Europe HBM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

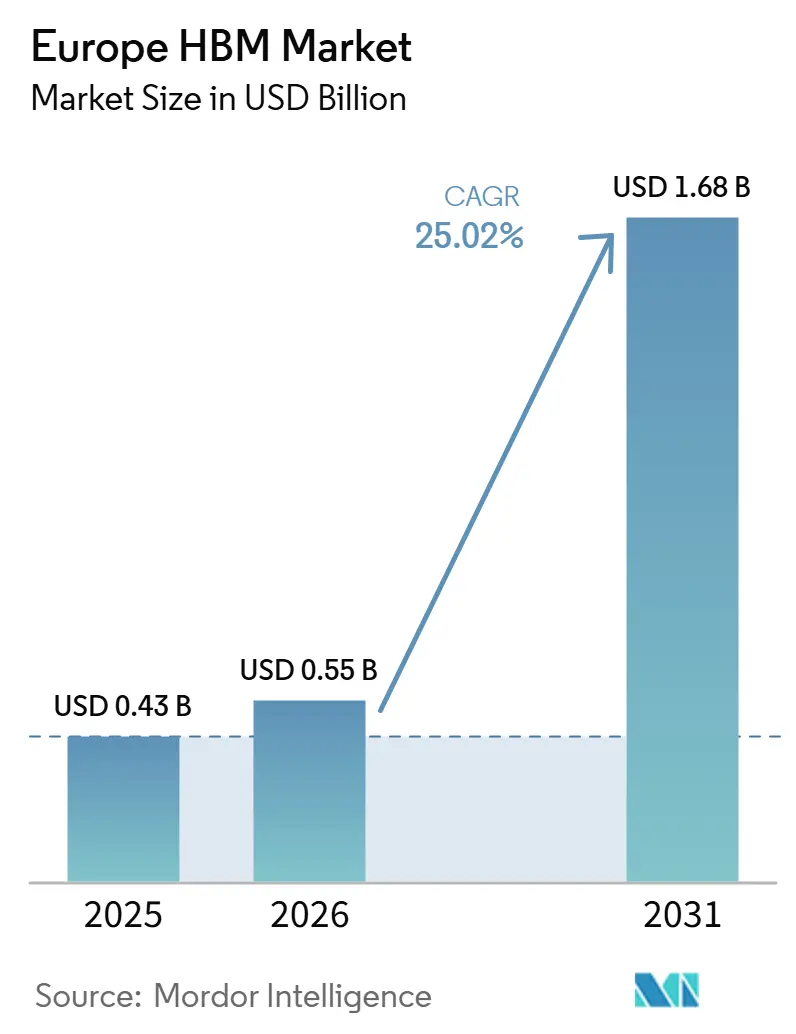

| Base Year Market Size (2025) | USD 0.43 Billion |

| Market Size (2026) | USD 0.55 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 25.02% CAGR |

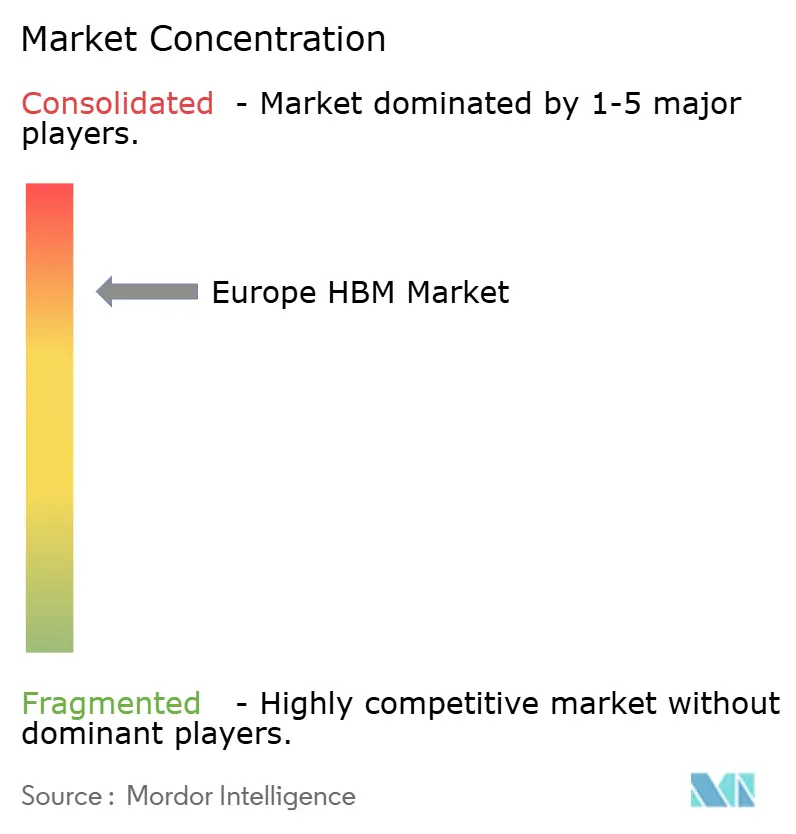

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe HBM Market Analysis by Mordor Intelligence

The Europe HBM market size is projected to be USD 0.43 billion in 2025, USD 0.55 billion in 2026, and reach USD 1.68 billion by 2031, growing at a CAGR of 25.02% from 2026 to 2031. The Europe HBM market is expanding as AI factory deployments are turning memory procurement into a recurring requirement across cloud, research, and sovereign compute programs. The region remains highly exposed to external supply because commercial HBM production is concentrated outside Europe, which keeps buyer dependence high and makes supply availability an important factor for the Europe HBM market. Demand is also becoming broader because the shift from model training toward production inference is raising the need for sustained bandwidth across more deployment settings. Public compute programs, hyperscale expansion, and next-generation automotive compute roadmaps are together widening the addressable base for the Europe HBM market. Competitive activity centers on securing early qualification for new GPU platforms, deepening packaging capabilities, and aligning with system integrators that can translate upstream memory supply into local deployments.

Key Report Takeaways

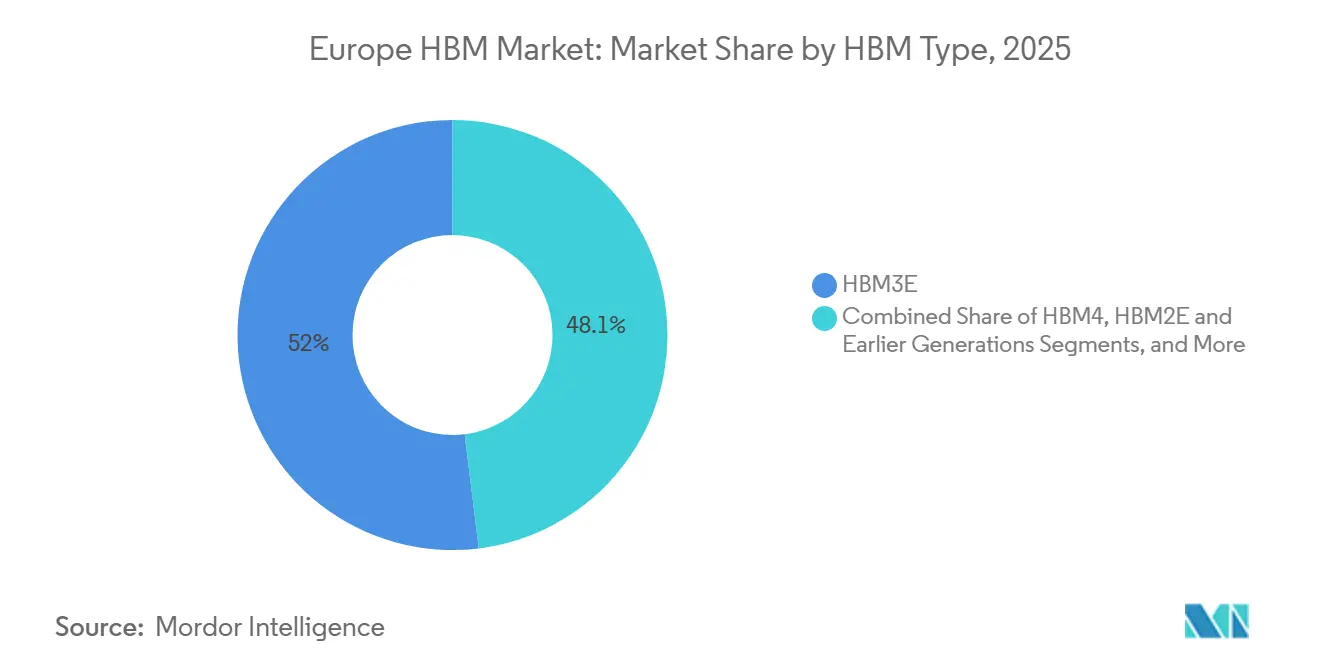

- By HBM type, HBM3E accounted for 51.95% of total market revenue in 2025, while HBM4E and later-generation HBM variants are projected to register the fastest CAGR of 25.94% over 2026-2031.

- By technology node, advanced nodes below 1Z held a 59.13% share of Europe HBM market in 2025, and the same sub-segment is projected to sustain the highest growth pace through 2031 at a CAGR of 25.82%.

- By end-use industry, cloud service providers and hyperscalers held a 43.28% share of the Europe HBM market in 2025, while internet platforms and AI model developers are projected to grow at the fastest CAGR of 26.22% through 2031.

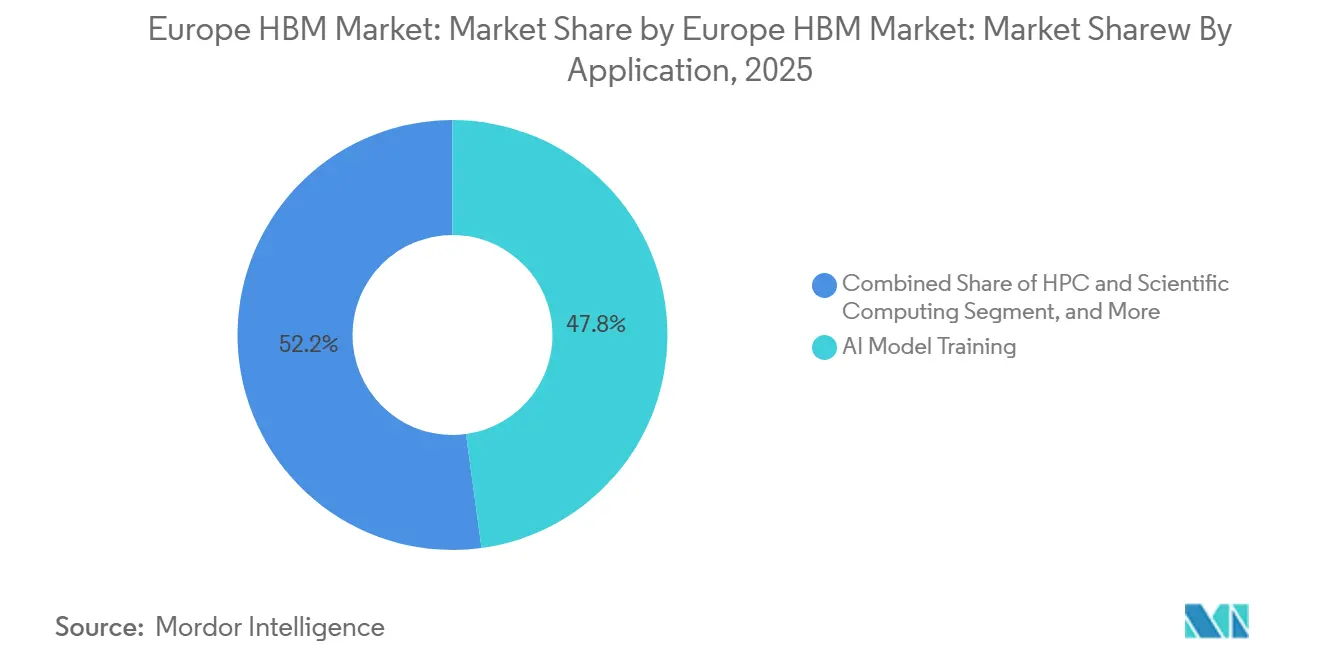

- By application, AI model training accounted for 47.84% of the Europe HBM market in 2025, while AI model inference is projected to be the fastest-growing application, with a CAGR of 26.14% through 2031.

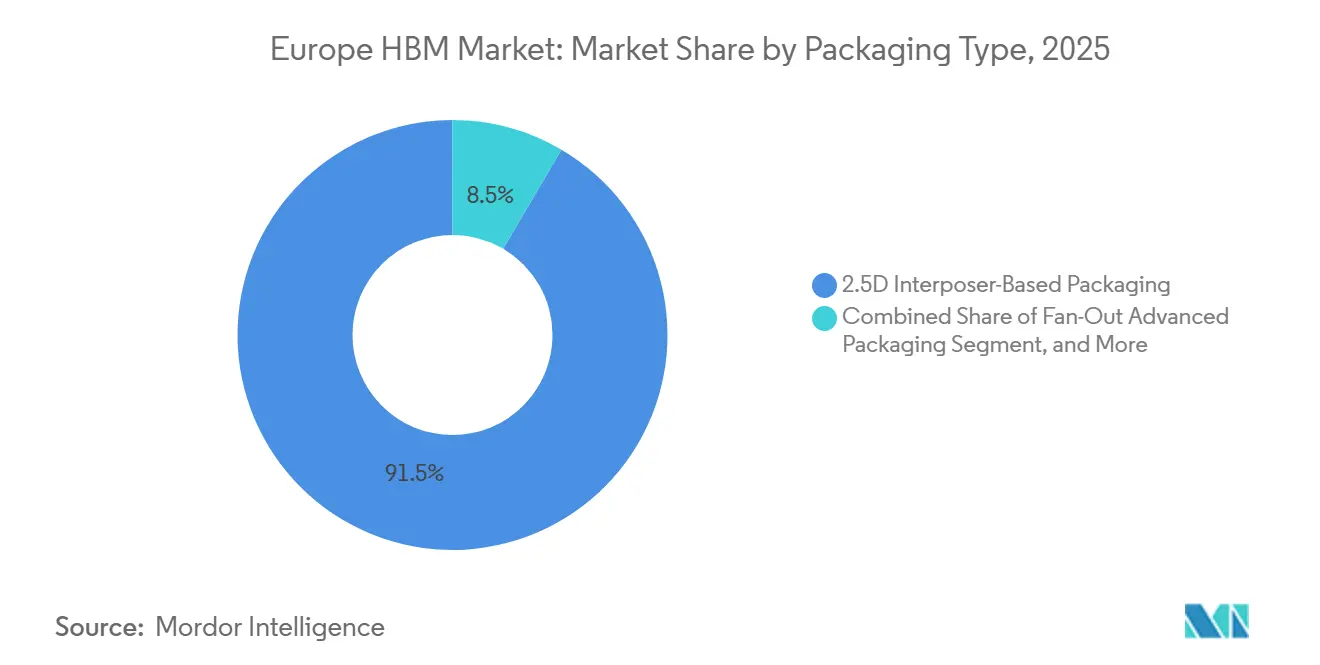

- By packaging type, 2.5D interposer-based packaging held a 91.54% share of the Europe HBM market in 2025, while 3D stacking and hybrid-bonded integration are projected to register the fastest growth at a CAGR of 25.53% through 2031.

- By geography, Germany held a 26.72% share of the Europe HBM market in 2025, while Spain is projected to register the fastest regional CAGR of 26.17% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe HBM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Accelerator Density in European Data Centers | +7.2% | Global, concentrated in Germany, UK, France, Spain, and the Nordics | Short term (≤ 2 years) |

| EuroHPC Sovereign Compute Buildout | +4.8% | Pan-European, with early gains in Germany, France, Italy, and Spain | Medium term (2-4 years) |

| Automotive ADAS and In-Vehicle AI Memory Intensity | +3.5% | Germany, France, Sweden, and the broader EU automotive corridor | Medium term (2-4 years) |

| HBM Adoption in Memory-Bound Scientific Workloads | +2.8% | Germany, France, Finland, Sweden, and Central and Eastern European research hubs | Medium term (2-4 years) |

| Advanced Packaging Pull-Through from European System Integrators | +2.3% | Belgium, Germany, France, and Italy | Long term (≥ 4 years) |

| Specialized Inference Platforms Using On-Package Memory | +3.6% | FLAP-D metros (Frankfurt, London, Amsterdam, Paris, Dublin) and emerging inference edge clusters in Spain and Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Driven Accelerator Density in European Data Centers

The rapid buildout of GPU-heavy infrastructure remains the strongest near-term support for the Europe HBM market because each new AI cluster adds high-bandwidth memory requirements at system scale. NVIDIA said in June 2026 that 35 new AI supercomputers were in development across 23 European countries, with more than 800 AI exaflops deployed or announced in Europe since 2025.[1]NVIDIA Corporation, “Europe Unveils a Record 35 New NVIDIA AI Supercomputers,” NVIDIA Newsroom, nvidianews.nvidia.com That buildout matters for the Europe HBM market because more than 90% of those AI factory deployments were tied to Blackwell and Hopper systems that use HBM as their memory base. The shift from model training to live inference is also widening demand, as production workloads require consistent memory throughput across multiple simultaneous sessions rather than periodic bursts. As that pattern spreads into more national and enterprise deployments, the Europe HBM market is moving from a narrow hyperscaler buying cycle toward a broader and more repeatable procurement base.

EuroHPC Sovereign Compute Buildout

The EuroHPC network is creating a policy-backed demand floor for the Europe HBM market that sits outside the usual commercial cloud spending cycle. EuroHPC moved from isolated flagship systems toward a wider network of AI factories, and that shift is spreading high-bandwidth compute demand across multiple member states. The IT4LIA AI Factory contract signed in April 2026 showed the scale of this demand because the system was built on NVIDIA GB200 NVL4 architecture with more than 8,000 GPUs and over 160 exaflops of peak inference performance. SiPearl’s Rhea1 completed power-on in May 2026, and its design with 4 integrated HBM stacks added a direct European pathway for HBM-enabled sovereign compute. Because these programs are tied to multiyear institutional roadmaps, they give the Europe HBM market a steadier source of demand even when commercial spending becomes less predictable

Specialized Inference Platforms Using On-Package Memory

Specialized inference platforms are becoming an important support for the Europe HBM market because they move HBM demand closer to production services and latency-sensitive deployments. Europe’s AI factory expansion is no longer centered solely on training systems, as newer deployments are now designed to handle large-scale inference as well. That change favors on-package memory since long-context and multi-user inference loads need fast access to large working sets. The result is a wider spread of HBM demand across metropolitan cloud regions, sovereign compute sites, and enterprise edge environments that are deploying AI services closer to the user base. As those deployments scale, the Europe HBM market benefits from a more diversified application mix rather than relying on a small number of very large training clusters.

Automotive ADAS and In-Vehicle AI Memory Intensity

Automotive compute is becoming a longer-cycle support for the Europe HBM market because future central compute platforms are being designed around higher bandwidth needs. The implications for Europe are important because local vehicle and supplier programs are moving from distributed electronics toward centralized, AI-heavy architectures. The Europe HBM market is therefore gaining a second source of structural demand that is tied to vehicle roadmaps rather than only data center investment. Bosch’s role in the European Automotive Base Die program also points to future chiplet designs aligned with higher-bandwidth interfaces in the region’s automotive corridor. As those programs mature, the Europe HBM market is likely to deepen its connection with Europe’s semiconductor and vehicle design base even before large-scale in-vehicle volumes fully arrive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Indigenous HBM Supply Base in Europe | -3.8% | Pan-European, particularly affecting Germany, France, and Southern Europe | Short term (≤ 2 years) |

| Advanced Packaging Capacity Concentration Outside Europe | -2.6% | Global supply risk, with concentrated impact in Western Europe | Medium term (2-4 years) |

| High Thermal and Power-Delivery Complexity at Scale | -1.7% | FLAP-D metros and energy-constrained Southern European markets | Medium term (2-4 years) |

| Long Qualification Cycles for Automotive and Industrial Platforms | -1.5% | Germany, France, Sweden, and the Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Indigenous HBM Supply Base in Europe

The biggest structural limit on the Europe HBM market is that the region still lacks local HBM fabrication at a commercial scale. That gap means European demand growth does not automatically translate into local value capture, because supply still depends on producers outside the region. The Europe HBM market, therefore, remains exposed to external allocation priorities, supplier qualification cycles, and packaging bottlenecks that European buyers do not directly control. The EU Chips Act has strengthened the broader semiconductor agenda, but the projects highlighted in the current pipeline are focused more on logic and power semiconductors than on HBM capacity itself. Until that gap narrows, the Europe HBM market will remain sensitive to upstream decisions in other regions, even as local AI infrastructure demand remains strong.

Advanced Packaging Capacity Concentration Outside Europe

The Europe HBM market also faces a second constraint: the advanced packaging required for HBM integration remains concentrated outside Europe. That matters because HBM demand depends not only on memory fabrication, but also on high-yield integration with GPUs and accelerators. Imec’s work in hybrid bonding and NanoIC process design kits shows that Europe has meaningful process research capability, yet those advances have not been translated into regional high-volume packaging capacity. Thermal and integration complexity further slow this transition because 3D approaches need tighter system-level control than the mature 2.5D baseline. As a result, the Europe HBM market remains dependent on external packaging ecosystems, even as local research institutions help define the next technical roadmap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Type: HBM3E Leads Deployments as HBM4E Builds Pipeline

HBM3E held 51.95% of the Europe HBM market by revenue in 2025, reflecting its role as the standard memory configuration on the AI accelerator platforms most widely deployed across the region. The installed base built around Hopper and early Blackwell systems keeps HBM3E central to current procurement because these platforms continue to anchor many cloud, research, and sovereign deployments. The Europe HBM market also shows that platform continuity matters, because existing HBM3E-based systems will remain active even as the next generation starts to scale. Samsung said in May 2026 that it shipped HBM4E samples to NVIDIA ahead of schedule, with specifications of up to 16 Gbps per pin, 48 GB capacity, and up to 3.6 TB/s per stack. NVIDIA’s confirmation of the Vera Rubin platform's production start in June 2026 reinforces that the market is already preparing for the HBM4 transition.[2]Samsung Semiconductor, “Samsung Unveils HBM4E, Showcasing Comprehensive AI Solutions, NVIDIA Partnership and Vision at NVIDIA GTC 2026,” Samsung Semiconductor, semiconductor.samsung.com

HBM4E and later variants are projected to record the fastest CAGR of 25.94% through 2031, indicating how quickly the demand mix is shifting toward the next performance tier. This part of the Europe HBM market is not only about a speed upgrade; the move also changes integration requirements due to new base-die and packaging expectations. Samsung’s early HBM4E sampling and the NVIDIA roadmap both suggest that qualification timing will play a major role in supplier positioning. Older generations such as HBM2E and HBM3, as well as legacy deployments, still have a place in academic, institutional, and earlier AI clusters, but they are no longer setting the direction of the Europe HBM market. The segment, therefore, reflects a layered adoption curve where current volume remains concentrated in HBM3E, while future growth is already defined by HBM4E readiness.

By Technology Node: Advanced Sub-1Z Nodes Concentrate HBM Demand

Advanced nodes below 1Z held 59.13% of the Europe HBM market in 2025, and this tier also represented the leading edge of new HBM deployment. That concentration shows that European procurement is closely aligned with the most advanced memory processes required to meet bandwidth density and power efficiency targets in modern AI systems. The Europe HBM market is therefore not spreading evenly across process generations, because the demand profile strongly favors memory built for the newest accelerator platforms. Supplier roadmaps from Samsung and SK Hynix indicate that the transition from HBM3E toward HBM4 is tied to continued migration into more advanced process classes. As a result, the share of advanced nodes within the Europe HBM market is likely to keep rising as new AI system generations move into production.

The 1Z tier remains relevant for HBM3 deployments that continue to serve institutions and operators that are not yet refreshing to HBM3E or HBM4-based configurations. Earlier nodes, such as 1Y and 1X, are increasingly tied to legacy HBM programs and older HPC installations rather than new mainstream deployment cycles. This creates a process-layer winner-takes-most pattern in the Europe HBM market, because each successful node migration increases the commercial gap with prior generations. Standards work around HBM interoperability helps reduce the risk of complete lock-in for system integrators, yet it does not change the fact that commercial demand is clustering around the most advanced manufacturing nodes. The segment therefore shows that process leadership is becoming one of the clearest structural filters for participation in the Europe HBM market.

By Packaging Type: 2.5D Interposer Dominates with Hybrid Bonding Emerging

2.5D interposer-based packaging accounted for 91.54% of the Europe HBM market in 2025, making it the clear standard for integrating HBM with GPUs and accelerators. In the Europe HBM market share structure by packaging, that 91.54% level showed how strongly procurement was tied to the mature CoWoS and silicon interposer ecosystem. The dominance of 2.5D matters because it effectively sets the practical integration baseline for many European system buyers and designers. The Europe HBM market has therefore been shaped not only by memory supply, but also by the availability of a proven packaging route with acceptable yield and thermal behavior. IMEC’s thermal work also reinforced the current advantage of 2.5D, as uncontrolled 3D stacking poses significantly higher temperature challenges than the established baseline.

3D stacking and hybrid-bonded integration are projected to record the fastest CAGR of 25.53% through 2031, indicating where packaging innovation is moving, even though the current volume remains concentrated elsewhere. Imec and EV Group demonstrated wafer-to-wafer hybrid bonding at a 200 nm copper interconnect pitch, achieving record overlay accuracy in 2026, demonstrating that Europe has advanced research capabilities in this area. NanoIC’s release of fine-pitch RDL and D2W hybrid bonding process design kits also gave startups and universities access to next-generation interconnect development tools. Fan-out advanced packaging remains the smallest packaging tier, serving more specialized uses where form factor and cost are more important than absolute bandwidth. The segment shows that the Europe HBM industry is still built on a very concentrated 2.5D foundation, while future differentiation is likely to come from how quickly new 3D approaches can overcome thermal and manufacturing limits.

By End Use Industry: Hyperscalers Command Share as AI Developers Scale Fastest

Cloud service providers and hyperscalers held 43.28% of the Europe HBM market in 2025, confirming that capital-intensive cloud infrastructure remained the main revenue anchor. Large regional cloud commitments, AI factory deployments, and rising rack density continue to give this buyer group the strongest purchasing influence in the current market. The Europe HBM market also shows a clear split between revenue leadership and growth leadership, as the fastest expansion is moving toward internet platforms and AI model developers rather than remaining with the largest cloud operators. That fast-growing segment is projected to advance at a 26.22% CAGR through 2031 as inference-oriented services, retrieval-augmented generation architectures, and proprietary model platforms scale across European cloud regions. The growth pattern suggests that the Europe HBM market is broadening from infrastructure ownership toward infrastructure use cases that depend on sustained high-bandwidth access.

Government, defense, research, and academic institutions remain a distinct buyer category because many of their purchases are connected to national or EuroHPC frameworks rather than pure commercial demand cycles. Enterprise data centers are also moving deeper into GPU-based inference, gradually shifting them from indirect buyers to more visible contributors to the Europe HBM market. Telecommunications operators constitute a smaller segment, but their role is technically important because network optimization and edge AI use cases can require on-package memory performance that conventional DRAM cannot deliver at a similar latency. The Europe HBM industry is therefore becoming more diverse at the customer level, even though hyperscalers still set the baseline for spending scale. This combination of concentrated revenue and expanding use cases gives the Europe HBM market a stronger long-term demand base than a single-buyer model would.

By Application: AI Training Drives Volume While Inference Accelerates Growth

AI model training accounted for 47.84% of the Europe HBM market in 2025, reflecting the concentration of HBM procurement within large GPU-dense clusters. That volume leadership came from training-heavy AI factories, flagship supercomputers, and large institutional systems where memory demand is created in very large procurement blocks. In the Europe HBM market, the size mix by application showed that AI training held the largest share because very large compute installations were still the primary sites of memory deployment in 2025. The Europe HBM market also benefited from scientific systems that blend classical HPC and AI tasks, which raised the importance of HBM beyond purely commercial data centers. SiPearl’s Rhea1 added to this pattern because its integrated HBM design showed that high-bandwidth memory is becoming relevant at the CPU layer as well.

AI model inference is projected to be the fastest-growing application, with a 26.14% CAGR through 2031, indicating that demand is shifting from building models to serving them at scale. This matters for the Europe HBM market because inference is spreading into sovereign cloud, enterprise, telecom, and metropolitan deployments rather than remaining limited to a few giant clusters. Long-context models and concurrent session loads increase working-set requirements, strengthening the case for HBM in production inference environments. HPC, professional graphics, rendering, and network processing remain smaller application categories, but together they provide a durable secondary base for the Europe HBM market. The segment, therefore, points to a market where training still drives current volume while inference is shaping the next stage of expansion.

Geography Analysis

Germany held 26.72% of the Europe HBM market in 2025, giving it the largest country share in the region. In the Europe HBM market, the size pattern by geography reflected Germany’s lead, driven by AI data centers, supercomputing assets, and automotive semiconductor activity. The concentration of demand around Frankfurt, Jülich, Stuttgart, Bavaria, and Silicon Saxony strengthens the country’s position. The UK and France formed the next important tier because both markets combine hyperscale expansion with institutional compute programs. France also gained support from the Alice Recoque exascale system and broader sovereign AI activity, which keeps its demand base visible through the forecast period.

Spain is projected to post the fastest regional CAGR of 26.17% through 2031, making it the standout growth story in the Europe HBM market. Amazon said in March 2026 that it would invest significantly in Spain’s Aragón cloud region, including dedicated AI and machine learning server manufacturing facilities. That level of investment is increasing Spain’s role from a data center destination toward a broader AI infrastructure node. The Barcelona ecosystem also matters because it connects cloud expansion with high-performance compute and local semiconductor design activity. Italy is another meaningful market because the IT4LIA AI Factory in Bologna adds a major sovereign compute deployment that directly supports the Europe HBM market.

The Nordics are moving into a stronger position as renewable energy economics and subsea connectivity continue to attract hyperscale and AI training investments.[3]European Data Centre Association, “State of European Data Centres 2026,” European Data Centre Association, eudca.org EUDCA data showing projected colocation IT power above 4.4 GW by 2031 supports the view that Nordic capacity growth will create recurring procurement cycles for the Europe HBM market. Central and Eastern European countries within the rest of Europe grouping are also gaining relevance as operators diversify geography and expand sovereign workload placement. The result is a regional map where the Europe HBM market still has a clear core in Germany, the UK, France, Spain, and Italy, but is gradually widening into a broader network of compute locations across the continent.

Competitive Landscape

The Europe HBM market is highly concentrated at the supply level, as Samsung Electronics, SK Hynix, and Micron collectively account for nearly all commercial HBM production capacity. That structure gives upstream suppliers strong influence over qualification timing, product availability, and platform alignment across the Europe HBM market. SK Hynix has maintained a strong competitive position in the HBM3E cycle, while Samsung is pursuing a more integrated strategy that combines memory design, foundry capabilities, and packaging for the HBM4 transition. NVIDIA and SK Hynix formalized a multiyear technology partnership in June 2026, underscoring how deeply HBM supplier strategy is now tied to accelerator roadmaps.[4]NVIDIA Corporation, “NVIDIA and SK hynix Announce Multiyear Technology Partnership to Advance Memory for AI Factories,” NVIDIA Investor Relations, investor.nvidia.com

Samsung made another visible strategic move when it shipped HBM4E samples to NVIDIA ahead of its previously communicated schedule, using early sampling to strengthen qualification momentum for the next platform cycle. Micron is pursuing a different route by expanding advanced packaging capacity in Singapore, which supports its HBM4 volume ambitions and gives buyers another geopolitical supply option over time. On the European demand side, competition is less about making HBM and more about securing access to HBM-bearing systems. System integrators such as Eviden, HPE, Dell Technologies, and E4 Computer Engineering are important because they convert upstream memory supply into deployable AI and HPC infrastructure for regional buyers.

Emerging European chip designers are also shaping the Europe HBM market by building high-bandwidth memory into their product roadmaps rather than treating it as a niche feature. SiPearl is the clearest example because Rhea1 combines a European CPU design with 4 integrated HBM stacks for sovereign supercomputing use cases. Research institutions remain strategically important as well, because imec’s work in hybrid bonding and NanoIC process development is helping define the technical path for next-generation HBM integration. This means the Europe HBM market is concentrated in supply, fragmented in demand, and increasingly shaped by partnerships that link memory makers, accelerator vendors, system integrators, and European compute programs.

Europe HBM Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK Hynix announced a multi-year technology partnership to co-develop next-generation HBM memory for AI factories, including memory for the Vera Rubin supercomputer, Vera CPUs, and Jetson Thor robotic computing platforms. The partnership also covers applying AI to semiconductor fabrication using NVIDIA CUDA-X libraries and NVIDIA PhysicsNeMo tools for fab digital twins at SK Hynix's facilities.

- June 2026: NVIDIA unveiled 35 new AI supercomputers across 23 European countries, with over 800 AI exaflops of Blackwell and Hopper infrastructure deployed or announced in Europe since 2025, powering over 90% of the continent's AI factory buildout. Confirmed deployments include the Leibniz Supercomputing Centre in Germany and multiple EuroHPC AI factory sites running NVIDIA GB200 NVL4 and GB300 NVL72 configurations.

- June 2026: IMEC and EV Group presented wafer-to-wafer hybrid bonding at a 200 nm copper pad pitch with sub-40 nm overlay accuracy at the 2026 IEEE ECTC (May 28, 2026, Leuven), advancing the European roadmap for logic-to-memory 3D stacking toward an interconnect pitch below 200 nm.

- June 2026: SK hynix showcased its AI memory portfolio at HPE Discover (HPED) 2026, presenting certified HBM products deployed in HPE servers alongside its CXL2 Memory Module-DDR5, reinforcing its positioning as a full-stack AI memory creator for European AI infrastructure partners.

Europe HBM Market Report Scope

The Europe HBM Market Report is Segmented by HBM Type (HBM2E and Earlier Generations, HBM3, HBM3E, HBM4, HBM4E and Later-Generation HBM), Technology Node (1X And Above Legacy Nodes, 1Y Node, 1Z Node, Advanced Nodes Below 1Z), End Use Industry (Cloud Service Providers and Hyperscalers, Internet Platforms and AI Model Developers, Government, Defense, Research, and Academic Institutions, Enterprise Data Centers, Telecommunications Operators and Network Equipment Providers, Other Enterprise Verticals), Application (AI Model Training, AI Model Inference, HPC and Scientific Computing, Professional Graphics, Rendering, and Visualization, Network and Telecom Processing, Other High-Bandwidth Compute Workloads), Packaging (2.5D Interposer-Based Packaging, 3D Stacking, Fan-Out Advanced Packaging), and Geography (Germany, United Kingdom, France, Italy, Spain, Nordics, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E and Earlier Generations |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E |

| 1X And Above Legacy Nodes |

| 1Y Node |

| 1Z Node |

| Advanced Nodes Below 1Z |

| 2.5D Interposer-Based Packaging |

| 3D Stacking |

| Fan-Out Advanced Packaging |

| Cloud Service Providers and Hyperscalers |

| Internet Platforms and AI Model Developers |

| Government, Defense, Research, and Academic Institutions |

| Enterprise Data Centers |

| Telecommunications Operators and Network Equipment Providers |

| Other Enterprise Verticals |

| AI Model Training |

| AI Model Inference |

| HPC and Scientific Computing |

| Professional Graphics, Rendering, and Visualization |

| Network and Telecom Processing |

| Other High-Bandwidth Compute Workloads |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Nordics |

| Rest of Europe |

| By HBM Type | HBM2E and Earlier Generations |

| HBM3 | |

| HBM3E | |

| HBM4 | |

| HBM4E | |

| By Technology Node | 1X And Above Legacy Nodes |

| 1Y Node | |

| 1Z Node | |

| Advanced Nodes Below 1Z | |

| By Packaging Type | 2.5D Interposer-Based Packaging |

| 3D Stacking | |

| Fan-Out Advanced Packaging | |

| By End Use Industry | Cloud Service Providers and Hyperscalers |

| Internet Platforms and AI Model Developers | |

| Government, Defense, Research, and Academic Institutions | |

| Enterprise Data Centers | |

| Telecommunications Operators and Network Equipment Providers | |

| Other Enterprise Verticals | |

| By Application | AI Model Training |

| AI Model Inference | |

| HPC and Scientific Computing | |

| Professional Graphics, Rendering, and Visualization | |

| Network and Telecom Processing | |

| Other High-Bandwidth Compute Workloads | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current and forecast value of the Europe HBM market?

The Europe HBM market was valued at USD 0.43 billion in 2025, reached USD 0.55 billion in 2026, and is projected to reach USD 1.68 billion by 2031 at a 25.02% CAGR.

Which HBM type leads Europe today?

HBM3E led in 2025 with 51.95% of total revenue because it was the core memory configuration for the accelerator platforms most widely deployed across Europe.

Which end use segment is expanding the fastest in Europe?

Internet platforms and AI model developers are projected to post the fastest CAGR at 26.22% through 2031 as inference services and proprietary model deployments scale.

Why is Germany the largest country in this space?

Germany led with 26.72% share in 2025 because it combines hyperscale data center activity, major supercomputing sites, and a strong automotive semiconductor base.

Why does 2.5D interposer packaging dominate current deployments?

2.5D interposer-based packaging held 91.54% share in 2025 because it remains the most mature and widely qualified route for integrating HBM with GPUs and accelerators.

What is the biggest structural risk for growth in Europe?

The main risk is Europe's lack of indigenous HBM fabrication and limited local advanced packaging capacity, which keeps buyers dependent on external supply chains.

Page last updated on: