ERP Platform Consolidation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.83 Billion |

| Market Size (2031) | USD 20.84 Billion |

| Growth Rate (2026 - 2031) | 18.75% CAGR |

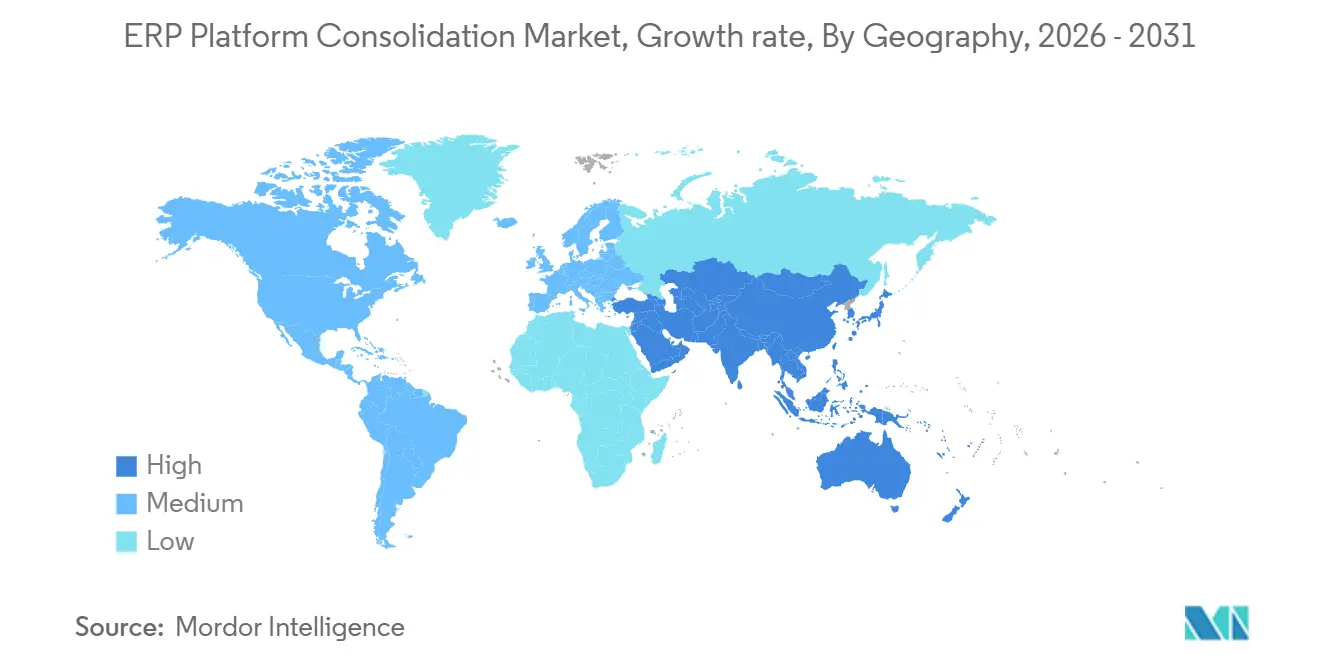

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

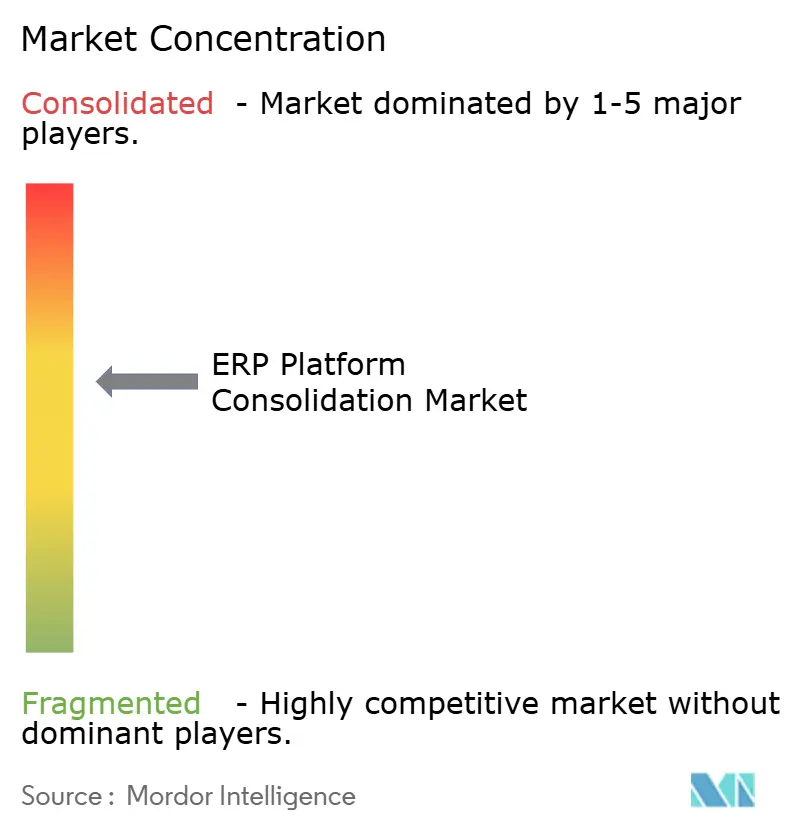

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ERP Platform Consolidation Market Analysis by Mordor Intelligence

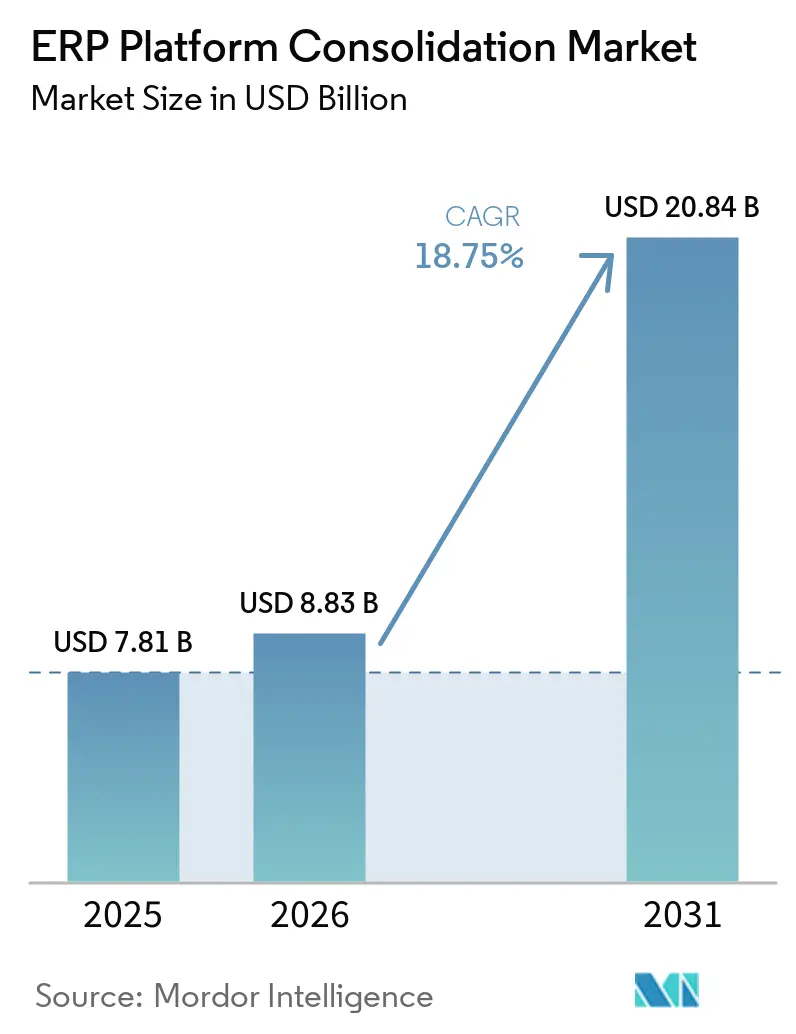

The ERP platform consolidation market size is projected to be USD 7.81 billion in 2025, USD 8.83 billion in 2026, and reach USD 20.84 billion by 2031, growing at a CAGR of 18.75% from 2026 to 2031. Near-term expansion is propelled by cloud-first mandates that compress migration timelines, hyperscaler partnerships that bundle infrastructure with software subscriptions, and board directives that tie ESG reporting to unified data models. Vendor investments in sovereign-cloud regions reduce geopolitical risk and open regulated sectors, while AI agents embedded in finance, procurement, and supply-chain modules cut transaction workloads for overstretched IT teams. Heightened scrutiny of the total cost of ownership is pushing enterprises to sunset redundant instances, retire aging hardware, and favor subscription models that turn capex into opex. Competitive differentiation now centers on the depth of automation, quality of sustainability analytics, and the ability to deliver single-contract offerings that include compliance certifications, managed services, and evergreen updates.

Key Report Takeaways

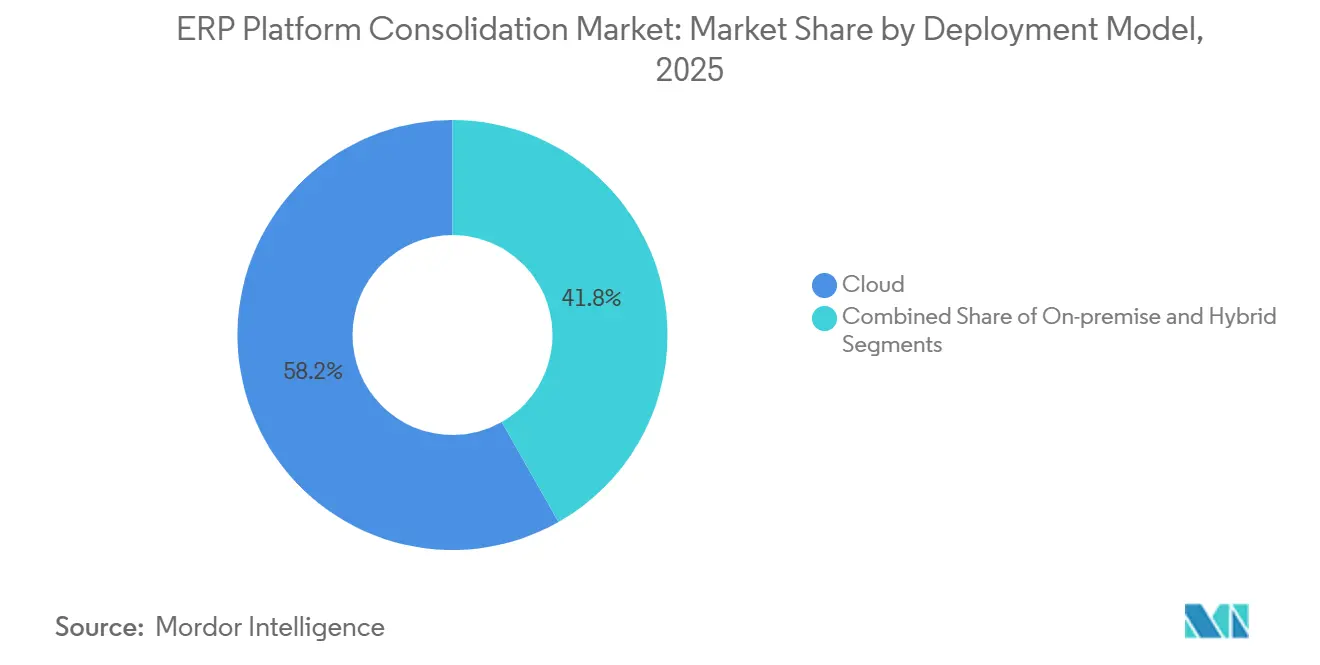

- By deployment model, cloud accounted for 58.20% of the ERP platform consolidation market share in 2025 and is forecast to expand at a 14.30% CAGR through 2031.

- By organization size, large enterprises held 46.50% of the ERP platform consolidation market share in 2025, while mid-market companies are advancing at an 11.80% CAGR to 2031.

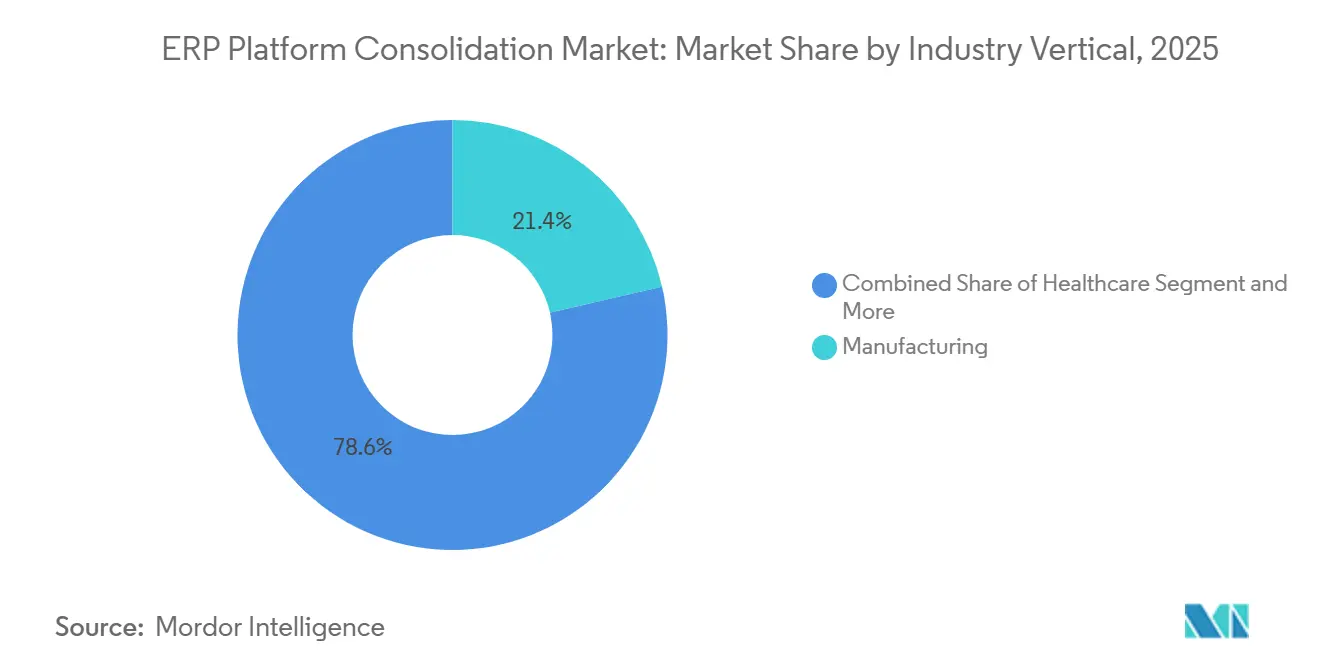

- By industry vertical, manufacturing led with 21.40% of 2025 revenue, whereas healthcare is projected to record a 13.70% CAGR through 2031.

- By service type, implementation and migration services accounted for 37.80% of 2025 revenue, while managed services are growing at a 15.60% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ERP Platform Consolidation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud-First Policies | +4.2% | Global, North America and Europe | Short term (≤ 2 years) |

| Unified Data Governance Needs | +3.8% | Global, with emphasis on EU multinationals | Medium term (2-4 years) |

| Cost Optimization Pressure | +3.5% | Global, acute in manufacturing and retail | Short term (≤ 2 years) |

| Shortage of Skilled ERP Talent | +2.9% | Global, notable in North America and Western Europe | Medium term (2-4 years) |

| Industry-Specific Composable Microservices | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Board-Level ESG Reporting Mandates | +1.8% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud-First Policies Among Large Enterprises

Large corporations are migrating finance and supply-chain workloads to hyperscaler clouds to eliminate data-center capex and unlock elastic compute for AI training. The United States SEC climate disclosure rules finalized in 2024 created an additional compliance layer that favors single-instance architectures capable of consolidating emissions data across subsidiaries. [1]United States Securities and Exchange Commission, “SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors,” SEC.gov Multicloud options such as Oracle Database on AWS and Google Cloud removed latency and egress cost barriers in 2025, allowing firms to co-locate ERP and AI workloads in their preferred clouds. [2]Oracle Corporation, “Oracle Announces Database at AWS,” Oracle.com Vendors with sovereign regions meet data-residency demands in Europe and the Middle East, tilting selection toward well-capitalized incumbents. Together, these forces drive consolidation in the ERP platform market by shortening decision cycles and concentrating budgets on cloud subscriptions.

Increasing Need for Unified Data Governance Across Subsidiaries

Divergent data-residency rules create fragmented landscapes that are a liability for multinationals. GDPR fines up to 4% of global revenue motivate companies to converge master data and access controls in a single platform. [3] European Commission, “Data Protection in the EU,” Europa.eu Column-level tagging tools introduced by Snowflake in 2024 reduce the effort required for lineage documentation, while Microsoft Purview automates retention policies across clouds. Post-merger projects often reveal duplicative vendor files and inconsistent customer IDs, prompting harmonization to avoid reconciliation delays. Case studies such as Imperial Brands demonstrate 35% support-cost savings after reducing 50 systems to one core ledger. Unified governance, therefore, delivers both compliance assurance and operational efficiency, reinforcing market growth.

Cost Optimization Pressure Amidst Margin Erosion in Key Verticals

Raw-material inflation and wage escalation force CFOs to trim software overhead. A 2025 study covering 200 migrations found a 28% reduction in five-year TCO when five or more on-premises systems were replaced with a single cloud instance. [4]Financial Times, “Enterprise ERP Migration Cost Analysis,” FT.com Bundled offerings like RISE with SAP turn large upfront licenses into predictable opex, appealing to manufacturers under pressure to improve profitability. RAK Ceramics expects a five-year payback after moving 55 entities into a single S/4HANA tenant in 2026.[5]SAP Community, “S/4HANA Migration Survey Results,” SAP.com As similar examples spread, budget holders prioritize rationalization, sustaining demand for ERP platform consolidation market projects.

Shortage of Skilled ERP Talent Driving Vendor-Led Automation

The global ABAP developer base fell 12% in 2024, pushing vendors to add low-code tools and AI code converters. Workday’s USD 1.1 billion Sana Labs deal in 2025 brought knowledge-management AI that shrinks consulting hours, while Oracle embedded 50 AI agents in Fusion ERP to automate finance workflows. Automation mitigates talent scarcity, reduces implementation risk, and broadens adoption among mid-market firms, fueling the trajectory of the ERP platform consolidation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged Custom Code Debt | −2.8% | Global, acute in Europe and North America | Medium term (2-4 years) |

| High Switching Costs | −2.3% | Global, significant in North America and Europe | Short term (≤ 2 years) |

| Limited Interoperability Standards | −1.6% | Global | Long term (≥ 4 years) |

| Geopolitical Export Controls | −1.4% | China, Russia, Middle East and other restricted regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Custom Code Debt Hindering Migration Velocity

Enterprises with extensive ABAP customizations average 24-month S/4HANA projects, compared with 12 months for standard implementations, according to a 2025 SAP Community survey. Hard-coded rules break during upgrades, forcing labor-intensive rewrites that tie up scarce consultants. Immature conversion tools mean human validation remains essential, slowing timelines and dampening near-term revenue realization for vendors.

High Switching Costs for Legacy License Holders

Maintenance fees of 17%-22% of net license value, along with exit penalties in unlimited agreements, deter clients from changing platforms, even when alternatives offer lower TCO. Data migration risk and training overhead add friction, especially in regulated sectors that require exhaustive testing. This inertia tempers the forecast CAGR despite strong top-line drivers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hyperscaler Alliances Secure Cloud Leadership

Cloud deployments accounted for 58.20% of 2025 revenue, supported by Oracle Database on AWS and Google Cloud, which removed latency and egress hurdles. The ERP platform consolidation market size for cloud implementations is projected to rise at 14.30% annually to 2031.

On-premises share declines as vendors divert R&D toward AI-rich cloud editions. Hybrid architectures remain for defense and life sciences organizations that must keep sensitive data on-site. SAP’s EU AI Cloud, launched in late 2025, meets the European AI Act's requirements, underscoring how sovereign infrastructure has become a competitive lever. Subscription contracts bundle software, compute, and managed services, locking customers in for multiyear terms and embedding the ERP platform consolidation market into long-range budgets.

By Organization Size: Automation Expands Mid-Market Uptake

Large enterprises accounted for 46.50% of the ERP platform consolidation market share in 2025, owing to their complex global footprints. However, mid-market firms are growing at 11.80% because AI-driven templates cut consulting hours. Workday’s Paradox acquisition added conversational AI to automate onboarding, easing resource constraints for mid-sized HR teams.

Simple legal structures let mid-market clients realize value sooner, but weaker purchasing power limits the ability to negotiate discounts. Modular suites such as Oracle NetSuite, whose revenue rose 13% in fiscal 2026, appeal by combining finance, e-commerce, and planning without on-premises servers. These dynamics broaden the addressable market for ERP platform consolidation beyond blue-chip corporations.

By Industry Vertical: Manufacturing Retains Primacy as Healthcare Surges

In 2025, the manufacturing sector accounted for 21.40% of total revenue, emphasizing the pivotal role of synchronized supply, production, and quality data in ensuring efficient plant operations. The integration of manufacturing execution systems with ERP solutions has enabled companies to achieve significant operational improvements, including reducing unplanned downtime by up to 25%.

The healthcare sector is anticipated to experience the most rapid growth, with a compound annual growth rate of 13.70% through 2031. This expansion is largely driven by hospitals' efforts to integrate electronic health records with financial and supply-chain modules, a move necessitated by interoperability mandates. Furthermore, the banking, retail, and government sectors are addressing their distinct compliance requirements. Leading market players are meeting these needs through pre-built, localized solutions, thereby fostering sustained, broad-based growth in the ERP platform consolidation market.

By Service Type: Managed Services Absorb Operational Risk

Implementation and migration services held 37.80% of 2025 revenue, reflecting the complexity of data conversion. Yet managed services are growing at 15.60% as enterprises offload monitoring and upgrades to vendors with AI-powered support desks. Oracle’s 50 Fusion AI agents reduce the workload for invoice matching and revenue recognition, lowering the cost per managed transaction.

Consumption-based support fees that align with usage replace flat maintenance percentages, giving customers cost predictability. Providers with global centers and automation tooling capture share, raising barriers for boutique firms and concentrating the ERP platform consolidation market size among full-service vendors.

Geography Analysis

North America accounted for 34.10% of 2025 revenue, driven by Fortune 500 density, early cloud adoption, and mature consulting ecosystems. Federal risk-management certifications in AWS GovCloud and Azure Government accelerate public-sector migrations. Investor scrutiny of ESG disclosure is driving demand for unified ledgers to track emissions under forthcoming SEC rules, reinforcing the consolidation of ERP platforms in the region.

Asia-Pacific is projected to grow at 12.90% annually through 2031 as governments subsidize digital infrastructure and enforce in-country hosting requirements. Oracle committed USD 8 billion in 2025 to build sovereign regions in Japan, aligning with the Act on the Protection of Specially Designated Secrets and unlocking defense and public-sector workloads. India’s production-linked incentive scheme for electronics manufacturing is driving factories to modernize planning and costing systems, creating new bids for consolidation projects. China’s cybersecurity law mandates local storage of personal and financial data, prompting multinationals to deploy dedicated Chinese instances while keeping global ledgers elsewhere.

Europe’s GDPR, the Network and Information Security Directive 2, and the Digital Operational Resilience Act make cross-border data flows complex, so enterprises are consolidating ERP systems within EU data centers. SAP’s EU AI Cloud directly addresses these rules, boosting vendor credibility. Sovereign-cloud momentum extends to the Middle East and Africa, where national cloud frameworks encourage in-country stacks. South America sees steady upgrades from spreadsheets to integrated ledgers as currency volatility drives treasury teams to demand real-time cash visibility, albeit from a smaller base.

Competitive Landscape

The top five players collectively hold a significant share of revenue, giving the ERP platform consolidation market a moderate level of concentration. Incumbents leverage installed bases to cross-sell adjacent HCM, CX, and planning modules, deepening footprint while raising switching costs. Oracle’s remaining performance obligation hit USD 523 billion in Q2 fiscal 2026, underpinned by long-term cloud deals with AI pioneers that embed ERP along with compute and database layers.

Disruptors such as Odoo and Acumatica target mid-market buyers with modular suites priced up to 60% below tier-1 offerings, trading functional breadth for speed and affordability. Competitive differentiation now hinges on embedded AI agents that automate routine finance work, sovereign cloud options that meet local regulations, and open APIs that support composable architectures. SAP’s Business AI release introduced two foundation models and 50 AI agents, signaling a pivot toward low-code extension over heavy customization. Vendors that demonstrate interoperability through certified connectors and standards body participation may erode incumbent lock-in and redraw share lines.

Despite fierce rivalry, M&A continues as vendors plug functional gaps. SAP’s planned acquisition of SmartRecruiters strengthens recruiting, while Workday’s Sana Labs and Paradox buys embed conversational AI and knowledge graphs.

ERP Platform Consolidation Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor, Inc.

The Sage Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oracle introduced 22 Fusion Agentic Applications that embed AI agents across procurement, finance, supply-chain, and HR workflows.

- February 2026: RAK Ceramics selected SAP RISE to consolidate 55 entities in 15 countries onto S/4HANA Cloud.

- December 2025: Oracle Database at Google Cloud reached general availability, extending Oracle’s multicloud roadmap.

- November 2025: Workday closed its USD 1.1 billion purchase of Sana Labs, adding AI-driven knowledge management.

Global ERP Platform Consolidation Market Report Scope

The ERP Platform Consolidation market refers to the ecosystem of software solutions and professional services that enable organizations to rationalize, unify, and streamline multiple Enterprise Resource Planning (ERP) systems into a simplified, standardized, and centrally governed ERP landscape.

The ERP Platform Consolidation Market Report is Segmented Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large, and SME), Industry Vertical (Manufacturing, Retail, and Other Industry Verticals), Service Type (Implementation, Consulting, and Other Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| Healthcare |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Sector |

| Other Industry Verticals |

| Implementation and Migration |

| Consulting and Strategy |

| Integration Services |

| Support and Maintenance |

| Managed Services |

| Other Services |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Industry Vertical | Manufacturing | |

| Retail and E-commerce | ||

| Healthcare | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Public Sector | ||

| Other Industry Verticals | ||

| By Service Type | Implementation and Migration | |

| Consulting and Strategy | ||

| Integration Services | ||

| Support and Maintenance | ||

| Managed Services | ||

| Other Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the ERP Platform Consolidation market by 2031?

The market is forecast to reach USD 20.84 billion by 2031.

Which sector contributes the largest revenue today?

Manufacturing retained 21.40% of 2025 revenue, maintaining its lead thanks to complex supply-chain and quality requirements.

Why are mid-market firms accelerating adoption?

AI-driven templates and bundled cloud subscriptions reduce consulting hours and upfront costs, letting mid-market companies grow at an 11.80% CAGR through 2031.

What is the main obstacle to faster migrations?

Prolonged custom code debt adds 6-12 months to schedules for organizations with extensive ABAP modifications.

How concentrated is vendor competition?

The five largest suppliers hold roughly 60% of revenue, giving the market a moderate concentration score of 6.

How do ESG rules influence ERP consolidation?

New disclosure mandates require unified ledgers that aggregate emissions across entities, prompting boards to fund consolidation initiatives that streamline reporting.

Page last updated on: