Europe ESIM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

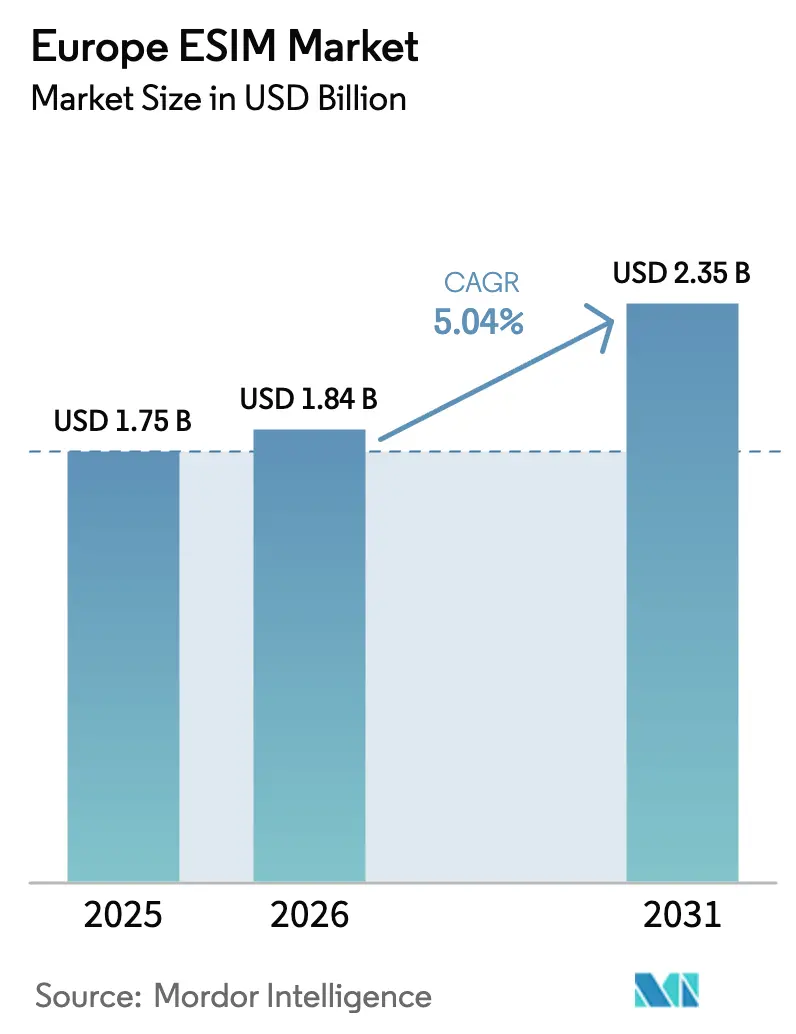

| Base Year Market Size (2025) | USD 1.75 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

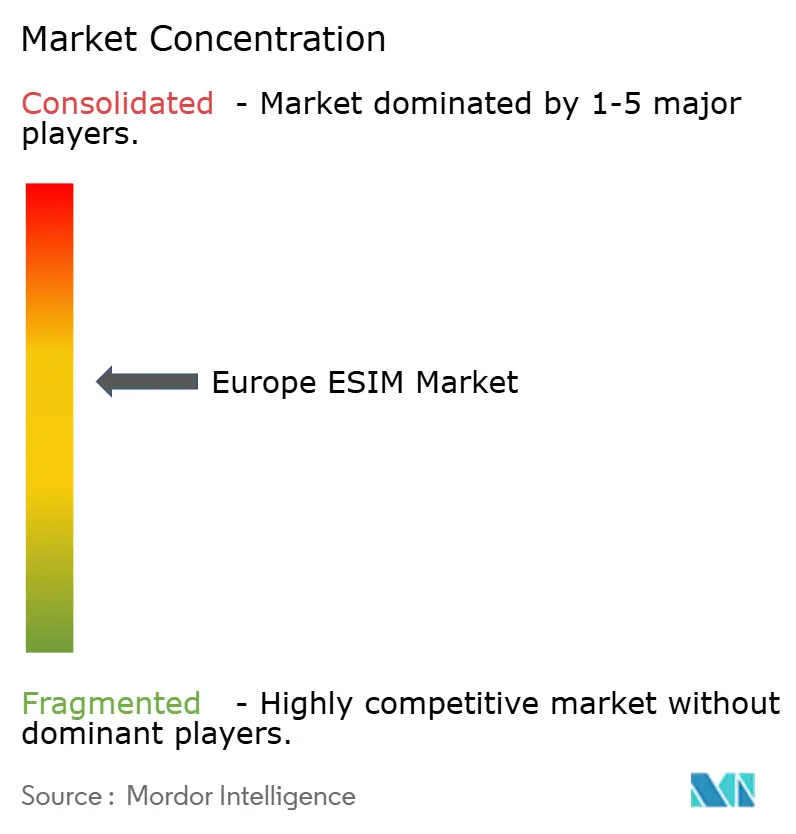

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe ESIM Market Analysis by Mordor Intelligence

Europe eSIM market size in 2026 is estimated at USD 1.84 billion, growing from 2025 value of USD 1.75 billion with 2031 projections showing USD 2.35 billion, growing at 5.04% CAGR over 2026-2031. In terms of installed base, the market is expected to grow from 125.84 million units in 2025 to 163.47 million units by 2030, at a CAGR of 5.37% during the forecast period (2025-2030). Moderate momentum reflects the region’s deliberate path toward standardization, the continued relevance of 4G services, and a measured shift toward software-defined connectivity. Early consumer enthusiasm has grown steadily as flagship smartphones transition to eSIM-only form factors, while industrial IoT programs accelerate demand across utilities, the automotive sector, and manufacturing. Large enterprises now prioritize remote SIM provisioning to reduce truck rolls, contain roaming costs, and simplify cross-border compliance. Hardware suppliers defend margins through integrated secure-element designs, but value migration toward cloud-native lifecycle management platforms is reshaping competitive dynamics. Supply-chain security and regulatory harmonization remain pivotal considerations as the European eSIM market scales across 27 member states.

Key Report Takeaways

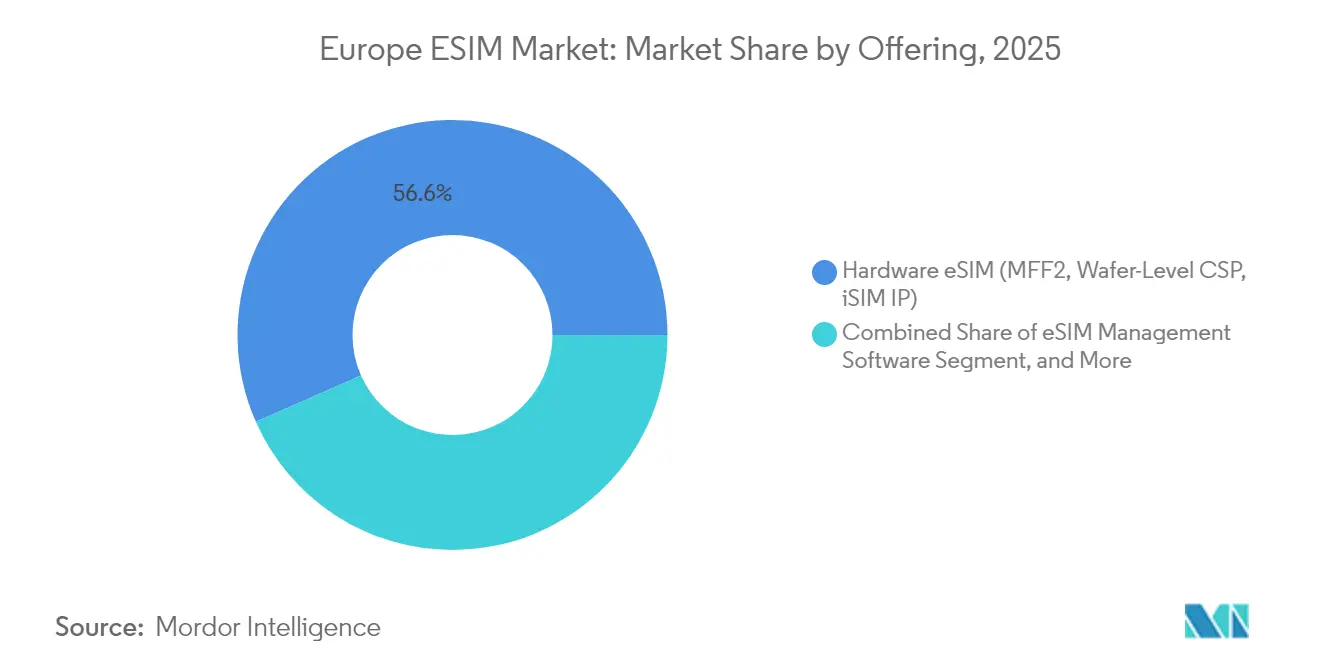

- By offering, the hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) segment led in the European eSIM market with a 56.62% share in 2025, whereas eSIM management software is projected to expand at a 9.41% CAGR through 2031.

- By device type, smartphones and feature phones accounted for 67.58% of the European eSIM market in 2025, whereas M2M/IoT modules are projected to grow at a 14.29% CAGR through 2031.

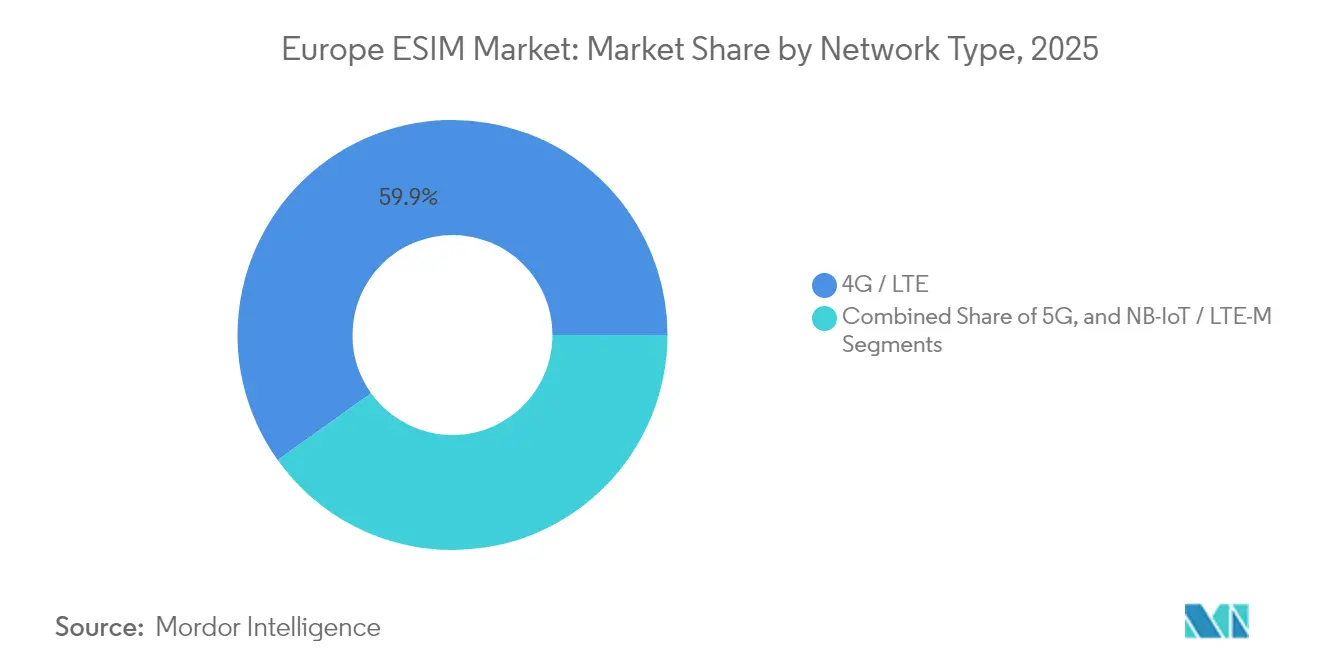

- By network type, 4G/LTE retained 59.88% share of the European eSIM market in 2025, while 5G is forecast to surge at 13.91% CAGR to 2031.

- By end-user industry, the consumer electronics segment accounted for 61.34% of the European eSIM market in 2025, while industrial and manufacturing are poised for the fastest growth, with a 14.31% CAGR through 2031.

- By country, Germany captured 21.75% of the European eSIM market in 2025, while the Rest of Europe is projected to register a 10.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe ESIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Rollout Across European Markets | +1.2% | EU-wide, strongest in Germany, UK, France | Medium term (2-4 years) |

| OEM Shift to eSIM-Only Flagship Smartphones | +1.8% | Global with EU regulatory alignment | Short term (≤ 2 years) |

| EU Regulatory Push for Seamless Roaming and Digital Onboarding | +0.9% | EU-wide, cross-border focus | Long term (≥ 4 years) |

| Public-Private Funding for Satellite-Cellular NTN eSIM Pilots in Remote Regions | +0.4% | Northern Europe, rural areas | Long term (≥ 4 years) |

| Mandated Smart-Meter Roll-outs with eSIM-Compatible NB-IoT Modules | +1.1% | Germany, Netherlands, France | Medium term (2-4 years) |

| Adoption of eSIM-based eID Programs for Cross-border Digital Identity | +0.6% | EU-wide, pilot markets first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Rollout Across European Markets

Fifth-generation networks now cover 89% of the EU population through more than 460,000 base stations, furnishing bandwidth and latency profiles that unlock network slicing for mission-critical industrial traffic.[1]European 5G Observatory, “5G Deployment Status in Europe,” 5gobservatory.eu As manufacturers deploy private 5G cells, eSIM authentication simplifies device onboarding across segmented slices, securing differentiated performance levels. German factories have pioneered this architecture, pairing embedded profiles with low-latency control loops for robotics lines. Leading operators are commercializing open network APIs that expose premium connectivity tiers, a model that hinges on seamless, programmable SIM profile transitions.[2]Deutsche Telekom Press Office, “Global Network API Venture,” telekom.com Traditional remote SIM provisioning software, however, must evolve to orchestrate dynamic service attributes in real time.

OEM Shift to eSIM-Only Flagship Smartphones

Apple’s 2025 European release of the eSIM-only iPhone 17 forced ecosystem-wide readiness, mirroring the US experience that began with iPhone 14. Samsung and Google have confirmed similar plans for flagships debuting by 2026, citing design simplicity and greater ingress protection. Device-centric onboarding eliminates physical distribution, steering consumers toward fully digital activation flows. Smaller mobile virtual network operators that lack robust remote provisioning stacks face churn risk, a concern flagged by European regulators reviewing the competitive neutrality of eSIM interoperability.[3]BEREC, “Report on eSIM Market Developments 2024,” berec.europa.eu Hardware makers also gain recurring revenue potential by bundling connectivity directly at the point of sale.

EU Regulatory Push for Seamless Roaming and Digital Onboarding

The European Commission has incorporated GSMA SAM.01 specifications into its Digital Identity Wallet regulation, enabling subscribers to validate their identity and activate services through secure mobile credentials starting in 2026. Harmonized rules are designed to eliminate cross-border activation hurdles, particularly for IoT fleets operating across member states. Enterprises anticipate administrative savings from paperless KYC processes, while eSIM vendors gain a standardized baseline for platform compliance. Implementation timelines, nevertheless, create a near-term gap in which disparate national rules persist, extending integration work for service providers.

Mandated Smart-Meter Roll-outs with eSIM-Compatible NB-IoT Modules

Germany, the Netherlands, and France require utilities to equip millions of residential and commercial sites with connected meters, fueling sustained demand for secure embedded modules. Thales, STMicroelectronics, and Infineon supply GSMA-certified secure elements, while platform players such as Netinium deliver cloud orchestration of meter profiles. Large-scale deployments demonstrate reduced truck rolls and higher data fidelity, but reliance on overseas module production underscores strategic supply-chain exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Operator Activation Workflows Across Countries | -1.4% | EU-wide, particularly smaller markets | Medium term (2-4 years) |

| Low Consumer Awareness Outside Early Adopters | -1.1% | Western Europe focus | Short term (≤ 2 years) |

| Supply-chain Exposure to Secure-element Chip Tariffs and Export Controls | -0.8% | Global supply chain, EU manufacturing | Long term (≥ 4 years) |

| Limited Interoperability of Emerging SGP.32 Profiles with Legacy RSP Platforms | -0.6% | EU-wide, technical implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Operator Activation Workflows Across Countries

BEREC’s 2024 assessment mapped wide divergence in eSIM onboarding requirements, ranging from in-person ID checks to fully digital flows. These variations inflate compliance costs and slow roll-out, especially for MVNOs targeting pan-European coverage. Service aggregators such as 1GLOBAL now partner with carriers like freenet to abstract local rules and deliver single-touch activation. Nonetheless, harmonization remains several years away, clouding near-term expansion plans for the European eSIM market.

Low Consumer Awareness Outside Early Adopters

According to the GSMA, only 19% of informed European consumers actively use eSIM services despite 50% awareness. A legacy attachment to retail SIM swaps and physical cards persists, slowing the mainstream adoption of these technologies. Operators have focused outreach on enterprise verticals, leaving a gap in mass-market education. Travel eSIM providers, such as Airalo, are registering strong growth among frequent flyers; however, these users represent a narrow demographic slice. Without broader marketing, the European eSIM market risks under-realizing its consumer potential during the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Unlock Next-Generation Value

Hardware eSIM segment secured 56.62% of Europe eSIM market share in 2025, anchored by secure-element chips that underpin every activated profile. Software, however, is growing rapidly; eSIM management software is projected to post a 9.41% CAGR, driven by enterprises demanding single-pane visibility across thousands of mobile devices. Remote SIM provisioning services complement both layers, streamlining lifecycle tasks from bootstrap credentialing to retirement.

Hardware vendors defend their pricing by incorporating integrated iSIM designs that embed secure-element logic into application processors, thereby reducing board area and power consumption. STMicroelectronics’ automotive iSIM launch positions the supplier for over-the-air updates mandated in connected cars. Thales and Giesecke+Devrient have introduced cloud orchestration suites, marking the convergence of signaling platforms. For buyers, shifting spend toward software enhances agility, lowers field-service costs, and aligns with zero-touch security frameworks, driving the modernization of factories and utilities.

By Device Type: IoT Modules Outpace Smartphones

Smartphones and feature phones account for 67.58% of the Europe eSIM market size in 2025; however, M2M/IoT modules are expected to surge at a 14.29% CAGR through 2031 as utilities, manufacturers, and logistics operators embed connectivity into their physical assets. Tablets, laptops, and wearables post incremental contributions but remain smaller pools.

The forthcoming wave of eSIM-only handsets from Apple, Samsung, and Google will sustain consumer demand, with travel roaming bundles facilitating adoption among mainstream subscribers. By contrast, metering, telemetry, and asset-tracking projects rely on NB-IoT and LTE-M modules with decade-long lifespans, where eSIM authentication minimizes the need for truck rolls. Utilities such as Stedin cite 95% fewer connectivity interventions after switching to embedded profiles. Automotive OEMs are embedding eSIM for eCall and infotainment, underscoring how industrial volumes will increasingly offset the flattening of handset growth within the European eSIM market.

By Network Type: 5G Momentum Chips Away at LTE

4G/LTE networks still carried 59.88% of 2025 revenue, underscoring a large installed base and broad handset compatibility across the Europe eSIM market. 5G, however, is projected to climb at a 13.91% CAGR through 2031, integrating network slicing and edge processing demanded by factory automation and mission-critical logistics.

Operators leverage existing LTE provisioning stacks to onboard millions of consumer devices with minimal incremental capex, but enterprises prefer 5G’s deterministic performance guarantees. Embedded modules shipping today carry multi-band radios and over-the-air upgrade pathways, ensuring that investments made in 2025 remain viable as slicing matures. NB-IoT retains a niche in deep indoor and battery-sensitive deployments, particularly smart meters mandated under EU efficiency directives.

By End-User Industry: Industrial Manufacturing Gains Velocity

Consumer electronics accounted for 61.34% of revenue in 2025, yet industrial and manufacturing are forecasted to expand at a 14.31% CAGR, reflecting Industry 4.0’s data-rich production lines that depend on secure, scalable connectivity. Automotive and transportation remain prominent adopters as vehicles transition to software-defined platforms.

Factory owners deploy private 5G microcells with eSIM gatekeeping, reducing lateral attack surfaces and enabling just-in-time reconfiguration of material-handling robots. Schneider Electric documents 30% faster commissioning cycles after standardizing on embedded profiles. In the energy sector, regulatory timelines compel utilities to equip every premise with eSIM-ready meters, ensuring sustained volume. Healthcare wearables utilize eSIM to comply with data-sovereignty regulations by dynamically selecting local networks when patients travel, demonstrating cross-industry support for the European eSIM market.

Geography Analysis

Germany captured 21.75% of the 2025 revenue in the Europe eSIM market, driven by mandatory smart meter deployments above 6,000 kWh annual usage and the penetration of connected vehicles among premium OEMs. The country’s deep industrial base accelerates private 5G expansion inside factories, where eSIM profiles secure deterministic slices on multi-vendor infrastructures. German operators offer bundled lifecycle management, making it easier to comply with rigorous cybersecurity norms.

The United Kingdom and France offer mature infrastructure with nationwide eSIM smartphone activations; however, adoption remains skewed toward business travelers and early adopters. Ofcom’s consultation on interoperability aims to level the playing field for smaller MVNOs, while France’s ARCEP spotlights IoT use cases under digital transformation grants. Italy and Spain are seeing a rise in tourist-driven downloads as travel rebounds, contributing incremental volumes to the European eSIM market.

The rest of Europe, spanning Nordic, Benelux, and Eastern states, is projected to outpace the region at a 10.03% CAGR. Nordic telcos leverage strong 5G footprints to pilot satellite-cellular continuity services that rely on embedded profiles. Eastern states, starting from lower penetration, show steep growth as handset OEMs phase out physical trays. Cross-border digital identity wallets, expected to be introduced post-2026, will further streamline activation, reinforcing geographic convergence across the Europe eSIM market.

Competitive Landscape

Leading secure-element manufacturers, including Thales, Giesecke+Devrient, STMicroelectronics, and Infineon Technologies, dominate the hardware supply chain with established GSMA certifications and strong operator partnerships. High R&D intensity and stringent audit requirements maintain oligopolistic margins, although the transition to iSIM is redefining traditional roles between chip vendors and application processor providers. To adapt, hardware incumbents are acquiring platform assets; such as, Thales acquired Telit Cinterion’s IoT unit, integrating devices with a cloud discovery service on Android.

Mobile network operators are exploring new revenue opportunities beyond airtime by collaborating on global network APIs. These APIs enable access to quality-of-service tiers through eSIM profile logic. Industry leaders such as Deutsche Telekom, Orange, Telefónica, and Vodafone have formed a joint venture to commercialize these interfaces, signaling a shift toward programmable connectivity. In contrast, smaller MVNOs are differentiating through specialized onboarding portals but face potential consolidation if they fail to meet compliance requirements, particularly with the upcoming mandate for the Digital Identity Wallet.

Disruptors like Airalo, Holafly, and Ubigi are reshaping the market with asset-light digital storefronts. These companies negotiate wholesale capacity and sell travel eSIM bundles directly to consumers, bypassing traditional brick-and-mortar distribution channels. This evolution highlights the growing impact of software and user experience in eroding the competitive edge of incumbents in the European eSIM market. Furthermore, specialized integrators are focusing on satellite-cellular hybrid services and industrial fleet orchestration, identifying untapped opportunities where legacy players have limited presence.

Europe ESIM Industry Leaders

Thales Group

Giesecke+Devrient GmbH

STMicroelectronics N.V.

Infineon Technologies AG

Deutsche Telekom AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Giesecke+Devrient integrated SGP.32 technology into Amazon’s new eero Signal router, marking one of the first consumer devices certified to the emerging standard.

- September 2025: TravelKon launched a 3UK eSIM for multi-country European itineraries, citing 1.3 million Australian visitors to the region last year.

- February 2024: Thales expanded its Android eSIM Discovery partnership with Google, automating profile detection and activation across European markets.

Europe ESIM Market Report Scope

The Europe eSIM Market Report is Segmented by Offering (Hardware eSIM [MFF2, Wafer-Level CSP, iSIM IP], eSIM Management Software, Remote SIM Provisioning Services), Device Type (Smartphones and Feature Phones, Tablets and Laptops, Wearables, M2M/IoT Modules), Network Type (5G, 4G/LTE, NB-IoT/LTE-M), End-user Industry (Consumer Electronics, Automotive and Transportation, Industrial and Manufacturing, Logistics and Asset Tracking, Energy and Utilities, Healthcare and Wearables), and Country (United Kingdom, Germany, France, Italy, Spain, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software |

| Remote SIM Provisioning Services |

| Smartphones and Feature Phones |

| Tablets and Laptops |

| Wearables |

| M2M/IoT Modules |

| 5G |

| 4G/LTE |

| NB-IoT/LTE-M |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Logistics and Asset Tracking |

| Energy and Utilities |

| Healthcare and Wearables |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Offering | Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software | |

| Remote SIM Provisioning Services | |

| By Device Type | Smartphones and Feature Phones |

| Tablets and Laptops | |

| Wearables | |

| M2M/IoT Modules | |

| By Network Type | 5G |

| 4G/LTE | |

| NB-IoT/LTE-M | |

| By End-User Industry | Consumer Electronics |

| Automotive and Transportation | |

| Industrial and Manufacturing | |

| Logistics and Asset Tracking | |

| Energy and Utilities | |

| Healthcare and Wearables | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe eSIM market in 2026?

The Europe eSIM market size reached USD 1.84 billion in 2026 and is forecast at USD 2.35 billion by 2031.

Which country leads adoption?

Germany holds 21.75% revenue share due to mandated smart-meter roll-outs and industrial IoT uptake.

Which segment is growing fastest?

M2M/IoT modules are projected to expand at 14.29% CAGR through 2031 on the back of utility and manufacturing projects.

What is driving enterprise interest?

Centralized eSIM management lowers field-service costs, simplifies cross-border compliance, and supports 5G network slicing.

How will EU regulation affect the market?

The Digital Identity Wallet framework, active from 2026, will standardize identity verification, reducing activation friction across borders and accelerating growth.

What supply-chain risks exist?

European deployments rely heavily on imported cellular IoT modules, raising exposure to export controls and tariff shifts on secure elements.

Page last updated on: