Europe Construction And Demolition Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

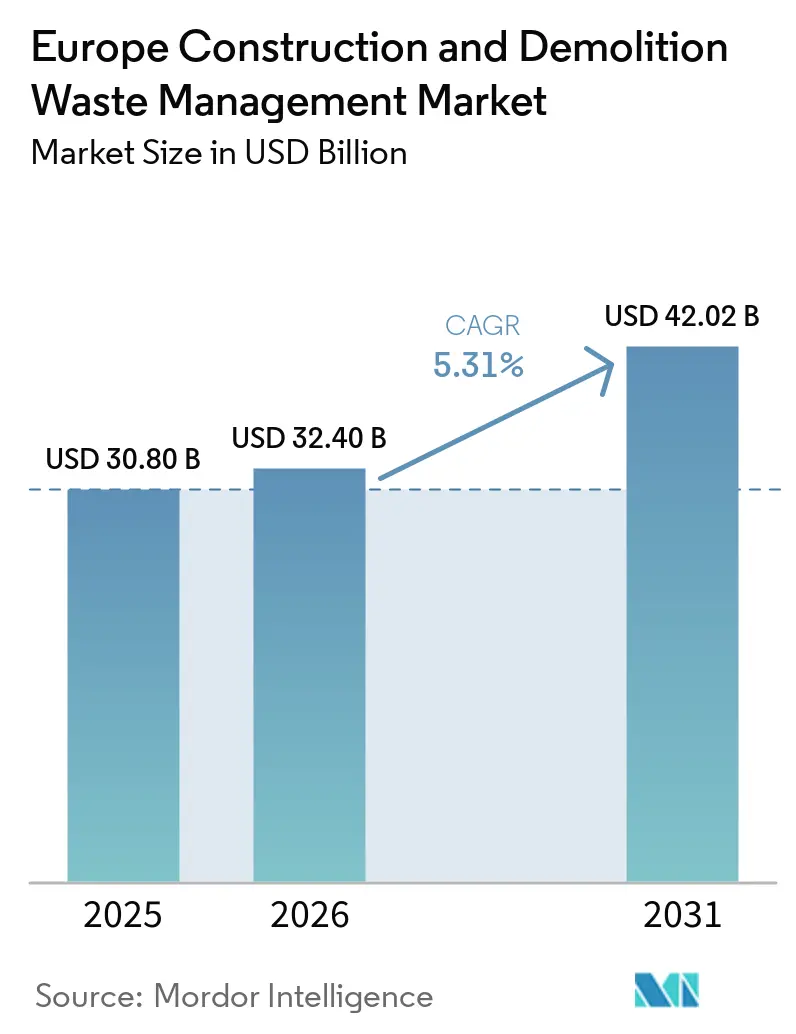

| Base Year Market Size (2025) | USD 30.80 Billion |

| Market Size (2026) | USD 32.40 Billion |

| Market Size (2031) | USD 42.02 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Construction And Demolition Waste Management Market Analysis by Mordor Intelligence

The Europe Construction And Demolition Waste Management Market size is expected to grow from USD 30.80 billion in 2025 to USD 32.40 billion in 2026 and is forecast to reach USD 42.02 billion by 2031 at 5.31% CAGR over 2026-2031.

Heightened regulatory pressure across the European Union, faster adoption of selective demolition, and growth in automated sorting are setting the near-term course for the Europe construction and demolition waste management market. Operators are improving material purity through robotics and image recognition, which supports higher value recovery and new end-use pathways. Vertical integration continues as materials producers expand into recycling to lock in feedstock for low-carbon product lines. Companies also compete on traceability and reporting performance because ESG-linked procurement and CSRD compliance now influence contract awards. A resilient project pipeline in renovations and urban regeneration is reinforcing stable, high-volume mineral flows across the region.

Key Report Takeaways

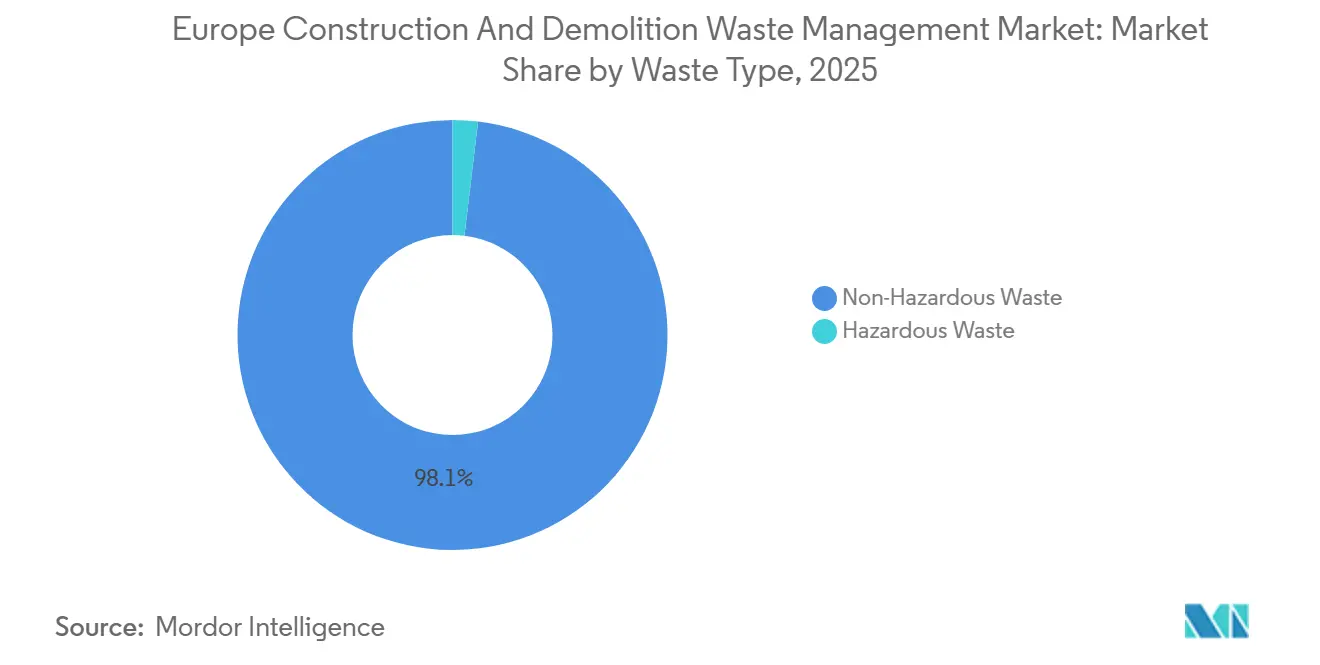

- By waste type, non-hazardous waste led with a 98.1% of the Europe construction and demolition waste management market share in 2025, while hazardous waste is projected to expand at a 6.2% CAGR through 2026-2031.

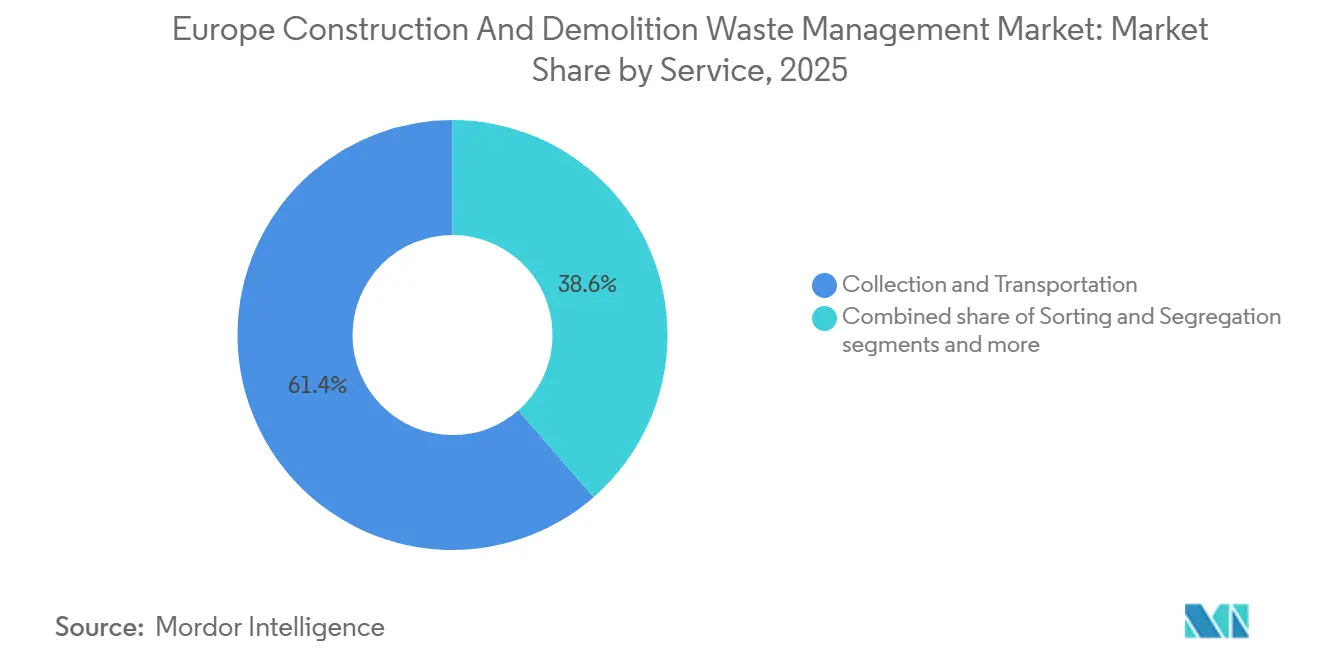

- By service line, collection and transportation accounted for 61.4% of Europe construction and demolition waste management market size in 2025, while sorting and segregation is projected to grow at a 5.8% CAGR through 2026-2031.

- By material, concrete and bricks held a 56.7% share of throughput in 2025, while gypsum and drywall are projected to grow at a 5.6% CAGR through 2026-2031.

- By geography, Germany commanded a 28.3% share in 2025, while the rest of Europe is projected to post the fastest growth at a 6.7% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Construction And Demolition Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate sustainability commitments and ESG reporting requirements are pushing waste reduction | +0.8% | Global, with early gains in Western Europe (UK, France, Germany, Netherlands) | Medium term (2-4 years) |

| Growing adoption of circular economy principles across the European construction sector | +1.2% | EU-wide, led by the Nordic and BENELUX regions | Long term (≥ 4 years) |

| Rising demand for recycled aggregates due to natural resource depletion and aggregate shortages | +1.0% | Central and Southern Europe (Germany, Poland, Spain, Italy) | Medium term (2-4 years) |

| Increasing infrastructure renovation and urban regeneration projects in aging European cities | +0.7% | EU core (France, Germany, Italy) and the UK | Medium term (2-4 years) |

| Technological advancements in automated sorting and AI-based waste segregation systems | +0.6% | Northern Europe (Denmark, Netherlands, Germany) with spillover to France, UK | Short term (≤ 2 years) |

| Rising construction activity driven by residential housing demand and green building initiatives | +0.9% | EU-wide, particularly Nordic, BENELUX, and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Sustainability Commitments and ESG Reporting Requirements Pushing Waste Reduction

The Corporate Sustainability Reporting Directive has increased disclosure requirements for large companies in 2024, emphasizing waste generation, recycling, and value chain impacts. Large contractors now prioritize waste diversion in performance systems and disclose waste flows, favoring verified recovery solutions. CRH reported 98% of its locations had waste management plans in 2024, recovering 44.7 million tonnes of waste and by-products. Balfour Beatty showed progress in its 2024 sustainability plan, with assured greenhouse gas disclosures boosting customer confidence in circular delivery. Financial access is shifting as verified waste and circularity data influence green financing eligibility. The Irish Green Building Council’s Home Performance Index integrates circularity into housing design, enhancing material recovery. France’s EPR organization for construction expanded professional deposit sites, improving collection and reporting for contractors across regions.

Growing Adoption of Circular Economy Principles Across the European Construction Sector

The EU’s Circular Material Use Rate reached 12.2% in 2024, reflecting gradual progress in secondary material usage.[1]European Environment Agency, “Circular material use rate in Europe,” European Environment Agency, eea.europa.eu Regions are implementing circular policies through mandates for separate collection, on-site sorting, and selective demolition. Flanders expanded mandatory sorting in 2024, requiring more material streams to be handled separately, improving feedstock quality for recyclers. Nordic countries enhanced building surveys and material mapping under new rules, increasing transparency of demolition flows. Denmark’s Solum facility showcased robotic sorting’s potential to improve purity and reduce emissions. The European Commission’s end-of-waste work for aggregates and other materials aims to harmonize definitions, enabling freer cross-border movement and scaling into higher-value applications. These developments strengthen market alignment with circular rules and raise standards for selective demolition and quality control.

Rising Demand for Recycled Aggregates Due to Natural Resource Depletion and Aggregate Shortages

Aggregate scarcity and tighter permitting have increased interest in recycled aggregates for road base, sub-base, and non-structural uses. UK data shows low replenishment rates for primary aggregates, driving substitution with recycled materials. Levy structures in some regions have made recycled options more competitive as landfill and extraction costs rise. Europe’s end-of-waste criteria for mineral waste streams aim to standardize specifications, boosting public procurement adoption. France’s programs fund upgrades and in-place recycling, promoting recycled aggregates in road construction.[2]Ministry for Ecological Transition France, “CiFREP 06/02/2025 Report,” Gouvernement Français, ecologie.gouv.fr Quality assurance remains key for structural uses, emphasizing selective demolition, audits, and sorting. Coordinated standards and verified data reduce buyer risk and support higher-value applications.

Increasing Infrastructure Renovation and Urban Regeneration Projects in Aging European Cities

The EU Renovation Wave and national retrofit programs have elevated demolition and refurbishment activity, which increases predictable mineral waste flows and creates repeatable recovery opportunities. The European Parliament projects millions of building units will require upgrades to meet climate goals, which drives demand for circular materials and construction methods that reduce embodied carbon and waste. Public roadmaps now include budgets for in-plant upgrades and specialized processing for mineral fractions, as well as actions to multiply in-place recycling that reduce transport intensity and emissions. Demonstration projects validate industrial approaches that reintegrate recovered fines into cement and concrete while reducing process emissions, which can scale when quality management systems and conformity checks are in place. Regeneration programs in Malta have advanced green public space and urban cooling goals, which underscores how municipal investments can align with circular procurement and material recovery.[3]Grand Harbour Regeneration Corporation, “Marsa Square Regeneration,” GHRC, ghrc.gov.mt The LIFE-funded Arec Reno project adds a multi-country proof point for deep renovation at the district scale using bio-based materials and innovative financing, which will expand learning on procurement, logistics, and material reuse models. These shifts sustain steady feedstock for processing plants and improve planning reliability for operators that link demolition schedules to recovery capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment for advanced waste processing facilities and equipment | -0.5% | EU-wide, particularly Eastern Europe and the Southern periphery | Short term (≤ 2 years) |

| Contamination issues are reducing the quality and market acceptance of recycled C&D materials | -0.4% | National, with acute challenges in Italy, Spain, and Greece | Medium term (2-4 years) |

| Lack of standardized quality specifications for recycled materials across EU member states | -0.3% | EU-wide, spill-over to the UK and EFTA states | Long term (≥ 4 years) |

| Fragmented waste collection infrastructure in Eastern European countries | -0.2% | Eastern Europe (Poland, Romania, Bulgaria, Czech Republic) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment for Advanced Waste Processing Facilities and Equipment

Shifting from manual to automated sorting requires significant capital that smaller operators struggle to finance. New deployments combine robotic systems with optical and hyperspectral imaging, which adds to upfront costs alongside systems integration. Danish evidence shows that robotic sorting can improve purity and lower emissions per tonne, but the pathway still demands coordinated funding and technical partnerships that smaller firms cannot easily secure. France’s policy support includes funding to increase recycling capacity for building materials, yet medium-term capacity build-out remains constrained by lead times and the need for robust quality management across plants. The Joint Research Centre finds that advanced C&D recycling methods can reduce life cycle emissions per tonne but still require new investments to close the processing gap across the EU. Where national frameworks update end-of-waste rules, operators must also invest in documentation and conformity assessment, which increases setup costs before monetization of higher-grade outputs begins. These realities favor well-capitalized firms or those with long-term supply contracts that de-risk repayment, which influences consolidation dynamics in the Europe construction and demolition waste management market.

Contamination Issues Reducing Quality and Market Acceptance of Recycled C&D Materials

Mixed waste streams that blend gypsum, plastics, and hazardous inclusions depress the quality of mineral fractions and limit reuse in higher-value applications. Evidence shows that much construction waste recovery still ends in low-grade uses, which underscores the need for stronger on-site segregation, selective demolition, and better plant-level sorting. France’s inter-ministerial commission signaled that while collection volumes are rising, gaps in territorial coverage and collection-point availability hinder consistent purity and increase the risk of illegal dumping. National requirements for pre-demolition audits improve planning for hazardous substances and material separation, yet their impact depends on enforcement and market access for sorted fractions. AI-driven sorting pilots in EU programs have shown high recognition accuracy for plastics and construction materials, which can support lower contamination rates at a commercial scale. Continued expansion of such pilots to industrial plants will be central to stabilizing quality and building end-user trust in recycled aggregates and gypsum. This will help shift more output from downcycling into reusable feedstock for concrete, cement, and certified gypsum board.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Non-Hazardous Dominates by Mass, Hazardous Gains Traction Through Regulatory Enforcement

The non-hazardous segment accounted for 98.1% of the Europe construction and demolition waste management market share in 2025, which reflects the mass dominance of mineral fractions in the regional waste mix. Across Europe, the built environment produces large volumes of concrete, brick, and asphalt flows that underpin throughput at processing sites, with annual C&D waste generation measured in the hundreds of millions of tonnes across the EU. Policy actions such as separate collection mandates and selective demolition protocols are raising the baseline for recovery and creating stable logistics for predictable material streams. France’s national roadmap sets aggressive targets for the separate collection of mineral waste by 2027, backed by national EPR implementation that helps standardize practice across regions. Under this policy environment, non-hazardous waste management is on a steady expansion path, with investments now targeting greater purity and higher-value outlets for recycled aggregates and other mineral derivatives.

Hazardous waste remains small by tonnage, yet it is gaining traction because pre-demolition audits and stricter handling rules are more common and better enforced. Member states with forward plans on asbestos removal and wood contamination are scaling up solutions to capture and treat this fraction under tighter supervision frameworks. Nordic countries have strengthened building surveys under new legal frameworks, which improves discovery and more reliable routing of hazardous fractions from rehabilitation projects. National requirements for documented handling under environmental management certifications also tighten data capture and governance for hazardous loads. In practice, hazardous material routing increases cost and time requirements per project and requires specialized logistics, which supports the business case for integrated operators with treatment capacity. This also materializes in contract structures that partition risk across the demolition and post-processing phases and align incentives for safety and compliance.

By Material: Concrete and Bricks Lead by Volume, Gypsum and Drywall Surge on Circular Loop Closures

Concrete and bricks held a 56.7% share of material throughput in 2025, driven by the mass of structural components in the European building stock. Plants are upgrading crushing, screening, and quality management to serve higher-value uses for recycled aggregates, including road base and selected non-structural concrete applications where standards allow. National programs in France are funding in-plant upgrades and five-fold increases in in-place recycling, which can raise recycled content in civil works and decrease transport dependence. Asphalt recycling remains mature, with extensive in-plant and in-place practices that support circular resurfacing and maintenance in many markets. For metals, existing scrap chains provide efficient, specification-grade outlets that remain the highest-value fraction among common construction materials, which underpins operator margins where ferrous and nonferrous content is recovered at scale. As quality assurance evolves, selective demolition and imaging-assisted sorting are improving mineral purity, which helps raise buyer confidence for more demanding end uses and reduces variability in product performance.

Gypsum and drywall are projected as the fastest-growing fraction with a 5.6% CAGR, supported by closed-loop initiatives and take-back systems that increase recycled content in board manufacturing lines. France’s EPR scheme continues to raise plasterboard recycling targets toward 2027, which helps build a predictable supply for manufacturer-led loops. Insulation take-back programs by manufacturers have expanded to Germany since 2024 and demonstrate how production can reincorporate high shares of site offcuts and post-consumer insulation into new materials. Robust documentation and product certification support premiums for verified recycled content, which strengthens economic incentives for more precise on-site sorting. Verified outputs and conformity assessments are increasingly required by public tenders and large private buyers, which reinforces material passporting and traceability across job sites. These advances support a steady pipeline of gypsum and mineral feedstock that can be certified and priced as higher-grade inputs, which lifts returns and contributes to segment-level growth of the Europe construction and demolition waste management market.

By Service: Collection and Transportation Dominate Cost Structures, Sorting Accelerates Through Automation

Collection and transportation accounted for 61.4% of the market value in 2025, driven by the logistics intensity of dispersive flows across building sites and infrastructure works. Country-level data confirm that building works generate significant volumes and rely on regional networks of collection points and haulers to route materials to treatment facilities. France’s network of EPR-backed deposit sites for professionals has expanded, although coverage gaps remain in several regions, which sustains transport inefficiencies and compliance risks. Digital solutions are becoming standard for route optimization, duty of care, and compliance reporting as national regulators mandate electronic tracking. The United Kingdom’s Digital Waste Tracking Service will make electronic waste transfer records mandatory from April 2026, which improves traceability for C&D flows and reduces fraudulent disposal risk. Operators that adopt digital forms and field data capture cut administrative tasks and improve audit readiness, which can become a competitive differentiator on large contracts. Market participants in several countries now integrate GPS-verified waste logistics and levy oversight to meet expanding taxation and reporting obligations in C&D waste.

Sorting and segregation are projected to grow at a 5.8% CAGR as facilities install robotic picking, hyperspectral sensors, and AI-enabled material recognition. Evidence from Denmark shows that robotic systems can reach high-purity outputs while lowering emissions per tonne, which eases downstream quality assurance and expands viable end uses. EU-funded pilots are developing self-learning robots for critical raw material recovery from mixed construction waste, which can preserve value and improve plant safety when batteries and electronics are detected accurately. Academic and industrial research confirms rapid improvements in pick rates and sorted-object accuracy, which points to steady reductions in contamination for facilities that adopt modern lines. Recovery and material processing continue to benefit from national end-of-waste updates that allow inert C&D outputs to exit waste status after specified recovery steps, with clear quality management and conformity declarations. Landfill taxes and updated operational standards make disposal an increasingly unattractive option, which pushes more flows into recovery and strengthens the case for investments in sorting and washing lines. These service-level shifts raise the role of automation and data to lift quality and compliance, which directly supports the Europe construction and demolition waste management market size as higher-purity outputs gain traction in public tenders.

Geography Analysis

Germany holds the largest national position with a 28.3% share in 2025, reflecting a dense recycling footprint and active policy frameworks that favor recovery. Western European markets, including France and the BENELUX countries, together account for a significant portion of demand due to established sorting mandates, high landfill levies, and capital programs that embed circularity into public works. France continues to scale its EPR-driven infrastructure for sorted construction waste and has introduced digital tools to register diagnostics and inventories upstream of project execution, which improves planning and market visibility for recyclers. The Netherlands and Belgium’s Flanders illustrate advanced circular practices through material passporting, coverage of mandatory sorting for additional streams, and active urban renewal that generates well-characterized mineral flows. Policy data show that the EU’s circular material use rate reached 12.2% in 2024, which is a useful benchmark for assessing the region’s progress toward a larger secondary materials economy. These advances reflect a broader convergence around high-quality recovery and traceability that supports the Europe construction and demolition waste management market.

Nordic countries are accelerating new compliance frameworks and pilots that extend beyond energy performance to material flows and circularity. Finland’s new Building Act, effective January 2025, requires mandatory construction and demolition waste surveys, which improve upstream transparency and enable earlier planning for reuse or recycling. Denmark’s robotic installations provide an operational model for high-purity outputs that ease downstream quality assurance and broaden end-use options for recycled aggregates. Sweden continues to refine national frameworks on waste taxation and reporting, which further disincentivize disposal and favor investment in sorting and processing. Norway’s public data confirm sizable flows of mineral and gypsum fractions within construction waste, which underscores the scale of circular opportunities in national markets with maturing collection and processing capacity. The cumulative effect is a steady increase in advanced recovery capacity and higher-quality outputs, which influence regional competition and investment priorities.

Eastern and Southern Europe are growing faster from a lower base as policy harmonization and EU funds expand collection and processing coverage. The Rest of Europe group, which includes Eastern markets, is projected to post the fastest growth at a 6.7% CAGR through 2031 as greenfield capacity and selective demolition practices scale. Municipal regeneration programs in Malta, supported by national development entities, are strengthening the pipeline of projects that align with circular procurement and green space targets. EU programs that fund pilots for robotic and AI-enabled sorting in Spain, Portugal, and Greece will help translate demonstrations into industrial deployments over the medium term. The UK is aligning digital tracking requirements from April 2026, which is expected to fortify the duty of care and improve national waste intelligence in construction flows. Germany’s leadership position anchors cross-border flows of know-how on selective demolition and processing, which will continue to inform upgrades in adjacent markets. Together, these developments lift the Europe construction and demolition waste management market by broadening compliant feedstock and improving the economics for recovery.

Competitive Landscape

The Europe construction and demolition waste management market is shifting from localized, service-centric operations to integrated systems that marry logistics, processing, and end-market activation. Large materials producers are pursuing vertical integration to secure recycled feedstock for low-carbon cements and concretes, which stabilizes supply for circular product lines. CRH disclosed that it maintained near-universal waste plans across operating sites and recovered tens of millions of tonnes of by-products in 2024, which signals the scale of internal loops and supplier partnerships among leading producers. Etex and Heidelberg Materials Benelux are collaborating on CEMLOOP XL, a project to turn fibre cement waste into carbonated, low-carbon inputs for cement lines, with key assets scheduled for commissioning by 2026 and 2028. These moves indicate a tighter coupling of demolition streams with cement and concrete product innovation that can meet public procurement requirements for recycled content.

Waste management incumbents continue to expand digital capabilities that track flows and verify compliance to support CSRD reporting and contracting. France’s EPR-backed Ecomaison network has scaled professional collection points for sorted construction waste, which simplifies participation for contractors and improves traceability of mineral and non-mineral fractions. Digital passporting and material tracking tools, such as those offered by platforms in the Netherlands, help contractors and recyclers identify reuse potential and quantify carbon savings, which reinforces the business case for circular procurement. In the UK, the government’s digital tracking mandate for April 2026 has catalyzed ecosystem moves by technology providers and operators to integrate electronic records into everyday logistics, which improves audit trails and reduces reporting burdens for haulers. These developments privilege operators that combine collection reach, processing scale, and verifiable data systems.

Technology suppliers are reshaping plant economics with robotic picking and AI-driven recognition that elevate output purity and throughput. Denmark’s Solum plant demonstrates that automated lines can deliver up to 90% purity and material-specific gains in CO₂ performance compared to manual methods, which allows facility managers to qualify more high-grade outputs. EU-funded pilots continue to advance robotic perception and manipulation for critical raw materials and mixed C&D streams, which supports the recovery of valuable fractions and reduces fire risks from embedded batteries and electronics. The EU’s updated Construction and Demolition Waste Management Protocol also reinforces selective demolition, quality management, and transparency, which complements technological adoption and helps market-makers standardize best practices across borders. Together, these strategic moves point toward a more data-driven, quality-assured operating model that can lift margins for recovered materials across the Europe construction and demolition waste management market.

Europe Construction And Demolition Waste Management Industry Leaders

ARJES

Biffa

Bywaters

CDE Group

CFlo World Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The European Commission announced the European Affordable Housing Plan to mobilize investments and improve housing supply with sustainability at the core, including the use of the Level(s) framework to align circular construction and energy performance in neighborhood regeneration initiatives.

- November 2025: The EU LIFE-funded Arec Reno project launched to drive district-scale deep renovation using bio-based materials, collective procurement, and innovative financing across six countries, with upgrades targeting net-zero energy performance

- October 2025: Etex and Heidelberg Materials Benelux unveiled the CEMLOOP XL project, targeting a fully closed-loop pathway for fibre cement waste with key assets scheduled for mid-2026 and end-2028, enabling low-carbon cement with recycled inputs

Europe Construction And Demolition Waste Management Market Report Scope

The Europe Construction and Demolition Waste Management Market is Segmented by Waste Type (Non-Hazardous Waste, and Hazardous Waste), by Material (Concrete & Bricks, Asphalt, Metal, Timber, Soil and Sand, Gypsum & Drywall, and Others), by Service (Collection & Transportation, Sorting & Segregation, Recycling & Material Recovery, and Landfilling & Disposal), and by Geography (United Kingdom, Germany, France, Italy, Spain, BENELUX, NORDICS, and Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

| Non-Hazardous Waste |

| Hazardous Waste |

| Concrete & Bricks |

| Asphalt |

| Metal |

| Timber |

| Soil and Sand |

| Gypsum & Drywall |

| Others (Plastic, Wood, Glass) |

| Collection & Transportation |

| Sorting & Segregation |

| Recycling & Material Recovery |

| Landfilling & Disposal |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Waste Type | Non-Hazardous Waste |

| Hazardous Waste | |

| By Material | Concrete & Bricks |

| Asphalt | |

| Metal | |

| Timber | |

| Soil and Sand | |

| Gypsum & Drywall | |

| Others (Plastic, Wood, Glass) | |

| By Service | Collection & Transportation |

| Sorting & Segregation | |

| Recycling & Material Recovery | |

| Landfilling & Disposal | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe construction and demolition waste management market?

The Europe construction and demolition waste management market size was valued at USD 30.8 billion in 2025 and is projected to grow from USD 32.4 billion in 2026 to USD 42 billion by 2031, at a 5.31% CAGR.

Which segments are leading and which are growing the fastest within Europe construction and demolition waste management?

In 2025, non-hazardous waste led by share at 98.1% and hazardous waste is the fastest-growing at a 6.2% CAGR; collection and transportation led by value at 61.4% while sorting and segregation is projected to grow at a 5.8% CAGR; concrete and bricks led by throughput at 56.7% while gypsum and drywall is projected to grow at a 5.6% CAGR; Germany led by share at 28.3%, while Rest of Europe is projected to grow the fastest at a 6.7% CAGR.

How are regulations shaping the trajectory of Europe construction and demolition waste management?

EU-level circularity initiatives, end-of-waste work, and national mandates for separate collection, pre-demolition audits, and digital tracking are tightening quality, traceability, and recovery performance, boosting adoption of selective demolition and advanced sorting.

What technologies are improving material recovery outcomes in Europe construction and demolition waste management?

AI-enabled sorting, hyperspectral imaging, and robotic pickers are delivering higher purity and better throughput; Denmark’s Solum facility demonstrates high-purity outputs and lower emissions per tonne compared to manual sorting.

Which countries are most influential for Europe construction and demolition waste management today?

Germany leads by share 28.3%, Western Europe deploys mature regulatory and processing frameworks, Nordic countries are scaling robotic sorting and new building rules, and Rest of Europe is projected to grow the fastest through 2031 due to harmonization and capacity build-outs.

What is driving demand for recycled aggregates within Europe construction and demolition waste management?

Constrained primary aggregate replenishment and levies that raise the competitiveness of recycled materials are boosting uptake, while EU efforts on end-of-waste criteria and national funding for in-plant and in-place recycling are opening higher-value uses.

Page last updated on: