Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

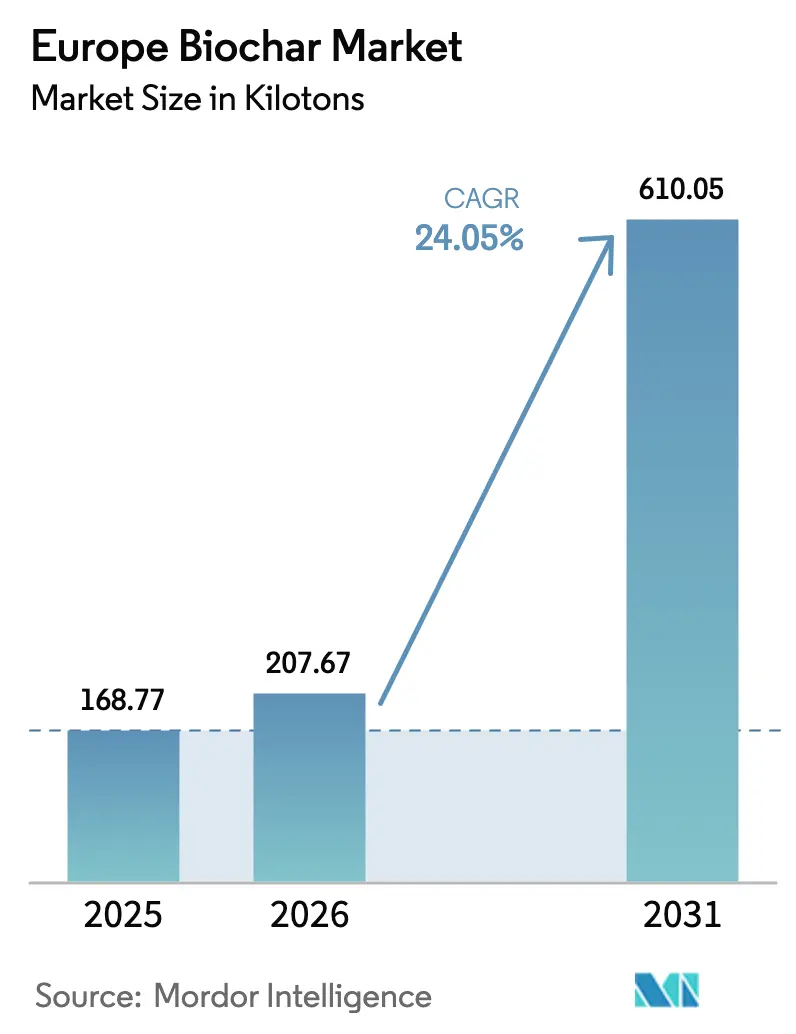

| Base Year Market Size (2025) | 168.77 kilotons |

| Market Volume (2026) | 207.67 kilotons |

| Market Volume (2031) | 610.05 kilotons |

| Growth Rate (2026 - 2031) | 24.05% CAGR |

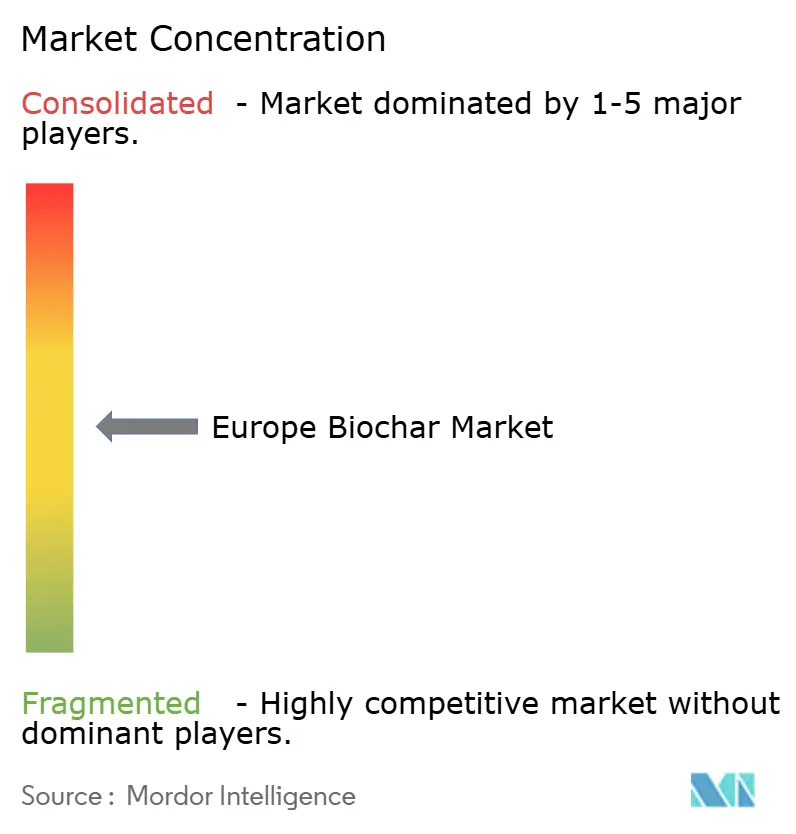

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Biochar Market Analysis by Mordor Intelligence

The Europe Biochar Market size was valued at 168.77 kilotons in 2025 and is estimated to grow from 207.67 kilotons in 2026 to reach 610.05 kilotons by 2031, at a CAGR of 24.05% during the forecast period (2026-2031). Market momentum is shifting from pilot projects to industrial deployment as the European Union’s carbon-removal mandates, the revised Emissions Trading System, and the inclusion of biochar in the EU Fertilising Products Regulation (CMC14) collectively formalize demand. Germany’s district-heating networks, the United Kingdom’s sewage-sludge valorization plans, and Nordic forestry residues anchor regional scale-up, while corporate prepaid carbon-credit deals de-risk new capacity. Technology choice is consolidating around modular pyrolysis reactors that integrate with existing biomass streams at lower capital intensity than gasifiers. Feed-additive use in livestock, cement and steel substitution, and phosphorus-rich char from municipal sludge diversify revenue, but fragmented biomass logistics and the absence of pan-EU agronomic field-rate guidance temper near-term adoption.

Key Report Takeaways

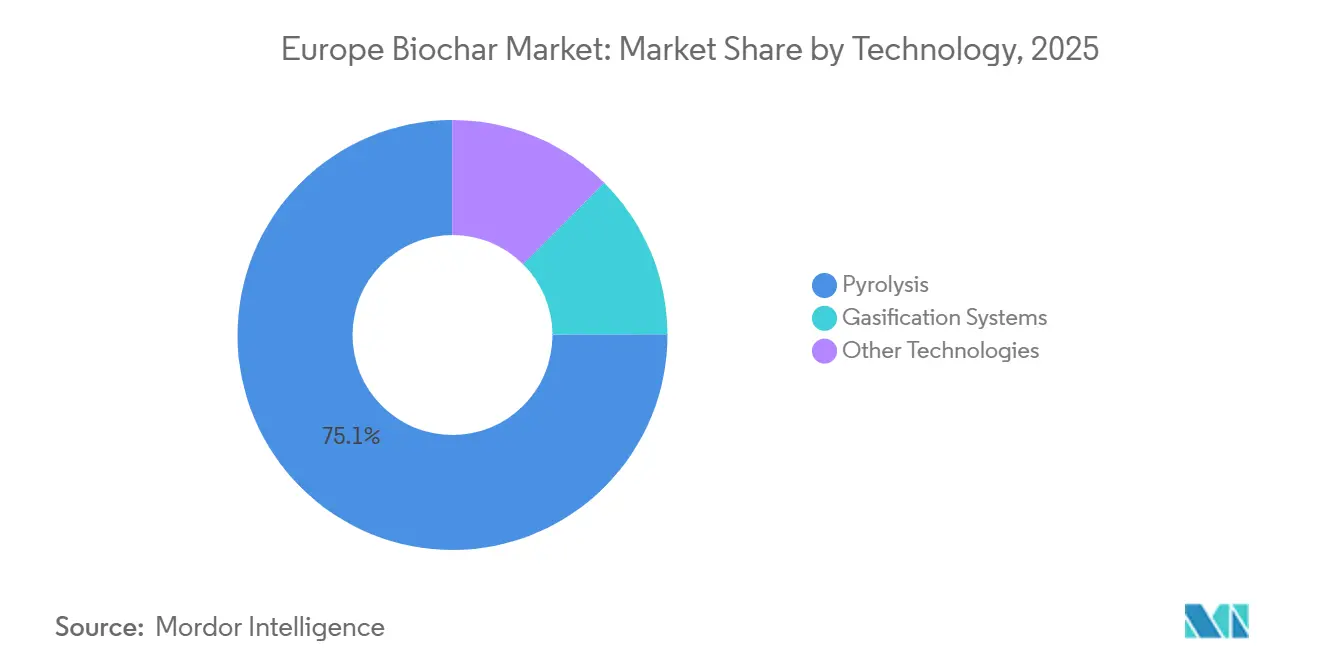

- By technology, pyrolysis held 75.06% of the Europe biochar market share in 2025 and is advancing at a 24.55% CAGR through 2031.

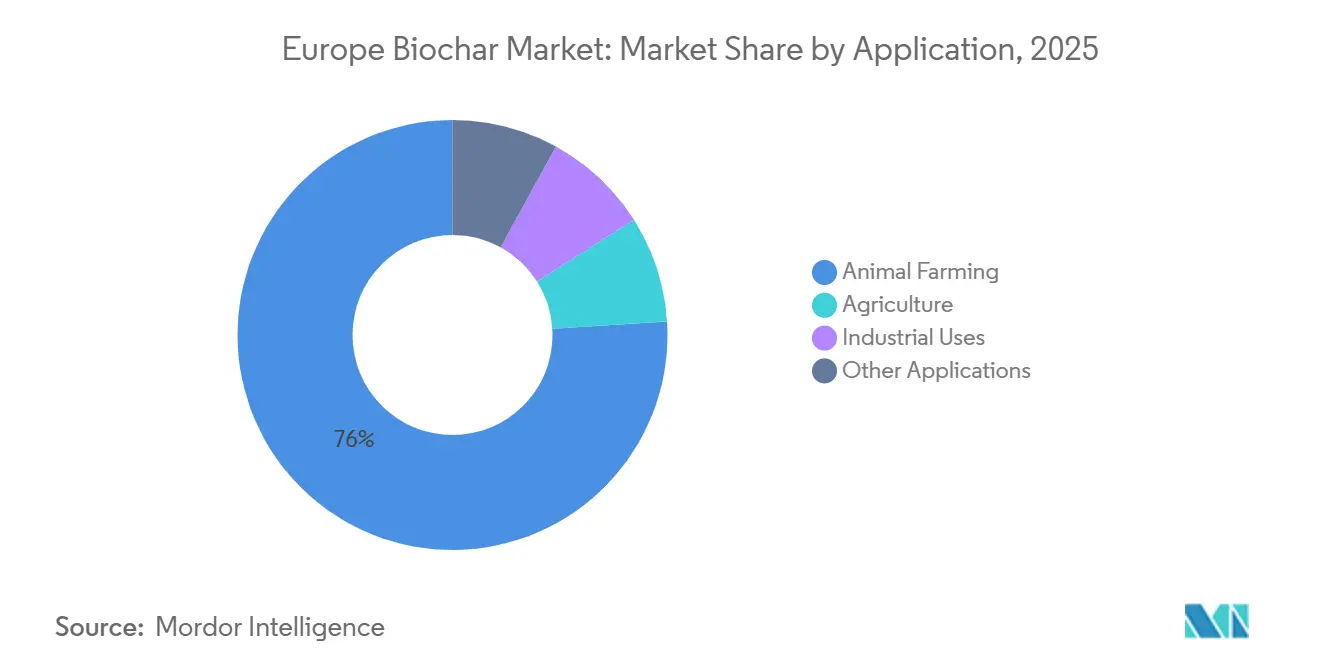

- By application, animal farming accounted for 75.99% of the Europe biochar market size in 2025, while industrial uses are projected to grow at a 26.10% CAGR to 2031.

- By geography, Germany led with 29.47% of the Europe biochar market share in 2025 and is forecast to rise at a 24.51% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Biochar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU regenerative & organic-farming demand surge | +6.2% | Germany, France, Italy, Nordic countries | Medium term (2-4 years) |

| Scale-up of carbon-credit purchase agreements | +5.8% | Global, with concentration in Germany, UK, Nordic | Short term (≤ 2 years) |

| Inclusion of CMC14 biochar in EU Fertilising Products Regulation | +4.5% | Pan-European, early gains in Germany, France, Netherlands | Medium term (2-4 years) |

| Industrial heat-recovery economics from district-heating pyrolysis | +3.9% | Germany, Nordic countries, Austria | Long term (≥ 4 years) |

| Biochar-enabled phosphorus recycling from sewage-sludge streams | +2.7% | UK, Germany, Netherlands, Nordic municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Regenerative & Organic-Farming Demand Surge

Organic and regenerative agriculture programs funded under the EU Common Agricultural Policy allocate EUR 8.1 billion for 2023-2027, and biochar qualifies as a subsidized soil amendment under Eco-Schemes. France expanded organic acreage by 11% in 2024 and documented cereal and vineyard yield gains of 15%-22% when biochar was applied under drought stress, prompting its Ministry of Agriculture to embed biochar in the national soil-health roadmap[1]French Ministry of Agriculture, “National Soil-Health Strategy Incorporating Biochar,” AGRICULTURE.GOUV.FR. Germany launched a EUR 50 million demonstration covering 500 farms in 2025 to validate sequestration and fine-tune field protocols. While subsidies pull demand forward, inconsistent agronomic guidelines on particle size, feedstock origin, and crop-specific rates create variable field results that slow mainstream adoption. Italy and Spain lag because biochar still carries an experimental classification until domestic law fully transposes EU Regulation 2019/2783.

Scale-Up of Carbon-Credit Purchase Agreements

Voluntary buyers procured 47,000 biochar removal certificates in 2024, up 161% year over year, at EUR 150-200 per t of CO₂e, as corporates such as Microsoft, Shopify, and Stripe prioritized durable removals[2]Puro.earth, “Biochar Carbon Removal Certificates 2024,” PURO.EARTH. NOVOCARBO locked a 10-year, 100,000-ton offtake with a Swiss reinsurer in 2025, securing EUR 18 million in advance revenue that financed a 12 kt plant in Brandenburg. European Biochar Certificate (EBC) audits now accompany 89% of issuances, tightening quality and permanence standards. Pricing remains volatile; spot values fell 22% in late 2025 amid scrutiny of durability claims, so producers without long-term contracts face margin pressure. Forthcoming EU Carbon Removal Certification, slated for 2026, is expected to raise monitoring and verification thresholds, advantaging integrated players with in-house analytics.

Inclusion of CMC14 Biochar in EU Fertilising Products Regulation

EU Regulation 2019/2783 allows biochar meeting carbon and contaminant limits to circulate freely across member states as CMC14 material. Germany clarified that char derived from forestry or green waste qualifies automatically, while treated wood or sludge feedstocks need extra dioxin tests. The Netherlands transposed CMC14 in early 2025, opening 1.8 million ha of arable land and triggering a 34% rise in imports from Germany and Austria. France and Italy lag in transposition, creating a two-speed market where certified biochar commands 30%-40% price premiums in early-adopter countries. Producers investing in blockchain-based traceability mitigate the risk of cross-border shipment rejection.

Industrial Heat-Recovery Economics from District-Heating Pyrolysis

District-heating networks retrofit pyrolysis units that convert forestry and agricultural residues into biochar while capturing high-grade heat for buildings, achieving system efficiencies above 80%. PYREG’s 3 kt plant in Dörth supplies 2.5 MWth to a local grid and generates EUR 1.2 million in annual heat sales in addition to biochar revenue. Finland’s Carbon Finland reports a 4.8-year payback for a comparable installation when sited within 5 km of heat demand. Germany’s Building Energy Act now requires new district heating to source at least 50% renewable energy by 2030, boosting project pipelines. Capital costs of EUR 3-5 million for a 2 kt unit with heat exchangers limit deployment to municipalities with investment-grade credit or EU cohesion funds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented EU biomass-waste logistics inflate feedstock costs | -3.80% | Pan-European, acute in Southern and Eastern regions (Spain, Italy, Poland) | Short term (≤ 2 years) |

| Absence of pan-EU agronomic guidelines for biochar field-rates | -2.10% | Germany, France, Italy, Spain, with spillover to Central Europe | Medium term (2-4 years) |

| Potential long-term PAH / heavy-metal liability for non-certified char | -1.90% | Pan-European, concentrated in markets with untreated wood or contaminated feedstocks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented EU Biomass-Waste Logistics Inflate Feedstock Costs

Feedstock costs swing from EUR 35/t for Nordic forestry residues to EUR 90/t for Southern European agricultural waste because collection and drying infrastructure is patchy. Only 38% of German agricultural residues were utilized industrially in 2024, with the remainder burned or left in the field. Olive-pruning residues in Spain and Italy are scattered across smallholder farms, and transport beyond 80 km often renders biochar production uneconomic. Mobile pyrolysis units piloted by France’s INRAE in 2025 cut feedstock expense 42% but carry a EUR 1.8 million capex that suits only well-capitalized cooperatives. The EU Biomass Mobilisation Strategy will co-fund aggregation hubs from 2026, yet meaningful relief may not arrive until 2028.

Absence of Pan-EU Agronomic Guidelines for Biochar Field-Rates

Safety thresholds under CMC14 do not specify application rates or incorporation depth, forcing farmers to rely on inconsistent supplier advice. Germany’s Thünen Institute suggests 5-10 t/ha for sandy soils but lacks cross-climate validation. French trials show that above 15 t/ha biochar can immobilize nitrogen and cut first-year yields by 8%-12%. The UK’s 2025 calculator covers only 12 crop-soil combinations and remains un-peer-reviewed. Absent harmonized protocols, auditors add 20%-30% to monitoring costs, eroding net carbon-credit value and slowing uptake among risk-averse growers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Pyrolysis Dominates on Modularity and Feedstock Flexibility

Pyrolysis controlled 75.06% of the 2025 Europe biochar market share, and its portion of the Europe biochar market size is forecast to grow at a 24.55% CAGR through 2031. Continuous-feed reactors such as PYREG’s P500 and P1500 process moisture-tolerant mixed residues at lower oxygen and temperature control requirements than gasifiers, slashing installation timelines to nine months and dropping per-ton capex by 28% between 2022 and 2025.

Gasification systems remain niche but appeal to integrated pulp, paper, and sawmill sites where syngas co-production offsets higher capex; Bussme Energy’s downdraft units in Sweden attain 85% thermal efficiency and attract mills targeting fossil fuel substitution. Hydrothermal carbonization and microwave pyrolysis remain at pilot scale due to high energy demand and limited feedstock compatibility. Regulatory regimes are technology-neutral, but pyrolysis plants have captured 92% of EBC certifications because of superior feedstock tolerance and consistent carbon stability.

By Application: Animal Farming Leads, Industrial Uses Accelerate

Animal farming absorbed 75.99% of the 2025 volume within the Europe biochar market, leveraging feed inclusion at 1%-3% to curb enteric methane by up to 18% in dairy herds. Subsidized trials under Germany’s Farm to Fork roadmap enrolled 14,000 cattle and 87,000 pigs during 2024-2025, validating emissions and gut-health benefits.

Industrial uses, though a smaller slice of the Europe biochar market size, are growing at 26.10% CAGR as cement and steel producers face embedded-carbon levies from the EU Carbon Border Adjustment Mechanism starting in 2026. Heidelberg Materials’ 2024 kiln test cut clinker CO₂ intensity by 9% without sacrificing compressive strength and is slated for replication at three plants in 2026. Agricultural soil-amendment demand is steadily rising in drought-prone viticulture and horticulture, but high upfront costs still deter broad arable uptake.

Geography Analysis

Germany anchors the Europe biochar market size at 29.47% of 2025 volume and is on track for a 24.51% CAGR through 2031, propelled by federal subsidies, dense district-heating grids, and leadership in EBC certification. Municipal utilities source forestry and green-waste feedstocks locally, keeping delivered costs below EUR 45/t and enabling sub-EUR 200/t biochar production.

The United Kingdom is a fast adopter as water utilities convert sewage sludge into phosphorus-rich char and as corporate buyers such as Lloyds Banking Group lock long-term carbon-credit agreements. Volume from sludge char is forecast to jump when the expected 2028 phosphorus-recovery mandate takes effect, expanding the UK share of the Europe biochar market to the high teens by 2031.

Nordic countries leverage integrated forestry complexes that supply low-cost residues and district-heating off-take, keeping feedstock costs near EUR 35/t. France shows robust momentum in organic viticulture and Eco-Scheme-backed cereals, yet national transposition delays of CMC14 temper full commercial rollout. Italy and Spain lag amid fragmented residue aggregation, but pilot olive-pomace projects could unlock 50-70 kt of annual capacity if logistics hubs mature post-2028.

Competitive Landscape

The Europe Biochar market is moderately fragmented. Vertically integrated strategies dominate: PYREG manufactures reactors and offers toll production; NOVOCARBO secures long-dated municipal feedstock contracts and co-locates at biomass power plants; Carbofex pairs pyrolysis with Finnish pulp-mill residues to lock sub-EUR 180/t costs. Smaller entrants leverage prepaid carbon-credit revenue to scale. The Europe biochar industry balances a maturing core of integrated incumbents, a pipeline of specialty-technology challengers, and a long tail of regional batch units confronting rising certification and feedstock reliability hurdles.

Europe Biochar Industry Leaders

Airex Energy

Carbofex Ltd

NOVOCARBO GMBH

PYREG GmbH

Sonnenerde GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Varaha ClimateAg Private Limited launched its Varaha Industrial Partners Program (VIPP), a global initiative enabling biomass processing plants to access sustainable feedstock. The program's first collaboration, with Revata Carbon and Valency International, will focus on an industrial biochar carbon removal project in Côte d’Ivoire.

- May 2024: The International Biochar Initiative and the European-based Certified Sustainable Biochar Initiative have merged their certification standards, aligning biochar quality requirements across regions to streamline certification processes and enhance market transparency for European producers and buyers.

Europe Biochar Market Report Scope

Biochar is a charcoal-like substance that burns organic material from agricultural and forest wastes through pyrolysis. Adding biochar to soil enhances fertility, improves water retention, and can sequester carbon, benefiting both agriculture and the environment.

The European biochar market is segmented by technology, application, and geography. By technology, the market is segmented into pyrolysis, gasification systems, and other technologies (microwave pyrolysis, traditional kilns). By application, the market is segmented into agriculture, animal farming, industrial uses, and other applications (water filtration and renewable energy). The report also covers market sizes and forecasts for the biochar market in 7 countries across Europe. The market sizes and forecasts are provided for each segment based on volume (tons).

Technology

| Pyrolysis |

| Gasification Systems |

| Other Technologies |

Application

| Agriculture |

| Animal Farming |

| Industrial Uses |

| Other Applications |

Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Nordic Countries |

| Turkey |

| Russia |

| Rest of Europe |

| Technology | Pyrolysis |

| Gasification Systems | |

| Other Technologies | |

| Application | Agriculture |

| Animal Farming | |

| Industrial Uses | |

| Other Applications | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is the Europe biochar market expected to grow to 2031?

It is forecast to expand from 207.67 kilotons in 2026 to 610.05 kilotons in 2031 at a 24.05% CAGR.

Which technology leads current production?

Modular pyrolysis reactors held 75.06% of 2025 volume due to feedstock flexibility and faster installation.

Why does animal farming dominate demand?

Livestock producers use biochar feed additives to cut methane up to 18% and qualify for carbon credits, accounting for 75.99% of 2025 volume.

Which countries are scaling the fastest?

Germany remains largest, while the United Kingdom and Nordic nations show the highest near-term growth as they deploy sewage-sludge and forestry-linked projects.

What restrains wider agricultural use today?

High feedstock logistics costs and the lack of EU-wide agronomic field-rate guidelines both increase risk for conventional crop farmers.

Page last updated on: