Europe AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

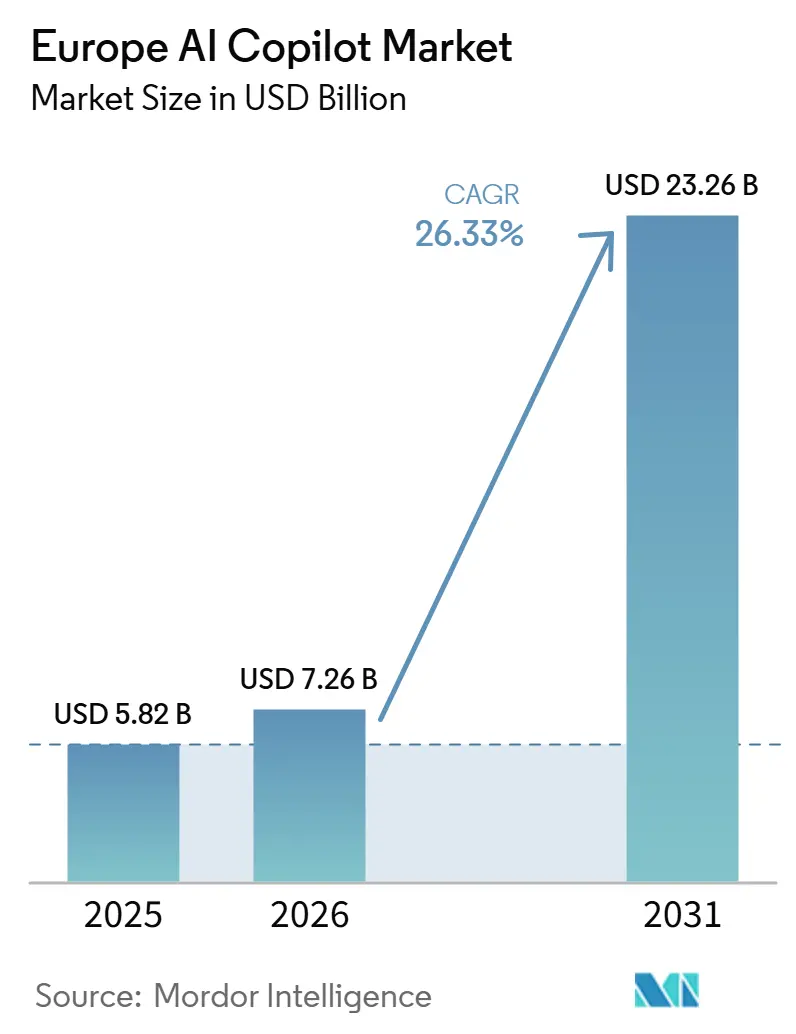

| Base Year Market Size (2025) | USD 5.82 Billion |

| Market Size (2026) | USD 7.26 Billion |

| Market Size (2031) | USD 23.26 Billion |

| Growth Rate (2026 - 2031) | 26.33% CAGR |

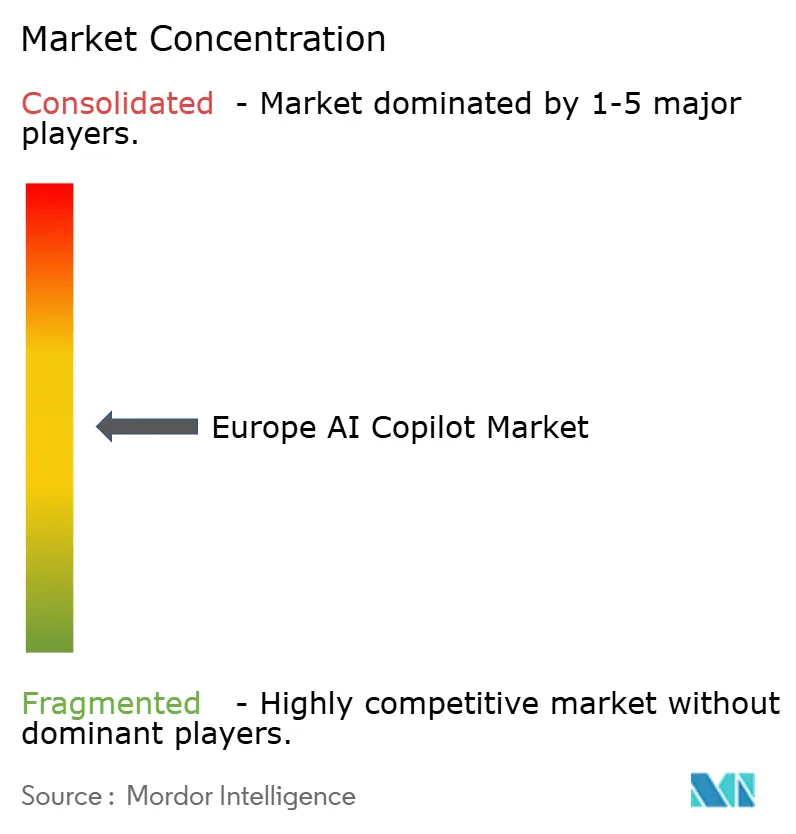

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe AI Copilot Market Analysis by Mordor Intelligence

The Europe AI copilot market size was valued at USD 5.82 billion in 2025, USD 7.26 billion in 2026 and is projected to reach USD 23.36 billion by 2031, growing at a CAGR of 26.33% during 2026-2031. The Europe AI copilot market is moving from pilot programs into broader operating use, as enterprises now treat copilots as a practical layer for daily work rather than as a stand-alone technology trial. Demand is supported by broader AI adoption among European enterprises, stronger management focus on measurable productivity gains, and a clearer link between AI adoption and near-term revenue expectations. Infrastructure choices are also shifting, with cloud still leading while hybrid models gain traction as organizations balance speed, governance, and local data handling requirements. The Europe AI copilot market is also benefiting from stronger public-sector adoption, especially as large administrations begin to roll out copilots at scale within the workforce rather than limiting use to small tests. Competition remains uneven, with global platform vendors controlling broad enterprise access while European-origin providers build positions in sovereign, regulated, and workflow-specific environments where transparency and hosting location matter more.

Key Report Takeaways

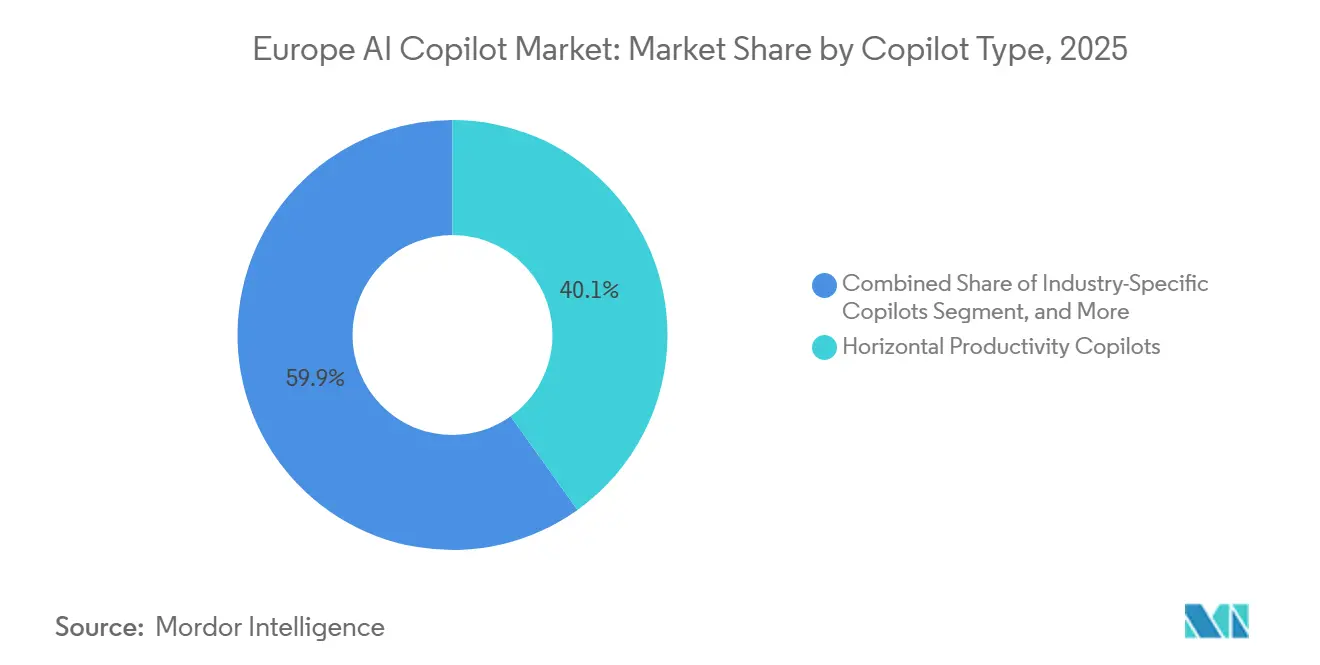

- By copilot type, Horizontal Productivity Copilots held 40.12% of the Europe AI copilot market share in 2025, while Industry-Specific Copilots are projected to expand at a 28.84% CAGR through 2031.

- By deployment, cloud-based deployment accounted for 71.24% of the Europe AI copilot market in 2026, while hybrid deployment is expected to grow at a 29.16% CAGR through 2031.

- By organization size, large enterprises held 68.43% of the market in 2025, while SMEs are projected to grow at a 28.41% CAGR through 2031.

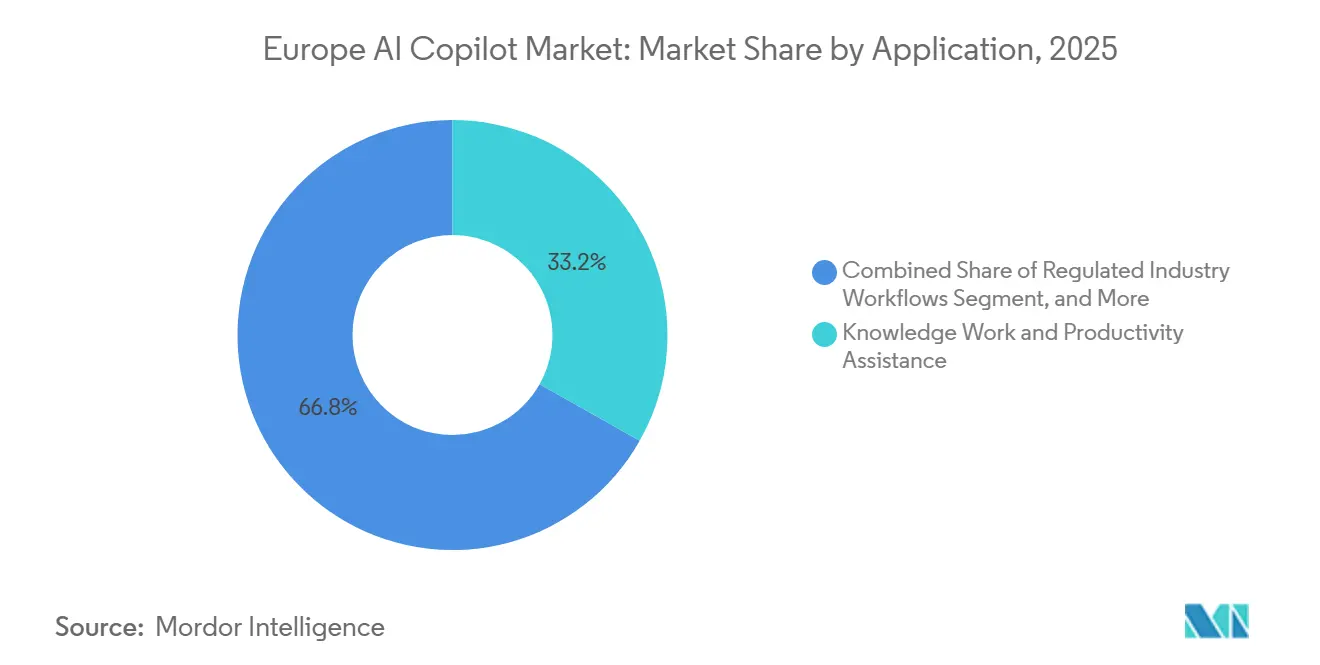

- By application, Knowledge Work and Productivity Assistance accounted for 33.18% of the Europe AI copilot market in 2025, while Regulated Industry Workflows are expected to expand at a 29.73% CAGR through 2031.

- By end-user industry, IT and Telecommunication held 22.47% of the Europe AI copilot market in 2025, while Government and Administration is projected to grow at a 28.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Enterprise Demand for Role-Specific Productivity Automation | +4.8% | Global, with concentration in UK, Germany, and Benelux | Short term (≤ 2 years) |

| Rising Adoption of Generative AI Across Knowledge Workflows | +3.9% | Global, with strong early adoption in Nordics and UK | Short term (≤ 2 years) |

| Expansion of Microsoft, Google, and Salesforce Ecosystems in Europe | +3.2% | Global, with EU Data Boundary applicability across EU and EFTA | Short term (≤ 2 years) |

| Regulatory Pressure on Data Governance and Traceability Driving Trusted Copilot Deployments | +2.6% | EU and UK, particularly BFSI and healthcare verticals | Medium term (2-4 years) |

| Use of Domain-Tuned Copilots in High-Value Regulated Functions | +2.1% | EU regulated industries, finance, healthcare, and public sector | Medium term (2-4 years) |

| Shift Toward Multilingual Copilot Interfaces for European Workforces | +1.8% | All European markets, with highest relevance in non-English-speaking EU economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Enterprise Demand for Role-Specific Productivity Automation

The Europe AI copilot market is gaining from a clear shift in enterprise buying priorities toward tools that remove repetitive work in defined roles. Microsoft stated in April 2026 that Accenture had deployed Microsoft 365 Copilot to 743,000 employees globally, making it the largest publicly announced enterprise AI deployment at that time. NHS England confirmed in June 2026 that 505,000 clinical and support staff would receive access to Microsoft 365 Copilot by October 2026, following a pilot across 90 organizations.[1]NHS England, “500,000 NHS Staff to Get New Artificial Intelligence Tools to Help Free Up More Time for Patients,” NHS England, england.nhs.uk The same pilot showed average savings of 43 minutes per administrative task day, providing large employers with a concrete benchmark for evaluating workforce-wide rollout cases. Academic evidence also supports this direction, with a 2025 study in The Quarterly Journal of Economics finding that AI assistance raised worker productivity by 15% on average in the measured setting. As more large organizations validate time savings and output gains in defined tasks, the Europe AI copilot market is seeing demand move from optional testing into planned operating budgets.

Rising Adoption of Generative AI Across Knowledge Workflows

The Europe AI copilot market is also being lifted by a broader normalization of AI in day-to-day enterprise activity. Eurostat reported that 19.95% of EU enterprises with 10 or more employees used AI technologies in 2025, up by 6.47 percentage points from 2024.[2]European Central Bank, “Adopting and Investing in AI, Evidence from Euro Area Firms in the SAFE,” ECB Economic Bulletin, ecb.europa.eu Large enterprises were the strongest contributors, with AI use reaching 55.03% among organizations with 250 or more employees. The European Central Bank stated that 38% of euro area firms were already at an advanced stage of AI adoption in Q4 2025. The same ECB study found that firms reporting significant AI use expected 21% higher turnover over the following 3 months than non-users, which helps explain why copilots are being discussed at the management level as a near-term business tool rather than solely as a technical upgrade. This wider base of enterprise AI familiarity is giving the Europe AI copilot market a larger pool of buyers that are already comfortable with AI-enabled workflows and are now moving toward more structured deployment.

Expansion of Microsoft, Google, and Salesforce Ecosystems in Europe

The Europe AI copilot market remains closely tied to the spread of large enterprise software ecosystems. Microsoft announced in November 2025 that it was offering in-country data processing for Microsoft 365 Copilot across 15 countries, with further expansion to Germany, Italy, Spain, and Poland scheduled for 2026.[3]Microsoft, “Unlocking Human Ambition to Drive Business Growth With AI,” Microsoft Blog, blogs.microsoft.com That step matters because it reduces one of the practical barriers that had slowed adoption in regulated settings across Europe. SAP also documented that the Joule and Microsoft 365 Copilot integration creates a shared working layer between ERP data and productivity tools already used across many European enterprises. This makes the Europe AI copilot market more accessible to customers who prefer to extend existing platforms rather than buy a separate tool stack. The result is stronger momentum for vendors that can attach copilot functions to software environments where users, permissions, and core business data are already in place.

Regulatory Pressure on Data Governance and Traceability Driving Trusted Copilot Deployments

The Europe AI copilot market is also being shaped by greater buyer focus on auditability, hosting, and traceability. Microsoft’s in-country data processing expansion shows that vendors are adjusting product delivery around European control requirements rather than treating them as a secondary feature. Aleph Alpha and STACKIT announced in May 2025 that they would deliver PhariaAI through fully EU-hosted infrastructure, directly targeting regulated enterprises and public-sector organizations in the DACH region. La Banque Postale also signed a strategic partnership with Mistral AI in 2025 to deploy sovereign generative AI on the bank’s own servers and in its data center. These moves show that trusted deployment is becoming part of product design, not just part of procurement review. As a result, the Europe AI copilot market is creating clearer space for vendors that can combine useful copilots with local hosting, governance controls, and documented handling of sensitive enterprise data.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Concerns Over Data Leakage and Prompt Exposure | -2.8% | Global, intensified within EU and EFTA due to GDPR and AI Act compliance | Short term (≤ 2 years) |

| Integration Complexity With Legacy Enterprise Applications | -2.1% | Germany, France, and Italy, where on-premises ERP and CRM penetration is high | Medium term (2-4 years) |

| AI Governance Gaps Across Mid-Market Buyers | -1.5% | Central and Eastern Europe, and Southern Europe SME segment | Medium term (2-4 years) |

| Budget Scrutiny on Recurring AI Software Subscriptions | -1.2% | Global, pronounced in enterprises with stagnant IT budgets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Enterprise Concerns Over Data Leakage and Prompt Exposure

The Europe AI copilot market still faces hesitation, where users and compliance teams are unsure how prompts, outputs, and enterprise content are handled. Eurostat reported that 48.83% of EU enterprises that considered adopting AI but did not do so cited data protection and privacy concerns as a main barrier in 2025. This is especially important in public services, healthcare, and other settings where internal content often includes personal or regulated information. NHS England’s staged rollout also shows that large public organizations are moving carefully, beginning with pilots before scaling access to hundreds of thousands of users. Microsoft’s move toward in-country processing further indicates that data handling concerns are important enough to influence product architecture in the region. Until buyers are fully confident that data exposure risks are under control, the Europe AI copilot market will continue to see longer review cycles and narrower early-deployment scopes in sensitive environments.

Integration Complexity with Legacy Enterprise Applications

Integration remains a practical limit on how quickly the Europe AI copilot market can scale beyond basic productivity use cases. The European Central Bank found that system incompatibilities were cited by 20% of non-adopting firms as a key barrier in Q4 2025, and the issue appeared across company sizes. That matters because many European organizations still rely on older ERP, CRM, and workflow environments that were not built for modern AI interfaces. SAP’s documented Joule and Microsoft 365 Copilot integration addresses one important path between ERP data and office productivity layers, but it also highlights how valuable such direct connectors have become. Siemens’ launch of Engineering Copilot TIA inside TIA Portal follows the same pattern in industrial automation, where copilots gain traction more easily when they are integrated into familiar, already approved systems. As long as value depends on deeper process integration, the Europe AI copilot market will grow fastest where vendors can reduce connection work and fit within software estates that buyers already trust.[4]Siemens AG, “Engineering Copilot TIA,” Siemens AG, assets.new.siemens.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Horizontal Suites Lead While Vertical Depth Accelerates

Horizontal Productivity Copilots held 40.12% of the Europe AI copilot market in 2025, which reflects the early advantage of broad enterprise suites already used across daily office work. The Europe AI copilot market initially expanded through these tools because bundled access reduced deployment friction for companies already using Microsoft 365 or Google Workspace. General drafting, summarization, search, and task support were easier to launch than highly specialized use cases that needed workflow redesign. This made horizontal products the most practical entry point for enterprises that wanted visible gains without deep technical integration. It also gave platform vendors a head start in distribution because procurement teams could expand existing software relationships rather than open entirely new vendor tracks.

The growth pattern is now shifting, as Industry-Specific Copilots are projected to advance at a 28.84% CAGR through 2031. Airbus stated in May 2026 that it partnered with Mistral AI to use the company’s product suite for aerospace engineering tasks such as flight safety support, technical documentation automation, and design acceleration. That example shows why specialized copilots are gaining attention in the Europe AI copilot industry, especially where accuracy, domain language, and controlled deployment matter more than broad generic assistance. Functional Workflow Copilots remain important in HR, finance, and supply chain processes because they sit closer to repeatable business work than pure productivity tools do. Technical and Engineering Copilots are also gaining depth, and Siemens showed this in November 2025 when it launched Engineering Copilot TIA as a managed service inside TIA Portal versions 19 and 20.

By Deployment: Cloud Dominates While Hybrid Gains Ground In Sensitive Environments

Cloud-based deployment accounted for 71.24% of the market in 2026, showing that most buyers still prefer faster setup, easier updates, and simpler operating models. This large share also reflects the influence of major software ecosystems that deliver copilots through cloud-first environments already familiar to enterprise users. The Europe AI copilot market has therefore grown fastest in organizations that can adopt standard commercial offerings without major hosting restrictions. Cloud remains attractive where companies want predictable subscription structures and do not want to build separate internal infrastructure for AI services. It also fits well with broad office productivity use cases where data sensitivity is lower than in tightly regulated operating functions.

At the same time, hybrid deployment is projected to grow at a 29.16% CAGR through 2031, which shows where demand is heading as use cases become more sensitive. Microsoft’s in-country processing expansion across Europe indicates that even large cloud vendors are adapting to stronger expectations around local control. Aleph Alpha and STACKIT also positioned PhariaAI as a sovereign AI-as-a-service offering, delivered via fully EU-hosted infrastructure for regulated enterprises and public-sector bodies. On-premises deployment remains a narrower path within the Europe AI copilot market, but it matters in defense, critical infrastructure, and central administration where external processing can be hard to approve. This is why the Europe AI copilot market is likely to maintain its cloud leadership, while hybrid becomes the preferred design for workloads that balance convenience with strict data-handling rules.

By Organization Size: Large Enterprises Hold The Base While SMEs Increase Their Presence

Large enterprises held 68.43% of the market in 2025, reflecting stronger internal resources for governance, change management, procurement, and integration. The Europe AI copilot market first scaled in this group because large employers could justify pilot programs, legal review, security testing, and staff training across multiple functions. They also had a clearer business case because even small efficiency gains could produce large aggregate savings across thousands of workers. Large organizations have therefore set many of the practical benchmarks now used in regional buying discussions. Their early decisions also influence peer behavior, especially when deployments become visible in finance, healthcare, and industrial operations.

The SME segment is projected to grow at a 28.41% CAGR through 2031, indicating a broadening of the Europe AI copilot market beyond its early enterprise base. The OECD reported in December 2025 that generative AI was already in use at 31% of SMEs, with performance improvement named as the main adoption motive. The same report noted that smaller firms also saw generative AI as a way to compensate for skill gaps, which is important where dedicated AI teams are absent. This suggests that the Europe AI copilot market size for SMEs is rising because vendors are adjusting pricing, packaging, and onboarding to meet the needs of firms that require quick setup and clear day-to-day value. As the Europe AI copilot industry matures, SME demand is likely to rise further, with copilots delivered via simple templates rather than lengthy integration projects.

By Application: Productivity Leads Today While Regulated Workflows Grow Faster

Knowledge Work and Productivity Assistance accounted for 33.18% of the application market in 2025, making it the largest application area in the Europe AI copilot market size by share. This lead reflects the breadth of use cases, including document drafting, meeting summarization, internal search, and personal task support. These functions are widely relevant across sectors and can often be introduced without changing the underlying business process. That makes them a natural first step for enterprises that want quick evidence of usefulness. It also explains why large software suite vendors have been able to build early scale through general-purpose work tools.

Regulated Industry Workflows are projected to expand at a 29.73% CAGR through 2031, showing where the next growth layer is forming. NHS England said its pilot across 90 organizations saved staff an average of 43 minutes per administrative task per day, providing healthcare organizations with a concrete example of value in controlled operational settings. Customer and Employee Service Operations are also moving forward, with service quality, response speed, and documentation to be improved through guided assistance. Software Engineering and Technical Operations continue to expand because output can be measured more directly than in many other enterprise functions. The Europe AI copilot market share is therefore still led by broad productivity tasks, while faster growth is shifting toward applications where copilots are embedded in more controlled, more consequential workflows.

By End-User Industry: IT And Telecommunication Lead While Government Changes The Growth Mix

IT and Telecommunication held 22.47% of the Europe AI copilot market in 2025, supported by a high concentration of developers, digital teams, and enterprise software users. This sector was well placed to adopt copilots early because it already had internal familiarity with automation, code tools, and cloud-based collaboration systems. The Europe AI copilot market has therefore seen strong initial demand from companies that could test copilots quickly and measure outcomes through developer activity, support operations, and internal knowledge access. IT buyers also tend to have clearer internal ownership of AI projects than in many other sectors. That made the sector a logical starting point for large-scale commercial adoption across the region.

Government and Administration is projected to grow at a 28.92% CAGR through 2031, which signals a major shift in the end-user mix of the Europe AI copilot market. NHS England’s full rollout and Spain’s policy actions show that public institutions are now moving from controlled tests into broader implementation planning. BFSI remains one of the largest areas of practical adoption because compliance, forecasting, documentation, and customer-facing work all create opportunities for guided AI support. Healthcare and life sciences are also advancing as large systems seek administrative savings and more structured access to knowledge. The Europe AI copilot market is therefore becoming less dependent on digital-native private sectors and more balanced across public administration, regulated services, and industrial users.

Geography Analysis

The United Kingdom held 23.64% of the Europe AI copilot market in 2025, giving it the largest geographic share in the region. The Europe AI copilot market is strongest in the United Kingdom because financial services demand, English-language use, and public-sector action reinforce one another. NHS England confirmed in July 2026 that 505,000 staff had access to Microsoft 365 Copilot, with the rollout backed by GBP 10 billion (USD 12.8 billion) in NHS technology investment over 3 years. The UK government also announced a Financial Services AI Adoption Plan in July 2026, showing direct policy support for wider AI use in a sector that already has strong software spending capacity. Ireland strengthens this cluster, and Microsoft stated in July 2025 that AIB had deployed Microsoft 365 Copilot to the vast majority of its more than 10,000 employees.

Germany remains a major center in the Europe AI copilot market because its enterprise base combines strong manufacturing, large software estates, and deep SAP usage. Eurostat’s 2025 enterprise data supports the wider regional pattern that larger companies are pulling adoption forward, which is highly relevant in Germany’s corporate landscape. SAP’s integration work with Microsoft 365 Copilot matters more in Germany than in many other markets because ERP-linked workflows are central to business operations there. France is showing a different profile, with stronger emphasis on governance, sovereign positioning, and large institutional deployments. Atos stated in June 2026 that it had rolled out Microsoft 365 Copilot E7 to all 56,000 employees across 54 countries, providing France with a visible large-scale enterprise reference point. La Banque Postale’s 2025 partnership with Mistral AI also shows how French adoption is linking Copilot use with local infrastructure and controlled deployment models.

Spain is projected to grow at a 29.38% CAGR through 2031, making it the fastest-growing geography in the Europe AI copilot market size by growth rate. Spain’s momentum is being supported by active public policy, and the government said in May 2026 that it was establishing a national framework for AI oversight through the Artificial Intelligence Oversight Agency. The Rest of Europe remains highly uneven, and Eurostat reported that Denmark reached 42.03% enterprise AI adoption in 2025, while Romania and Bulgaria remained below 9%. Russia remains present in the regional framing, but its enterprise AI copilot activity is separated from the EU software and procurement environment described in this Europe AI copilot market analysis.

Competitive Landscape

The Europe AI copilot market is moderately concentrated at the platform level and much more fragmented at the workflow and vertical level. Microsoft has the broadest installed base through Microsoft 365 Copilot and GitHub Copilot, while Alphabet and Salesforce compete through adjacent productivity, CRM, and cloud environments already used by enterprise customers. The Europe AI copilot market, therefore, favors vendors that can leverage an existing software position rather than build distribution from scratch. SAP plays a distinct role because Joule connects directly with ERP-centric workflows already embedded in many European enterprises. Its integration with Microsoft 365 Copilot strengthens that position by linking business system data with common productivity tools in a way that smaller vendors cannot easily match at scale.

The next layer of competition in the Europe AI copilot market comes from vendors that focus on sovereignty, regulated deployment, or specialized workflow depth. Aleph Alpha and STACKIT targeted this opening by launching a fully EU-hosted managed offering for regulated enterprises and public organizations. Mistral AI is building on the same logic, and Airbus confirmed in May 2026 that it would use Mistral’s suite in aerospace engineering settings. La Banque Postale’s partnership with Mistral AI adds a second example from banking, where local control and deployment architecture can matter as much as raw model capability. These moves show that competition in the Europe AI copilot market is not only about model quality, but also about where systems run, how they integrate, and whether they fit institutional procurement rules.

Strategic moves since 2025 also show that vendors are competing through large deployments that create visible proof points. Microsoft highlighted Accenture’s 743,000-user rollout in April 2026 and Atos’s 56,000-user deployment in June 2026, which reinforces its leadership in enterprise-wide adoption. Siemens took a different route by embedding Engineering Copilot TIA into an established industrial toolchain, making competitive entry harder in that specific environment. The Europe AI copilot market still has room for growth in mid-market and sector-specific deployments, where many buyers want more depth than platform defaults provide but less complexity than sovereign custom builds often require.

Europe AI Copilot Industry Leaders

Microsoft Corporation

Alphabet Inc.

Salesforce, Inc.

SAP SE

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: NHS England accelerated its full AI rollout, confirming that 505,000 NHS staff are receiving access to Microsoft 365 Copilot following a 30,000-employee pilot that showed an average admin time reduction of 2 days per month per worker. The rollout is backed by GBP 10 billion (USD 12.8 billion) in NHS technology investment over three years, with full deployment targeted by October 2026 and GBP 41 billion (USD 52.48 billion) in projected total benefits over the following decade.

- June 2026: Atos Group and Microsoft announced the rollout of Microsoft 365 Copilot E7 to all 56,000 Atos employees across 54 countries, making Atos the first French global systems integrator to deploy the platform at company-wide scale. The deployment incorporates Microsoft Copilot Studio and Microsoft Foundry for custom agent design and client service delivery.

- May 2026: Airbus signed a strategic partnership agreement with Mistral AI to deploy the full Mistral AI product suite, including on-premises and trusted cloud configurations, for aerospace engineering applications covering flight safety, technical documentation automation, and engineering design acceleration.

- April 2026: Accenture confirmed a Microsoft 365 Copilot deployment to approximately 743,000 employees across more than 120 countries, the largest enterprise AI deployment ever announced, with its European delivery workforce operating within this rollout as a primary beneficiary.

Europe AI Copilot Market Report Scope

The Europe AI copilot market refers to the ecosystem of artificial intelligence-driven intelligent assistants integrated into enterprise software applications to enhance human capabilities and automate complex tasks. These copilots leverage advanced foundation models, including large language models (LLMs) and generative AI, to provide real-time contextual suggestions, generate content, analyze data, and execute workflows. The market encompasses various copilot types, ranging from general horizontal productivity tools and technical engineering assistants to specialized, functional, and industry-specific solutions. Deployed across cloud, hybrid, and on-premises environments, these AI systems serve organizations of all sizes across Europe. They are used across diverse applications, including knowledge work assistance, software development, customer and employee service operations, and sales enablement, in industries such as IT, BFSI, healthcare, and manufacturing. By seamlessly integrating into existing workflows, AI copilots help European organizations drive operational efficiency, reduce manual cognitive load, improve decision-making, and accelerate digital transformation while navigating regional data privacy and regulatory frameworks such as the GDPR and the EU AI Act.

The Europe AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries), and Geography (Germany, United Kingdom, France, Russia, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other end-user industries |

| Germany |

| United Kingdom |

| France |

| Russia |

| Spain |

| Rest of Europe |

| By Copilot Type | Horizontal Productivity Copilots |

| Functional Workflow Copilots | |

| Technical and Engineering Copilots | |

| Industry-Specific Copilots | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations | |

| Customer and Employee Service Operations | |

| Sales, Marketing and Revenue Enablement | |

| Business Process and Enterprise Operations | |

| Regulated Industry Workflows | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Healthcare and Life Sciences | |

| Retail and E-Commerce | |

| Industrial Manufacturing | |

| Education and Research Institutions | |

| Media and Entertainment | |

| Government and administration | |

| Energy and Utilities | |

| Other end-user industries | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe AI copilot market size and growth outlook?

The Europe AI copilot market size was USD 5.82 billion in 2025 and is projected to reach USD 23.36 billion by 2031 at a 26.33% CAGR during 2026-2031.

Which copilot type leads adoption across Europe?

Horizontal Productivity Copilots led with 40.12% share in 2025 because they were easier to launch through existing enterprise software environments.

Which deployment model is expanding the fastest?

Hybrid deployment is expected to grow at a 29.16% CAGR through 2031 as buyers balance ease of use with stronger data handling and governance requirements.

Why are large enterprises ahead in adoption?

Large enterprises held 68.43% of the market in 2025 because they had more capacity for procurement, security review, integration work, and workforce-wide rollout.

Which application area is growing the quickest?

Regulated Industry Workflows are projected to grow at a 29.73% CAGR through 2031 as copilots move into compliance-sensitive and accuracy-critical tasks.

Which country is growing the fastest in Europe?

Spain is the fastest-growing country, with a projected 29.38% CAGR through 2031, supported by active policy steps and stronger public backing for AI deployment.

Page last updated on: