Europe Fixed Broadband Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

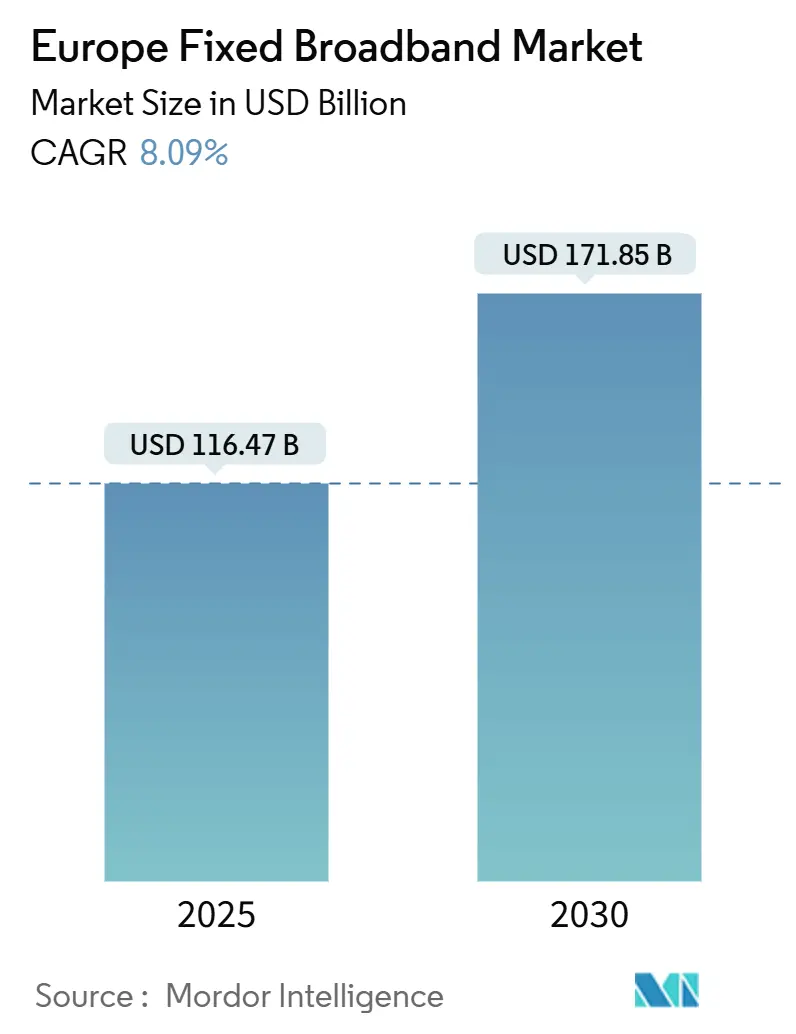

| Market Size (2025) | USD 116.47 Billion |

| Market Size (2030) | USD 171.85 Billion |

| Growth Rate (2025 - 2030) | 8.09% CAGR |

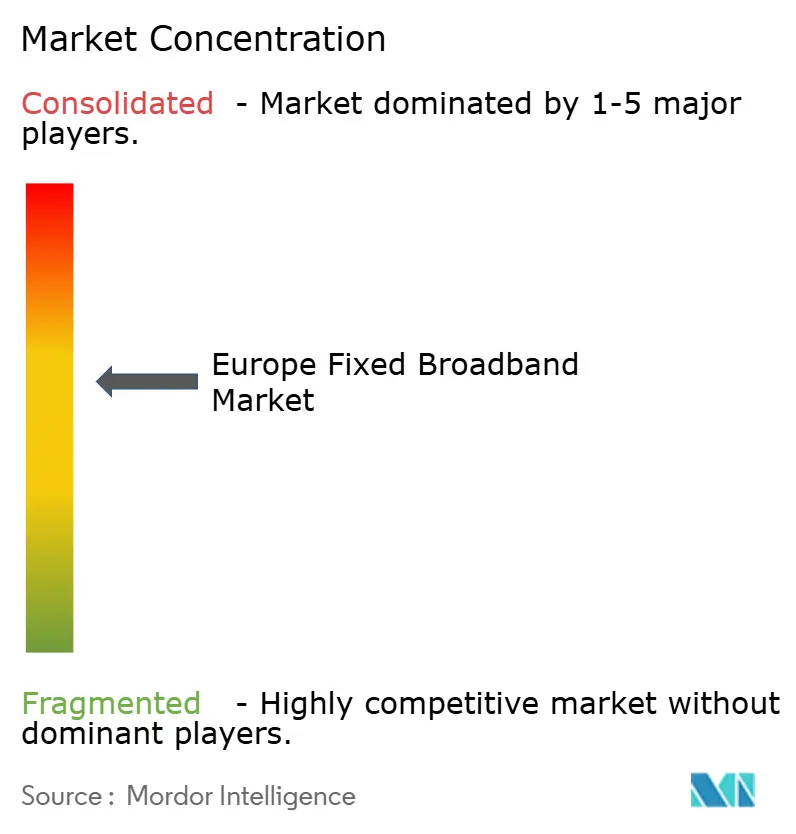

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fixed Broadband Market Analysis by Mordor Intelligence

The European fixed Broadband Market size is estimated at USD 116.47 billion in 2025, and is expected to reach USD 171.85 billion by 2030, at a CAGR of 8.09% during the forecast period (2025-2030). Demand surges because the EU Gigabit Society targets mandate universal gigabit coverage, operators accelerate copper-to-fiber migration, and recovery funds earmark EUR 13 billion for connectivity. Operators gain pricing power from premium multi-gig packages while energy-efficient fiber lowers OPEX, improving margins despite rising electricity costs. Cable MSOs continue to monetize their extensive DOCSIS footprints, while strategic investor attention shifts toward fiber wholesale platforms that promise future-proof, symmetric speeds. Competitive intensity increases as fixed-wireless and satellite entrants fill rural gaps, and edge data-center projects amplify last-mile gigabit requirements across industrial zones.

Key Report Takeaways

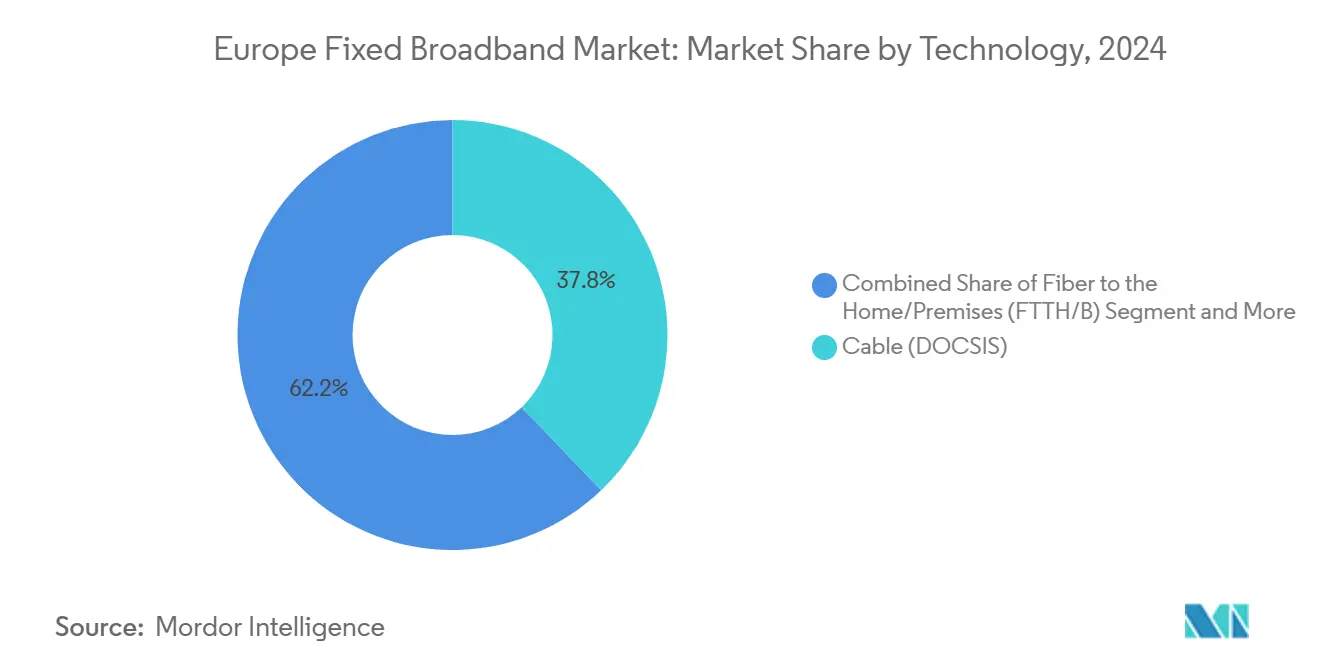

- By technology, cable DOCSIS commanded 37.84% of the European fixed broadband market share in 2024, while FTTH/B recorded the fastest CAGR of 15.66% through 2030.

- By speed tier, the 100 Mbps-1 Gbps segment accounted for 65.35% of the European fixed broadband market size in 2024, while services above 1 Gbps are projected to advance at a 15.22% CAGR through 2030.

- By end user, residential connections held an 84.50% value share in the European fixed broadband market in 2024, whereas the commercial lines segment registered the highest segmental CAGR at 9.75% through 2030.

- By application, video streaming and entertainment accounted for 65.01% of the revenue in the European fixed broadband market in 2024; online gaming and immersive media are projected to grow at a 15.14% CAGR to 2030.

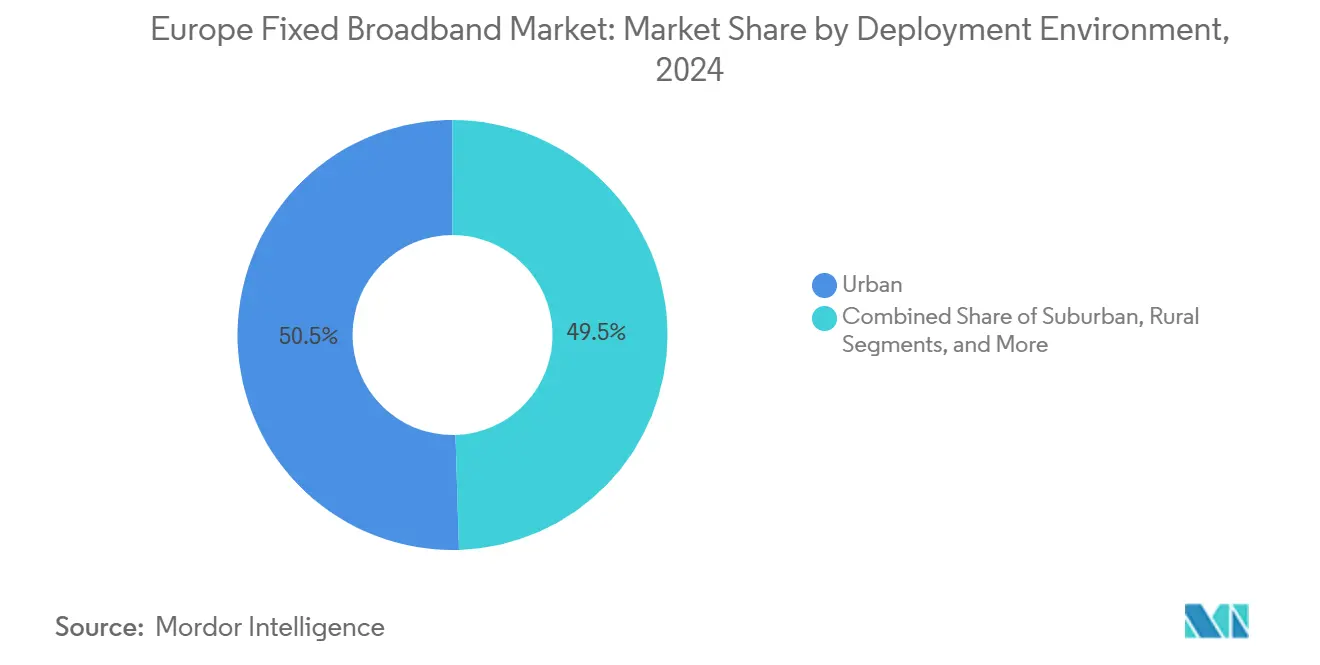

- By deployment environment, urban areas captured 50.49% value share of the European fixed broadband market in 2024, while suburban build-outs expanded at 8.93% CAGR to 2030.

- By ownership, cable multiple system operators (MSOs) captured a 34.22% value share in the European fixed broadband market in 2024, while fixed wireless ISPs' build-outs expanded at a 11.15% CAGR to 2030.

- By country, Germany generated a 35.96% share in the European fixed broadband market in 2024, while Spain is forecast to grow at a 11.54% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Europe includes both locally based firms and those operating across multiple regions. The market landscape in the global fixed broadband industry research shows how these players are arranged internationally.

Europe Fixed Broadband Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiber Network Expansion Driven by EU Gigabit Society targets | +2.1% | EU-wide with emphasis on Germany, France, Spain | Medium term (2-4 years) |

| Government Subsidies and RRF Accelerating Rural Broadband Roll-outs | +1.8% | Rural districts across EU, Eastern Europe strongest | Long term (≥ 4 years) |

| Rising Household Demand for 4K/8K Streaming and Cloud Gaming | +1.5% | Urban and suburban zones, Nordic and Western Europe | Short term (≤ 2 years) |

| Persistent Remote/Hybrid Work Models Sustaining High Bandwidth Demand | +1.3% | Metropolitan corridors in UK, Netherlands, Germany | Medium term (2-4 years) |

| Emergence of Open-access Wholesale Fiber Models Attracting Alternative Capital | +0.9% | UK, Italy, Spain | Long term (≥ 4 years) |

| Edge Data Center Densification Requiring Last-mile Gigabit Connectivity | +0.7% | Major cities and industrial parks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fiber Network Expansion Driven by EU Gigabit Society Targets

The EU Gigabit Infrastructure Act mandates universal gigabit connectivity by 2030, accelerating fiber deployment beyond market-driven timelines. Member states must ensure 100% fiber coverage in populated areas and gigabit access for all socio-economic groups, making infrastructure investment mandatory. This framework enables operators to secure long-term financing for FTTH projects with guaranteed visibility of demand. Co-investment provisions allow operators to share deployment costs, reducing CAPEX and expediting rollouts. Germany's Deutsche Telekom committed EUR 6 billion to expand fiber to 10 million additional premises by 2025, while France's Orange allocated EUR 3.5 billion for similar initiatives. The Act's focus on symmetric speeds gives fiber providers a competitive edge over cable networks, which are constrained by upload bandwidth.

Government Subsidies and RRF Accelerating Rural Broadband Roll

The Recovery and Resilience Facility has allocated EUR 13.4 billion for digital connectivity projects, with a particular focus on rural broadband to bridge the digital divide. This historic investment enables rural deployments through subsidies and state aid. Italy's Open Fiber secured EUR 3.7 billion in government funding to deploy rural fiber to 6.9 million premises in commercially unviable areas. The funding mandates open-access wholesale models to prevent duplication and ensure competitive retail markets. Spain aims to achieve 100% rural fiber coverage by 2025, supported by EUR 2.1 billion in EU and national funding. These subsidies are transforming rural markets, creating growth opportunities for alternative fiber providers.

Rising Household Demand for 4K/8K Streaming and Cloud Gaming

Netflix's expansion of 4K content libraries and the rise of 8K streaming services are driving bandwidth demands beyond traditional broadband limits, with 4K requiring 25 Mbps and 8K exceeding 100 Mbps per session. Cloud gaming platforms, such as NVIDIA GeForce Now and Xbox Cloud Gaming, require ultra-low latency of under 20ms, which is achievable only through fiber networks with edge computing. European households, averaging 3.2 connected devices per person, face peak bandwidth demands exceeding 200 Mbps due to the simultaneous use of 4K streaming, video conferencing, and gaming. [1]NVIDIA, “GeForce Now Technical Requirements 2024,” nvidia.com The growing adoption of the PlayStation 5 and Xbox Series X in Europe boosts cloud gaming subscriptions, with Microsoft reporting 25 million Game Pass Ultimate subscribers globally, many of whom rely on fiber-grade connectivity. This shift makes multi-gig services essential, accelerating the transition from cable to fiber networks.

Persistent Remote/Hybrid Work Models Sustaining Bandwidth Demand

Following the pandemic, 42% of European knowledge workers work remotely at least three days a week, sustaining residential bandwidth demand that was previously centered in commercial hubs. [2]Eurostat, “Labour Force Survey 2024,” ec.europa.eu Platforms like Microsoft Teams and Zoom require symmetric upload speeds for HD video, favoring fiber over cable's asymmetric bandwidth. Home offices require enterprise-grade reliability for cloud applications, VPNs, and collaboration tools, which can strain networks during business hours. This shift drives demand for commercial-grade residential services, with BT Business reporting a 35% rise in premium home office connectivity packages. The permanence of remote work stabilizes bandwidth demand, justifying investments in fiber and multi-gig service tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for FTTH in Low-density Areas | -1.4% | Rural Europe, notably Nordic countries | Long term (≥ 4 years) |

| Regulatory Complexity and Rights-of-way Delays | -1.1% | Dense urban zones in Germany and Italy | Medium term (2-4 years) |

| Energy Price Volatility Elevating Network OPEX and ROI Risk | -0.8% | EU-wide, energy-heavy markets | Short term (≤ 2 years) |

| Competitive Threat from LEO Satellite Broadband in Remote Regions | -0.6% | Remote and sparsely populated regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for FTTH in Low-Density Areas

Fiber deployment in rural Europe costs EUR 1,500-4,000 per premises, far higher than EUR 300-800 in urban areas, posing economic challenges that subsidies only partially address. Low-density regions incur high costs due to trenching, river crossings, and the need for specialized equipment in mountainous terrain. In Nordic countries, frozen ground conditions extend timelines by 40-60% and necessitate the use of expensive boring equipment. [3]FTTH Council Europe, “Cost Modeling and the Case for Fibre 2024,” ftthcouncil.eu Areas with fewer than 50 premises per square kilometer need over 70% take-up rates to achieve ROI within 15 years. Providers like CityFibre prioritize suburban markets with more than 200 premises per kilometer, avoiding rural areas despite incentives. These CAPEX constraints hinder fiber expansion in regions most affected by the digital divide.

Regulatory Complexity and Rights-of-Way Delays

Fiber deployment in Europe faces fragmented permitting processes across 27 member states, with approval timelines ranging from 3 months in Estonia to over 18 months in Germany for complex urban projects. Municipal authorities often lack standardized procedures, resulting in delays and increased costs. Rights-of-way negotiations involve multiple stakeholders, including transportation, environmental, and heritage authorities, each with distinct criteria and timelines. In Italy, archaeological reviews can delay urban fiber projects by 12-24 months when historical sites are involved, often necessitating route redesigns or the abandonment of marginal areas. [4]BEREC, “Regulatory Framework Study 2024,” berec.europa.eu The EU Broadband Cost Reduction Directive aims to streamline permitting; however, inconsistent implementation sustains outdated processes that favor incumbent operators. These inefficiencies disproportionately impact alternative providers lacking government relationships and multi-jurisdictional legal expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Fiber Ascendancy Challenges Cable Dominance

Cable DOCSIS retained a 37.84% share of the European fixed broadband market in 2024. FTTH/B is growing at a 15.66% CAGR, ensuring it overtakes cable before 2030. The European fixed broadband market gains resilience because fiber’s symmetric speeds and lower maintenance costs offset the near-term advantages of DOCSIS. The decline in copper usage accelerates as operators decommission legacy networks and redirect capital to fiber. Fixed wireless access fills rural gaps with service exceeding 100 Mbps, while satellite focuses on remote locales. Over the forecast horizon, fiber wholesale models unlock investment flows from pension funds and infrastructure funds, which are attracted by predictable, utility-like cash flows. Incumbents aim to defend their revenue by accelerating cabinet-to-home upgrades, yet greenfield overbuilders exploit suburban territories where coaxial and copper cannot support multi-gigabit demand. The European fixed broadband industry, therefore, navigates dual investments in last-mile fiber and DOCSIS 4.0; however, investor narratives increasingly favor all-fiber paths due to energy efficiency and higher lifetime capacity headroom.

A second growth driver involves open-access rules that allow multiple ISPs to rent fiber capacity, improving network monetization. Deutsche Telekom’s ten-million-premise target demonstrates how incumbents hedge cable pressure with deep fiber builds. Orange’s EUR 3.5 billion French program follows the same logic. Cable operators respond with DOCSIS 4.0 to offer downstream multi-gig, yet their uploads remain constrained, pushing gamers and remote workers toward fiber. Satellite and 5G fixed wireless remain complementary, providing temporary relief where trenching remains uneconomic. The Europe fixed broadband market continues to value technology diversity, yet investor confidence aligns squarely behind FTTH/B because of regulatory momentum and consumer speed expectations.

By Speed Tier: Multi-Gig Services Drive Premium Migration

The 100 Mbps-1 Gbps bracket, representing 65.35% of the European fixed broadband market size in 2024, delivers stable cash flows for most incumbents. Services above 1 Gbps grow at 15.22% CAGR because 8K streams and cloud gaming lift peak throughput needs. Early adopters are willing to pay higher tariffs for a future-proof service. Operators bundle multi-gig with cloud storage and cybersecurity add-ons that boost ARPU by 15-20%. Entry-level tiers under 25 Mbps decline in relevance as video services demand higher minimums.

Multi-gig also enhances customer stickiness because downgrading risks visible quality loss in multi-device households. Wholesale fiber networks price bandwidth in scalable increments so that retail ISPs can upsell without major CAPEX. Cable upgrades extend download speeds but cannot match fiber’s symmetric uploads, making multi-gig an effective churn-reduction play. Consequently, the European fixed broadband market embeds speed tier upselling into most operator growth roadmaps, particularly in saturated urban areas where subscriber additions are slow. Marketing emphasizes gaming latency and 8K readiness, helping operators justify price premiums even in price-sensitive Southern European markets.

By End User: Commercial Acceleration Outpaces Residential Growth

Residential accounts contribute 84.50% of 2024 revenue, but commercial lines expand faster at 9.75% CAGR. Hybrid work underscores the need for enterprise-grade connectivity solutions to homes, extending business connectivity budgets into the consumer domain. SMEs choose fiber because it offers superior cost-performance compared with legacy leased lines. Packages with static IPs, advanced security, and 24-hour support command premiums over standard residential offers. The European fixed broadband market thus enjoys revenue diversification as small enterprises digitize processes and migrate systems to cloud platforms.

Large corporates consolidate branch connectivity onto gigabit broadband combined with SD-WAN overlays, replacing aging MPLS circuits. Fiber’s lower latency and symmetric capacity enhance real-time analytics and remote collaboration. Providers monetize demand spikes by offering tiered SLAs, reinforcing network quality as a profit lever. The European fixed broadband industry benefits as commercial upgrades stabilize cash flows against residential saturation, and subsidy programs enable providers to reach business parks that were previously beyond their fiber footprints.

By Application: Gaming and Immersive Media Challenge Entertainment Dominance

Video streaming controlled 65.01% of the 2024 traffic share, while gaming and immersive media grew at a 15.14% CAGR as VR adoption surged in training, healthcare, and education. Multi-gig fiber removes latency bottlenecks for cloud gaming platforms like NVIDIA GeForce NOW and Xbox Cloud Gaming, enabling mass market adoption. Operators partner with OTT players to include gaming credits in broadband bundles, deepening customer engagement. Remote work sustains daytime traffic peaks and underscores the importance of symmetric bandwidth.

Smart-home devices surpass 15 per household, increasing always-on upstream traffic for cloud video and security feeds. Telehealth and distance learning persist post-pandemic, driving stable baseline bandwidth usage. Industrial automation emerges as a niche but strategic application because factories need deterministic, low-latency systems. Fiber providers pilot dedicated network slices to monetize mission-critical traffic without congesting consumer flows.

By Deployment Environment: Suburban Expansion Accelerates Beyond Urban Saturation

Urban districts still generate 50.49% of the revenue, but penetration nears the ceiling, prompting operators to redirect resources toward suburban towns, where competitive intensity is lower. CityFibre’s focus on 20,000-100,000 resident locations demonstrates how challengers claim a share outside dense metropolitan areas. Suburban build-outs yield higher take-up and loyalty because residents often have limited pre-existing choices. The European fixed broadband market, therefore, grows horizontally into commuter belts, aided by expedited permits and supportive local councils eager for digital inclusion.

Rural progress accelerates once subsidies offset trenching costs. Fixed-wireless 5G and satellite serve as stop-gaps until fiber arrives, ensuring basic 100 Mbps availability. Remote mountain or island communities remain in a satellite domain because terrain renders fiber uneconomic even with aid. Operators adopt cluster deployment models, wiring small villages in a rolling schedule to hit coverage targets without overextending crews. Suburban success stories convince investors that non-metro areas yield attractive risk-adjusted returns once scale is reached and churn remains low.

By Ownership: Alternative Providers Disrupt Incumbent Dominance

Cable MSOs held 34.22% infrastructure share in 2024, tapping DOCSIS upgrades to defend ARPU. Fixed wireless ISPs are growing at a 11.15% CAGR because 5G enables rapid roll-out in underserved suburbs. Open-access fiber overbuilders attract pension fund capital owing to predictable wholesale cash flows. Incumbent telcos press ahead with cabinet-to-home upgrades but face margin pressure as regulated wholesale fees fall. Satellite operators led by Starlink secure a niche share in remote zones, yet capacity constraints limit market penetration. The European fixed broadband market is witnessing growing fragmentation as various infrastructure modalities coexist, yet fiber networks are garnering the majority of new investment because they anchor future gigabit economies.

Wholesale mandates tied to public subsidies ensure retail competition; any ISP can sell over subsidized fiber. This ruleset accelerates price competition, raising the stakes for service differentiation in customer experience. Incumbents leverage brand recognition and bundled mobile offers to reduce churn, while challengers emphasize faster installations and symmetrical speeds. Competitive intensity drives continuous network investment cycles because falling unit bandwidth costs enable providers to offer multi-gigabit services at mass-market price points.

Geography Analysis

Germany generated 35.96% of Deutsche Telekom's 2024 revenue, reflecting the company's economic scale and its EUR 6 billion fiber plan. Municipalities grant streamlined permits, yet archaeological requirements slow certain corridors, favoring operators with local planning expertise. Competition intensifies as cable and alternative fiber networks overlap in major cities, driving promotional pricing but also stimulating innovation in service bundles.

Spain achieves the fastest CAGR at 11.54% because the national strategy targets universal fiber by 2025, backed by EUR 2.1 billion in funding. Incumbent Telefónica and Orange deploy in parallel, while smaller overbuilders specialize in underserved provincial towns. Open-access obligations spur healthy retail rivalry, keeping tariffs competitive despite premium speed tiers. Spain thus exemplifies how the alignment of subsidies and pro-competitive rules accelerates both coverage and penetration.

The United Kingdom, France, and Italy present mature yet divergent dynamics. UK separation of Openreach stimulated alternative build; CityFibre’s capital-light suburban model gains traction. France mandates infrastructure sharing that streamlines rural roll-out, but urban projects wrestle with municipal approvals. Italy leverages Open Fiber’s wholesale-only network to overcome historical under-investment, though complex concession rules extend contract lead times. Eastern Europe benefits from EU connectivity funds as Russian vendors retreat, opening the door for Western equipment providers. The Europe fixed broadband market therefore progresses at different speeds, but common gigabit goals align policy and capital across the continent.

Mordor Intelligence tracks the fixed broadband market across other major regions such as Asia, Middle East, and South America.

Competitive Landscape

The competitive landscape is characterized by moderate concentration. The combined top five players hold roughly a 55-60% share, leaving room for agile challengers. Incumbent telcos count on brand loyalty and multi-play bundles to defend their position, yet face cannibalization of legacy copper revenue as migrations accelerate. Cable MSOs are pushing DOCSIS 4.0 upgrades, but still face fiber encroachment in high-value postcodes. Fiber overbuilders raise record capital from infrastructure funds that prize long-dated, inflation-linked wholesale contracts.

Strategic examples highlight shifting tactics. Deutsche Telekom has launched an AI-based dynamic line management system to optimize capacity and reduce energy consumption by 15%. Orange trialed 25G PON in experimental zones to future-proof the backbone. CityFibre consolidated Connexin’s footprint in Hull to reach scale quickly in an incumbent-heavy market. Satellite operator Starlink partnered with regional ISPs in Norway to tap remote coastal demand. Fixed-wireless players deploy 5G millimeter wave backhaul at industrial parks to deliver low-latency private networks. This mosaic of strategies highlights how the European fixed broadband industry strikes a balance between incremental DOCSIS enhancements and emerging leapfrogging fiber deployments.

Incumbents also confront ESG pressures, with networks consuming up to 30 TWh of electricity yearly. Energy-efficient fiber helps meet carbon objectives and lowers OPEX. Owners sell mature footprints to infrastructure funds, recycling cash into greenfield builds or adjacent services, such as edge computing. The competitive position increasingly rests on the breadth of wholesale partners, the depth of content ecosystems, and agility in product releases, rather than raw subscriber counts alone.

Europe Fixed Broadband Industry Leaders

Deutsche Telekom AG

Orange S.A.

BT Group plc

Vodafone Group plc

Telefónica S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Virgin Media extended gigabit fiber to 13,000 additional Worcester homes on behalf of nexfibre, which allocated GBP 4.5 billion for nationwide FTTH roll-out.

- March 2025: CityFibre acquired Connexin’s entire fiber network in Hull and East Riding, unlocking potential reach to 185,000 premises.

Europe Fixed Broadband Market Report Scope

| Fiber to the Home / Premises (FTTH/B) |

| Cable (DOCSIS) |

| Digital Subscriber Line (DSL) and Copper |

| Fixed Wireless Access (5G/LTE) |

| Satellite Broadband |

| Up to 25 Mbps |

| 100 Mbps – 1 Gbps |

| Above 1 Gbps (Multi-Gig) |

| Residential |

| Commercial |

| Video Streaming and Entertainment |

| Online Gaming and Immersive Media |

| Remote Work and Cloud Collaboration |

| Smart Home and IoT Connectivity |

| Telehealth and Distance Learning |

| Industrial and Enterprise Automation |

| Urban |

| Suburban |

| Rural |

| Remote and Hard-to-Reach |

| Incumbent Telcos |

| Competitive Fiber Overbuilders |

| Cable Multiple System Operators (MSOs) |

| Fixed Wireless ISPs |

| Satellite Network Operators |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Technology | Fiber to the Home / Premises (FTTH/B) |

| Cable (DOCSIS) | |

| Digital Subscriber Line (DSL) and Copper | |

| Fixed Wireless Access (5G/LTE) | |

| Satellite Broadband | |

| By Speed Tier | Up to 25 Mbps |

| 100 Mbps – 1 Gbps | |

| Above 1 Gbps (Multi-Gig) | |

| By End User | Residential |

| Commercial | |

| By Application | Video Streaming and Entertainment |

| Online Gaming and Immersive Media | |

| Remote Work and Cloud Collaboration | |

| Smart Home and IoT Connectivity | |

| Telehealth and Distance Learning | |

| Industrial and Enterprise Automation | |

| By Deployment Environment | Urban |

| Suburban | |

| Rural | |

| Remote and Hard-to-Reach | |

| By Ownership | Incumbent Telcos |

| Competitive Fiber Overbuilders | |

| Cable Multiple System Operators (MSOs) | |

| Fixed Wireless ISPs | |

| Satellite Network Operators | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe fixed broadband market?

The market stands at USD 116.47 billion in 2025.

How fast is the market expected to grow by 2030?

It is forecast to reach USD 171.85 billion, reflecting an 8.09% CAGR.

Which technology segment is expanding the quickest?

FTTH/B is the fastest-growing segment at 15.66% CAGR through 2030.

Why are multi-gig broadband packages gaining traction?

8K streaming and cloud gaming push household bandwidth needs above 1 Gbps, driving demand for premium plans.

Which country shows the highest forecast growth?

Spain leads with an expected 11.54% CAGR through 2030.

How does hybrid work influence broadband demand?

Persistent remote work elevates residential traffic and sustains demand for symmetric fiber services with business-grade reliability.

Page last updated on: