Europe Legal Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 6.17 Billion |

| Market Size (2030) | USD 10.31 Billion |

| Growth Rate (2025 - 2030) | 10.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Legal Technology Market Analysis by Mordor Intelligence

The Europe legal technology market size reached USD 6.17 billion in 2025 and is forecast to expand at a CAGR of 10.81% to USD 10.31 billion by 2030. Rapid digital transformation among European law firms, intensified regulatory obligations following the GDPR, and European Commission funding for artificial intelligence sandbox projects underpin the sustained expansion. Post-Schrems II data-transfer constraints heighten demand for compliant cross-border platforms, while multilingual natural language processing tools close talent gaps across the continent. Cloud architecture outperforms on-premises infrastructure as firms emphasize scalability, cyber-resilience, and remote collaboration capabilities. Competitive intensity remains moderate as established software vendors and emerging AI specialists pursue regional data-center rollouts and local compliance certifications to meet jurisdiction-specific standards.

Key Report Takeaways

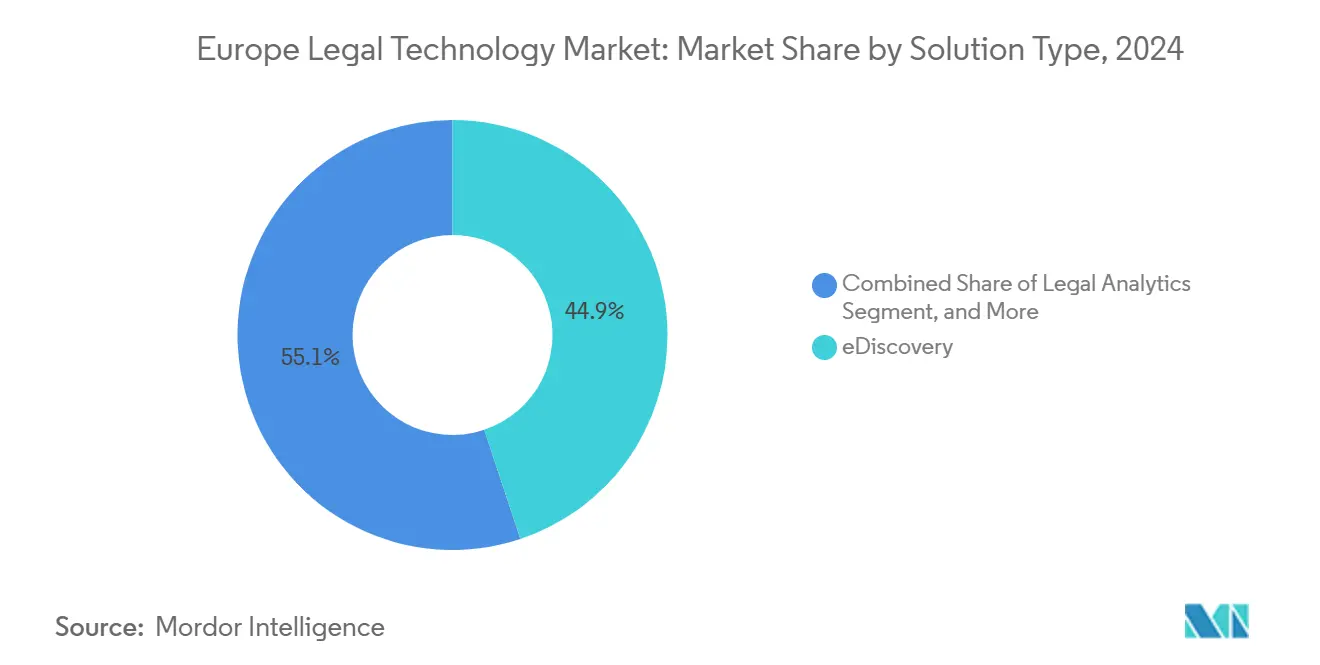

- By solution type, eDiscovery led the Europe legal technology market with a 44.87% share in 2024, and contract lifecycle management recorded the fastest 11.89% CAGR through 2030.

- By deployment model, cloud accounted for a 64.92% share of the Europe legal technology market size in 2024, while hybrid architectures are projected to post a 10.93% CAGR through 2030.

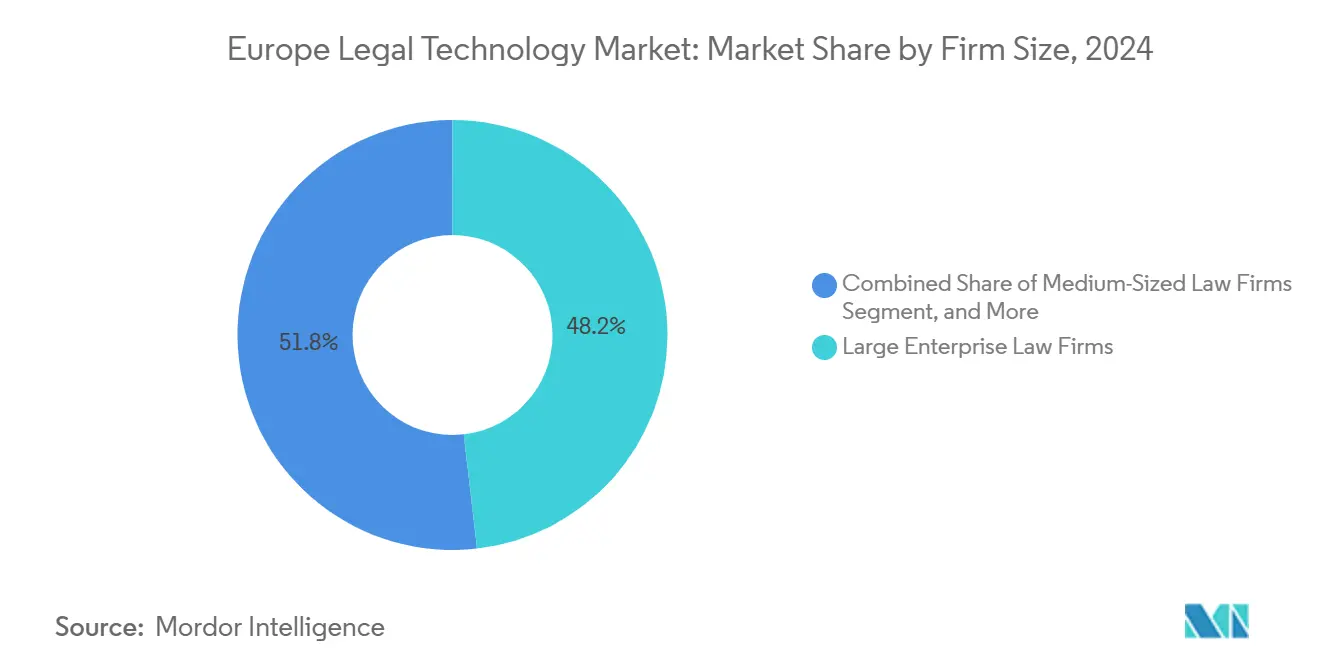

- By firm size, large enterprise law firms held 48.19% revenue share in 2024; small firms are expanding at the highest 11.17% CAGR to 2030.

- By end user, law firms commanded 53.67% of the Europe legal technology market size in 2024, and corporate legal departments are projected to show an 11.37% CAGR outlook to 2030.

- By geography, the United Kingdom captured 29.76% of the Europe legal technology market share in 2024, and the Nordic countries are expected to exhibit an 11.71% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Legal Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Volume of Digital Legal Documents | +2.1% | UK, Germany, France | Medium term (2-4 years) |

| Rising Demand for Automation in Law Firms | +2.8% | Western Europe | Short term (≤ 2 years) |

| Growing Adoption of Cloud Based Solutions | +2.3% | Nordic countries, UK | Medium term (2-4 years) |

| Surge in Cross Border Data Transfer Needs | +1.9% | EU-wide | Long term (≥ 4 years) |

| European Commission Funding for AI Projects | +1.2% | Germany, France, Netherlands | Long term (≥ 4 years) |

| Multilingual Talent Shortage Accelerating NLP | +1.4% | Central and Eastern Europe, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Automation in Law Firms

European practices utilize AI-enabled document review, which reduces average turnaround times by 60-70%. Leading firms in London and Frankfurt invest in automated diligence tools, while mid-tier practices adopt cloud-based practice management suites to remain competitive.[1]Jamie Bryant, “Automation Transforms European Legal Services,” Bloomberg Law, bloomberglaw.com The European Legal Technology Association notes that 78% of surveyed firms plan new automation budgets by 2026. Fee pressure, junior talent costs, and stricter compliance audits drive consistent investment momentum.

Growing Adoption of Cloud-Based Solutions

Cloud penetration reached 73% among Nordic law firms in 2024, driven by the European Banking Authority's guidance that clarifies outsourcing risk safeguards.[2]European Banking Authority, “Guidelines on Outsourcing Arrangements,” eba.europa.eu Microsoft Azure and Amazon Web Services offer data-residency zones that meet GDPR mandates. Subscription models reduce upfront capital outflow by approximately 45%, enabling small practices to acquire advanced analytics that were previously exclusive to large firms.

Surge in Cross-Border Data Transfer Needs

The Schrems II ruling obliges supplementary transfer assessments, prompting vendors such as Relativity and iManage to launch dedicated EU cloud footprints.[3]Court of Justice of the European Union, “Schrems II Ruling Impact Assessment,” curia.europa.eu Multinational M&A workflows require granular data-mapping modules, fueling the adoption of specialized platforms that embed Standard Contractual Clauses and provide real-time risk scoring.

Multilingual Talent Shortage Accelerating NLP Tools

EU policymakers identify language barriers as a hindrance to the single market for legal services. AI vendors respond with translation-ready analytics handling German, French, Italian, and Slavic languages in unified workspaces. Central and Eastern European firms leverage these tools to enter cross-border deals without external linguistic counsel, resulting in a 30% reduction in average translation costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Data Privacy Regulations | -1.8% | Germany, France, EU-wide | Long term (≥ 4 years) |

| High Initial Implementation Costs for SMEs | -1.4% | Southern and Eastern Europe | Medium term (2-4 years) |

| Fragmented Procedure Standards | -1.1% | 27 member states | Long term (≥ 4 years) |

| Conservative Bar Association Culture | -0.9% | Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Data Privacy Regulations Under GDPR

Data-protection authorities levied fines of EUR 1.2 million (USD 1.36 million) against legal entities in 2024, citing inadequate safeguards. German and French regulators favor explicit consent for AI analytics, which can extend deployment cycles by up to 12 months. Vendors respond with privacy-by-design frameworks and ISO 27001 certifications, yet the compliance costs inflate subscription pricing for end-users.

High Initial Implementation Costs for SMEs

Comprehensive suites can require EUR 50,000-150,000 (USD 56,500-169,500) upfront, which can deter small practices. Southern and Eastern European firms often lack access to low-interest financing, and limited in-house IT expertise raises integration expenses. Although cloud subscriptions reduce capital outlay, training and data migration remain significant hidden costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: eDiscovery Dominates While Contract Management Accelerates

eDiscovery solutions held a 44.87% market share in the Europe legal technology market in 2024, reflecting growth in litigation across financial services and life sciences. Automated review, predictive coding, and localized data centers strengthen vendor positioning across Germany, France, and the United Kingdom. Contract lifecycle management is projected to achieve a high-growth 11.89% CAGR as procurement teams pursue real-time obligation tracking amid supply-chain disruptions. Legal analytics tools are gaining traction for predicting outcomes and informing pricing strategies, particularly among Magic Circle firms seeking a competitive advantage. Document automation platforms simplify the generation of multi-language templates, reducing drafting time by approximately 50%. Intellectual property management benefits from the rise in patent application volumes in electronics and biotech, while compliance suites target ESG and sector-specific mandates.

Growth prospects align with evolving enterprise priorities. Corporations integrate contract solutions with enterprise resource planning systems to identify and surface risks in vendor agreements. eDiscovery spending scales with regulatory probes into antitrust and data-privacy matters. Tight integration across modules supports single-pane client experiences, and vendors that bundle analytics with document management command premium pricing.

By Deployment Model: Cloud Solutions Drive Market Transformation

Cloud architecture accounted for 64.92% of Europe legal technology market size in 2024, reflecting robust investment in secure, scalable services. Nordic firms average 73% cloud uptake, facilitated by government digitalization incentives and dependable broadband. Updated European Banking Authority guidance encourages migration of sensitive legal workloads to approved hyperscale zones, boosting confidence in remote hosting. Hybrid patterns emerge as multinationals retain classified datasets on-premises while routing high-volume discovery or analytics to the cloud.

On-premises solutions persist in defense and life sciences practices that mandate maximum data control, yet cost-benefit analyses increasingly favor managed services. Small firms can achieve a 40-50% lower total cost of ownership through subscription, while continuous updates ensure alignment with evolving data-protection rules. Vendors differentiate through in-region disaster-recovery nodes, encryption key ownership options, and zero-trust architectures.

By Firm Size: Small Firms Emerge as Growth Leaders

Large firms generated 48.19% of the revenue in 2024, reflecting extensive cross-border caseloads and the capacity to fund integrated ecosystems. Typical annual spend ranges from EUR 500,000 to 2 million (USD 565,000 to 2.26 million) for enterprise suites that combine workflow, analytics, and client portals. The Europe legal technology market is expanding faster among small practices, with an 11.17% CAGR forecasted to 2030, as SaaS lowers entry barriers. Subscription bundles tailored for niche disciplines, such as family law, insolvency, and real estate, enable parity with larger competitors.

Medium-sized firms maintain selective deployment, emphasizing niche functionality such as intellectual property docketing or regulatory change monitoring. Professional indemnity insurers are increasingly linking premium discounts to documented cybersecurity postures, prompting even small chambers to adopt certified cloud platforms. Regional resellers and managed-service providers play a pivotal role, offering bundled onboarding, training, and help-desk support.

By End User: Corporate Legal Departments Accelerate Adoption

Law firms represented 53.67% of the Europe legal technology market size in 2024, yet in-house legal teams delivered the fastest 11.37% CAGR. Boards press counsel to cap external fees, spurring investment in self-service contract negotiation, e-billing, and matter analytics. Integrated dashboards furnish real-time visibility into workload and cost performance. Government agencies digitize case files and freedom-of-information workflows, though procurement governance can protract buying cycles.

Alternative Legal Service Providers utilize robust technology stacks to deliver fixed-fee document reviews and regulatory gap analyses. Multinational corporate counsel view ALSPs as flexible capacity buffers during peak due diligence periods. Vendor roadmaps are increasingly incorporating APIs to facilitate seamless integration with enterprise resource planning, risk, and compliance environments, thereby ensuring data continuity across corporate functions.

Geography Analysis

The United Kingdom led the Europe legal technology market with a 29.76% share in 2024. London hosts a dense cluster of global law firms and attracts technology pilots through regulator-approved sandboxes (LAW SOCIETY OF ENGLAND AND WALES). Brexit-related divergence drives demand for platforms capable of managing dual regulatory regimes, especially in contract oversight and cross-border litigation support. Historical growth accelerated from an 8.2% CAGR during 2019-2024 to a projected 10.1% through 2030 as firms compete for international mandates.

Germany ranks as the largest continental contributor, driven by its export-oriented manufacturing, automotive, and pharmaceutical sectors, which require sophisticated intellectual property and compliance suites. Federal court digitalization initiatives boost spending on electronic filing and virtual-hearing platforms. France follows with steady uptake among Paris-based international firms, though conservative professional culture and strict data-protection interpretations lengthen implementation cycles.

Nordic countries are expected to register the highest forecast growth at 11.71% CAGR, thanks to their advanced national infrastructure and public-sector digital agendas. Central and Eastern Europe are experiencing a rise in investment as EU convergence encourages the adoption of technology for cross-border mergers and acquisitions (M&A) and regulatory filings. Poland and the Czech Republic lead regional SaaS penetration, supported by European Investment Bank programs. Italy and Spain remain value-conscious markets; however, younger professionals are increasingly advocating for cloud-first tools to enhance client responsiveness. The Netherlands benefits from Amsterdam’s role as a European tech hub, with local vendors exporting AI solutions across the continent.

Competitive Landscape

Competitive dynamics remain moderately fragmented. Relativity, Luminance Technologies, and iManage anchor the eDiscovery and document-management segments, each operating EU data centers certified under ISO 27001. Dozens of emerging vendors target contract lifecycle management and legal analytics niches, offering AI-driven clause extraction, risk scoring, and predictive outcome modeling. Differentiation hinges on natural language processing accuracy across multiple European languages, a visible return on investment, and demonstrable GDPR compliance.

Regional expansion strategies focus on localized hosting and partnerships with bar associations. For instance, Relativity opened facilities in Amsterdam and Frankfurt in 2024 to address data-sovereignty mandates, while iManage integrated Azure AI services to enhance on-platform analytics. Intellectual property-focused platforms, such as Anaqua, expand their European reach by aligning workflows with European Patent Office processes. Competitive white space persists among small and medium-sized law firms, where affordable, user-friendly SaaS solutions remain scarce.

Vendor consolidation is likely as larger providers acquire specialized startups to shorten time-to-market for niche functions. The October 2024 acquisition of LegalMind by ContractPod illustrates this trend. Pricing levers include usage-based billing and modular add-ons that scale with firm growth. Customer stickiness increases when platforms interconnect billing, matter management, and knowledge bases under a single user interface.

Europe Legal Technology Industry Leaders

Relativity ODA LLC

Luminance Technologies Ltd.

iManage LLC

Everlaw Inc.

ContractPod Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The European Commission proposed a EUR 150 million (USD 168 million) extension of its justice AI sandbox fund through 2028, prioritizing projects focused on multilingual regulatory-compliance automation.

- September 2025: iManage inaugurated a Milan data center certified under ISO 27001 and ENS high-level security standards, strengthening in-country hosting options for Italian and Southern European clients.

- June 2025: Luminance deployed portfolio-wide Arabic and Nordic language modules, enabling cross-border due-diligence workflows for firms managing Middle East and Northern Europe transactions.

- March 2025: Relativity acquired French contract-analytics startup PredictaLex for EUR 62 million (USD 69.4 million), expanding multilingual AI capabilities for civil-law jurisdictions.

Europe Legal Technology Market Report Scope

| eDiscovery |

| Contract Lifecycle Management |

| Practice Management |

| Legal Analytics |

| Document Automation |

| Intellectual Property Management |

| Compliance Management |

| Other Solution Type |

| On-Premises |

| Cloud |

| Large Enterprise Law Firms |

| Medium-Sized Law Firms |

| Small Law Firms |

| Law Firms |

| Corporate Legal Departments |

| Government Agencies |

| Alternative Legal Service Providers (ALSPs) |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordic Countries |

| Central and Eastern Europe |

| Rest of Europe |

| By Solution Type | eDiscovery |

| Contract Lifecycle Management | |

| Practice Management | |

| Legal Analytics | |

| Document Automation | |

| Intellectual Property Management | |

| Compliance Management | |

| Other Solution Type | |

| By Deployment Model | On-Premises |

| Cloud | |

| By Firm Size | Large Enterprise Law Firms |

| Medium-Sized Law Firms | |

| Small Law Firms | |

| By End User | Law Firms |

| Corporate Legal Departments | |

| Government Agencies | |

| Alternative Legal Service Providers (ALSPs) | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordic Countries | |

| Central and Eastern Europe | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe legal technology market in 2025?

It is valued at USD 6.17 billion and is projected to grow to USD 10.31 billion by 2030.

Which European country spends the most on legal technology?

The United Kingdom leads with 29.76% market share due to London’s concentration of global law firms and technology pilots.

What solution type accounts for the highest Europe legal technology market share?

EDiscovery holds the top position with 44.87% share in 2024.

Why are corporate legal departments increasing technology budgets?

Boards seek tighter cost control and visibility, prompting in-house teams to deploy integrated contract, compliance, and litigation platforms that reduce external counsel spend.

How is GDPR shaping technology deployment?

Strict privacy enforcement lengthens implementation timelines and drives adoption of privacy-by-design architectures and EU data-center hosting.

What growth rate do small law firms exhibit?

Small practices are expanding technology spend at an 11.17% CAGR through 2030, supported by affordable SaaS models.

Page last updated on: