Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

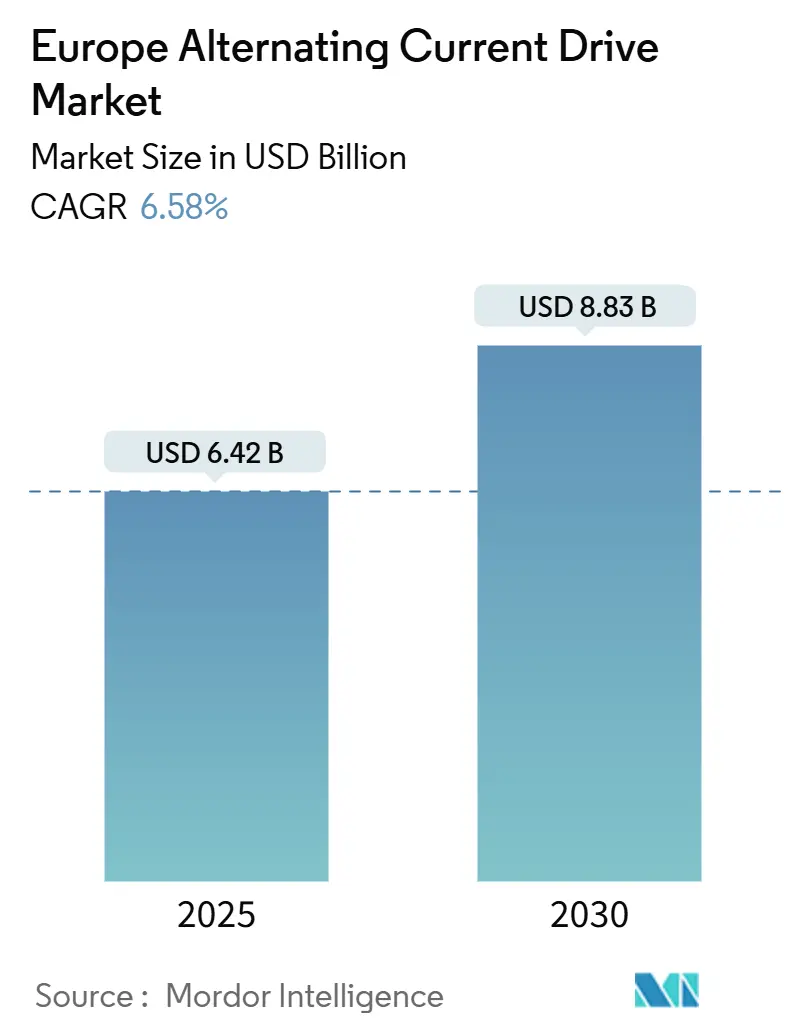

| Market Size (2025) | USD 6.42 Billion |

| Market Size (2030) | USD 8.83 Billion |

| Growth Rate (2025 - 2030) | 6.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Alternating Current Drive Market Analysis by Mordor Intelligence

The Europe alternating current drive market size is USD 6.42 billion in 2025 and is projected to reach USD 8.83 billion by 2030, reflecting a 6.58% CAGR. The Europe alternating current drive market is benefiting from the European Union’s Clean Industrial Deal, accelerating upgrades from fixed-speed to variable-frequency motors that cut electricity use by 30%–60% in pump and fan duty cycles. Battery gigafactory construction, led by Northvolt and the Stellantis-CATL venture, is creating fresh demand for precision servo and regenerative drives that handle tight torque and speed tolerances. Medium-voltage drives are also gaining widespread acceptance in offshore wind, district heating, and large water infrastructure where kilovolt-class inverters lower cable losses. As industrial automation spreads, embedded analytics and functional-safety features are becoming standard, letting operators verify carbon savings for EU compliance programs.

Key Report Takeaways

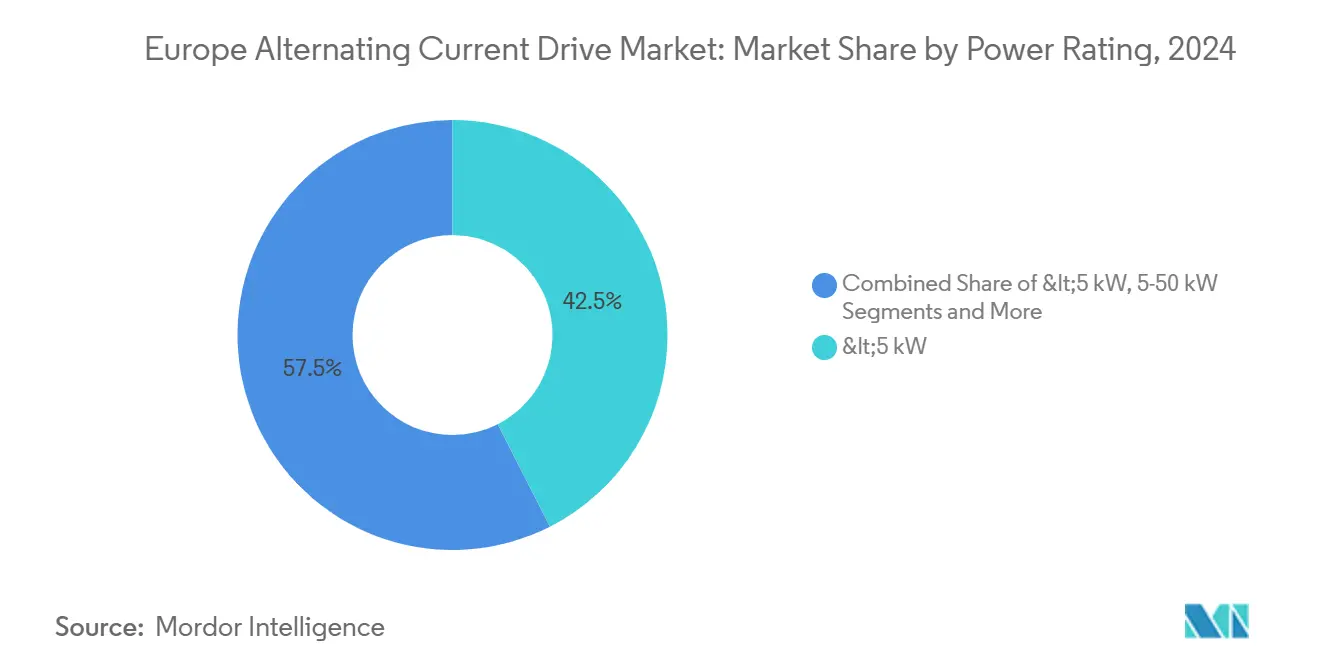

- By power rating, compact drives below 5 kW held 42.51% of the Europe alternating current drive market size in 2024. High-power systems above 200 kW are projected to advance at a 6.91% CAGR to 2030.

- By end-use industry, manufacturing commanded 31.23% of 2024 demand, while water and wastewater treatment is the fastest-growing end-use at a 6.86% CAGR through 2030.

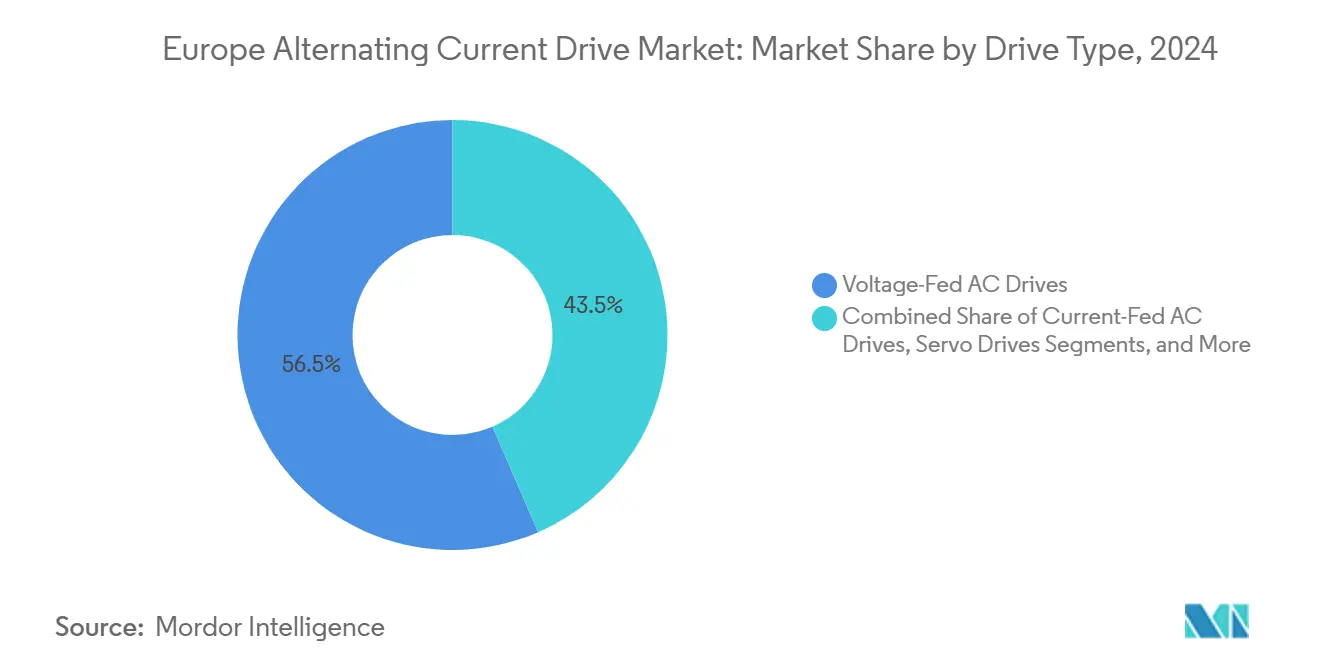

- By drive type, Voltage-fed ac drive delivered 56.53% of 2024, regenerative drives is the fastest-growing drive type at a 6.58% CAGR through 2030.

- By voltage range, low voltage held 78.72% of the 2024 market, while Medium Voltage is the fastest-growing voltage range segment, with an 8.21% CAGR through 2030.

- By country, Germany captured 27.43% of the Europe alternating current drive market share in 2024. Spain is forecast to post the fastest growth, expanding at a 6.47% CAGR through 2030.

Europe Alternating Current Drive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decarbonization targets accelerating industrial energy efficiency upgrades | +1.5% | Germany, France, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Expansion of battery gigafactories requiring precision motor control | +1.2% | Germany, Spain, France, Hungary | Medium term (2–4 years) |

| Growing adoption of electric heat pumps in buildings | +0.9% | Germany, France, Italy, Poland | Medium term (2–4 years) |

| Surge in offshore wind supply chain localization | +0.8% | Spain, Netherlands, United Kingdom, Denmark | Medium term (2–4 years) |

| EU Carbon Border Adjustment Mechanism influencing process industries | +0.7% | Germany, France, Italy, Belgium | Short term (≤ 2 years) |

| Resilient reshoring of manufacturing to Europe | +0.6% | Germany, France, Poland, Czech Republic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decarbonization Targets Accelerating Industrial Energy Efficiency Upgrades

Industrial electrification is rising from 21.3% in 2024 toward a 32% target by 2030, prompting manufacturers to replace fixed-speed motors with variable-frequency drives that match load in real time, thereby delivering documented carbon savings.[1]European Commission, “A Clean Industrial Deal for the Competitiveness and Decarbonisation of European Industry,” commission.europa.eu The Clean Industrial Deal directs more than EUR 100 billion (USD 106 billion) into efficiency retrofits, with drives accounting for roughly one-third of qualifying spend. Germany’s BMWK earmarked EUR 3.5 billion (USD 3.7 billion) in incentives that cover up to 30% of drive project costs, accelerating payback periods to under three years for cement and steel plants. Embedded power analytics let operators meet ISO 14064 reporting rules and substantiate cuts in scope-2 emissions to auditors. As a result, regenerative braking is spreading in conveyors and mixers, where energy recovery reaches 20%–25% of daily consumption

Expansion of Battery Gigafactories Requiring Precision Motor Control

Electrode coating lines demand speed stability within ±0.1% and torque ripple below 2%, specifications only achieved with high-performance servo drives. Northvolt’s Heide site alone will deploy more than 800 such units to manage roll-to-roll laminators and automated material handling. Stellantis-CATL’s Zaragoza plant specifies medium-voltage drives for clean-room HVAC that must keep temperature within ±0.5 °C and humidity within ±2% RH around the clock. Across Europe, three Automotive Cell Company sites will integrate IEC 61800-compliant drives with SIL 2–SIL 3 safety, ensuring shutdown on fault detection to minimize fire risk in lithium-ion production. These projects contribute over EUR 16 billion (USD 18.61 billion) combined capital outlay and underline why the Europe alternating current drive market expects ongoing servo demand through 2030

EU Carbon Border Adjustment Mechanism Influencing Process Industries

The Carbon Border Adjustment Mechanism began tariff collection on steel, aluminum, and cement in 2024, obligating importers to report embedded emissions and spurring retrofits that add embedded metering to each drive. ArcelorMittal’s Dunkirk steelworks invested EUR 1.7 billion (USD 1.8 billion) to fit medium-voltage drives on blast furnace blowers, cutting electricity use by 18% while generating the real-time data needed for CBAM filings. As CBAM widens to chemicals in 2026, petrochemical operators are shifting to drives with Modbus TCP and OPC UA interfaces to align energy data with ERP systems for billing and carbon allocation. This compliance push is supporting a replacement cycle for legacy drives that lack harmonic mitigation or embedded analytics. Vendors offering built-in energy meters and easy CBAM reporting trackers are winning bids in process industries across Germany, France, and Belgium

Surge in Offshore Wind Supply Chain Localization

Spain’s 23.9 GW floating wind pipeline, including a 2 GW Canary Islands tender, demands medium-voltage drives for dynamic positioning on floating platforms subjected to complex wave loads. The Netherlands targets 21 GW of offshore wind by 2030, fueling investments at IJmuiden and Rotterdam ports where heavy-lift cranes use regenerative drives to manage turbine sections weighing up to 1,200 t. Siemens Gamesa expanded its Hull blade plant by 40% in 2024, installing servo drives with sub-millisecond response for automated fiber placement lines. Fifteen-megawatt turbines now specify 6.6 kV or 11 kV inverters to meet low-voltage ride-through codes, widening the technical opportunity for medium-voltage products in the Europe alternating current drive market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain disruptions in semiconductor components | −0.8% | Germany, France, Italy, Poland | Short term (≤ 2 years) |

| Volatile raw material prices for power electronics | −0.6% | Germany, France, United Kingdom, Spain | Medium term (2–4 years) |

| Skill shortage in drive system commissioning | −0.3% | Poland, Czech Republic, Romania, Spain | Long term (≥ 4 years) |

| Grid harmonics compliance costs in retrofit projects | −0.3% | Italy, France, United Kingdom, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skill Shortage in Drive System Commissioning

Lead times for medium-voltage projects increased by four to six weeks in 2024 due to a shortage of IEC 61800-5-1-certified technicians in Poland and the Czech Republic, according to national engineering chambers. Many plants deferred upgrades after bids quoted EUR 15,000–EUR 20,000 (USD 17450 - USD 23270) premiums for scarce field engineers who can program active-front-end filters and conduct IEC 61000 harmonic tests. Training centers in Romania added only 120 new graduates in power-electronics commissioning last year, one-third of forecast demand, exacerbating project bottlenecks. Vendors such as Danfoss now bundle remote-commissioning tools and augmented-reality manuals, yet utilities still require on-site sign-off for grid-tie equipment. The persistent talent gap trims 0.3 percentage points off forecast growth until regional upskilling efforts mature post-2027

Grid Harmonics Compliance Costs in Retrofit Projects

Italy and the United Kingdom tightened harmonic-distortion limits in the 2024 network codes, forcing retrofit jobs to add LCL filters or active front-ends that raise the bill of materials by USD 15,000–USD 25,000 per drive. Older motors paired with new inverters sometimes fail to meet IEEE 519 compliance without derating, which can extend shutdown windows in chemical plants where downtime costs reach USD 1 million per day. Medium-voltage drives must now pass conducted-emission tests up to the 50th harmonic, adding two weeks to factory-acceptance schedules. French paper mills report 8% budget overruns when last-minute site tests reveal excessive total harmonic distortion, compelling engineers to retrofit dV/dt filters. These unplanned costs temper the retrofit cycle and shave 0.3 percentage points from the Europe alternating current drive market CAGR

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Compact Drives Dominate, yet High-Power Systems Capture Infrastructure Spend

Compact models below 5 kW controlled 42.51% of the Europe alternating current drive market share in 2024, driven by rooftop HVAC units, conveyors, and building pumps where space and budget are tight. The 5 kW–50 kW band benefits from modular plug-in designs that keep unplanned stoppages under 30 minutes in food packaging lines. Units from 50 kW–200 kW are expanding in chiller and district-heating loops that shift from fixed-speed to variable-speed duty as gas boilers are phased out. Above 200 kW, high-power drives are rising at a 6.91% CAGR, with water utilities retrofitting pumping stations to meet the Urban Wastewater Treatment Directive upgrade budget of EUR 255 billion (USD 271 billion) through 2030.

Battery gigafactories push an emerging ultra-high-power niche: drives rated 800 kW–1.2 MW for ISO Class 5 clean-room air handlers at Northvolt’s Heide site. Offshore wind nacelles require 2 MW–3 MW pitch-control drives that replace hydraulics and reduce maintenance on 15 MW turbines. Every uptick in power class pushes sales of silicon-carbide switching stacks that cut cooling load by 30%, underscoring the premium segment’s future in the Europe alternating current drive market.

By End-Use Industry: Manufacturing Leads, yet Water Infrastructure Posts Fastest Growth

Manufacturing accounted for 31.23% of total demand in 2024 as automotive, machinery, and robotics plants embraced Ethernet-enabled drives for predictive maintenance. Water and wastewater treatment grows the fastest at 6.86% CAGR, reflecting directive-driven upgrades to nutrient removal and microplastics filtration by 2030, projects that favor sensorless vector drives able to throttle pumps below 20% speed without stalling.

Oil and gas operators deploy drives on compressors to comply with methane-reduction targets, cutting venting by 25% while saving energy. Power utilities use medium-voltage drives on boiler feed pumps in coal-to-biomass retrofits, where variable speed improves ramp rates for peaking duty. HVAC installations soar as revised Energy Performance of Buildings rules require near-zero-energy new builds, compelling rooftop equipment to switch to variable flow. Mining and marine clients, grouped under “Others,” specify explosion-proof enclosures and anti-corrosion coatings, broadening customization revenue in the Europe alternating current drive industry.

By Drive Type: Voltage-Fed Systems Prevail, Regenerative Architectures Gain Traction

Voltage-fed topologies delivered 56.53% of 2024 shipments, offering cost-effective control for standard induction motors in conveyors and fans. Regenerative architectures, though smaller, will rise 6.58% CAGR because ports, elevators, and cranes seek energy recovery that can slice demand charges by 30%-40%. Servo drives gain ground in battery module assembly where ±0.05 mm repeatability is mandatory. Meanwhile, silicon-carbide voltage-fed drives such as ABB’s ACS880 series hit 98% efficiency and run at up to 85 °C ambient without derating, attracting underground mining and marine users.[2]ABB Ltd., “ABB Secures TenneT Contract for Offshore Wind Grid Integration,” abb.com

Current-fed drives remain a niche above 5 MW for rolling mills and kiln duties where inherent current limitation offers grid-fault tolerance. Compliance with the updated Machinery Directive requiring SIL 2 safety is accelerating adoption of servo models with safe torque-off built in, eliminating the cost of external relays.

By Voltage Range: Low-Voltage Dominates, Medium-Voltage Surges with Utility Investments

Low-voltage products below 690 V served 78.72% of 2024 installations across the massive installed base of sub-500 kW motors. Medium-voltage drives, however, will grow at 8.21% CAGR to 2030 as offshore wind, district heating, and long-distance water transfer plants seek kilovolt-class inverters to trim cable size and transformer costs.

Germany’s TenneT plans over 100,000 km of new transmission lines by 2033, with substations specifying medium-voltage active-front-end drives for reactive power support. Low-voltage units retain dominance in building automation thanks to IP54/IP65 plug-and-play enclosures, while medium-voltage systems face an extra 12–16-week switchgear engineering lead time. The updated IEC 61800-4 electromagnetic compatibility rules add USD 15,000–USD 25,000 per unit for filtering, yet users accept the premium because harmonic compliance avoids penalties on industrial metering tariffs.

Geography Analysis

Germany’s entrenched machine-building sector keeps the Europe alternating current drive market anchored, with OEMs like Trumpf connecting drives via OPC UA to enable 25% downtime cuts through predictive maintenance. Energy subsidies covering up to 30% of capital outlay shorten payback horizons, sustaining replacements. Northvolt’s Heide plant alone pushes 800 new drive points into the German installed base.

Spain climbs fastest as its 23.9 GW floating wind backlog demands medium-voltage inverters for platform station-keeping, while desalination projects in Murcia and Almería specify energy-saving drives on 60 bar high-pressure pumps. The United Kingdom’s Contract-for-Difference awards inject 11 GW of offshore wind capacity, pulling through drive demand for dockside cranes at Teesside and Humber.

France invests EUR 8 billion (USD 9.30 billion) under the France 2030 plan, allocating 15%–20% to drives in industrial electrification projects. Italy channels EU recovery funds to water upgrades, ordering variable-speed pumping equipment compliant with the Urban Wastewater Treatment Directive. Poland, the Czech Republic, and Romania attract automotive reshoring, each plant specifying torque-controlled drives for battery module lines, while EU Just Transition grants finance coal-to-gas conversions that install variable-speed boiler feed pumps.

Competitive Landscape

The Europe alternating current drive market shows moderate concentration. ABB deepens vertical integration by embedding predictive-maintenance software that trims downtime. Siemens invests EUR 150 million to expand medium-voltage drive output at Bad Neustadt, adding high-voltage stator winding lines and a 15 kV grid disturbance test laboratory.[3]Siemens AG, “Siemens Expands Bad Neustadt Drive Manufacturing Facility,” siemens.com Schneider’s Altivar Process 900 series introduces silicon-carbide switching, pushing 98.5% efficiency while shrinking heatsinks by 30%.

Niche challengers thrive where compact footprint and rapid commissioning matter. Invertek Drives gains traction in retrofit pump and fan projects by shipping IP66 units pre-loaded with hydraulic curve macros, cutting setup time to under one hour. Lenze and Vacon target marine customers with seawater-resistant coatings that double service intervals, while Danfoss leverages a newly acquired Polish integrator to fill the regional skills gap in IEC 61800-5-1 safety commissioning. ABB filed a modular power-stack patent in 2024 that standardizes die-attach processes across voltage classes to slash manufacturing costs.

Cybersecurity is another differentiator. Mitsubishi Electric’s FR-F800 adds IEC 62443 encrypted Modbus TCP communication, pre-empting remote-access vulnerabilities in networked drives for water operators. Yaskawa opened a Slovenian servo plant to halve European lead times, signaling that localization also drives competitive advantage.

Europe Alternating Current Drive Industry Leaders

ABB Ltd.

Siemens AG

Schneider Electric SE

Danfoss A/S

Yaskawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens earmarked EUR 150 million to enlarge its Bad Neustadt plant, adding automated winding lines and a 15 kV test lab for medium-voltage drives.

- February 2025: ABB secured a USD 85 million TenneT contract to supply medium-voltage drives and reactive-power systems for 12 offshore wind substations.

- January 2025: Schneider Electric launched the Altivar Process 900 silicon-carbide series, boosting efficiency to 98.5% and cutting cooling needs 30%.

- December 2024: Danfoss acquired a 60% stake in a Polish drive integrator for EUR 45 million, expanding service coverage in Central Europe.

Europe Alternating Current Drive Market Report Scope

The Europe Alternating Current (AC) Drive Market encompasses the sales and adoption of AC drive technologies used to control the speed and torque of electric motors across various industrial and commercial applications. This market encompasses a diverse range of power ratings, drive types, and voltage categories, catering to the needs of various sectors, including manufacturing, oil and gas, power generation, HVAC, water and wastewater, and others.

The Europe Alternating Current Drive Market Report is Segmented by Power Rating (below 5 kilowatts, 5 to 50 kilowatts, 50 to 200 kilowatts, above 200 kilowatts), End-Use Industry (Manufacturing, Oil and Gas, Power Generation, HVAC and Building Automation, Water and Wastewater, Others), Drive Type (Voltage-Fed AC Drives, Current-Fed AC Drives, Servo Drives, Regenerative Drives), Voltage Range (Low Voltage below 690 volts, Medium Voltage 690 volts and above), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value in USD.

By Power Rating

| <5 kW |

| 5-50 kW |

| 50-200 kW |

| >200 kW |

By End-Use Industry

| Manufacturing |

| Oil and Gas |

| Power Generation |

| HVAC and Building Automation |

| Water and Wastewater |

| Others |

By Drive Type

| Voltage-Fed AC Drives |

| Current-Fed AC Drives |

| Servo Drives |

| Regenerative Drives |

By Voltage Range

| Low Voltage (<690 V) |

| Medium Voltage (≥690 V) |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Power Rating | <5 kW |

| 5-50 kW | |

| 50-200 kW | |

| >200 kW | |

| By End-Use Industry | Manufacturing |

| Oil and Gas | |

| Power Generation | |

| HVAC and Building Automation | |

| Water and Wastewater | |

| Others | |

| By Drive Type | Voltage-Fed AC Drives |

| Current-Fed AC Drives | |

| Servo Drives | |

| Regenerative Drives | |

| By Voltage Range | Low Voltage (<690 V) |

| Medium Voltage (≥690 V) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe alternating current drive market in 2030?

It is forecast to reach USD 8.83 billion by 2030.

Which country holds the largest share of European demand?

Germany leads with 27.43% market share in 2024.

Which end-use segment is growing the fastest?

Water and wastewater treatment, expanding at a 6.86% CAGR through 2030.

Why are medium-voltage drives gaining traction?

They support large-scale offshore wind, district heating, and water projects where kilovolt-class inverters cut cable losses and ease grid integration.

How are silicon-carbide inverters influencing adoption?

They raise efficiency by up to 3 percentage points and allow operation at higher ambient temperatures without derating, which appeals to marine and mining users.

What impact does the Carbon Border Adjustment Mechanism have on drive upgrades?

CBAM forces process industries to document real-time energy use, pushing adoption of drives with embedded metering and communication capabilities.

Page last updated on: