Europe Customer Journey Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

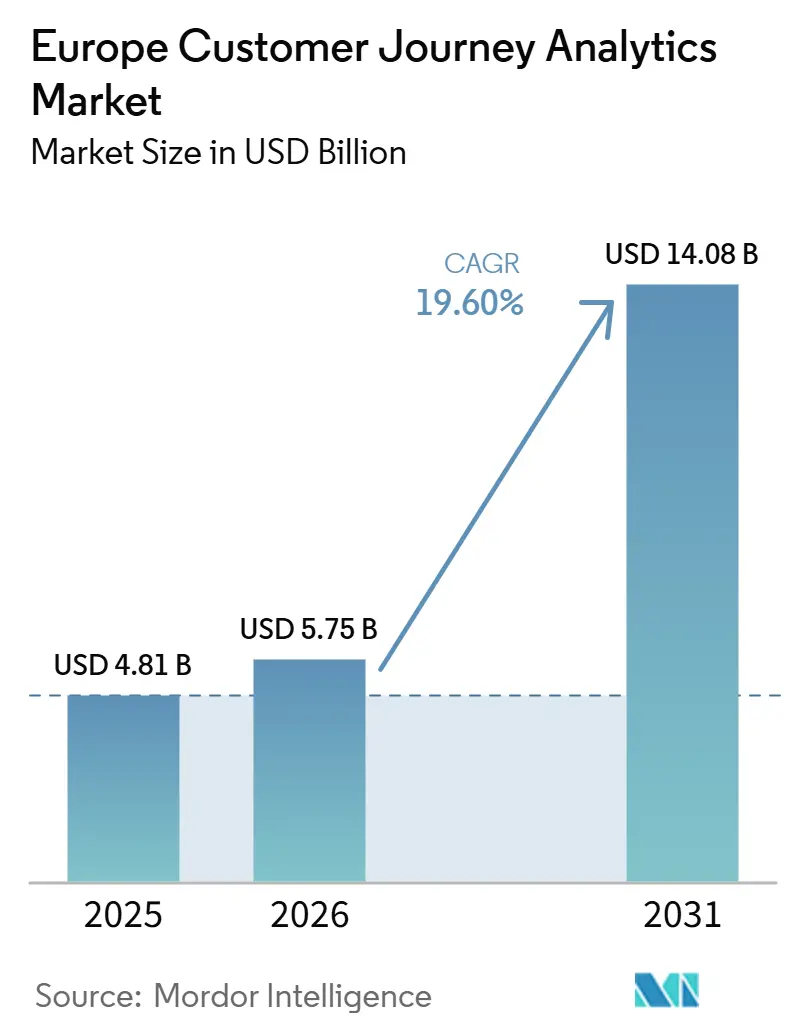

| Base Year Market Size (2025) | USD 4.81 Billion |

| Market Size (2026) | USD 5.75 Billion |

| Market Size (2031) | USD 14.08 Billion |

| Growth Rate (2026 - 2031) | 19.60% CAGR |

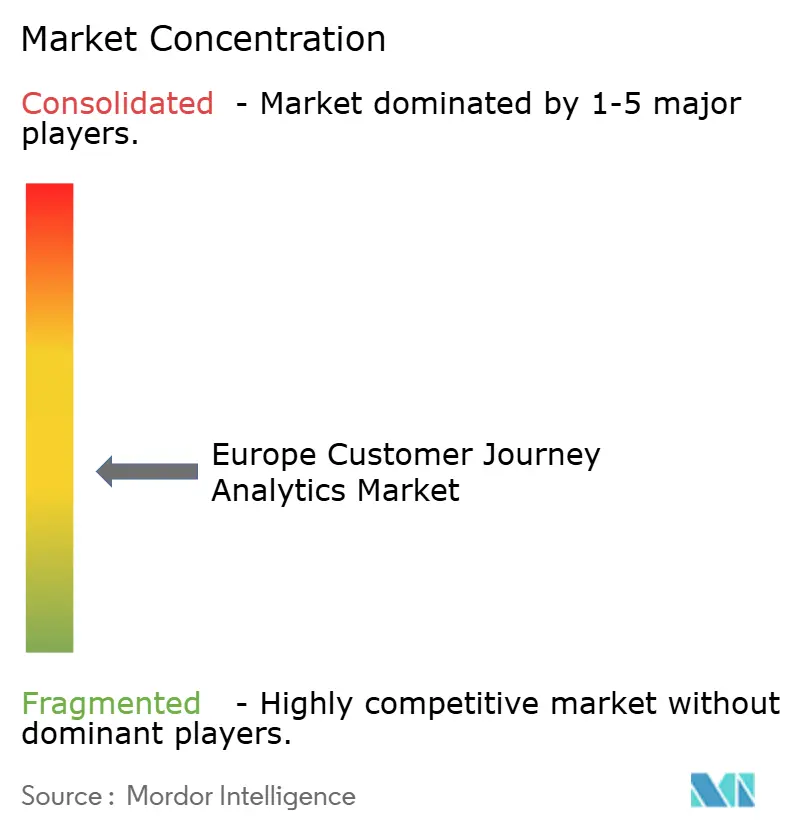

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Customer Journey Analytics Market Analysis by Mordor Intelligence

The Europe customer journey analytics market size is projected to be USD 4.81 billion in 2025, USD 5.75 billion in 2026, and reach USD 14.08 billion by 2031, growing at a CAGR of 19.60% from 2026 to 2031. Growth is being supported by the shift from isolated analytics tools to integrated platforms that connect data capture, analysis, and action across customer touchpoints. Enterprises are also moving away from delayed reporting because live journey visibility now matters more in digital commerce, service operations, and customer retention programs. Cloud-native architecture is driving adoption, as it enables companies to process larger data volumes and deploy AI functions faster than in legacy environments. Privacy rules are still shaping buying decisions, yet they are also pushing organizations to build stronger first-party data programs and improve internal data quality. Competition in the Europe customer journey analytics market remains active, with large software vendors defending installed accounts while cloud-built specialists win attention through faster product releases and more flexible analytics workflows.

Key Report Takeaways

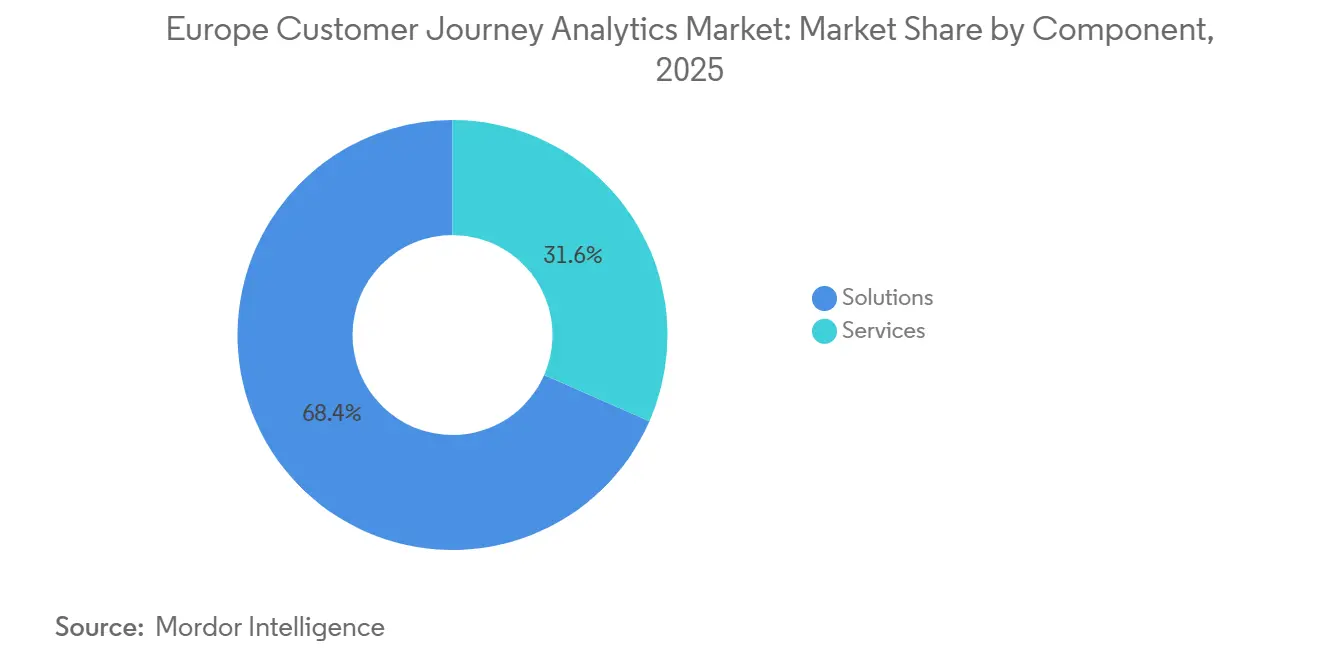

- By component, solutions held 68.44% of the Europe customer journey analytics market revenue in 2025, while services are projected to expand at a 22.68% CAGR through 2031.

- By deployment mode, cloud accounted for 70.86% of the Europe customer journey analytics market revenue in 2025 and is projected to expand at a 22.45% CAGR through 2031.

- By application, Journey Mapping and Visualisation accounted for 58.91% share of the Europe customer journey analytics market size in 2025, while Campaign and Journey Orchestration is projected to grow at a 21.78% CAGR through 2031.

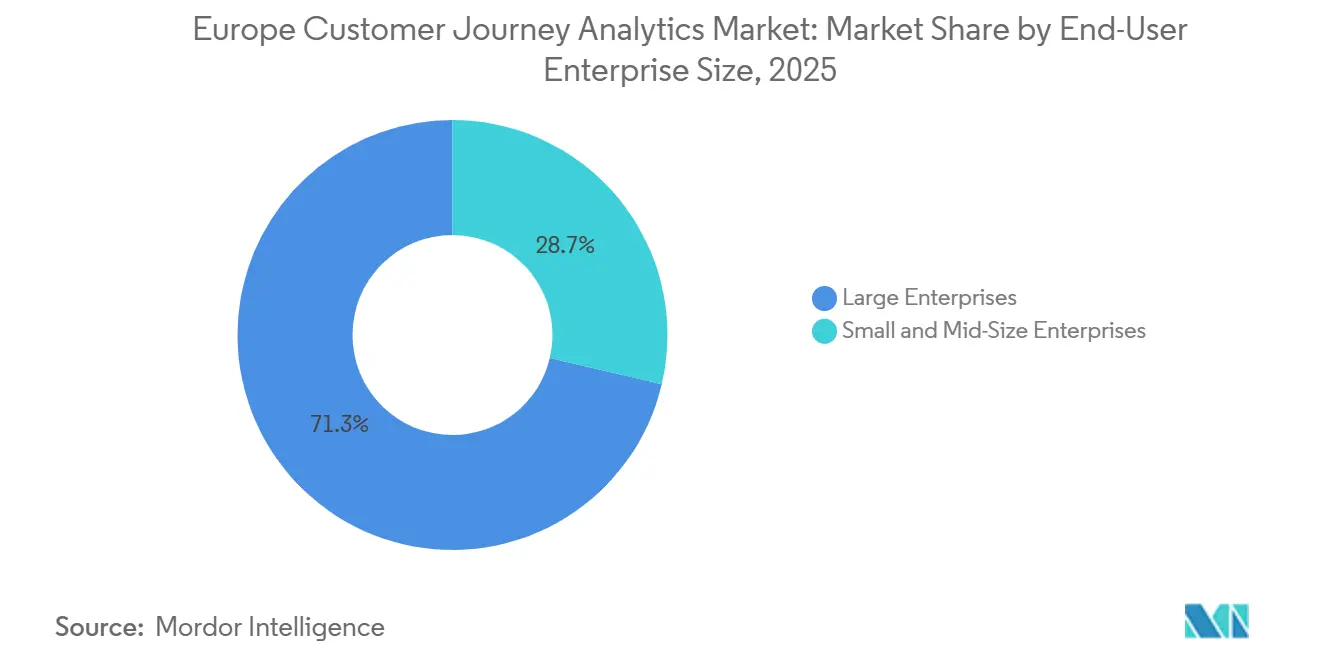

- By end-user enterprise size, large enterprises held 71.32% of the Europe customer journey analytics market share in 2025, while SMEs are projected to expand at a 22.12% CAGR through 2031.

- By end-user industry, retail and eCommerce led with 26.71% of the Europe customer journey analytics market revenue share in 2025, while healthcare and life-sciences is projected to grow at a 21.04% CAGR through 2031.

- By geography, the United Kingdom held 37.22% of the Europe customer journey analytics market share in 2025, while Spain is projected to record the fastest growth at a 21.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Customer Journey Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Real-Time Journey Orchestration | +4.2% | Global | Short term (≤ 2 years) |

| Expansion of First-Party Data Programs | +3.6% | EU-27, UK | Medium term (2-4 years) |

| Wider Adoption of AI-Based Next-Best-Action Models | +3.1% | Global | Medium term (2-4 years) |

| Migration to Cloud-Native CX and Analytics Stacks | +2.7% | Pan-European | Short term (≤ 2 years) |

| Growth of Composable Customer Data Architectures | +2.0% | Western Europe, Global | Long term (≥ 4 years) |

| Need for Cross-Channel Attribution in Complex Buying Journeys | +1.6% | Global, UK and Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Journey Orchestration

Enterprises across Europe are replacing delayed journey reporting with systems that respond while the customer is still active, because static analysis no longer protects conversion or service outcomes. Adobe connected Customer Journey Analytics, Journey Optimizer, and Real-Time CDP within CX Enterprise Coworker in 2026, which shows how live decision support is moving into core customer workflows. Contentsquare also launched AI agent capabilities, prompt analytics, and conversation intelligence in 2026, which reflects the shift toward active journey monitoring rather than passive dashboards. FullStory added StoryAI Agents and Workflow Intelligence in June 2026, extending autonomous discovery and action into digital experience management. As buyers close this execution gap, the Europe customer journey analytics market is moving toward larger platform contracts that combine detection, recommendation, and activation into a single operating layer.

Expansion of First-Party Data Programs Across Privacy-Constrained Channels

Privacy restrictions and weaker third-party signal availability are pushing companies to depend more on owned behavioral data, CRM records, and loyalty interactions to rebuild a complete customer path. Adobe said in 2026 that its CX Analytics launch addressed enterprise demand for cross-channel journey measurement in a post-cookie environment, which shows how first-party data has become central to product design. Adobe also introduced the Customer Journey Analytics B2B Edition in 2025 to analyze journeys across individuals, buying groups, accounts, and opportunities, underscoring a broader need for durable, owned data models in complex decision-making cycles. In practical terms, this means the Europe customer journey analytics market is gaining momentum as organizations seek stronger visibility without relying on unstable external tracking methods. The result is a buying pattern in which data integration quality matters as much as dashboard depth, because poor first-party foundations limit the value of advanced modeling.

Wider Adoption of AI-Based Journey Next-Best-Action Models

Descriptive journey analysis is losing ground to systems that recommend the next action, because enterprises increasingly want measurable intervention rather than backward-looking explanation. Adobe expanded AI agents for business use in 2025, including a Data Insights Agent inside Customer Journey Analytics that lets teams visualize, forecast, and remediate customer experience issues with natural-language queries. Adobe reinforced that direction in 2026 through CX Enterprise Coworker and Adobe CX Analytics, which tied governed intelligence more directly to journeys, content, and customer data. This trend is raising expectations inside the Europe customer journey analytics market, because buyers now want models that can rank friction, identify likely outcomes, and support rapid decisions across channels. It is also widening the gap between vendors with strong governance and workflow controls and those that still rely on static reporting or manual analyst support.

Migration to Cloud-Native CX and Analytics Stacks

Legacy environments are becoming harder to justify because the volume of journey data and the pace of AI updates continue to rise across enterprise use cases. Deutsche Telekom said its sovereign data platform on Google Cloud helped reduce the cost of on-premises preprocessing infrastructure while enabling cloud-scale analytics and agentic AI use cases. Vodafone Italy also modernized customer data workflows with Google Cloud and BigQuery without disrupting operations, demonstrating how large European enterprises are shifting critical analytics functions to scalable cloud environments. AWS also outlined an event-driven, composable CDP architecture using Snowplow and Databricks, which supports the move toward modular, warehouse-linked analytics design.[1]Amazon Web Services, “Event-Driven Composable CDP Architecture Powered by Snowplow and Databricks,” AWS Partner Network Blog, aws.amazon.com As this transition continues, the Europe customer journey analytics market is seeing stronger demand for implementation support, migration planning, and ongoing architecture services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy CRM and Contact Center Systems | -2.6% | Global | Short term (≤ 2 years) |

| Data Privacy Consent Fragmentation across European Markets | -2.3% | EU-27, acute in Germany and France | Medium term (2-4 years) |

| Shortage of Journey Analytics Talent and Data Engineering Capacity | -1.4% | Pan-European | Long term (≥ 4 years) |

| Model Drift and Governance Risk in AI-Driven Journey Decisions | -1.0% | Global, regulated sectors such as BFSI and healthcare | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy CRM and Contact Center Systems

Customer journey analytics only works when data from CRM, contact center, billing, and digital channels can be connected consistently, and that remains difficult in many large organizations. The problem is not limited to the technology age, because many enterprises still operate business-unit systems with separate owners, different workflows, and inconsistent data definitions. Deutsche Telekom’s migration case shows why companies are leaving behind heavy-preprocessing environments, yet it also highlights the scale of architectural work required before cloud analytics can operate smoothly. Vodafone Italy’s modernization path points to the same issue, because moving customer data workflows into BigQuery required a staged transformation rather than a simple software installation. This keeps deployment cycles long in the Europe customer journey analytics market, especially where hidden dependencies in older systems are discovered only after integration begins.

Data Privacy Consent Fragmentation across European Markets

Privacy compliance in Europe remains uneven across countries, making regional analytics programs harder to standardize than many global vendors initially expect. Data loss due to consent rejections affects journey visibility before modeling even starts, weakening attribution quality and limiting confidence in cross-country comparisons. Buyers, therefore, need separate governance choices for markets with stricter interpretations, which increases deployment costs even when the software platform itself is already in place. Adobe’s 2026 product positioning around a post-cookie environment shows that this issue has moved from a legal matter to a core product and procurement concern. Until privacy conditions become more consistent, the Europe customer journey analytics market will continue to face a structural limit on how quickly pan-European deployments can scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Points to Outcome-Based Engagement

Solutions held 68.44% revenue share in 2025, while services are projected to grow at a 22.68% CAGR through 2031. The revenue lead shows that enterprise platform contracts still anchor the Europe customer journey analytics market, especially where large buyers already use broad software ecosystems. These contracts usually cover core analytics capabilities, identity management, reporting layers, and journey measurement across several business functions. That installed base keeps solutions in front of current revenue, because replacement cycles for enterprise platforms are long and procurement still favors established vendors in large accounts. It also explains why many organizations first secure the technology stack and then expand the operating model around it.

The faster service growth shows that software alone is no longer enough to deliver commercial results from journey data. Buyers increasingly need help with implementation, data model design, governance setup, dashboard tuning, and business adoption after go-live. This pattern is especially evident when cloud migration, AI workflows, and privacy controls must be coordinated simultaneously. As a result, the Europe customer journey analytics market is shifting toward longer vendor relationships that mix platform subscriptions with advisory and managed support. In practical terms, services are becoming a performance layer around the software rather than a basic post-sale add-on.

By Deployment Mode: Cloud Consolidation Changes Architecture Priorities

Cloud accounted for 70.86% of deployment-mode revenue in 2025, confirming that elastic infrastructure has become the default setting for new analytics investments. That lead reflects the need to process larger behavioral datasets, unify channels faster, and support AI functions without maintaining heavy local hardware. In the Europe customer journey analytics market, cloud adoption aligns with the broader shift toward API-based architectures and warehouse-connected workflows. Buyers see value in lower infrastructure friction and faster rollout of analytics updates, especially when customer volumes change across seasons or campaigns. This is why cloud has moved from an alternative deployment choice to the main architecture baseline across many large accounts.

On-premises deployments still matter in regulated or sovereignty-sensitive settings, particularly where public cloud processing remains a harder internal approval path. Hybrid models, therefore, retain a role because they allow organizations to modernize in stages rather than force an abrupt replacement of legacy systems. Deutsche Telekom’s sovereign platform migration illustrates how cloud-scale analytics can be introduced while still respecting European data location requirements.[2]Google Cloud, “Vodafone Italy Modernizes with Amdocs and Google Cloud,” Google Cloud Blog, cloud.google.com Vodafone Italy’s move to Google Cloud and BigQuery also shows that major enterprises are willing to modernize core customer data workflows when operational continuity can be protected. Together, these shifts are raising the standard for vendors competing in the Europe customer journey analytics market, because buyers now expect both scale and regional compliance support.

By Application: Journey Mapping Leads While Orchestration Gains Speed

Journey Mapping and Visualisation held 58.91% share in 2025, which shows that many buyers still begin with visibility before they move into intervention. This segment captures the first stage of maturity, in which organizations seek a structured view of friction points, drop-offs, and channel behavior along the customer path. It remains the most common entry point in the Europe customer journey analytics market because mapping is easier to justify internally and easier to align across business teams. Companies often need a clear visual model before they can commit budget to predictive actions, automated triggers, or more advanced decision logic. That is why mapping retains the largest installed base even as more sophisticated use cases gain attention.

Campaign and Journey Orchestration is projected to grow at a 21.78% CAGR through 2031, making it the fastest-growing application area in the current mix. Adobe’s 2025 launch of Customer Journey Analytics B2B Edition shows how vendors are responding to demand for deeper analysis across accounts, opportunities, and buying groups rather than simple single-user tracking. Adobe’s 2026 CX Analytics and CX Enterprise Coworker launch pushed that further by linking journey data more closely with action and governed intelligence. As activation use cases expand, the Europe customer journey analytics market is moving beyond static diagnosis toward operating systems that support real-time intervention. That change will keep orchestration growth ahead of visualization, even though visualization remains the larger revenue pool today.

By End-User Enterprise Size: Large Enterprises Lead While SMEs Build Momentum

Large enterprises accounted for 71.32% of revenue in 2025, reflecting where data infrastructure, budget control, and integration capacity already sit. These organizations manage broader channel mixes, larger customer bases, and more complex compliance conditions, so journey analytics serves a practical operating need rather than an experimental project. In the Europe customer journey analytics market, large accounts also move first because they can fund platform deployment, service support, and governance work simultaneously. Their scale lets them justify longer procurement cycles and more extensive integrations across CRM, commerce, service, and marketing environments. This makes them the main source of current revenue even as adoption widens into smaller business tiers.

SMEs are projected to expand at a 22.12% CAGR through 2031, which shows that access barriers are falling as cloud delivery becomes more flexible. A major reason is that more vendors now offer consumption-based or modular entry points that reduce upfront commitment. Public digitalization programs are also supporting the shift, with Spain’s national digital transformation roadmap allocating EUR 33.8 billion (USD 36.8 billion), with EUR 26.7 billion (USD 29.1 billion) from public budgets, across broad digital measures. As these conditions improve, the Europe customer journey analytics market is becoming more accessible to companies that previously lacked the technical team or capital required for a full enterprise deployment. The growth pattern suggests that future expansion will come from broader account volume, even if large enterprises remain the primary revenue base.

By End-User Industry: Retail and eCommerce Lead While Healthcare and Life-Sciences Accelerate

Retail and eCommerce accounted for 26.71% of total revenue in 2025, placing it clearly ahead of other end-user industries. The sector’s lead reflects heavy dependence on conversion visibility, personalization, multichannel merchandising, and post-purchase experience management. In the Europe customer journey analytics market, retail buyers often feel pressure earlier than other sectors because weak journey design immediately affects basket completion and repeat buying. Metapack’s 2026 eCommerce Delivery Benchmark findings showed that 80% of UK retailers expected online sales growth in 2026, which supports continued spending on digital customer measurement and experience tools. This keeps retail and eCommerce in the lead, especially in digitally mature countries where online commerce and delivery expectations remain high.

Healthcare and life-sciences is projected to grow at a 21.04% CAGR through 2031, making it the fastest-growing vertical in the Europe customer journey analytics market. The segment is benefiting from a stronger focus on coordinated care pathways, interoperability, and better digital engagement across the patient experience. BFSI remains one of the larger user groups as well, because onboarding, retention, churn control, and cross-sell measurement rely on connected journey analysis. Information technology and telecom also remain important, particularly where high interaction volumes require real-time visibility across service and subscriber touchpoints. Media, travel, automotive, and other industries add a wider demand base, but the main growth shift is coming from sectors that now need customer journey intelligence as part of core service delivery rather than only as a marketing support tool.

Geography Analysis

The United Kingdom held 37.22% of the European customer journey analytics market share in 2025, making it the largest market in the region. That lead reflects a strong digital commerce base, mature enterprise demand, and wider use of AI-led customer tools across retail and service environments. Metapack’s 2026 benchmark findings showed that 80% of UK retailers expected online sales growth in 2026 and that 90% of global retailers planned to increase AI spending over the next 12 to 24 months. Those conditions keep the United Kingdom at the center of current demand in the Europe customer journey analytics market. Germany remained the second-largest geography, supported by large BFSI, automotive, and manufacturing activity, as well as customer interaction models that require deeper analytics across long, complex buying cycles.

France, Italy, and the rest of Europe form the next layer of regional demand, though each market follows a different adoption path. France benefits from a large enterprise base and steady digital customer engagement across commerce, financial services, and communications. Italy shows demand from multichannel retail, fashion, and financial services, and Vodafone Italy’s cloud modernization program illustrates how large companies are improving customer data workflows without business disruption. The rest of Europe continues to expand through a wider mix of smaller national markets, where adoption is rising as cloud availability and analytics maturity improve.

Spain is projected to record the fastest growth at a 21.36% CAGR through 2031, which gives it the strongest forward profile in the Europe customer journey analytics market. Public investment is a major reason, with Spain’s digital roadmap allocating EUR 33.8 billion (USD 36.8 billion) and EUR 26.7 billion (USD 29.1 billion) from public budgets, across 67 measures.[3]European Commission, “Spain 2025 Digital Decade Country Report,” European Commission Digital Decade, digital-strategy.ec.europa.eu That policy support is helping broaden digital capabilities across businesses that were previously outside advanced analytics adoption. Spain is also benefiting from a more accessible SME demand base, which gives vendors a larger pool of new buyers than in earlier years. For that reason, Spain stands out as the most dynamic growth market within the Europe customer journey analytics market through the forecast period.

Competitive Landscape

The Europe customer journey analytics market is moderately fragmented, with global enterprise software groups competing alongside cloud-built specialists that focus more narrowly on digital experience analytics. Large incumbents such as Adobe, Salesforce, Oracle, Microsoft, SAP, and IBM benefit from installed systems already in customer environments, which lowers switching pressure in large accounts. That advantage remains important because buyers often prefer to extend existing platforms when journey analytics can be added with less procurement friction. At the same time, specialist vendors such as Contentsquare, FullStory, Glassbox, Quantum Metric, Amplitude, and Mixpanel are gaining attention through faster release cycles and simpler deployment paths. This balance keeps the Europe customer journey analytics market competitive, because scale still matters, but speed of product execution matters more than before.

Adobe has been one of the clearest examples of platform expansion, with the B2B edition of Customer Journey Analytics in 2025, followed by CX Enterprise Coworker and Adobe CX Analytics in 2026.[4]Adobe, “Adobe Unveils CX Enterprise Coworker to Build Agentic-Enabled Workflows for Customer Experience Orchestration,” Adobe Newsroom, news.adobe.com Those moves show a strategy centered on linking measurement, AI assistance, and cross-functional action within a broader experience stack. Contentsquare has followed a different route, adding AI agent capabilities, a Snowflake Native App, a Dust integration, and a Claude connector across 2026.

FullStory added another strong example in June 2026, launching Model Context Protocol, StoryAI Agents, and Workflow Intelligence. These launches show that competition is moving toward warehouse-linked analytics, natural-language access, and autonomous monitoring, rather than relying solely on basic visualization. The Europe customer journey analytics market is also creating space for vendors that can meet EU data residency requirements while still delivering AI-led functionality at scale. That favors companies that can connect open architectures with stronger governance, because regulated buyers want flexibility without losing control over customer data. As a result, competitive pressure is likely to stay high, with incumbents defending broad suites and specialists pushing innovation through faster, more targeted product development.

Europe Customer Journey Analytics Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

Microsoft Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Contentsquare and Snowflake announced a strategic collaboration and the launch of the first Contentsquare Snowflake Native App on the Snowflake Marketplace. The native app enables category managers and merchandisers to analyze add-to-cart rates, conversion rates, and revenue data within Snowflake environments, advancing the adoption of composable analytics in retail and ecommerce.

- June 2026: Contentsquare integrated with Dust, an enterprise AI agent platform, enabling cross-functional use cases including quantified revenue-impact ranking of friction points and real-time error-spike triage via automated routing to product and operations teams. The integration expands behavioral data accessibility to non-technical stakeholders across organizations using Slack-based workflows.

- June 2026: FullStory launched three new solutions: FullStory Model Context Protocol (MCP), StoryAI Agents, and Workflow Intelligence, enabling AI-driven discovery, autonomous journey monitoring, and browser-based capture of hidden workflow inefficiencies in enterprise operations. StoryAI Agents replace manual data retrieval with autonomous intelligence, collapsing the feedback loop from discovery to execution.

- June 2026: Contentsquare became one of the first experience analytics solutions listed in Anthropic's Claude Connectors Directory, enabling teams to query customer experience data in natural language inside Claude with no technical setup. The integration allows AI agents to continuously monitor journey performance, identify conversion opportunities, and surface actionable insights.

Europe Customer Journey Analytics Market Report Scope

The Europe Customer Journey Analytics Market comprises software platforms and associated services that help organizations collect, analyze, visualize, and optimize customer interactions across multiple touchpoints and channels throughout the customer lifecycle. These solutions enable businesses to understand customer behavior, identify journey patterns, evaluate engagement effectiveness, and deliver personalized experiences across digital and physical channels. Growing adoption of omnichannel customer engagement strategies, increasing investments in advanced analytics and artificial intelligence, and rising demand for data-driven decision-making drive the market. These solutions help organizations improve customer acquisition, satisfaction, retention, and the overall customer experience.

The Europe Customer Journey Analytics Market Report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Application (Journey Mapping and Visualisation, Campaign and Journey Orchestration, Brand and Product Management, and Customer Behaviour and Attribution), End-User Enterprise Size (Large Enterprises, and Small and Mid-Size Enterprises), End-User Industry (Banking, Financial Services, and Insurance [BFSI], Retail and eCommerce, Information Technology and Telecom, Healthcare and Life-Sciences, Media and Entertainment, Travel and Hospitality, Automotive and Mobility, and Other End-User Industries), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Journey Mapping and Visualisation |

| Campaign and Journey Orchestration |

| Brand and Product Management |

| Customer Behaviour and Attribution |

| Large Enterprises |

| Small and Mid-Size Enterprises |

| Banking, Financial Services, and Insurance (BFSI) |

| Retail and eCommerce |

| Information Technology and Telecom |

| Healthcare and Life-Sciences |

| Media and Entertainment |

| Travel and Hospitality |

| Automotive and Mobility |

| Other End-User Industries |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Application | Journey Mapping and Visualisation |

| Campaign and Journey Orchestration | |

| Brand and Product Management | |

| Customer Behaviour and Attribution | |

| By End-User Enterprise Size | Large Enterprises |

| Small and Mid-Size Enterprises | |

| By End-User Industry | Banking, Financial Services, and Insurance (BFSI) |

| Retail and eCommerce | |

| Information Technology and Telecom | |

| Healthcare and Life-Sciences | |

| Media and Entertainment | |

| Travel and Hospitality | |

| Automotive and Mobility | |

| Other End-User Industries | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size outlook for the Europe customer journey analytics market?

The Europe customer journey analytics market size is projected at USD 4.81 billion in 2025, USD 5.75 billion in 2026, and USD 14.08 billion by 2031, with a 19.60% CAGR over 2026-2031.

Which segment leads by component in Europe customer journey analytics?

Solutions led the component mix with 68.44% revenue share in 2025, while services is set to grow faster at a 22.68% CAGR through 2031.

Why is cloud deployment leading in this space across Europe?

Cloud held 70.86% of deployment-mode revenue in 2025 because enterprises want scalable analytics, faster AI rollout, and lower infrastructure friction.

Which application area is growing the fastest in Europe customer journey analytics?

Campaign and Journey Orchestration is the fastest-growing application, with a projected 21.78% CAGR through 2031, while Journey Mapping and Visualisation remains the largest current segment.

Which country is driving the strongest growth across Europe?

Spain is projected to post the fastest growth at a 21.36% CAGR through 2031, supported by broad national digital investment and a widening SME buyer base.

Who are the main competitors in customer journey analytics across Europe?

The field includes large software vendors such as Adobe, Salesforce, Oracle, Microsoft, SAP, and IBM, along with specialists such as Contentsquare, FullStory, Glassbox, Quantum Metric, Amplitude, and Mixpanel.

Page last updated on: