Europe Bariatric Surgery Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.32 Billion |

| Market Size (2030) | USD 1.72 Billion |

| Growth Rate (2025 - 2030) | 5.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bariatric Surgery Devices Market Analysis by Mordor Intelligence

The Europe bariatric surgery devices market is valued at USD 1.32 billion in 2025 and is projected to reach USD 1.72 billion by 2030, expanding at a 5.46% CAGR over the forecast period. Sleeve gastrectomy retains procedural dominance because of shorter operating times and lower complication rates, and new endoscopic sleeve gastroplasty (ESG) techniques received a reimbursement tail-wind after NICE approval under IPG783 in 2024. Hospitals and specialty clinics still perform most operations, yet day-case pathways are spreading quickly as Dutch centers documented 93% same-day discharge with <2% major complications. Competitive intensity remains moderate; Intuitive Surgical’s installed base of 10,600 robotic systems gives it scale, but European manufacturers such as KARL STORZ and CMR Surgical are fielding lower-cost modular robots that resonate with budget-pressed hospitals.

Key Report Takeaways

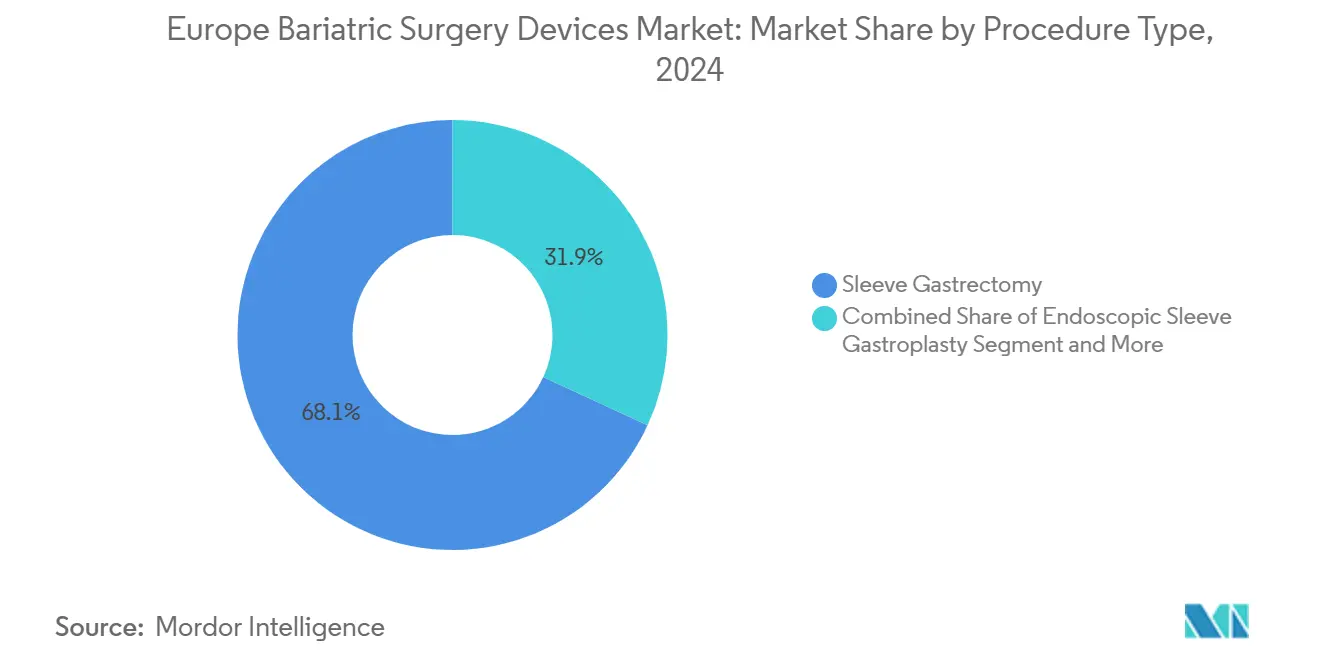

- By procedure type, sleeve gastrectomy accounted for 68.12% of 2024 revenue and Endoscopic Sleeve Gastroplasty projected to grow at 7.6% CAGR of the Europe bariatric surgery devices market by 2030.

- By device type, staplers and related suturing systems held 58.1% of the Europe bariatric surgery devices market size in 2024, while implantable balloons and stimulators are projected to grow at an 8.8% CAGR to 2030.

- By end user, hospitals and specialty clinics commanded 68.4% of 2024 revenue; ambulatory surgical centers represent the fastest-growing channel, rising at an 8.7% CAGR through 2030.

- By patient age group, adults 18-64 years represented 46.5% of 2024 volume; adolescent procedures are increasing at an 7.7% CAGR during 2025-2030.

- By country, Germany generated 36.5% of regional revenue in 2024, whereas Spain is forecast to post the fastest 7.2% CAGR over 2025-2030 as regional health authorities scale capacity.

Europe Bariatric Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating obesity and metabolic syndrome prevalence | +1.2% | EU-5 core, spreading to Central and Eastern Europe | Long term (≥ 4 years) |

| Preference for minimally-invasive and day-care procedures | +0.8% | Netherlands, UK, France leading; Spain and Italy adopting | Medium term (2-4 years) |

| Enhanced reimbursement across major EU-5 | +1.0% | UK (NICE NG246), France (HAS 2024), Germany (Hospital Reform Act 2024) | Medium term (2-4 years) |

| Employer-sponsored bariatric coverage and wellness programs | +0.2% | Limited to multinational corporations in Germany, UK | Long term (≥ 4 years) |

| Hospital uptake of robotic and endoluminal platforms | +0.7% | Germany, UK, France (tertiary centers); Italy (regional hubs) | Short term (≤ 2 years) |

| Proven cost-effectiveness versus chronic GLP-1 therapy | +0.9% | EU-5 with restricted GLP-1 reimbursement (Germany, Italy, Spain) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Obesity and Metabolic Syndrome Prevalence

WHO Europe attributes over 1.2 million annual deaths to obesity, and Eurostat placed 50.6% of adults in the overweight or obese category during 2022[1]World Health Organization, “Obesity and Overweight,” who.int. The 2022 ASMBS/IFSO guidelines broadened surgical eligibility to any patient with BMI > 35 kg/m², doubling the potential pool. Italy’s Emilia-Romagna region recently instituted a three-tier care model that routes candidates from preventive clinics to accredited surgery centers, illustrating how regional policies convert latent need into device demand. Because only 4% of EU health budgets target prevention, downstream interventional spend, including on staplers, trocars, and balloons, should stay resilient over the long term.

Preference for Minimally-Invasive and Day-Care Procedures

A January 2023 Dutch cohort of 500 Roux-en-Y patients achieved 93% same-day discharge, <2% severe complications, and zero mortality, aligning bariatric risk with routine cholecystectomy. Comparable French data on sleeve gastrectomy showed 85.2% protocol adherence and 96.8% patient satisfaction, with per-case savings of up to 43%. Device makers responded: Olympus released the THUNDERBEAT energy platform in May 2025, and Creo Medical’s SpydrBlade Flex gained EU clearance in March 2025, both designed to speed laparoscopic or endoluminal workflows.

Enhanced Reimbursement Across Major EU-5

NICE guideline NG246 (2025) scrapped the tier-3 weight-management prerequisite, directly shrinking UK wait lists, and IPG783 opened ESG reimbursement for the first time[2]National Institute for Health and Care Excellence, “Guideline NG246,” nice.org.uk. France refreshed adult obesity pathways in February 2024, embedding multidisciplinary follow-up that locks in device utilization over time. Germany’s Hospital Care Reform Act funnels a EUR 50 billion transformation fund into high-volume centers between 2026 and 2035, though heterogeneous insurer policies still suppress procedure counts relative to peers.

Hospital Uptake of Robotic and Endoluminal Platforms

Intuitive Surgical logged >80,000 global robotic bariatric cases in 2024, helped by the da Vinci SP system’s new CE mark. German vendor KARL STORZ countered by acquiring Asensus Surgical and its Senhance robot in August 2024. Boston Scientific’s OverStitch NXT, validated by 13.6% total body-weight loss at 12 months, extends endoscopic revenue opportunities across primary and revisional procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront procedure and device costs | -0.4% | Central and Eastern Europe, southern EU (Italy, Spain) with elevated out-of-pocket costs | Medium term (2-4 years) |

| Post-operative complications and follow-up burden | -0.5% | EU-5 core; higher impact in regions with limited multidisciplinary infrastructure (Rest of Europe) | Long term (≥ 4 years) |

| Uptake of GLP-1 weight-loss medications | -1.0% | Germany, UK, France (private-pay segments); limited public reimbursement tempers impact | Short term (≤ 2 years) |

| Shortage of accredited surgeons and center-volume requirements | -0.6% | Germany (72 procedures/million vs France 571/million), Spain, Italy (regional concentration), Rest of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Procedure and Device Costs

France does not reimburse gastric balloon placement, leaving patients to cover roughly EUR 3,000 out-of-pocket, and mutual-insurance caps often sit near EUR 200, dissuading uptake. Central and Eastern European systems levy similar co-pays and face workforce scarcities, slowing adoption even when clinical need is evident. Staple-line reinforcement cuts leak rates by 30% but adds cost that some payers currently decline, exemplifying the price-efficacy tension.

Uptake of GLP-1 Weight-Loss Medications

Semaglutide and tirzepatide generate 14-20% weight loss, narrowing the efficacy gap versus surgery, and Roche committed up to USD 5.3 billion in 2025 to co-develop next-generation peptides with Zealand Pharma. Yet Germany excludes GLP-1 coverage, and UK, France, and Spain restrict access to narrow diabetes cohorts, keeping surgery the only reimbursed option for most obese patients. Device manufacturers therefore retain a protected revenue base despite rising prescription volumes in private-pay segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Sleeve Gastrectomy Maintains Dominance

Sleeve gastrectomy secured 68.12% of 2024 procedures, translating to the largest share of the Europe bariatric surgery devices market. Clinical simplicity—no anastomoses and shorter operating times—keeps leak and bleeding rates low, qualities that resonate with day-case ambitions. Roux-en-Y gastric bypass remains vital for severe diabetes or reflux disease, but its complexity caps usage at roughly 22%. OAGB/MGB and duodenal switch fulfill niche roles, while adjustable gastric banding persists mainly in regions that value reversibility despite 20% re-operation risk.

Endoscopic sleeve gastroplasty represents the fastest-growing technique at a 7.6% CAGR, empowered by NICE IPG783 and 13.6% weight-loss evidence from the MERIT trial[3]National Institute for Health and Care Excellence, “IPG783: Endoscopic Sleeve Gastroplasty,” nice.org.uk. ESG shifts procedures to endoscopy rooms, lowering capital barriers and broadening provider participation, a dynamic that enlarges the bariatric surgery devices market footprint across hospitals and ambulatory centers.

By Device Type: Stapling Systems Anchor Revenue, Balloons Accelerate

Staplers, energy devices, trocars, and suturing tools generated 58.1% of 2024 sales, holding the largest slice of the Europe bariatric surgery devices market share. Medtronic’s Tri-Staple 2.0 and Ethicon’s Echelon reinforcement mats underscore how incremental upgrades defend margin. W.L. Gore’s SEAMGUARD buttress, supported by 85 publications, entrenches premium consumables within routine workflows.

Implantables—balloons, electrical stimulators, and bands—are projected to climb at an 8.8% CAGR through 2030, the highest growth across the bariatric surgery devices market size segments. Allurion’s swallowable balloon produced a 13.1% adolescent weight loss at 4 months and 22.1% after sequential placements, illustrating temporary devices’ versatility. France still blocks reimbursement, limiting penetration, yet self-pay demand in Germany, Spain, and parts of the UK is expanding.

By End User: Hospitals Still Lead, Ambulatory Centers Surge

Accredited hospitals and specialty clinics captured 68.4% of 2024 revenue due to multidisciplinary infrastructure and insurer preference for certified centers. Germany’s Hospital Reform Act may encourage smaller facilities to exit bariatric surgery, further concentrating volumes in high-throughput hubs that can amortize robotic platforms.

Ambulatory surgical centers, however, will rise at an 8.7% CAGR as same-day discharge models propagate. Dutch, French, and UK evidence proves safety parity with inpatient care when BMI and comorbidity criteria are tightly managed. The bariatric surgery devices industry therefore finds new revenue in smaller, procedure-focused settings across Northern and Western Europe.

By Patient Age Group: Adult Core, Adolescent Upswing

Adults aged 18-64 remain the core cohort, representing 46.5% of 2024 procedures, consistent with peak metabolic-syndrome incidence. Adolescents aged 12-17 exhibit the fastest 7.7% CAGR as updated guidelines lowered BMI thresholds, and registry upgrades in the UK and Italy now capture real-world pediatric outcomes. Temporary balloons and ESG favor adolescents because they avoid permanent anatomical change, expanding the addressable Europe bariatric surgery devices market without competing directly with adult staples and trocars.

Geography Analysis

Germany produced 36.5% of 2024 revenue for the bariatric surgery devices market, yet at only 72 procedures per million people—one-seventh France’s rate—because staggered insurer policies and limited center capacity restrict throughput. The EUR 50 billion transformation fund (2026-2035) aims to consolidate activity into high-volume hubs, where robotic and endoluminal platform adoption is already highest.

The United Kingdom should see accelerated growth after NICE removed tier-3 program prerequisites in 2025, shortening wait times, while IPG783 legitimized ESG reimbursement. Private GLP-1 use is rising, but strict NHS criteria and long-term cost-effectiveness models maintain surgery’s reimbursement priority.

France continues to lead by utilization, exceeding 55,000 annual cases and 571 procedures per million inhabitants, supported by strong multidisciplinary mandates from HAS. Nonetheless, cash-pay balloons remain limited, confining implantable-device mix.

Italy’s Emilia-Romagna three-tier network and near-universal adoption of minimally-invasive techniques illustrate regional pockets of best practice, though overall capacity lags demand. Spain represents the fastest-growing EU-5 market at a projected 7.2% CAGR to 2030, propelled by an EUR 8 billion ten-year cost-savings case for 15% nationwide weight loss that justifies new center accreditations. Outside the EU-5, Belgium’s 928 procedures per million sets the regional high watermark, and Nordic systems also post robust penetration, yet smaller absolute populations temper aggregate revenue contribution.

Competitive Landscape

Multinationals lead with broad portfolios—Medtronic, Johnson & Johnson (Ethicon), Intuitive Surgical, and Boston Scientific together capture the biggest slices of Europe’s bariatric surgery devices market, yet category-level fragmentation persists. Boston Scientific’s 2023 acquisition of Apollo Endosurgery injected the Orbera balloon and OverStitch suturing platform into its lineup, enabling cross-selling across endoscopic and surgical channels. KARL STORZ’s 2024 purchase of Asensus Surgical equips it with a lower-cost Senhance robot, reflecting a strategy to compete on capital accessibility for European hospitals.

Incremental innovation dominates: Medtronic’s Tri-Staple 2.0, Ethicon’s Echelon reinforcement device, and W.L. Gore’s SEAMGUARD each aim to shave leak rates or operative time without altering established workflows. Disruptors such as Creo Medical (SpydrBlade Flex) and Olympus (THUNDERBEAT) focus on hybrid energy or multifunctional tools that fit both OR and endoscopy suites, resonating with facilities embracing day-case bariatrics. Pharmaceutical entrants led by Roche and Lilly continue to invest billions in GLP-1 and dual GLP-1/GIP agonists, but constrained reimbursement maintains device primacy for the forecast horizon.

Europe Bariatric Surgery Devices Industry Leaders

Intuitive Surgical Inc.

Olympus Corp.

Medtronic plc

Johnson and Johnson

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: MOVIVA gastric mucosal ablation reached 80 procedures across eight countries within months of its first-in-human case, inaugurating a new endoscopic treatment class.

- November 2025: Nitinotes secured CE mark for the EndoZip automated suturing system for ESG, clearing the way for EU commercialization.

Europe Bariatric Surgery Devices Market Report Scope

Bariatric surgery devices, tailored for weight loss procedures, play a pivotal role in aiding patients grappling with obesity. These specialized tools and implants work by either reducing stomach capacity, altering digestion, or inducing a sense of fullness, all aimed at achieving significant and lasting weight loss. Common examples encompass gastric bands, gastric balloons, and a range of other devices, both implantable and removable, crafted for bariatric interventions.

The European market for bariatric surgery devices is segmented by procedure type, encompassing sleeve gastrectomy, Roux-en-Y gastric bypass, adjustable gastric banding, biliopancreatic diversion with duodenal switch, one anastomosis gastric bypass, and endoscopic sleeve gastroplasty, among others. Device-wise, the market differentiates between assisting tools, like suturing, closure, and stapling devices, trocars, and more, and implantable options, which feature gastric bands, electrical stimulation devices, gastric balloons, gastric emptying devices, and others. End users span hospitals & specialty clinics, dedicated bariatric surgery centers, ambulatory surgical centers, and beyond. Age-wise, the market segments into adolescents (12–17), adults (18–64), and the geriatric group (≥65). Each segment's market size is quantified in USD value terms.

| Sleeve Gastrectomy |

| Roux-en-Y Gastric Bypass |

| Adjustable Gastric Banding |

| Biliopancreatic Diversion w/ Duodenal Switch |

| One Anastomosis Gastric Bypass |

| Endoscopic Sleeve Gastroplasty |

| Other Procedures |

| Assisting Devices | Suturing Devices |

| Closure Devices | |

| Stapling Devices | |

| Trocars | |

| Other Assisting Devices | |

| Implantable Devices | Gastric Bands |

| Electrical Stimulation Devices | |

| Gastric Balloons | |

| Gastric Emptying Devices | |

| Other Devices |

| Hospitals & Specialty Clinics |

| Bariatric Surgery Centers |

| Ambulatory Surgical Centers |

| Others |

| Adolescents (12-17) |

| Adults (18-64) |

| Geriatric (>64) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Procedure Type | Sleeve Gastrectomy | |

| Roux-en-Y Gastric Bypass | ||

| Adjustable Gastric Banding | ||

| Biliopancreatic Diversion w/ Duodenal Switch | ||

| One Anastomosis Gastric Bypass | ||

| Endoscopic Sleeve Gastroplasty | ||

| Other Procedures | ||

| By Device Type | Assisting Devices | Suturing Devices |

| Closure Devices | ||

| Stapling Devices | ||

| Trocars | ||

| Other Assisting Devices | ||

| Implantable Devices | Gastric Bands | |

| Electrical Stimulation Devices | ||

| Gastric Balloons | ||

| Gastric Emptying Devices | ||

| Other Devices | ||

| By End User | Hospitals & Specialty Clinics | |

| Bariatric Surgery Centers | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Patient Age Group | Adolescents (12-17) | |

| Adults (18-64) | ||

| Geriatric (>64) | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the bariatric surgery devices market in Europe in 2025?

It is valued at USD 1.32 billion and is forecast to reach USD 1.72 billion by 2030, growing at a 5.46% CAGR.

Which procedure dominates current device demand?

Sleeve gastrectomy accounts for roughly 68% of all procedures and therefore drives the majority of stapler and energy-device sales.

What limits adoption of GLP-1 weight-loss drugs in Europe?

Statutory payers in Germany exclude coverage, and the UK, France, and Spain restrict reimbursement to narrow diabetes cohorts, keeping surgery as the principal reimbursed option.

Why are ambulatory surgical centers gaining share?

Same-day discharge protocols proven in the Netherlands and France demonstrate comparable safety with up to 43% cost savings, prompting more centers to adopt laparo-endoscopic pathways.

Which country is expected to grow fastest through 2030?

Spain is projected to achieve a 7.2% CAGR as regional health authorities expand accredited bariatric capacity following an EUR 8 billion cost-savings study.

What role do robotic platforms play in bariatric surgery?

Robots facilitate complex anastomotic work, and systems like Intuitive Surgicals da Vinci SP now support over 80,000 annual bariatric procedures worldwide, with European hospitals increasingly investing as capital budgets allow.

Page last updated on: