Europe Electric Vehicle Wireless Charging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 32.16 Million |

| Market Size (2030) | USD 173.71 Million |

| Growth Rate (2025 - 2030) | 40.05% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Vehicle Wireless Charging Equipment Market Analysis by Mordor Intelligence

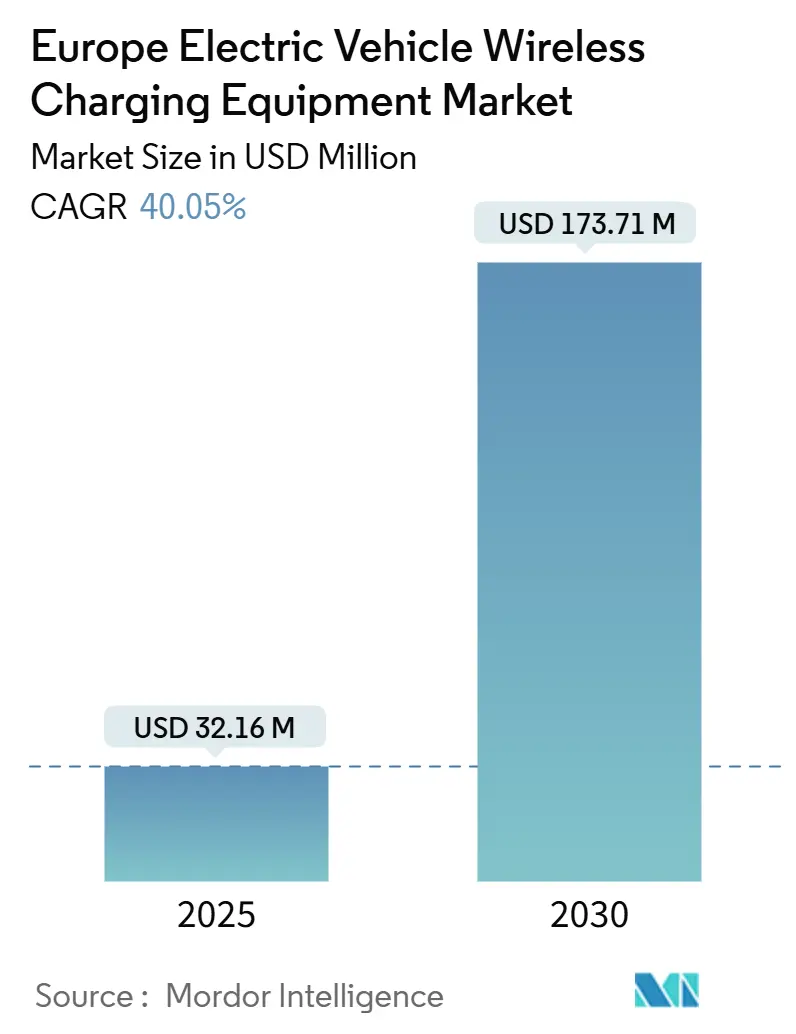

The Europe Electric Vehicle Wireless Charging Equipment Market size is estimated at USD 32.16 million in 2025, and is expected to reach USD 173.71 million by 2030, at a CAGR of 40.05% during the forecast period (2025-2030).

The Europe Electric Vehicle Wireless Charging Equipment Market is positioned as a technology-led, regulation-driven market, supported by high EV penetration, strong public charging networks, and early adoption of advanced mobility solutions. Wireless EV charging equipment enables contactless power transfer through inductive coupling, supporting static and dynamic charging use cases across residential, fleet, and public infrastructure environments.

Europe’s market development is shaped by stringent emission regulations, strong public-sector involvement, and a high concentration of pilot programs across transit and smart-city initiatives. While plug-in charging infrastructure is already well established, wireless charging is gaining relevance in applications where automation, safety, and operational efficiency are prioritized, particularly in public transport and municipal fleets.

Key Report Takeaways

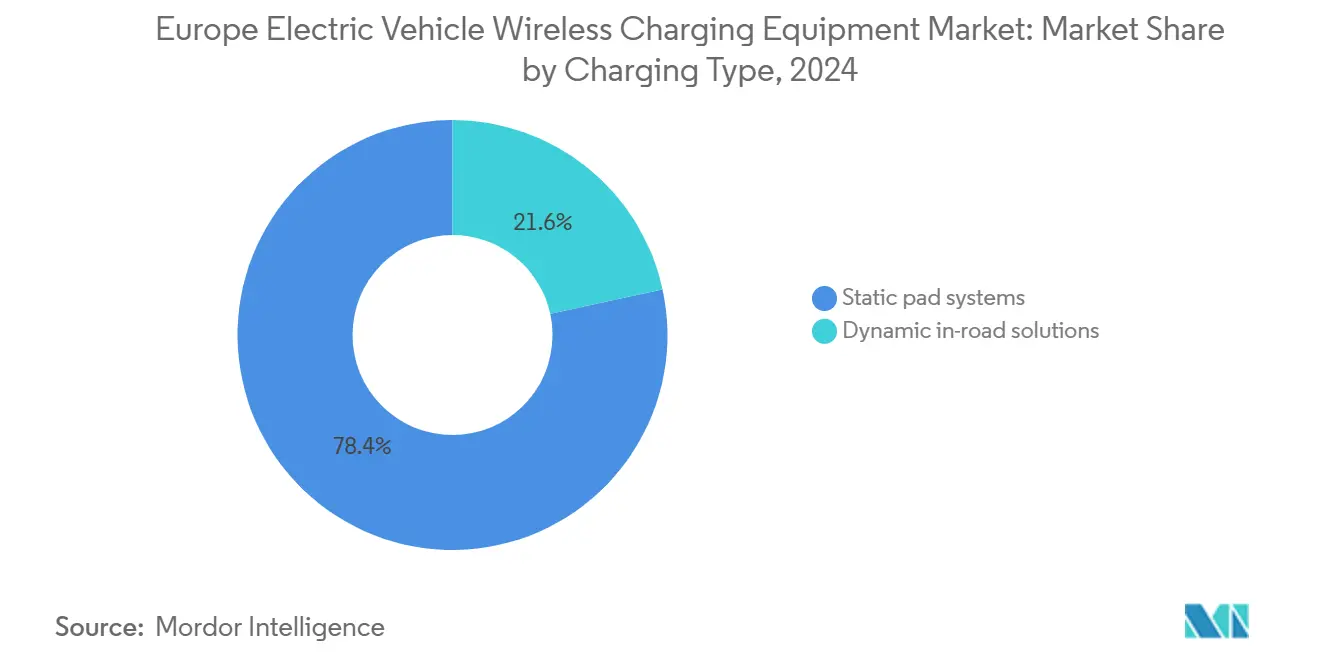

- By charging type, static pad systems held 78.40% share in 2024, while dynamic in-road solutions are forecast to grow at 54.80% CAGR through 2030.

- By vehicle type, passenger cars accounted for 60.10% of 2024 revenue; commercial vehicles (incl. buses/coaches) are projected to expand at 42.60% CAGR through 2030.

- By power output, up to 11 kW systems represented 50.20% of 2024 market size; above 150 kW systems are expected to grow at 61.40% CAGR through 2030.

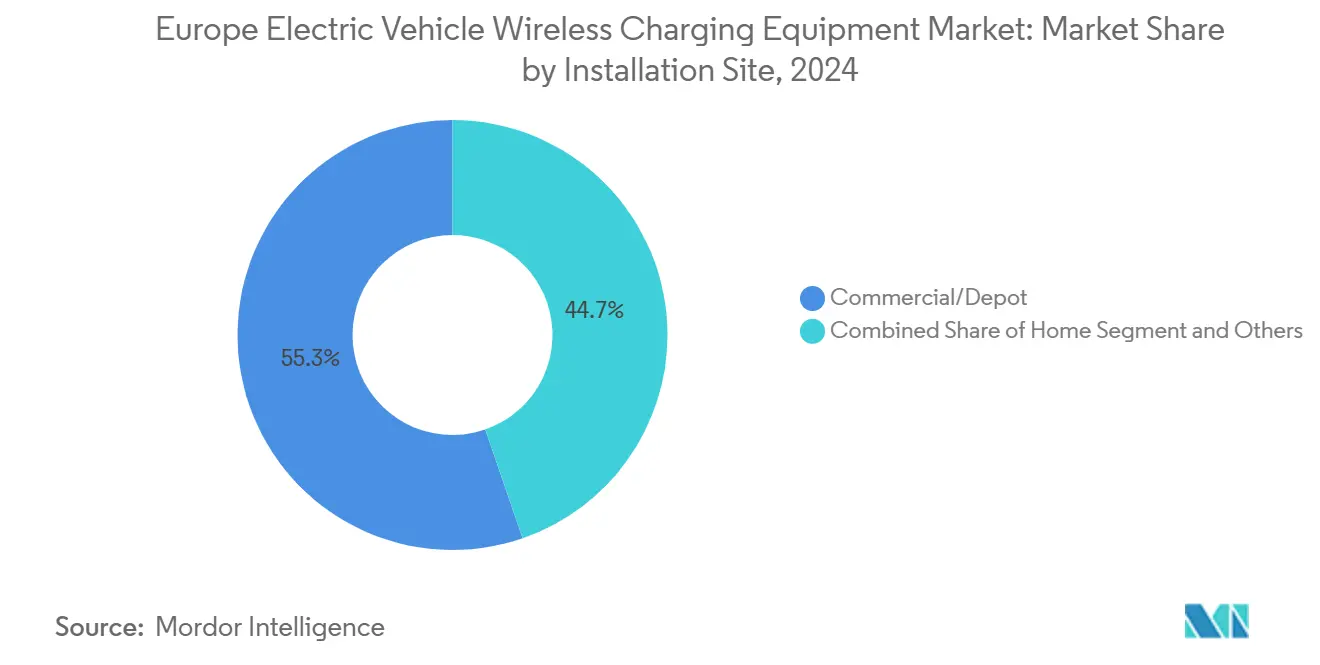

- By installation site, commercial and depot installations captured 55.30% of 2024 market size, while highway lane projects show the highest growth at 49.90% CAGR through 2030

- By technology platform, inductive resonant coupling led with 71.60% share in 2024; multi-coil alignment platforms are forecast to grow at 58.70% CAGR through 2030.

- By geography, Germany accounted for 28.50% of the 2024 Europe market size, while the Nordics are projected to be the fastest-growing cluster at 52.10% CAGR through 2030.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global electric vehicle wireless charging equipment market data by Mordor Intelligence represents that combined structure.

Europe Electric Vehicle Wireless Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Standards and Certification Clarity | +1.0% | Germany, France, Netherlands, Nordics (multi-OEM sites) | Medium term (2–4 years) |

| Public Transit and Municipal Fleet Electrification | +0.9% | Germany, France, UK, Italy, Spain (bus depots and city fleets) | Short term (≤ 2 years) |

| Depot Automation and Uptime Economics | +0.8% | Germany, UK, Nordics (centralized fleet operations) | Short term (≤ 2 years) |

| High-Power Wireless for Bus Terminals and Depots | +0.7% | France, Germany, Nordics (route-based opportunity charging) | Medium term (2–4 years) |

| Dynamic Pilot Corridors Backed by Public Works | +0.6% | France, Germany, Netherlands (showcase corridors) | Long term (≥ 4 years) |

| Urban Streetscape Constraints and Above-Ground Hardware Reduction | +0.5% | Netherlands, UK, Italy, Spain (dense urban cores) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Interoperability Standards and Certification Clarity

Europe’s charging environment is multi-brand by design, which increases the value of interoperable wireless charging systems. Clear standards and certification pathways reduce engineering uncertainty for OEMs, Tier-1 suppliers, and site operators by defining alignment tolerances, communication requirements, and safety concepts. This improves confidence in multi-brand site planning for shared parking operators and fleet hubs, where equipment must support mixed vehicle populations without customization by model line.

Public Transit and Municipal Fleet Electrification

European cities continue to electrify buses and municipal fleets to meet clean mobility mandates and low-emission zone requirements. Wireless charging becomes relevant where fleets require predictable uptime and standardized daily routines, especially in depots and terminal loops. In these operations, automated charging reduces manual handling, improves consistency across shifts, and supports higher vehicle availability, which strengthens the business case in public procurement-driven programs.

Depot Automation and Uptime Economics

Depot-centric charging environments support the most repeatable wireless charging deployments in Europe. Vehicle schedules and parking positions are controlled, maintenance teams are centralized, and utilization rates are measurable. This allows wireless charging to deliver operational efficiency through reduced connector wear, fewer manual steps, and lower process variability. These factors shorten payback periods in comparison to public parking installations, where utilization and operating control are weaker.

High-Power Wireless for Bus Terminals and Depots

Europe’s fleet and transit operators increasingly require high-power charging to minimize dwell time and keep vehicles in service across long duty cycles. Wireless systems above standard residential power ranges support this need, particularly for buses and coaches that return to terminals for short intervals. However, high-power wireless adoption remains linked to demonstrated field performance, safety validation, and proven reliability under daily cycling, which makes large transit operators important early adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CapEx Versus Mature DC Fast-Charging Networks | -1.2% | Western Europe (Germany, France, UK, Netherlands) | Short term (≤ 2 years) |

| Permitting, Civil Works, and Multi-Stakeholder Approvals | -0.9% | EU cities and highway authorities | Medium term (2–4 years) |

| Efficiency, Alignment, and EMF Compliance Complexity | -0.8% | High-power depots and shared parking | Medium term (2–4 years) |

| Limited Factory-Fit Receiver Availability in Mass Segments | -0.6% | Across Europe (OEM gating) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CapEx Versus Mature DC Fast-Charging Networks

Europe has a comparatively advanced wired charging base, including expanding high-power DC networks, which sets a high benchmark for wireless ROI. Wireless deployments require both ground-side infrastructure and in-vehicle receiver hardware, raising total installed cost relative to many wired alternatives. Where utilization is uncertain or tariffs are unfavorable, payback periods extend, which concentrates early wireless deployments in controlled fleet environments rather than open public parking.

Permitting, Civil Works, and Multi-Stakeholder Approvals

Wireless charging programs that extend beyond private depots typically require coordination with municipalities, utilities, and transport authorities. Civil works complexity increases sharply for public-space projects and in-road pilots, where lane closures, safety approvals, and construction scheduling become material constraints. These factors slow scaling, limit deployment volumes to a small number of projects at a time, and increase execution risk for corridor-based strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Type: Static systems dominate current deployments, while dynamic in-road charging drives future growth.

Static wireless charging remains the commercial anchor in Europe, holding 78.40% share in 2024. Adoption is concentrated in depot and structured-site deployments where installation conditions are controlled and operational benefits are measurable.

Dynamic in-road solutions are expected to be the fastest-growing segment at 54.80% CAGR through 2030. Growth is driven by corridor demonstrations linked to public transport and freight lanes; however, scale remains dependent on permitting, civil works, and multi-party funding.

By Vehicle Type: Passenger cars lead adoption, while commercial fleets scale faster.

Passenger cars led the market in 2024 with 60.10% revenue share. Demand is tied to premium trims and controlled home or private parking settings, where user convenience is the primary value driver.

Commercial vehicles (including buses and coaches) are forecast to grow at 42.60% CAGR through 2030. Fleet economics support adoption through higher utilization, standardized depot procedures, and reduced manual connector handling.

By Power Output: Low-power systems lead today, with high-power deployments accelerating.

Up to 11 kW systems dominated 2024 with 50.20% share. This band aligns with residential and light-commercial deployments where electrical upgrades are constrained and solution maturity is higher.

Above 150 kW systems are projected to grow at 61.40% CAGR through 2030. Demand is led by high-throughput depots and transit operations that require meaningful energy transfer in short dwell windows.

By Installation Site: Depot installations anchor the market, while highway corridors expand fastest.

Commercial and depot installations formed the largest site category at 55.30% share in 2024. Europe’s early adoption is concentrated where asset ownership, utilization, and maintenance are controlled by a single operator.

Highway lane projects are expected to grow fastest at 49.90% CAGR through 2030. Rollouts remain project-led and concentrated in a limited number of corridors owing to approval cycles and civil cost intensity.

By Technology Platform: Inductive systems lead today, while multi-coil platforms gain momentum.

Inductive resonant coupling led with 71.60% share in 2024, supported by the most established component ecosystem and easier certification pathways.

Multi-coil alignment platforms are forecast to expand at 58.70% CAGR through 2030. Adoption increases as deployments shift to shared parking and fleets, where alignment tolerance directly affects uptime and ROI.

Geography Analysis

Germany leads Europe with 28.50% of 2024 market size, supported by a large EV parc, strong OEM integration activity, and fleet electrification programs that favor standardized depot deployments. The country also benefits from concentrated infrastructure investment capacity, supporting repeatable installations and earlier learning-curve benefits.

The Nordics are projected to be the fastest-growing cluster at 52.10% CAGR through 2030, driven by high EV penetration, strong policy support, and municipal fleet electrification. Growth is expected to remain clustered around high-density metros and transit depots, then expand as unit economics stabilize and interoperability improves.

The electric vehicle wireless charging equipment market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia.

Competitive Landscape

The European market is moderately concentrated, led by global wireless charging technology providers, automotive Tier-1 suppliers, and infrastructure integrators. Competitive strength is driven by certified technology platforms, OEM partnerships, and successful public-sector pilot deployments.

Tier-1 suppliers play a central role by integrating wireless charging into broader electrification portfolios, while infrastructure specialists focus on system delivery and compliance with European regulatory frameworks. Public–private partnerships remain a key route to scale, particularly for dynamic and transit-focused deployments.

Europe Electric Vehicle Wireless Charging Equipment Industry Leaders

WiTricity Corporation

Plugless Power (Evatran Group)

HEVO Power

Nissan Motor Co., Ltd.

Toyota Motor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Infineon partners with Electreon to advance electric road charging from pilot tracks toward highway applications for commercial EVs in Europe

- November 2025: Electreon signs a memorandum of understanding to acquire InductEV assets, uniting dynamic and high-power static wireless charging technologies for broader Europe and global deployments.

- October 2025: The world’s first dynamic wireless-charging motorway launched on France’s A10 near Paris, enabling EVs to charge while driving under real traffic and delivering over 300 kW power in tests.

Europe Electric Vehicle Wireless Charging Equipment Market Report Scope

Electric vehicle wireless charging equipment refers to hardware and embedded control/communication systems that enable contactless power transfer between a ground-side transmitter (pad/coil + power electronics + controls) and a vehicle-side receiver (coil + rectification/control), supporting static (park-and-charge) and dynamic (in-motion) wireless charging configurations.

The scope includes segmentation by Charging Type (Static, Dynamic), Vehicle Type (Passenger Cars, Commercial Vehicles), Power Output (Up to 11 kW, 11–50 kW, 50–150 kW, Above 150 kW), Installation Site (Home, Commercial/Depot, Public Parking, Highway/Lane), Technology Platform (Inductive Resonant Coupling, Multi-Coil Alignment Platforms, and Others), Distribution Channel (OEMs, Aftermarket), and Country. The market forecasts are provided in terms of value (USD).

| Static |

| Dynamic |

| Passenger Cars |

| Commercial Vehicles |

| Up to 11 kW |

| 11–50 kW |

| 50–150 kW |

| Above 150 kW |

| Home |

| Commercial/Depot |

| Public Parking |

| Highway/Lane |

| Inductive Resonant Coupling |

| Multi-Coil Alignment Platforms |

| Others |

| OEMs |

| Aftermarket |

| Germany |

| France |

| United Kingdom |

| Spain |

| Italy |

| Norway |

| Finland |

| Russia |

| Netherlands |

| Rest of Europe |

| Segmentation by Charging Type (Value, USD) | Static |

| Dynamic | |

| Segmentation by Vehicle Type (Value, USD) | Passenger Cars |

| Commercial Vehicles | |

| Segmentation by Power Output (Value, USD) | Up to 11 kW |

| 11–50 kW | |

| 50–150 kW | |

| Above 150 kW | |

| Segmentation by Installation Site (Value, USD) | Home |

| Commercial/Depot | |

| Public Parking | |

| Highway/Lane | |

| Segmentation by Technology Platform (Value, USD) | Inductive Resonant Coupling |

| Multi-Coil Alignment Platforms | |

| Others | |

| Segmentation by Distribution Channel (Value, USD) | OEMs |

| Aftermarket | |

| Segmentation by Country/Cluster (Value, USD) | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Norway | |

| Finland | |

| Russia | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

Which charging type is largest in 2024, and what grows fastest?

Static pad systems lead at 78.40% in 2024; dynamic in-road solutions grow fastest at 54.80% CAGR (2025–2030E).

Which vehicle type leads now, and which scales faster?

Passenger cars lead at 60.10% in 2024; commercial vehicles grow fastest at 42.60% CAGR (2025–2030E).

Which power band dominates, and which expands quickest?

Up to 11 kW leads at 50.20% in 2024; above 150 kW grows fastest at 61.40% CAGR (2025–2030E).

Which installation site is largest, and which grows fastest?

Commercial/depot sites lead at 55.30% in 2024; highway lane projects grow fastest at 49.90% CAGR (2025–2030E).

Which technology platform leads, and which gains share?

Inductive resonant coupling leads at 71.60% in 2024; multi-coil platforms grow fastest at 58.70% CAGR (2025–2030E).

Page last updated on: