCEI funding helps SMEs deploy digital twins and sovereign on-premise AI, easing the investment hurdle for retrofit packages. Targeted retrofits also yield massive efficiency gains; for instance, Mazak’s Worcester site swapped four legacy CO₂ lasers for two automated fiber systems, boosting output by 40% and trimming power use by 67%. Ultimately, by postponing greenfield purchases, retrofits can shave as much as 70% off capital outlay, a vital financial cushion when order books thin.

EU IPCEI Funding Boosts Strategic Investment in Advanced Machine-Tool Capacity

The IPCEI scheme allows national governments to exceed standard state-aid caps for projects key to continental competitiveness. The sweeping IPCEI-AI framework prioritizes manufacturing applications such as digital twins and edge analytics, which depend on machining centers with open OPC UA or MTConnect interfaces. Germany committed billions to semiconductor tooling, hydrogen-electrolyzer stack machining, and battery-cell housings, seeding demand for spindle technologies that hold sub-5-micrometer repeatability. European Digital Innovation Hubs (EDIHs) supply simulation and additive guidelines, lowering SME entry barriers to hybrid platforms. Joint-country consortia can now co-develop gantry machines for wind-turbine bearings under shared IP rules, cutting time-to-market by a year. By heavily subsidizing the risk of early-stage deep-tech spending, IPCEI unlocks massive capital investments that would otherwise stall, nudging the Europe machining centers market toward higher-end technology adoption.

Near-Shoring of Aerospace Titanium Machining to Eastern Europe Increases Precision-Machining Demand

Western primes are relocating titanium roughing to Poland, the Czech Republic, and Romania, blending lower labor costs with supply-chain proximity. Collins Aerospace added 4,000 square meters at Tajęcina, Poland, to machine titanium landing-gear structures using five-axis horizontal machining. Pratt & Whitney will pour USD 100 million into isothermal forging and sonic machining in Rzeszów by 2028, cementing the region’s Tier 1 status. MTU Aero Engines Polska shipped its 5,000th low-pressure turbine module in 2025 under AS 9100 quality regimes. Safran’s new Belgian facility will produce 700,000 titanium blades annually by 2026, combining EDM drilling with five-axis airfoil profiling. As Eastern shops adopt Siemens NX CAM and TNC7 controls, their productivity gap versus German peers narrows, reinforcing premium machine uptake.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical capex cuts driven by EU industrial output volatility reduce equipment investments | -0.5% | Germany, France, Italy; spillover to Spain and Eastern Europe | Short term (≤2 years) |

| Skilled operator shortages persist despite increasing automation adoption | -0.4% | Germany, United Kingdom, Spain, Italy, Czech Republic | Medium term (2-4 years) |

| High energy costs impact operational viability of large-format gantry machining centers | -0.3% | Spain, Italy, Germany; partial relief in France and the Nordics | Short term (≤2 years) |

| Extended lead times for precision spindles and controllers delay machine deployment | -0.2% | Pan-European machining hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Cyclical Capex Cuts Driven by EU Industrial-Output Volatility Reduce Equipment Investments

German machine-tool orders declined sharply in the first half of 2025 as automakers deferred EV-platform tooling amid uncertainty over battery chemistry. Production dropped 3%, yet headcount stayed near 64,000 because builders leaned on shorter workweeks over layoffs, compressing profit margins. Eurostat shows capital-goods inflation at 1.8%, while electricity prices remain structurally above pre-2022 levels despite modest 2025 retreats.[2]Eurostat, “Industrial Producer Price Index 2025,” eurostat.eu Chemical capacity shrank by 10%, and investment plummeted by 80%, underscoring the erosion of competitiveness against the United States producers that enjoy lower energy costs. Customers answer by stretching replacement cycles to 12–15 years and pushing OEMs to finance extended terms, sapping near-term momentum in the Europe machining centers market.

Skilled-Operator Shortages Persist Despite Increasing Automation Adoption

A late-2024 CECIMO poll, drawing responses heavily from small and mid-sized builders, found an overwhelming majority struggling to hire production engineers. The EU aims to train 20 million ICT specialists by 2030, but advanced manufacturing curricula lag, especially in CNC, robotics, and data analytics. Zaragoza’s automotive cluster faces an acute deficit of EV-specialist engineers while graduating only a fraction of the required talent, forcing firms to outbid each other or relocate work. To compensate, Hurco’s Max5 conversational interface enabled Wellington Engineering to reduce setups from 5 to 2 and shorten lead times from weeks to days, empowering semi-skilled staff. With a three-to-five-year gap before new graduates arrive, automation and simplified HMIs are the only near-term salve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Versatile Verticals Dominate a Shifting Mix

Vertical machining centers accounted for 35% of the Europe machining centers market in 2025, thanks to their flexibility across stamping-die finishing, medical micro-milling, and general job-shop tasks. Three-axis versions serve mold roughing or prismatic automotive parts at attractive capital costs, while four-axis rotary tables add indexed positioning for side features. The fastest-growing slice, universal/5-axis platforms, is expanding at a 5.8% CAGR through 2031 as aerospace primes and medical-device makers chase one-setup contouring. Advanced mill-turn platforms like Okuma’s MULTUS U3000 2SW fold heavy-duty 12,000-rpm milling inside a twin-spindle frame, trimming floor space 30% and inventory 40%. As labor scarcity lifts the value of unattended machining, builders bundle pallet pools, in-process probing, and cloud condition monitoring, tilting new orders away from basic verticals.

The migration is reinforced by the complexity of the parts. Titanium turbine blades, orthopedic joints, and aluminum battery trays all need tool vectors that strike freeform surfaces at variable lead and tilt angles. Five-axis cycles cut setup time in half and raise first-pass yield, offsetting sticker premiums that run 40–60% above equivalent three-axis units. Because VMC iron already dominates the install base, retrofit kits that add trunnions or rotary tables offer a transition path, but most buyers now opt for ground-up universal machines with gantry-style Y-axis support that suppresses vibration on interpolated moves, future-proofing capacity while consolidating programming know-how.

By Axis Configuration: Five-Axis Simultaneous Motion Gains Ground

Three-axis systems held 42% of the Europe machining centers market share in 2025, underpinned by high-volume automotive work where features lie in a single plane. Yet the 5-axis & above cohort is forecast to grow at 6.2% CAGR because simultaneous contouring eliminates re-fixturing, halves cycle times, and unlocks sculptured geometries. DMG MORI’s DMU 65 H monoBLOCK, released in 2026, carries a 453-tool magazine and 5-µm positioning accuracy, targeting turbine casings that demand continuous tool engagement. FANUC’s compact Robodrill α-D14MiA5 squeezes five-axis kinematics into an ultra-compact footprint of less than 2 square meters, making it highly viable for space-constrained medical implant cleanrooms.

Indexed four-axis horizontals remain popular for engine blocks and transmission housings, offering two-face machining in a single clamp with adder pallets for lights-out cycles. However, soaring titanium and Inconel volumes require tool tilts that four-axis units cannot deliver without manual reclamping, pushing aerospace suppliers toward full five-axis horizontals rated for 1,200 Nm spindle torque. Certification bodies now expect ISO 230-1 and ISO 230-2 compliance reports during factory acceptance testing, nudging smaller shops to upgrade metrology and environmental controls alongside machine purchases.

By Structure Type: Column Machines Hold the Middle While Gantries Address XXL Workpieces

Column-type frames delivered 44% of 2025 revenue, balancing rigidity, footprint, and cost for parts under 1 m in any dimension. Moving-table variants process diesel engine blocks and die-cast molds efficiently, with cast-iron beds damping vibration. Gantry-type machines, though energy-hungry, are set to grow at a 5.7% CAGR as wind-turbine hubs, aerospace wing spars, and injection-mold plates push beyond column capacities. GROB’s new GP1350 portal spans 1.95 m across Y-travel and carries 3.6-ton payloads, servicing body-in-white tooling without turning the part.

Gantry electric bills push operators to schedule roughing at night tariffs and fit regenerative axes that feed braking energy back into the grid. Meanwhile, composite and polymer-concrete structures cut moving mass by up to 20% while increasing stiffness, a trade-off that reduces spindle power demands. Chiron and Fraunhofer’s HoverLIGHT collaboration utilizes an aluminum foam and hollow-sphere composite to reduce crossbeam weight by 20% while matching cast-iron damping, hinting that next-generation gantries may narrow the operating-cost gap with columns.

By Spindle Orientation: Multi-Spindle Designs Lift Throughput Without Extra Floor Space

Vertical spindles accounted for 48% of shipments in the Europe machining centers market, with widespread use in automotive, mold, and electronics subcontracting. Gravity-aided chip flow suits open-top coolant wash and simplifies robotic loading. The fastest-growing segment through 2031 is the multi-spindle category at a 6.0% CAGR, because dual or triple cutting heads let factories double output without doubling real estate. Brother’s SPEEDIO S1000X3 leverages an ultra-fast 0.6-second tool change and a high-speed 30,000-rpm spindle to drive maximum productivity, particularly when machining small aluminum housings.

Horizontal spindles remain dominant in high-torque steel or titanium cutting, where sideward chip evacuation prevents recutting. Multi-spindle adoption is gated by programming complexity: each head needs independent tool offsets, coolant pressure, and thermal maps. New controls, such as Heidenhain’s TNC7, now orchestrate four spindles with collision avoidance, shrinking learning curves. Wage inflation above USD 32 per hour in Germany and the United Kingdom makes these investments palatable, especially when amortized over multi-shift unattended schedules.

By End-User Industry: Automotive Leads While Medical Devices Surge

Automotive OEMs and Tier 1s accounted for 31% of 2025 demand in the Europe machining centers market, relying on high-volume cells for dies, battery cases, and powertrain housings. Platform uncertainty around battery chemistry constrained fresh purchases in 2025, but retrofit work kept spindle hours healthy. Medical devices, though smaller today, will outpace all others at a 5.6% CAGR to 2031. The shift is driven by aging demographics and the popularity of minimally invasive surgeries that require cobalt-chrome and titanium implants with micron-level accuracy. FANUC’s advanced Robodrill platforms specifically target implants, packaging sub-0.004 mm repeatability inside cleanroom-ready footprints.

Aerospace and defense orders were buoyant thanks to geared-turbofan programs and composite fuselage sections, forcing suppliers to install torque-rich horizontals and hybrid additive repair cells. Energy, including wind and hydrogen, needs XXL gantries for turbine housings and electrolyzer plates, benefiting from IPCEI-Hydrogen grants.[3]European Commission, “Approved IPCEIs in the Hydrogen Value Chain,” ec.europa.eu Mold and die work remains a stable revenue pillar, especially where high-cavitation tools justify five-axis finish cuts and mirror-grade surfaces. Across sectors, regulatory overlays from IATF 16949 for cars to AS 9100 for jets favor builders with audited quality processes, shoring up mid-priced European players against low-cost imports.

Geography Analysis

Germany generated 28% of regional revenue in 2025, anchored by a dense web of automotive OEMs, Tier 1s, and machine-tool champions that collectively generate industry-leading capital-goods revenues. Yet orders experienced a notable year-on-year decline as carmakers paused EV retooling, nudging builders to rely on services and retrofits to protect margins. France and the United Kingdom follow in mid-teens, powered by Airbus final assembly in Toulouse, Safran’s turbine-blade works, and Rolls-Royce engine cores, all of which require five-axis titanium machining. Italy’s mold-and-packaging niche remains export-competitive thanks to rapid customization, though energy tariffs weigh more heavily than in its Northern peers.

Spain is the breakout, advancing at a 4.8% CAGR to 2031 on USD 324 million of battery assembly investment by Seat and the USD 216 million aluminum-housing upgrade at BMW’s Landshut for cross-border modules. ITP Aero’s USD 2.03 billion in revenue in 2025, up 17%, underscores the momentum of its turbine modules; its new Ajalvir MRO center will bolster domestic demand for multitasking cells. Spanish PMI reached 52.1 in October 2025, confirming expansion, but USD 0.19 /kWh industrial electricity still challenges gantry operations, steering shops toward regenerative drives and energy-efficient controls.

The rest of Europe, including Poland, the Czech Republic, Romania, Switzerland, and the Nordics, welcomes nearshore aerospace work. Collins Aerospace and Pratt & Whitney’s USD 100 million Rzeszów project, plus MTU’s turbine milestone position, position Poland as a titanium-machining hotspot. Swiss contract manufacturers, though outside the EU, dominate ultra-precision implants under ISO 13485, buying wire-EDM and micro-milling systems in steady volumes. Czech and Romanian shops pick up automotive-casting and electronics work that seeks labor savings but still demands CE-marked equipment. Across all borders, compliance with the EU Machinery Directive ensures that even imported hardware carries documented safety and electromagnetic-compatibility credentials.[4]European Commission, “Machinery Directive 2006/42/EC,” Official Journal of the European Union, eur-lex.europa.eu

Competitive Landscape

The Europe machining centers market exhibits a moderately concentrated. The top five suppliers, DMG MORI, Mazak, GF Machining Solutions, Makino, and Haas, collectively capture a substantial portion of regional demand, leaving space for specialists such as Hermle, Chiron, Starrag, and GROB to claim vertical niches. Japanese brands lean on installed-base service contracts and global financing arms for customer stickiness, while German and Swiss builders emphasize turnkey automation cells and co-development with aerospace primes. In February 2025, DMG MORI unveiled the DMU 60 eVo second generation, featuring a 40% larger work envelope and 4-µm accuracy, bundled with robotic pallet changers and cloud monitoring to slash commissioning time from weeks to days.

Digital convergence is narrowing product gaps. Siemens and Heidenhain now embed AI-driven adaptive feed algorithms that self-tune in real time, commoditizing performance once exclusive to proprietary mechanical designs. Mid-tier entrants like Hurco exploit conversational controls to win job-shop orders where ease of use and fast training trump ultimate rigidity, offering 10–15% capex savings and 50% shorter learning curves. The EU Machinery Directive creates a regulatory moat via mandatory risk assessments and CE marking, deterring low-cost Asian imports that lack accredited safety documentation.

Innovation spending pivots toward hybrid manufacturing, lightweight composite frames, and energy-saving drives. Hermle’s 2025 HS flex hybrid automation kit enables legacy centers to run 24-hour unmanned shifts, expanding the addressable market among SME mold shops. GROB’s GP1350 portal, which debuted in March 2026, targets body-in-white and wing-spars with 408-tool magazines and 3.6-ton payloads. Market fragmentation persists, medical cleanroom suppliers want ultra-compact five-axis units, aerospace MROs seek hybrid repair machines, and wind-energy OEMs need 5-m gantries with low-rpm high-torque spindles. Such divergence sustains pricing power even as core iron becomes more standardized.

Europe Machining Centers Industry Leaders

DMG MORI AG

Yamazaki Mazak Europe

Makino Europe GmbH

Haas Automation Europe

GF Machining Solutions (United Grinding Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GROB-Werke, industrial manufacturer, premiered the GP1350 five-axis portal with 1.95 m Y-travel, 3.6-ton payload, and 408 tools, targeting body-in-white and wing-spar work. The introduction of GROB-Werke’s heavy-duty GP1350 portal significantly elevates the European gantry segment, equipping regional aerospace and automotive manufacturers with the advanced, single-setup architecture required to efficiently process massive structural components.

- February 2026: Collins Aerospace, an aerospace and defense technology company, completed a 4,000 m² expansion in Tajecina for five-axis titanium landing-gear machining. This will drive sustained regional demand for high-torque, five-axis machining platforms capable of precision titanium profiling.

- January 2026: DMG MORI AG, a high-precision cutting machine tools manufacturer, launched the DMU 65 H monoBLOCK Gen 2 horizontal with 5-µm accuracy and a 453-tool magazine for titanium casings. DMG MORI AG's launch advances European manufacturing by pairing extreme automation with aerospace-grade precision to combat labor costs through high-capacity, unmanned production of complex titanium components.

- October 2025: DMG MORI, a high-precision cutting machine tools manufacturer, and Haimer, a precision tool-holding manufacturer, opened a “Tool Room of the Future” demo center that integrates presetting, shrink-fit, and digital twins to raise productivity by 30%.

Europe Machining Centers Market Report Scope

The Europe Machining Centers Market Report is Segmented by Machine Type (Horizontal Machining Centers, and more), by Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), by Spindle Orientation (Horizontal, Vertical, Multi-Spindle), by Structure Type (Column-Type, Gantry-Type, Moving-Table), by End-User Industry (Automotive, and more), and by Country (Germany, and more). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Machining Centers (HMC) |

| Vertical Machining Centers (VMC) |

| Universal/5-Axis Machining Centers |

| Multi-Tasking Machining Centers (MTM) |

| Others (Gantry/Bridge-Type Centers, Turn-Mill Centers) |

| 3-Axis |

| 4-Axis |

| 5-Axis & Above |

| Horizontal |

| Vertical |

| Multi-spindle |

| Column-Type |

| Gantry-Type |

| Moving-Table |

| Automotive |

| Aerospace & Defense |

| Energy (Oil-Gas, Renewables) |

| Medical Devices |

| Mold and Die Manufacturing |

| Others (General Manufacturing, Job Shops, Electronics, etc.) |

| Germany |

| France |

| United Kingdom |

| Spain |

| Italy |

| Rest of Europe |

| By Machine Type | Horizontal Machining Centers (HMC) |

| Vertical Machining Centers (VMC) | |

| Universal/5-Axis Machining Centers | |

| Multi-Tasking Machining Centers (MTM) | |

| Others (Gantry/Bridge-Type Centers, Turn-Mill Centers) | |

| By Axis Configuration | 3-Axis |

| 4-Axis | |

| 5-Axis & Above | |

| By Spindle Orientation | Horizontal |

| Vertical | |

| Multi-spindle | |

| By Structure Type | Column-Type |

| Gantry-Type | |

| Moving-Table | |

| By End-User Industry | Automotive |

| Aerospace & Defense | |

| Energy (Oil-Gas, Renewables) | |

| Medical Devices | |

| Mold and Die Manufacturing | |

| Others (General Manufacturing, Job Shops, Electronics, etc.) | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe machining centers market?

The Europe machining centers market size reached USD 4.93 billion in 2025 and is projected at USD 5.11 billion for 2026.

How fast will the market grow by 2031?

The market is forecast to expand to USD 6.04 billion by 2031, reflecting a 3.4% CAGR from 2026 to 2031.

Which machine type holds the largest market share?

Vertical machining centers led with 35% share in 2025, while universal/5-axis units are the fastest-growing at 5.8% CAGR.

Which European country is growing quickest?

Spain is the fastest-rising geography, advancing at a 4.8% CAGR through 2031 on EV and turbine investments.

Why are five-axis platforms gaining popularity?

Five-axis machines allow one-setup contouring that halves cycle time and meets tight tolerances demanded by EV battery housings, implants, and turbine blades.

What restrains near-term equipment spending?

Volatile industrial output has triggered capex cuts in Germany and France, while long spindle lead times and energy costs further delay new-machine decisions.

Page last updated on: