Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

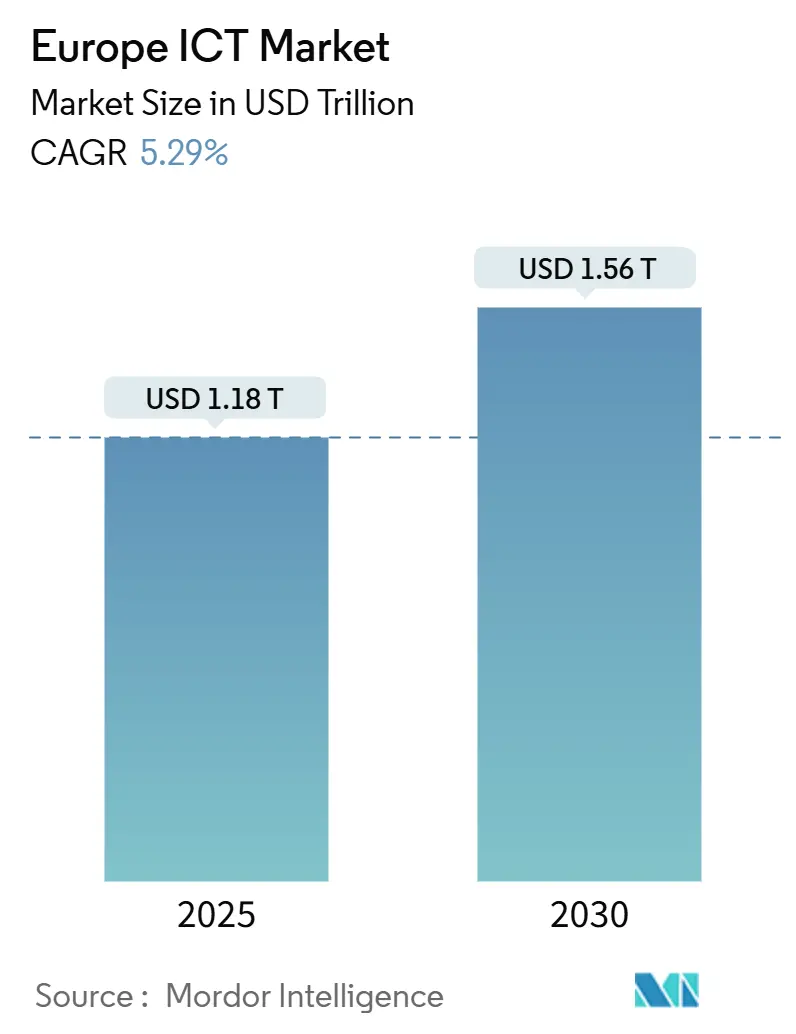

| Market Size (2025) | USD 1.18 Trillion |

| Market Size (2030) | USD 1.56 Trillion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

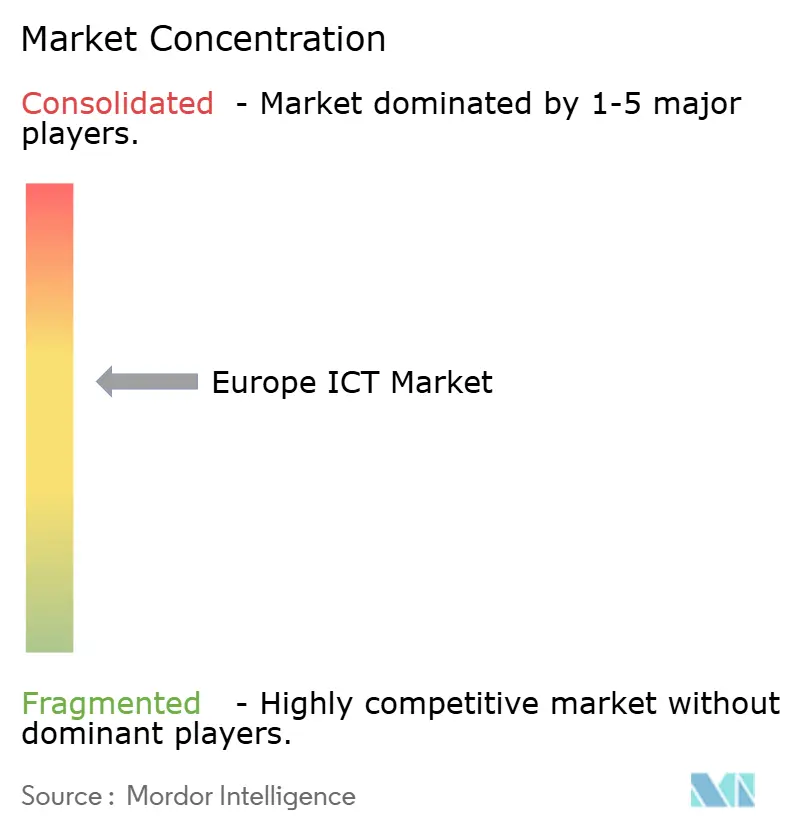

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe ICT Market Analysis by Mordor Intelligence

Europe ICT market currently stands at USD 1.18 trillion in 2025 and is projected to reach USD 1.56 trillion by 2030, implying a 5.29% CAGR for the forecast period. The upward trajectory reflects the European Union’s Digital Decade programme, which funnels EUR 205 billion (USD 222 billion) into digital priorities, including 5G corridors and sovereign cloud capacity. [1]European Commission, “State of the Digital Decade 2024,” eur-lex.europa.eu Heightened regulatory requirements after the Schrems II ruling, stricter energy-efficiency directives for data centers, and sizable corporate investments such as AWS’s EUR 7.8 billion (USD 8.5 billion) sovereign-cloud strategy continue to reshape capital allocation. Momentum also stems from industrial edge-computing pilots that help manufacturers optimise production quality, while EU-wide skills initiatives seek to close a cybersecurity talent gap hovering near 300,000 professionals. [2]OECD, “Building a Skilled Cyber Security Workforce in Europe,” oecd.org However, escalating power tariffs and carbon taxes threaten data-center profitability, and fragmented spectrum allocation continues to dilute 5G economies of scale.

Key Report Takeaways

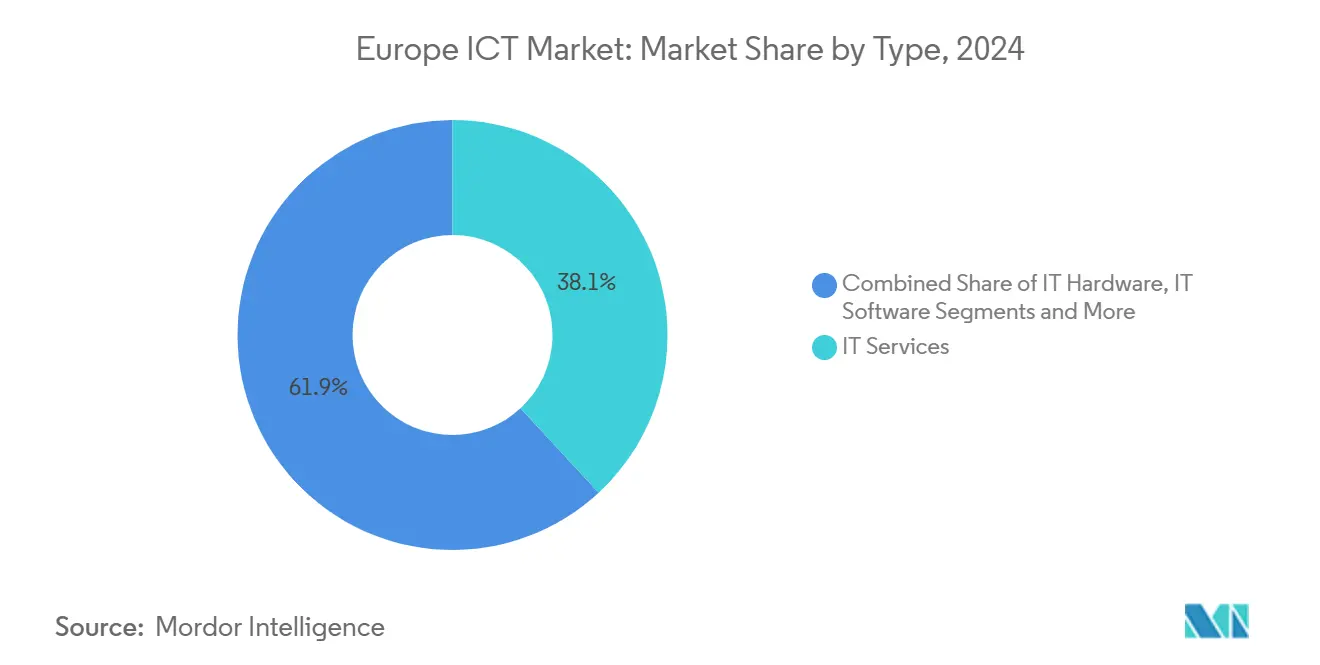

- By type, IT Services led with 38.1% of Europe ICT market share in 2024, whereas IT Security/Cybersecurity is expanding at an 8.3% CAGR through 2030.

- By deployment, on-premise accounted for 55% share of the Europe ICT market size in 2024, yet Public Cloud is advancing at a 9.1% CAGR to 2030.

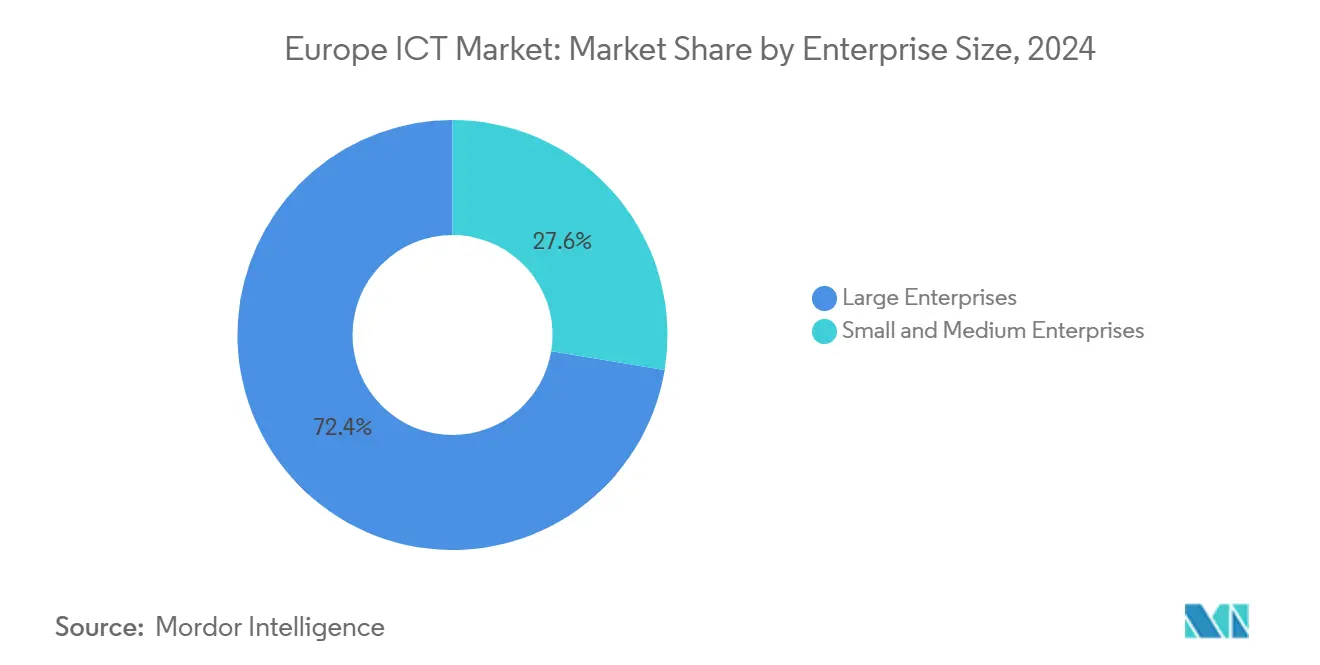

- By enterprise size, Large Enterprises held 72.4% spending in 2024, while SMEs post a stronger 7.9% CAGR up to 2030.

- By industry vertical, BFSI captured 18.2% Europe ICT market share in 2024; Healthcare & Life Sciences is growing at a 6.3% CAGR to 2030.

- By geography, Germany commanded 20.3% of the Europe ICT market size in 2024, whereas Spain is forecast to grow fastest at an 8.7% CAGR.

Europe ICT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EU Digital Decade Funding 2021-2030 Catalyzing Cloud and 5G Roll-outs | +1.2% | EU-wide, strongest in Germany, France, Spain | Medium term (2-4 years) |

| Surge in Sovereign Cloud and Data Residency Requirements Post-Schrems II Ruling | +0.8% | EU-wide, particularly Germany, Netherlands, France | Short term (≤ 2 years) |

| Industrial Edge Computing Demand Driven by Europe's Industry 4.0 Corridors | +0.7% | Germany, Netherlands, Northern Italy, Czech Republic | Medium term (2-4 years) |

| Rising ICT Sustainability Mandates (EU Green Deal) Fueling Green Data Centers | +0.5% | EU-wide, strongest enforcement in Nordic countries, Germany | Long term (≥ 4 years) |

| O-RAN Trials and Early 5G Stand-Alone Deployments Enabling New B2B Services | +0.6% | Germany, UK, Netherlands, Nordic countries | Medium term (2-4 years) |

Source: Mordor Intelligence

Accelerated EU Digital Decade Funding 2021-2030 Catalyzing Cloud & 5G Roll-outs

EU-level grants worth EUR 128 million (USD 139 million) released in December 2024 for 31 new 5G infrastructure projects illustrate how public finance compresses enterprise migration timelines. [3] European Commission, “128 Million in Funding Announced to Advance 5G Connectivity,” digital-strategy.ec.europa.eu These funds target ‘5G for Smart Communities’, linking edge-cloud deployments to use cases such as remote surgery and drone surveillance. The scheme’s focus on cross-border ‘5G Corridor’ routes demands ICT upgrades from logistics firms seeking uninterrupted coverage. Luxembourg’s roadmap sets an 80% digital-skills target and near-universal 5G coverage by 2030, providing a template other member states emulate. Multi-country consortia simplify standards and shorten vendor selection cycles, boosting the Europe ICT market over the medium term.

Surge in Sovereign Cloud and Data Residency Requirements Post-Schrems II Ruling

Oracle’s EU-sovereign cloud regions run solely by EU staff redefine cloud-economics, as compliance-certified workloads now command premium pricing. The prospective EU Cloud Certification Scheme may become compulsory for sectors deemed critical, pushing enterprises toward hybrid architectures. Broadcom’s VMware licensing model faces antitrust scrutiny, underscoring how sovereignty regulations spotlight anti-competitive practices. Meanwhile, the DOME project promotes a distributed marketplace aligning edge and cloud services with EU guidelines, intensifying rivalry among hyperscalers.

Industrial Edge-Computing Demand Driven by Industry 4.0 Corridors

HORIZON EUROPE earmarked EUR 45 million (USD 49 million) for cloud-edge-IoT pilots, reinforcing Germany’s Industry 4.0 leadership. German electrical-industry exports rose 7.1% year-on-year to EUR 21.9 billion (USD 23.7 billion) in March 2025, illustrating payoff from real-time quality control systems. European semiconductor houses look to claim a sizeable portion of a global thick-computing market anticipated to double by 2027. Patent activity, such as Intel’s multi-tenant edge-security filing, signals technical advances that address former adoption hurdles.

Rising ICT Sustainability Mandates Fueling Green Data Centers

The updated Energy Efficiency Directive obliges data centers above 500 kW to publish energy and water metrics annually, driving mergers among smaller operators unable to absorb compliance costs. [4]European Commission, “Commission Adopts EU-Wide Scheme for Rating Sustainability Data Centres,” energy.ec.europa.eu Germany’s Energy Efficiency Act adds renewable-power requirements, accelerating the pivot toward hyperscale sites that negotiate long-term green-energy contracts. The Digital Operational Resilience Act forces banks to marry cyber-security with energy efficiency, nudging workloads into cloud facilities built for sustainability. Data centers already account for nearly 3% of EU electricity demand, making power usage effectiveness a market differentiator.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Intensive Data Centers Facing Escalating Power and Carbon Taxes | -0.6% | Germany, Netherlands, Nordic countries | Short term (≤ 2 years) |

| Persistent Digital Skills Gap Slowing Project Timelines | -0.9% | EU-wide, most acute in Eastern Europe | Medium term (2-4 years) |

| Fragmented Spectrum Policies Hindering 5G Economies of Scale | -0.4% | EU-wide, particularly smaller member states | Medium term (2-4 years) |

| Heightened Cyber-sovereignty Concerns Limiting US Hyperscaler Penetration | -0.6% | EU-wide, strongest in Germany, France | Short term (≤ 2 years) |

Source: Mordor Intelligence

Energy-Intensive Data Centers Facing Escalating Power and Carbon Taxes

Goldman Sachs predicts data-center power demand will rise 160% by 2030, colliding with EU targets to cut energy use 11.7% over the same horizon. German regulations obliging renewable-energy sourcing add complexity that only hyperscale providers can efficiently manage. Ireland and Denmark observe expansion moratoria where grid capacity is constrained, widening the cost gap between compliant and non-compliant sites. Underutilised retrofits remain untapped, leaving structural bottlenecks that cannot be solved by technology alone, tempering Europe ICT market expansion.

Persistent Digital Skills Gap Slowing Project Timelines

Europe lacks nearly 300,000 cybersecurity practitioners, a deficit that lengthens project cycles and inflates wages. ISACA reports 61% of regional organisations run understaffed security teams, while burnout drives attrition. KfW finds 48% of German SMEs rate digitalisation urgent yet struggle to hire talent, delaying deployments. The EU Cybersecurity Skills Academy plans to train 75,000 people through 2027, covering only a quarter of current shortages, implying that execution risk remains embedded in the Europe ICT market outlook.

Segment Analysis

By Type: Services Drive Growth while Security Accelerates

IT Services held 38.1% Europe ICT market share in 2024, reflecting a shift toward managed and outcome-based engagements that absorb regulatory risk for clients. Telefónica Tech exceeded EUR 2 billion (USD 2.2 billion) revenue in FY24 by expanding AI, data, and IoT practices, demonstrating how service lines align with compliance-heavy workloads. IT Security/Cybersecurity is the fastest-growing sub-category, recording an 8.3% CAGR through 2030 as the NIS2 Directive and the Cyber Resilience Act mandate hardened defences. Hardware spending remains steady, supported by Intel’s EUR 53.1 billion (USD 57.5 billion) 2024 sales, yet supply-chain friction caps upside. Software uptake tracks cloud migration; SAP grew 9.5% year-on-year to EUR 34.18 billion (USD 37.0 billion), propelled by ERP modernisation in highly regulated sectors.

Demand for infrastructure services links directly to sovereign-cloud requirements, with Spain’s data-center footprint forecast to multiply sixfold by 2026. Communication Services players migrate to platform models; Deutsche Telekom earned EUR 115.8 billion (USD 125.4 billion) in 2024, 76.3% from outside Germany, underscoring exportable expertise. Patent offices and regulators increasingly deploy AI-enabled software, blurring traditional segment lines but enriching the Europe ICT market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment: Cloud Gains despite Sovereignty Concerns

On-premise solutions still account for 55% of Europe ICT market size in 2024, illustrating enterprise caution in handling sensitive data. Public Cloud, however, grows at 9.1% CAGR to 2030, propelled by AWS’s EUR 7.8 billion (USD 8.5 billion) European sovereign-cloud plan. Certified cloud services narrow the cost differential, making compliance a value driver rather than a hurdle. Hybrid models dominate manufacturing, where edge nodes must meet latency requirements for industrial control.

Private Cloud adoption accelerates as German enterprises balance sovereignty with scalability. Edge Computing, forecast to eclipse USD 155.9 billion globally by 2030, emerges as the third pillar, improving latency for critical applications. The Europe ICT market thus transitions from a two-tier to a three-tier deployment landscape.

By Enterprise Size: SMEs Embrace Cloud-Native Strategies

Large enterprises contributed 72.4% of 2024 spending as they negotiate bulk contracts and operate complex hybrid estates. Their share implies purchasing leverage, but slower growth indicates a mature adoption curve. SMEs, by contrast, are set to expand at 7.9% CAGR, exploiting cloud-native offerings to sidestep capital expenditure. German SMEs invested EUR 31.9 billion (USD 34.5 billion) in 2023 digitalisation despite macro headwinds, signalling market depth.

Skills shortages bite hardest at the SME level, pushing firms toward managed-security and SaaS stacks that externalise expertise. Meanwhile, 45% of EU businesses already consume some form of cloud service, a share expected to climb as budget-friendly compliance solutions proliferate.

By Industry Vertical: BFSI Leads while Healthcare Accelerates

BFSI retained 18.2% Europe ICT market share in 2024, underpinned by roughly 60 digital-only banks in the euro area and fresh Digital Operational Resilience Act requirements. Spending foci include zero-trust architectures and open-banking APIs that deliver incremental revenues from embedded finance offerings.

Healthcare and Life Sciences is the fastest-growing vertical with 6.3% CAGR through 2030. Digital patient records, tele-medicine, and AI-enabled diagnostics deliver efficiency gains evidenced by empirical studies linking digital maturity to health-system performance. Manufacturing continues to fund Industry 4.0 upgrades, while government units pursue ambitious cloud migration paths consistent with Digital Decade milestones.

Geography Analysis

Germany’s leading share stems from sustained investment in automation and edge-enabled workflows that secure export competitiveness. Deutsche Telekom’s multinational revenue mix validates the scalability of German expertise beyond its borders. Nonetheless, energy-price volatility and intricate permitting processes moderate growth velocity. Spain’s expansion owes to strategic submarine-cable links and competitively priced renewable power, positioning the country as a node connecting Europe to Africa and the Americas.

France, Italy, and the Netherlands each pursue differentiated strategies: France prioritises cyber-sovereignty, Italy channels EU funds toward southern connectivity gaps, and the Netherlands banks on physical gateway advantages. Nordic states bundle renewable-energy abundance with digital-government maturity, boosting their share in cloud and AI workloads. Smaller eastern markets accelerate adoption through structural-fund inflows yet continue to wrestle with skills shortfalls and administrative fragmentation that inhibit full-scale digital transformation across the Europe ICT market.

Competitive Landscape

Europe ICT market exhibits moderate fragmentation despite high entry requirements in telecom infrastructure and cloud hyperscale. Telco incumbents—Deutsche Telekom, Orange, Telefónica—retain network dominance, while cloud leadership tilts toward AWS, Microsoft, and Google. EU sovereignty rules, however, give European providers such as OVHcloud and T-Systems an opportunity to differentiate on compliance grounds.

Strategic moves focus on vertical integration and AI-enabled platforms. SAP pivots from ERP to holistic transformation suites, whereas Intel secures foundry financing to rebalance geography-specific production. Digital-only banks capture incremental consumer share, pressuring legacy financial institutions to double down on platform modernisation. Patent activity around multi-tenant edge security and generative-AI workloads underscores innovation intensity. The combined top five players control roughly 45% of addressable spend, placing market concentration at Score 6.

Europe ICT Industry Leaders

-

IBM Corporation

-

Cisco Systems, Inc.

-

Samsung Electronics Co., Ltd

-

Dell Technologies Inc.

-

Fujitsu Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: HPE CEO Antonio Neri stated confidence in closing the USD 14 billion Juniper acquisition after approvals from 14 regulators, including the European Commission, to strengthen an AI-driven edge-to-cloud networking portfolio.

- May 2025: The European Cloud Competition Observatory criticised Broadcom’s VMware licensing framework for potential antitrust violations and urged contract-change notice periods to protect service-provider margins.

- March 2025: Microsoft introduced a telecom-specific data model in Microsoft Fabric, enabling unified analytics for operators, while Nokia announced AI-powered network alliances targeting multi-purpose 5G platforms.

- January 2025: Intel secured a capital infusion via Apollo for operating rights to Fab 34 in Leixlip, Ireland, aligning with its geographically balanced manufacturing model.

Europe ICT Market Report Scope

The study is structured to track the spending on ICT solutions and services by different industry verticals across the European Region.

Europe ICT Market is segmented by type (IT hardware (computer hardware, networking equipment, peripherals), IT software, IT services (managed services, business process services, business consulting services, cloud services), IT infrastructure/data centers (colocation data centers, data center storage, data center servers, data center compute), IT security/ cybersecurity (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security), communication services), by enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT & Telecom, government, retail & e-commerce, manufacturing, energy & utilities, others), by Country (United Kingdom, Germany, France, Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | IT Hardware | Computer Hardware | |

| Networking Equipment | |||

| Peripherals and IoT Devices | |||

| IT Software | System Infrastructure Software | ||

| Application Software | |||

| IT Services | Managed Services | ||

| Business Process Services | |||

| Consulting and Integration Services | |||

| Cloud Services | |||

| IT Infrastructure / Data Centers | Colocation Data Centers | ||

| Hyperscale and Edge Facilities | |||

| Data Center Storage | |||

| Data Center Servers | |||

| Data Center Compute | |||

| IT Security / Cybersecurity | Identity and Access Management | ||

| Network Security Equipment | |||

| Infrastructure Protection | |||

| Cloud Security | |||

| Application and Data Security | |||

| Endpoint Security | |||

| Integrated Risk Management | |||

| Communication Services | Fixed Voice and Data | ||

| Mobile Voice and Data | |||

| Unified Comms and Collaboration | |||

| By Deployment | On-Premise | ||

| Cloud | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Government and Public Sector | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Healthcare and Life Sciences | |||

| Transportation and Logistics | |||

| Other Industry Verticals (Education, Media) | |||

| By Country | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Nordics | |||

| Rest of Europe | |||

By Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals and IoT Devices | |

| IT Software | System Infrastructure Software |

| Application Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Consulting and Integration Services | |

| Cloud Services | |

| IT Infrastructure / Data Centers | Colocation Data Centers |

| Hyperscale and Edge Facilities | |

| Data Center Storage | |

| Data Center Servers | |

| Data Center Compute | |

| IT Security / Cybersecurity | Identity and Access Management |

| Network Security Equipment | |

| Infrastructure Protection | |

| Cloud Security | |

| Application and Data Security | |

| Endpoint Security | |

| Integrated Risk Management | |

| Communication Services | Fixed Voice and Data |

| Mobile Voice and Data | |

| Unified Comms and Collaboration |

By Deployment

| On-Premise |

| Cloud |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By Industry Vertical

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Other Industry Verticals (Education, Media) |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordics |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current Europe ICT market size in 2025?

The Europe ICT market size is USD 1.18 trillion in 2025, on track to reach USD 1.56 trillion by 2030.

Which segment of the Europe ICT market is growing fastest?

IT Security/Cybersecurity is expanding at an 8.3% CAGR through 2030 due to new EU cyber-resilience mandates.

Why does on-premise deployment still dominate the Europe ICT market?

Data-residency and sovereignty rules keep many sensitive workloads in-house, sustaining 55% on-premise share despite public-cloud growth.

How large is the skills gap affecting Europe ICT market growth?

Europe faces a shortage of roughly 300,000 cybersecurity professionals, causing project delays and higher labour costs.

Which country is the fastest-growing geography within the Europe ICT market?

Spain leads with an 8.7% CAGR to 2030 as hyperscalers invest in new data-center capacity.

Page last updated on: June 23, 2025